Economics Assignment: Market Structures, Efficiency, and Inflation

VerifiedAdded on 2020/04/07

|8

|1041

|93

Homework Assignment

AI Summary

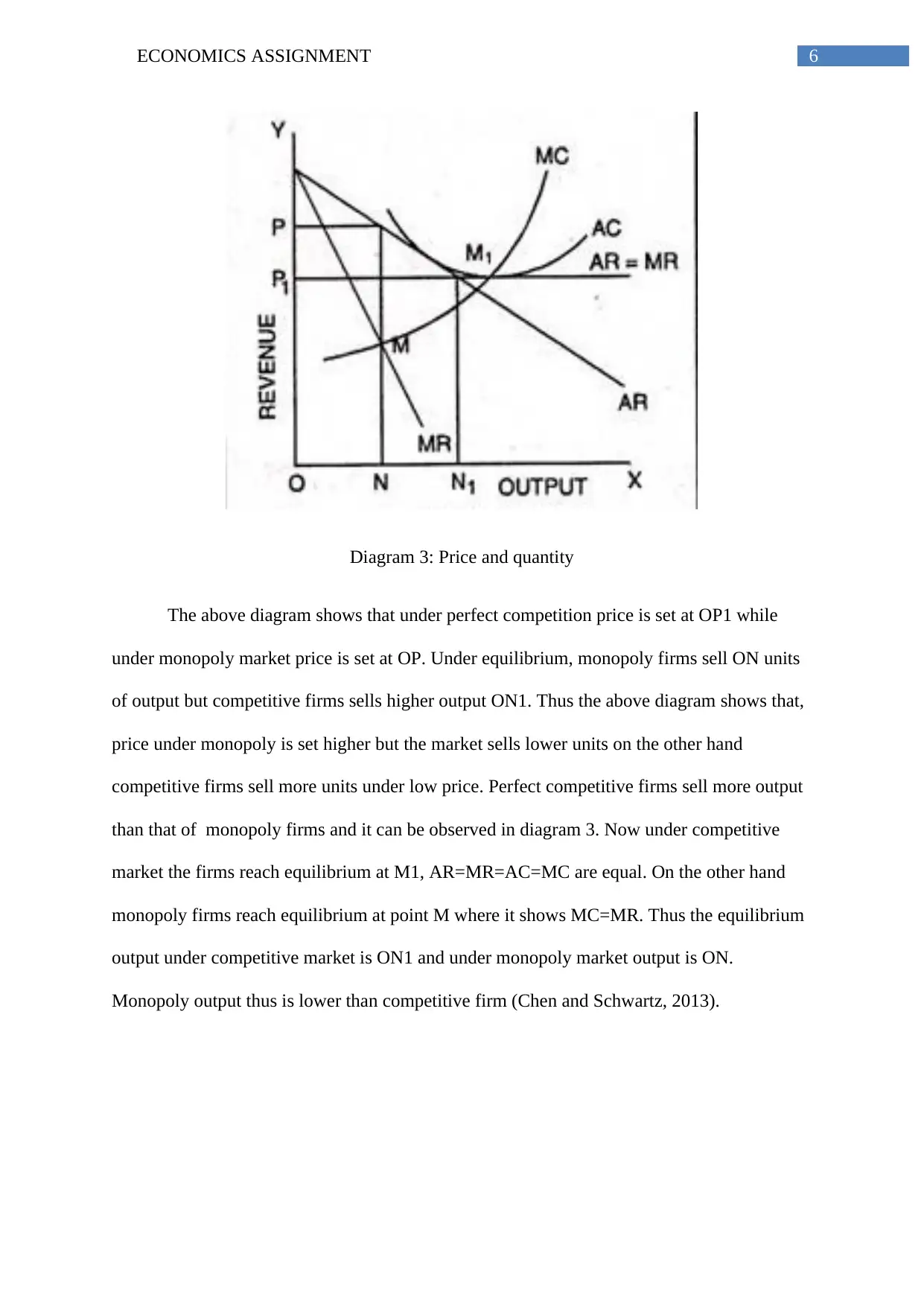

This economics assignment analyzes key economic concepts, including productive and allocative efficiency within the context of perfect competition. It examines the characteristics of monopoly markets in contrast to perfect competition, comparing price and quantity outcomes. Furthermore, the assignment addresses cost-push inflation, using diagrams to illustrate the effects of supply shifts on price levels and real GDP. The student references various academic sources to support the analysis, providing a comprehensive overview of market structures and macroeconomic principles. The assignment covers topics such as market equilibrium, price setting, and the impact of inflation on an economy.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.