ECO511 Economics Assignment: Monopoly in Australian Banking

VerifiedAdded on 2022/12/29

|12

|2908

|1

Essay

AI Summary

This economics assignment examines the monopoly structure within the Australian banking sector, focusing on the influence of major banks and the role of the Australian Competition and Consumer Commission (ACCC). The assignment delves into issues such as cartel behavior, high interest rates, an...

Running Head: ECONOMICS ASSIGNMENT

Economics Assignment

Name of Student:

Name of University:

Author’s Note:

Economics Assignment

Name of Student:

Name of University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ECONOMICS ASSIGNMENT

Introduction

The market structure in Australia is in nature of Monopoly. Most of the service sectors

operates together starting with the industry for retail banking. The banks actively work together

and share the profits among themselves. The Australian Competition and Consumer Commission

(ACCC) has two most important query regarding the competition in banking industry.

ACCC Chairman, Rod Sims has addressed that the sections addresses the oligopoly

market structure of the banking industry. Yet, the cases of the banks formation of cartel is not

alleged. Till date the market structure is influenced by mainly four banks creating monopoly

power. However, that is not the only concerned case because there are other factors that comes

into existence and effectively challenging the banks. Simon has also mentioned how the ACCC

findings on exchange would be analytical to understand the type of competition (Altman &

Ward, 2018). The aim of this paper is to understand the working structure of Australian banks

and the suitable measures to be taken in order to solve the issues of monopoly banking sector.

Australian Competition and Consumer Commission (ACCC)

The commission is an autonomous authority of the Australian government, established in

1905. The prime objective is to look after the business rights, consumer rights, regulation of

industries, monitoring of prices and stop illegal anti-competitive behavior. ACCC does not favor

anyone, be it consumers or producers and seeks to reach a competitive market structure without

unreal restriction. They have the power to bring about court actions against firms that rupture the

Competition and Consumers Act and would be fined by the Federal Court (Bakir, 2013).

Scandals by Australian Banks

Introduction

The market structure in Australia is in nature of Monopoly. Most of the service sectors

operates together starting with the industry for retail banking. The banks actively work together

and share the profits among themselves. The Australian Competition and Consumer Commission

(ACCC) has two most important query regarding the competition in banking industry.

ACCC Chairman, Rod Sims has addressed that the sections addresses the oligopoly

market structure of the banking industry. Yet, the cases of the banks formation of cartel is not

alleged. Till date the market structure is influenced by mainly four banks creating monopoly

power. However, that is not the only concerned case because there are other factors that comes

into existence and effectively challenging the banks. Simon has also mentioned how the ACCC

findings on exchange would be analytical to understand the type of competition (Altman &

Ward, 2018). The aim of this paper is to understand the working structure of Australian banks

and the suitable measures to be taken in order to solve the issues of monopoly banking sector.

Australian Competition and Consumer Commission (ACCC)

The commission is an autonomous authority of the Australian government, established in

1905. The prime objective is to look after the business rights, consumer rights, regulation of

industries, monitoring of prices and stop illegal anti-competitive behavior. ACCC does not favor

anyone, be it consumers or producers and seeks to reach a competitive market structure without

unreal restriction. They have the power to bring about court actions against firms that rupture the

Competition and Consumers Act and would be fined by the Federal Court (Bakir, 2013).

Scandals by Australian Banks

2ECONOMICS ASSIGNMENT

A national investigation into Australia’s financial section had reportedly shown sweeping

changes over the last ten years and has engaged in scandals. This has been done after twelve

months of research by an organization named Royal Commission Misconduct in the Banking,

Superannuation and Financial Service Industry. They revealed that banks have been charging

fees without providing services. 76 recommendations were objected towards the banking

industry for the series of scams performed which lost confidence among people. Banks have

collected fees even for dead customers and customers who lost everything; including country’s

biggest moneylender, Commonwealth Bank of Australia (Banks et al., 2015).

