Economics and Finance Report: Financial Analysis and Strategies

VerifiedAdded on 2019/11/08

|12

|2114

|154

Report

AI Summary

This report provides a comprehensive analysis of a capital investment project, focusing on financial details and strategic planning. It begins by defining and describing key aspects of investment, including capital expenditures, raw materials, and cash for operations. The report then presents detailed financial projections, including profit and loss statements, cost projections, and cash flow analysis, alongside the calculation of Internal Rate of Return (IRR). Furthermore, it identifies and assesses potential opportunities and threats associated with the investment, using a smart watch manufacturing company as a case study, and proposes actions to mitigate identified risks. Finally, the report outlines operating plans and strategies essential for the success of a manufacturing business venture, emphasizing the importance of budget alignment with corporate strategy, strategic resource allocation, performance incentives, budget flexibility, and simplicity.

Running head: ECONOMICS AND FINANCE

Economics and Finance

Student’s Name:

University Name:

Author Note

Economics and Finance

Student’s Name:

University Name:

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ECONOMICS AND FINANCE

Table of Contents

Investment Detail.......................................................................................................................2

Opportunities and Threats..........................................................................................................3

Operating Plans / Strategies.......................................................................................................5

References..................................................................................................................................6

Table of Contents

Investment Detail.......................................................................................................................2

Opportunities and Threats..........................................................................................................3

Operating Plans / Strategies.......................................................................................................5

References..................................................................................................................................6

2ECONOMICS AND FINANCE

Investment Detail

The capital investment project is of utmost importance in relation to investment

control. The purpose of capital investment project is to check and measure the acceptability

of the project in terms of the benefit it generates.

The aspects of the investment project that have been asked to identify and describe are

Capital Expenditures, Raw Materials and Cash for operations.

Capital Expenditures can be defined as those expenditures whose perks are to be

considered for a time period more than one year. Capital expenditures do not get created very

often, but they are essentially for larger sums of money. Capital Budgeting or Capital

Expenditure Analysis involves determining the value potential of a project/investment. This

is known as Net Present Value (Cvijanović, 2014). Capital Expenditure can be divided into

three different forms that are cost reducing expenditures, increasing the revenue related

expenditures and non-economic expenditures. In simple terms of accounting, a particular

expenditure is said to be a capital expenditure when a capital asset is purchased or a specific

investment is incurred that extends the utilizable life of the capital asset. The value of capital

expenditures a firm will most probably incur is dependent on the type of industry it occupies

(Cho, Freedman & Patten, 2012).

Raw materials are essentially substances that are used in the primary manufacturing of

inventory or goods. Raw Materials have a totally different or separate market which is called

the factor market, as raw materials are primarily factors of production including capital and

labor (Kingsman, 2014). In more simple accounting terms, when the raw materials are used,

there is a reduction in the raw materials inventory and simultaneously the work in progress

account increases and finally transferred to the finished goods (Tung, 2012).

Investment Detail

The capital investment project is of utmost importance in relation to investment

control. The purpose of capital investment project is to check and measure the acceptability

of the project in terms of the benefit it generates.

The aspects of the investment project that have been asked to identify and describe are

Capital Expenditures, Raw Materials and Cash for operations.

Capital Expenditures can be defined as those expenditures whose perks are to be

considered for a time period more than one year. Capital expenditures do not get created very

often, but they are essentially for larger sums of money. Capital Budgeting or Capital

Expenditure Analysis involves determining the value potential of a project/investment. This

is known as Net Present Value (Cvijanović, 2014). Capital Expenditure can be divided into

three different forms that are cost reducing expenditures, increasing the revenue related

expenditures and non-economic expenditures. In simple terms of accounting, a particular

expenditure is said to be a capital expenditure when a capital asset is purchased or a specific

investment is incurred that extends the utilizable life of the capital asset. The value of capital

expenditures a firm will most probably incur is dependent on the type of industry it occupies

(Cho, Freedman & Patten, 2012).

Raw materials are essentially substances that are used in the primary manufacturing of

inventory or goods. Raw Materials have a totally different or separate market which is called

the factor market, as raw materials are primarily factors of production including capital and

labor (Kingsman, 2014). In more simple accounting terms, when the raw materials are used,

there is a reduction in the raw materials inventory and simultaneously the work in progress

account increases and finally transferred to the finished goods (Tung, 2012).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ECONOMICS AND FINANCE

