Economics Assignment: Microeconomic Principles and Analysis

VerifiedAdded on 2023/01/18

|16

|2299

|40

Homework Assignment

AI Summary

This economics assignment addresses key microeconomic principles through a series of short-answer questions. Question 1 explores the production possibilities frontier (PPF) for a wine producer, analyzing efficient production points and the impact of external factors like drought. Question 2 delves into demand elasticity, calculating elasticity values and analyzing how price changes affect revenue. Question 3 examines market equilibrium, the effects of taxes on supply and demand, and the resulting consumer and producer surplus changes, as well as deadweight loss. Question 4 analyzes the impact of a price ceiling in a tutoring market. Finally, Question 5 investigates a firm's cost structure, including marginal product, break-even points, diminishing returns, and the relationship between various cost curves (AFC, AVC, ATC, MC) and labor costs.

Running head: ECONOMICS

Economics

Name of the Student

Name of the University

Course ID

Economics

Name of the Student

Name of the University

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ECONOMICS

Table of Contents

Question 1..................................................................................................................................2

Question a...............................................................................................................................2

Question b..............................................................................................................................2

Question c...............................................................................................................................3

Question d..............................................................................................................................3

Question 2..................................................................................................................................4

Question a...............................................................................................................................4

Question b..............................................................................................................................4

Question c...............................................................................................................................5

Question e...............................................................................................................................6

Question 3..................................................................................................................................7

Question a...............................................................................................................................7

Question b..............................................................................................................................8

Question c...............................................................................................................................8

Question d..............................................................................................................................8

Question e...............................................................................................................................8

Question f...............................................................................................................................8

Question g..............................................................................................................................9

Question h............................................................................................................................10

Question 4................................................................................................................................10

Question a.............................................................................................................................10

Question b............................................................................................................................11

Question c.............................................................................................................................11

Question d............................................................................................................................12

Question 5................................................................................................................................12

Question a.............................................................................................................................12

Question b............................................................................................................................13

Question c.............................................................................................................................13

Question d............................................................................................................................13

Question e.............................................................................................................................13

References................................................................................................................................14

Table of Contents

Question 1..................................................................................................................................2

Question a...............................................................................................................................2

Question b..............................................................................................................................2

Question c...............................................................................................................................3

Question d..............................................................................................................................3

Question 2..................................................................................................................................4

Question a...............................................................................................................................4

Question b..............................................................................................................................4

Question c...............................................................................................................................5

Question e...............................................................................................................................6

Question 3..................................................................................................................................7

Question a...............................................................................................................................7

Question b..............................................................................................................................8

Question c...............................................................................................................................8

Question d..............................................................................................................................8

Question e...............................................................................................................................8

Question f...............................................................................................................................8

Question g..............................................................................................................................9

Question h............................................................................................................................10

Question 4................................................................................................................................10

Question a.............................................................................................................................10

Question b............................................................................................................................11

Question c.............................................................................................................................11

Question d............................................................................................................................12

Question 5................................................................................................................................12

Question a.............................................................................................................................12

Question b............................................................................................................................13

Question c.............................................................................................................................13

Question d............................................................................................................................13

Question e.............................................................................................................................13

References................................................................................................................................14

