BEO1105 Economic Principles: Supply, Demand, and Market Analysis

VerifiedAdded on 2023/04/21

|12

|1578

|152

Homework Assignment

AI Summary

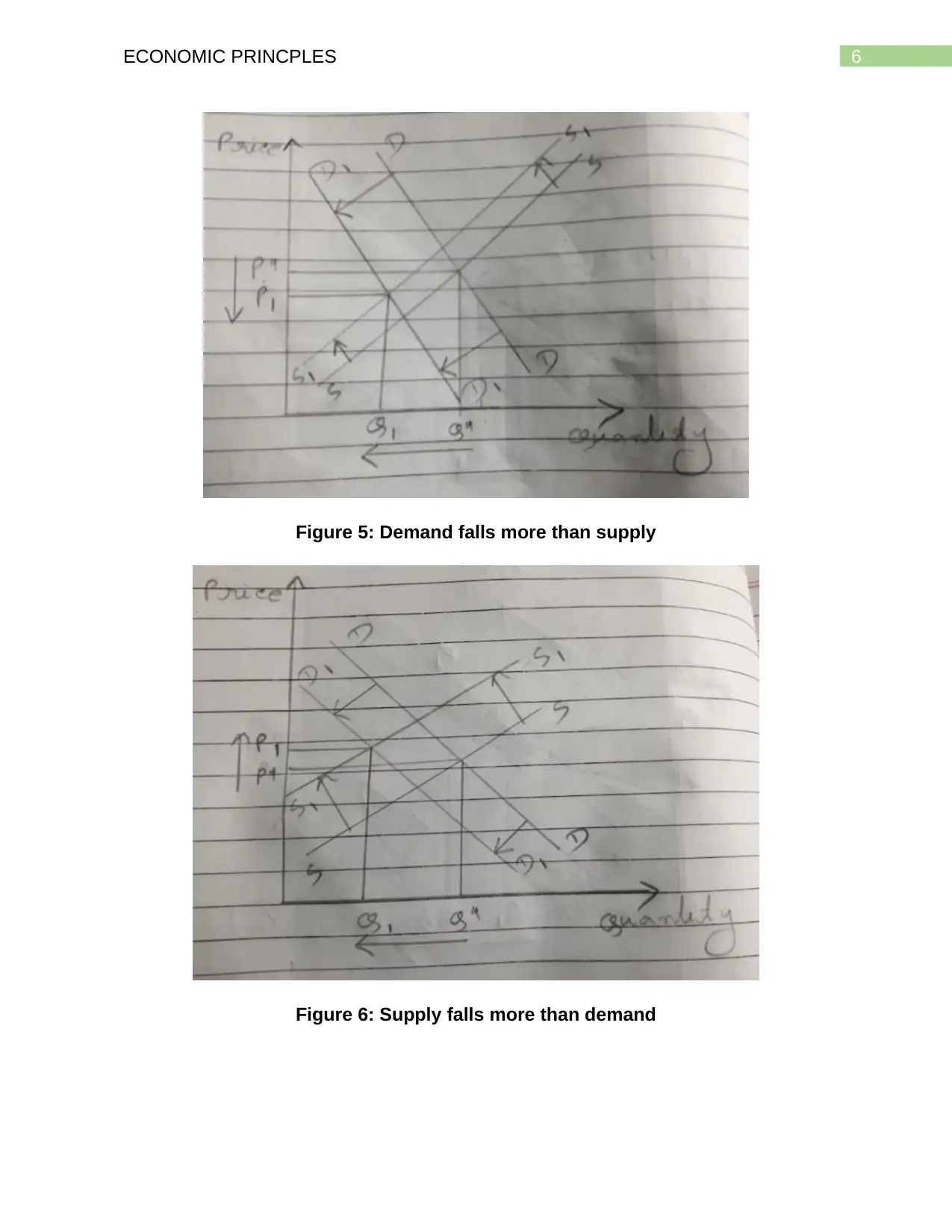

This assignment delves into fundamental economic principles, particularly focusing on demand and supply analysis within the Australian market context. It examines the impact of various factors such as changes in the price of substitute goods, technological advancements, and income fluctuations on the market for woollen jumpers. The assignment also addresses the flaws in reasoning related to shifts and movements along demand and supply curves, using the example of garlic consumption. Furthermore, it analyzes the effects of simultaneous changes in demand and supply, as illustrated by the bird flu scenario affecting the live chicken market in Sweden. The concepts of elastic and inelastic demand are explored in relation to changes in supply and their impact on total revenue. Finally, the assignment discusses the impact of new firms entering an industry due to economic profits, leading to increased market supply and a subsequent fall in equilibrium prices. Desklib offers a wide range of resources, including past papers and solved assignments, to aid students in their academic pursuits.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.