Economics Alternative Assessment

Added on 2022-12-29

15 Pages3608 Words73 Views

Economics Alternative

Assessment

1

Assessment

1

Table of Contents

Introduction .....................................................................................................................................3

Microeconomics - Question 2:.........................................................................................................3

a) Relationships between short run costs................................................................................3

b) Difference between short run equilibrium of firms – one which operates as monopolist and

another operating under perfectly competitive market...........................................................8

Macroeconomics - Question 4:......................................................................................................10

a) Domestic final demand and its components.....................................................................10

b) GDP is not a perfect tool to measure welfare of people of a nation................................12

Conclusion.....................................................................................................................................13

References......................................................................................................................................14

2

Introduction .....................................................................................................................................3

Microeconomics - Question 2:.........................................................................................................3

a) Relationships between short run costs................................................................................3

b) Difference between short run equilibrium of firms – one which operates as monopolist and

another operating under perfectly competitive market...........................................................8

Macroeconomics - Question 4:......................................................................................................10

a) Domestic final demand and its components.....................................................................10

b) GDP is not a perfect tool to measure welfare of people of a nation................................12

Conclusion.....................................................................................................................................13

References......................................................................................................................................14

2

Introduction

Economics as a subject is concerned with activities related to products and services such

as production, distribution and consumption (Mäki, 2020). Study of economics can be bifurcated

into two categories – microeconomics and macroeconomics. Microeconomics is that segment of

economics which is concerned with study of individual market, industry or firm, their demand

and supply, price equilibrium, etc. while macroeconomics is that segment of economics which is

concerned with analysis of whole economy, general price level, inflation, deflation, national

income, etc. This essay is aimed at exploring various concepts related to microeconomics and

macroeconomics. In the microeconomics part, relationship between short run costs is explored

and difference between short run equilibrium of firms – one which operates as monopolist and

another operating under perfectly competitive market is discussed. Under the macroeconomics

section, various components of aggregate demands are explored. Further, discussions are made

on how GDP isn't a perfect tool to measure welfare of people of a nation.

Microeconomics - Question 2:

a) Relationships between short run costs

A firm employs several resources for the purpose of manufacturing goods and services.

These resources are known as factors of production. Factors of production can be bifurcated into

four categories which are land, labour, capital and entrepreneurship. Out of these factors of

production, income from land is known as rent, income of labour is known as wages and income

earned by capital owners is known as interest (Shute, 2016). Entrepreneur combines all the other

factors of production to earn income which is known as profit. Cost is that monetary value which

a firm has to incur for the purpose of manufacturing goods and services using above-mentioned

factors of production. In microeconomics while dealing with the production function of an

individual firm, costs incurred is divided into fixed costs and variable costs. Fixed costs is that

cost which is independent of quantity of output produced and therefore, is constant in nature.

Variable cost is that cost which is dependent on the defined amount of production and therefore,

is variable in nature (Puttaswamaiah, 2018). Fixed cost and changeable cost of a firm combined

together forms total cost of a firm i.e. at a defined amount of production, sum of the fixed cost

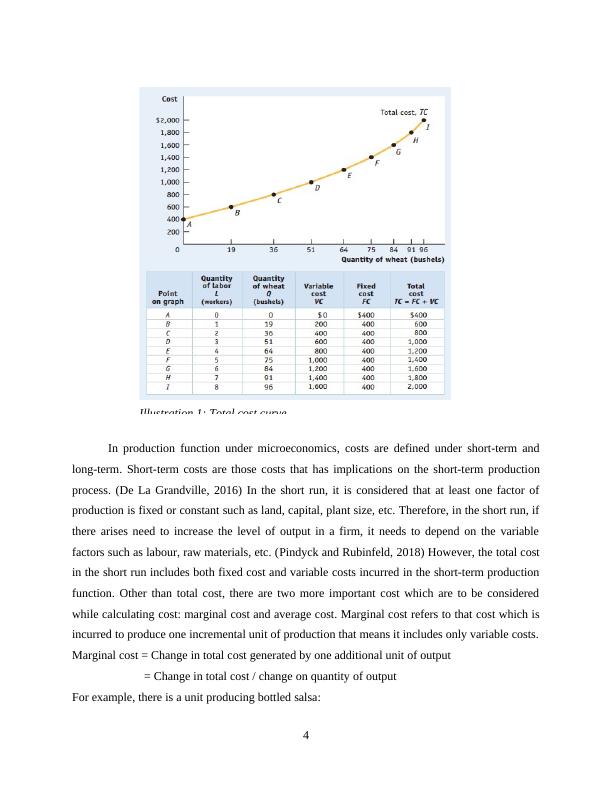

and changeable costs of production is known as total cost of production. Below mentioned is cost

function in a wheat producing farm:

3

Economics as a subject is concerned with activities related to products and services such

as production, distribution and consumption (Mäki, 2020). Study of economics can be bifurcated

into two categories – microeconomics and macroeconomics. Microeconomics is that segment of

economics which is concerned with study of individual market, industry or firm, their demand

and supply, price equilibrium, etc. while macroeconomics is that segment of economics which is

concerned with analysis of whole economy, general price level, inflation, deflation, national

income, etc. This essay is aimed at exploring various concepts related to microeconomics and

macroeconomics. In the microeconomics part, relationship between short run costs is explored

and difference between short run equilibrium of firms – one which operates as monopolist and

another operating under perfectly competitive market is discussed. Under the macroeconomics

section, various components of aggregate demands are explored. Further, discussions are made

on how GDP isn't a perfect tool to measure welfare of people of a nation.

Microeconomics - Question 2:

a) Relationships between short run costs

A firm employs several resources for the purpose of manufacturing goods and services.

These resources are known as factors of production. Factors of production can be bifurcated into

four categories which are land, labour, capital and entrepreneurship. Out of these factors of

production, income from land is known as rent, income of labour is known as wages and income

earned by capital owners is known as interest (Shute, 2016). Entrepreneur combines all the other

factors of production to earn income which is known as profit. Cost is that monetary value which

a firm has to incur for the purpose of manufacturing goods and services using above-mentioned

factors of production. In microeconomics while dealing with the production function of an

individual firm, costs incurred is divided into fixed costs and variable costs. Fixed costs is that

cost which is independent of quantity of output produced and therefore, is constant in nature.

Variable cost is that cost which is dependent on the defined amount of production and therefore,

is variable in nature (Puttaswamaiah, 2018). Fixed cost and changeable cost of a firm combined

together forms total cost of a firm i.e. at a defined amount of production, sum of the fixed cost

and changeable costs of production is known as total cost of production. Below mentioned is cost

function in a wheat producing farm:

3

In production function under microeconomics, costs are defined under short-term and

long-term. Short-term costs are those costs that has implications on the short-term production

process. (De La Grandville, 2016) In the short run, it is considered that at least one factor of

production is fixed or constant such as land, capital, plant size, etc. Therefore, in the short run, if

there arises need to increase the level of output in a firm, it needs to depend on the variable

factors such as labour, raw materials, etc. (Pindyck and Rubinfeld, 2018) However, the total cost

in the short run includes both fixed cost and variable costs incurred in the short-term production

function. Other than total cost, there are two more important cost which are to be considered

while calculating cost: marginal cost and average cost. Marginal cost refers to that cost which is

incurred to produce one incremental unit of production that means it includes only variable costs.

Marginal cost = Change in total cost generated by one additional unit of output

= Change in total cost / change on quantity of output

For example, there is a unit producing bottled salsa:

4

Illustration 1: Total cost curve

long-term. Short-term costs are those costs that has implications on the short-term production

process. (De La Grandville, 2016) In the short run, it is considered that at least one factor of

production is fixed or constant such as land, capital, plant size, etc. Therefore, in the short run, if

there arises need to increase the level of output in a firm, it needs to depend on the variable

factors such as labour, raw materials, etc. (Pindyck and Rubinfeld, 2018) However, the total cost

in the short run includes both fixed cost and variable costs incurred in the short-term production

function. Other than total cost, there are two more important cost which are to be considered

while calculating cost: marginal cost and average cost. Marginal cost refers to that cost which is

incurred to produce one incremental unit of production that means it includes only variable costs.

Marginal cost = Change in total cost generated by one additional unit of output

= Change in total cost / change on quantity of output

For example, there is a unit producing bottled salsa:

4

Illustration 1: Total cost curve

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Managerial Economics Assignment | Economics Assignmentlg...

|12

|1408

|107

Economics for Businesslg...

|23

|5441

|9

Relationship between Short Run Cost and Equilibrium in Perfect Competition and Monopolylg...

|11

|2994

|1

Microeconomicslg...

|8

|756

|57

Economic Analysis - Assignment Samplelg...

|16

|2549

|123

Principles of Microeconomics Assignmentlg...

|13

|2832

|54