Principles of Economics: Assignment on Economic Concepts

VerifiedAdded on 2022/10/02

|10

|2868

|226

Homework Assignment

AI Summary

This economics assignment addresses four key concepts: elasticity of demand, long-run average cost, economic productivity, and inflation. The first question analyzes price elasticity and its impact on revenue, advising on price adjustments based on elasticities of 1.4, 0.6, and 1. The second question examines the long-run average cost in the automobile industry, considering economies and diseconomies of scale. The third question explores the relationship between economic productivity and GDP per capita growth, comparing high, middle, and low-income economies with examples from Australia, India, and Afghanistan. The final question discusses inflation, focusing on the Consumer Price Index (CPI) and the effects of updating the basket of goods measurement frequency from ten to five years, highlighting the problem of substitution biasness.

Running head: ECONOMICS 1

Principles of Economics

Name

Institution

Principles of Economics

Name

Institution

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ECONOMICS 2

Principles of Economics

Question 1 Solution

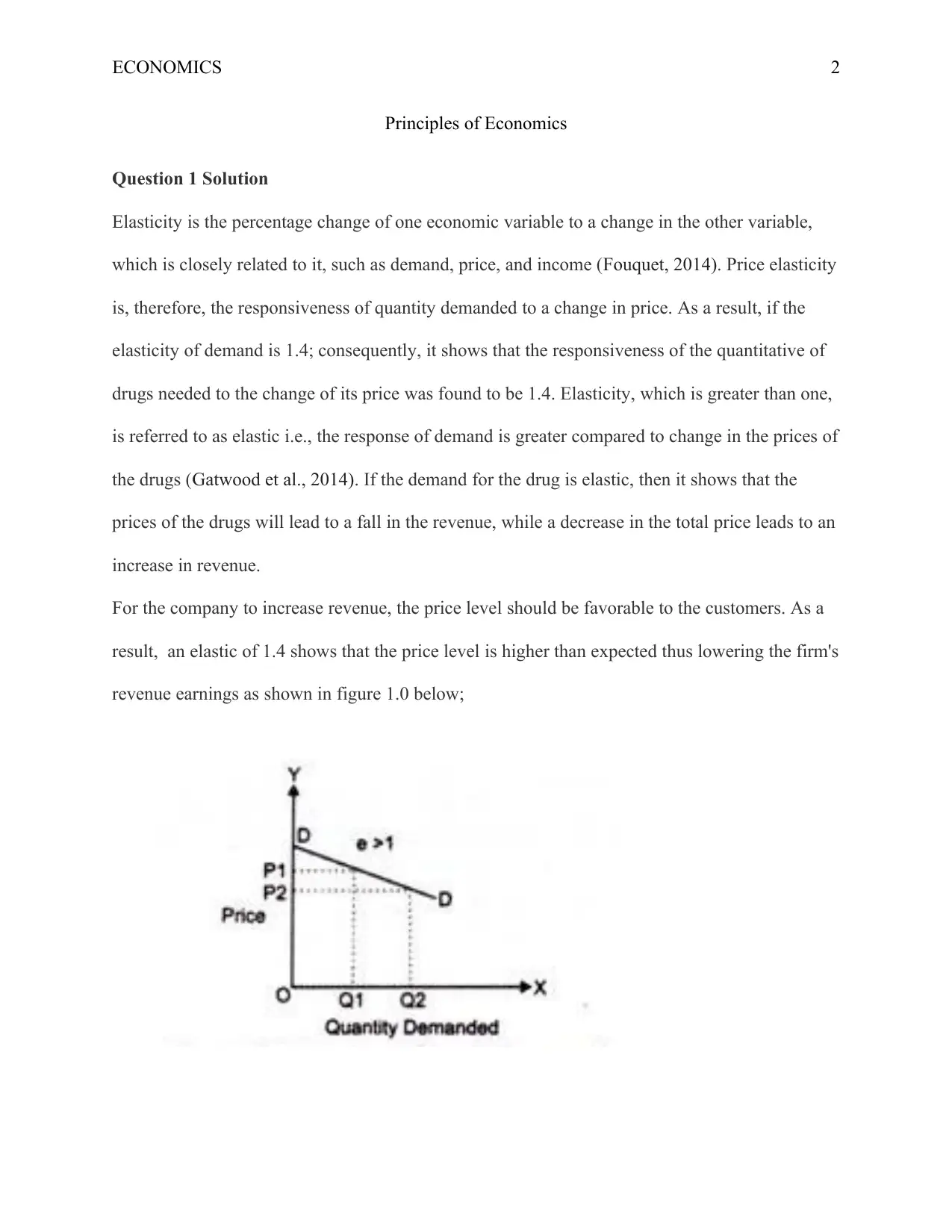

Elasticity is the percentage change of one economic variable to a change in the other variable,

