Economics Assignment: Short Run Costs, Firm Equilibrium, and Inflation

VerifiedAdded on 2022/12/28

|11

|2994

|1

Essay

AI Summary

This economics assignment analyzes several key concepts. It begins by examining the relationship between short-run costs, including fixed and variable costs, using tables and diagrams. It then differentiates between the short-run equilibrium situations of perfectly competitive firms and monopolist firms. The essay defines inflation, explores its sources, such as demand-pull inflation, and evaluates the associated costs, including reduced international competitiveness and economic uncertainty. The analysis considers the UK's economic context, including the impact of factors like Brexit and exchange rate fluctuations on inflation and the overall economy. The assignment also delves into the effects of inflation on investment, savings, and the standard of living, offering a comprehensive overview of these important economic principles.

Economics

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

Analysing the relationship between the short run cost through using table and diagram............1

Evaluating difference between short run equilibrium situation of perfectly competitive firm

and monopolist firm.....................................................................................................................5

Defining the inflation ..................................................................................................................6

Analysing the cost of inflation ....................................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

Analysing the relationship between the short run cost through using table and diagram............1

Evaluating difference between short run equilibrium situation of perfectly competitive firm

and monopolist firm.....................................................................................................................5

Defining the inflation ..................................................................................................................6

Analysing the cost of inflation ....................................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION

Economics concerned with the social science that deals with production, distribution and

consumption of goods and services. It is important form of study that an individual, businesses,

government and facilitates in making choices about how it allocate the resources effectively

(Anderegg and et.al, 2018).

In the UK, the economy is highly developed social market and also market oriented

economy and it is fifth largest national economy in the world. In this essay it is discussed about

the relationship of short run costs and critically examine through table and diagram. It is studied

the difference exist between short run equilibrium situation of perfectly competitive firm in

Monopolist firm. Apart from that it is define the inflation and mentioning the least three sources

and critically evaluate the cost of inflation of the economy is being discussed.

MAIN BODY

Analysing the relationship between the short run cost through using table and diagram

Short run cost contains both fixed and variable cost and in long run there is no fixed cost

and in short run cost price has short term inferences in the manufacturing procedure (Andor and

Fels, 2018). In this concept the short run the quantity of at least one input is fixed and quantities

of other input might be varied. In this period land and machinery remain the same and in this

expansion is done by hiring more labour and increasing capital. In the context of UK company,

the short run means that an output that increases by adding more variable factors that include the

employing the more worker and that increases the buying in more raw materials. There are

certain types of short run cost which is discussed below-

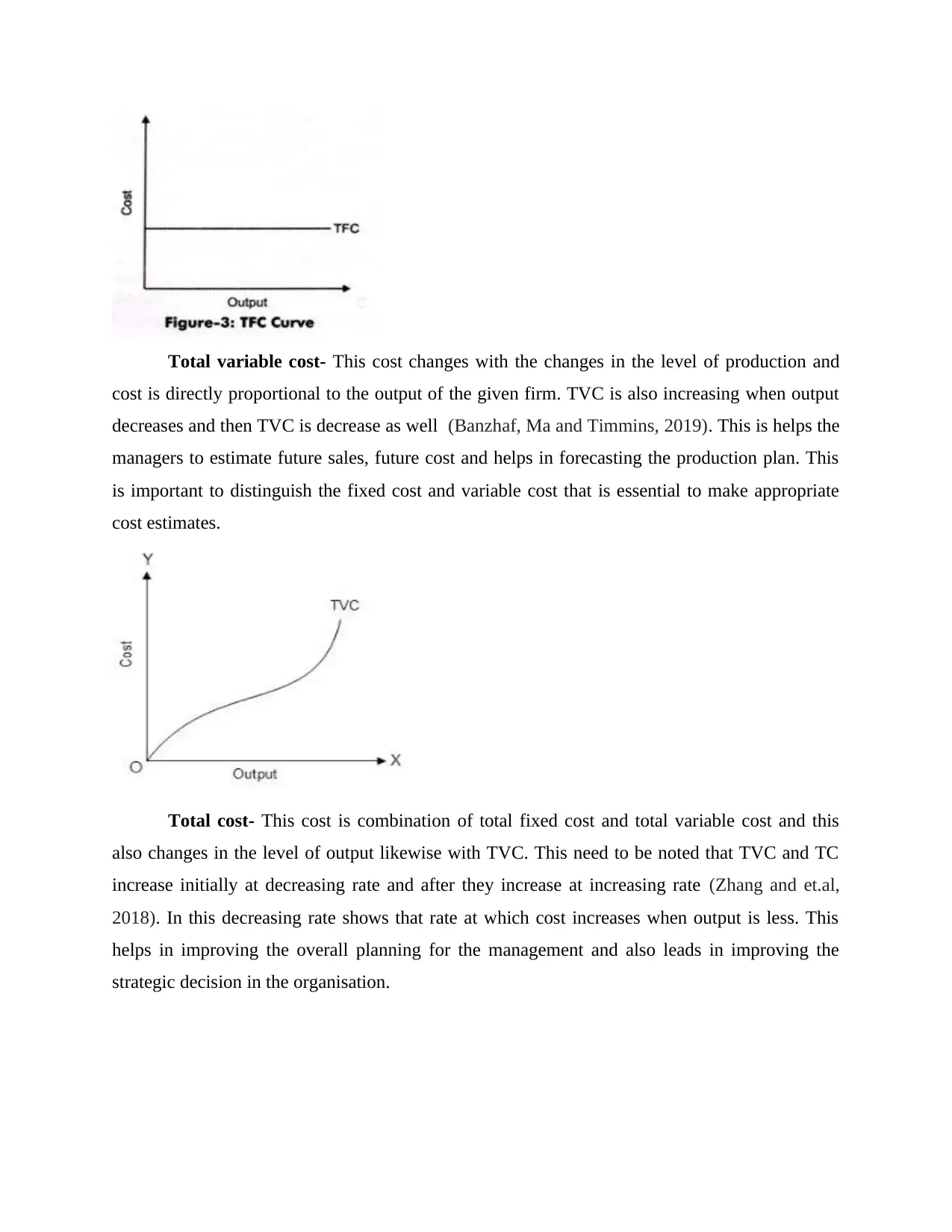

Total Fixed cost- This types of cost that used to remain constant in short period of period

