Economics Assignment: Interest Rates and Exchange Rate Determination

VerifiedAdded on 2023/05/30

|13

|1819

|281

Homework Assignment

AI Summary

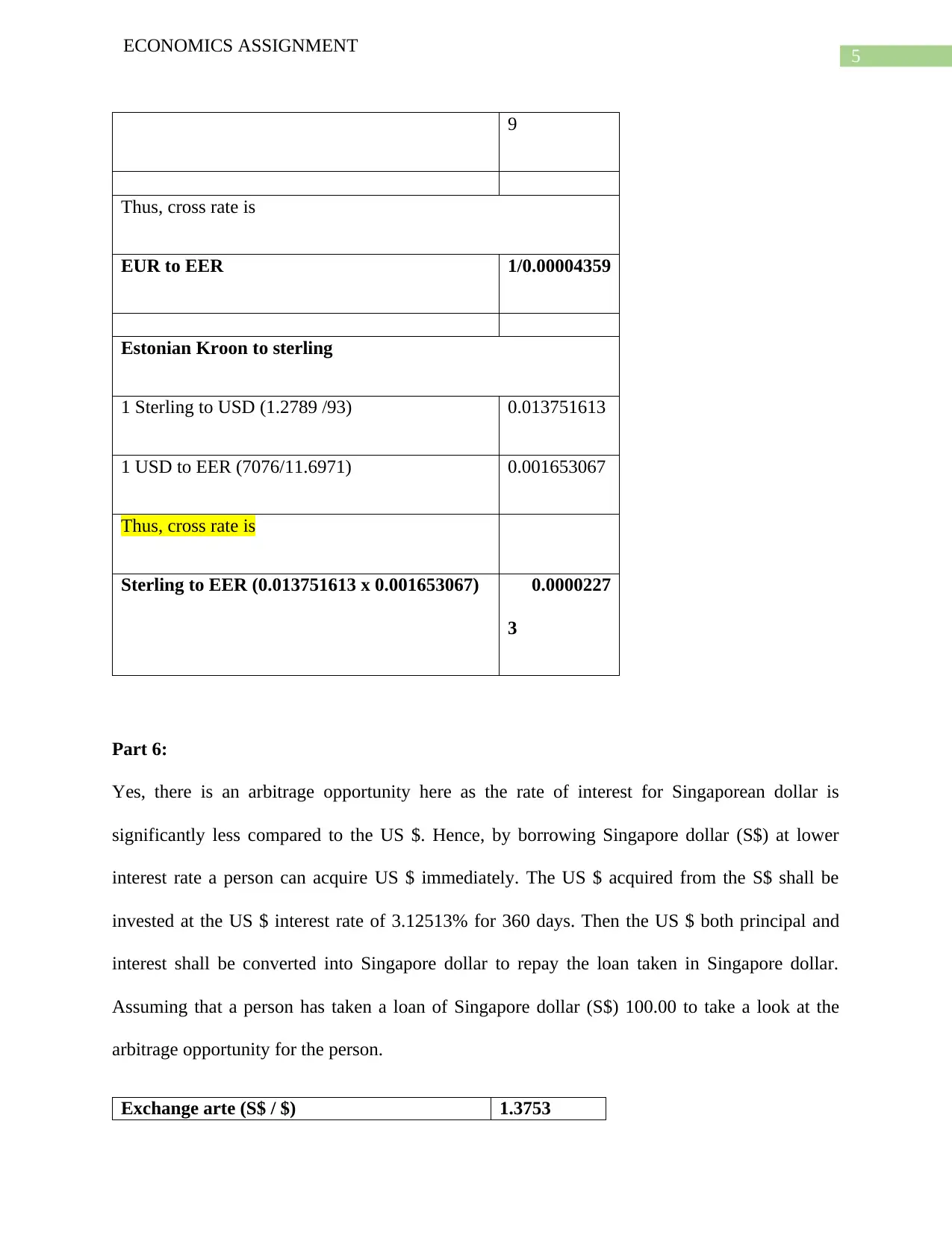

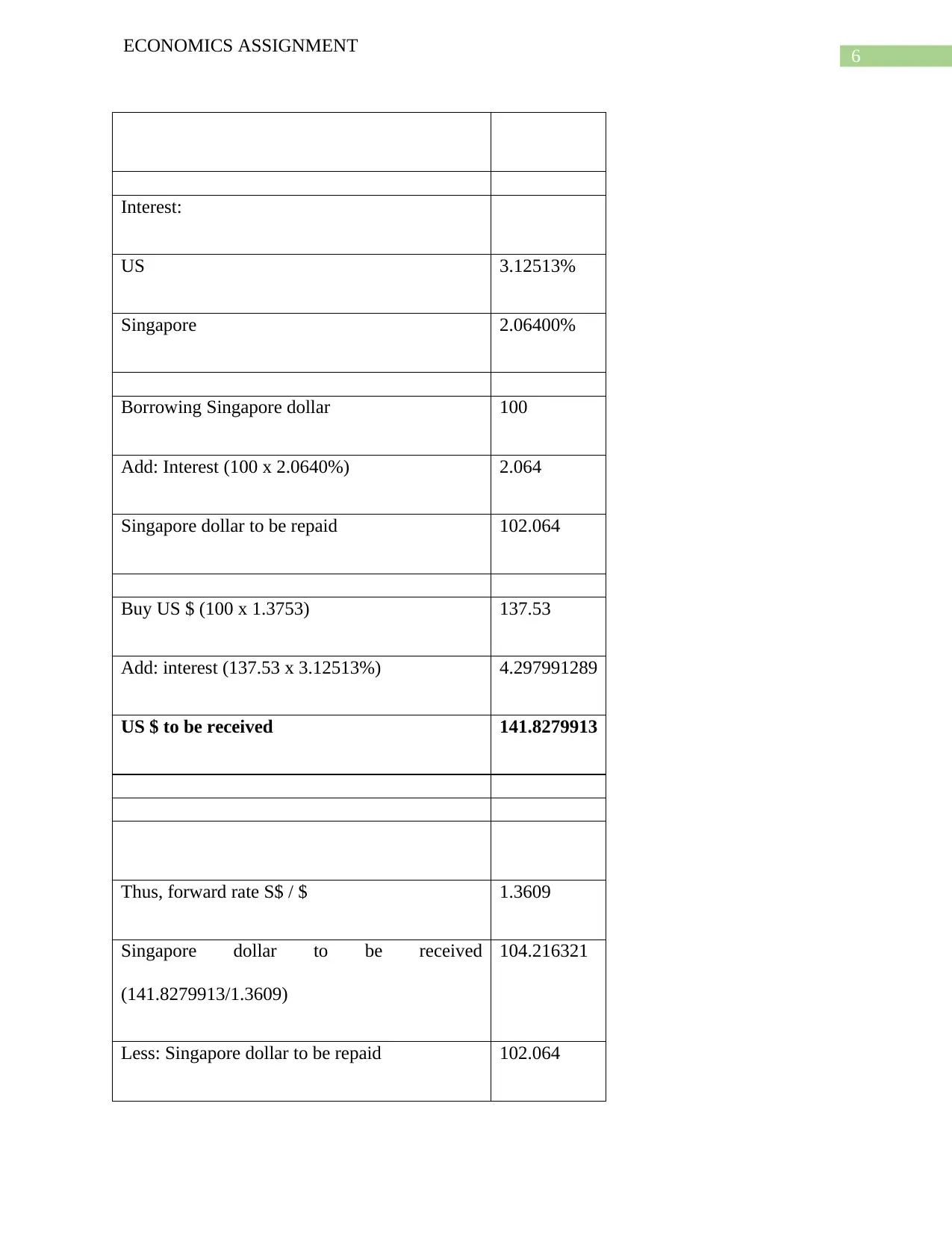

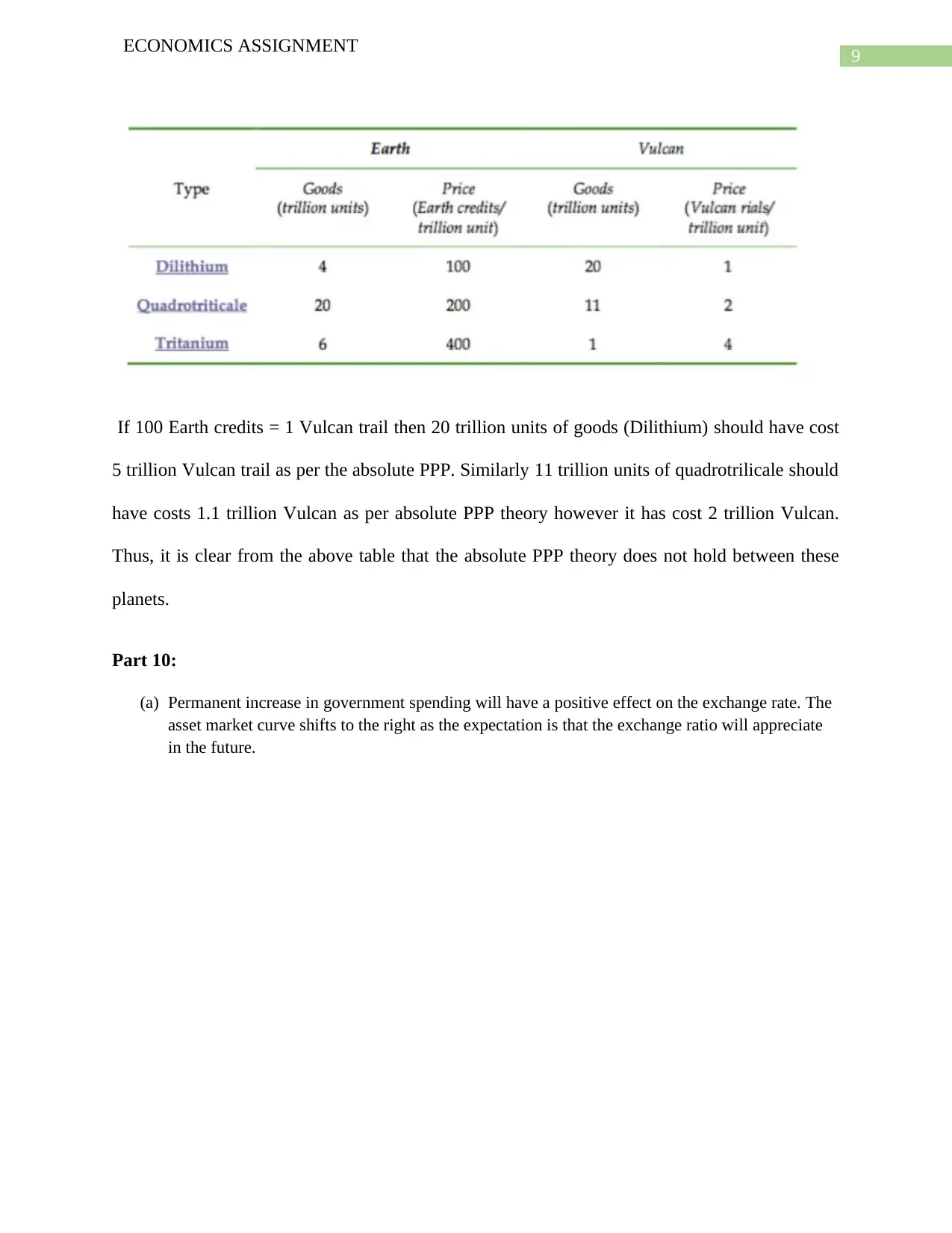

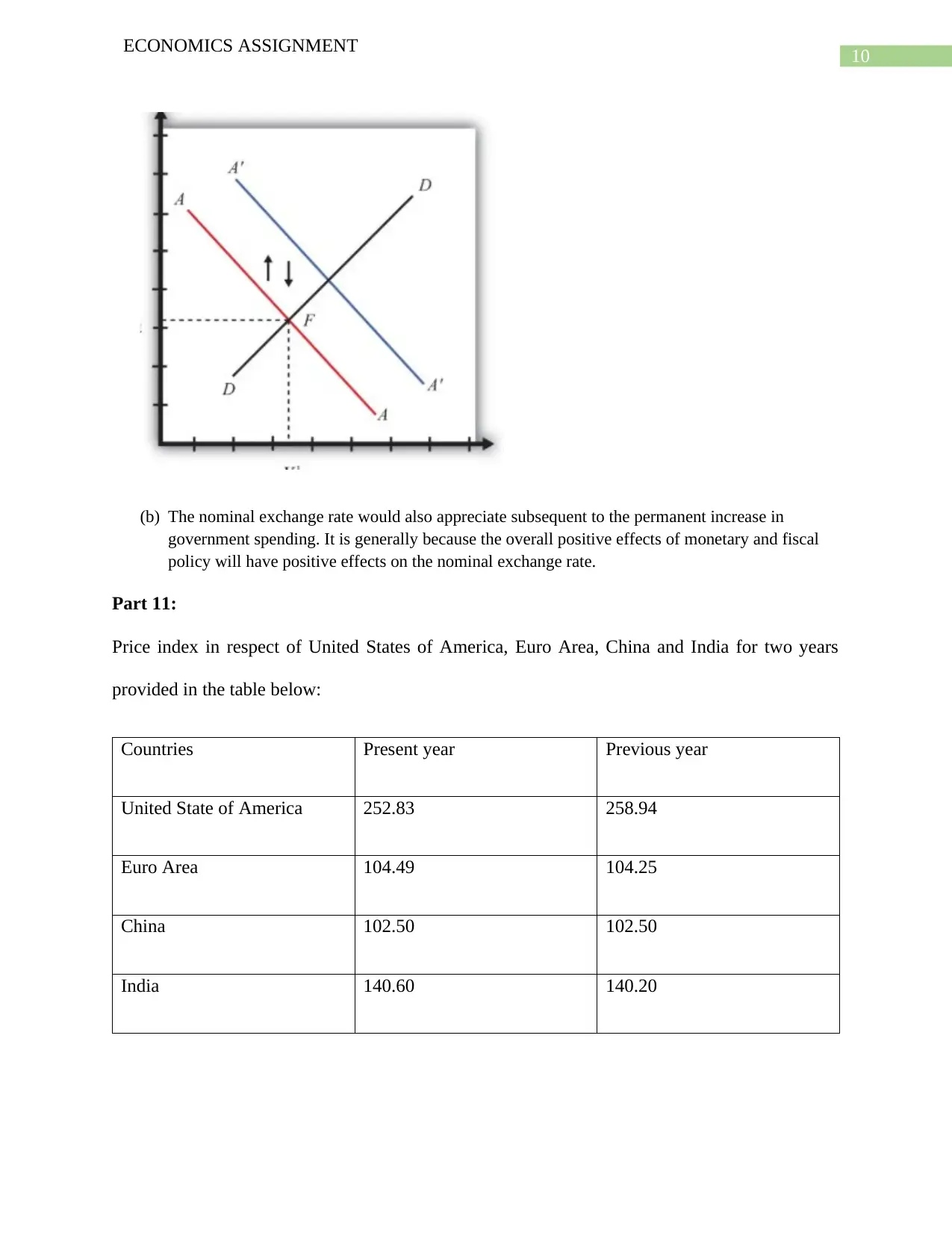

This economics assignment delves into various aspects of international finance, starting with the differentiation between foreign exchange swaps and currency swaps, highlighting their economic motives and balance sheet implications. It explores the International Fisher Effect (IFE) theory, emphasizing the relationship between interest rates and exchange rate depreciation. The assignment critically examines the Purchasing Power Parity (PPP) theory, discussing reasons for its failure and differentiating between absolute and relative PPP. Practical calculations of cross rates are demonstrated, followed by an analysis of arbitrage opportunities arising from interest rate differentials between Singapore and the US. The impact of changes in foreign interest rates and expected appreciation in exchange rates on arbitrage opportunities is graphically illustrated. Furthermore, the assignment discusses the effects of changes in the rate of money growth on price levels, interest rates, and exchange rates, and it empirically tests the absolute PPP theory using data from different planets. Finally, the assignment analyzes the effects of permanent increases in government spending on exchange rates and provides a comparative analysis of price indices and spot exchange rates across the United States, Euro Area, China, and India, concluding with a critique of the absolute PPP theory's applicability.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.