According to media reports, the Commonwealth Bank of Australia (CBA has made profit

of billion dollars by paying huge dividends to its shareholders. The scenario is same in other

three important banks as well. These deep seated problems arising due to way Australians buy

insurance, advice and superannuation and for poor management standards. CBA has been

involved in matters relating to money laundering for drug syndicates, ignoring legal

responsibilities and impudent foreign exchange trading. The bank led its smart money depositing

machine to be used by money-laundering syndicates associated to drug distribution and

importation networks. The bank received a penalty of about 375 million dollars which the bank

has underestimated.

A report by the Productivity Commission made it clear that the big financial institutions

exploited the loyal customers and faced a constant public caning. The institution is suspected to

finance for suspicious matters such as terrorism. They failed to provide terrorism financing

suspicions within 24 hours, did not monitor risk of 38 instances and neglected over 54 cases

under law enforcement investigation. Westpac triggered Australia’s interest rates and secretly

lending money to elderly pensioners. The National Bank of Australia (NAB) had to pay millions

A national investigation into Australia’s financial section had reportedly shown sweeping

changes over the last ten years and has engaged in scandals. This has been done after twelve

months of research by an organization named Royal Commission Misconduct in the Banking,

Superannuation and Financial Service Industry. They revealed that banks have been charging

fees without providing services. 76 recommendations were objected towards the banking

industry for the series of scams performed which lost confidence among people. Banks have

collected fees even for dead customers and customers who lost everything; including country’s

biggest moneylender, Commonwealth Bank of Australia (Banks et al., 2015).

According to media reports, the Commonwealth Bank of Australia (CBA has made profit

of billion dollars by paying huge dividends to its shareholders. The scenario is same in other

three important banks as well. These deep seated problems arising due to way Australians buy

insurance, advice and superannuation and for poor management standards. CBA has been

involved in matters relating to money laundering for drug syndicates, ignoring legal

responsibilities and impudent foreign exchange trading. The bank led its smart money depositing

machine to be used by money-laundering syndicates associated to drug distribution and

importation networks. The bank received a penalty of about 375 million dollars which the bank

has underestimated.

A report by the Productivity Commission made it clear that the big financial institutions

exploited the loyal customers and faced a constant public caning. The institution is suspected to

finance for suspicious matters such as terrorism. They failed to provide terrorism financing

suspicions within 24 hours, did not monitor risk of 38 instances and neglected over 54 cases

under law enforcement investigation. Westpac triggered Australia’s interest rates and secretly

lending money to elderly pensioners. The National Bank of Australia (NAB) had to pay millions

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ECONOMICS ASSIGNMENT

of dollars for giving wrong advices to business planners which eventually led to immense losses

(Buckley & Ooi, 2015).

Monopoly Banking Sector

The banking industry in Australia is influenced by four major banks such as the

Australia and New Zealand Banking Group, Westpac Banking Corporation, National Australia

Bank and the Commonwealth Bank of Australia. Although the country has a large number of

smaller banks and many other financial institutions, the banking industry is influenced by the

working structure of these particular banks. Presence of large foreign banks are there, yet a few

among them has a functioning on retail banking. Smaller financial institutions like credit unions,

mutual banks and building societies are there which have little banking services and is

considered to perform under authorized deposit taking institutions (Chaly et al., 2017).

The productivity commission has reported these banks to generate huge costs, by putting high

price for upgrading the net revenue instead of carrying the burden of lowering the market share

at every stage of the business cycle. Dead weight loss is created due to lack of competition in the

major banks. This high concentration makes firms makes the institutions to enact as a single firm

with similar rate of interest.

Consequences of monopoly structure

The central four banks have organized a cartel arrangement because the greater chunk of

the shareholders are from those important banks. Thus, a common enthusiasm and interest exist

in the same banks. The shareholder’s work is to take away the maximum profit from the firms by

creating a monopoly market structure such that they can dominate and influence the market

price. Profit maximization is achievable by the formation of cartel. About 450,000 people are

of dollars for giving wrong advices to business planners which eventually led to immense losses

(Buckley & Ooi, 2015).