2ECONOMICS

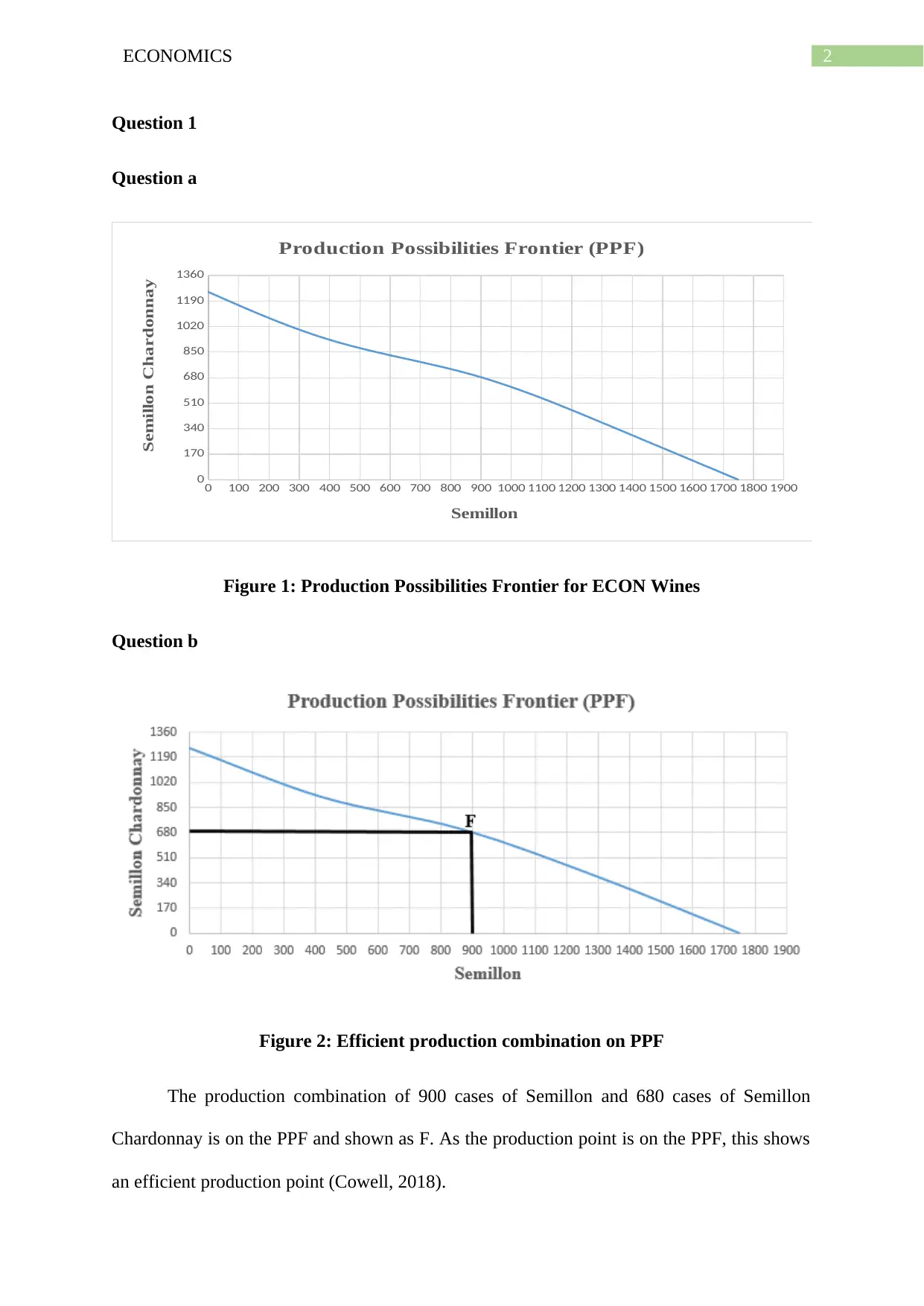

Question 1

Question a

0 100 200 300 400 500 600 700 800 900 1000 1100 1200 1300 1400 1500 1600 1700 1800 1900

0

170

340

510

680

850

1020

1190

1360

Production Possibilities Frontier (PPF)

Semillon

Semillon Chardonnay

Figure 1: Production Possibilities Frontier for ECON Wines

Question b

Figure 2: Efficient production combination on PPF

The production combination of 900 cases of Semillon and 680 cases of Semillon

Chardonnay is on the PPF and shown as F. As the production point is on the PPF, this shows

an efficient production point (Cowell, 2018).

Question 1

Question a

0 100 200 300 400 500 600 700 800 900 1000 1100 1200 1300 1400 1500 1600 1700 1800 1900

0

170

340

510

680

850

1020

1190

1360

Production Possibilities Frontier (PPF)

Semillon

Semillon Chardonnay

Figure 1: Production Possibilities Frontier for ECON Wines

Question b

Figure 2: Efficient production combination on PPF

The production combination of 900 cases of Semillon and 680 cases of Semillon

Chardonnay is on the PPF and shown as F. As the production point is on the PPF, this shows

an efficient production point (Cowell, 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ECONOMICS

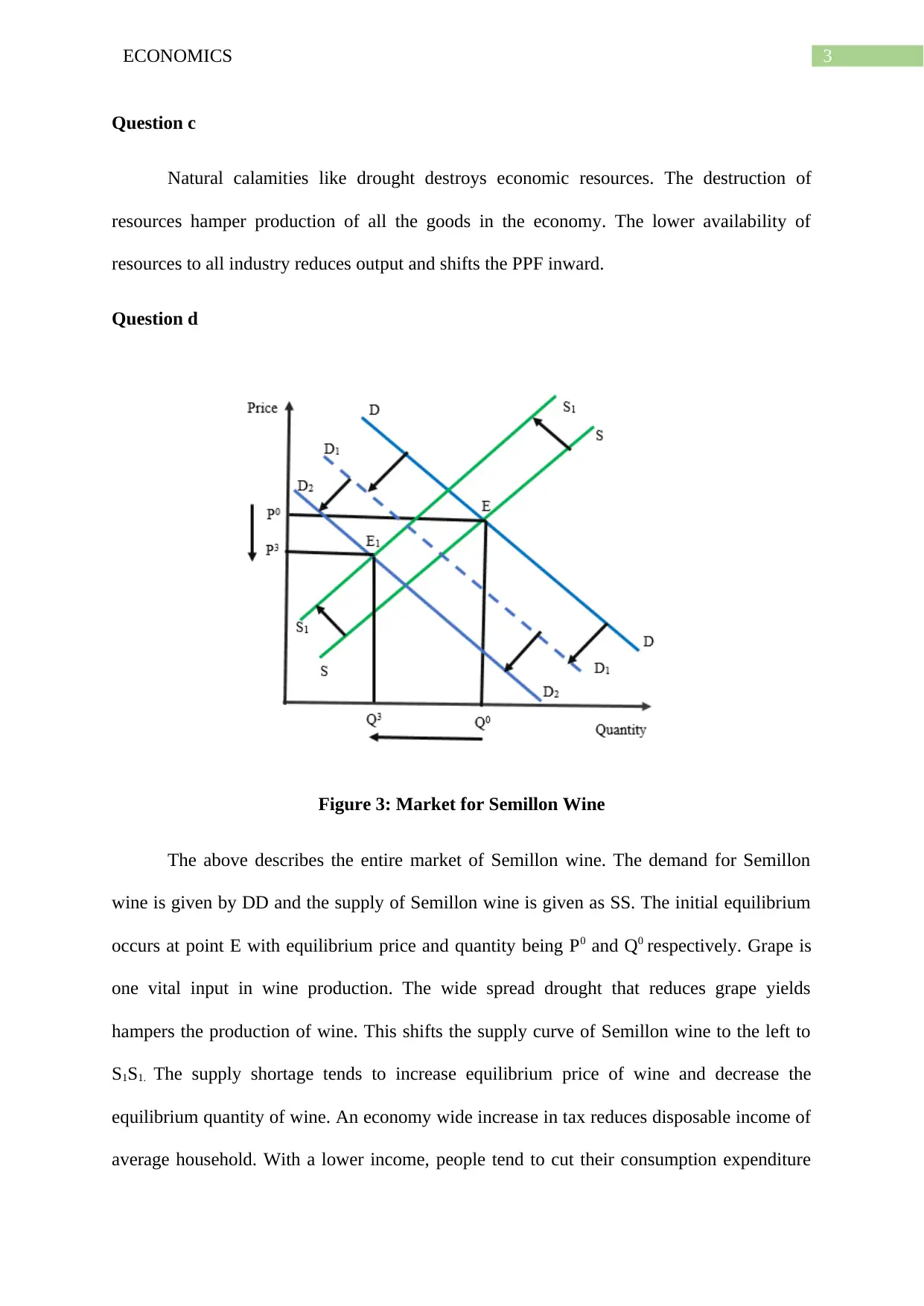

Question c

Natural calamities like drought destroys economic resources. The destruction of

resources hamper production of all the goods in the economy. The lower availability of

resources to all industry reduces output and shifts the PPF inward.

