Economics Question 2022

VerifiedAdded on 2022/10/04

|17

|3216

|33

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Economics

August 12

2019

August 12

2019

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

Question 1: Production Possibility Curve..............................................................................................2

(1) Study of Joan’s Production Possibility Curve........................................................................2

(i) Production Possibility Curve for Joan....................................................................................2

(ii) Production Possibility Curve if opportunity cost was constant..........................................3

(iii) Combinations inside the Production Possibility Curve (PPC)............................................4

(iv) Combinations outside the Production Possibility Curve (PPC)..........................................5

(2) Concept of ‘Scarcity’.............................................................................................................6

Question 2: Demand and Supply...........................................................................................................7

(1) Improvement in technology...................................................................................................7

(i) Effect on the equilibrium price and quantity of solar-powered motor vehicle.......................7

(ii) Effect on the equilibrium price and quantity of conventional motor vehicle......................7

(2) Impact of the price ceiling.....................................................................................................7

Question 3: Price Elasticity of Demand.................................................................................................8

(1) Calculation of price elasticity using the midpoint method.....................................................8

(2) Price elasticity of demand for ice-creams in winter...............................................................9

(3) Price elasticity of demand for cigarettes..............................................................................10

Question 4: Types of Costs..................................................................................................................10

(1) Calculation of costs and profit.............................................................................................10

(2) Firm’s operation in short-run...............................................................................................11

(3) Price-taking firm profit maximization..................................................................................11

Question 1: Production Possibility Curve..............................................................................................2

(1) Study of Joan’s Production Possibility Curve........................................................................2

(i) Production Possibility Curve for Joan....................................................................................2

(ii) Production Possibility Curve if opportunity cost was constant..........................................3

(iii) Combinations inside the Production Possibility Curve (PPC)............................................4

(iv) Combinations outside the Production Possibility Curve (PPC)..........................................5

(2) Concept of ‘Scarcity’.............................................................................................................6

Question 2: Demand and Supply...........................................................................................................7

(1) Improvement in technology...................................................................................................7

(i) Effect on the equilibrium price and quantity of solar-powered motor vehicle.......................7

(ii) Effect on the equilibrium price and quantity of conventional motor vehicle......................7

(2) Impact of the price ceiling.....................................................................................................7

Question 3: Price Elasticity of Demand.................................................................................................8

(1) Calculation of price elasticity using the midpoint method.....................................................8

(2) Price elasticity of demand for ice-creams in winter...............................................................9

(3) Price elasticity of demand for cigarettes..............................................................................10

Question 4: Types of Costs..................................................................................................................10

(1) Calculation of costs and profit.............................................................................................10

(2) Firm’s operation in short-run...............................................................................................11

(3) Price-taking firm profit maximization..................................................................................11

Question 5: Market Structure...............................................................................................................12

References...........................................................................................................................................14

References...........................................................................................................................................14

Question 1: Production Possibility Curve

(1) Study of Joan’s Production Possibility Curve

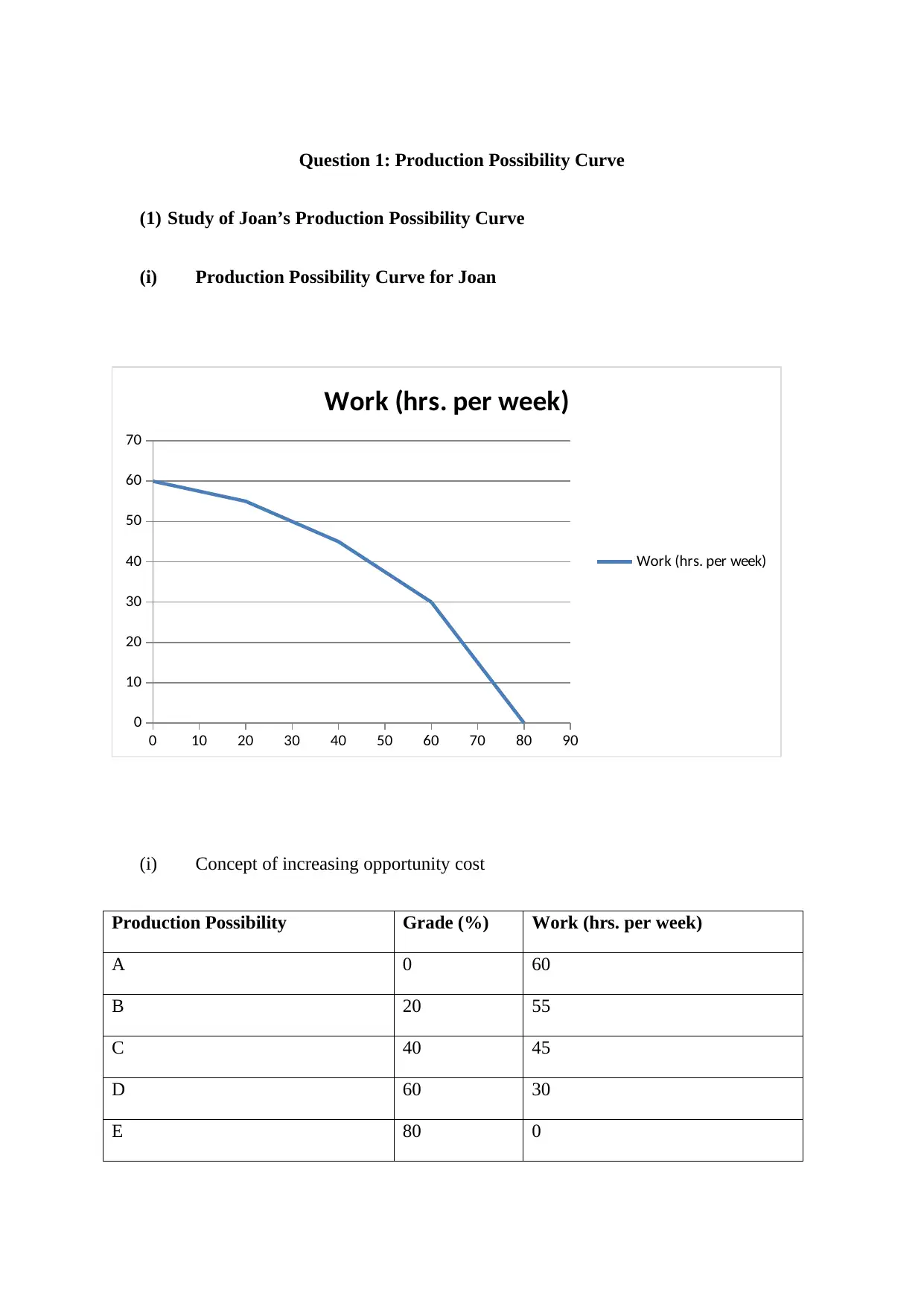

(i) Production Possibility Curve for Joan

0 10 20 30 40 50 60 70 80 90

0

10

20

30

40

50

60

70

Work (hrs. per week)

Work (hrs. per week)

(i) Concept of increasing opportunity cost

Production Possibility Grade (%) Work (hrs. per week)

A 0 60

B 20 55

C 40 45

D 60 30

E 80 0

(1) Study of Joan’s Production Possibility Curve

(i) Production Possibility Curve for Joan

0 10 20 30 40 50 60 70 80 90

0

10

20

30

40

50

60

70

Work (hrs. per week)

Work (hrs. per week)

(i) Concept of increasing opportunity cost

Production Possibility Grade (%) Work (hrs. per week)

A 0 60

B 20 55

C 40 45

D 60 30

E 80 0

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Opportunity cost is said to be the cost of doing one activity in terms of the benefits

forgone from other activity. It occurs because resources are limited in nature and few

activities could be carried out with limited resources. In the problem, Joan has limited

time which is considered her limited resources. She has the option of increasing the

number of working hours for earning money or she can invest the time in studying to

improve her grades.