Monopoly Banking Sector

The banking industry in Australia is influenced by four major banks such as the

Australia and New Zealand Banking Group, Westpac Banking Corporation, National Australia

Bank and the Commonwealth Bank of Australia. Although the country has a large number of

smaller banks and many other financial institutions, the banking industry is influenced by the

working structure of these particular banks. Presence of large foreign banks are there, yet a few

among them has a functioning on retail banking. Smaller financial institutions like credit unions,

mutual banks and building societies are there which have little banking services and is

considered to perform under authorized deposit taking institutions (Chaly et al., 2017).

The productivity commission has reported these banks to generate huge costs, by putting high

price for upgrading the net revenue instead of carrying the burden of lowering the market share

at every stage of the business cycle. Dead weight loss is created due to lack of competition in the

major banks. This high concentration makes firms makes the institutions to enact as a single firm

with similar rate of interest.

Consequences of monopoly structure

The central four banks have organized a cartel arrangement because the greater chunk of

the shareholders are from those important banks. Thus, a common enthusiasm and interest exist

in the same banks. The shareholder’s work is to take away the maximum profit from the firms by

creating a monopoly market structure such that they can dominate and influence the market

price. Profit maximization is achievable by the formation of cartel. About 450,000 people are

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ECONOMICS ASSIGNMENT

employed in the financial service sector that contributes a humongous number to economic

growth. A banking sector requires huge amount of capital investment to start with their business.

Most of the people are enlightened to work and deposit for big companies which reduces

chances for small firms to operate. The seller in the monopoly market is known as a monopolist.

He has control over the price and market output. A cartel is the market structure where a

gathering of firms that has the same goals and targets take joint venture to make equilibrium

price and output decisions. These strategies give rise to an oligopolistic system which are

dependent on the formation of cartel which operate with few companies, having a powerful share

on the economy (Gilligan et al., 2017).

The operation by the arrangement of cartel has been prohibited by CCA under a civil law

and has marked it as a criminal offence if businesses work in a cartel. Firms found guilty of

cartel strategy are penalized both by civil and criminal ways. The dignitaries are charged with

fines of 420,000 dollars along with sentence of imprisonment up to ten years. Pecuniary penalties

for provision of civil contravention and cartel offence has to provide over 500,000 dollars. It is

not legal for corporations to indemnify its agents against financial fines and legal costs (Gitman,

Juchau & Flanagan, 2015).

Dead-weight loss of Monopoly Structure

The structure in monopoly markets is marked by barriers to entry of new firms and no

competition is being faced due to lack of substitutes. Although monopolies have huge profits, yet

there are huge dead weight losses faced by the economy. The maximum level of profit is

measured by the intersection of marginal revue with marginal cost curves and keep price as

determined by market demand curve (U-Din, Tripe & Kabir, 2017).

employed in the financial service sector that contributes a humongous number to economic

growth. A banking sector requires huge amount of capital investment to start with their business.

Most of the people are enlightened to work and deposit for big companies which reduces

chances for small firms to operate. The seller in the monopoly market is known as a monopolist.

He has control over the price and market output. A cartel is the market structure where a

gathering of firms that has the same goals and targets take joint venture to make equilibrium

price and output decisions. These strategies give rise to an oligopolistic system which are

dependent on the formation of cartel which operate with few companies, having a powerful share

on the economy (Gilligan et al., 2017).

The operation by the arrangement of cartel has been prohibited by CCA under a civil law

and has marked it as a criminal offence if businesses work in a cartel. Firms found guilty of

cartel strategy are penalized both by civil and criminal ways. The dignitaries are charged with

fines of 420,000 dollars along with sentence of imprisonment up to ten years. Pecuniary penalties

for provision of civil contravention and cartel offence has to provide over 500,000 dollars. It is

not legal for corporations to indemnify its agents against financial fines and legal costs (Gitman,

Juchau & Flanagan, 2015).