Question d

Figure 3: Market for Semillon Wine

The above describes the entire market of Semillon wine. The demand for Semillon

wine is given by DD and the supply of Semillon wine is given as SS. The initial equilibrium

occurs at point E with equilibrium price and quantity being P0 and Q0 respectively. Grape is

one vital input in wine production. The wide spread drought that reduces grape yields

hampers the production of wine. This shifts the supply curve of Semillon wine to the left to

S1S1. The supply shortage tends to increase equilibrium price of wine and decrease the

equilibrium quantity of wine. An economy wide increase in tax reduces disposable income of

average household. With a lower income, people tend to cut their consumption expenditure

Question c

Natural calamities like drought destroys economic resources. The destruction of

resources hamper production of all the goods in the economy. The lower availability of

resources to all industry reduces output and shifts the PPF inward.

Question d

Figure 3: Market for Semillon Wine

The above describes the entire market of Semillon wine. The demand for Semillon

wine is given by DD and the supply of Semillon wine is given as SS. The initial equilibrium

occurs at point E with equilibrium price and quantity being P0 and Q0 respectively. Grape is

one vital input in wine production. The wide spread drought that reduces grape yields

hampers the production of wine. This shifts the supply curve of Semillon wine to the left to

S1S1. The supply shortage tends to increase equilibrium price of wine and decrease the

equilibrium quantity of wine. An economy wide increase in tax reduces disposable income of

average household. With a lower income, people tend to cut their consumption expenditure

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ECONOMICS

(Friedman, 2017). As a result, the demand of wine will be reduced as shown by the inward of

supply curve from DD to D1D1. Demand of wine further reduces following a decrease in price

of beer. As beer and wine are substitute a decrease in price of beer encourages people to

consume more beer while discouraging consumption of wine. The demand curve of wine

again shifts leftward to D2D2. The lower demand causes a downward pressure on price. The

final equilibrium occurs where the new supply curve and new demand curve intersects. The

effect on equilibrium price depends on magnitude of change in demand and supply. As

change in demand far exceeds the change in supply, equilibrium price lowers to P3 and

equilibrium quantity lowers to Q3.

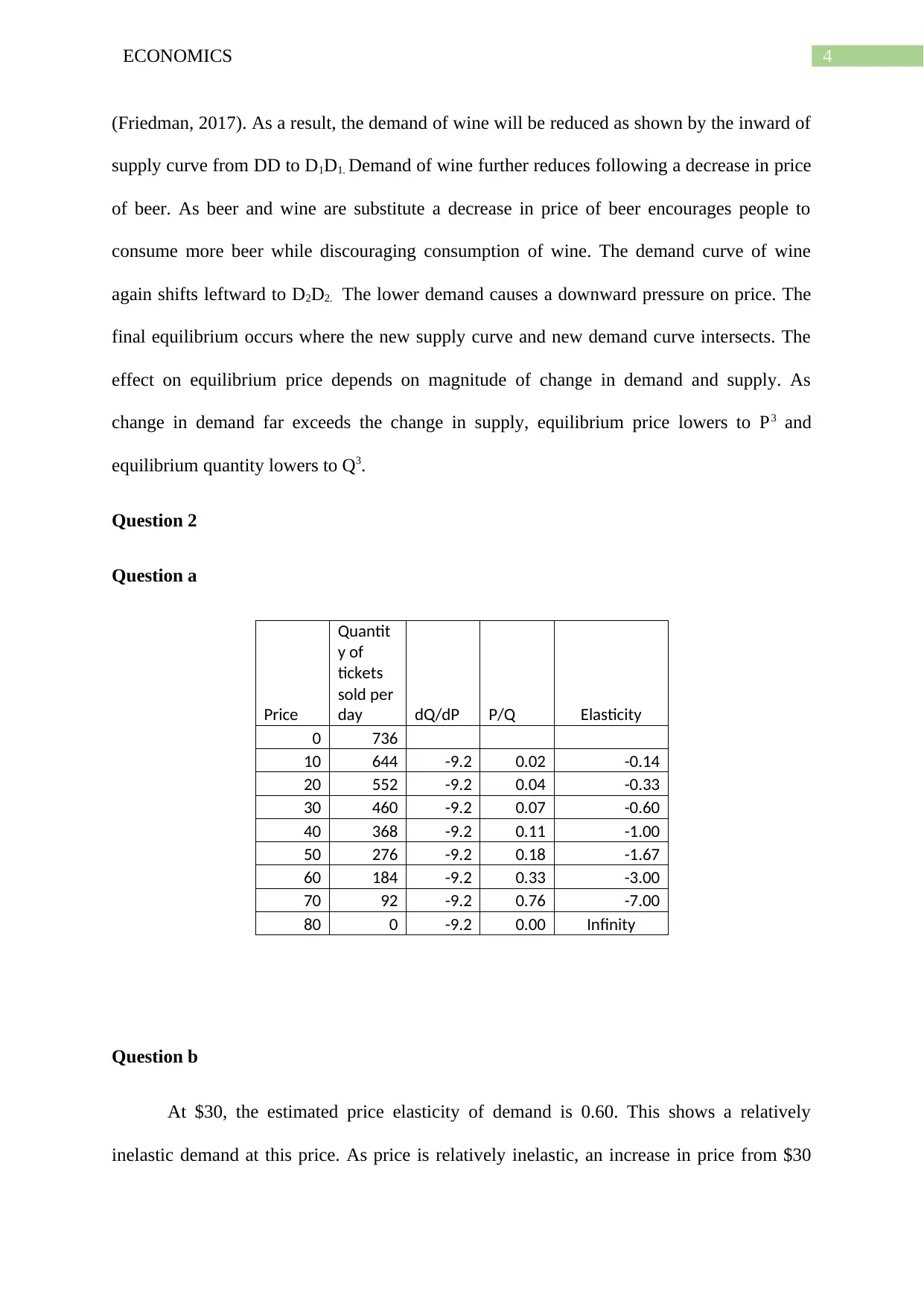

Question 2

Question a

Price

Quantit

y of

tickets

sold per

day dQ/dP P/Q Elasticity

0 736

10 644 -9.2 0.02 -0.14

20 552 -9.2 0.04 -0.33

30 460 -9.2 0.07 -0.60

40 368 -9.2 0.11 -1.00

50 276 -9.2 0.18 -1.67

60 184 -9.2 0.33 -3.00

70 92 -9.2 0.76 -7.00

80 0 -9.2 0.00 Infinity

Question b

At $30, the estimated price elasticity of demand is 0.60. This shows a relatively

inelastic demand at this price. As price is relatively inelastic, an increase in price from $30

(Friedman, 2017). As a result, the demand of wine will be reduced as shown by the inward of

supply curve from DD to D1D1. Demand of wine further reduces following a decrease in price

of beer. As beer and wine are substitute a decrease in price of beer encourages people to

consume more beer while discouraging consumption of wine. The demand curve of wine

again shifts leftward to D2D2. The lower demand causes a downward pressure on price. The

final equilibrium occurs where the new supply curve and new demand curve intersects. The

effect on equilibrium price depends on magnitude of change in demand and supply. As

change in demand far exceeds the change in supply, equilibrium price lowers to P3 and

equilibrium quantity lowers to Q3.