and it does not change with the changes in the level of output. It is sum of shot run explicit fixed

cost and implicit cost that is incurred by entrepreneur. It will show the amount even when there

is no production in the company as they will occurred even when there is none activity in the

output. These cost are also known as supplementary cost, indirect cost, overhead cost, historical

cost. Therefore their slope of TFC Curve is horizontal straight line. This curve is horizontal to x-

axis and it can be seen that TFC remains the constant at all levels with the change in output.

Economics concerned with the social science that deals with production, distribution and

consumption of goods and services. It is important form of study that an individual, businesses,

government and facilitates in making choices about how it allocate the resources effectively

(Anderegg and et.al, 2018).

In the UK, the economy is highly developed social market and also market oriented

economy and it is fifth largest national economy in the world. In this essay it is discussed about

the relationship of short run costs and critically examine through table and diagram. It is studied

the difference exist between short run equilibrium situation of perfectly competitive firm in

Monopolist firm. Apart from that it is define the inflation and mentioning the least three sources

and critically evaluate the cost of inflation of the economy is being discussed.

MAIN BODY

Analysing the relationship between the short run cost through using table and diagram

Short run cost contains both fixed and variable cost and in long run there is no fixed cost

and in short run cost price has short term inferences in the manufacturing procedure (Andor and

Fels, 2018). In this concept the short run the quantity of at least one input is fixed and quantities

of other input might be varied. In this period land and machinery remain the same and in this

expansion is done by hiring more labour and increasing capital. In the context of UK company,

the short run means that an output that increases by adding more variable factors that include the

employing the more worker and that increases the buying in more raw materials. There are

certain types of short run cost which is discussed below-

Total Fixed cost- This types of cost that used to remain constant in short period of period

and it does not change with the changes in the level of output. It is sum of shot run explicit fixed

cost and implicit cost that is incurred by entrepreneur. It will show the amount even when there

is no production in the company as they will occurred even when there is none activity in the

output. These cost are also known as supplementary cost, indirect cost, overhead cost, historical

cost. Therefore their slope of TFC Curve is horizontal straight line. This curve is horizontal to x-

axis and it can be seen that TFC remains the constant at all levels with the change in output.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Total variable cost- This cost changes with the changes in the level of production and

cost is directly proportional to the output of the given firm. TVC is also increasing when output

decreases and then TVC is decrease as well (Banzhaf, Ma and Timmins, 2019). This is helps the

managers to estimate future sales, future cost and helps in forecasting the production plan. This

is important to distinguish the fixed cost and variable cost that is essential to make appropriate

cost estimates.