Dead-weight loss of Monopoly Structure

The structure in monopoly markets is marked by barriers to entry of new firms and no

competition is being faced due to lack of substitutes. Although monopolies have huge profits, yet

there are huge dead weight losses faced by the economy. The maximum level of profit is

measured by the intersection of marginal revue with marginal cost curves and keep price as

determined by market demand curve (U-Din, Tripe & Kabir, 2017).

5ECONOMICS ASSIGNMENT

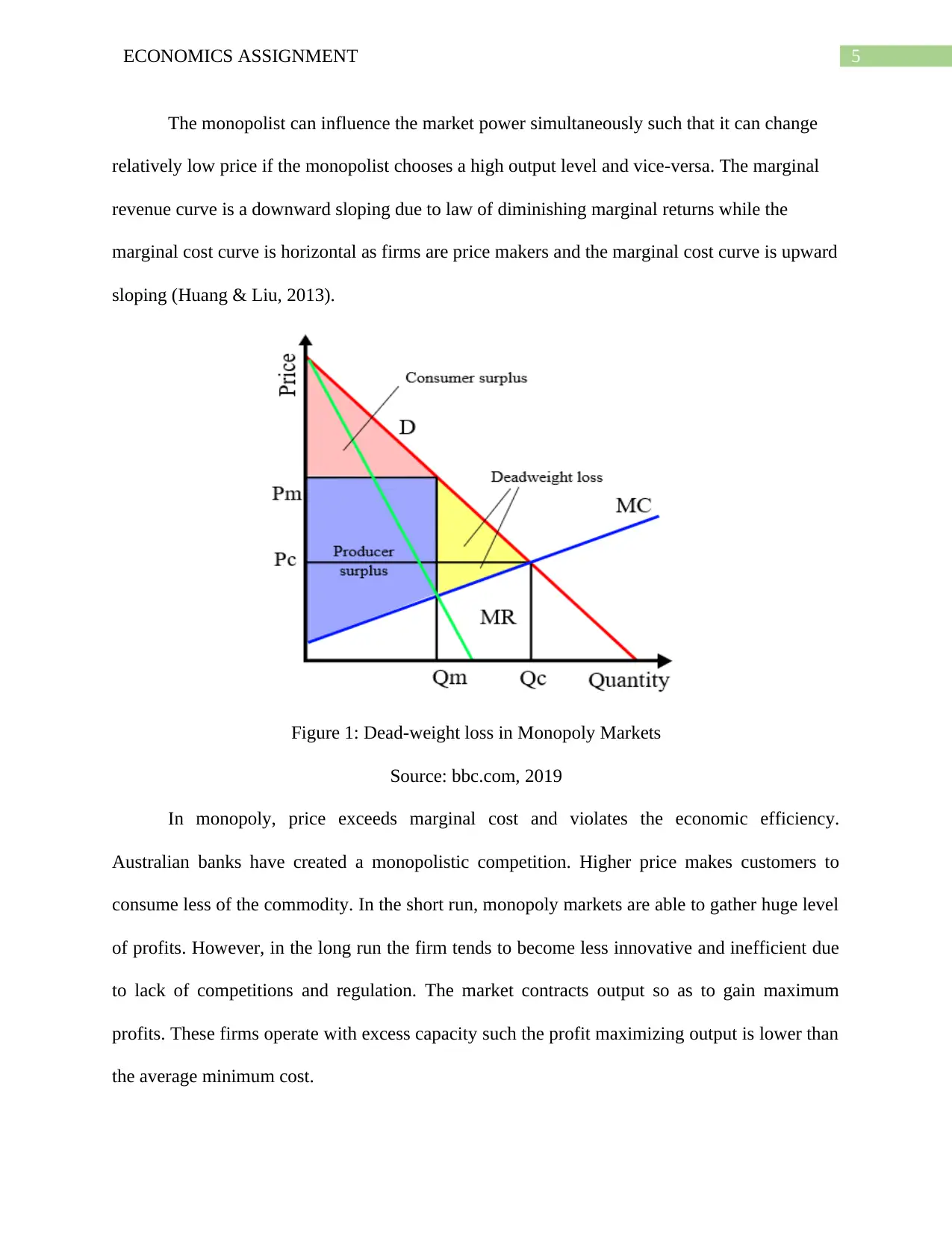

The monopolist can influence the market power simultaneously such that it can change

relatively low price if the monopolist chooses a high output level and vice-versa. The marginal

revenue curve is a downward sloping due to law of diminishing marginal returns while the

marginal cost curve is horizontal as firms are price makers and the marginal cost curve is upward

sloping (Huang & Liu, 2013).

Figure 1: Dead-weight loss in Monopoly Markets

Source: bbc.com, 2019

In monopoly, price exceeds marginal cost and violates the economic efficiency.

Australian banks have created a monopolistic competition. Higher price makes customers to

consume less of the commodity. In the short run, monopoly markets are able to gather huge level

of profits. However, in the long run the firm tends to become less innovative and inefficient due

to lack of competitions and regulation. The market contracts output so as to gain maximum

profits. These firms operate with excess capacity such the profit maximizing output is lower than

the average minimum cost.

The monopolist can influence the market power simultaneously such that it can change

relatively low price if the monopolist chooses a high output level and vice-versa. The marginal

revenue curve is a downward sloping due to law of diminishing marginal returns while the

marginal cost curve is horizontal as firms are price makers and the marginal cost curve is upward

sloping (Huang & Liu, 2013).

Figure 1: Dead-weight loss in Monopoly Markets

Source: bbc.com, 2019

In monopoly, price exceeds marginal cost and violates the economic efficiency.

Australian banks have created a monopolistic competition. Higher price makes customers to

consume less of the commodity. In the short run, monopoly markets are able to gather huge level

