ECO1000 Economics Assignment: Evaluating Tax on Sugary Drinks

VerifiedAdded on 2023/04/21

|9

|2278

|185

Essay

AI Summary

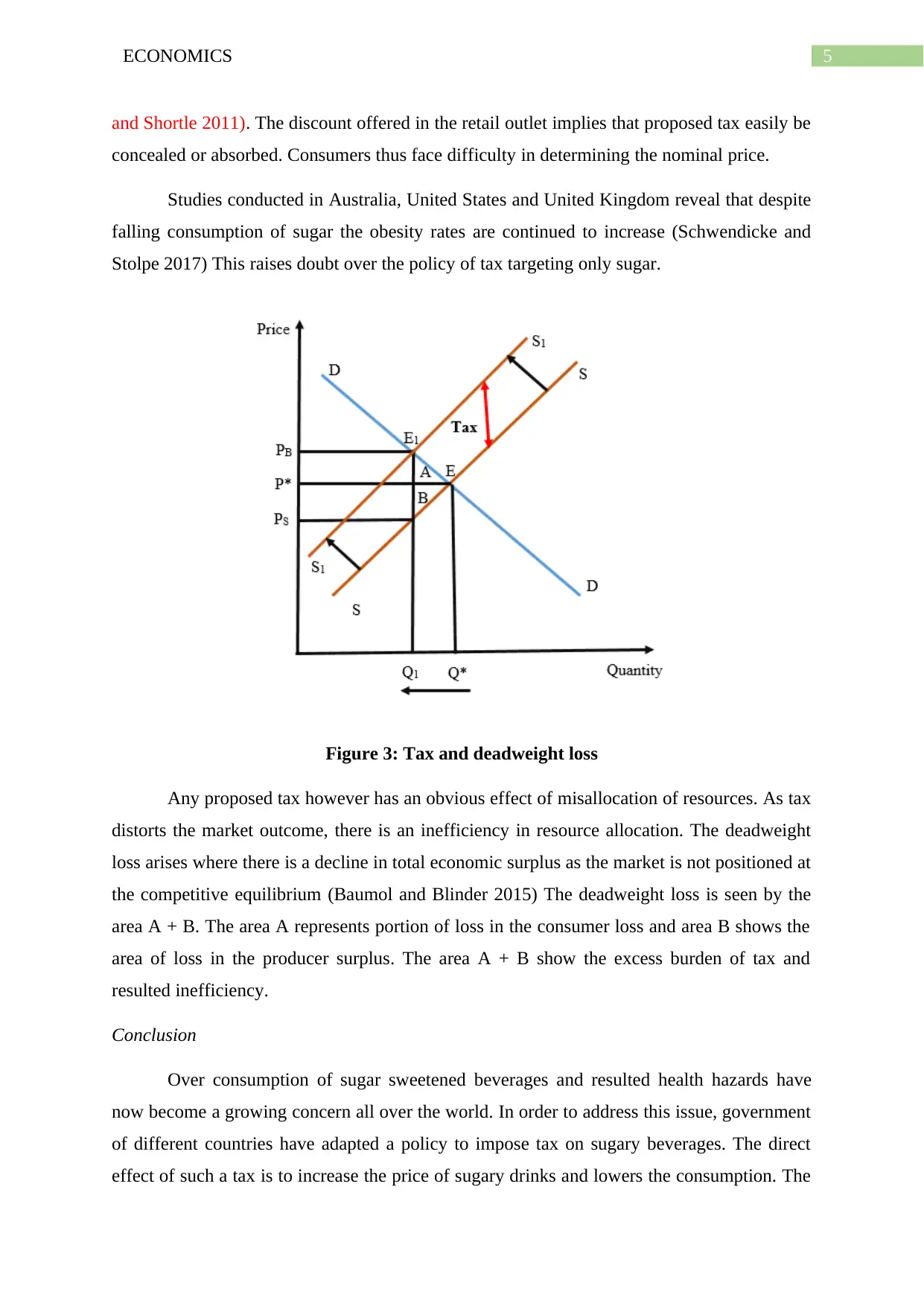

This essay provides an in-depth evaluation of the economic consequences of imposing taxes on sugar-sweetened beverages (SSBs). It begins by highlighting the growing health concerns associated with excessive sugar consumption, including the rise in type II diabetes, heart diseases, and obesity. The analysis uses a demand-supply model to illustrate how a tax on SSBs increases prices for consumers and reduces the effective price received by sellers, leading to a decrease in the equilibrium quantity sold. The essay also discusses the price elasticity of demand for SSBs, noting its inelastic nature due to the addictive qualities of sugar. Alternative policies, such as setting a price floor and health awareness campaigns, are considered. Furthermore, the effectiveness of taxation in reducing SSB consumption is examined, along with criticisms regarding its regressive nature and potential for resource misallocation, resulting in deadweight loss. The essay concludes that while SSB taxes can raise revenue and potentially reduce consumption, their effectiveness depends on demand elasticity and the availability of substitutes, suggesting that a comprehensive approach, including education and alternative policies, may be more effective in addressing the health issues associated with excessive sugar consumption. Desklib provides a platform to explore similar assignments and study resources for students.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.