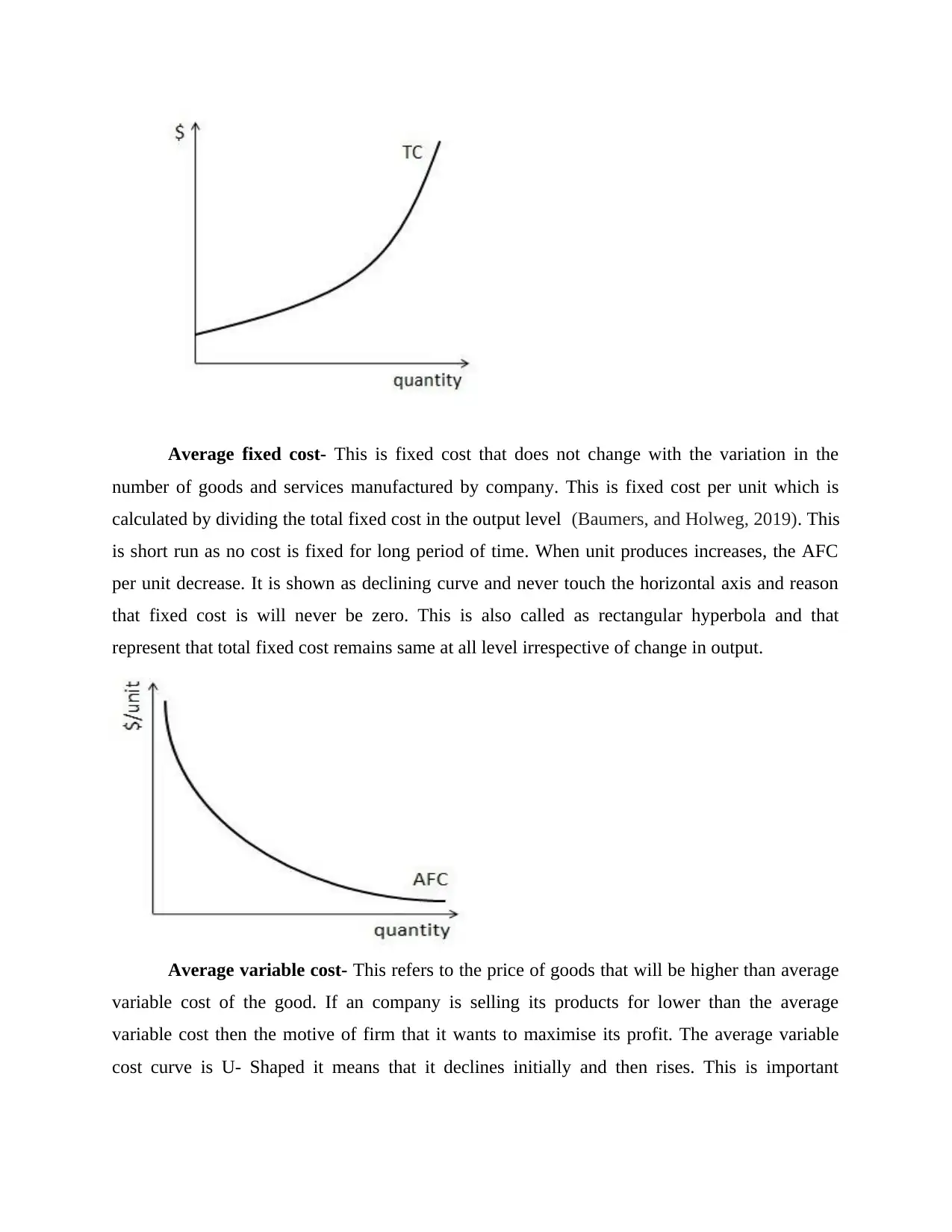

Total cost- This cost is combination of total fixed cost and total variable cost and this

also changes in the level of output likewise with TVC. This need to be noted that TVC and TC

increase initially at decreasing rate and after they increase at increasing rate (Zhang and et.al,

2018). In this decreasing rate shows that rate at which cost increases when output is less. This

helps in improving the overall planning for the management and also leads in improving the

strategic decision in the organisation.

cost is directly proportional to the output of the given firm. TVC is also increasing when output

decreases and then TVC is decrease as well (Banzhaf, Ma and Timmins, 2019). This is helps the

managers to estimate future sales, future cost and helps in forecasting the production plan. This

is important to distinguish the fixed cost and variable cost that is essential to make appropriate

cost estimates.

Total cost- This cost is combination of total fixed cost and total variable cost and this

also changes in the level of output likewise with TVC. This need to be noted that TVC and TC

increase initially at decreasing rate and after they increase at increasing rate (Zhang and et.al,

2018). In this decreasing rate shows that rate at which cost increases when output is less. This

helps in improving the overall planning for the management and also leads in improving the

strategic decision in the organisation.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

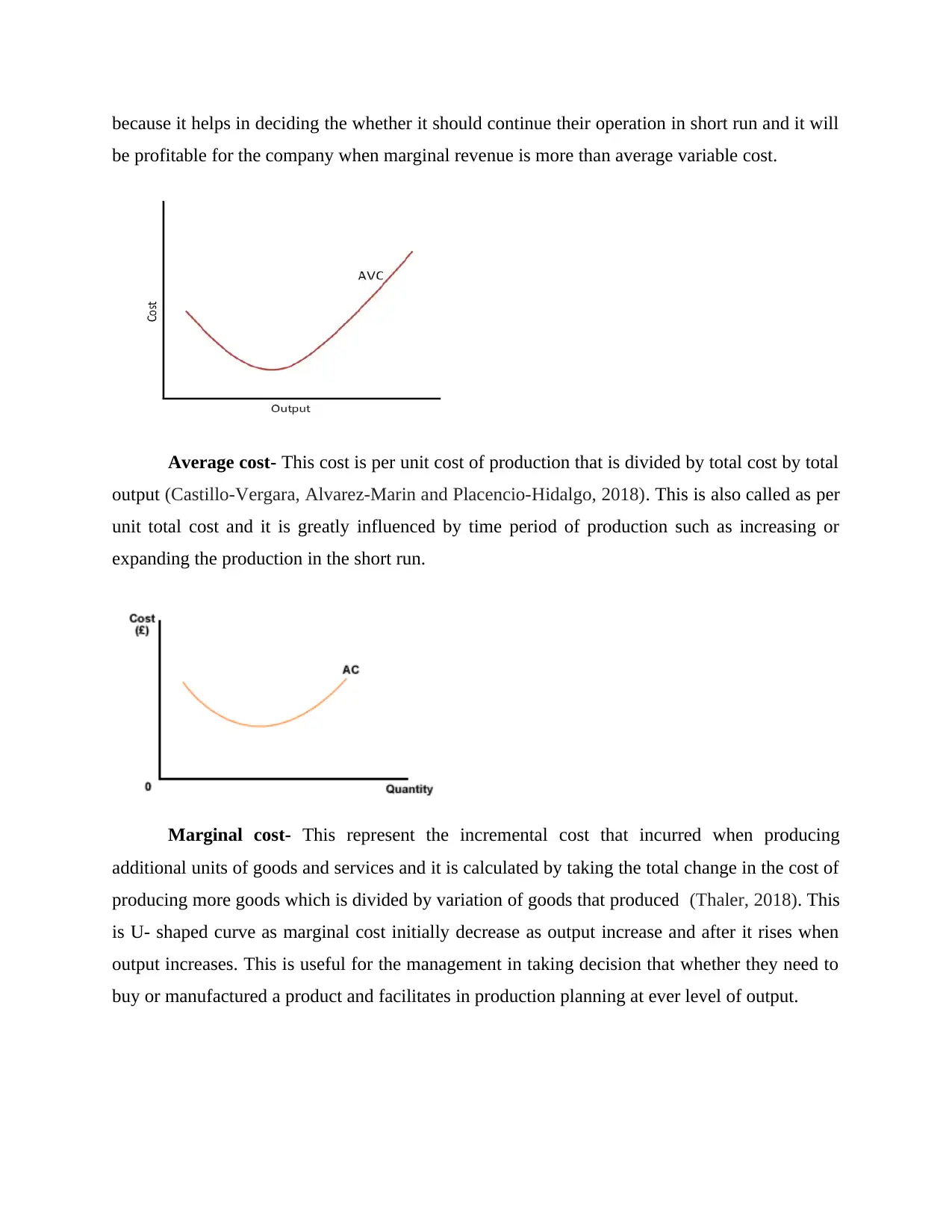

Average fixed cost- This is fixed cost that does not change with the variation in the