which is closely related to it, such as demand, price, and income (Fouquet, 2014). Price elasticity

is, therefore, the responsiveness of quantity demanded to a change in price. As a result, if the

elasticity of demand is 1.4; consequently, it shows that the responsiveness of the quantitative of

drugs needed to the change of its price was found to be 1.4. Elasticity, which is greater than one,

is referred to as elastic i.e., the response of demand is greater compared to change in the prices of

the drugs (Gatwood et al., 2014). If the demand for the drug is elastic, then it shows that the

prices of the drugs will lead to a fall in the revenue, while a decrease in the total price leads to an

increase in revenue.

For the company to increase revenue, the price level should be favorable to the customers. As a

result, an elastic of 1.4 shows that the price level is higher than expected thus lowering the firm's

revenue earnings as shown in figure 1.0 below;

Principles of Economics

Question 1 Solution

Elasticity is the percentage change of one economic variable to a change in the other variable,

which is closely related to it, such as demand, price, and income (Fouquet, 2014). Price elasticity

is, therefore, the responsiveness of quantity demanded to a change in price. As a result, if the

elasticity of demand is 1.4; consequently, it shows that the responsiveness of the quantitative of

drugs needed to the change of its price was found to be 1.4. Elasticity, which is greater than one,

is referred to as elastic i.e., the response of demand is greater compared to change in the prices of

the drugs (Gatwood et al., 2014). If the demand for the drug is elastic, then it shows that the

prices of the drugs will lead to a fall in the revenue, while a decrease in the total price leads to an

increase in revenue.

For the company to increase revenue, the price level should be favorable to the customers. As a

result, an elastic of 1.4 shows that the price level is higher than expected thus lowering the firm's

revenue earnings as shown in figure 1.0 below;

