Economic and Financial Management: Impact on Business and Accounting Ratios

VerifiedAdded on 2023/01/13

|15

|3212

|64

AI Summary

This study explores the impact of economic factors on business and the importance of accounting ratios. It focuses on Sainsbury, a leading supermarket chain in the UK, and analyzes its performance over three years. The report provides insights into macro and microeconomic factors, computing ratios, and their significance in the business.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

ECONOMIC AND

FINANCIAL MANAGEMENT

FINANCIAL MANAGEMENT

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Executive Summary

Economics and financial management are seen as closely related as FM emphasize on managing

the funds for achieving objectives of the company. Economics focuses on using, creating and

transferring the commodities where microeconomics relates specifically with individuals and the

business decisions & macroeconomics focus on broader view of government implication on

nation economy. The present study is based on Sainsbury, a second leading supermarket chain in

UK having around 502 supermarket and the convenience stores. Furthermore, the report provides

deeper insights towards an effect of economic factors on the business and an importance of

accounting ratios. Moreover, comparative assessment would be made for three years in order to

analyse trend of company’s performance.

Economics and financial management are seen as closely related as FM emphasize on managing

the funds for achieving objectives of the company. Economics focuses on using, creating and

transferring the commodities where microeconomics relates specifically with individuals and the

business decisions & macroeconomics focus on broader view of government implication on

nation economy. The present study is based on Sainsbury, a second leading supermarket chain in

UK having around 502 supermarket and the convenience stores. Furthermore, the report provides

deeper insights towards an effect of economic factors on the business and an importance of

accounting ratios. Moreover, comparative assessment would be made for three years in order to

analyse trend of company’s performance.

Table of Contents

INTRODUCTION...........................................................................................................................4

a. Assessment of an economic factors and its effect on business................................................4

b. computing ratios for 3 years....................................................................................................6

c. Explaining the meaning of accounting ratios and its significance in the business..................8

d. Recommendations..................................................................................................................13

CONCLUSION..............................................................................................................................13

REFERENCES................................................................................................................................1

INTRODUCTION...........................................................................................................................4

a. Assessment of an economic factors and its effect on business................................................4

b. computing ratios for 3 years....................................................................................................6

c. Explaining the meaning of accounting ratios and its significance in the business..................8

d. Recommendations..................................................................................................................13

CONCLUSION..............................................................................................................................13

REFERENCES................................................................................................................................1

INTRODUCTION

Financial management refers to the strategic planning and organizing and directing the

financial undertakings in an organization. While, economic factor are that factor which deals

with tax rates, unemployment and polices. These factor creates both positive and negative impact

upon business such that inflation rate creates opposite impact while, decrease in tax rate affect

business in positive manner. Therefore, these economic factor may create hinder and success of

the business. Further, the current report will describe how the macro as well as micro- economic

factor affect the business using diagrams. Also, current study will describe some financial ratio

of Sainsbury for each consecutive years i.e. return on capital employed, net profit margin, current

ratio, debtor collection period, creditor payment period and efficiency ratio with their

importance. Last, report will recommend three strategic actions that a company should take by

evaluating the financial performance of company.

a. Assessment of an economic factors and its effect on business

Economic factors are stated as the factors that impact an overall economy and the

business that involves tax rates, wages, governmental activities, interest rates etc. there are

mainly two major economic factors that has a great impact on the business organizations that

includes macro and micro economic factors.

Macro economic factors referred as the factor that affects national economy as a whole

while a micro economic factor impacts business and an individual’s (Fernández, González and

Rodriguez, 2018). Major macro-economic factors that influence the business are unemployment,

interest rate, inflation and economic output. Main micro-economic factors that impact the

business are employees, competitors, shareholders, suppliers and the customers.

Financial management refers to the strategic planning and organizing and directing the

financial undertakings in an organization. While, economic factor are that factor which deals

with tax rates, unemployment and polices. These factor creates both positive and negative impact

upon business such that inflation rate creates opposite impact while, decrease in tax rate affect

business in positive manner. Therefore, these economic factor may create hinder and success of

the business. Further, the current report will describe how the macro as well as micro- economic

factor affect the business using diagrams. Also, current study will describe some financial ratio

of Sainsbury for each consecutive years i.e. return on capital employed, net profit margin, current

ratio, debtor collection period, creditor payment period and efficiency ratio with their

importance. Last, report will recommend three strategic actions that a company should take by

evaluating the financial performance of company.

a. Assessment of an economic factors and its effect on business

Economic factors are stated as the factors that impact an overall economy and the

business that involves tax rates, wages, governmental activities, interest rates etc. there are

mainly two major economic factors that has a great impact on the business organizations that

includes macro and micro economic factors.

Macro economic factors referred as the factor that affects national economy as a whole

while a micro economic factor impacts business and an individual’s (Fernández, González and

Rodriguez, 2018). Major macro-economic factors that influence the business are unemployment,

interest rate, inflation and economic output. Main micro-economic factors that impact the

business are employees, competitors, shareholders, suppliers and the customers.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

