Economic and Financial Management: Imperial Brand plc Analysis Report

VerifiedAdded on 2023/01/13

|19

|2906

|22

Report

AI Summary

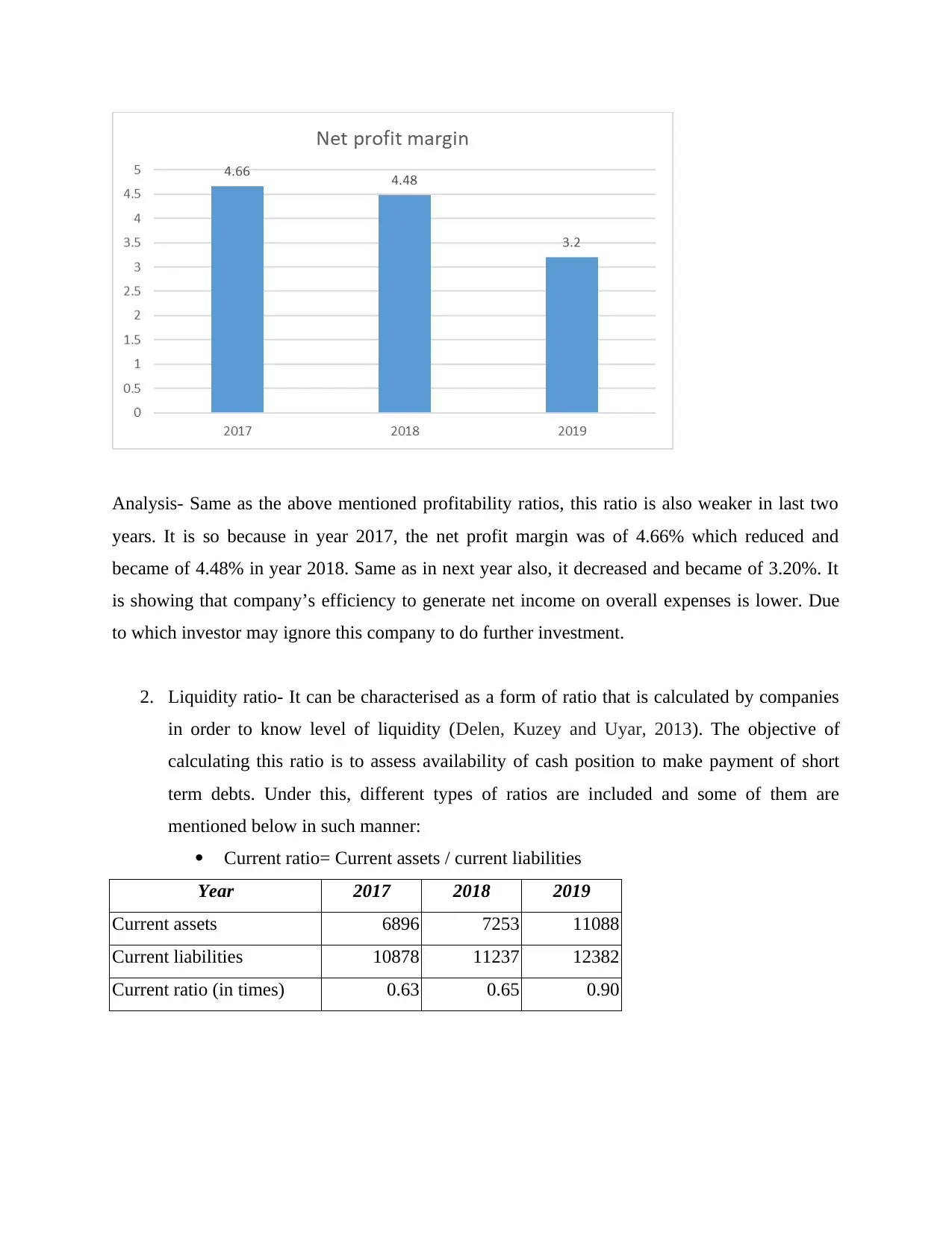

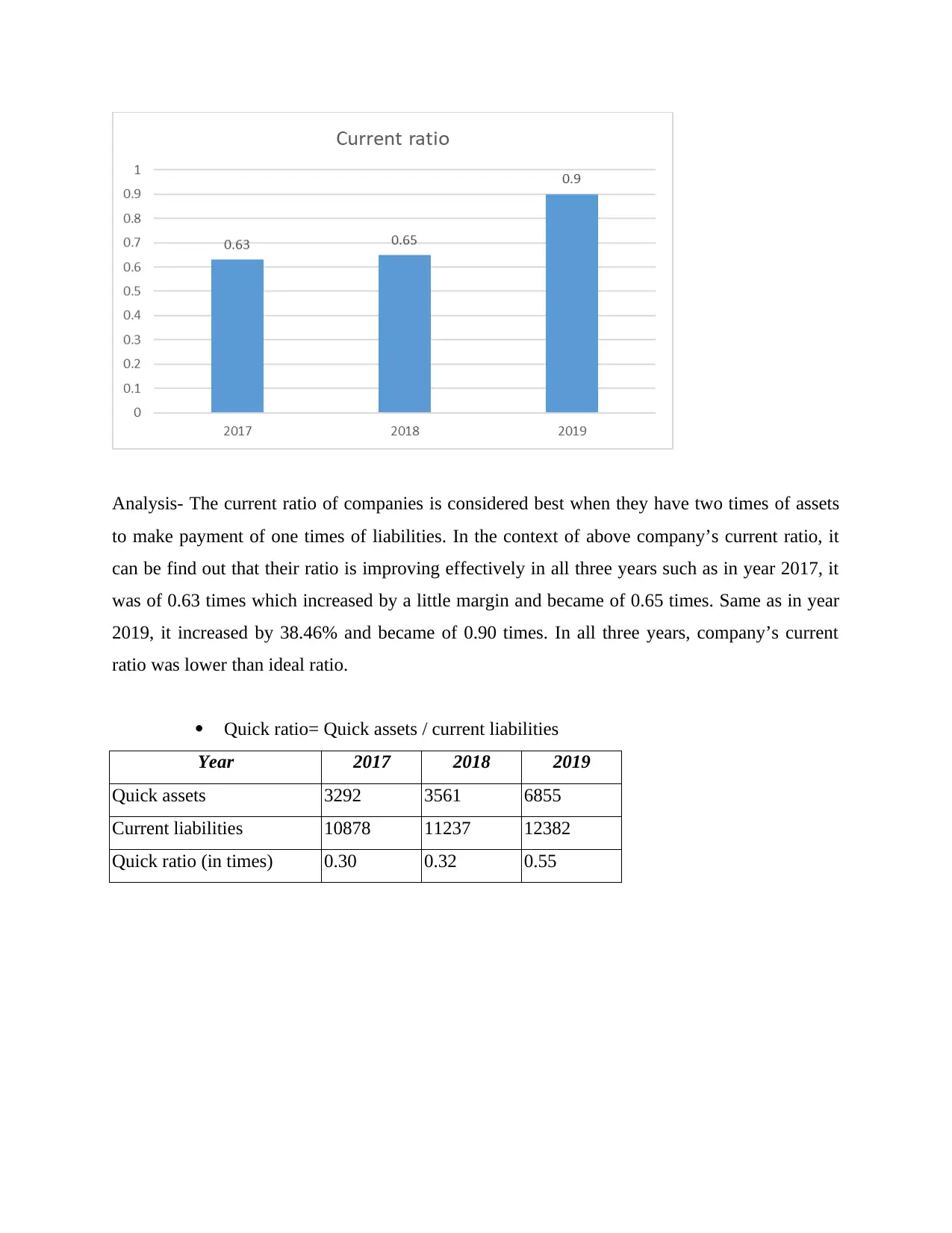