number of goods and services manufactured by company. This is fixed cost per unit which is

calculated by dividing the total fixed cost in the output level (Baumers, and Holweg, 2019). This

is short run as no cost is fixed for long period of time. When unit produces increases, the AFC

per unit decrease. It is shown as declining curve and never touch the horizontal axis and reason

that fixed cost is will never be zero. This is also called as rectangular hyperbola and that

represent that total fixed cost remains same at all level irrespective of change in output.

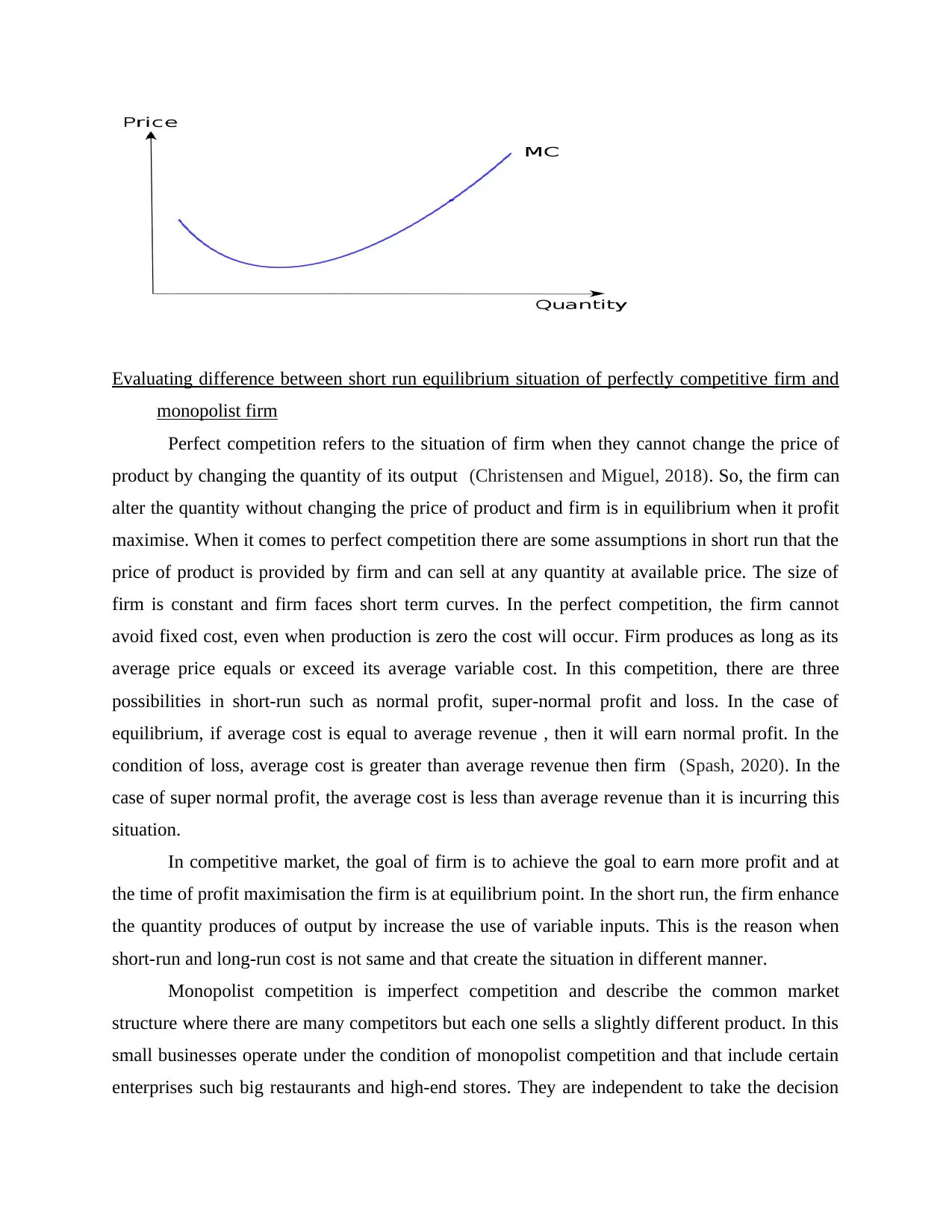

Average variable cost- This refers to the price of goods that will be higher than average

variable cost of the good. If an company is selling its products for lower than the average

variable cost then the motive of firm that it wants to maximise its profit. The average variable

cost curve is U- Shaped it means that it declines initially and then rises. This is important

number of goods and services manufactured by company. This is fixed cost per unit which is

calculated by dividing the total fixed cost in the output level (Baumers, and Holweg, 2019). This

is short run as no cost is fixed for long period of time. When unit produces increases, the AFC

per unit decrease. It is shown as declining curve and never touch the horizontal axis and reason

that fixed cost is will never be zero. This is also called as rectangular hyperbola and that

represent that total fixed cost remains same at all level irrespective of change in output.