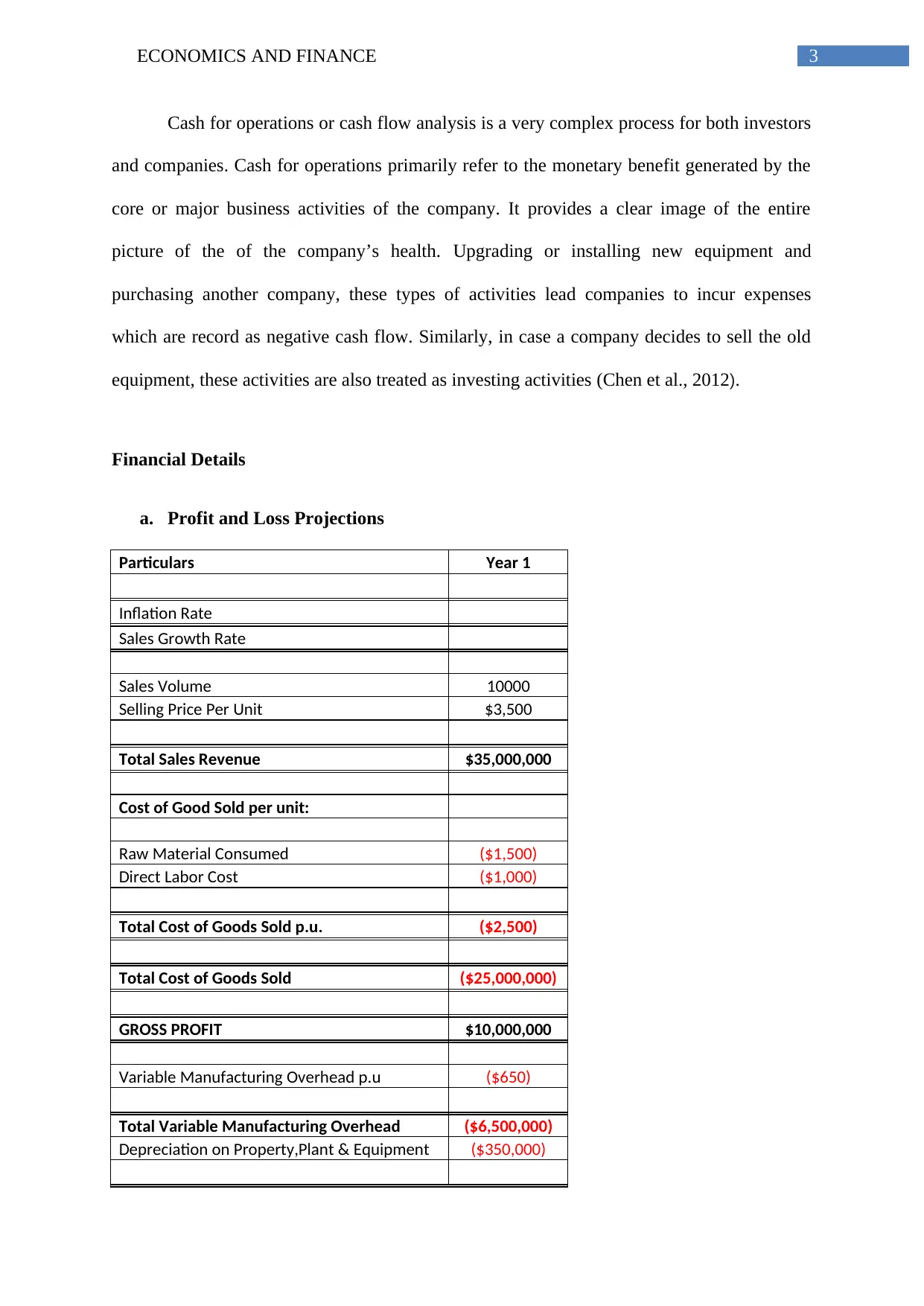

Cash for operations or cash flow analysis is a very complex process for both investors

and companies. Cash for operations primarily refer to the monetary benefit generated by the

core or major business activities of the company. It provides a clear image of the entire

picture of the of the company’s health. Upgrading or installing new equipment and

purchasing another company, these types of activities lead companies to incur expenses

which are record as negative cash flow. Similarly, in case a company decides to sell the old

equipment, these activities are also treated as investing activities (Chen et al., 2012).

Financial Details

a. Profit and Loss Projections

Particulars Year 1

Inflation Rate

Sales Growth Rate

Sales Volume 10000

Selling Price Per Unit $3,500

Total Sales Revenue $35,000,000

Cost of Good Sold per unit:

Raw Material Consumed ($1,500)

Direct Labor Cost ($1,000)

Total Cost of Goods Sold p.u. ($2,500)

Total Cost of Goods Sold ($25,000,000)

GROSS PROFIT $10,000,000

Variable Manufacturing Overhead p.u ($650)

Total Variable Manufacturing Overhead ($6,500,000)

Depreciation on Property,Plant & Equipment ($350,000)

Cash for operations or cash flow analysis is a very complex process for both investors

and companies. Cash for operations primarily refer to the monetary benefit generated by the

core or major business activities of the company. It provides a clear image of the entire

picture of the of the company’s health. Upgrading or installing new equipment and

purchasing another company, these types of activities lead companies to incur expenses

which are record as negative cash flow. Similarly, in case a company decides to sell the old

equipment, these activities are also treated as investing activities (Chen et al., 2012).

Financial Details

a. Profit and Loss Projections

Particulars Year 1

Inflation Rate

Sales Growth Rate

Sales Volume 10000

Selling Price Per Unit $3,500

Total Sales Revenue $35,000,000

Cost of Good Sold per unit:

Raw Material Consumed ($1,500)

Direct Labor Cost ($1,000)

Total Cost of Goods Sold p.u. ($2,500)

Total Cost of Goods Sold ($25,000,000)

GROSS PROFIT $10,000,000

Variable Manufacturing Overhead p.u ($650)

Total Variable Manufacturing Overhead ($6,500,000)

Depreciation on Property,Plant & Equipment ($350,000)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ECONOMICS AND FINANCE