The concept of increasing opportunity cost states that when the production possibility

is increased for one item or activity the opportunity cost of producing an additional item

will also increase (Lugert, Thaller, Tetens, Schulz, & Krieter, 2016). This happens

because for every other production possibility of one item the cost of another item will be

more for the producer. Here, if Joan increases her working hours then the cost of

decreasing grades will also increase for her. This is why; production possibility curve is

used to determine all the possible combination of the activities or items that can be

carried on with the limited resources available with the producer.

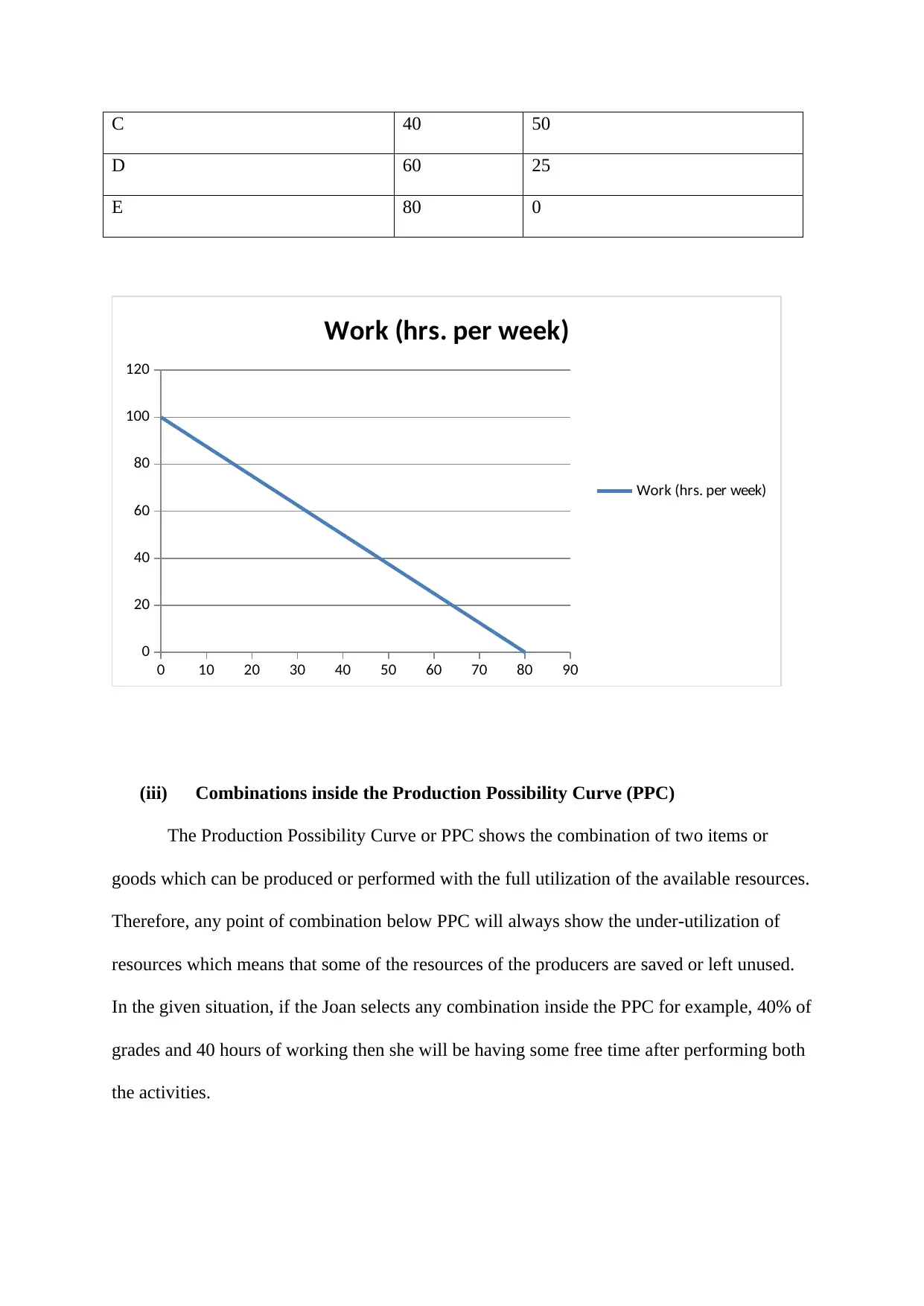

(ii) Production Possibility Curve if opportunity cost was constant

It is assumed that every 25 hours of working has an opportunity cost of 20% of Joan's

grade. The maximum working hours in a week are 100 hours and the maximum grades are

80% which can be achieved by investing the full time of Joan in a single activity. It is to be

noted that when the opportunity cost is constant then the production possibility curve would

be a straight line. In this scenario, the production possibility table and production possibility

curve for Joan would be as follow:

Production Possibility Grade (%) Work (hrs. per week)

A 0 100

B 20 75

forgone from other activity. It occurs because resources are limited in nature and few

activities could be carried out with limited resources. In the problem, Joan has limited

time which is considered her limited resources. She has the option of increasing the

number of working hours for earning money or she can invest the time in studying to

improve her grades.

The concept of increasing opportunity cost states that when the production possibility

is increased for one item or activity the opportunity cost of producing an additional item

will also increase (Lugert, Thaller, Tetens, Schulz, & Krieter, 2016). This happens

because for every other production possibility of one item the cost of another item will be

more for the producer. Here, if Joan increases her working hours then the cost of

decreasing grades will also increase for her. This is why; production possibility curve is

used to determine all the possible combination of the activities or items that can be

carried on with the limited resources available with the producer.

(ii) Production Possibility Curve if opportunity cost was constant

It is assumed that every 25 hours of working has an opportunity cost of 20% of Joan's

grade. The maximum working hours in a week are 100 hours and the maximum grades are

80% which can be achieved by investing the full time of Joan in a single activity. It is to be

noted that when the opportunity cost is constant then the production possibility curve would

be a straight line. In this scenario, the production possibility table and production possibility

curve for Joan would be as follow:

Production Possibility Grade (%) Work (hrs. per week)

A 0 100

B 20 75

C 40 50

D 60 25

E 80 0

0 10 20 30 40 50 60 70 80 90

0

20

40

60

80

100

120

Work (hrs. per week)

Work (hrs. per week)

(iii) Combinations inside the Production Possibility Curve (PPC)

The Production Possibility Curve or PPC shows the combination of two items or

goods which can be produced or performed with the full utilization of the available resources.

Therefore, any point of combination below PPC will always show the under-utilization of

resources which means that some of the resources of the producers are saved or left unused.

In the given situation, if the Joan selects any combination inside the PPC for example, 40% of

grades and 40 hours of working then she will be having some free time after performing both

the activities.

D 60 25

E 80 0

0 10 20 30 40 50 60 70 80 90

0

20

40

60

80

100

120

Work (hrs. per week)

Work (hrs. per week)

(iii) Combinations inside the Production Possibility Curve (PPC)

The Production Possibility Curve or PPC shows the combination of two items or

goods which can be produced or performed with the full utilization of the available resources.

Therefore, any point of combination below PPC will always show the under-utilization of

resources which means that some of the resources of the producers are saved or left unused.

In the given situation, if the Joan selects any combination inside the PPC for example, 40% of

grades and 40 hours of working then she will be having some free time after performing both

the activities.