of profits. However, in the long run the firm tends to become less innovative and inefficient due

to lack of competitions and regulation. The market contracts output so as to gain maximum

profits. These firms operate with excess capacity such the profit maximizing output is lower than

the average minimum cost.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ECONOMICS ASSIGNMENT

The consumer surplus is the profit earned by consumers as measured by area under the

demand curve and producer surplus is the surplus of producer estimated by the area above the

marginal cost curve. The firm sets equilibrium price above the price in perfectly competitive

markets. The consumer surplus is marked by the ‘pink’ portion, while producer surplus is the

blue portion. The area represented by yellow color is the deadweight loss as no one receives that

area due to high price of the monopoly markets (Joshi, 2013).

As the Australian banks imposed a high rate of interest, many people reduced the quantity they

borrowed leading to a fall in demand. Customer confidence weakened and they were not

satisfied.

High rate of interest facilitated greater supply of money for lending. Banks operated by

giving huge amounts of loans at a high rate. They were unable to find any long-term solution to

the problem as their debts got abolished. The effect could be faced by customers as they had to

sell their houses, to make ends meet. Many victims devoted to hardship relief for providing the

huge amount of money taken as loans (Lumsden, 2019).

Interest rates of banks

The average interest rate of Australian banks is about 2.75 percent. Concentration of

market has significant effect on the economy that includes financial aspect, economic efficiency,

profitability, stability and economic efficiency of Australia. Increase in market concentration

cause inefficiency in markets due to less competition. Generation of huge producer surplus by

low cost of production and low consumer surplus is not good for economic well-being. The

lending rate specifically increased for housing loans to more than the official cut rate in Reserve

Bank of Australia (RBA). Due to this domination, customers were forced to accept the rate for

the lack of options (Smyth, 2019).