Question 2

Question a

Price

Quantit

y of

tickets

sold per

day dQ/dP P/Q Elasticity

0 736

10 644 -9.2 0.02 -0.14

20 552 -9.2 0.04 -0.33

30 460 -9.2 0.07 -0.60

40 368 -9.2 0.11 -1.00

50 276 -9.2 0.18 -1.67

60 184 -9.2 0.33 -3.00

70 92 -9.2 0.76 -7.00

80 0 -9.2 0.00 Infinity

Question b

At $30, the estimated price elasticity of demand is 0.60. This shows a relatively

inelastic demand at this price. As price is relatively inelastic, an increase in price from $30

5ECONOMICS

will increase revenue of the theatre company. Because of inelastic nature of demand, the

proportionate decrease in demand following the increase in price is less than the

proportionate increase in price (Baumol & Blinder, 2015). This results in an increase in

revenue following a price increase.

Question c

The obtained equation for daily demand for theatre ticket is

P=80−0.1087 Q

Question d

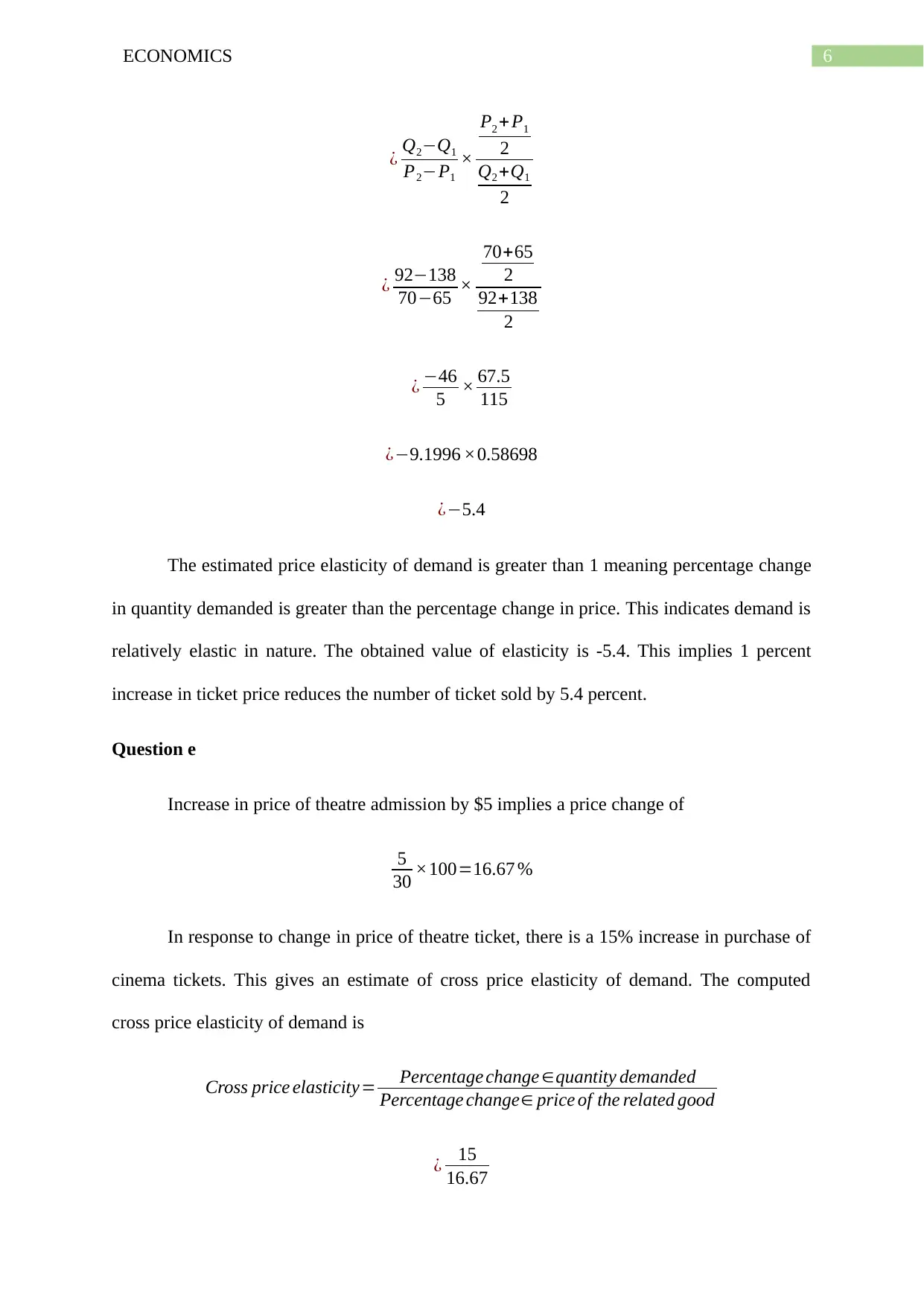

From estimated demand function in terms of Q can be rewritten as

Q= 80−P

0.1087

At price $65, the obtained demand for ticket is

Q= 80−65

0.1087

¿ 15

0.1087

¿ 138

At price $70, the demand for ticket is given as 92.

Price elasticity of demand ( Mid Point elasticty method ) = Percentage change ∈Quantity demanded

Percentage change∈ Price

¿ Change∈ quantity demanded

Change∈Price × Average Price

Average Quantity demand

will increase revenue of the theatre company. Because of inelastic nature of demand, the

proportionate decrease in demand following the increase in price is less than the

proportionate increase in price (Baumol & Blinder, 2015). This results in an increase in

revenue following a price increase.