0 10 20 30 40 50 60 70 80 90

0

10

20

30

40

50

60

70

Work (hrs. per week)

Work (hrs. per week)

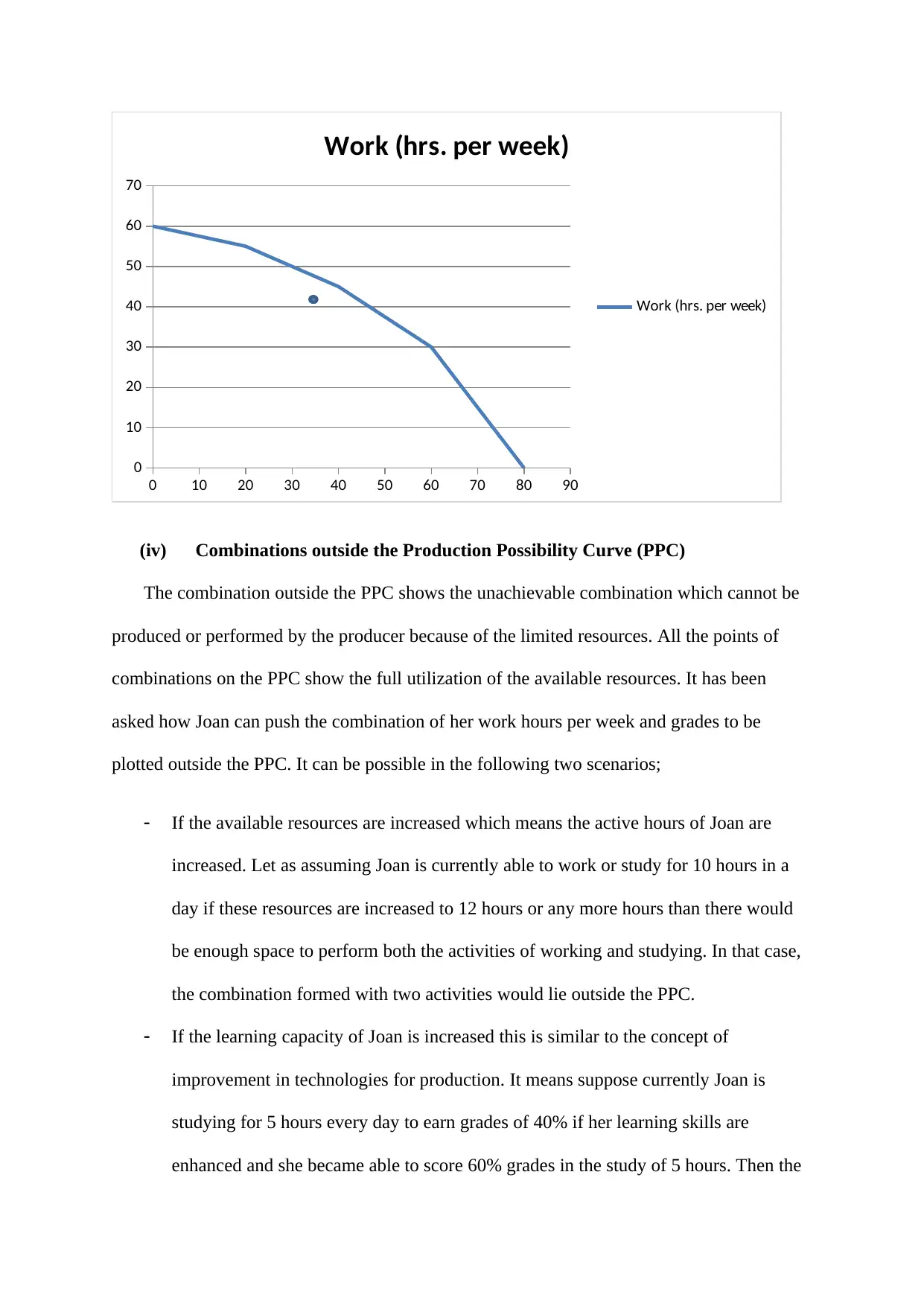

(iv) Combinations outside the Production Possibility Curve (PPC)

The combination outside the PPC shows the unachievable combination which cannot be

produced or performed by the producer because of the limited resources. All the points of

combinations on the PPC show the full utilization of the available resources. It has been

asked how Joan can push the combination of her work hours per week and grades to be

plotted outside the PPC. It can be possible in the following two scenarios;

If the available resources are increased which means the active hours of Joan are

increased. Let as assuming Joan is currently able to work or study for 10 hours in a

day if these resources are increased to 12 hours or any more hours than there would

be enough space to perform both the activities of working and studying. In that case,

the combination formed with two activities would lie outside the PPC.

If the learning capacity of Joan is increased this is similar to the concept of

improvement in technologies for production. It means suppose currently Joan is

studying for 5 hours every day to earn grades of 40% if her learning skills are

enhanced and she became able to score 60% grades in the study of 5 hours. Then the

0

10

20

30

40

50

60

70

Work (hrs. per week)

Work (hrs. per week)

(iv) Combinations outside the Production Possibility Curve (PPC)

The combination outside the PPC shows the unachievable combination which cannot be

produced or performed by the producer because of the limited resources. All the points of

combinations on the PPC show the full utilization of the available resources. It has been

asked how Joan can push the combination of her work hours per week and grades to be

plotted outside the PPC. It can be possible in the following two scenarios;

If the available resources are increased which means the active hours of Joan are

increased. Let as assuming Joan is currently able to work or study for 10 hours in a

day if these resources are increased to 12 hours or any more hours than there would

be enough space to perform both the activities of working and studying. In that case,

the combination formed with two activities would lie outside the PPC.

If the learning capacity of Joan is increased this is similar to the concept of

improvement in technologies for production. It means suppose currently Joan is

studying for 5 hours every day to earn grades of 40% if her learning skills are

enhanced and she became able to score 60% grades in the study of 5 hours. Then the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