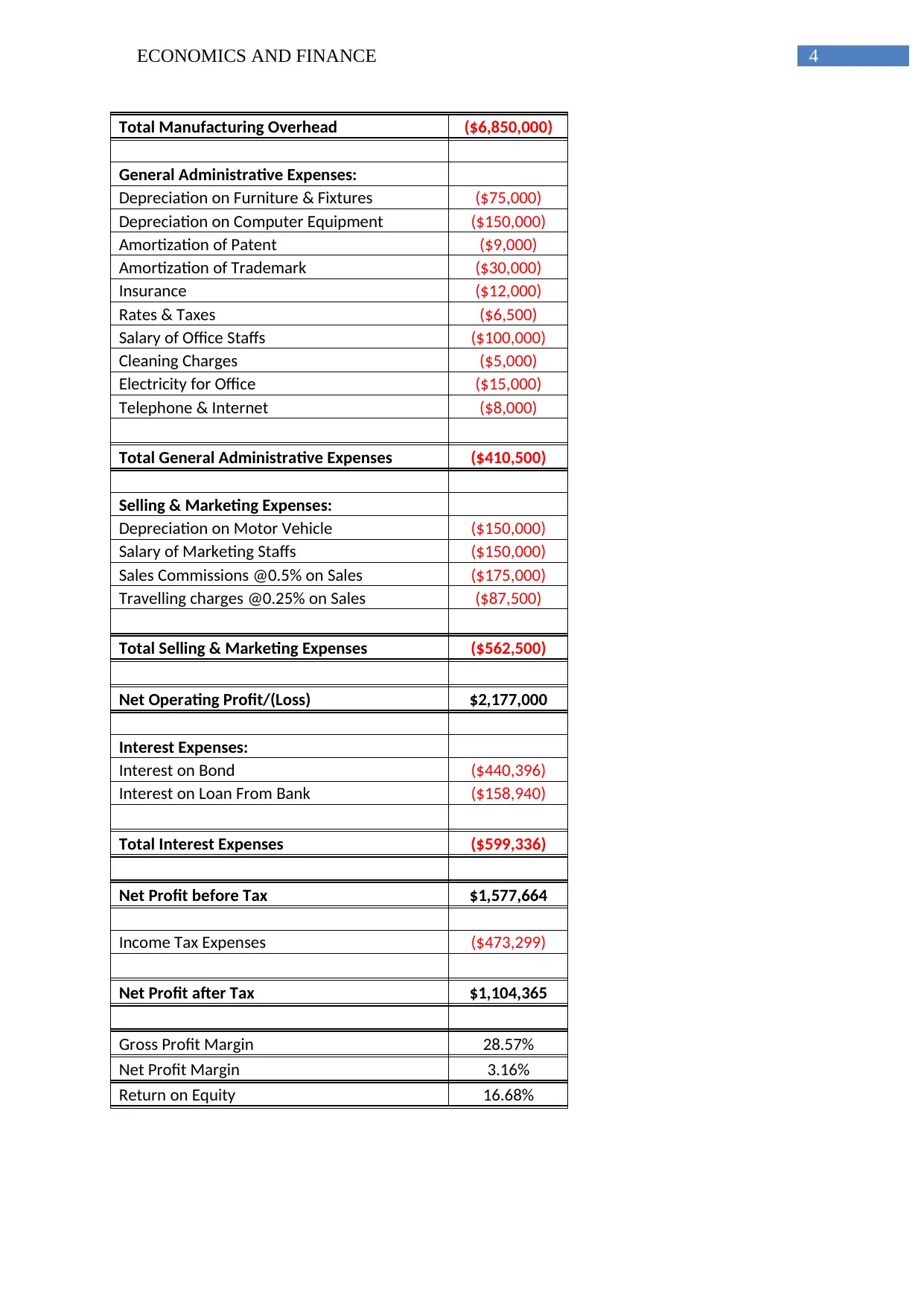

Total Manufacturing Overhead ($6,850,000)

General Administrative Expenses:

Depreciation on Furniture & Fixtures ($75,000)

Depreciation on Computer Equipment ($150,000)

Amortization of Patent ($9,000)

Amortization of Trademark ($30,000)

Insurance ($12,000)

Rates & Taxes ($6,500)

Salary of Office Staffs ($100,000)

Cleaning Charges ($5,000)

Electricity for Office ($15,000)

Telephone & Internet ($8,000)

Total General Administrative Expenses ($410,500)

Selling & Marketing Expenses:

Depreciation on Motor Vehicle ($150,000)

Salary of Marketing Staffs ($150,000)

Sales Commissions @0.5% on Sales ($175,000)

Travelling charges @0.25% on Sales ($87,500)

Total Selling & Marketing Expenses ($562,500)

Net Operating Profit/(Loss) $2,177,000

Interest Expenses:

Interest on Bond ($440,396)

Interest on Loan From Bank ($158,940)

Total Interest Expenses ($599,336)

Net Profit before Tax $1,577,664

Income Tax Expenses ($473,299)

Net Profit after Tax $1,104,365

Gross Profit Margin 28.57%

Net Profit Margin 3.16%

Return on Equity 16.68%

Total Manufacturing Overhead ($6,850,000)

General Administrative Expenses:

Depreciation on Furniture & Fixtures ($75,000)

Depreciation on Computer Equipment ($150,000)

Amortization of Patent ($9,000)

Amortization of Trademark ($30,000)

Insurance ($12,000)

Rates & Taxes ($6,500)

Salary of Office Staffs ($100,000)

Cleaning Charges ($5,000)

Electricity for Office ($15,000)

Telephone & Internet ($8,000)

Total General Administrative Expenses ($410,500)

Selling & Marketing Expenses:

Depreciation on Motor Vehicle ($150,000)

Salary of Marketing Staffs ($150,000)