Average variable cost- This refers to the price of goods that will be higher than average

variable cost of the good. If an company is selling its products for lower than the average

variable cost then the motive of firm that it wants to maximise its profit. The average variable

cost curve is U- Shaped it means that it declines initially and then rises. This is important

because it helps in deciding the whether it should continue their operation in short run and it will

be profitable for the company when marginal revenue is more than average variable cost.

Average cost- This cost is per unit cost of production that is divided by total cost by total

output (Castillo-Vergara, Alvarez-Marin and Placencio-Hidalgo, 2018). This is also called as per

unit total cost and it is greatly influenced by time period of production such as increasing or

expanding the production in the short run.

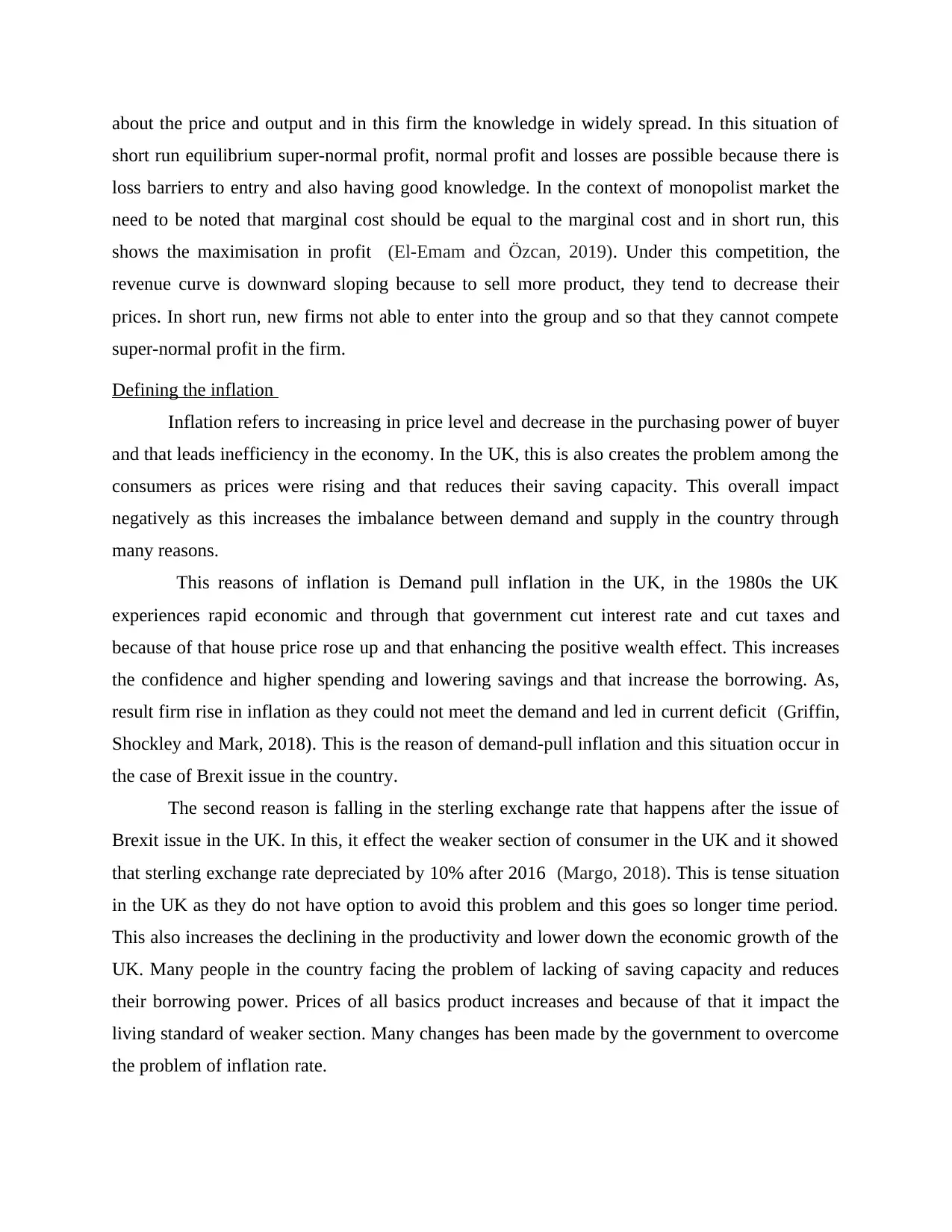

Marginal cost- This represent the incremental cost that incurred when producing

additional units of goods and services and it is calculated by taking the total change in the cost of

producing more goods which is divided by variation of goods that produced (Thaler, 2018). This

is U- shaped curve as marginal cost initially decrease as output increase and after it rises when

output increases. This is useful for the management in taking decision that whether they need to

buy or manufactured a product and facilitates in production planning at ever level of output.

be profitable for the company when marginal revenue is more than average variable cost.

Average cost- This cost is per unit cost of production that is divided by total cost by total

output (Castillo-Vergara, Alvarez-Marin and Placencio-Hidalgo, 2018). This is also called as per

unit total cost and it is greatly influenced by time period of production such as increasing or

expanding the production in the short run.