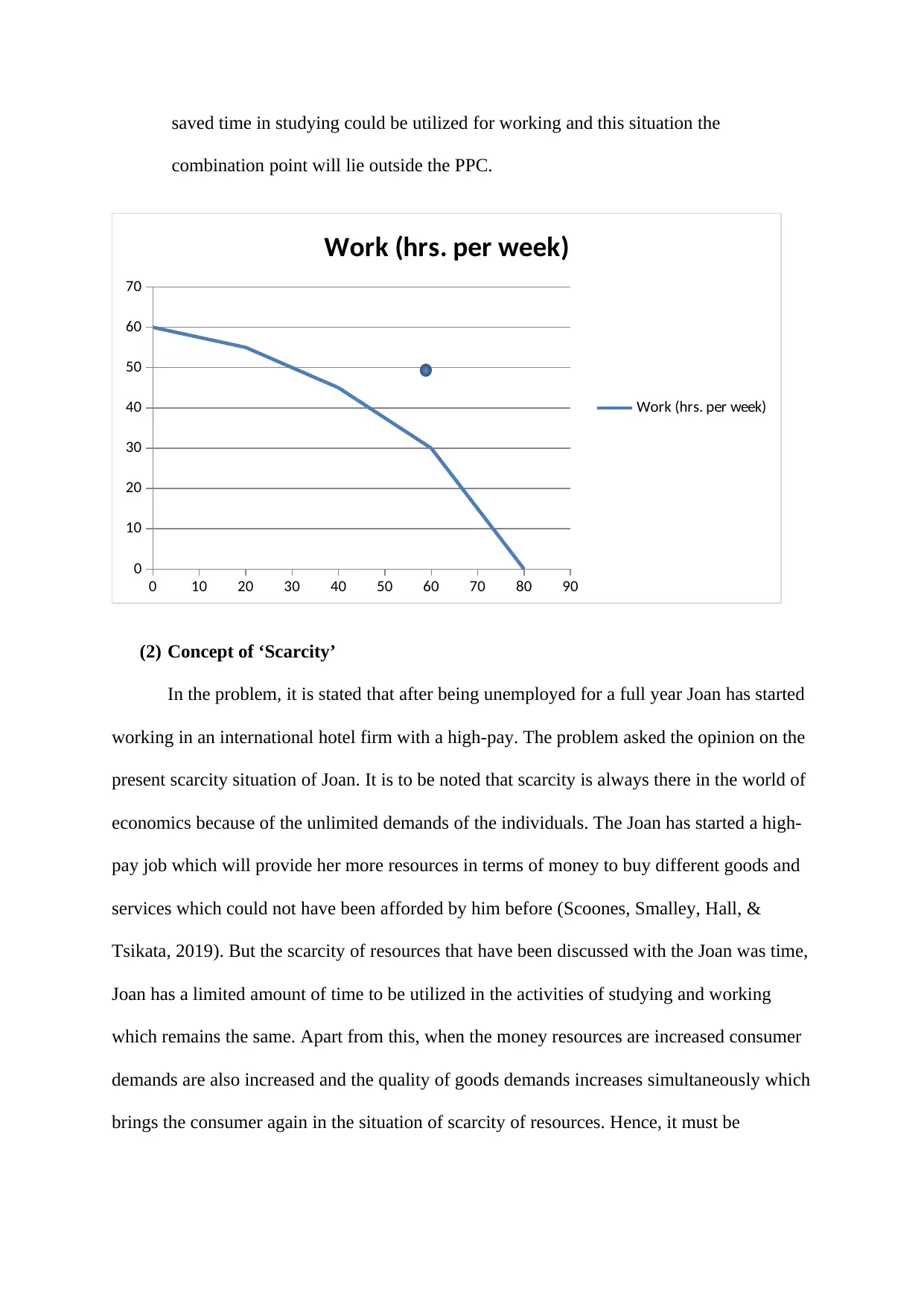

saved time in studying could be utilized for working and this situation the

combination point will lie outside the PPC.

0 10 20 30 40 50 60 70 80 90

0

10

20

30

40

50

60

70

Work (hrs. per week)

Work (hrs. per week)

(2) Concept of ‘Scarcity’

In the problem, it is stated that after being unemployed for a full year Joan has started

working in an international hotel firm with a high-pay. The problem asked the opinion on the

present scarcity situation of Joan. It is to be noted that scarcity is always there in the world of

economics because of the unlimited demands of the individuals. The Joan has started a high-

pay job which will provide her more resources in terms of money to buy different goods and

services which could not have been afforded by him before (Scoones, Smalley, Hall, &

Tsikata, 2019). But the scarcity of resources that have been discussed with the Joan was time,

Joan has a limited amount of time to be utilized in the activities of studying and working

which remains the same. Apart from this, when the money resources are increased consumer

demands are also increased and the quality of goods demands increases simultaneously which

brings the consumer again in the situation of scarcity of resources. Hence, it must be

combination point will lie outside the PPC.

0 10 20 30 40 50 60 70 80 90

0

10

20

30

40

50

60

70

Work (hrs. per week)

Work (hrs. per week)

(2) Concept of ‘Scarcity’

In the problem, it is stated that after being unemployed for a full year Joan has started

working in an international hotel firm with a high-pay. The problem asked the opinion on the

present scarcity situation of Joan. It is to be noted that scarcity is always there in the world of

economics because of the unlimited demands of the individuals. The Joan has started a high-

pay job which will provide her more resources in terms of money to buy different goods and

services which could not have been afforded by him before (Scoones, Smalley, Hall, &

Tsikata, 2019). But the scarcity of resources that have been discussed with the Joan was time,

Joan has a limited amount of time to be utilized in the activities of studying and working

which remains the same. Apart from this, when the money resources are increased consumer

demands are also increased and the quality of goods demands increases simultaneously which

brings the consumer again in the situation of scarcity of resources. Hence, it must be

understood that Joan can increase her standard of living or can buy more goods than before

but the problem of scarcity will always be there in the economic world.

Question 2: Demand and Supply

(1) Improvement in technology

(i) Effect on the equilibrium price and quantity of solar-powered motor vehicle

The improvement in the manufacturing technology of the solar power motor vehicle

will reduce the cost of production of these vehicles. The reduction in the production cost will

reduce the selling price of the item which will impact the demand for the product (Igos,

Rugani, Rege, Benetto, Drouet, & Zachary, 2015). The law of demand states that when the

price of the good is decreased its demanded quantity will increase. Hence, the equilibrium

price of the vehicle will decrease and the equilibrium quantity will increase.

(ii) Effect on the equilibrium price and quantity of conventional motor vehicle

It is a problem related to the impact on the substitute goods. The conventional motor

vehicle can be used in place of solar motor vehicles. When the price of substitute goods

decreases the demand for the original goods also decreases because the consumers shift to

substitute goods. Here, the demand for the conventional motor vehicle will decrease and the

equilibrium price will adjust accordingly.

(2) Impact of the price ceiling

To promote the industry of solar motor vehicle the government sets the price of the

vehicle lower than its equilibrium market price. In such a case, when the government ceils the

price of any product below the equilibrium price it brings disturbance in the equilibrium. The

quantity demanded that product increases and the supply remains constant; therefore, the

quantity demanded will exceed the supplied quantity for that product (Perkis, Cason, &

but the problem of scarcity will always be there in the economic world.

Question 2: Demand and Supply

(1) Improvement in technology

(i) Effect on the equilibrium price and quantity of solar-powered motor vehicle

The improvement in the manufacturing technology of the solar power motor vehicle

will reduce the cost of production of these vehicles. The reduction in the production cost will

reduce the selling price of the item which will impact the demand for the product (Igos,

Rugani, Rege, Benetto, Drouet, & Zachary, 2015). The law of demand states that when the

price of the good is decreased its demanded quantity will increase. Hence, the equilibrium

price of the vehicle will decrease and the equilibrium quantity will increase.

(ii) Effect on the equilibrium price and quantity of conventional motor vehicle

It is a problem related to the impact on the substitute goods. The conventional motor

vehicle can be used in place of solar motor vehicles. When the price of substitute goods

decreases the demand for the original goods also decreases because the consumers shift to

substitute goods. Here, the demand for the conventional motor vehicle will decrease and the

equilibrium price will adjust accordingly.