Sales Commissions @0.5% on Sales ($175,000)

Travelling charges @0.25% on Sales ($87,500)

Total Selling & Marketing Expenses ($562,500)

Net Operating Profit/(Loss) $2,177,000

Interest Expenses:

Interest on Bond ($440,396)

Interest on Loan From Bank ($158,940)

Total Interest Expenses ($599,336)

Net Profit before Tax $1,577,664

Income Tax Expenses ($473,299)

Net Profit after Tax $1,104,365

Gross Profit Margin 28.57%

Net Profit Margin 3.16%

Return on Equity 16.68%

5ECONOMICS AND FINANCE

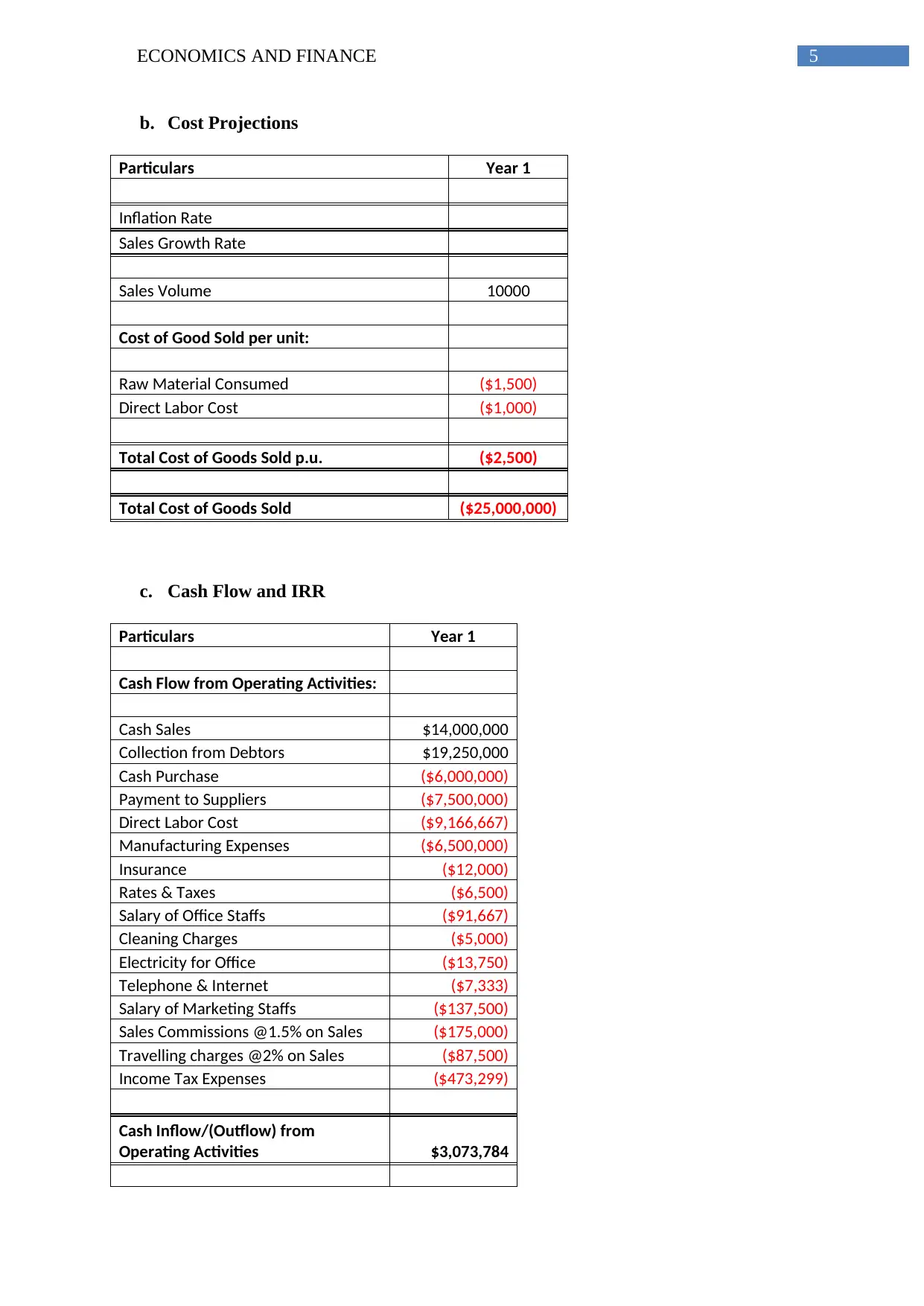

b. Cost Projections

Particulars Year 1

Inflation Rate

Sales Growth Rate

Sales Volume 10000

Cost of Good Sold per unit:

Raw Material Consumed ($1,500)

Direct Labor Cost ($1,000)

Total Cost of Goods Sold p.u. ($2,500)

Total Cost of Goods Sold ($25,000,000)

c. Cash Flow and IRR

Particulars Year 1

Cash Flow from Operating Activities:

Cash Sales $14,000,000

Collection from Debtors $19,250,000

Cash Purchase ($6,000,000)

Payment to Suppliers ($7,500,000)

Direct Labor Cost ($9,166,667)

Manufacturing Expenses ($6,500,000)

Insurance ($12,000)

Rates & Taxes ($6,500)

Salary of Office Staffs ($91,667)

Cleaning Charges ($5,000)

Electricity for Office ($13,750)

Telephone & Internet ($7,333)

Salary of Marketing Staffs ($137,500)