ECONOMICS 3

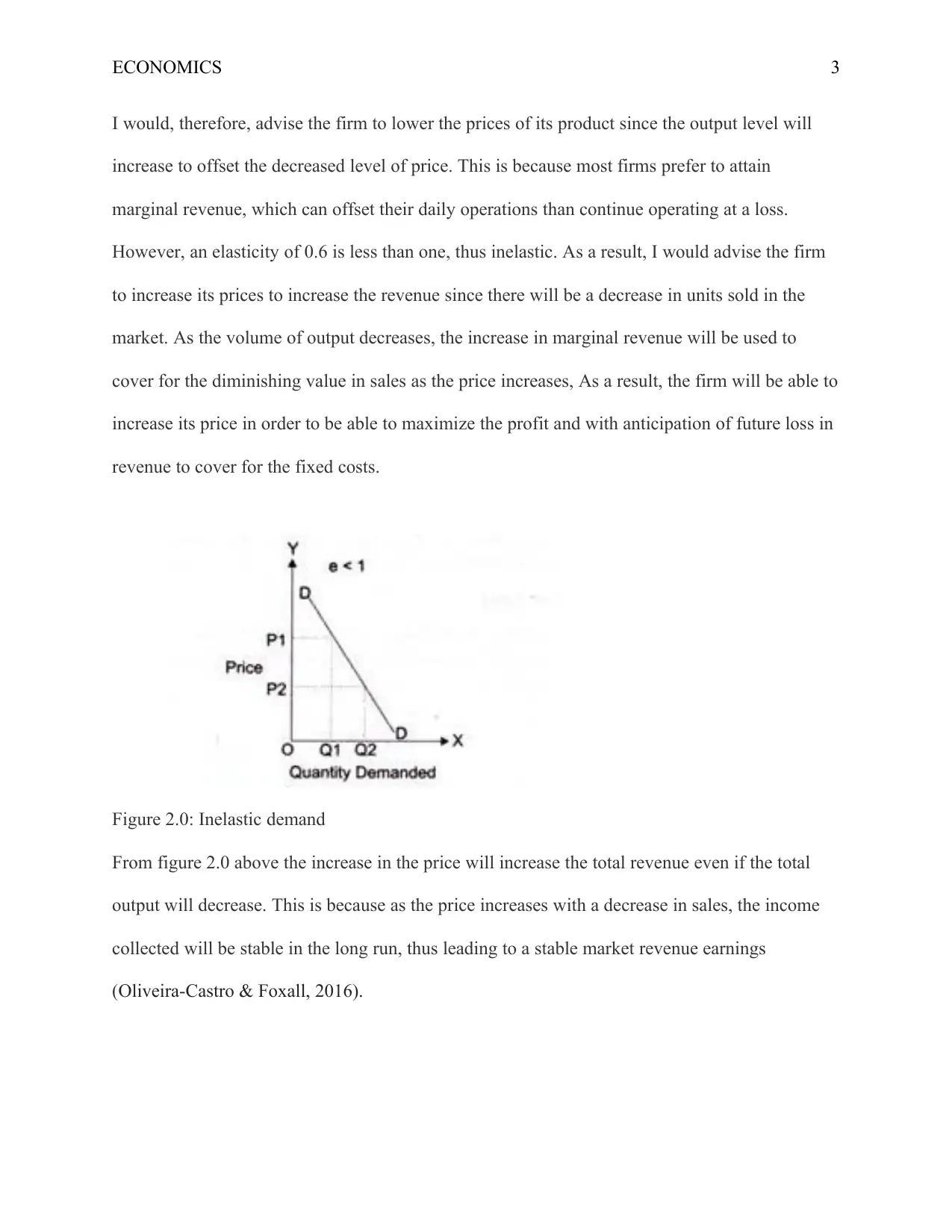

I would, therefore, advise the firm to lower the prices of its product since the output level will

increase to offset the decreased level of price. This is because most firms prefer to attain

marginal revenue, which can offset their daily operations than continue operating at a loss.

However, an elasticity of 0.6 is less than one, thus inelastic. As a result, I would advise the firm

to increase its prices to increase the revenue since there will be a decrease in units sold in the

market. As the volume of output decreases, the increase in marginal revenue will be used to

cover for the diminishing value in sales as the price increases, As a result, the firm will be able to

increase its price in order to be able to maximize the profit and with anticipation of future loss in

revenue to cover for the fixed costs.

Figure 2.0: Inelastic demand

From figure 2.0 above the increase in the price will increase the total revenue even if the total

output will decrease. This is because as the price increases with a decrease in sales, the income

collected will be stable in the long run, thus leading to a stable market revenue earnings

(Oliveira-Castro & Foxall, 2016).

I would, therefore, advise the firm to lower the prices of its product since the output level will

increase to offset the decreased level of price. This is because most firms prefer to attain

marginal revenue, which can offset their daily operations than continue operating at a loss.

However, an elasticity of 0.6 is less than one, thus inelastic. As a result, I would advise the firm

to increase its prices to increase the revenue since there will be a decrease in units sold in the

market. As the volume of output decreases, the increase in marginal revenue will be used to

cover for the diminishing value in sales as the price increases, As a result, the firm will be able to

increase its price in order to be able to maximize the profit and with anticipation of future loss in

revenue to cover for the fixed costs.

Figure 2.0: Inelastic demand

From figure 2.0 above the increase in the price will increase the total revenue even if the total

output will decrease. This is because as the price increases with a decrease in sales, the income

collected will be stable in the long run, thus leading to a stable market revenue earnings

(Oliveira-Castro & Foxall, 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ECONOMICS 4