Question c

The obtained equation for daily demand for theatre ticket is

P=80−0.1087 Q

Question d

From estimated demand function in terms of Q can be rewritten as

Q= 80−P

0.1087

At price $65, the obtained demand for ticket is

Q= 80−65

0.1087

¿ 15

0.1087

¿ 138

At price $70, the demand for ticket is given as 92.

Price elasticity of demand ( Mid Point elasticty method ) = Percentage change ∈Quantity demanded

Percentage change∈ Price

¿ Change∈ quantity demanded

Change∈Price × Average Price

Average Quantity demand

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ECONOMICS

¿ Q2−Q1

P2−P1

×

P2 + P1

2

Q2 +Q1

2

¿ 92−138

70−65 ×

70+65

2

92+138

2

¿ −46

5 × 67.5

115

¿−9.1996 ×0.58698

¿−5.4

The estimated price elasticity of demand is greater than 1 meaning percentage change

in quantity demanded is greater than the percentage change in price. This indicates demand is

relatively elastic in nature. The obtained value of elasticity is -5.4. This implies 1 percent

increase in ticket price reduces the number of ticket sold by 5.4 percent.

Question e

Increase in price of theatre admission by $5 implies a price change of

5

30 ×100=16.67 %

In response to change in price of theatre ticket, there is a 15% increase in purchase of

cinema tickets. This gives an estimate of cross price elasticity of demand. The computed

cross price elasticity of demand is

Cross price elasticity= Percentage change ∈quantity demanded

Percentage change∈ price of the related good

¿ 15

16.67

¿ Q2−Q1

P2−P1

×

P2 + P1

2

Q2 +Q1

2

¿ 92−138

70−65 ×

70+65

2

92+138

2

¿ −46

5 × 67.5

115

¿−9.1996 ×0.58698

¿−5.4

The estimated price elasticity of demand is greater than 1 meaning percentage change

in quantity demanded is greater than the percentage change in price. This indicates demand is

relatively elastic in nature. The obtained value of elasticity is -5.4. This implies 1 percent

increase in ticket price reduces the number of ticket sold by 5.4 percent.

Question e

Increase in price of theatre admission by $5 implies a price change of

5

30 ×100=16.67 %

In response to change in price of theatre ticket, there is a 15% increase in purchase of

cinema tickets. This gives an estimate of cross price elasticity of demand. The computed

cross price elasticity of demand is

Cross price elasticity= Percentage change ∈quantity demanded

Percentage change∈ price of the related good

¿ 15

16.67

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ECONOMICS

¿ 0. 90

The obtained cross price elasticity shows that 1 percent increase in price of cinema

theatre admission increases demand for cinema tickets by 0.9 percent.

The elasticity value tells the cinema managers that theatre ticket price and cinema

tickets are substitutes (Cowen & Tabarrok, 2015).

Given the information that increase in price results in a 15% increase in purchase of

cinema tickets, number of cinema tickets purchased after increase in ticket price of theatre is

obtained as

350+ ( 350 ×15 % )