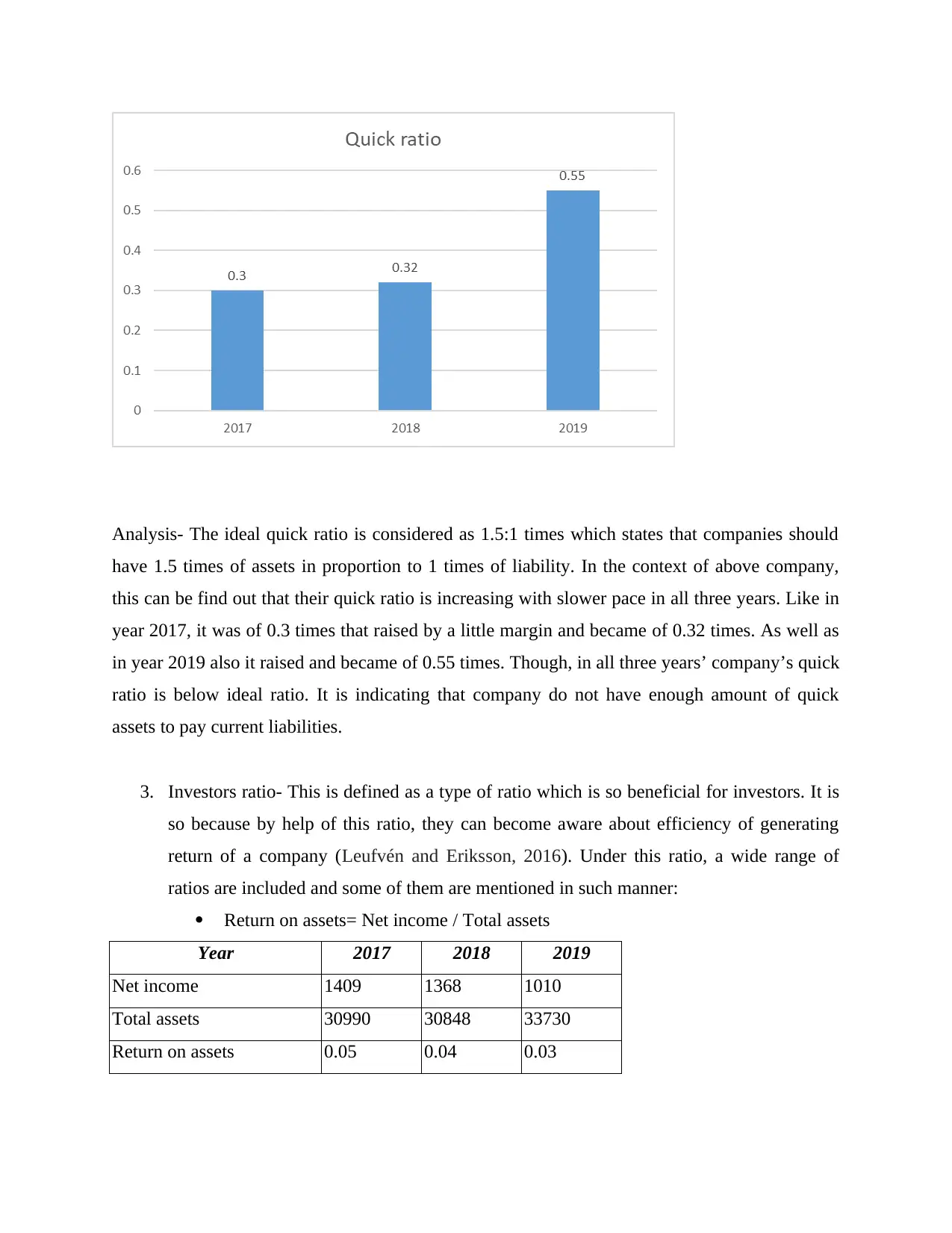

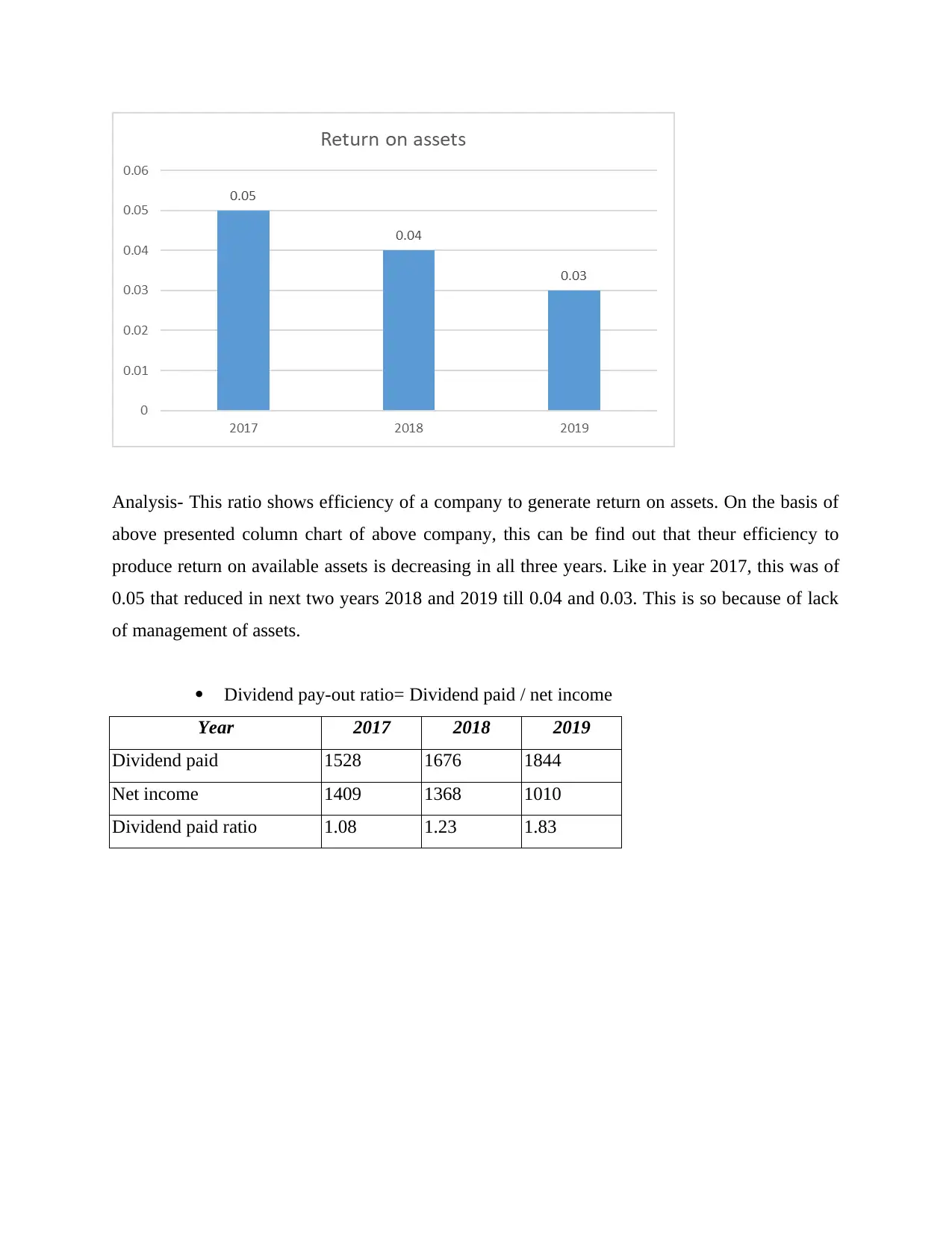

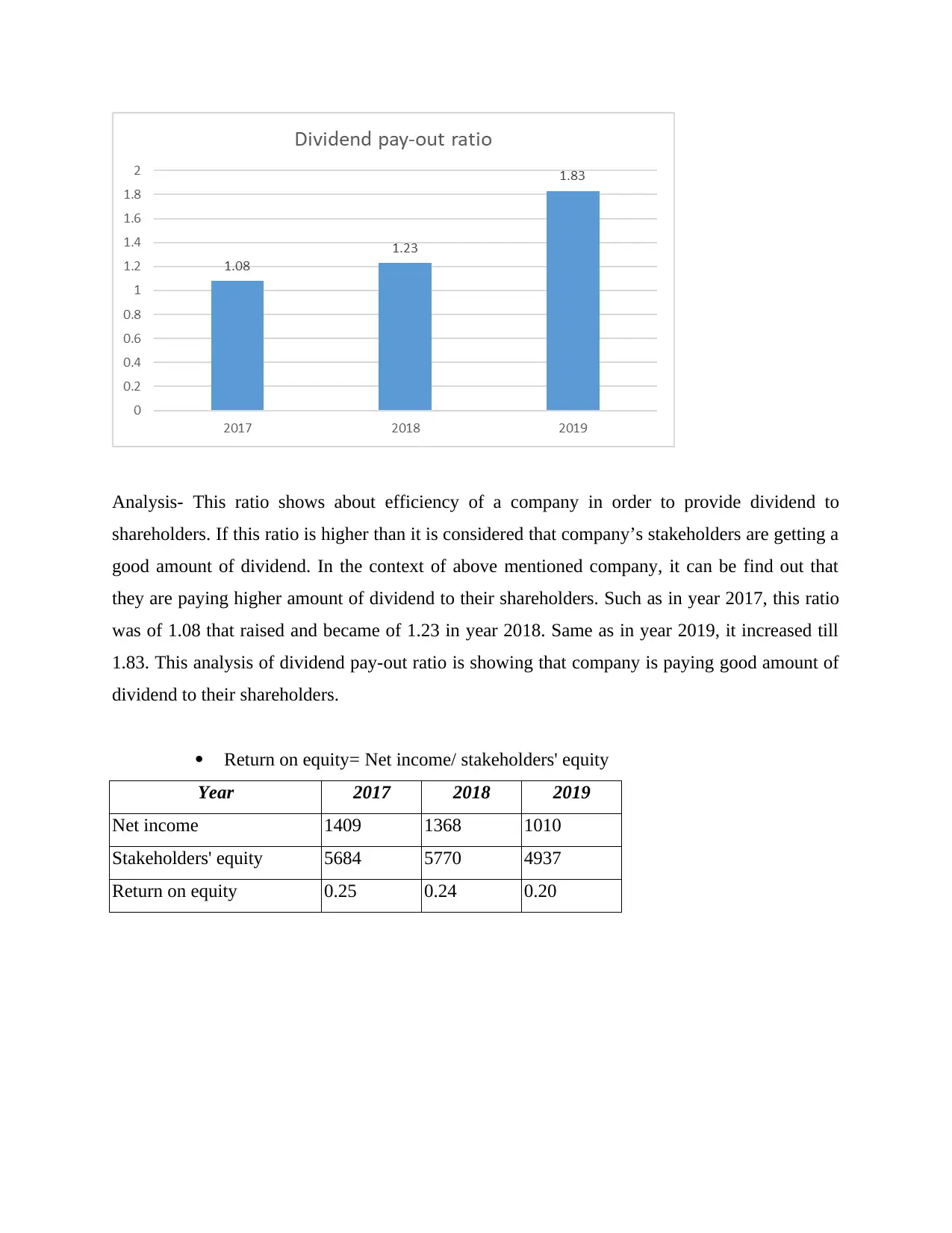

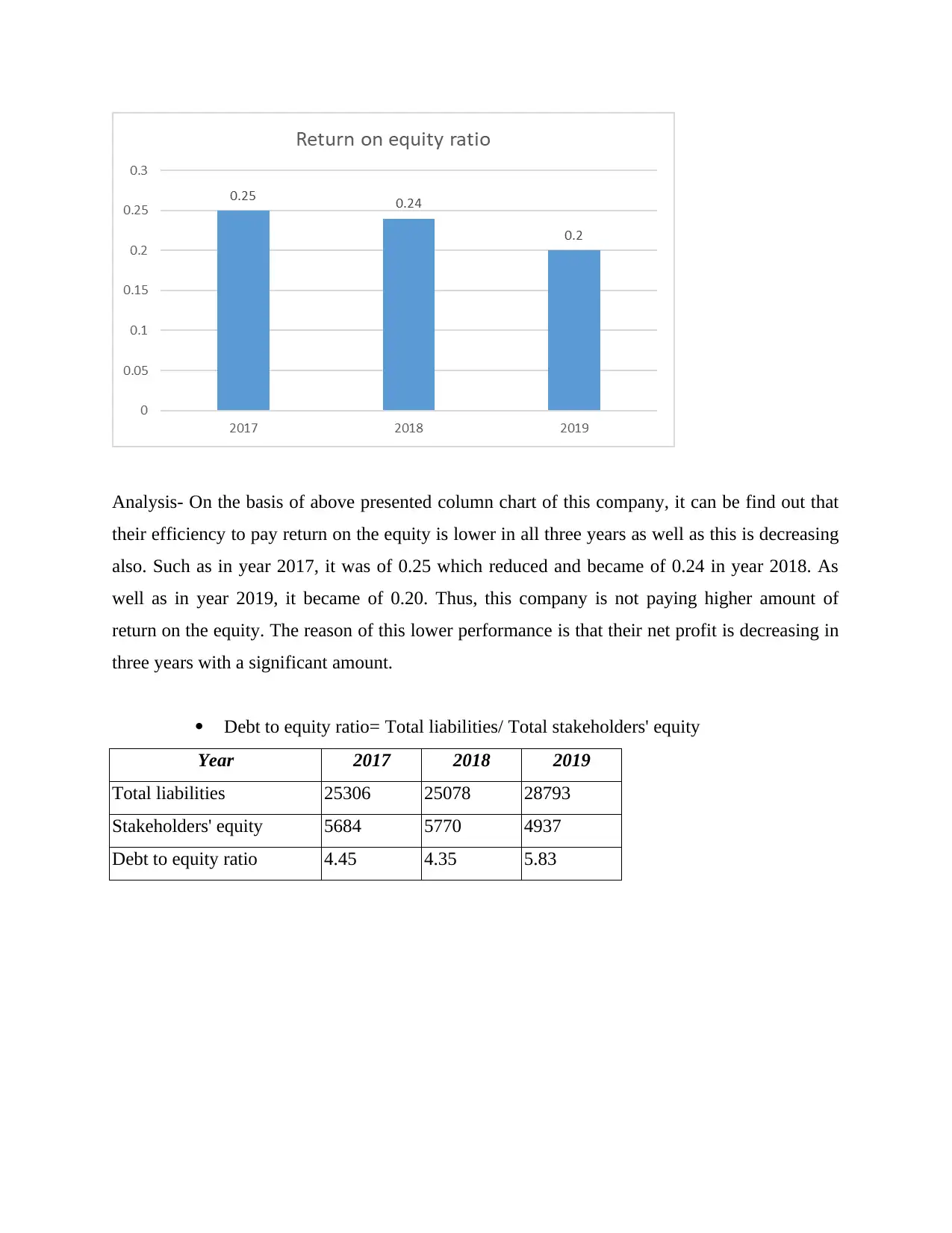

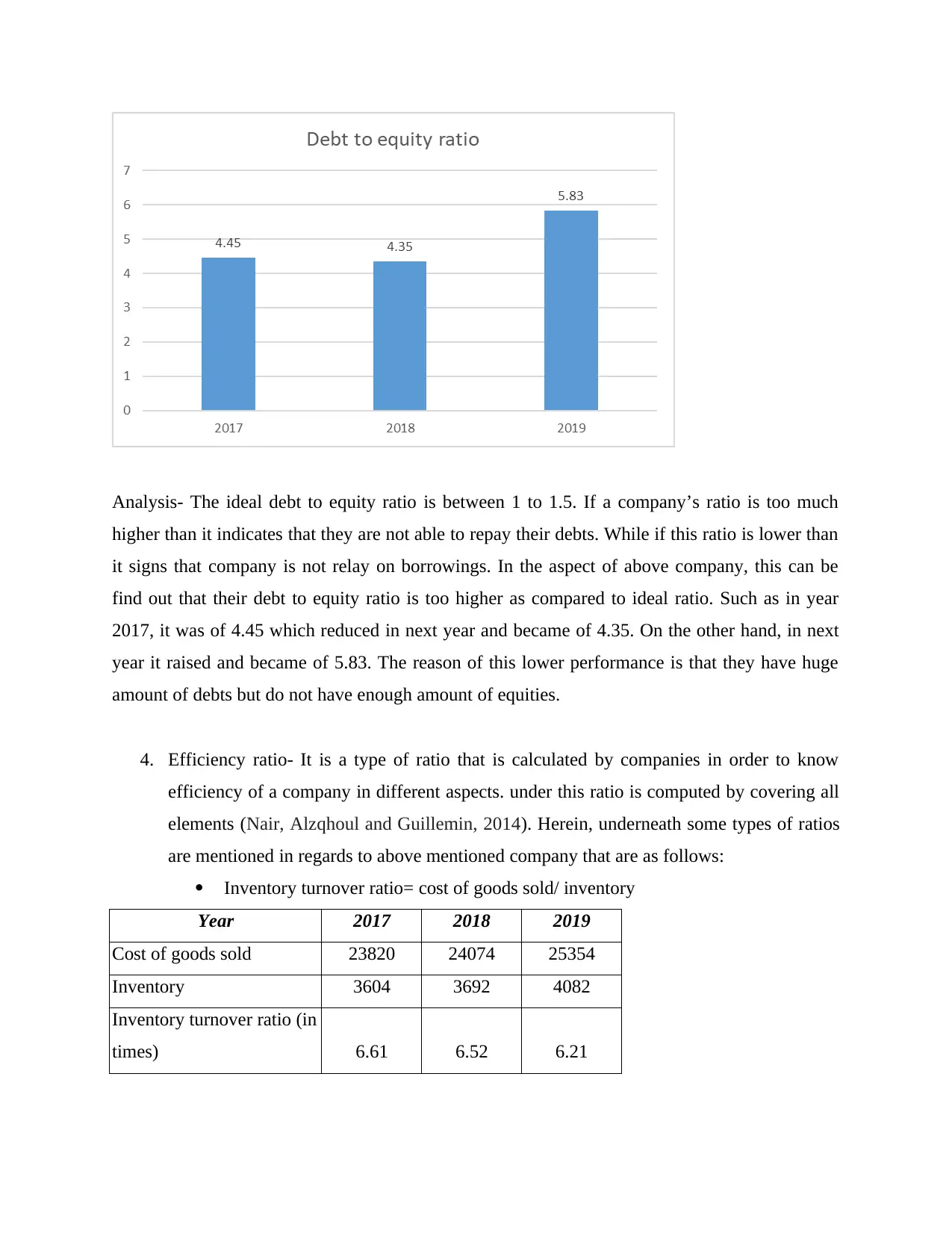

This report offers a comprehensive financial analysis of Imperial Brand plc, a UK-based tobacco manufacturing company. It meticulously examines the company's financial performance over three years (2017-2019) by calculating and interpreting various financial ratios. The analysis covers profitability ratios (gross profit margin, operating profit margin, net profit margin), liquidity ratios (current ratio, quick ratio), investor ratios (return on assets, dividend payout ratio, return on equity, debt to equity ratio), and efficiency ratios (inventory turnover, accounts receivable turnover, accounts payable turnover, total assets turnover, fixed assets turnover). The report evaluates the trends and implications of these ratios, offering insights into the company's financial health, efficiency, and ability to meet its financial obligations and provide returns to investors. The report also includes strategic recommendations based on the financial analysis.

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.