The consumer surplus is the profit earned by consumers as measured by area under the

demand curve and producer surplus is the surplus of producer estimated by the area above the

marginal cost curve. The firm sets equilibrium price above the price in perfectly competitive

markets. The consumer surplus is marked by the ‘pink’ portion, while producer surplus is the

blue portion. The area represented by yellow color is the deadweight loss as no one receives that

area due to high price of the monopoly markets (Joshi, 2013).

As the Australian banks imposed a high rate of interest, many people reduced the quantity they

borrowed leading to a fall in demand. Customer confidence weakened and they were not

satisfied.

High rate of interest facilitated greater supply of money for lending. Banks operated by

giving huge amounts of loans at a high rate. They were unable to find any long-term solution to

the problem as their debts got abolished. The effect could be faced by customers as they had to

sell their houses, to make ends meet. Many victims devoted to hardship relief for providing the

huge amount of money taken as loans (Lumsden, 2019).

Interest rates of banks

The average interest rate of Australian banks is about 2.75 percent. Concentration of

market has significant effect on the economy that includes financial aspect, economic efficiency,

profitability, stability and economic efficiency of Australia. Increase in market concentration

cause inefficiency in markets due to less competition. Generation of huge producer surplus by

low cost of production and low consumer surplus is not good for economic well-being. The

lending rate specifically increased for housing loans to more than the official cut rate in Reserve

Bank of Australia (RBA). Due to this domination, customers were forced to accept the rate for

the lack of options (Smyth, 2019).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ECONOMICS ASSIGNMENT

An increase of cash price gives a good stimulus to businesses, while a high rate of

interest leads to losses for the repayment of mortgage and loans. Australians had difficulty in

borrowing money as they had to give huge amount as loan and personal finances were rendered

expensive. The official cash rate must be kept low so that banks are able to borrow money from

other banks. A high interest rate leads other banks to keep raising their rates as well (Maddison

& Denniss, 2013).

Ways to stop the monopoly structure of banks

In monopoly markets, firms have huge power both financially as well as legally. The

government has to play a crucial role in the market so as the preserve the interest of the

customers and reduce the dead weight loss received by the economy. The banks must keep a

high interest rate on deposits so that consumers deposit money which will lead to increase in

money supply of banks (Meng, Hoang & Siriwardana, 2013).

Loans must be given at a lower interest rate such that customers who are in need of

money can take it without worrying on the rate of return. Monopoly firms have little incentives

to build quality service. Improving the service system of the smart machines and provide new

schemes for the customers without getting indulged in crimes. A strong government structure is

also required to keep tract of the performance and functioning of the monetary institutions

(Pakhchanyan, 2016).

Conclusion

The ACCC Chairman has mentioned about the cozy oligopoly market structure of

Australian banks as there are only a few banks who influence the market structure. The banks

perform in a cartel making one single high interest rate and creating monopoly power in

An increase of cash price gives a good stimulus to businesses, while a high rate of

interest leads to losses for the repayment of mortgage and loans. Australians had difficulty in

borrowing money as they had to give huge amount as loan and personal finances were rendered

expensive. The official cash rate must be kept low so that banks are able to borrow money from

other banks. A high interest rate leads other banks to keep raising their rates as well (Maddison

& Denniss, 2013).

Ways to stop the monopoly structure of banks

In monopoly markets, firms have huge power both financially as well as legally. The

government has to play a crucial role in the market so as the preserve the interest of the

customers and reduce the dead weight loss received by the economy. The banks must keep a

high interest rate on deposits so that consumers deposit money which will lead to increase in

money supply of banks (Meng, Hoang & Siriwardana, 2013).

Loans must be given at a lower interest rate such that customers who are in need of

money can take it without worrying on the rate of return. Monopoly firms have little incentives

to build quality service. Improving the service system of the smart machines and provide new

schemes for the customers without getting indulged in crimes. A strong government structure is

also required to keep tract of the performance and functioning of the monetary institutions

(Pakhchanyan, 2016).