¿ 350+52.5

¿ 402.5 403

Question 3

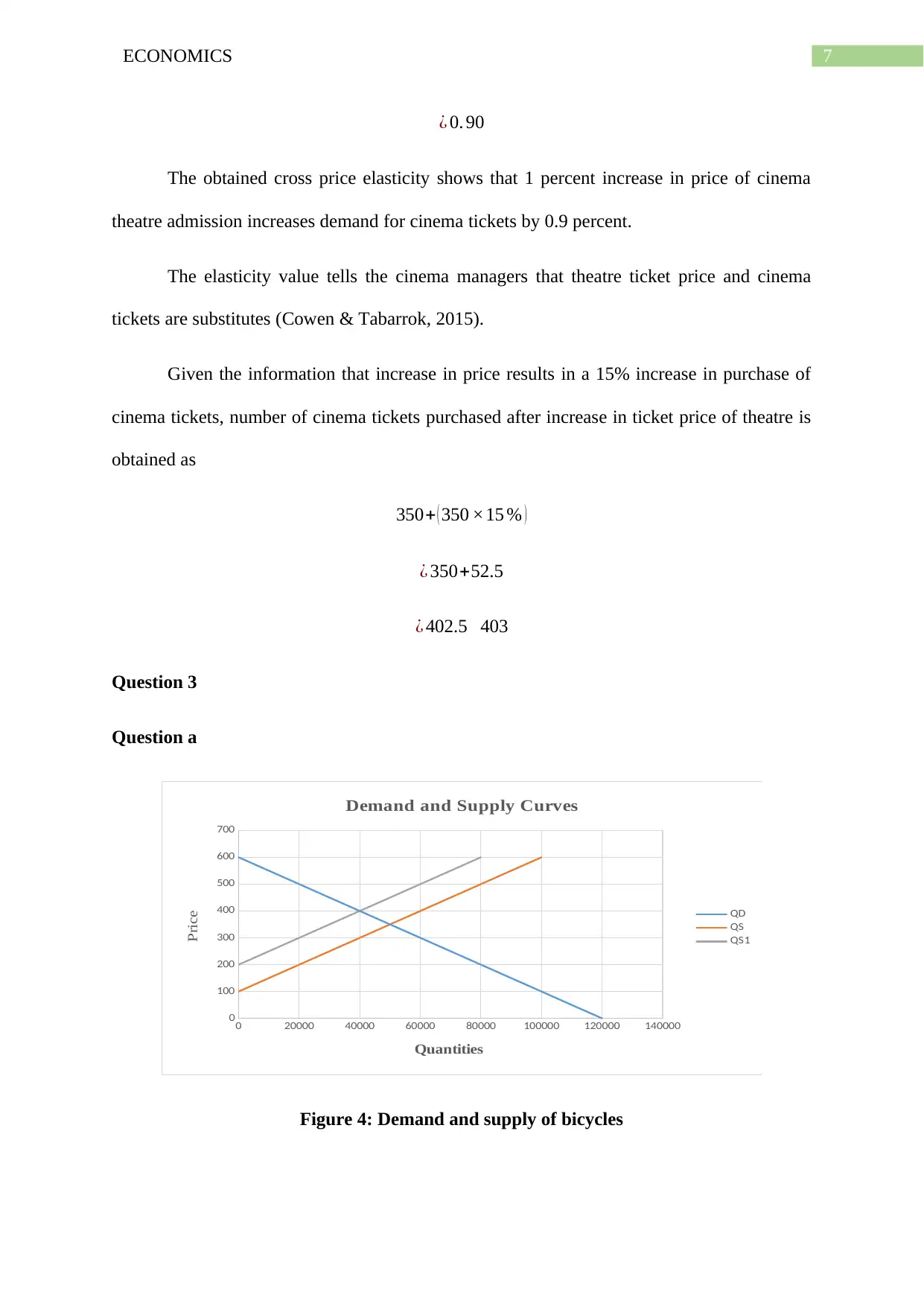

Question a

0 20000 40000 60000 80000 100000 120000 140000

0

100

200

300

400

500

600

700

Demand and Supply Curves

QD

QS

QS1

Quantities

Price

Figure 4: Demand and supply of bicycles

¿ 0. 90

The obtained cross price elasticity shows that 1 percent increase in price of cinema

theatre admission increases demand for cinema tickets by 0.9 percent.

The elasticity value tells the cinema managers that theatre ticket price and cinema

tickets are substitutes (Cowen & Tabarrok, 2015).

Given the information that increase in price results in a 15% increase in purchase of

cinema tickets, number of cinema tickets purchased after increase in ticket price of theatre is

obtained as

350+ ( 350 ×15 % )

¿ 350+52.5

¿ 402.5 403

Question 3

Question a

0 20000 40000 60000 80000 100000 120000 140000

0

100

200

300

400

500

600

700

Demand and Supply Curves

QD

QS

QS1

Quantities

Price

Figure 4: Demand and supply of bicycles

8ECONOMICS

Question b

The initial equilibrium price of bicycle is $500 and equilibrium quantity of bicycle is

50000.

Question c

After the imposition of tax equilibrium price increases to $400 while equilibrium

quantity of bicycles is 40000.

Question d

Of the imposed tax of $100, $50 is borne by the sellers of bicycles and rest of the $50

is borne by the seller of bicycles.

Question e

Tax Revenue=unit tax ×Quantities sold

¿ $ 100× 40000

¿ $ 4000000

Question f

Consumer surplus before tax

CS=1

2 × ( 600−350 ) × 50000

¿ 1

2 ×250 ×50000

¿ 6250000

Consumer surplus after tax

Question b

The initial equilibrium price of bicycle is $500 and equilibrium quantity of bicycle is

50000.

Question c

After the imposition of tax equilibrium price increases to $400 while equilibrium

quantity of bicycles is 40000.

Question d

Of the imposed tax of $100, $50 is borne by the sellers of bicycles and rest of the $50

is borne by the seller of bicycles.