(2) Impact of the price ceiling

To promote the industry of solar motor vehicle the government sets the price of the

vehicle lower than its equilibrium market price. In such a case, when the government ceils the

price of any product below the equilibrium price it brings disturbance in the equilibrium. The

quantity demanded that product increases and the supply remains constant; therefore, the

quantity demanded will exceed the supplied quantity for that product (Perkis, Cason, &

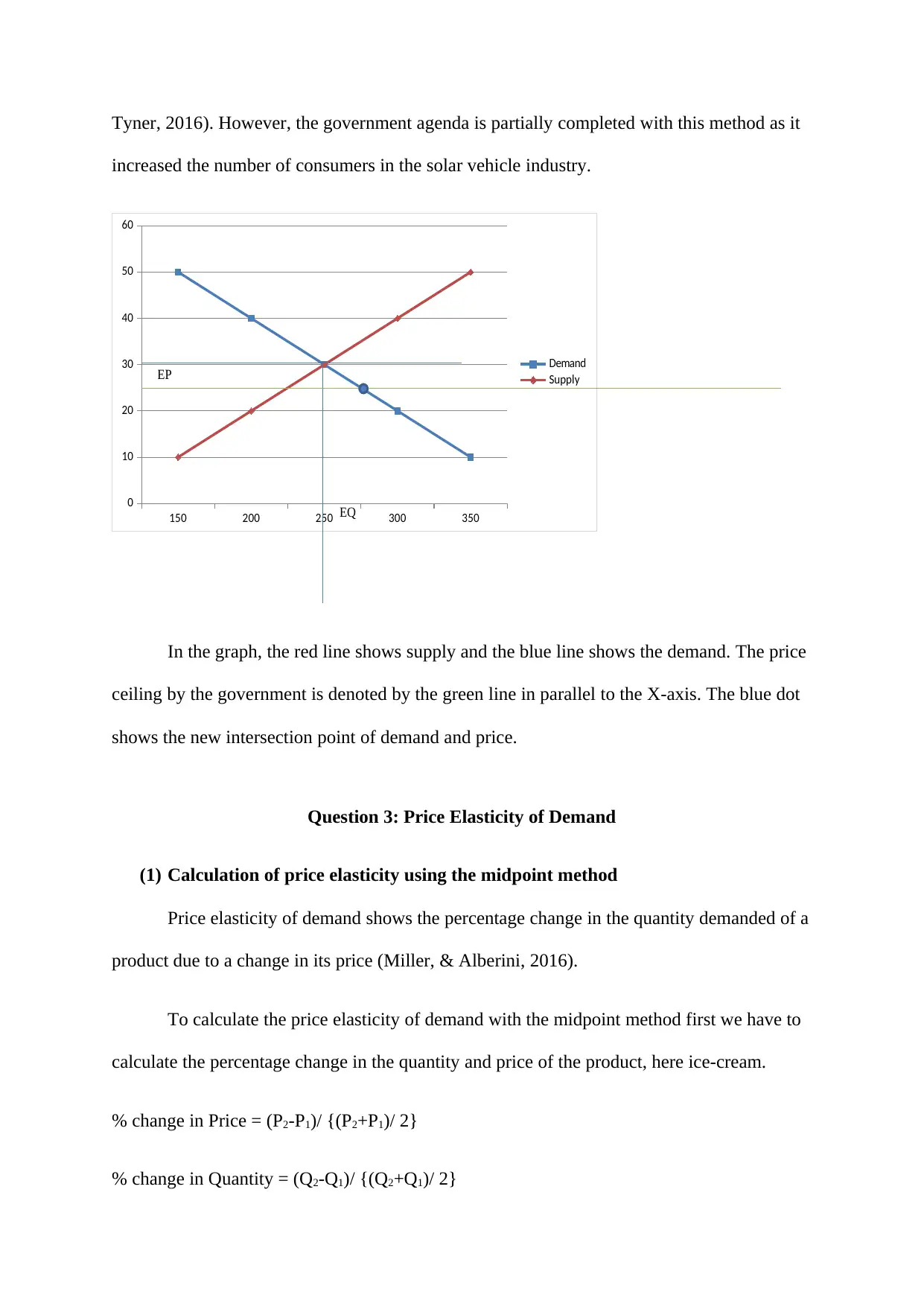

Tyner, 2016). However, the government agenda is partially completed with this method as it

increased the number of consumers in the solar vehicle industry.

150 200 250 300 350

0

10

20

30

40

50

60

Demand

Supply

EQ

EP

In the graph, the red line shows supply and the blue line shows the demand. The price

ceiling by the government is denoted by the green line in parallel to the X-axis. The blue dot

shows the new intersection point of demand and price.

Question 3: Price Elasticity of Demand

(1) Calculation of price elasticity using the midpoint method

Price elasticity of demand shows the percentage change in the quantity demanded of a

product due to a change in its price (Miller, & Alberini, 2016).

To calculate the price elasticity of demand with the midpoint method first we have to

calculate the percentage change in the quantity and price of the product, here ice-cream.

% change in Price = (P2-P1)/ {(P2+P1)/ 2}

% change in Quantity = (Q2-Q1)/ {(Q2+Q1)/ 2}

increased the number of consumers in the solar vehicle industry.

150 200 250 300 350

0

10

20

30

40

50

60

Demand

Supply

EQ

EP

In the graph, the red line shows supply and the blue line shows the demand. The price

ceiling by the government is denoted by the green line in parallel to the X-axis. The blue dot

shows the new intersection point of demand and price.

Question 3: Price Elasticity of Demand

(1) Calculation of price elasticity using the midpoint method

Price elasticity of demand shows the percentage change in the quantity demanded of a

product due to a change in its price (Miller, & Alberini, 2016).

To calculate the price elasticity of demand with the midpoint method first we have to

calculate the percentage change in the quantity and price of the product, here ice-cream.