Marginal cost- This represent the incremental cost that incurred when producing

additional units of goods and services and it is calculated by taking the total change in the cost of

producing more goods which is divided by variation of goods that produced (Thaler, 2018). This

is U- shaped curve as marginal cost initially decrease as output increase and after it rises when

output increases. This is useful for the management in taking decision that whether they need to

buy or manufactured a product and facilitates in production planning at ever level of output.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Evaluating difference between short run equilibrium situation of perfectly competitive firm and

monopolist firm

Perfect competition refers to the situation of firm when they cannot change the price of

product by changing the quantity of its output (Christensen and Miguel, 2018). So, the firm can

alter the quantity without changing the price of product and firm is in equilibrium when it profit

maximise. When it comes to perfect competition there are some assumptions in short run that the

price of product is provided by firm and can sell at any quantity at available price. The size of

firm is constant and firm faces short term curves. In the perfect competition, the firm cannot

avoid fixed cost, even when production is zero the cost will occur. Firm produces as long as its

average price equals or exceed its average variable cost. In this competition, there are three

possibilities in short-run such as normal profit, super-normal profit and loss. In the case of

equilibrium, if average cost is equal to average revenue , then it will earn normal profit. In the

condition of loss, average cost is greater than average revenue then firm (Spash, 2020). In the

case of super normal profit, the average cost is less than average revenue than it is incurring this

situation.

In competitive market, the goal of firm is to achieve the goal to earn more profit and at

the time of profit maximisation the firm is at equilibrium point. In the short run, the firm enhance

the quantity produces of output by increase the use of variable inputs. This is the reason when

short-run and long-run cost is not same and that create the situation in different manner.

Monopolist competition is imperfect competition and describe the common market

structure where there are many competitors but each one sells a slightly different product. In this

small businesses operate under the condition of monopolist competition and that include certain

enterprises such big restaurants and high-end stores. They are independent to take the decision

monopolist firm

Perfect competition refers to the situation of firm when they cannot change the price of

product by changing the quantity of its output (Christensen and Miguel, 2018). So, the firm can

alter the quantity without changing the price of product and firm is in equilibrium when it profit

maximise. When it comes to perfect competition there are some assumptions in short run that the

price of product is provided by firm and can sell at any quantity at available price. The size of

firm is constant and firm faces short term curves. In the perfect competition, the firm cannot

avoid fixed cost, even when production is zero the cost will occur. Firm produces as long as its

average price equals or exceed its average variable cost. In this competition, there are three

possibilities in short-run such as normal profit, super-normal profit and loss. In the case of

equilibrium, if average cost is equal to average revenue , then it will earn normal profit. In the

condition of loss, average cost is greater than average revenue then firm (Spash, 2020). In the

case of super normal profit, the average cost is less than average revenue than it is incurring this

situation.

In competitive market, the goal of firm is to achieve the goal to earn more profit and at

the time of profit maximisation the firm is at equilibrium point. In the short run, the firm enhance

the quantity produces of output by increase the use of variable inputs. This is the reason when

short-run and long-run cost is not same and that create the situation in different manner.

Monopolist competition is imperfect competition and describe the common market

structure where there are many competitors but each one sells a slightly different product. In this

small businesses operate under the condition of monopolist competition and that include certain

enterprises such big restaurants and high-end stores. They are independent to take the decision

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

about the price and output and in this firm the knowledge in widely spread. In this situation of

short run equilibrium super-normal profit, normal profit and losses are possible because there is

loss barriers to entry and also having good knowledge. In the context of monopolist market the

need to be noted that marginal cost should be equal to the marginal cost and in short run, this

shows the maximisation in profit (El-Emam and Özcan, 2019). Under this competition, the

revenue curve is downward sloping because to sell more product, they tend to decrease their

prices. In short run, new firms not able to enter into the group and so that they cannot compete

super-normal profit in the firm.

Defining the inflation

Inflation refers to increasing in price level and decrease in the purchasing power of buyer

and that leads inefficiency in the economy. In the UK, this is also creates the problem among the

consumers as prices were rising and that reduces their saving capacity. This overall impact

negatively as this increases the imbalance between demand and supply in the country through

many reasons.

This reasons of inflation is Demand pull inflation in the UK, in the 1980s the UK

experiences rapid economic and through that government cut interest rate and cut taxes and

because of that house price rose up and that enhancing the positive wealth effect. This increases

the confidence and higher spending and lowering savings and that increase the borrowing. As,

result firm rise in inflation as they could not meet the demand and led in current deficit (Griffin,

Shockley and Mark, 2018). This is the reason of demand-pull inflation and this situation occur in

the case of Brexit issue in the country.

The second reason is falling in the sterling exchange rate that happens after the issue of

Brexit issue in the UK. In this, it effect the weaker section of consumer in the UK and it showed

that sterling exchange rate depreciated by 10% after 2016 (Margo, 2018). This is tense situation

in the UK as they do not have option to avoid this problem and this goes so longer time period.

This also increases the declining in the productivity and lower down the economic growth of the

UK. Many people in the country facing the problem of lacking of saving capacity and reduces

their borrowing power. Prices of all basics product increases and because of that it impact the

living standard of weaker section. Many changes has been made by the government to overcome

the problem of inflation rate.

short run equilibrium super-normal profit, normal profit and losses are possible because there is

loss barriers to entry and also having good knowledge. In the context of monopolist market the

need to be noted that marginal cost should be equal to the marginal cost and in short run, this

shows the maximisation in profit (El-Emam and Özcan, 2019). Under this competition, the

revenue curve is downward sloping because to sell more product, they tend to decrease their

prices. In short run, new firms not able to enter into the group and so that they cannot compete

super-normal profit in the firm.

Defining the inflation

Inflation refers to increasing in price level and decrease in the purchasing power of buyer

and that leads inefficiency in the economy. In the UK, this is also creates the problem among the

consumers as prices were rising and that reduces their saving capacity. This overall impact

negatively as this increases the imbalance between demand and supply in the country through

many reasons.