Question e

Tax Revenue=unit tax ×Quantities sold

¿ $ 100× 40000

¿ $ 4000000

Question f

Consumer surplus before tax

CS=1

2 × ( 600−350 ) × 50000

¿ 1

2 ×250 ×50000

¿ 6250000

Consumer surplus after tax

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ECONOMICS

CS=1

2 × ( 600−400 ) ×40000

¿ 1

2 ×200 × 40000

¿ 4000000

Change∈consumer surplus=6250000−4000000

¿ 2250000

There is a loss in consumer surplus by 2250000

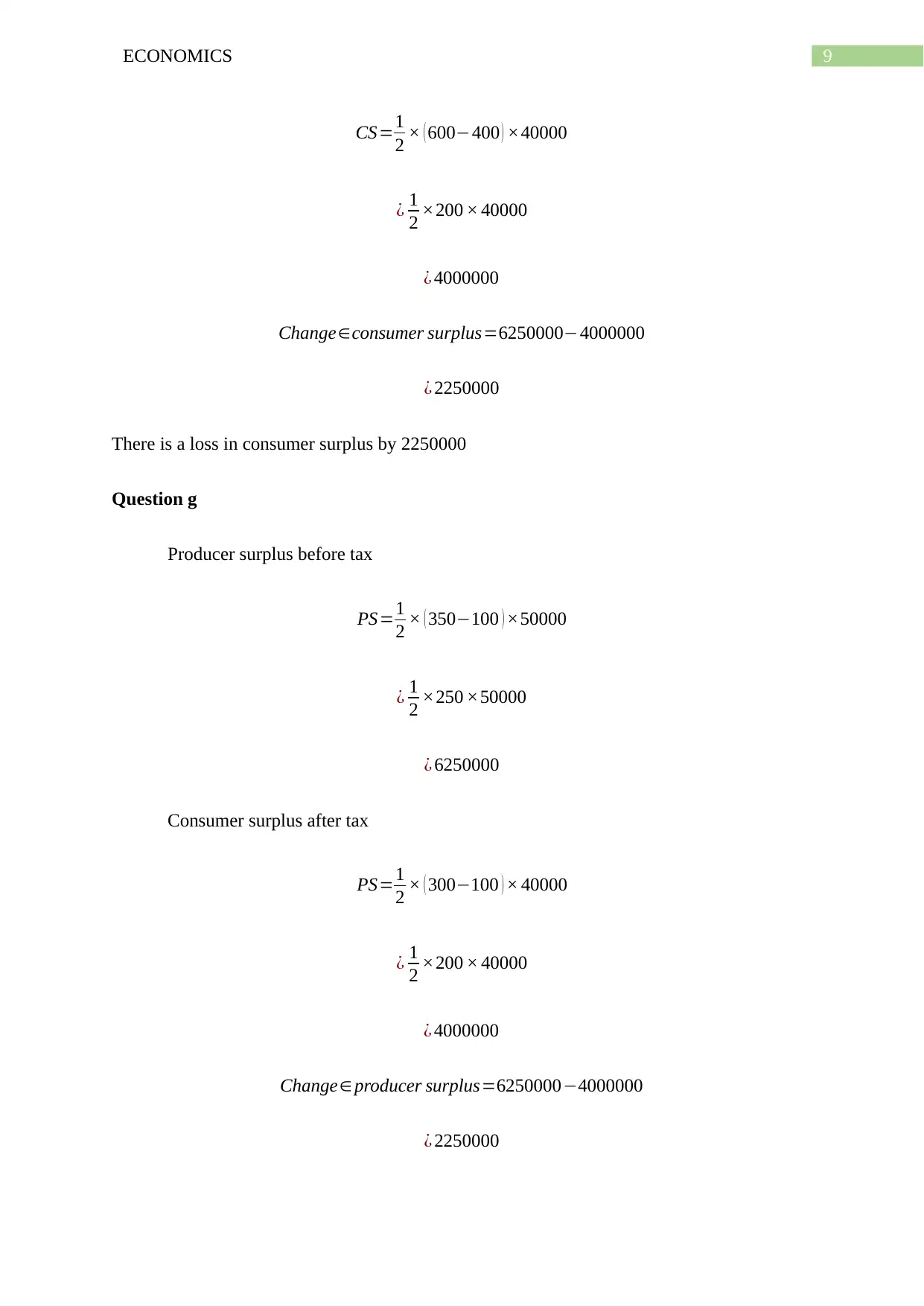

Question g

Producer surplus before tax

PS=1

2 × ( 350−100 ) ×50000

¿ 1

2 ×250 ×50000

¿ 6250000

Consumer surplus after tax

PS=1

2 × ( 300−100 ) × 40000

¿ 1

2 ×200 × 40000

¿ 4000000

Change∈ producer surplus=6250000−4000000

¿ 2250000

CS=1

2 × ( 600−400 ) ×40000

¿ 1

2 ×200 × 40000

¿ 4000000

Change∈consumer surplus=6250000−4000000

¿ 2250000

There is a loss in consumer surplus by 2250000

Question g

Producer surplus before tax

PS=1

2 × ( 350−100 ) ×50000

¿ 1

2 ×250 ×50000

¿ 6250000

Consumer surplus after tax

PS=1

2 × ( 300−100 ) × 40000

¿ 1

2 ×200 × 40000

¿ 4000000

Change∈ producer surplus=6250000−4000000

¿ 2250000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ECONOMICS

There is a loss in producer surplus by 2250000

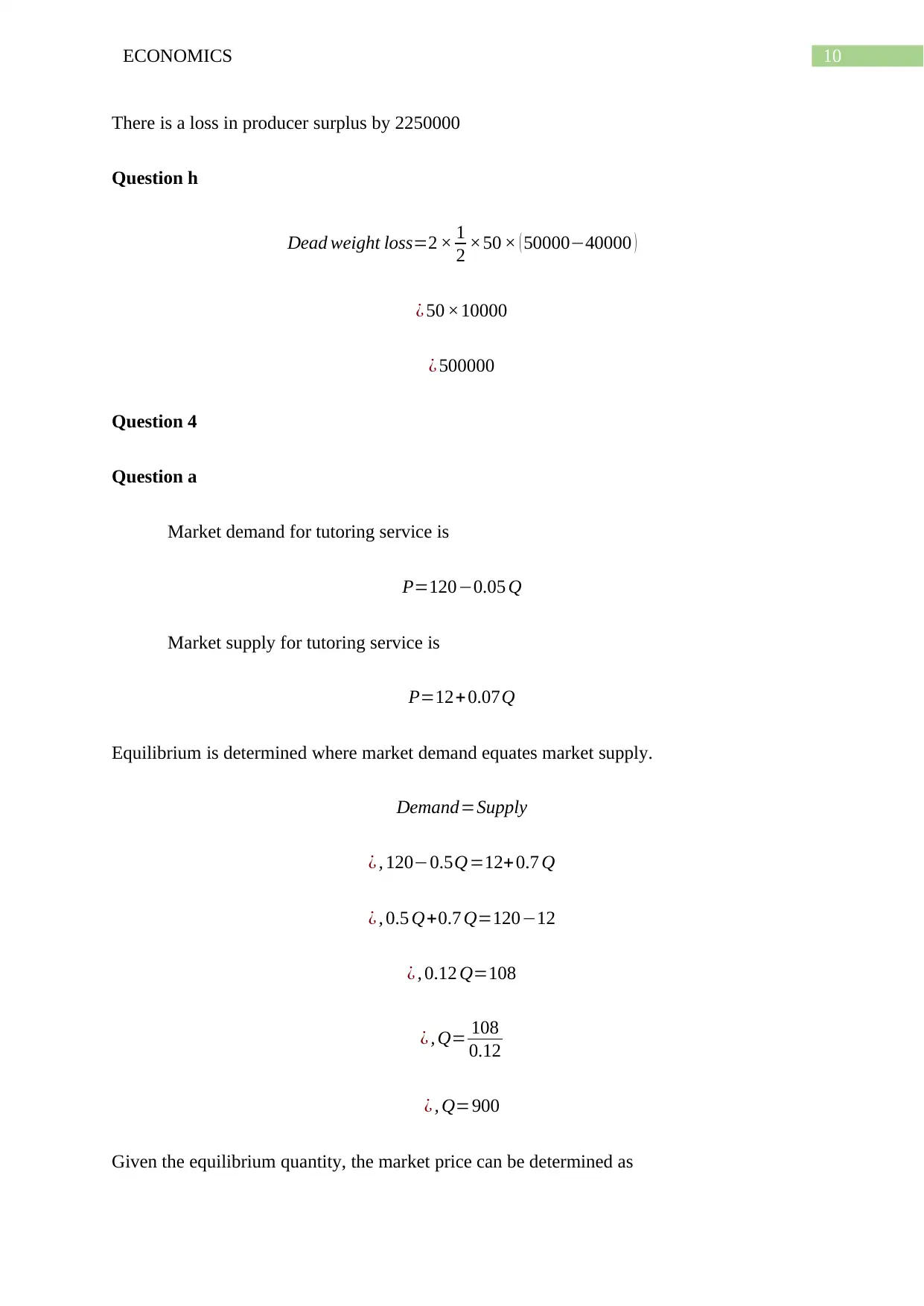

Question h

Dead weight loss=2 × 1

2 ×50 × ( 50000−40000 )

¿ 50 ×10000

¿ 500000

Question 4

Question a

Market demand for tutoring service is

P=120−0.05 Q

Market supply for tutoring service is

P=12+0.07Q

Equilibrium is determined where market demand equates market supply.