% change in Price = (P2-P1)/ {(P2+P1)/ 2}

% change in Quantity = (Q2-Q1)/ {(Q2+Q1)/ 2}

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

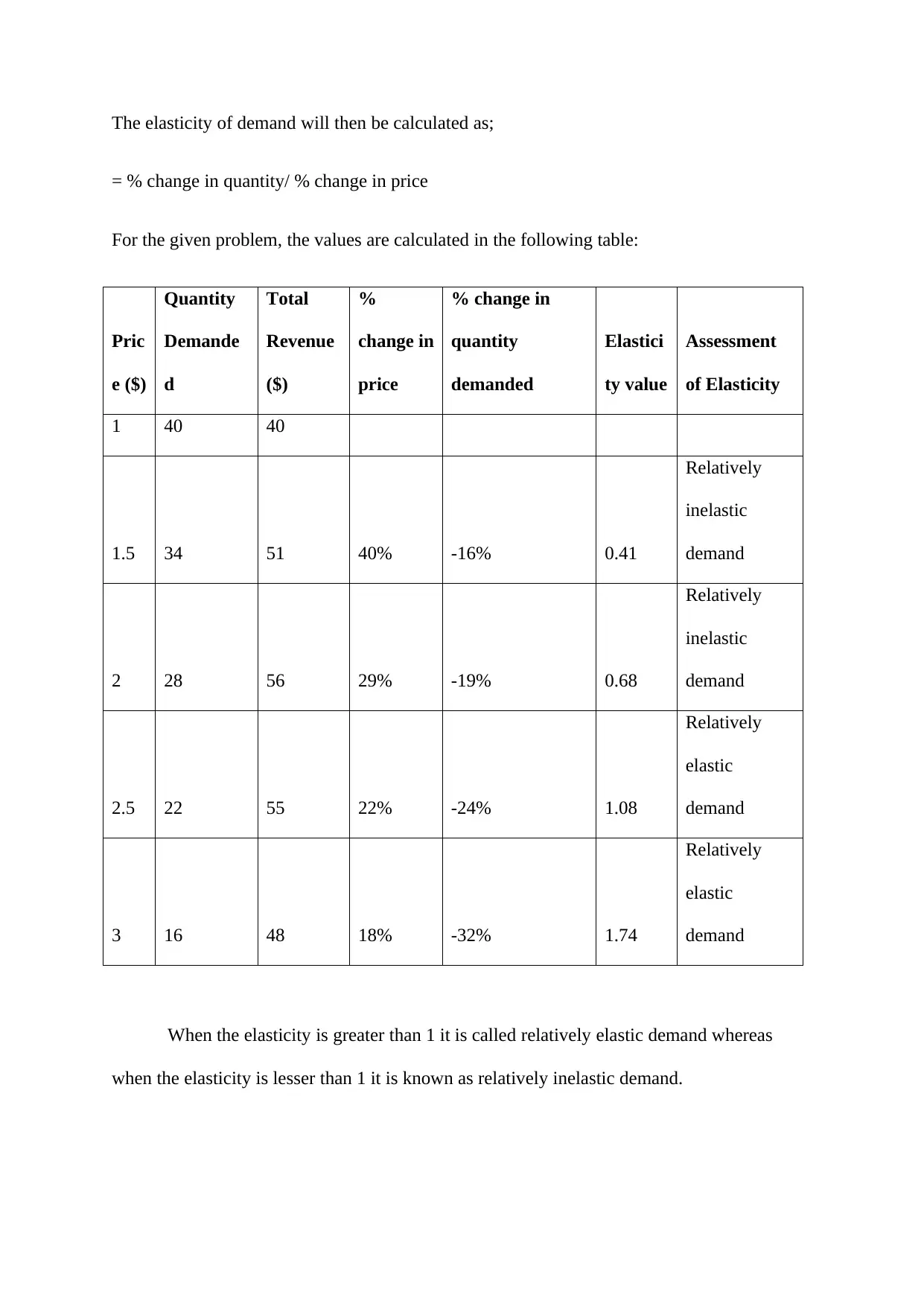

The elasticity of demand will then be calculated as;

= % change in quantity/ % change in price

For the given problem, the values are calculated in the following table:

Pric

e ($)

Quantity

Demande

d

Total

Revenue

($)

%

change in

price

% change in

quantity

demanded

Elastici

ty value

Assessment

of Elasticity

1 40 40

1.5 34 51 40% -16% 0.41

Relatively

inelastic

demand

2 28 56 29% -19% 0.68

Relatively

inelastic

demand

2.5 22 55 22% -24% 1.08

Relatively

elastic

demand

3 16 48 18% -32% 1.74

Relatively

elastic

demand

When the elasticity is greater than 1 it is called relatively elastic demand whereas

when the elasticity is lesser than 1 it is known as relatively inelastic demand.

= % change in quantity/ % change in price

For the given problem, the values are calculated in the following table:

Pric

e ($)

Quantity

Demande

d

Total

Revenue

($)

%

change in

price

% change in

quantity

demanded

Elastici

ty value

Assessment

of Elasticity

1 40 40

1.5 34 51 40% -16% 0.41

Relatively

inelastic

demand

2 28 56 29% -19% 0.68

Relatively

inelastic

demand

2.5 22 55 22% -24% 1.08

Relatively

elastic

demand

3 16 48 18% -32% 1.74

Relatively

elastic

demand

When the elasticity is greater than 1 it is called relatively elastic demand whereas

when the elasticity is lesser than 1 it is known as relatively inelastic demand.

(2) Price elasticity of demand for ice-creams in winter

The price elasticity of demand for the ice-creams will be relatively inelastic in winter

because in the winter the weather is already very cool and in such weather the demand for

ice-cream is low. However, the ice-creams are sold in winter in low quantity and such

demand will not be much affected by the changes in prices as seen in the summers.

Therefore, the demand will be relatively inelastic in winters.

(3) Price elasticity of demand for cigarettes

Cigarettes are the items that are put in the categories of addictive items and the

elasticity of such items are assumed to be inelastic or relatively inelastic (Jawad, Lee, Glantz,

& Millett, 2018). The tobacco products are assumed to have an elasticity of demand lesser

than one or inelastic which its demand will have a little or no impact on the price change of

the items.

Question 4: Types of Costs

(1) Calculation of costs and profit

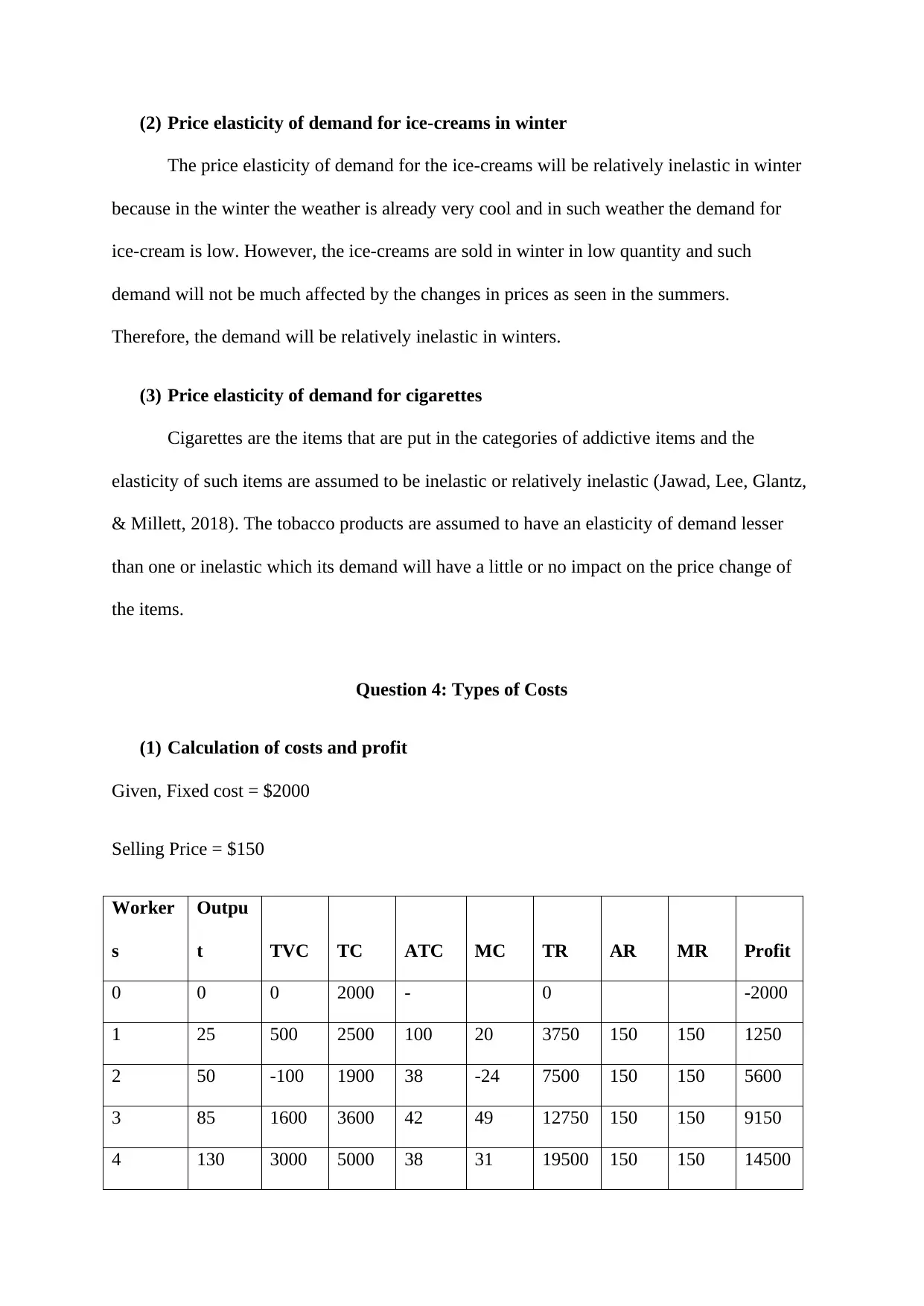

Given, Fixed cost = $2000

Selling Price = $150

Worker

s

Outpu

t TVC TC ATC MC TR AR MR Profit

0 0 0 2000 - 0 -2000

1 25 500 2500 100 20 3750 150 150 1250

2 50 -100 1900 38 -24 7500 150 150 5600

3 85 1600 3600 42 49 12750 150 150 9150

4 130 3000 5000 38 31 19500 150 150 14500

The price elasticity of demand for the ice-creams will be relatively inelastic in winter

because in the winter the weather is already very cool and in such weather the demand for

ice-cream is low. However, the ice-creams are sold in winter in low quantity and such

demand will not be much affected by the changes in prices as seen in the summers.