Sales Commissions @1.5% on Sales ($175,000)

Travelling charges @2% on Sales ($87,500)

Income Tax Expenses ($473,299)

Cash Inflow/(Outflow) from

Operating Activities $3,073,784

b. Cost Projections

Particulars Year 1

Inflation Rate

Sales Growth Rate

Sales Volume 10000

Cost of Good Sold per unit:

Raw Material Consumed ($1,500)

Direct Labor Cost ($1,000)

Total Cost of Goods Sold p.u. ($2,500)

Total Cost of Goods Sold ($25,000,000)

c. Cash Flow and IRR

Particulars Year 1

Cash Flow from Operating Activities:

Cash Sales $14,000,000

Collection from Debtors $19,250,000

Cash Purchase ($6,000,000)

Payment to Suppliers ($7,500,000)

Direct Labor Cost ($9,166,667)

Manufacturing Expenses ($6,500,000)

Insurance ($12,000)

Rates & Taxes ($6,500)

Salary of Office Staffs ($91,667)

Cleaning Charges ($5,000)

Electricity for Office ($13,750)

Telephone & Internet ($7,333)

Salary of Marketing Staffs ($137,500)

Sales Commissions @1.5% on Sales ($175,000)

Travelling charges @2% on Sales ($87,500)

Income Tax Expenses ($473,299)

Cash Inflow/(Outflow) from

Operating Activities $3,073,784

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

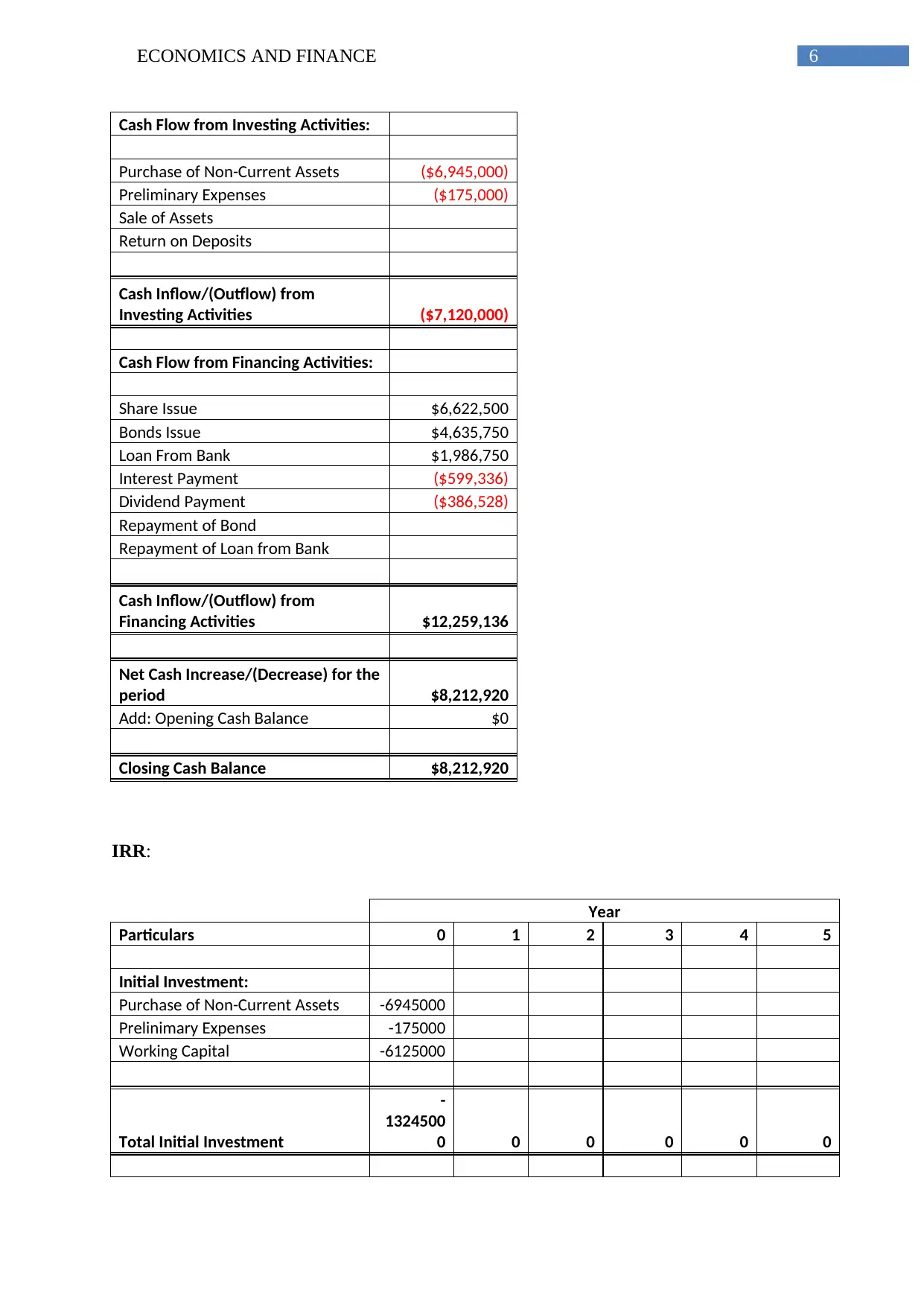

6ECONOMICS AND FINANCE

Cash Flow from Investing Activities:

Purchase of Non-Current Assets ($6,945,000)