This reasons of inflation is Demand pull inflation in the UK, in the 1980s the UK

experiences rapid economic and through that government cut interest rate and cut taxes and

because of that house price rose up and that enhancing the positive wealth effect. This increases

the confidence and higher spending and lowering savings and that increase the borrowing. As,

result firm rise in inflation as they could not meet the demand and led in current deficit (Griffin,

Shockley and Mark, 2018). This is the reason of demand-pull inflation and this situation occur in

the case of Brexit issue in the country.

The second reason is falling in the sterling exchange rate that happens after the issue of

Brexit issue in the UK. In this, it effect the weaker section of consumer in the UK and it showed

that sterling exchange rate depreciated by 10% after 2016 (Margo, 2018). This is tense situation

in the UK as they do not have option to avoid this problem and this goes so longer time period.

This also increases the declining in the productivity and lower down the economic growth of the

UK. Many people in the country facing the problem of lacking of saving capacity and reduces

their borrowing power. Prices of all basics product increases and because of that it impact the

living standard of weaker section. Many changes has been made by the government to overcome

the problem of inflation rate.

Third reason of inflation rate in the UK is concerned with the higher prices in import as

this is states that imported goods and services will increase in process if exchange rate

depreciate. This also leads in increasing in the inflation rate as it firstly impact the businesses and

infrastructure of economy of UK. Through this, the company is not able to produces the product

at large level and that also reduces their inefficiency in the management. It somewhere als

negatively influence the consumer and reduces their purchasing power (Lee, Miguel and

Wolfram, 2020). To control this situation organisation has build up the some measurable action

that gives positive effect on the economy.

Analysing the cost of inflation

There are certain inflation cost are leads to lower down the investment capacity and

reduces the economic growth and also fall in the value their savings, This create imbalance in the

situation of economy and destroy confidence in the system. Some of the inflation cost are

Reduced international competitiveness, this country has relatively higher inflation rate

than trading partners. This create the export will become less competitive and decreases the

current account of UK. This is more important to concentrate on increasing in competitive

strength in the economy.

Confusion and uncertainty When there s increasing in the inflation then people where

confused about the where they need to spend their money. In the UK, if inflation is high than the

chances of firm has reduces in terms of investment and create the uncertainty about the future

prices, profits and cost. This also decreases the growth of economy of the UK and decreases the

purchasing power of costumer.

Income redistribution is another cost of inflation that make borrower better off and

decrease the stability of lender more worse as this tends to reduce the value in savings. Many

times savings are in the form of cash at bank and that decrease the low interest rate. In the UK,

the inflation impact the older people more as they were rely more on the savings, High rate

inflation reduce the real value and real income (Lybbert and Wydick, 2018). This influence the

working condition of many people has they were not able to fulfil their better standard of living.

Falling real incomes is termed as cost of inflation as this reduces the wages and pay

restraints has been experienced by UK. As in the period of 2010-2017 this has developed major

problem with the public sector workers an wages were limited by 1% . Through this, it observed

this is states that imported goods and services will increase in process if exchange rate

depreciate. This also leads in increasing in the inflation rate as it firstly impact the businesses and

infrastructure of economy of UK. Through this, the company is not able to produces the product

at large level and that also reduces their inefficiency in the management. It somewhere als

negatively influence the consumer and reduces their purchasing power (Lee, Miguel and

Wolfram, 2020). To control this situation organisation has build up the some measurable action

that gives positive effect on the economy.

Analysing the cost of inflation

There are certain inflation cost are leads to lower down the investment capacity and

reduces the economic growth and also fall in the value their savings, This create imbalance in the

situation of economy and destroy confidence in the system. Some of the inflation cost are

Reduced international competitiveness, this country has relatively higher inflation rate

than trading partners. This create the export will become less competitive and decreases the

current account of UK. This is more important to concentrate on increasing in competitive

strength in the economy.

Confusion and uncertainty When there s increasing in the inflation then people where

confused about the where they need to spend their money. In the UK, if inflation is high than the

chances of firm has reduces in terms of investment and create the uncertainty about the future

prices, profits and cost. This also decreases the growth of economy of the UK and decreases the

purchasing power of costumer.

Income redistribution is another cost of inflation that make borrower better off and

decrease the stability of lender more worse as this tends to reduce the value in savings. Many

times savings are in the form of cash at bank and that decrease the low interest rate. In the UK,

the inflation impact the older people more as they were rely more on the savings, High rate

inflation reduce the real value and real income (Lybbert and Wydick, 2018). This influence the

working condition of many people has they were not able to fulfil their better standard of living.

Falling real incomes is termed as cost of inflation as this reduces the wages and pay

restraints has been experienced by UK. As in the period of 2010-2017 this has developed major

problem with the public sector workers an wages were limited by 1% . Through this, it observed

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

that real fall in wages has impacted directly on workers and from which their life will going to

effect badly as they were highly dependable on their wages pay.

CONCLUSION

From the above essay it is concluded that economics is kind of study from that people

allocate scarce resources for production, distribution and consumption. There are two types of

economics micro and macro and both were concerned with efficiency in the production and

exchange and examine overall situation of country. In this report some short run cost such as

Total cost, Total Variable cost, Total fixed cost, Average cost, Marginal cost, Average fixed cost

has been critically examined and their relationship. It is evaluated the difference between the

short run equilibrium in monopolist and perfect competition and evaluate the many ways that

could be use in short run. Some certain reason of inflation rate such as Demand pull inflation,

Falling in the sterling exchange rate and increase in import prices is being studied and analysing

cost of inflation such as Reduced international competitiveness,Confusion and uncertainty,

Income redistribution and Falling real incomes.

effect badly as they were highly dependable on their wages pay.

