Ask a question from expert

Economics Assignment: Supply & Demand

23 Pages4439 Words118 Views

Added on 2020-05-28

Economics Assignment: Supply & Demand

Added on 2020-05-28

BookmarkShareRelated Documents

Running head: ECONOMICS ASSIGNMENT Economics AssignmentName of the StudentName of the UniversityAuthor Note

1ECONOMICS ASSIGNMENT Table of ContentsAnswer 1..........................................................................................................................................2Differences in Characteristics......................................................................................................2Equilibrium condition in perfect competition..............................................................................3Equilibrium under monopolistically competitive market............................................................8Allocative and Productive Efficiencies in the markets................................................................9Answer 2........................................................................................................................................12Oligopoly in the Australian Economy.......................................................................................13Answer 3........................................................................................................................................17Crisis of Housing Affordability in Australia.............................................................................17References......................................................................................................................................20

2ECONOMICS ASSIGNMENT Answer 1 In terms of economics, market is defined to be a place of interaction of the demand andthe supply side players, where the price and quantity related decisions are taken by the same.There exist different types of market in the global framework, depending upon the number ofplayers in the supply and demand side, the powers of the buyers and sellers in the market, thenature of the goods and services dealt with in the concerned market and several other attributes(Baumol & Blinder, 2015). Of the different forms of such markets, two of the popular andwidely discussed market structures are that of the perfectly competitive one and themonopolistically competitive one. The assignment tries to discuss these two markets, taking intoaccount their long run equilibrium situations (Nicholson & Snyder, 2014). The two above-discussed markets have significant differences in the key features, whichare discussed in the following sections of the assignment: Differences in Characteristics Types of product dealt in the market- In case of a perfectly competitive market, theproduct sold and bought is perfectly homogenous in nature, which implies that the products soldby the sellers are exactly similar in all aspects, including nature, taste, smell and others.However, in case of a monopolistically competitive firm, the products dealt with are somewhatdifferentiated, at least by the names of the brands (Hall & Lieberman, 2012). Number of players in the market- In this aspect both the market types are similar as both thenumber of buyers and sellers are high in two of these markets.

3ECONOMICS ASSIGNMENT Barriers to entry and exit- In perfectly competitive market, there are no entry and exit barriersand player can enter or exit from the market without any cost. However, in case ofmonopolistically competitive market, the barriers are very low but still existent. Market power- In the perfectly competitive market, due to the presence of huge numbers ofbuyers as well as sellers, neither the buyers nor the sellers has any extra market power and boththe parties are price takers. However, as the products sold and bought in the monopolisticallycompetitive market are differentiated to some extent, so the supply side players enjoy someextent of market and price decisive power (Rader, 2014). Keeping this into consideration, the equilibrium in a market, in terms of economics, canbe defined to be the condition of mutual agreement of the producers and the buyers, which isreached by mutual interaction of both the parties in the market. The equilibrium of the marketalso differs depending on the nature and type of markets, in short run as well as in the long run,which are discussed in the following sections: Equilibrium condition in perfect competition In the perfectly competitive markets, the number of buyers as well as sellers beingnumerous, the products being perfectly homogenous and the firms being price takers, thedemand curve existing in the market is perfectly elastic. The demand curve, like that of theaverage revenue curve and also the marginal revenue curve, is parallel to the horizontal axis, at aparticular level of price prevailing in the market. The equilibrium, in such a market, occurswhere the marginal cost of producing one additional unit of output by the perfectly competitivefirm is equal to that of the marginal revenue earned by selling that additional unit of output(Kolmar, 2017).