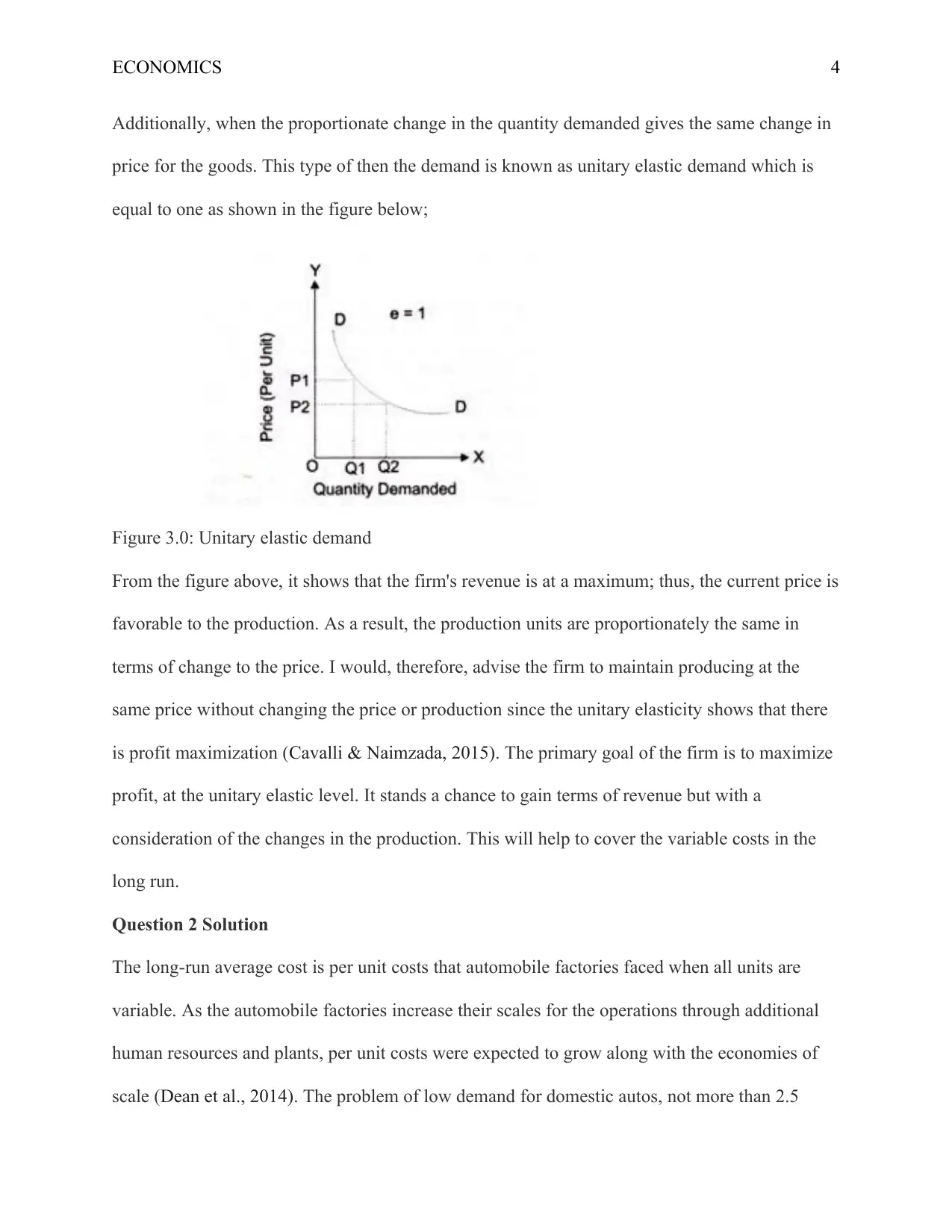

Additionally, when the proportionate change in the quantity demanded gives the same change in

price for the goods. This type of then the demand is known as unitary elastic demand which is

equal to one as shown in the figure below;

Figure 3.0: Unitary elastic demand

From the figure above, it shows that the firm's revenue is at a maximum; thus, the current price is

favorable to the production. As a result, the production units are proportionately the same in

terms of change to the price. I would, therefore, advise the firm to maintain producing at the

same price without changing the price or production since the unitary elasticity shows that there

is profit maximization (Cavalli & Naimzada, 2015). The primary goal of the firm is to maximize

profit, at the unitary elastic level. It stands a chance to gain terms of revenue but with a

consideration of the changes in the production. This will help to cover the variable costs in the

long run.

Question 2 Solution

The long-run average cost is per unit costs that automobile factories faced when all units are

variable. As the automobile factories increase their scales for the operations through additional

human resources and plants, per unit costs were expected to grow along with the economies of

scale (Dean et al., 2014). The problem of low demand for domestic autos, not more than 2.5

Additionally, when the proportionate change in the quantity demanded gives the same change in

price for the goods. This type of then the demand is known as unitary elastic demand which is

equal to one as shown in the figure below;

Figure 3.0: Unitary elastic demand

From the figure above, it shows that the firm's revenue is at a maximum; thus, the current price is

favorable to the production. As a result, the production units are proportionately the same in

terms of change to the price. I would, therefore, advise the firm to maintain producing at the

same price without changing the price or production since the unitary elasticity shows that there

is profit maximization (Cavalli & Naimzada, 2015). The primary goal of the firm is to maximize

profit, at the unitary elastic level. It stands a chance to gain terms of revenue but with a

consideration of the changes in the production. This will help to cover the variable costs in the

long run.

Question 2 Solution

The long-run average cost is per unit costs that automobile factories faced when all units are

variable. As the automobile factories increase their scales for the operations through additional

human resources and plants, per unit costs were expected to grow along with the economies of

scale (Dean et al., 2014). The problem of low demand for domestic autos, not more than 2.5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ECONOMICS 5

times the total quantity produced locally was a predicament that faced the United States

Automobile manufacturing industry during the early 1970s. This was due to the financial

recession that hit the country, thus lowering the demand for the locally produced autos (Oh,

2014). As a result, since there was only demand one firm provides, which was equated to the 2.5

firms’ outputs to hit bottom average cost, the other firms were, therefore, making a massive loss.

