Applying Economic Principles: Cost, Production, Pricing & Competition

VerifiedAdded on 2023/06/11

|9

|1937

|167

Homework Assignment

AI Summary

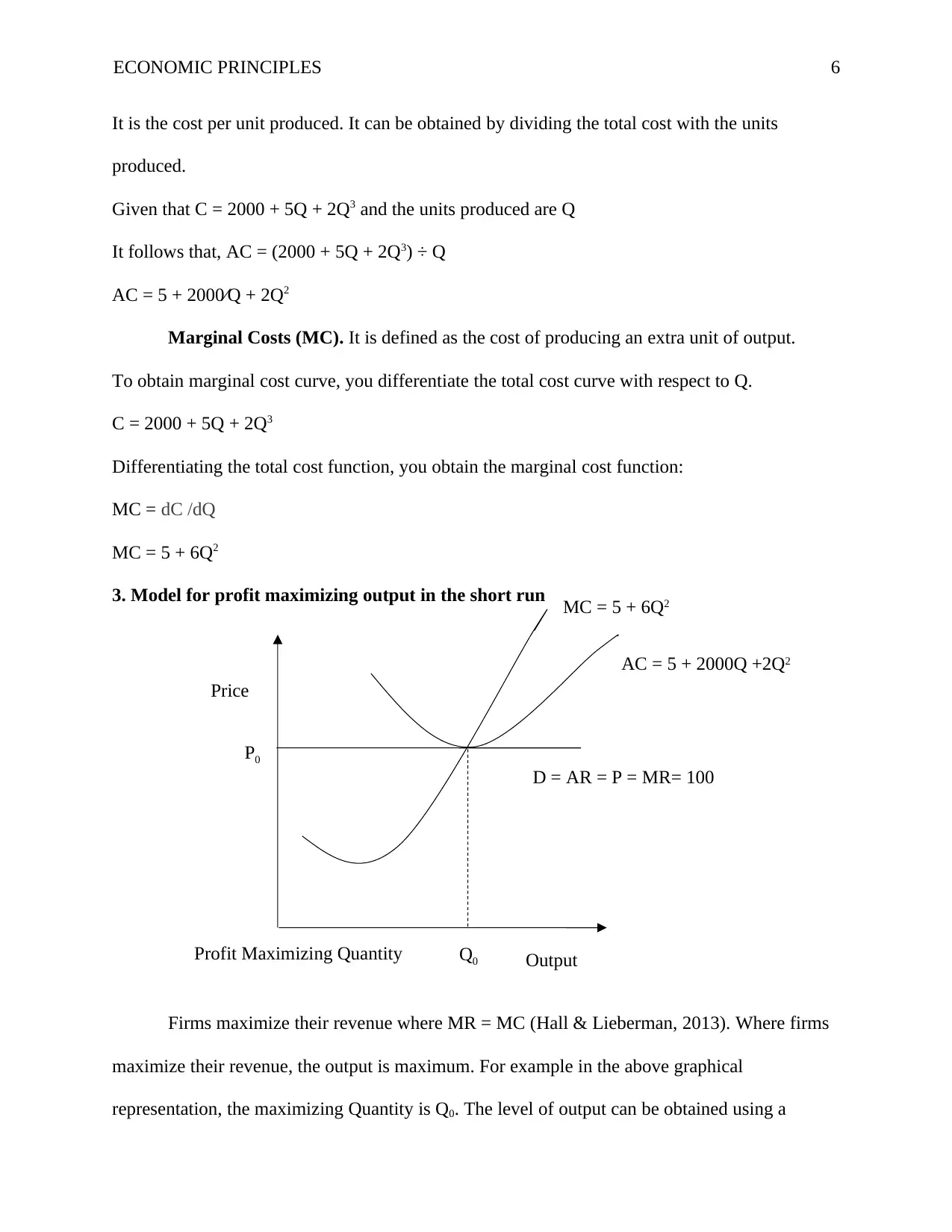

This assignment delves into key economic principles, focusing on cost and production analysis, pricing strategies, and competitive strategies within a perfectly competitive market. It differentiates between short-run and long-run production, explaining how variable and fixed costs influence total production costs. Various pricing strategies, including marginal cost pricing and cost-plus pricing, are examined, highlighting their significance for organizations in maximizing profits and maintaining competitive advantage. The assignment also explores competitive strategies like cost leadership and differentiation, emphasizing their role in driving a firm's profitability. Furthermore, it derives cost functions, including fixed costs, variable costs, average costs, and marginal costs, using a given total cost function. Finally, it models profit-maximizing output in both the short run and long run, applying mathematical models to determine optimal output levels under perfect competition. Desklib provides access to this assignment and a wealth of other study resources for students.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.