Therefore, the demand will be relatively inelastic in winters.

(3) Price elasticity of demand for cigarettes

Cigarettes are the items that are put in the categories of addictive items and the

elasticity of such items are assumed to be inelastic or relatively inelastic (Jawad, Lee, Glantz,

& Millett, 2018). The tobacco products are assumed to have an elasticity of demand lesser

than one or inelastic which its demand will have a little or no impact on the price change of

the items.

Question 4: Types of Costs

(1) Calculation of costs and profit

Given, Fixed cost = $2000

Selling Price = $150

Worker

s

Outpu

t TVC TC ATC MC TR AR MR Profit

0 0 0 2000 - 0 -2000

1 25 500 2500 100 20 3750 150 150 1250

2 50 -100 1900 38 -24 7500 150 150 5600

3 85 1600 3600 42 49 12750 150 150 9150

4 130 3000 5000 38 31 19500 150 150 14500

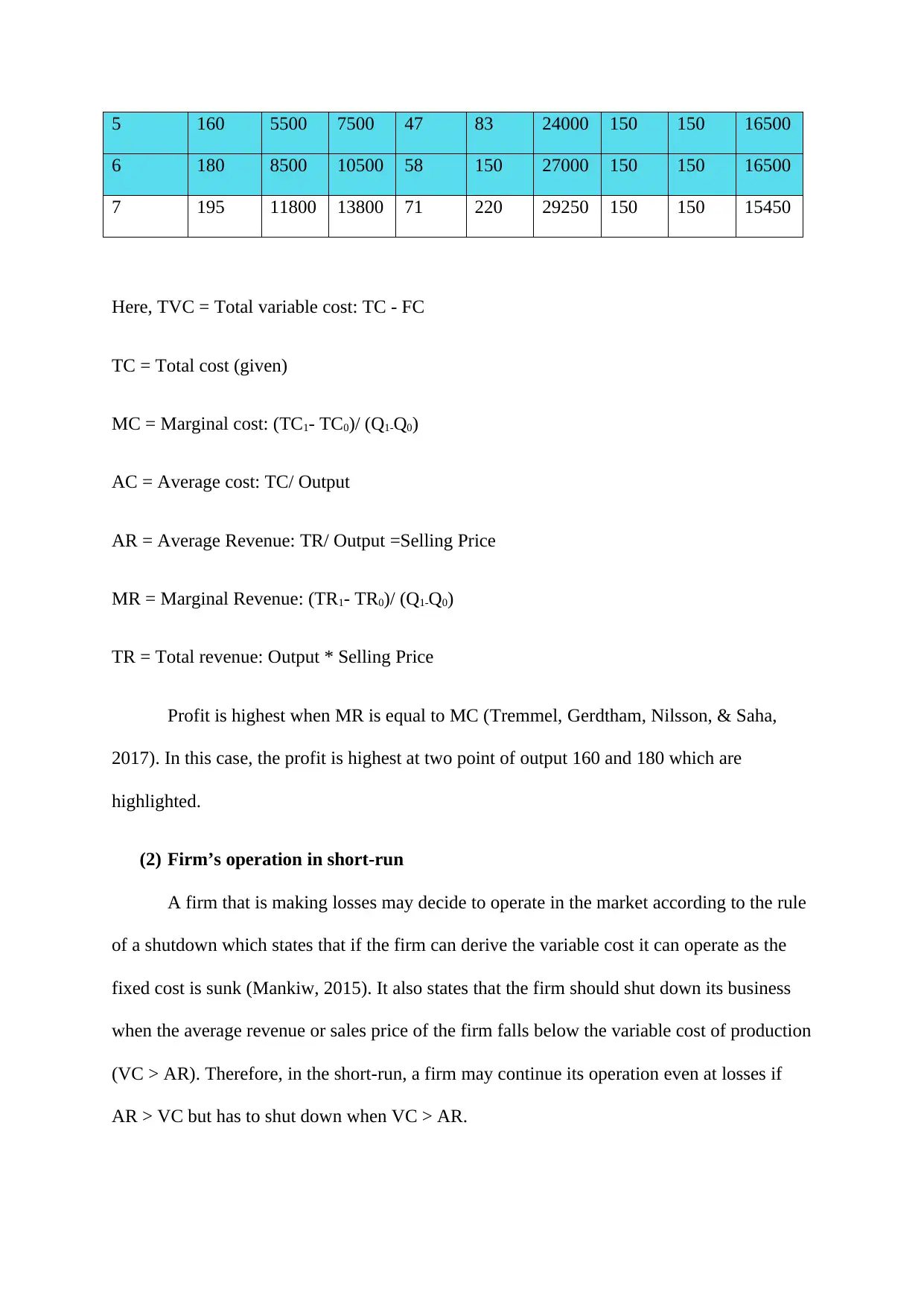

5 160 5500 7500 47 83 24000 150 150 16500

6 180 8500 10500 58 150 27000 150 150 16500

7 195 11800 13800 71 220 29250 150 150 15450

Here, TVC = Total variable cost: TC - FC

TC = Total cost (given)

MC = Marginal cost: (TC1- TC0)/ (Q1-Q0)

AC = Average cost: TC/ Output

AR = Average Revenue: TR/ Output =Selling Price

MR = Marginal Revenue: (TR1- TR0)/ (Q1-Q0)

TR = Total revenue: Output * Selling Price

Profit is highest when MR is equal to MC (Tremmel, Gerdtham, Nilsson, & Saha,

2017). In this case, the profit is highest at two point of output 160 and 180 which are

highlighted.

(2) Firm’s operation in short-run

A firm that is making losses may decide to operate in the market according to the rule

of a shutdown which states that if the firm can derive the variable cost it can operate as the

fixed cost is sunk (Mankiw, 2015). It also states that the firm should shut down its business

when the average revenue or sales price of the firm falls below the variable cost of production

(VC > AR). Therefore, in the short-run, a firm may continue its operation even at losses if

AR > VC but has to shut down when VC > AR.

6 180 8500 10500 58 150 27000 150 150 16500

7 195 11800 13800 71 220 29250 150 150 15450

Here, TVC = Total variable cost: TC - FC

TC = Total cost (given)

MC = Marginal cost: (TC1- TC0)/ (Q1-Q0)

AC = Average cost: TC/ Output

AR = Average Revenue: TR/ Output =Selling Price

MR = Marginal Revenue: (TR1- TR0)/ (Q1-Q0)

TR = Total revenue: Output * Selling Price

Profit is highest when MR is equal to MC (Tremmel, Gerdtham, Nilsson, & Saha,

2017). In this case, the profit is highest at two point of output 160 and 180 which are

highlighted.

(2) Firm’s operation in short-run

A firm that is making losses may decide to operate in the market according to the rule

of a shutdown which states that if the firm can derive the variable cost it can operate as the

fixed cost is sunk (Mankiw, 2015). It also states that the firm should shut down its business

when the average revenue or sales price of the firm falls below the variable cost of production

(VC > AR). Therefore, in the short-run, a firm may continue its operation even at losses if

AR > VC but has to shut down when VC > AR.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(3) Price-taking firm profit maximization

A price-taking firm is the one which has to accept the market price as its selling price

while operating in the market. These firms determine their profit maximization by the firm's

optimal output rule (Wong, 2015). This rule states that the firm will earn a maximum profit

when the marginal cost of the goods is equal to the market price of the product. Hence profit

is maximized when AR= MC or MC =MR.