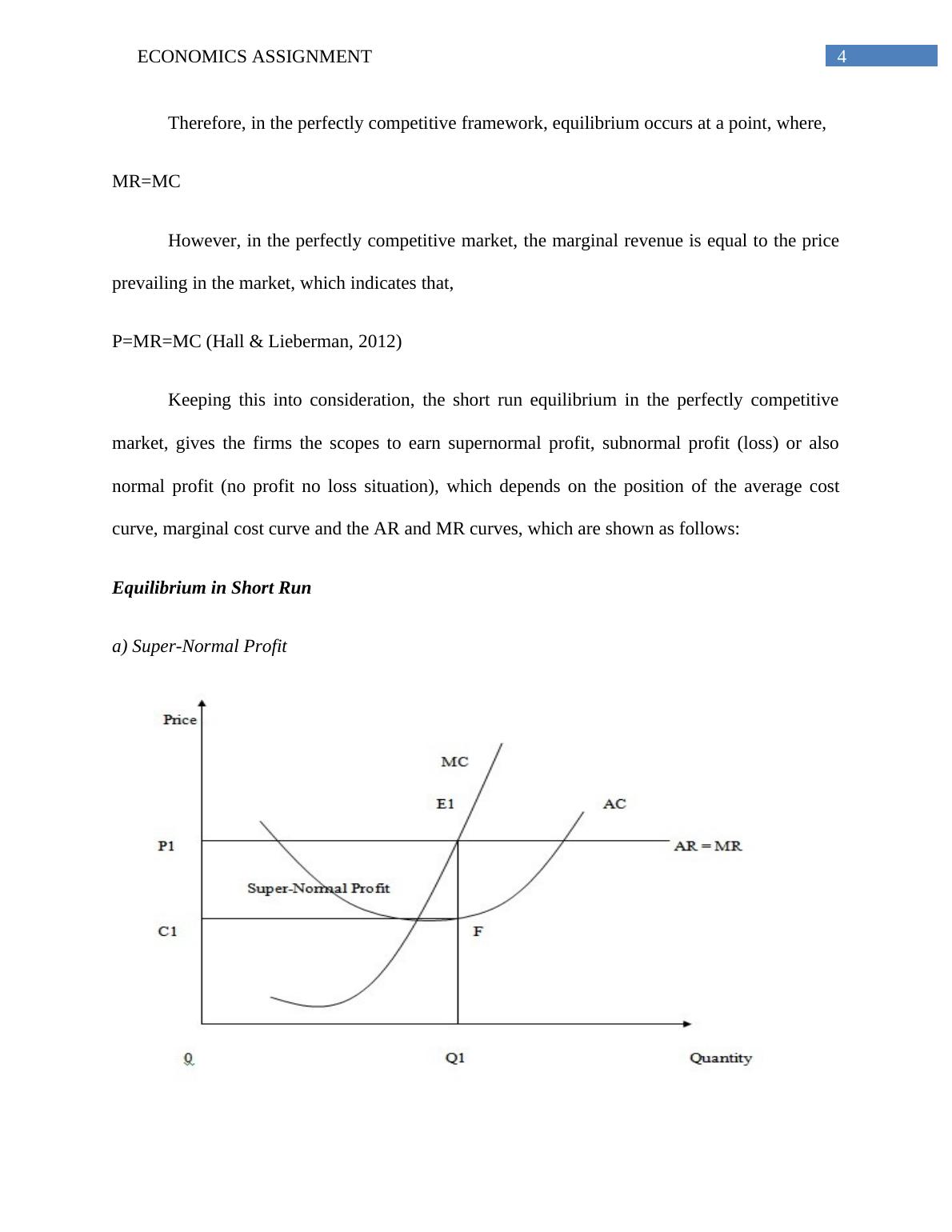

4ECONOMICS ASSIGNMENT Therefore, in the perfectly competitive framework, equilibrium occurs at a point, where, MR=MC However, in the perfectly competitive market, the marginal revenue is equal to the priceprevailing in the market, which indicates that, P=MR=MC (Hall & Lieberman, 2012)Keeping this into consideration, the short run equilibrium in the perfectly competitivemarket, gives the firms the scopes to earn supernormal profit, subnormal profit (loss) or alsonormal profit (no profit no loss situation), which depends on the position of the average costcurve, marginal cost curve and the AR and MR curves, which are shown as follows: Equilibrium in Short Run a) Super-Normal Profit

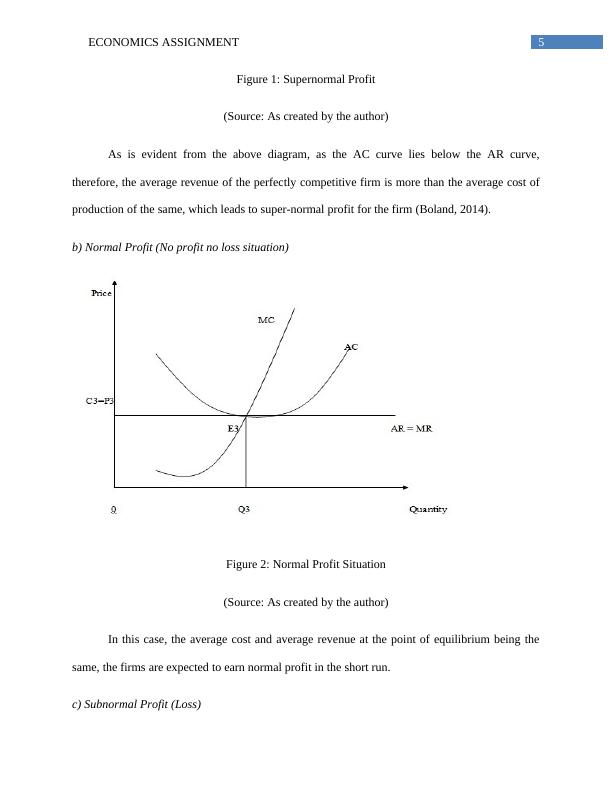

5ECONOMICS ASSIGNMENT Figure 1: Supernormal Profit(Source: As created by the author)As is evident from the above diagram, as the AC curve lies below the AR curve,therefore, the average revenue of the perfectly competitive firm is more than the average cost ofproduction of the same, which leads to super-normal profit for the firm (Boland, 2014). b) Normal Profit (No profit no loss situation) Figure 2: Normal Profit Situation(Source: As created by the author)In this case, the average cost and average revenue at the point of equilibrium being thesame, the firms are expected to earn normal profit in the short run. c) Subnormal Profit (Loss)

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

ECON102 - Economics - Question Answerlg...

|12

|5242

|142

Theoretical Framework of Economics - PDFlg...

|20

|4226

|246

ECON20039 Perfect Competition and Monopolistic Competition : Assignmentlg...

|23

|4137

|50

Characteristics of Perfect Competition and Monopoly Marketlg...

|19

|4154

|468

Managerial Economics Assignment | Economics Assignmentlg...

|12

|1408

|107

Economics for Managerslg...

|21

|3971

|408