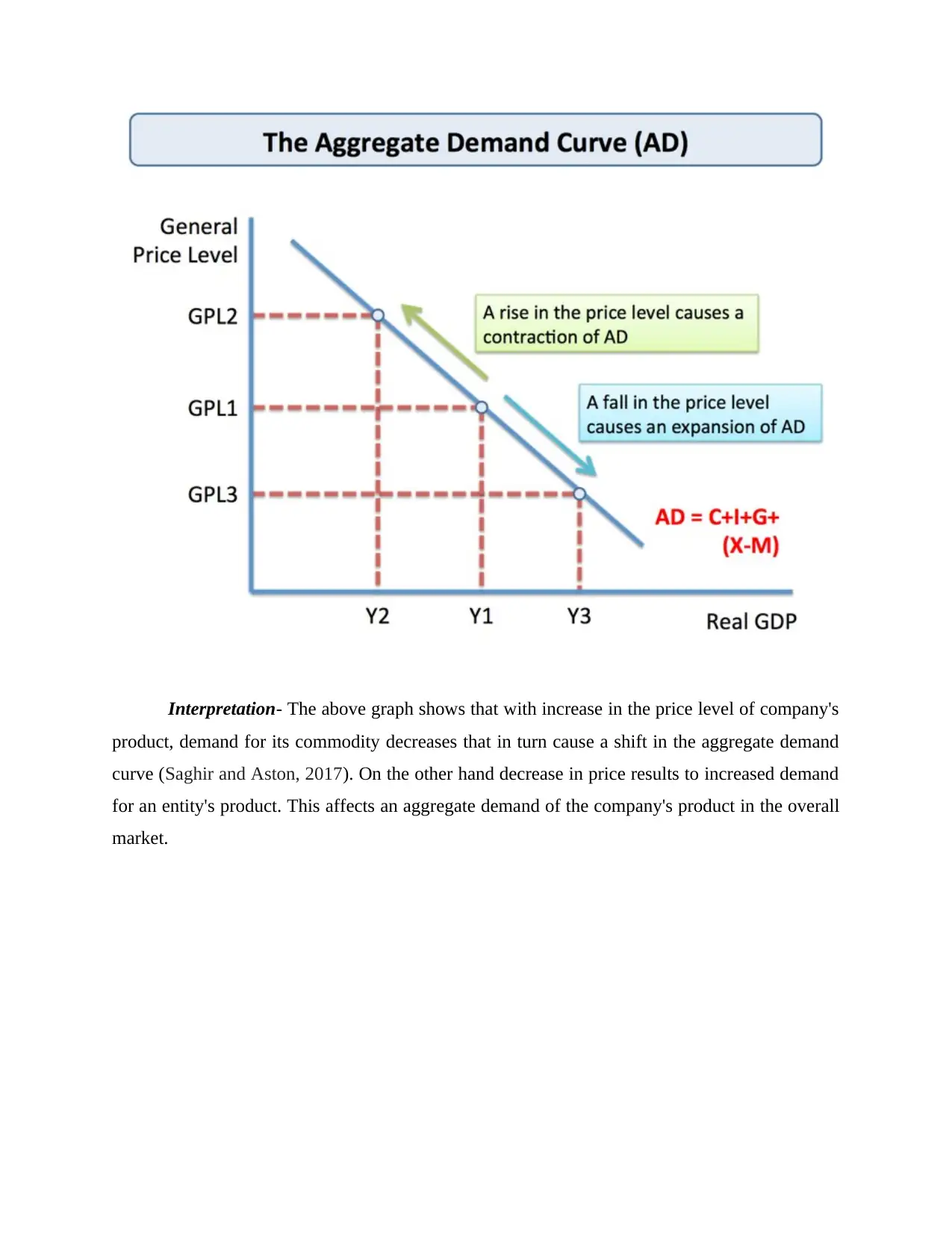

Interpretation- The above graph shows that with increase in the price level of company's

product, demand for its commodity decreases that in turn cause a shift in the aggregate demand

curve (Saghir and Aston, 2017). On the other hand decrease in price results to increased demand

for an entity's product. This affects an aggregate demand of the company's product in the overall

market.

product, demand for its commodity decreases that in turn cause a shift in the aggregate demand

curve (Saghir and Aston, 2017). On the other hand decrease in price results to increased demand

for an entity's product. This affects an aggregate demand of the company's product in the overall

market.

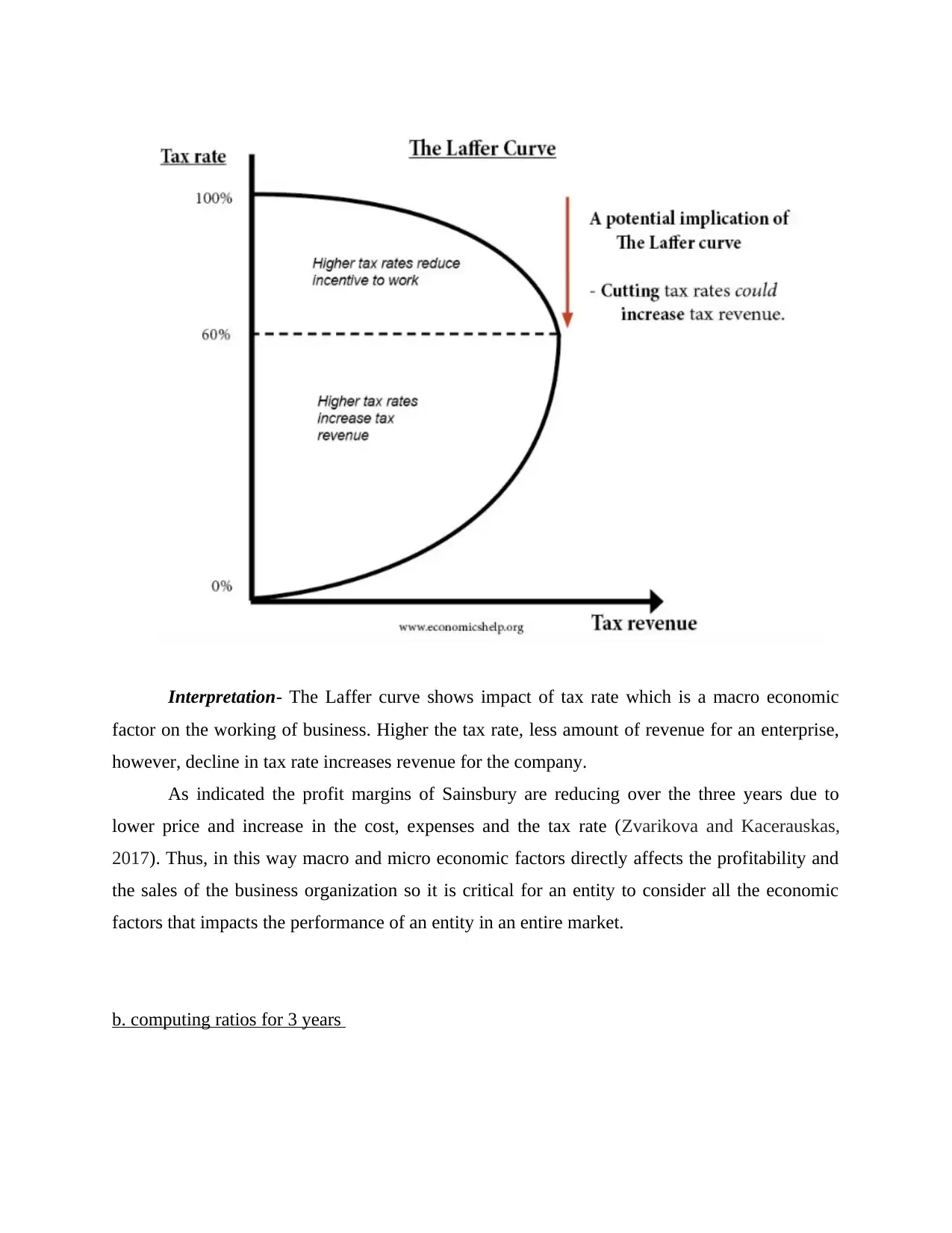

Interpretation- The Laffer curve shows impact of tax rate which is a macro economic

factor on the working of business. Higher the tax rate, less amount of revenue for an enterprise,

however, decline in tax rate increases revenue for the company.

As indicated the profit margins of Sainsbury are reducing over the three years due to

lower price and increase in the cost, expenses and the tax rate (Zvarikova and Kacerauskas,

2017). Thus, in this way macro and micro economic factors directly affects the profitability and

the sales of the business organization so it is critical for an entity to consider all the economic

factors that impacts the performance of an entity in an entire market.

b. computing ratios for 3 years

factor on the working of business. Higher the tax rate, less amount of revenue for an enterprise,

however, decline in tax rate increases revenue for the company.

As indicated the profit margins of Sainsbury are reducing over the three years due to

lower price and increase in the cost, expenses and the tax rate (Zvarikova and Kacerauskas,

2017). Thus, in this way macro and micro economic factors directly affects the profitability and

the sales of the business organization so it is critical for an entity to consider all the economic

factors that impacts the performance of an entity in an entire market.