Preliminary Expenses ($175,000)

Sale of Assets

Return on Deposits

Cash Inflow/(Outflow) from

Investing Activities ($7,120,000)

Cash Flow from Financing Activities:

Share Issue $6,622,500

Bonds Issue $4,635,750

Loan From Bank $1,986,750

Interest Payment ($599,336)

Dividend Payment ($386,528)

Repayment of Bond

Repayment of Loan from Bank

Cash Inflow/(Outflow) from

Financing Activities $12,259,136

Net Cash Increase/(Decrease) for the

period $8,212,920

Add: Opening Cash Balance $0

Closing Cash Balance $8,212,920

IRR:

Year

Particulars 0 1 2 3 4 5

Initial Investment:

Purchase of Non-Current Assets -6945000

Prelinimary Expenses -175000

Working Capital -6125000

Total Initial Investment

-

1324500

0 0 0 0 0 0

Cash Flow from Investing Activities:

Purchase of Non-Current Assets ($6,945,000)

Preliminary Expenses ($175,000)

Sale of Assets

Return on Deposits

Cash Inflow/(Outflow) from

Investing Activities ($7,120,000)

Cash Flow from Financing Activities:

Share Issue $6,622,500

Bonds Issue $4,635,750

Loan From Bank $1,986,750

Interest Payment ($599,336)

Dividend Payment ($386,528)

Repayment of Bond

Repayment of Loan from Bank

Cash Inflow/(Outflow) from

Financing Activities $12,259,136

Net Cash Increase/(Decrease) for the

period $8,212,920

Add: Opening Cash Balance $0

Closing Cash Balance $8,212,920

IRR:

Year

Particulars 0 1 2 3 4 5

Initial Investment:

Purchase of Non-Current Assets -6945000

Prelinimary Expenses -175000

Working Capital -6125000

Total Initial Investment

-

1324500

0 0 0 0 0 0

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ECONOMICS AND FINANCE

Net Opearting Profit before Tax 0

217700

0

250959

4 2850499

320419

4 3574794

Less: Income Tax 0 653100 752878 855150 961258 1072438

Net Operating Profit after Tax 0

283010

0

326247

3 3705649

416545

3 4647232

Add: Depreciation & Amortization 0 764000 692750

635187.

5 588659 551030

Net Operating Cash Flow 0

359410

0

395522

3 4340836

475411

2 5198263

Terminal Value:

Sale of Non-Current Assets 1125000

Recovery of Preliminary Expenses 17500

Recovery of Working Capital 6125000

Total Terminal Value 0 0 0 0 0 7267500

Net Annual Cash Flow

-

1324500

0

359410

0

395522

3 4340836

475411

2

1246576

3

Discount Rate (WACC) 8.17% 8.17% 8.17% 8.17% 8.17% 8.17%

Discounted Cash Flow

-

1324500

0

332271

7

338047

2 3429912

347282

0 8418503

IRR 16.71%

Opportunities and Threats

For the easy understanding of the opportunities and threats that are related to

venturing into an investment project, the investment in a smart watch manufacturing

company is taken into consideration (Bundy, Shropshire & Buchholtz, 2013).

OPPORTUNITIES IMPACT ON GROSS INCOME

Net Opearting Profit before Tax 0

217700

0

250959

4 2850499

320419

4 3574794

Less: Income Tax 0 653100 752878 855150 961258 1072438

Net Operating Profit after Tax 0

283010

0

326247

3 3705649

416545

3 4647232

Add: Depreciation & Amortization 0 764000 692750

635187.

5 588659 551030

Net Operating Cash Flow 0

359410

0

395522

3 4340836

475411

2 5198263

Terminal Value:

Sale of Non-Current Assets 1125000

Recovery of Preliminary Expenses 17500

Recovery of Working Capital 6125000

Total Terminal Value 0 0 0 0 0 7267500

Net Annual Cash Flow

-

1324500

0

359410

0

395522

3 4340836

475411

2

1246576

3

Discount Rate (WACC) 8.17% 8.17% 8.17% 8.17% 8.17% 8.17%

Discounted Cash Flow

-

1324500

0

332271

7

338047

2 3429912

347282

0 8418503

IRR 16.71%

Opportunities and Threats

For the easy understanding of the opportunities and threats that are related to

venturing into an investment project, the investment in a smart watch manufacturing

company is taken into consideration (Bundy, Shropshire & Buchholtz, 2013).

OPPORTUNITIES IMPACT ON GROSS INCOME

8ECONOMICS AND FINANCE

1. Infrastructure capitalization and

increase in research and

development.

2. Emerging departments which lead

to further innovations and help to

shape up the economy.

3. Environmental assets in abundance

in order to increase the

productivity.

4. The existing physical assets and

social capital which have a great

potential of growth with extra

investment will lead to

enhancement of profit.

5. Interest collected on further

investments will lead to economic

growth.

Gross Income will increase and IRR will

decrease.

Gross Income will increase and IRR will

decrease.

Gross Income will increase and IRR will

decrease.

Gross Income will increase and IRR will

decrease.

Gross Income will increase and IRR will

decrease.

THREATS

1. External and internal connectivity

issues.

2. Unable to clearly figure out the

loopholes in strategic planning that

leads to blockage in further

development.

IMPACT ON GROSS INCOME

Gross Income will decrease and IRR will

increase.

Gross Income will decrease and IRR will

increase.

1. Infrastructure capitalization and

increase in research and

development.