At the same time, the remaining firm was struggling to sustain its operation in the market.

As the cost of production increases, total revenue will be reduced at the same stead. It, therefore,

leads to a diseconomy of scale where there will be a layoff of workers and a decrease in the wage

rage to sustain the variable costs of operations. However, in the constant return to scale level, if

firms decide to increase their inputs concerning non-changes in the average costs, they will still

experience diseconomies of scale (Dorman, 2014). This is because, in the average long run, each

firm is entitled to produce units that increase as its total output increases. The long run average

cost (LRAC) depicts the lowest cost of providing the autos in the market. When the producers

vary the inputs of productions, including technology, there will be an increase in its production

multiplier in the industry.

The increase in the units produced within the automobile industries led to a decrease in the

average cost for each unit due to increased cost for producing additional products. As a result,

the demand for the autos increased, thus leading to 2.5 times demand at the lower average cost.

The increase I the demand was due to the lower prices for the raw materials in the industry, thus

leading to increment in production. However, in the long run, as the output level will be

increasing, the long-run average cost will be decreasing in the economies of scale due to costs in

production and demand change in the demand for the auto products (Mankiw, 2014).

Question 3 Solution

times the total quantity produced locally was a predicament that faced the United States

Automobile manufacturing industry during the early 1970s. This was due to the financial

recession that hit the country, thus lowering the demand for the locally produced autos (Oh,

2014). As a result, since there was only demand one firm provides, which was equated to the 2.5

firms’ outputs to hit bottom average cost, the other firms were, therefore, making a massive loss.

At the same time, the remaining firm was struggling to sustain its operation in the market.

As the cost of production increases, total revenue will be reduced at the same stead. It, therefore,

leads to a diseconomy of scale where there will be a layoff of workers and a decrease in the wage

rage to sustain the variable costs of operations. However, in the constant return to scale level, if

firms decide to increase their inputs concerning non-changes in the average costs, they will still

experience diseconomies of scale (Dorman, 2014). This is because, in the average long run, each

firm is entitled to produce units that increase as its total output increases. The long run average

cost (LRAC) depicts the lowest cost of providing the autos in the market. When the producers

vary the inputs of productions, including technology, there will be an increase in its production

multiplier in the industry.

The increase in the units produced within the automobile industries led to a decrease in the

average cost for each unit due to increased cost for producing additional products. As a result,

the demand for the autos increased, thus leading to 2.5 times demand at the lower average cost.

The increase I the demand was due to the lower prices for the raw materials in the industry, thus

leading to increment in production. However, in the long run, as the output level will be

increasing, the long-run average cost will be decreasing in the economies of scale due to costs in

production and demand change in the demand for the auto products (Mankiw, 2014).

Question 3 Solution

ECONOMICS 6

The economic rate of productivity growth is directly related to the rate of GDP per Capita

growth, even though the two are unique in their functions (Aghion et al., 2016). Australia is one

of the high-income economies in terms of employment availability, thus showing that as the

percentage of population holding jobs increases, the GDP per capita also increases. It, therefore,

shows that the productivity of an individual worker in a country leads to a GDP per capita

growth since, in Australia; the average worker's productivity is determined by the corresponding

increase in capital creation.

Availability of physical capital, which includes the plant and machinery, infrastructure growth is

also a determinant of GDP per capita growth in Australia (Qu et al., 2016). As the physical

capital enhances, there is an increase in output i.e., the country is stable in terms of technological

growth thus increases the productivity level compared to less developed economies. As a result,

there will be economic growth and development due to enhance human and physical capital,

which are steadily available. Technological progress is described in high-income economies as a

'joker in the deck' because of its combination of innovation and invention capabilities (Kim &

Loayza, 2017). For instance, Australia has ensured that it assembles new technological progress

in the agricultural development, in the manufacturing, and service industries to help its economy

produce quality output in the factories. At the same time, the tertiary institutions are aligned to

the research and development of new ideas that are facilitating the conversion of inputs from the

industries to complete goods and services. As a result, there is an increase in growth of GDP Per

Capita in Australia will increase in the long run compared to middle or low-income countries.