CONCLUSION

From the above essay it is concluded that economics is kind of study from that people

allocate scarce resources for production, distribution and consumption. There are two types of

economics micro and macro and both were concerned with efficiency in the production and

exchange and examine overall situation of country. In this report some short run cost such as

Total cost, Total Variable cost, Total fixed cost, Average cost, Marginal cost, Average fixed cost

has been critically examined and their relationship. It is evaluated the difference between the

short run equilibrium in monopolist and perfect competition and evaluate the many ways that

could be use in short run. Some certain reason of inflation rate such as Demand pull inflation,

Falling in the sterling exchange rate and increase in import prices is being studied and analysing

cost of inflation such as Reduced international competitiveness,Confusion and uncertainty,

Income redistribution and Falling real incomes.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Anderegg, L. D. and et.al, 2018. Within‐species patterns challenge our understanding of the leaf

economics spectrum. Ecology letters. 21(5). pp.734-744.

Andor, M. A. and Fels, K. M., 2018. Behavioral economics and energy conservation–a

systematic review of non-price interventions and their causal effects. Ecological

Economics. 148. pp.178-210.

Banzhaf, S., Ma, L. and Timmins, C., 2019. Environmental justice: The economics of race,

place, and pollution. Journal of Economic Perspectives. 33(1). pp.185-208.

Baumers, M. and Holweg, M., 2019. On the economics of additive manufacturing: Experimental

findings. Journal of Operations Management. 65(8). pp.794-809.

Castillo-Vergara, M., Alvarez-Marin, A. and Placencio-Hidalgo, D., 2018. A bibliometric

analysis of creativity in the field of business economics. Journal of Business Research.

85. pp.1-9.

Christensen, G. and Miguel, E., 2018. Transparency, reproducibility, and the credibility of

economics research. Journal of Economic Literature. 56(3). pp.920-80.

El-Emam, R. S. and Özcan, H., 2019. Comprehensive review on the techno-economics of

sustainable large-scale clean hydrogen production. Journal of Cleaner Production, 220,

pp.593-609.

Griffin, T. W., Shockley, J. M. and Mark, T. B., 2018. Economics of precision

farming. Precision agriculture basics, pp.221-230.

Lee, K., Miguel, E. and Wolfram, C., 2020. Experimental evidence on the economics of rural

electrification. Journal of Political Economy. 128(4). pp.1523-1565.

Lybbert, T. J. and Wydick, B., 2018. Poverty, aspirations, and the economics of hope. Economic

Development and Cultural Change. 66(4). pp.709-753.

Margo, R. A., 2018. The integration of economic history into economics. Cliometrica. 12(3).

pp.377-406.

Spash, C. L., 2020. A tale of three paradigms: Realising the revolutionary potential of ecological

economics. Ecological Economics. 169. p.106518.

Thaler, R. H., 2018. From cashews to nudges: The evolution of behavioral economics. American

Economic Review, 108(6), pp.1265-87.

Zhang, Q. and et.al, 2018. Factors influencing the economics of public charging infrastructures

for EV–A review. Renewable and Sustainable Energy Reviews. 94. pp.500-509.

Books and Journals

Anderegg, L. D. and et.al, 2018. Within‐species patterns challenge our understanding of the leaf

economics spectrum. Ecology letters. 21(5). pp.734-744.

Andor, M. A. and Fels, K. M., 2018. Behavioral economics and energy conservation–a

systematic review of non-price interventions and their causal effects. Ecological

Economics. 148. pp.178-210.

Banzhaf, S., Ma, L. and Timmins, C., 2019. Environmental justice: The economics of race,

place, and pollution. Journal of Economic Perspectives. 33(1). pp.185-208.

Baumers, M. and Holweg, M., 2019. On the economics of additive manufacturing: Experimental

findings. Journal of Operations Management. 65(8). pp.794-809.

Castillo-Vergara, M., Alvarez-Marin, A. and Placencio-Hidalgo, D., 2018. A bibliometric

analysis of creativity in the field of business economics. Journal of Business Research.

85. pp.1-9.

Christensen, G. and Miguel, E., 2018. Transparency, reproducibility, and the credibility of

economics research. Journal of Economic Literature. 56(3). pp.920-80.

El-Emam, R. S. and Özcan, H., 2019. Comprehensive review on the techno-economics of

sustainable large-scale clean hydrogen production. Journal of Cleaner Production, 220,

pp.593-609.

Griffin, T. W., Shockley, J. M. and Mark, T. B., 2018. Economics of precision

farming. Precision agriculture basics, pp.221-230.

Lee, K., Miguel, E. and Wolfram, C., 2020. Experimental evidence on the economics of rural

electrification. Journal of Political Economy. 128(4). pp.1523-1565.

Lybbert, T. J. and Wydick, B., 2018. Poverty, aspirations, and the economics of hope. Economic

Development and Cultural Change. 66(4). pp.709-753.

Margo, R. A., 2018. The integration of economic history into economics. Cliometrica. 12(3).

pp.377-406.

Spash, C. L., 2020. A tale of three paradigms: Realising the revolutionary potential of ecological

economics. Ecological Economics. 169. p.106518.

Thaler, R. H., 2018. From cashews to nudges: The evolution of behavioral economics. American

Economic Review, 108(6), pp.1265-87.

Zhang, Q. and et.al, 2018. Factors influencing the economics of public charging infrastructures

for EV–A review. Renewable and Sustainable Energy Reviews. 94. pp.500-509.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.