2. Emerging departments which lead

to further innovations and help to

shape up the economy.

3. Environmental assets in abundance

in order to increase the

productivity.

4. The existing physical assets and

social capital which have a great

potential of growth with extra

investment will lead to

enhancement of profit.

5. Interest collected on further

investments will lead to economic

growth.

Gross Income will increase and IRR will

decrease.

Gross Income will increase and IRR will

decrease.

Gross Income will increase and IRR will

decrease.

Gross Income will increase and IRR will

decrease.

Gross Income will increase and IRR will

decrease.

THREATS

1. External and internal connectivity

issues.

2. Unable to clearly figure out the

loopholes in strategic planning that

leads to blockage in further

development.

IMPACT ON GROSS INCOME

Gross Income will decrease and IRR will

increase.

Gross Income will decrease and IRR will

increase.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ECONOMICS AND FINANCE

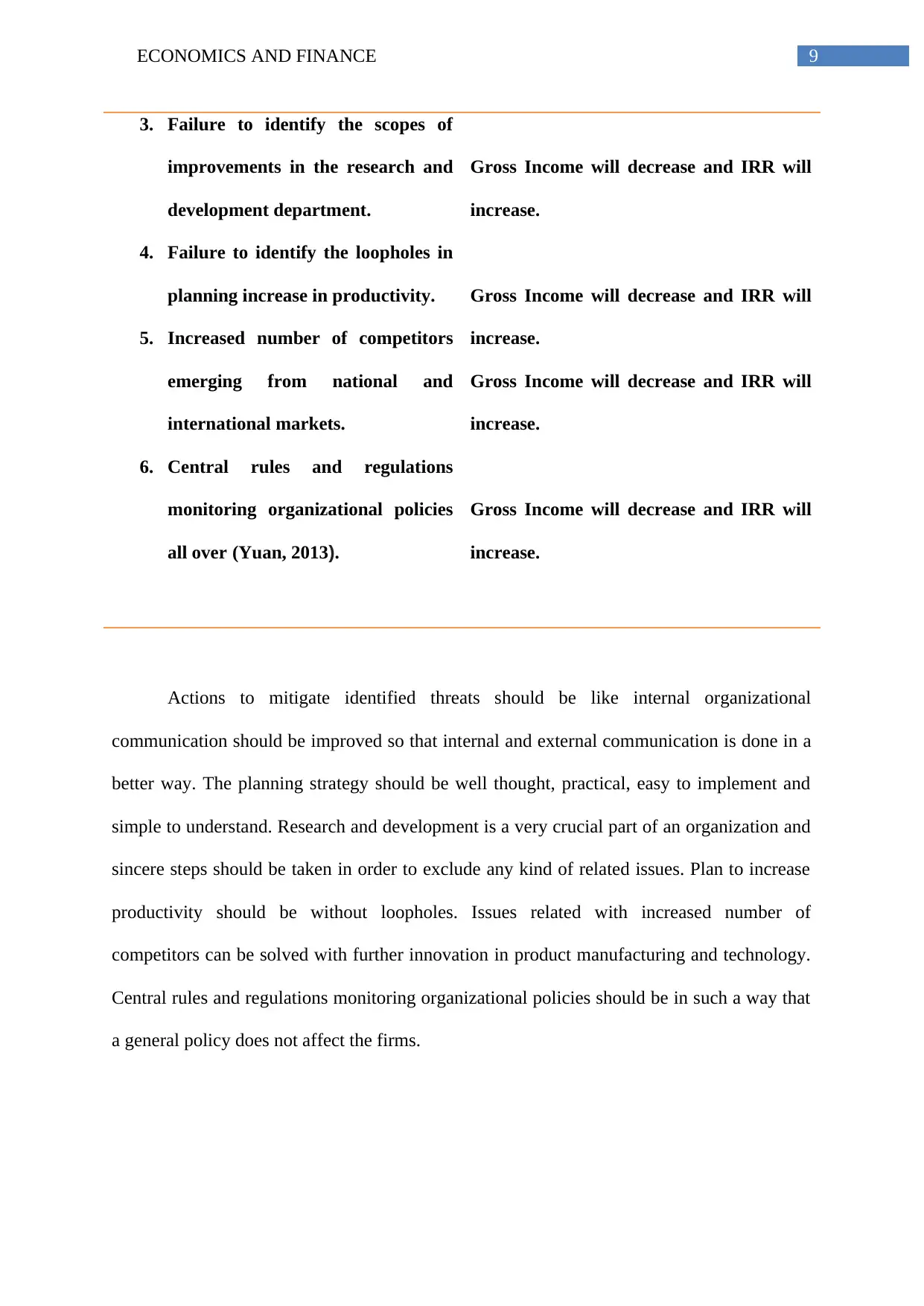

3. Failure to identify the scopes of

improvements in the research and

development department.

4. Failure to identify the loopholes in

planning increase in productivity.

5. Increased number of competitors

emerging from national and

international markets.

6. Central rules and regulations

monitoring organizational policies

all over (Yuan, 2013).

Gross Income will decrease and IRR will

increase.

Gross Income will decrease and IRR will

increase.

Gross Income will decrease and IRR will

increase.

Gross Income will decrease and IRR will

increase.

Actions to mitigate identified threats should be like internal organizational

communication should be improved so that internal and external communication is done in a

better way. The planning strategy should be well thought, practical, easy to implement and

simple to understand. Research and development is a very crucial part of an organization and

sincere steps should be taken in order to exclude any kind of related issues. Plan to increase

productivity should be without loopholes. Issues related with increased number of

competitors can be solved with further innovation in product manufacturing and technology.