However, in a middle-income earning country like India, this might not be the case because there

might be economic growth without development. India has the availability of physical capital but

lacks the financial superiorly to invest in the nation increased population since there unbalanced

The economic rate of productivity growth is directly related to the rate of GDP per Capita

growth, even though the two are unique in their functions (Aghion et al., 2016). Australia is one

of the high-income economies in terms of employment availability, thus showing that as the

percentage of population holding jobs increases, the GDP per capita also increases. It, therefore,

shows that the productivity of an individual worker in a country leads to a GDP per capita

growth since, in Australia; the average worker's productivity is determined by the corresponding

increase in capital creation.

Availability of physical capital, which includes the plant and machinery, infrastructure growth is

also a determinant of GDP per capita growth in Australia (Qu et al., 2016). As the physical

capital enhances, there is an increase in output i.e., the country is stable in terms of technological

growth thus increases the productivity level compared to less developed economies. As a result,

there will be economic growth and development due to enhance human and physical capital,

which are steadily available. Technological progress is described in high-income economies as a

'joker in the deck' because of its combination of innovation and invention capabilities (Kim &

Loayza, 2017). For instance, Australia has ensured that it assembles new technological progress

in the agricultural development, in the manufacturing, and service industries to help its economy

produce quality output in the factories. At the same time, the tertiary institutions are aligned to

the research and development of new ideas that are facilitating the conversion of inputs from the

industries to complete goods and services. As a result, there is an increase in growth of GDP Per

Capita in Australia will increase in the long run compared to middle or low-income countries.

However, in a middle-income earning country like India, this might not be the case because there

might be economic growth without development. India has the availability of physical capital but

lacks the financial superiorly to invest in the nation increased population since there unbalanced

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ECONOMICS 7

income distribution among the citizens. For example, the differences in wage distribution are due

to lack of proper education amongst the citizens, thus reduces GDP per capita growth in the

economy (Yeager, 2018). Even though India is one of the middle-income countries who's GDP

per capita increases per year, lack of capital creation with an equitable resource allocation has led

to sluggish economic growth and development in the country.

A low-income country is one that has low capital creation; there is wage gap disparity, and lack

of necessary provisions such as education, health, and meals (Rodrik, 2014). As a result, capital

creation in Afghanistan reduces due to lack of knowledge that promotes human capital growth

and technological progress (Ncube et al., 2014). Productivity rate in Afghanistan is diminishing

with a decrease in human capital creation, thus reduces the rate of GDP Per Capita growth.

Governance and security are also a significant factor in steady GDP Per Capita growth in any

economy therefore, due to insecurity in most of the low-income economies, including

Afghanistan.

Question 4 Solution

Inflation is the persistent change in the basket reasonable prices over some time; thus, a change

in the measurement of the inflation by the government statisticians had significant effects in

terms of quality of goods, prices, and consumers' behavior in terms of substitution biasness

(Tongur, 2019). Consumer Price Index is the commonly used measurement for the inflation

indicator as it measures the purchasing cost of the pre-determined basket goods and services. The

index is more convenient since it takes in to account the nominal cost of the fixed basket prices

of products at a given time.

Government is at liberty to accurately measure and update the prices of the basket goods in order

to help define the nature and type of inflation that a country is anticipating or facing already. If

income distribution among the citizens. For example, the differences in wage distribution are due

to lack of proper education amongst the citizens, thus reduces GDP per capita growth in the

economy (Yeager, 2018). Even though India is one of the middle-income countries who's GDP

per capita increases per year, lack of capital creation with an equitable resource allocation has led

to sluggish economic growth and development in the country.

A low-income country is one that has low capital creation; there is wage gap disparity, and lack

of necessary provisions such as education, health, and meals (Rodrik, 2014). As a result, capital

creation in Afghanistan reduces due to lack of knowledge that promotes human capital growth

and technological progress (Ncube et al., 2014). Productivity rate in Afghanistan is diminishing

with a decrease in human capital creation, thus reduces the rate of GDP Per Capita growth.

Governance and security are also a significant factor in steady GDP Per Capita growth in any

economy therefore, due to insecurity in most of the low-income economies, including

Afghanistan.

Question 4 Solution

Inflation is the persistent change in the basket reasonable prices over some time; thus, a change

in the measurement of the inflation by the government statisticians had significant effects in

terms of quality of goods, prices, and consumers' behavior in terms of substitution biasness

(Tongur, 2019). Consumer Price Index is the commonly used measurement for the inflation

indicator as it measures the purchasing cost of the pre-determined basket goods and services. The

index is more convenient since it takes in to account the nominal cost of the fixed basket prices

of products at a given time.