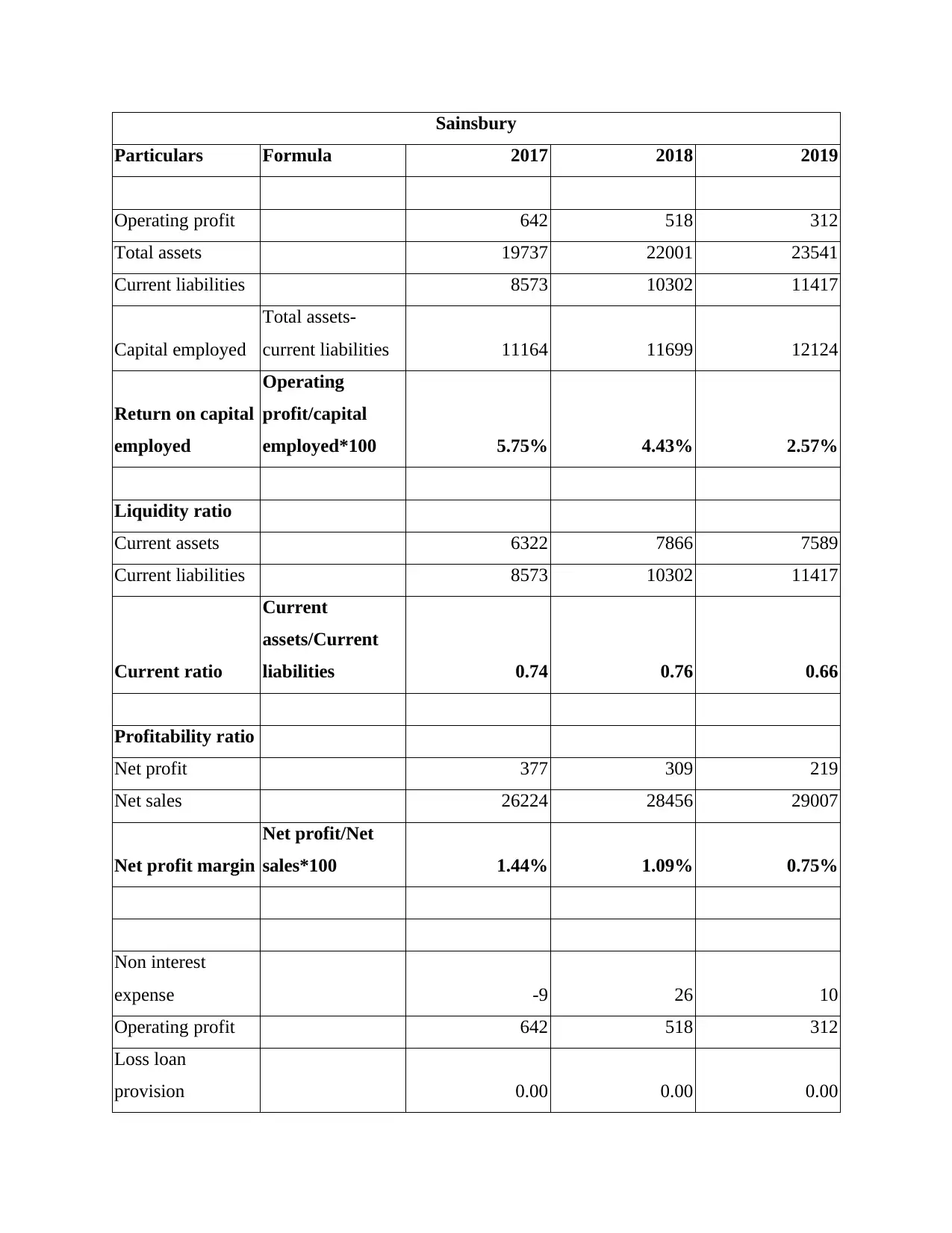

b. computing ratios for 3 years

Sainsbury

Particulars Formula 2017 2018 2019

Operating profit 642 518 312

Total assets 19737 22001 23541

Current liabilities 8573 10302 11417

Capital employed

Total assets-

current liabilities 11164 11699 12124

Return on capital

employed

Operating

profit/capital

employed*100 5.75% 4.43% 2.57%

Liquidity ratio

Current assets 6322 7866 7589

Current liabilities 8573 10302 11417

Current ratio

Current

assets/Current

liabilities 0.74 0.76 0.66

Profitability ratio

Net profit 377 309 219

Net sales 26224 28456 29007

Net profit margin

Net profit/Net

sales*100 1.44% 1.09% 0.75%

Non interest

expense -9 26 10

Operating profit 642 518 312

Loss loan

provision 0.00 0.00 0.00

Particulars Formula 2017 2018 2019

Operating profit 642 518 312

Total assets 19737 22001 23541

Current liabilities 8573 10302 11417

Capital employed

Total assets-

current liabilities 11164 11699 12124

Return on capital

employed

Operating

profit/capital

employed*100 5.75% 4.43% 2.57%

Liquidity ratio

Current assets 6322 7866 7589

Current liabilities 8573 10302 11417

Current ratio

Current

assets/Current

liabilities 0.74 0.76 0.66

Profitability ratio

Net profit 377 309 219

Net sales 26224 28456 29007

Net profit margin

Net profit/Net

sales*100 1.44% 1.09% 0.75%

Non interest

expense -9 26 10

Operating profit 642 518 312

Loss loan

provision 0.00 0.00 0.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

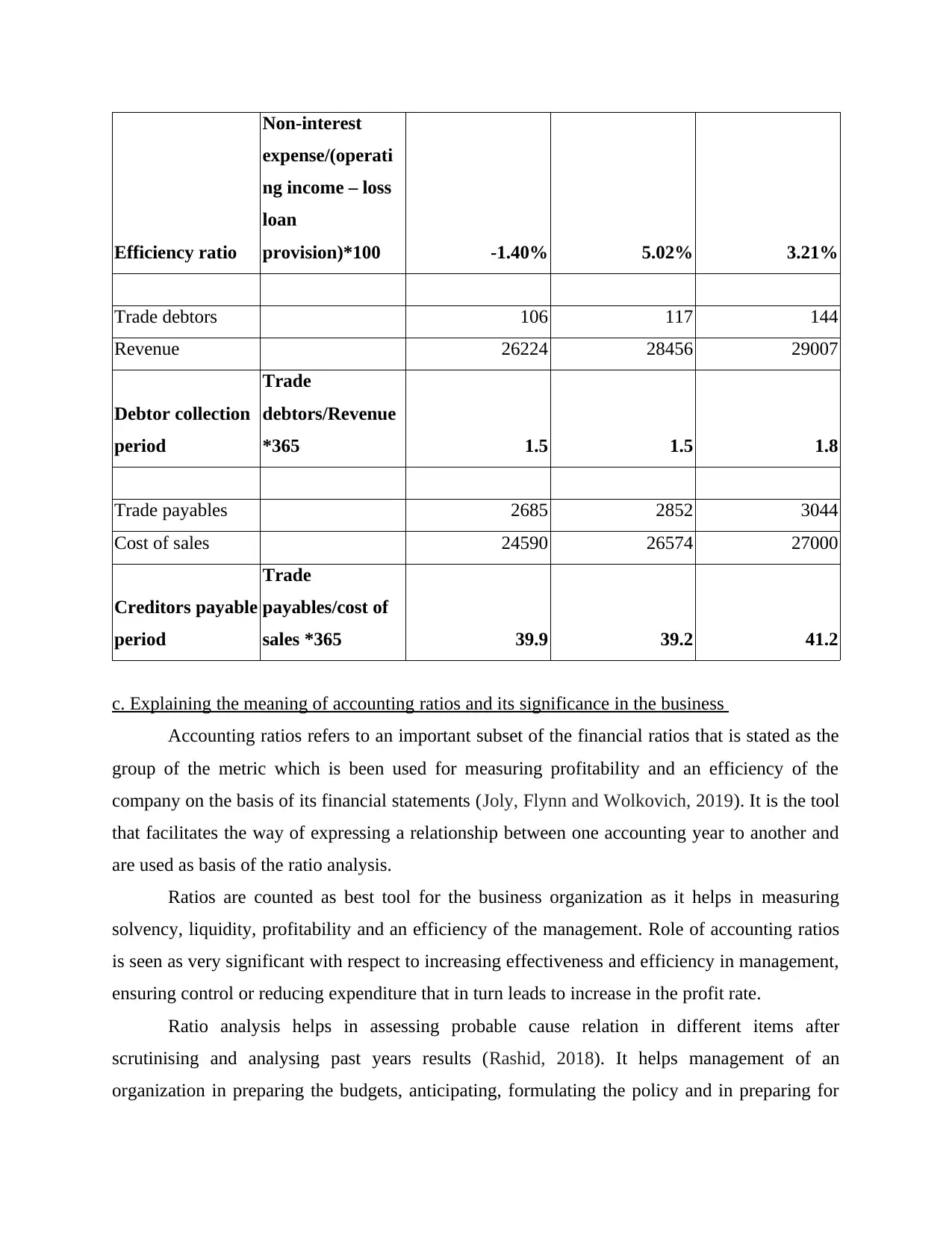

Efficiency ratio

Non-interest

expense/(operati

ng income – loss

loan

provision)*100 -1.40% 5.02% 3.21%

Trade debtors 106 117 144

Revenue 26224 28456 29007

Debtor collection

period

Trade

debtors/Revenue

*365 1.5 1.5 1.8

Trade payables 2685 2852 3044

Cost of sales 24590 26574 27000

Creditors payable

period

Trade

payables/cost of

sales *365 39.9 39.2 41.2

c. Explaining the meaning of accounting ratios and its significance in the business

Accounting ratios refers to an important subset of the financial ratios that is stated as the

group of the metric which is been used for measuring profitability and an efficiency of the

company on the basis of its financial statements (Joly, Flynn and Wolkovich, 2019). It is the tool

that facilitates the way of expressing a relationship between one accounting year to another and

are used as basis of the ratio analysis.

Ratios are counted as best tool for the business organization as it helps in measuring

solvency, liquidity, profitability and an efficiency of the management. Role of accounting ratios

is seen as very significant with respect to increasing effectiveness and efficiency in management,

ensuring control or reducing expenditure that in turn leads to increase in the profit rate.

Ratio analysis helps in assessing probable cause relation in different items after

scrutinising and analysing past years results (Rashid, 2018). It helps management of an