Conclusion

The ACCC Chairman has mentioned about the cozy oligopoly market structure of

Australian banks as there are only a few banks who influence the market structure. The banks

perform in a cartel making one single high interest rate and creating monopoly power in

8ECONOMICS ASSIGNMENT

Australia. This power has led banks to get engaged in illegal practices and the ACCC working

actively to understand the misconducts made to the clients. Rod Sims, ACCC chairman has

warned the big firms to avoid illegal offences by break the enlisted laws leading to potential

court actions.

Formation of cartel has to be avoided otherwise strong actions would be taken against the

firms. The misconducts made by the banks has negative impacts on the society.

The frauds escorted billions of dollars out of Australia’s account making a downfall of growth

and GDP. Thus, it is to be concluded that regulators are in need of more organized powers.

Markets perform more efficiently as monopoly power gets reduced along with lower dead weight

lost and higher benefits.

Australia. This power has led banks to get engaged in illegal practices and the ACCC working

actively to understand the misconducts made to the clients. Rod Sims, ACCC chairman has

warned the big firms to avoid illegal offences by break the enlisted laws leading to potential

court actions.

Formation of cartel has to be avoided otherwise strong actions would be taken against the

firms. The misconducts made by the banks has negative impacts on the society.

The frauds escorted billions of dollars out of Australia’s account making a downfall of growth

and GDP. Thus, it is to be concluded that regulators are in need of more organized powers.

Markets perform more efficiently as monopoly power gets reduced along with lower dead weight

lost and higher benefits.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ECONOMICS ASSIGNMENT

Reference List

Altman, J., & Ward, S. (2018). Competition and consumer issues for Indigenous Australians: A

report to the Australian Competition and Consumer Commission by the Centre for

Aboriginal Economic Policy Research, the Australian National University, Canberra.

Canberra, ACT: Australian Competition and Consumer Commission.

Bakir, C. (2013). Bank behaviour and resilience: The effect of structures, institutions and agents.

Springer.

Banks, M., Marston, G., Russell, R., & Karger, H. (2015). ‘In a perfect world it would be great if

they didn't exist’: How A ustralians experience payday loans. International Journal of

Social Welfare, 24(1), 37-47.

bbc.com. (2019). Australia banks faulted for 'broken lives'. Retrieved 30 August 2019, from

https://www.bbc.com/news/world-australia-47112040

Buckley, R. P., & Ooi, K. (2015). Pacific injustice and instability: Bank account closures of

Australian money transfer operators. Pacific injustice and instability: Bank account

closures of Australian money transfer operators”,(2014), 25, 243-256.

Chaly, S., Hennessy, J., Menand, L., Stiroh, K., Tracy, J., Gutt, L. H., ... & Hirtle, B. (2017).

Misconduct risk, culture and supervision. Federal Reserve Bank of New York.

Gilligan, G., Godwin, A., Hedges, J., & Ramsay, I. (2017). Penalties regimes to counter

corporate and financial wrongdoing in Australia–views of governance professionals. Law

and Financial Markets Review, 11(1), 4-12.

Reference List

Altman, J., & Ward, S. (2018). Competition and consumer issues for Indigenous Australians: A

report to the Australian Competition and Consumer Commission by the Centre for

Aboriginal Economic Policy Research, the Australian National University, Canberra.

Canberra, ACT: Australian Competition and Consumer Commission.

Bakir, C. (2013). Bank behaviour and resilience: The effect of structures, institutions and agents.

Springer.

Banks, M., Marston, G., Russell, R., & Karger, H. (2015). ‘In a perfect world it would be great if

they didn't exist’: How A ustralians experience payday loans. International Journal of

Social Welfare, 24(1), 37-47.

bbc.com. (2019). Australia banks faulted for 'broken lives'. Retrieved 30 August 2019, from

https://www.bbc.com/news/world-australia-47112040

Buckley, R. P., & Ooi, K. (2015). Pacific injustice and instability: Bank account closures of

Australian money transfer operators. Pacific injustice and instability: Bank account

closures of Australian money transfer operators”,(2014), 25, 243-256.