Government is at liberty to accurately measure and update the prices of the basket goods in order

to help define the nature and type of inflation that a country is anticipating or facing already. If

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ECONOMICS 8

the government statistician decides to update the national basket prices of goods and services

after just five years instead of after every ten years, there will be a problem of substitution

biasness which will affect the quality of the new measurement in terms of variability in the time

period for the prices of goods and services (Crayton & Hart, 2015). As a result, there will be a

reduction in the standard measurement, thus leading to a misguidance principle of inflation. This

is because when using the price index as a tool for measuring the inflation rate, the problem of

substitution biasness will be prone to occur. As a result, consumers can substitute goods due to

changes in their prices. For instance, an increase in the amount of apple will force consumers to

replace apple with oranges, thus avoids the increase in price a little bit.

Change in the measurability pattern for the basket goods from ten years to five years will likely

omit the consumers' choice in substituting the increment in the price for one good with the other.

This is because the existence of substitution biasness will neglect the change in the purchasing

choices over ten years to five years (Krugman, 2014). Prices of basket goods change within a

period, thus assuming that within five years, it will remain constant is economically unrealistic.

This is because as the consumer substitutes one good to the other, they forgo a higher price,

which is actively provided in the market for a low price. Changes in consumption patterns due to

change in price will, therefore, result in a difference in the price index (Krugman, 2014).

The changes in prices of goods majorly determine the inflation rate, thus assuming the

substitution effect when consumers switch from a higher-priced commodity to relatively less

expensive products will generally affect the calculation of the inflation rate from ten years to five

years. It will, therefore, lead to an overestimated CPI since the actual changes in prices of basket

goods and services are not included in the measurement (Kaplan & Schulhofer-Wohl, 2017). The

assumption that consumers will always purchase a fixed basket of products over the period

the government statistician decides to update the national basket prices of goods and services

after just five years instead of after every ten years, there will be a problem of substitution

biasness which will affect the quality of the new measurement in terms of variability in the time

period for the prices of goods and services (Crayton & Hart, 2015). As a result, there will be a

reduction in the standard measurement, thus leading to a misguidance principle of inflation. This

is because when using the price index as a tool for measuring the inflation rate, the problem of

substitution biasness will be prone to occur. As a result, consumers can substitute goods due to

changes in their prices. For instance, an increase in the amount of apple will force consumers to

replace apple with oranges, thus avoids the increase in price a little bit.

Change in the measurability pattern for the basket goods from ten years to five years will likely

omit the consumers' choice in substituting the increment in the price for one good with the other.

This is because the existence of substitution biasness will neglect the change in the purchasing

choices over ten years to five years (Krugman, 2014). Prices of basket goods change within a

period, thus assuming that within five years, it will remain constant is economically unrealistic.

This is because as the consumer substitutes one good to the other, they forgo a higher price,

which is actively provided in the market for a low price. Changes in consumption patterns due to

change in price will, therefore, result in a difference in the price index (Krugman, 2014).

The changes in prices of goods majorly determine the inflation rate, thus assuming the

substitution effect when consumers switch from a higher-priced commodity to relatively less

expensive products will generally affect the calculation of the inflation rate from ten years to five

years. It will, therefore, lead to an overestimated CPI since the actual changes in prices of basket

goods and services are not included in the measurement (Kaplan & Schulhofer-Wohl, 2017). The

assumption that consumers will always purchase a fixed basket of products over the period

ECONOMICS 9

works against the government statisticians. This is because the national government is obliged to

observe any changes that come to it as a result of the difference in the national consumption

pattern of the individual in an economy.

References

Aghion, P., Comin, D., Howitt, P., & Tecu, I. (2016). When does domestic savings matter for

economic growth?. IMF Economic Review, 64(3), 381-407.

Cavalli, F., & Naimzada, A. (2015). Effect of price elasticity of demand in monopolies with

gradient adjustment. Chaos, Solitons & Fractals, 76, 47-55.

Crayton, L. A., & Hart, J. (2015). Inflation: What it is and how it Works. Enslow Publishing,

LLC.

Dean, E., Elardo, J., Green, M., Wilson, B., & Berger, S. (2014). 10.3 The Structure of Costs in

the Long Run. Principles of Economics.

Dorman, P. (2014). Production Costs and the Theory of Supply. In Microeconomics (pp. 249-

274). Springer, Berlin, Heidelberg.

Fouquet, R. (2014). Long-run demand for energy services: Income and price elasticities over two

hundred years. Review of Environmental Economics and Policy, 8(2), 186-207.

Gatwood, J., Gibson, T. B., Chernew, M. E., Farr, A. M., Vogtmann, E., & Fendrick, A. M.

(2014). Price elasticity and medication use: cost sharing across multiple clinical

conditions. Journal of Managed Care Pharmacy, 20(11), 1102-1107.