organization in preparing the budgets, anticipating, formulating the policy and in preparing for

Non-interest

expense/(operati

ng income – loss

loan

provision)*100 -1.40% 5.02% 3.21%

Trade debtors 106 117 144

Revenue 26224 28456 29007

Debtor collection

period

Trade

debtors/Revenue

*365 1.5 1.5 1.8

Trade payables 2685 2852 3044

Cost of sales 24590 26574 27000

Creditors payable

period

Trade

payables/cost of

sales *365 39.9 39.2 41.2

c. Explaining the meaning of accounting ratios and its significance in the business

Accounting ratios refers to an important subset of the financial ratios that is stated as the

group of the metric which is been used for measuring profitability and an efficiency of the

company on the basis of its financial statements (Joly, Flynn and Wolkovich, 2019). It is the tool

that facilitates the way of expressing a relationship between one accounting year to another and

are used as basis of the ratio analysis.

Ratios are counted as best tool for the business organization as it helps in measuring

solvency, liquidity, profitability and an efficiency of the management. Role of accounting ratios

is seen as very significant with respect to increasing effectiveness and efficiency in management,

ensuring control or reducing expenditure that in turn leads to increase in the profit rate.

Ratio analysis helps in assessing probable cause relation in different items after

scrutinising and analysing past years results (Rashid, 2018). It helps management of an

organization in preparing the budgets, anticipating, formulating the policy and in preparing for

the future action plan. It enables in considering time dimension by way of trend analysis that is

whether a firm is deteriorating or is improving over the years. Accounting ratios assist in making

an inter firm comparison between different departments or between same type of companies.

With the use of ratios, meaningful information could be communicated to all the users and

resulting, analyst could draw for right decisions. There are different ratios which depicts

efficiency, liquidity and profitability of the company that are as follows-

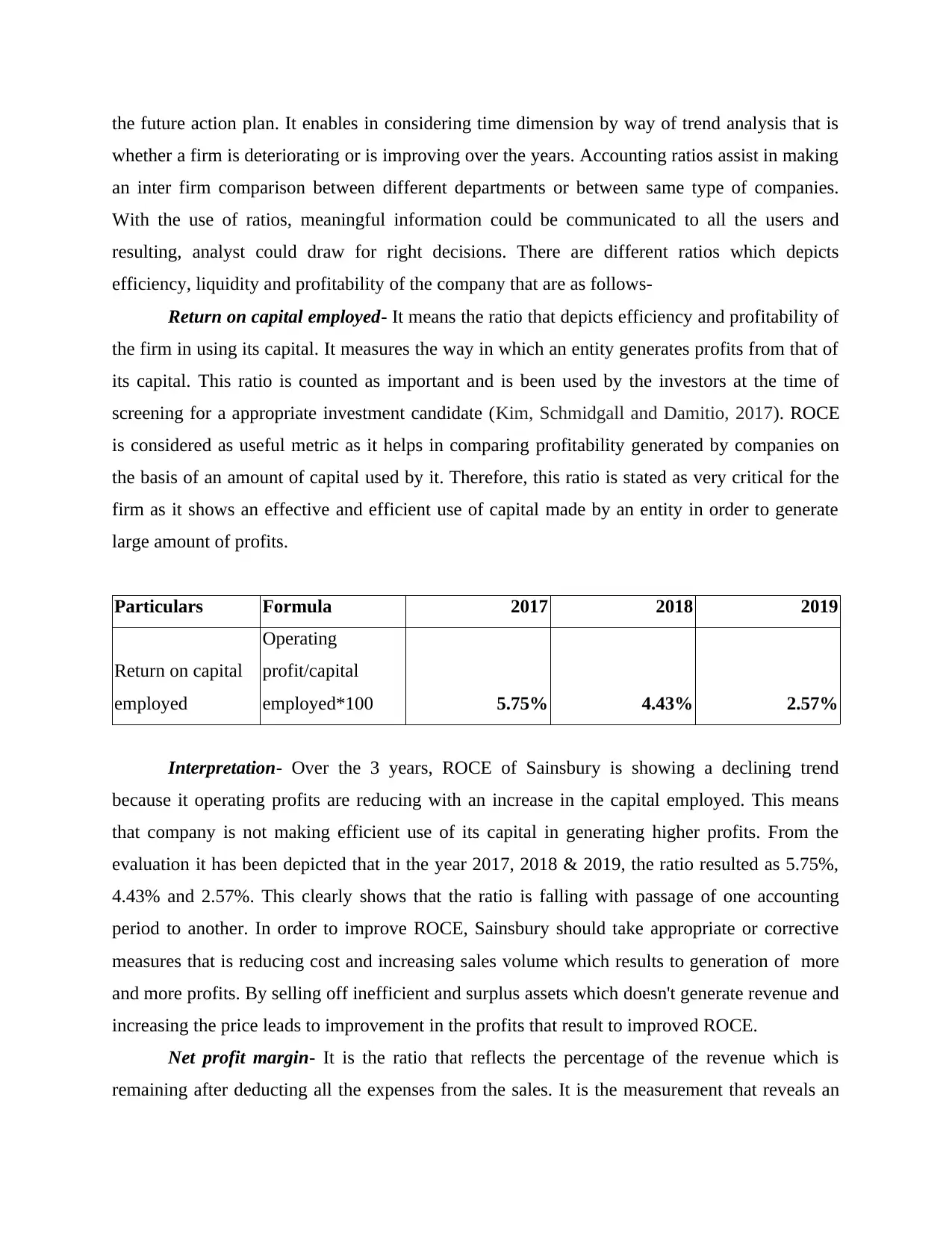

Return on capital employed- It means the ratio that depicts efficiency and profitability of

the firm in using its capital. It measures the way in which an entity generates profits from that of

its capital. This ratio is counted as important and is been used by the investors at the time of

screening for a appropriate investment candidate (Kim, Schmidgall and Damitio, 2017). ROCE

is considered as useful metric as it helps in comparing profitability generated by companies on

the basis of an amount of capital used by it. Therefore, this ratio is stated as very critical for the

firm as it shows an effective and efficient use of capital made by an entity in order to generate

large amount of profits.