Demand=Supply

¿ , 120−0.5Q=12+0.7 Q

¿ , 0.5 Q+0.7 Q=120−12

¿ , 0.12 Q=108

¿ , Q= 108

0.12

¿ , Q=900

Given the equilibrium quantity, the market price can be determined as

There is a loss in producer surplus by 2250000

Question h

Dead weight loss=2 × 1

2 ×50 × ( 50000−40000 )

¿ 50 ×10000

¿ 500000

Question 4

Question a

Market demand for tutoring service is

P=120−0.05 Q

Market supply for tutoring service is

P=12+0.07Q

Equilibrium is determined where market demand equates market supply.

Demand=Supply

¿ , 120−0.5Q=12+0.7 Q

¿ , 0.5 Q+0.7 Q=120−12

¿ , 0.12 Q=108

¿ , Q= 108

0.12

¿ , Q=900

Given the equilibrium quantity, the market price can be determined as

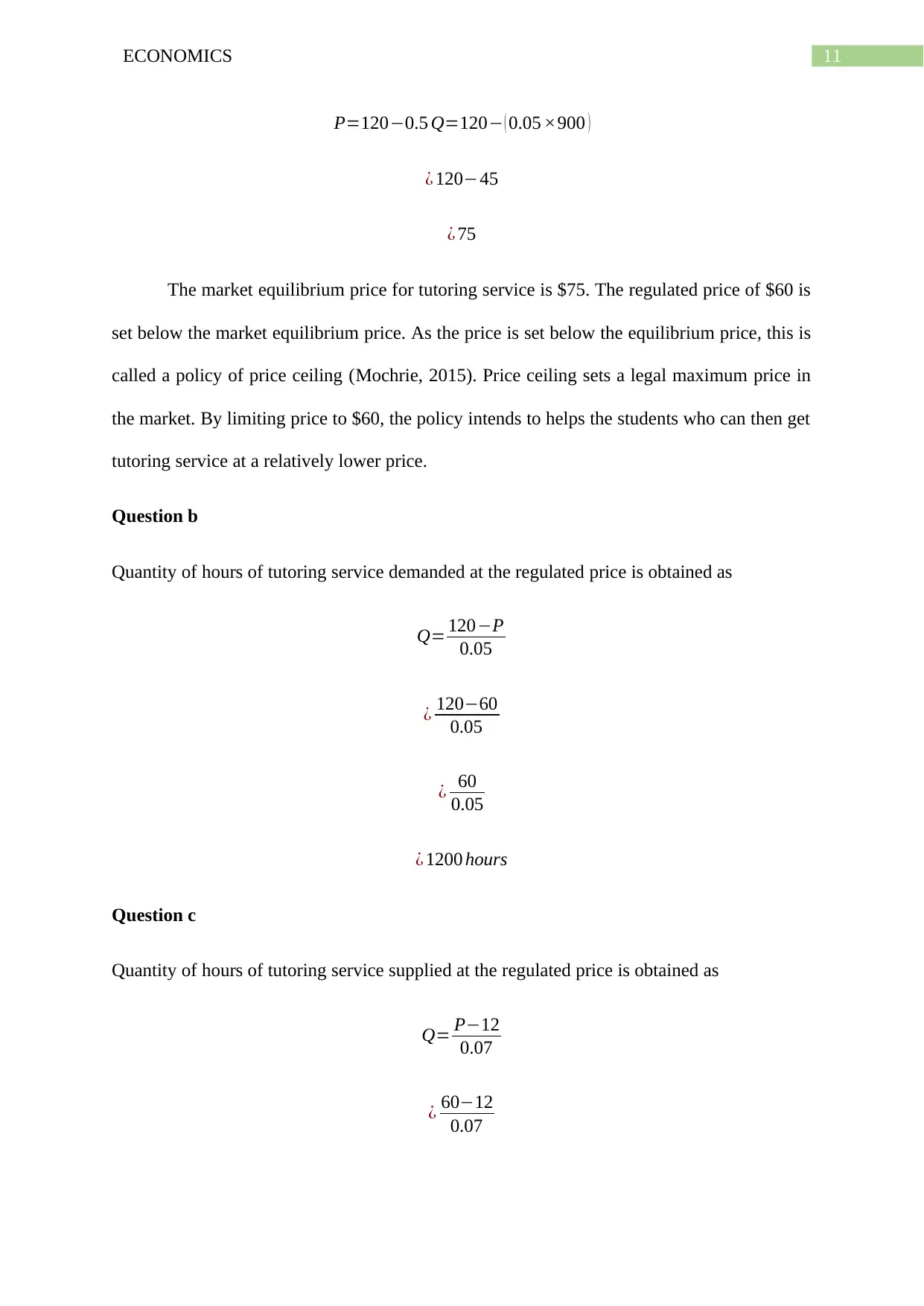

11ECONOMICS

P=120−0.5 Q=120− ( 0.05 ×900 )

¿ 120−45

¿ 75

The market equilibrium price for tutoring service is $75. The regulated price of $60 is

set below the market equilibrium price. As the price is set below the equilibrium price, this is

called a policy of price ceiling (Mochrie, 2015). Price ceiling sets a legal maximum price in

the market. By limiting price to $60, the policy intends to helps the students who can then get

tutoring service at a relatively lower price.

Question b

Quantity of hours of tutoring service demanded at the regulated price is obtained as

Q= 120−P

0.05

¿ 120−60

0.05

¿ 60

0.05

¿ 1200 hours

Question c

Quantity of hours of tutoring service supplied at the regulated price is obtained as

Q= P−12

0.07

¿ 60−12

0.07

P=120−0.5 Q=120− ( 0.05 ×900 )

¿ 120−45

¿ 75

The market equilibrium price for tutoring service is $75. The regulated price of $60 is

set below the market equilibrium price. As the price is set below the equilibrium price, this is

called a policy of price ceiling (Mochrie, 2015). Price ceiling sets a legal maximum price in

the market. By limiting price to $60, the policy intends to helps the students who can then get

tutoring service at a relatively lower price.

Question b

Quantity of hours of tutoring service demanded at the regulated price is obtained as

Q= 120−P

0.05

¿ 120−60

0.05

¿ 60

0.05

¿ 1200 hours

Question c

Quantity of hours of tutoring service supplied at the regulated price is obtained as

Q= P−12

0.07

¿ 60−12

0.07

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.