Kaplan, G., & Schulhofer-Wohl, S. (2017). Inflation at the household level. Journal of Monetary

Economics, 91, 19-38.

works against the government statisticians. This is because the national government is obliged to

observe any changes that come to it as a result of the difference in the national consumption

pattern of the individual in an economy.

References

Aghion, P., Comin, D., Howitt, P., & Tecu, I. (2016). When does domestic savings matter for

economic growth?. IMF Economic Review, 64(3), 381-407.

Cavalli, F., & Naimzada, A. (2015). Effect of price elasticity of demand in monopolies with

gradient adjustment. Chaos, Solitons & Fractals, 76, 47-55.

Crayton, L. A., & Hart, J. (2015). Inflation: What it is and how it Works. Enslow Publishing,

LLC.

Dean, E., Elardo, J., Green, M., Wilson, B., & Berger, S. (2014). 10.3 The Structure of Costs in

the Long Run. Principles of Economics.

Dorman, P. (2014). Production Costs and the Theory of Supply. In Microeconomics (pp. 249-

274). Springer, Berlin, Heidelberg.

Fouquet, R. (2014). Long-run demand for energy services: Income and price elasticities over two

hundred years. Review of Environmental Economics and Policy, 8(2), 186-207.

Gatwood, J., Gibson, T. B., Chernew, M. E., Farr, A. M., Vogtmann, E., & Fendrick, A. M.

(2014). Price elasticity and medication use: cost sharing across multiple clinical

conditions. Journal of Managed Care Pharmacy, 20(11), 1102-1107.

Kaplan, G., & Schulhofer-Wohl, S. (2017). Inflation at the household level. Journal of Monetary

Economics, 91, 19-38.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ECONOMICS 10

Kim, Y. E., & Loayza, N. (2017). Productivity and its Determinants: Innovation, Education,

Efficiency, Infrastructure, and Institutions. Unpublished Working Paper.

Krugman, P. (2014). Inflation targets reconsidered. In ECB Forum on Central Banking,

Conference Proceedings (pp. 110-122).

Mankiw, N. G. (2014). Principles of economics. Cengage Learning.

Ncube, M., Anyanwu, J. C., & Hausken, K. (2014). Inequality, economic growth and poverty in

the Middle East and North Africa (MENA). African Development Review, 26(3), 435-453.

Oh, S. Y. (2014). Shifting gears: industrial policy and automotive industry after the 2008

financial crisis. Business and Politics, 16(4), 641-665.

Oliveira-Castro, J. M., & Foxall, G. R. (2016). Dimensions of demand elasticity. The Routledge

companion to consumer behavior analysis, 121-137.

Qu, J., Simes, R., O’Mahony, J., & Economics, D. A. (2016). How Do Digital Technologies

Drive Economic Growth? Research Outline.

Rodrik, D. (2014). The past, present, and future of economic growth. Challenge, 57(3), 5-39.

Tongur, C. (2019). Inflation Measurement with Scanner Data and an Ever-Changing Fixed

Basket. Economie et Statistique, 509(1), 31-47.

Yeager, T. (2018). Institutions, transition economies, and economic development. Routledge.

Kim, Y. E., & Loayza, N. (2017). Productivity and its Determinants: Innovation, Education,

Efficiency, Infrastructure, and Institutions. Unpublished Working Paper.

Krugman, P. (2014). Inflation targets reconsidered. In ECB Forum on Central Banking,

Conference Proceedings (pp. 110-122).

Mankiw, N. G. (2014). Principles of economics. Cengage Learning.

Ncube, M., Anyanwu, J. C., & Hausken, K. (2014). Inequality, economic growth and poverty in

the Middle East and North Africa (MENA). African Development Review, 26(3), 435-453.

Oh, S. Y. (2014). Shifting gears: industrial policy and automotive industry after the 2008

financial crisis. Business and Politics, 16(4), 641-665.

Oliveira-Castro, J. M., & Foxall, G. R. (2016). Dimensions of demand elasticity. The Routledge

companion to consumer behavior analysis, 121-137.

Qu, J., Simes, R., O’Mahony, J., & Economics, D. A. (2016). How Do Digital Technologies

Drive Economic Growth? Research Outline.

Rodrik, D. (2014). The past, present, and future of economic growth. Challenge, 57(3), 5-39.

Tongur, C. (2019). Inflation Measurement with Scanner Data and an Ever-Changing Fixed

Basket. Economie et Statistique, 509(1), 31-47.

Yeager, T. (2018). Institutions, transition economies, and economic development. Routledge.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.