Particulars Formula 2017 2018 2019

Return on capital

employed

Operating

profit/capital

employed*100 5.75% 4.43% 2.57%

Interpretation- Over the 3 years, ROCE of Sainsbury is showing a declining trend

because it operating profits are reducing with an increase in the capital employed. This means

that company is not making efficient use of its capital in generating higher profits. From the

evaluation it has been depicted that in the year 2017, 2018 & 2019, the ratio resulted as 5.75%,

4.43% and 2.57%. This clearly shows that the ratio is falling with passage of one accounting

period to another. In order to improve ROCE, Sainsbury should take appropriate or corrective

measures that is reducing cost and increasing sales volume which results to generation of more

and more profits. By selling off inefficient and surplus assets which doesn't generate revenue and

increasing the price leads to improvement in the profits that result to improved ROCE.

Net profit margin- It is the ratio that reflects the percentage of the revenue which is

remaining after deducting all the expenses from the sales. It is the measurement that reveals an

whether a firm is deteriorating or is improving over the years. Accounting ratios assist in making

an inter firm comparison between different departments or between same type of companies.

With the use of ratios, meaningful information could be communicated to all the users and

resulting, analyst could draw for right decisions. There are different ratios which depicts

efficiency, liquidity and profitability of the company that are as follows-

Return on capital employed- It means the ratio that depicts efficiency and profitability of

the firm in using its capital. It measures the way in which an entity generates profits from that of

its capital. This ratio is counted as important and is been used by the investors at the time of

screening for a appropriate investment candidate (Kim, Schmidgall and Damitio, 2017). ROCE

is considered as useful metric as it helps in comparing profitability generated by companies on

the basis of an amount of capital used by it. Therefore, this ratio is stated as very critical for the

firm as it shows an effective and efficient use of capital made by an entity in order to generate

large amount of profits.

Particulars Formula 2017 2018 2019

Return on capital

employed

Operating

profit/capital

employed*100 5.75% 4.43% 2.57%

Interpretation- Over the 3 years, ROCE of Sainsbury is showing a declining trend

because it operating profits are reducing with an increase in the capital employed. This means

that company is not making efficient use of its capital in generating higher profits. From the

evaluation it has been depicted that in the year 2017, 2018 & 2019, the ratio resulted as 5.75%,

4.43% and 2.57%. This clearly shows that the ratio is falling with passage of one accounting

period to another. In order to improve ROCE, Sainsbury should take appropriate or corrective

measures that is reducing cost and increasing sales volume which results to generation of more

and more profits. By selling off inefficient and surplus assets which doesn't generate revenue and

increasing the price leads to improvement in the profits that result to improved ROCE.

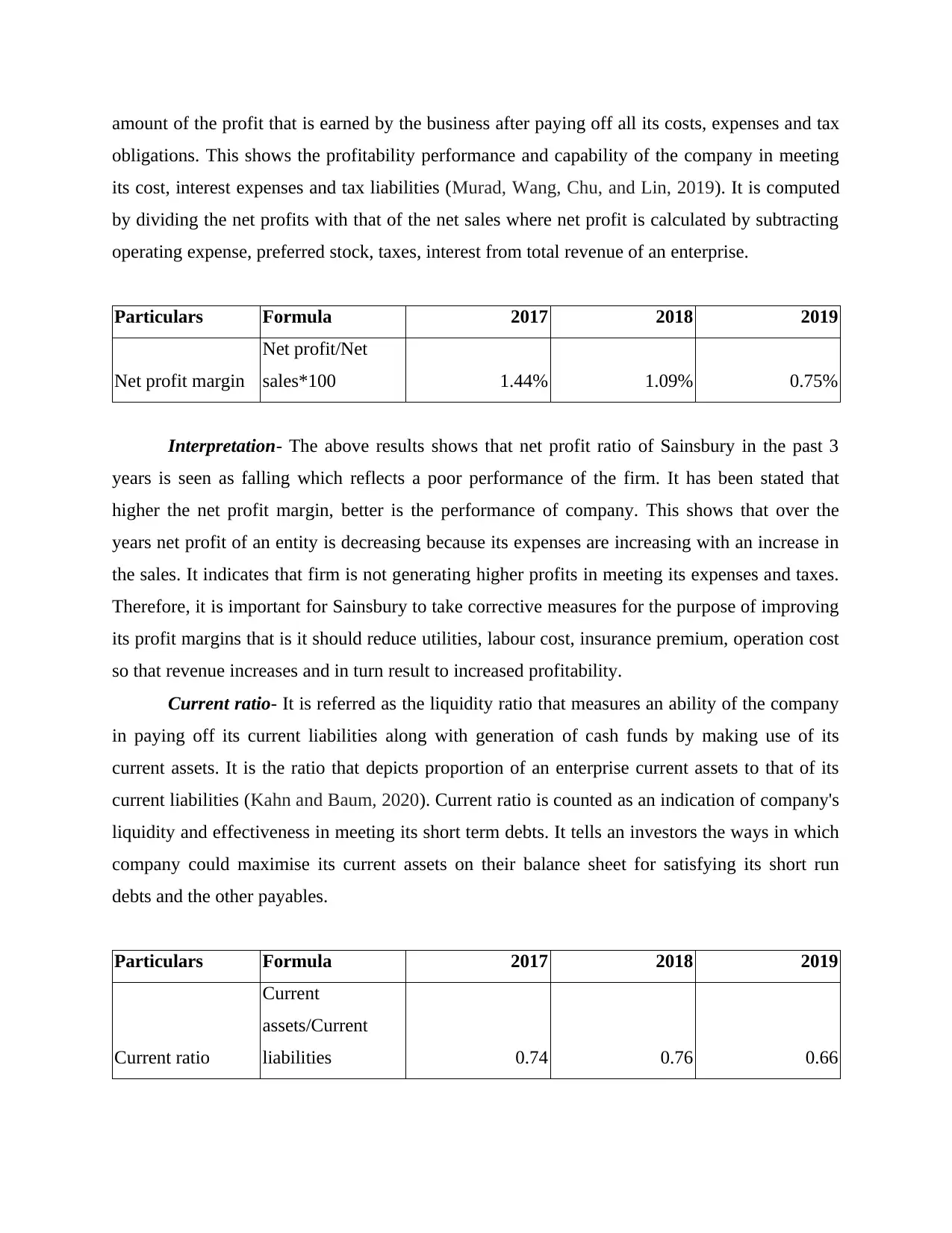

Net profit margin- It is the ratio that reflects the percentage of the revenue which is

remaining after deducting all the expenses from the sales. It is the measurement that reveals an

amount of the profit that is earned by the business after paying off all its costs, expenses and tax

obligations. This shows the profitability performance and capability of the company in meeting

its cost, interest expenses and tax liabilities (Murad, Wang, Chu, and Lin, 2019). It is computed

by dividing the net profits with that of the net sales where net profit is calculated by subtracting

operating expense, preferred stock, taxes, interest from total revenue of an enterprise.