Central rules and regulations monitoring organizational policies should be in such a way that

a general policy does not affect the firms.

3. Failure to identify the scopes of

improvements in the research and

development department.

4. Failure to identify the loopholes in

planning increase in productivity.

5. Increased number of competitors

emerging from national and

international markets.

6. Central rules and regulations

monitoring organizational policies

all over (Yuan, 2013).

Gross Income will decrease and IRR will

increase.

Gross Income will decrease and IRR will

increase.

Gross Income will decrease and IRR will

increase.

Gross Income will decrease and IRR will

increase.

Actions to mitigate identified threats should be like internal organizational

communication should be improved so that internal and external communication is done in a

better way. The planning strategy should be well thought, practical, easy to implement and

simple to understand. Research and development is a very crucial part of an organization and

sincere steps should be taken in order to exclude any kind of related issues. Plan to increase

productivity should be without loopholes. Issues related with increased number of

competitors can be solved with further innovation in product manufacturing and technology.

Central rules and regulations monitoring organizational policies should be in such a way that

a general policy does not affect the firms.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ECONOMICS AND FINANCE

Operating Plans / Strategies

The operating plan for a successful manufacturing business venture is that the budget

development plan should be linked with corporate strategy. This is because the budget

constitutes of the plans and strategies linked with evaluating the productivity, revenues and

other expected losses, thus the corporate strategy should be framed in such a way that it is in

accordance with the budget planning.

Resources should be allocated in a strategic manner so as to ensure optimum

utilization of all the resources.

Affix incentives to measure the performance hike so that the employees are motivated

in such a way that they perform in the best manner.

The next measure should be that the budget complexity should be reduced that is the

allocation decisions should be taken quickly, targets should be achieved in less time and

organizational operations should be carried out without further disturbance.

The budget should also be flexible in order to accommodate change (Bullinger &

Warschat, 2012).

Operating Plans / Strategies

The operating plan for a successful manufacturing business venture is that the budget

development plan should be linked with corporate strategy. This is because the budget

constitutes of the plans and strategies linked with evaluating the productivity, revenues and

other expected losses, thus the corporate strategy should be framed in such a way that it is in

accordance with the budget planning.

Resources should be allocated in a strategic manner so as to ensure optimum

utilization of all the resources.

Affix incentives to measure the performance hike so that the employees are motivated

in such a way that they perform in the best manner.

The next measure should be that the budget complexity should be reduced that is the

allocation decisions should be taken quickly, targets should be achieved in less time and

organizational operations should be carried out without further disturbance.

The budget should also be flexible in order to accommodate change (Bullinger &

Warschat, 2012).

11ECONOMICS AND FINANCE

References

Bullinger, H. J., & Warschat, J. (Eds.). (2012). Concurrent simultaneous engineering

systems: the way to successful product development. Springer Science & Business

Media.

Bundy, J., Shropshire, C., & Buchholtz, A. K. (2013). Strategic cognition and issue salience:

Toward an explanation of firm responsiveness to stakeholder concerns. Academy of

Management Review, 38(3), 352-376.

Chen, Q., Chen, X., Schipper, K., Xu, Y., & Xue, J. (2012). The sensitivity of corporate cash

holdings to corporate governance. The Review of Financial Studies, 25(12), 3610-

3644.

Cho, C. H., Freedman, M., & Patten, D. M. (2012). Corporate disclosure of environmental

capital expenditures: A test of alternative theories. Accounting, Auditing &

Accountability Journal, 25(3), 486-507.

Cvijanović, D. (2014). Real estate prices and firm capital structure. The Review of Financial

Studies, 27(9), 2690-2735.

Kingsman, B. G. (2014). Raw materials purchasing: an operational research approach (Vol.

4). Elsevier.

Tung, J. (2012). A study of product innovation on firm performance. International Journal of

Organizational Innovation (Online), 4(3), 84.

Yuan, H. (2013). A SWOT analysis of successful construction waste management. Journal of

Cleaner Production, 39, 1-8.

References

Bullinger, H. J., & Warschat, J. (Eds.). (2012). Concurrent simultaneous engineering

systems: the way to successful product development. Springer Science & Business

Media.

Bundy, J., Shropshire, C., & Buchholtz, A. K. (2013). Strategic cognition and issue salience:

Toward an explanation of firm responsiveness to stakeholder concerns. Academy of

Management Review, 38(3), 352-376.

Chen, Q., Chen, X., Schipper, K., Xu, Y., & Xue, J. (2012). The sensitivity of corporate cash

holdings to corporate governance. The Review of Financial Studies, 25(12), 3610-

3644.

Cho, C. H., Freedman, M., & Patten, D. M. (2012). Corporate disclosure of environmental

capital expenditures: A test of alternative theories. Accounting, Auditing &

Accountability Journal, 25(3), 486-507.

Cvijanović, D. (2014). Real estate prices and firm capital structure. The Review of Financial

Studies, 27(9), 2690-2735.

Kingsman, B. G. (2014). Raw materials purchasing: an operational research approach (Vol.

4). Elsevier.

Tung, J. (2012). A study of product innovation on firm performance. International Journal of

Organizational Innovation (Online), 4(3), 84.

Yuan, H. (2013). A SWOT analysis of successful construction waste management. Journal of

Cleaner Production, 39, 1-8.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.