Question 5: Market Structure

A Monopoly market structure is the market structure in which there is a single seller

of the product who has full control over the prices of the product because of high demand

(Weller, Kleer, & Piller, 2015). On the other hand, the perfect competition market is the one

where there is a large number of sellers and buyers (Simatele, 2015). In the perfect

competition market, the seller is a price taker from the market and not the price maker.

The Australian banking industry is operating in an Oligopoly market structure where

there are very few large firms that collectively excise control on the market share. The

Australian banking industry is said to be closer to the monopoly market because monopoly

comes into existence when there is a low number of sellers or producers. This happens

because of the restrictions on the entry of new firms in the industry. The banking industry is a

type of industry that requires a huge investment to begin. The Australian banking industry

presently has very few numbers of banks (Sheedy, & Griffin, 2018). Also, the restrictions on

the entry of the because of large investment pushes the industry to the monopoly structure.

It is understood that the customers are always benefitted in the perfect competition

market as in this market the prices are fixed with the market demand and supply equilibrium

and the firms have to accept the market price as selling price of their product. However, in

the monopoly market structure, the firm is the price maker and it sells is goods or services at

A price-taking firm is the one which has to accept the market price as its selling price

while operating in the market. These firms determine their profit maximization by the firm's

optimal output rule (Wong, 2015). This rule states that the firm will earn a maximum profit

when the marginal cost of the goods is equal to the market price of the product. Hence profit

is maximized when AR= MC or MC =MR.

Question 5: Market Structure

A Monopoly market structure is the market structure in which there is a single seller

of the product who has full control over the prices of the product because of high demand

(Weller, Kleer, & Piller, 2015). On the other hand, the perfect competition market is the one

where there is a large number of sellers and buyers (Simatele, 2015). In the perfect

competition market, the seller is a price taker from the market and not the price maker.

The Australian banking industry is operating in an Oligopoly market structure where

there are very few large firms that collectively excise control on the market share. The

Australian banking industry is said to be closer to the monopoly market because monopoly

comes into existence when there is a low number of sellers or producers. This happens

because of the restrictions on the entry of new firms in the industry. The banking industry is a

type of industry that requires a huge investment to begin. The Australian banking industry

presently has very few numbers of banks (Sheedy, & Griffin, 2018). Also, the restrictions on

the entry of the because of large investment pushes the industry to the monopoly structure.

It is understood that the customers are always benefitted in the perfect competition

market as in this market the prices are fixed with the market demand and supply equilibrium

and the firms have to accept the market price as selling price of their product. However, in

the monopoly market structure, the firm is the price maker and it sells is goods or services at

the prices which are beneficial to their business. In such a situation, the inclination of the

banking industry towards the monopoly structure is against the public interest.

Apart from this banking industry, the Australian post already holds the monopoly in

the market of Australia.

banking industry towards the monopoly structure is against the public interest.

Apart from this banking industry, the Australian post already holds the monopoly in

the market of Australia.

References

Igos, E., Rugani, B., Rege, S., Benetto, E., Drouet, L., & Zachary, D. S. (2015). Combination

of equilibrium models and hybrid life cycle-input–output analysis to predict the

environmental impacts of energy policy scenarios. Applied energy, 145, 234-245.

Jawad, M., Lee, J. T., Glantz, S., & Millett, C. (2018). Price elasticity of demand of non-

cigarette tobacco products: a systematic review and meta-analysis. Tobacco

control, 27(6), 689-695.

Lugert, V., Thaller, G., Tetens, J., Schulz, C., & Krieter, J. (2016). A review on fish growth

calculation: multiple functions in fish production and their specific

application. Reviews in Aquaculture, 8(1), 30-42.

Mankiw, N. G. (2015). Firms in competitive markets. Principles of economics, 279-298.).

Firms in competitive markets. Principles of economics, 279-298.

Miller, M., & Alberini, A. (2016). Sensitivity of price elasticity of demand to aggregation,

unobserved heterogeneity, price trends, and price endogeneity: Evidence from US

Data. Energy Policy, 97, 235-249.

Perkis, D. F., Cason, T. N., & Tyner, W. E. (2016). An experimental investigation of hard

and soft price ceilings in emissions permit markets. Environmental and Resource

Economics, 63(4), 703-718.

Scoones, I., Smalley, R., Hall, R., & Tsikata, D. (2019). Narratives of scarcity: Framing the

global land rush. Geoforum, 101, 231-241.

Sheedy, E., & Griffin, B. (2018). Risk governance, structures, culture, and behavior: A view

from the inside. Corporate Governance: An International Review, 26(1), 4-22.

Igos, E., Rugani, B., Rege, S., Benetto, E., Drouet, L., & Zachary, D. S. (2015). Combination

of equilibrium models and hybrid life cycle-input–output analysis to predict the

environmental impacts of energy policy scenarios. Applied energy, 145, 234-245.

Jawad, M., Lee, J. T., Glantz, S., & Millett, C. (2018). Price elasticity of demand of non-

cigarette tobacco products: a systematic review and meta-analysis. Tobacco

control, 27(6), 689-695.

Lugert, V., Thaller, G., Tetens, J., Schulz, C., & Krieter, J. (2016). A review on fish growth

calculation: multiple functions in fish production and their specific

application. Reviews in Aquaculture, 8(1), 30-42.

Mankiw, N. G. (2015). Firms in competitive markets. Principles of economics, 279-298.).

Firms in competitive markets. Principles of economics, 279-298.

Miller, M., & Alberini, A. (2016). Sensitivity of price elasticity of demand to aggregation,

unobserved heterogeneity, price trends, and price endogeneity: Evidence from US

Data. Energy Policy, 97, 235-249.

Perkis, D. F., Cason, T. N., & Tyner, W. E. (2016). An experimental investigation of hard

and soft price ceilings in emissions permit markets. Environmental and Resource

Economics, 63(4), 703-718.

Scoones, I., Smalley, R., Hall, R., & Tsikata, D. (2019). Narratives of scarcity: Framing the

global land rush. Geoforum, 101, 231-241.

Sheedy, E., & Griffin, B. (2018). Risk governance, structures, culture, and behavior: A view

from the inside. Corporate Governance: An International Review, 26(1), 4-22.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Simatele, M. (2015). Market Structure and competition in the South African banking

sector. Procedia Economics and Finance, 30, 825-835.

Tremmel, M., Gerdtham, U. G., Nilsson, P., & Saha, S. (2017). Economic burden of obesity:

a systematic literature review. International journal of environmental research and

public health, 14(4), 435.

Weller, C., Kleer, R., & Piller, F. T. (2015). Economic implications of 3D printing: Market

structure models in light of additive manufacturing revisited. International Journal of

Production Economics, 164, 43-56.

Wong, K. P. (2015). A smooth ambiguity model of the competitive firm. Bulletin of

Economic Research, 67(S1), S97-S110.

sector. Procedia Economics and Finance, 30, 825-835.

Tremmel, M., Gerdtham, U. G., Nilsson, P., & Saha, S. (2017). Economic burden of obesity:

a systematic literature review. International journal of environmental research and

public health, 14(4), 435.

Weller, C., Kleer, R., & Piller, F. T. (2015). Economic implications of 3D printing: Market

structure models in light of additive manufacturing revisited. International Journal of

Production Economics, 164, 43-56.

Wong, K. P. (2015). A smooth ambiguity model of the competitive firm. Bulletin of

Economic Research, 67(S1), S97-S110.

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.