Financial Analysis and Production Plan for Billing AS Report

VerifiedAdded on 2020/05/04

|7

|997

|84

Report

AI Summary

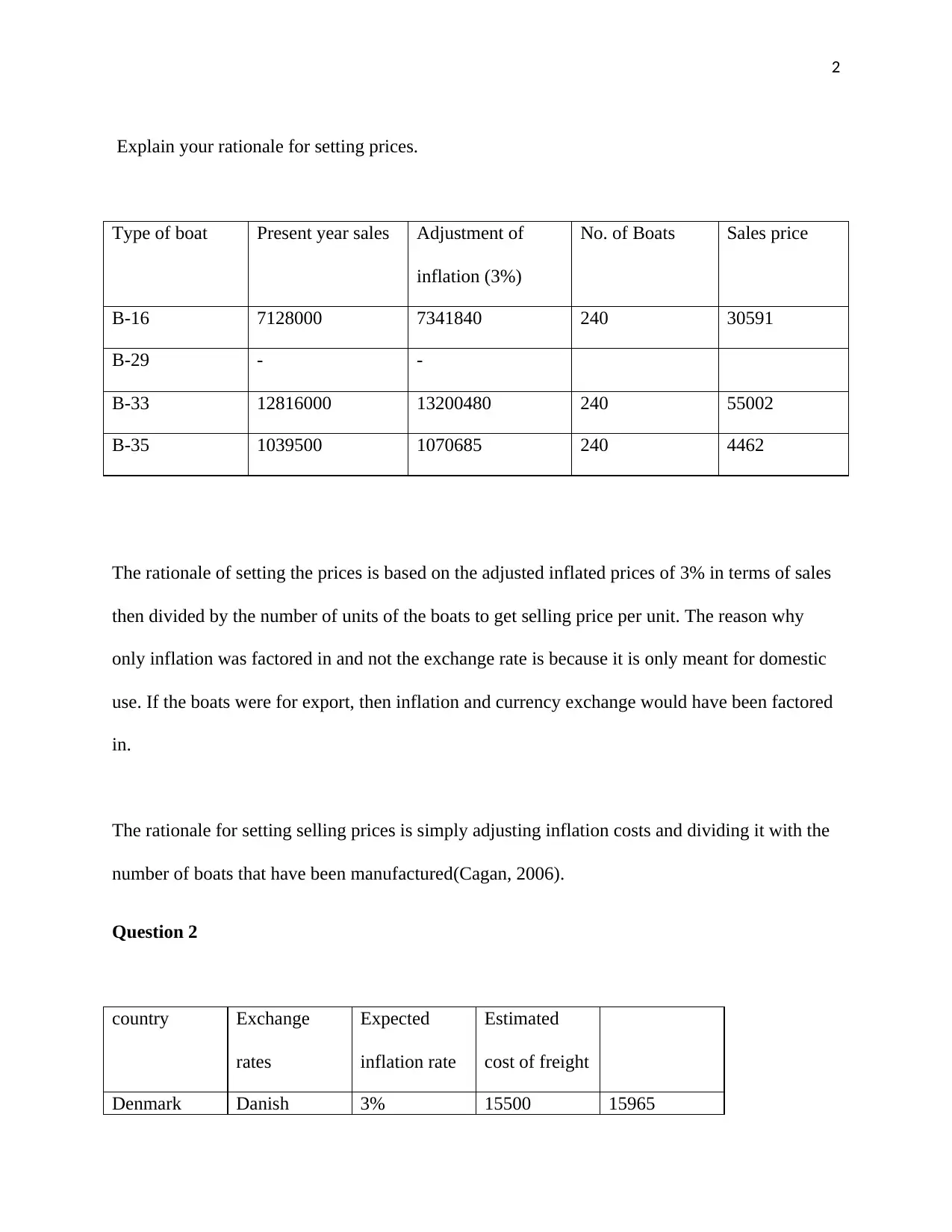

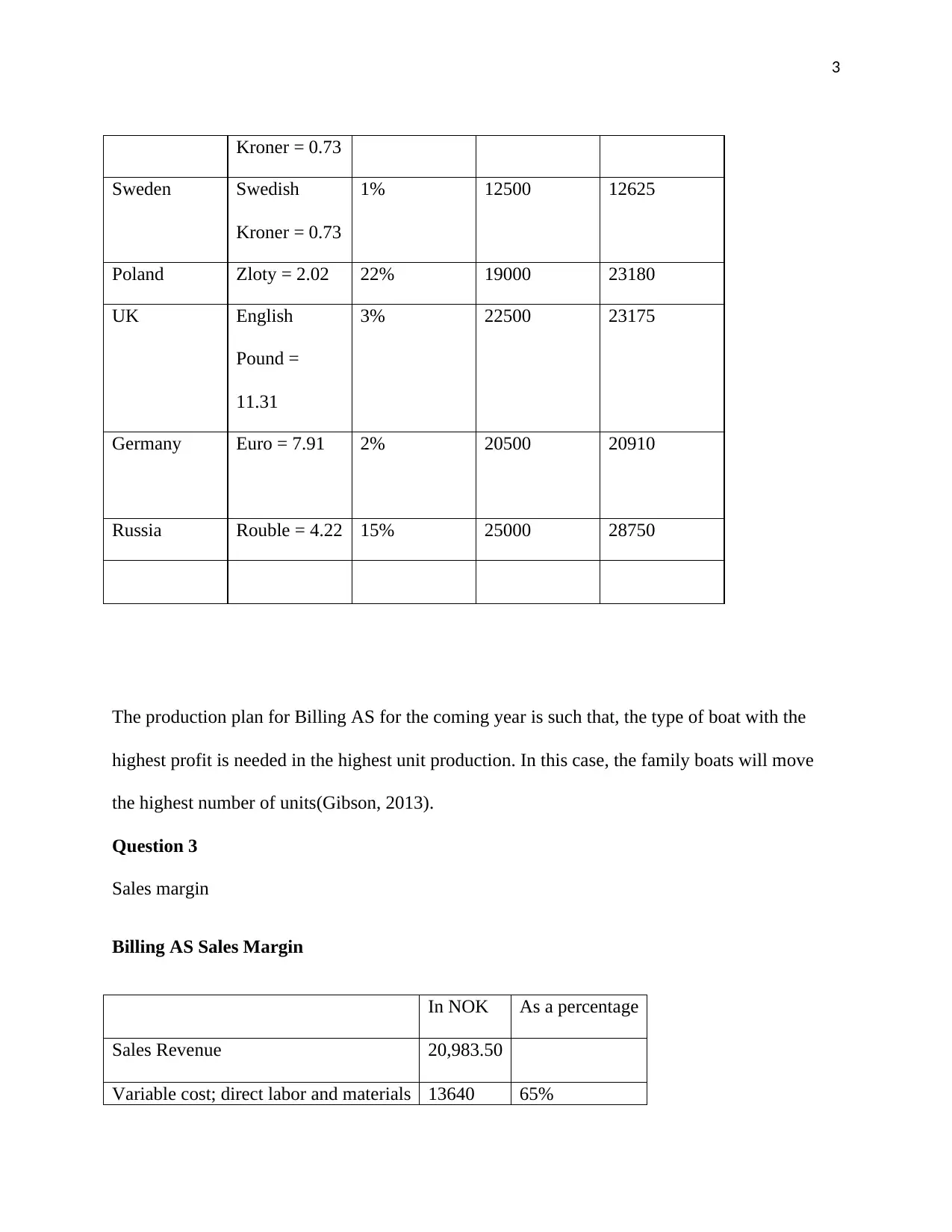

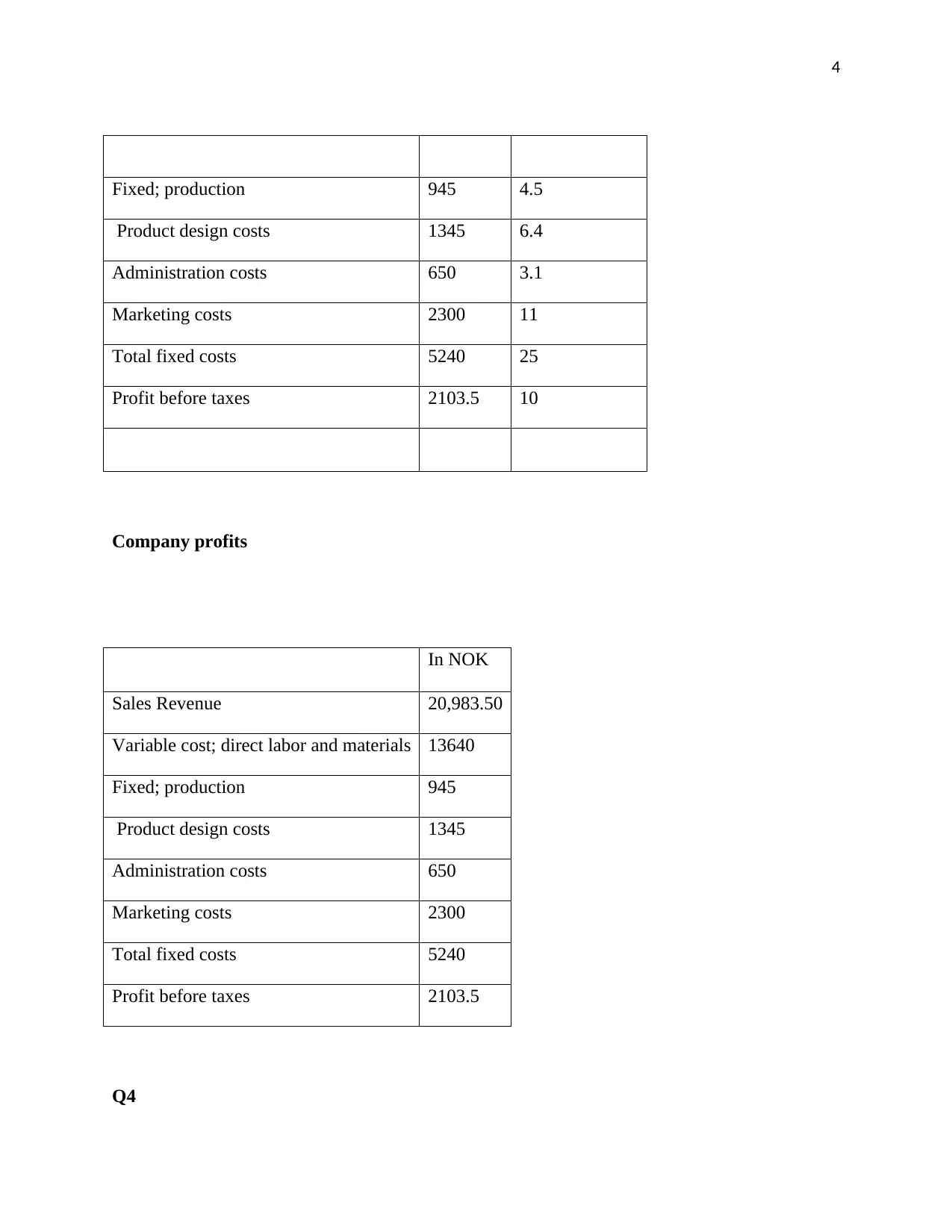

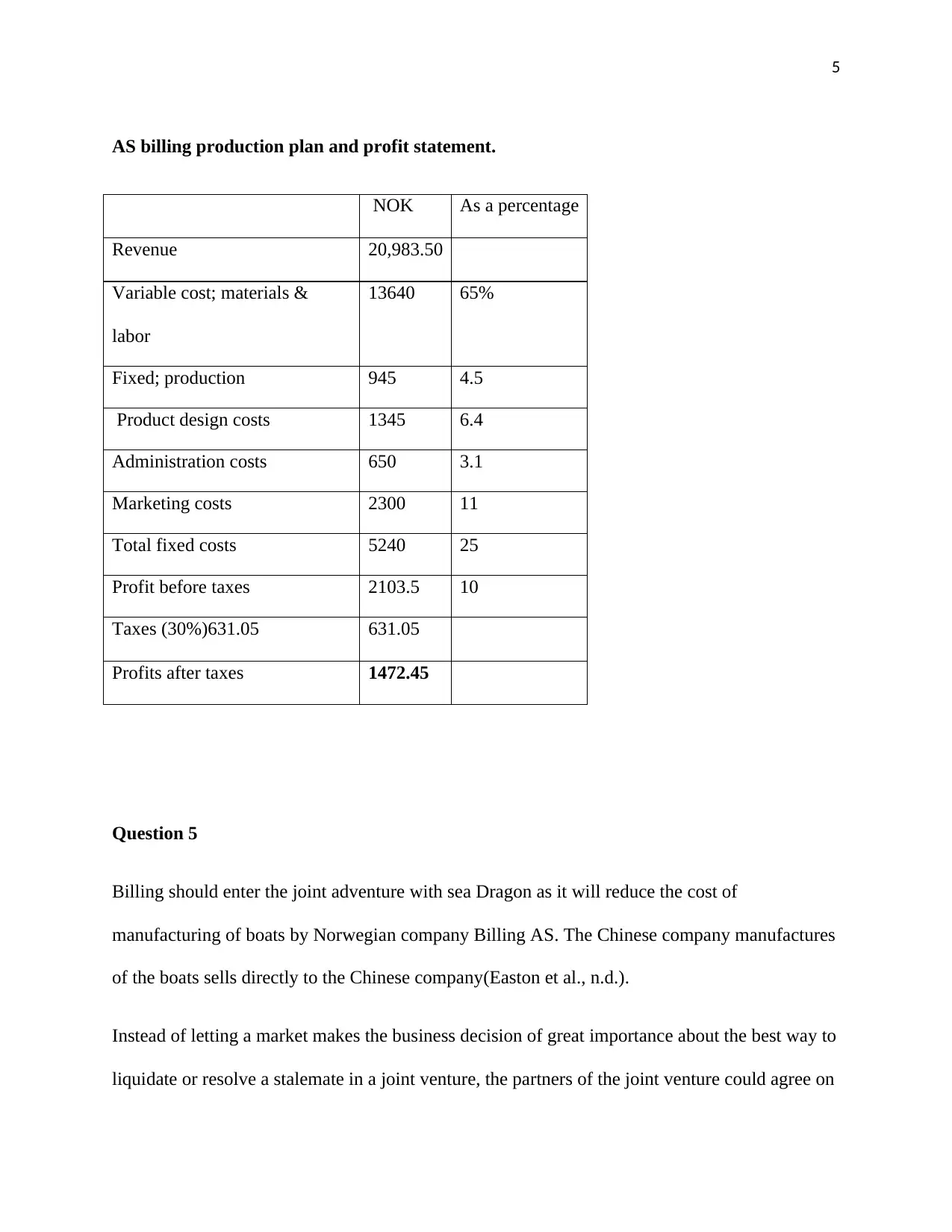

This report presents a financial analysis of Billing AS, examining pricing strategies, sales data, and production plans. It details the rationale behind price setting, considering inflation adjustments. The report analyzes production costs, sales margins, and profit statements, providing a comprehensive overview of the company's financial health. Furthermore, it explores the implications of a joint venture with Sea Dragon, evaluating the potential benefits in terms of cost reduction and dispute resolution. The analysis also considers various methods for resolving stalemates within a joint venture, such as purchase-sale arrangements. The report uses data to calculate costs, revenue, and profit margins, offering a clear understanding of Billing AS's financial performance and strategic recommendations.

1 out of 7

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.