Particulars Formula 2017 2018 2019

Net profit margin

Net profit/Net

sales*100 1.44% 1.09% 0.75%

Interpretation- The above results shows that net profit ratio of Sainsbury in the past 3

years is seen as falling which reflects a poor performance of the firm. It has been stated that

higher the net profit margin, better is the performance of company. This shows that over the

years net profit of an entity is decreasing because its expenses are increasing with an increase in

the sales. It indicates that firm is not generating higher profits in meeting its expenses and taxes.

Therefore, it is important for Sainsbury to take corrective measures for the purpose of improving

its profit margins that is it should reduce utilities, labour cost, insurance premium, operation cost

so that revenue increases and in turn result to increased profitability.

Current ratio- It is referred as the liquidity ratio that measures an ability of the company

in paying off its current liabilities along with generation of cash funds by making use of its

current assets. It is the ratio that depicts proportion of an enterprise current assets to that of its

current liabilities (Kahn and Baum, 2020). Current ratio is counted as an indication of company's

liquidity and effectiveness in meeting its short term debts. It tells an investors the ways in which

company could maximise its current assets on their balance sheet for satisfying its short run

debts and the other payables.

Particulars Formula 2017 2018 2019

Current ratio

Current

assets/Current

liabilities 0.74 0.76 0.66

obligations. This shows the profitability performance and capability of the company in meeting

its cost, interest expenses and tax liabilities (Murad, Wang, Chu, and Lin, 2019). It is computed

by dividing the net profits with that of the net sales where net profit is calculated by subtracting

operating expense, preferred stock, taxes, interest from total revenue of an enterprise.

Particulars Formula 2017 2018 2019

Net profit margin

Net profit/Net

sales*100 1.44% 1.09% 0.75%

Interpretation- The above results shows that net profit ratio of Sainsbury in the past 3

years is seen as falling which reflects a poor performance of the firm. It has been stated that

higher the net profit margin, better is the performance of company. This shows that over the

years net profit of an entity is decreasing because its expenses are increasing with an increase in

the sales. It indicates that firm is not generating higher profits in meeting its expenses and taxes.

Therefore, it is important for Sainsbury to take corrective measures for the purpose of improving

its profit margins that is it should reduce utilities, labour cost, insurance premium, operation cost

so that revenue increases and in turn result to increased profitability.

Current ratio- It is referred as the liquidity ratio that measures an ability of the company

in paying off its current liabilities along with generation of cash funds by making use of its

current assets. It is the ratio that depicts proportion of an enterprise current assets to that of its

current liabilities (Kahn and Baum, 2020). Current ratio is counted as an indication of company's

liquidity and effectiveness in meeting its short term debts. It tells an investors the ways in which

company could maximise its current assets on their balance sheet for satisfying its short run

debts and the other payables.

Particulars Formula 2017 2018 2019

Current ratio

Current

assets/Current

liabilities 0.74 0.76 0.66

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

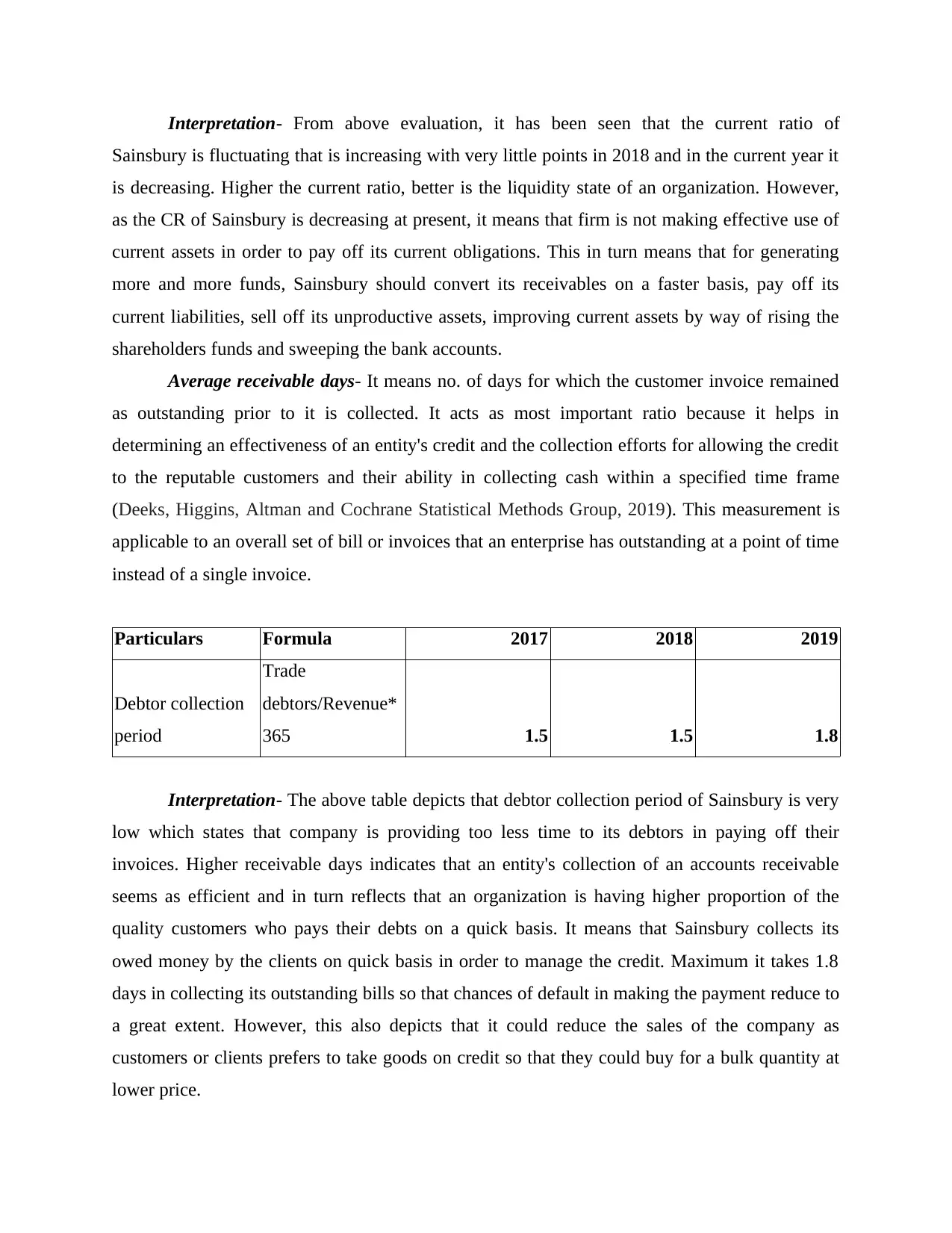

Interpretation- From above evaluation, it has been seen that the current ratio of

Sainsbury is fluctuating that is increasing with very little points in 2018 and in the current year it

is decreasing. Higher the current ratio, better is the liquidity state of an organization. However,

as the CR of Sainsbury is decreasing at present, it means that firm is not making effective use of

current assets in order to pay off its current obligations. This in turn means that for generating

more and more funds, Sainsbury should convert its receivables on a faster basis, pay off its

current liabilities, sell off its unproductive assets, improving current assets by way of rising the

shareholders funds and sweeping the bank accounts.

Average receivable days- It means no. of days for which the customer invoice remained

as outstanding prior to it is collected. It acts as most important ratio because it helps in

determining an effectiveness of an entity's credit and the collection efforts for allowing the credit

to the reputable customers and their ability in collecting cash within a specified time frame

(Deeks, Higgins, Altman and Cochrane Statistical Methods Group, 2019). This measurement is

applicable to an overall set of bill or invoices that an enterprise has outstanding at a point of time

instead of a single invoice.