Chaly, S., Hennessy, J., Menand, L., Stiroh, K., Tracy, J., Gutt, L. H., ... & Hirtle, B. (2017).

Misconduct risk, culture and supervision. Federal Reserve Bank of New York.

Gilligan, G., Godwin, A., Hedges, J., & Ramsay, I. (2017). Penalties regimes to counter

corporate and financial wrongdoing in Australia–views of governance professionals. Law

and Financial Markets Review, 11(1), 4-12.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ECONOMICS ASSIGNMENT

Gitman, L. J., Juchau, R., & Flanagan, J. (2015). Principles of managerial finance. Pearson

Higher Education AU.

Huang, A., & Liu, B. (2013). The impact of the goods and services tax on mortgage costs:

evidence from Australian mortgage corporations. International Journal of Financial

Research, 4(1), 54.

Joshi, M., Cahill, D., Sidhu, J., & Kansal, M. (2013). Intellectual capital and financial

performance: an evaluation of the Australian financial sector. Journal of intellectual

capital, 14(2), 264-285.

Lumsden, A. (2019). The Wider Implications of the Hayne Report for Corporate Australia.

Available at SSRN 3342855.

Maddison, S., & Denniss, R. (2013). An introduction to Australian public policy: theory and

practice. Cambridge University Press.

Meng, X., Hoang, N. T., & Siriwardana, M. (2013). The determinants of Australian household

debt: A macro level study. Journal of Asian Economics, 29, 80-90.

Pakhchanyan, S. (2016). Operational risk management in financial institutions: A literature

review. International Journal of Financial Studies, 4(4), 20.

Smyth, J. (2019). Foreign banks take aim at Australia’s big four oligopoly | Financial Times.

Retrieved 30 August 2019, from https://www.ft.com/content/668d60fe-97de-11e9-8cfb-

30c211dcd229

U-Din, S., Tripe, D. W., & Kabir, M. (2017). Market Competition and Bank Efficiency: A Post

GFC Assessment of Australia and New Zealand. Available at SSRN 3021357.

Gitman, L. J., Juchau, R., & Flanagan, J. (2015). Principles of managerial finance. Pearson

Higher Education AU.

Huang, A., & Liu, B. (2013). The impact of the goods and services tax on mortgage costs:

evidence from Australian mortgage corporations. International Journal of Financial

Research, 4(1), 54.

Joshi, M., Cahill, D., Sidhu, J., & Kansal, M. (2013). Intellectual capital and financial

performance: an evaluation of the Australian financial sector. Journal of intellectual

capital, 14(2), 264-285.

Lumsden, A. (2019). The Wider Implications of the Hayne Report for Corporate Australia.

Available at SSRN 3342855.

Maddison, S., & Denniss, R. (2013). An introduction to Australian public policy: theory and

practice. Cambridge University Press.

Meng, X., Hoang, N. T., & Siriwardana, M. (2013). The determinants of Australian household

debt: A macro level study. Journal of Asian Economics, 29, 80-90.

Pakhchanyan, S. (2016). Operational risk management in financial institutions: A literature

review. International Journal of Financial Studies, 4(4), 20.

Smyth, J. (2019). Foreign banks take aim at Australia’s big four oligopoly | Financial Times.

Retrieved 30 August 2019, from https://www.ft.com/content/668d60fe-97de-11e9-8cfb-

30c211dcd229

U-Din, S., Tripe, D. W., & Kabir, M. (2017). Market Competition and Bank Efficiency: A Post

GFC Assessment of Australia and New Zealand. Available at SSRN 3021357.

11ECONOMICS ASSIGNMENT

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.