Particulars Formula 2017 2018 2019

Debtor collection

period

Trade

debtors/Revenue*

365 1.5 1.5 1.8

Interpretation- The above table depicts that debtor collection period of Sainsbury is very

low which states that company is providing too less time to its debtors in paying off their

invoices. Higher receivable days indicates that an entity's collection of an accounts receivable

seems as efficient and in turn reflects that an organization is having higher proportion of the

quality customers who pays their debts on a quick basis. It means that Sainsbury collects its

owed money by the clients on quick basis in order to manage the credit. Maximum it takes 1.8

days in collecting its outstanding bills so that chances of default in making the payment reduce to

a great extent. However, this also depicts that it could reduce the sales of the company as

customers or clients prefers to take goods on credit so that they could buy for a bulk quantity at

lower price.

Sainsbury is fluctuating that is increasing with very little points in 2018 and in the current year it

is decreasing. Higher the current ratio, better is the liquidity state of an organization. However,

as the CR of Sainsbury is decreasing at present, it means that firm is not making effective use of

current assets in order to pay off its current obligations. This in turn means that for generating

more and more funds, Sainsbury should convert its receivables on a faster basis, pay off its

current liabilities, sell off its unproductive assets, improving current assets by way of rising the

shareholders funds and sweeping the bank accounts.

Average receivable days- It means no. of days for which the customer invoice remained

as outstanding prior to it is collected. It acts as most important ratio because it helps in

determining an effectiveness of an entity's credit and the collection efforts for allowing the credit

to the reputable customers and their ability in collecting cash within a specified time frame

(Deeks, Higgins, Altman and Cochrane Statistical Methods Group, 2019). This measurement is

applicable to an overall set of bill or invoices that an enterprise has outstanding at a point of time

instead of a single invoice.

Particulars Formula 2017 2018 2019

Debtor collection

period

Trade

debtors/Revenue*

365 1.5 1.5 1.8

Interpretation- The above table depicts that debtor collection period of Sainsbury is very

low which states that company is providing too less time to its debtors in paying off their

invoices. Higher receivable days indicates that an entity's collection of an accounts receivable

seems as efficient and in turn reflects that an organization is having higher proportion of the

quality customers who pays their debts on a quick basis. It means that Sainsbury collects its

owed money by the clients on quick basis in order to manage the credit. Maximum it takes 1.8

days in collecting its outstanding bills so that chances of default in making the payment reduce to

a great extent. However, this also depicts that it could reduce the sales of the company as

customers or clients prefers to take goods on credit so that they could buy for a bulk quantity at

lower price.

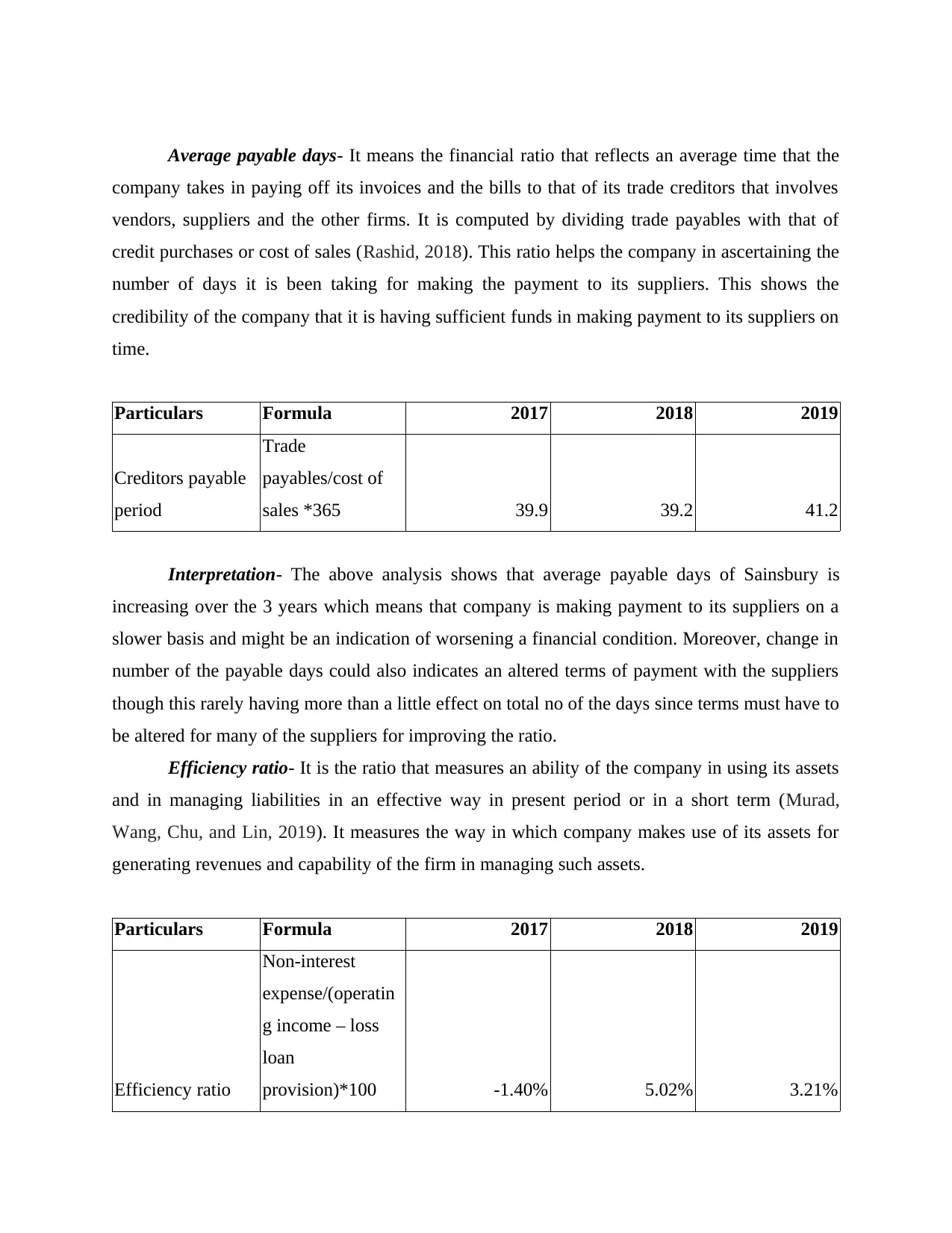

Average payable days- It means the financial ratio that reflects an average time that the

company takes in paying off its invoices and the bills to that of its trade creditors that involves

vendors, suppliers and the other firms. It is computed by dividing trade payables with that of

credit purchases or cost of sales (Rashid, 2018). This ratio helps the company in ascertaining the

number of days it is been taking for making the payment to its suppliers. This shows the

credibility of the company that it is having sufficient funds in making payment to its suppliers on

time.

Particulars Formula 2017 2018 2019

Creditors payable

period

Trade

payables/cost of

sales *365 39.9 39.2 41.2

Interpretation- The above analysis shows that average payable days of Sainsbury is

increasing over the 3 years which means that company is making payment to its suppliers on a

slower basis and might be an indication of worsening a financial condition. Moreover, change in

number of the payable days could also indicates an altered terms of payment with the suppliers

though this rarely having more than a little effect on total no of the days since terms must have to

be altered for many of the suppliers for improving the ratio.

Efficiency ratio- It is the ratio that measures an ability of the company in using its assets

and in managing liabilities in an effective way in present period or in a short term (Murad,

Wang, Chu, and Lin, 2019). It measures the way in which company makes use of its assets for

generating revenues and capability of the firm in managing such assets.

Particulars Formula 2017 2018 2019

Efficiency ratio

Non-interest

expense/(operatin

g income – loss

loan

provision)*100 -1.40% 5.02% 3.21%

company takes in paying off its invoices and the bills to that of its trade creditors that involves

vendors, suppliers and the other firms. It is computed by dividing trade payables with that of

credit purchases or cost of sales (Rashid, 2018). This ratio helps the company in ascertaining the

number of days it is been taking for making the payment to its suppliers. This shows the

credibility of the company that it is having sufficient funds in making payment to its suppliers on

time.

Particulars Formula 2017 2018 2019

Creditors payable

period

Trade

payables/cost of

sales *365 39.9 39.2 41.2

Interpretation- The above analysis shows that average payable days of Sainsbury is

increasing over the 3 years which means that company is making payment to its suppliers on a

slower basis and might be an indication of worsening a financial condition. Moreover, change in

number of the payable days could also indicates an altered terms of payment with the suppliers

though this rarely having more than a little effect on total no of the days since terms must have to

be altered for many of the suppliers for improving the ratio.

Efficiency ratio- It is the ratio that measures an ability of the company in using its assets

and in managing liabilities in an effective way in present period or in a short term (Murad,

Wang, Chu, and Lin, 2019). It measures the way in which company makes use of its assets for

generating revenues and capability of the firm in managing such assets.

Particulars Formula 2017 2018 2019

Efficiency ratio

Non-interest

expense/(operatin

g income – loss

loan

provision)*100 -1.40% 5.02% 3.21%

Interpretation- It has been analysed that an efficiency ratio of Sainsbury is increasing in

the year 2018 resulted as 5.02% from -1.40% in 2017, this clearly shows that it has take adequate

measures like effective use of assets that resulted. On the other side, in 2019, ratio decreases and

accounted as 3.21% which means that efficiency of Sainsbury in using its assets decreases.

d. Recommendations

The above computation shows that overall the liquidity, profitability and efficiency of

Sainsbury over three years does not seems as good so it should take appropriate steps for

increasing its profitability, cash and revenue. For improving the liquidity position or current

ratio, Sainsbury should opt for submitting the invoices on an early basis or in a timely manner. It

should switch from the short run debs to the long run debts so that money can be saved and could

be used in near term in a better way. By increasing the sales and reducing the cost, Sainsbury

could improve its profitability condition. Sainsbury should focus on managing its expenses and

the income in order to optimize its efficiency ratio.

CONCLUSION

By summing up the above report it has been summarised that economic factors has great

influence on the business and affects the smooth functioning of an enterprise in terms of

aggregate demand, tax rate etc. Accounting ratios is the most useful tool that helps in making the

comparative analysis of current year results with that of past year results so that trend relating to

financial performance of Sainsbury could be made effectively and efficiently.

the year 2018 resulted as 5.02% from -1.40% in 2017, this clearly shows that it has take adequate

measures like effective use of assets that resulted. On the other side, in 2019, ratio decreases and

accounted as 3.21% which means that efficiency of Sainsbury in using its assets decreases.

d. Recommendations

The above computation shows that overall the liquidity, profitability and efficiency of

Sainsbury over three years does not seems as good so it should take appropriate steps for

increasing its profitability, cash and revenue. For improving the liquidity position or current

ratio, Sainsbury should opt for submitting the invoices on an early basis or in a timely manner. It

should switch from the short run debs to the long run debts so that money can be saved and could

be used in near term in a better way. By increasing the sales and reducing the cost, Sainsbury

could improve its profitability condition. Sainsbury should focus on managing its expenses and

the income in order to optimize its efficiency ratio.

CONCLUSION

By summing up the above report it has been summarised that economic factors has great

influence on the business and affects the smooth functioning of an enterprise in terms of

aggregate demand, tax rate etc. Accounting ratios is the most useful tool that helps in making the

comparative analysis of current year results with that of past year results so that trend relating to

financial performance of Sainsbury could be made effectively and efficiently.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and journals

Deeks, J. J., Higgins, J. P., Altman, D. G. and Cochrane Statistical Methods Group, 2019.

Analysing data and undertaking meta‐analyses. Cochrane handbook for systematic reviews

of interventions. pp.241-284.

Fernández, A., González, A. and Rodriguez, D., 2018. Sharing a ride on the commodities roller

coaster: Common factors in business cycles of emerging economies. Journal of

International Economics. 111. pp.99-121.

Joly, S., Flynn, D. F. and Wolkovich, E. M., 2019. On the importance of accounting for

intraspecific genomic relatedness in multi‐species studies. Methods in Ecology and

Evolution. 10(7). pp.994-1001.

Kahn, M. J. and Baum, N., 2020. Basic Accounting and Interpretation of Financial Statements.

In The Business Basics of Building and Managing a Healthcare Practice (pp. 13-18).

Springer, Cham.

Kim, M., Schmidgall, R. S. and Damitio, J. W., 2017. Key managerial accounting skills for

lodging industry managers: The third phase of a repeated cross-sectional

study. International Journal of Hospitality & Tourism Administration. 18(1). pp.23-40.

Murad, M. H., Wang, Z., Chu, H. and Lin, L., 2019. When continuous outcomes are measured

using different scales: guide for meta-analysis and interpretation. Bmj. 364. p.k4817.

Rashid, C. A., 2018. Efficiency of Financial Ratios Analysis for Evaluating Companies’

Liquidity. International Journal of Social Sciences & Educational Studies. 4(4). pp.110-

123.

Saghir, M. and Aston, J., 2017. The Impact of Various Economic Factors in accessing Finance

within the Business Sector: Cases from UK Financial Services Companies.

Zvarikova, K. and Kacerauskas, T., 2017. Social and economic factors affecting the

entrepreneurial intention of university students. Transformations in Business &

Economics. 16(3). pp.220-239.

1

Books and journals

Deeks, J. J., Higgins, J. P., Altman, D. G. and Cochrane Statistical Methods Group, 2019.

Analysing data and undertaking meta‐analyses. Cochrane handbook for systematic reviews

of interventions. pp.241-284.

Fernández, A., González, A. and Rodriguez, D., 2018. Sharing a ride on the commodities roller

coaster: Common factors in business cycles of emerging economies. Journal of

International Economics. 111. pp.99-121.

Joly, S., Flynn, D. F. and Wolkovich, E. M., 2019. On the importance of accounting for

intraspecific genomic relatedness in multi‐species studies. Methods in Ecology and

Evolution. 10(7). pp.994-1001.

Kahn, M. J. and Baum, N., 2020. Basic Accounting and Interpretation of Financial Statements.

In The Business Basics of Building and Managing a Healthcare Practice (pp. 13-18).

Springer, Cham.

Kim, M., Schmidgall, R. S. and Damitio, J. W., 2017. Key managerial accounting skills for

lodging industry managers: The third phase of a repeated cross-sectional

study. International Journal of Hospitality & Tourism Administration. 18(1). pp.23-40.

Murad, M. H., Wang, Z., Chu, H. and Lin, L., 2019. When continuous outcomes are measured

using different scales: guide for meta-analysis and interpretation. Bmj. 364. p.k4817.

Rashid, C. A., 2018. Efficiency of Financial Ratios Analysis for Evaluating Companies’

Liquidity. International Journal of Social Sciences & Educational Studies. 4(4). pp.110-

123.

Saghir, M. and Aston, J., 2017. The Impact of Various Economic Factors in accessing Finance

within the Business Sector: Cases from UK Financial Services Companies.

Zvarikova, K. and Kacerauskas, T., 2017. Social and economic factors affecting the

entrepreneurial intention of university students. Transformations in Business &

Economics. 16(3). pp.220-239.

1

2

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.