Economics Assignment: Exploring Microeconomic Principles and Concepts

VerifiedAdded on 2023/04/23

|14

|2267

|433

Homework Assignment

AI Summary

This economics assignment explores microeconomic principles through a series of questions. It analyzes the impact of price changes of substitute goods on demand, the effects of new technology on supply, and the influence of income on demand, using woollen jumpers as an example. The assignment also distinguishes between changes in quantity demanded and changes in demand, using the garlic market as an illustration. Furthermore, it examines the combined effects of changes in demand and supply on market equilibrium, considering the chicken market and the impact of bird flu. The assignment also calculates and interprets price elasticity of demand and discusses its implications for revenue maximization. Finally, it addresses the long-run effects of economic profit and the role of entry barriers in an industry, particularly in the context of internet platforms.

Running head: ECONOMICS

Economics

Name of the Student

Name of the University

Course ID

Economics

Name of the Student

Name of the University

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ECONOMICS

Table of Contents

Answer 1....................................................................................................................................2

Answer a.................................................................................................................................2

Answer b................................................................................................................................3

Answer c.................................................................................................................................4

Answer 2....................................................................................................................................5

Answer 3....................................................................................................................................6

Answer 4....................................................................................................................................8

Answer a.................................................................................................................................8

Answer b................................................................................................................................9

Answer 5....................................................................................................................................9

Reference list............................................................................................................................12

Table of Contents

Answer 1....................................................................................................................................2

Answer a.................................................................................................................................2

Answer b................................................................................................................................3

Answer c.................................................................................................................................4

Answer 2....................................................................................................................................5

Answer 3....................................................................................................................................6

Answer 4....................................................................................................................................8

Answer a.................................................................................................................................8

Answer b................................................................................................................................9

Answer 5....................................................................................................................................9

Reference list............................................................................................................................12

2ECONOMICS

Answer 1

Answer a

Price of related goods is a significant determinant of demand. For substitute goods,

change in price of one good has a positive effect on demand of the related good. With

increase in price of one good, demand for the substitute good increases and vice-versa. Now,

given that leather jackets are substitutes of woollen jumpers, a decrease in price of leather

jacket decreases the demand for woollen jumpers (Cowell 2018). This is because, with a

decrease in price of leather jacket, the relative price of woollen jumpers increase, which

reduces its demand. The equilibrium adjustment in the market of woollen jumper is described

below.

Figure 1: Impact of a price decrease of leather jacket

(As created by Author)

In figure 1, the initial demand and supply condition in woollen jumper market are

portrait by the respective demand and supply curve of DD and SS. Now, following a decline

in price of leather jackets, demand for leather jacket increases (Friedman 2017). As people

Answer 1

Answer a

Price of related goods is a significant determinant of demand. For substitute goods,

change in price of one good has a positive effect on demand of the related good. With

increase in price of one good, demand for the substitute good increases and vice-versa. Now,

given that leather jackets are substitutes of woollen jumpers, a decrease in price of leather

jacket decreases the demand for woollen jumpers (Cowell 2018). This is because, with a

decrease in price of leather jacket, the relative price of woollen jumpers increase, which

reduces its demand. The equilibrium adjustment in the market of woollen jumper is described

below.

Figure 1: Impact of a price decrease of leather jacket

(As created by Author)

In figure 1, the initial demand and supply condition in woollen jumper market are

portrait by the respective demand and supply curve of DD and SS. Now, following a decline

in price of leather jackets, demand for leather jacket increases (Friedman 2017). As people

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ECONOMICS

purchase more leather jackets, demand for woollen jumpers fall. Consequently, demand curve

for woollen jumpers shifts inward to D1D1. Lower demand reduces equilibrium price of

woollen jumpers to P1. The equilibrium quantity falls to Q1.

Answer b

The adaption of new machines, which has increased the productivity of knitting

industry increase supply of woollen jumpers in the industry. At each price, there is now a

larger quantity of woollen jumper available in the market. The increase in supply of woollen

jumpers increases equilibrium quantity and reduces equilibrium price (Stoneman, Bartoloni

and Baussola 2018). The process of equilibrium adjustment in the market is explained with

the help of following figure.

Figure 2: Impact of new productive technology in knitting industry

(As created by Author)

The resulted increase in supply following adaption of new technology increase supply

of woollen jumpers. The supply curve shifts outward. The new supply curve is obtained as

S1S1. New equilibrium in the market occurs where new supply curve and existing demand

purchase more leather jackets, demand for woollen jumpers fall. Consequently, demand curve

for woollen jumpers shifts inward to D1D1. Lower demand reduces equilibrium price of

woollen jumpers to P1. The equilibrium quantity falls to Q1.

Answer b

The adaption of new machines, which has increased the productivity of knitting

industry increase supply of woollen jumpers in the industry. At each price, there is now a

larger quantity of woollen jumper available in the market. The increase in supply of woollen

jumpers increases equilibrium quantity and reduces equilibrium price (Stoneman, Bartoloni

and Baussola 2018). The process of equilibrium adjustment in the market is explained with

the help of following figure.

Figure 2: Impact of new productive technology in knitting industry

(As created by Author)

The resulted increase in supply following adaption of new technology increase supply

of woollen jumpers. The supply curve shifts outward. The new supply curve is obtained as

S1S1. New equilibrium in the market occurs where new supply curve and existing demand

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ECONOMICS

curve intersect (Mankiw 2014). Corresponding to new equilibrium price lowers to the level

P1. The equilibrium quantity in the market increases to Q1.

Answer c

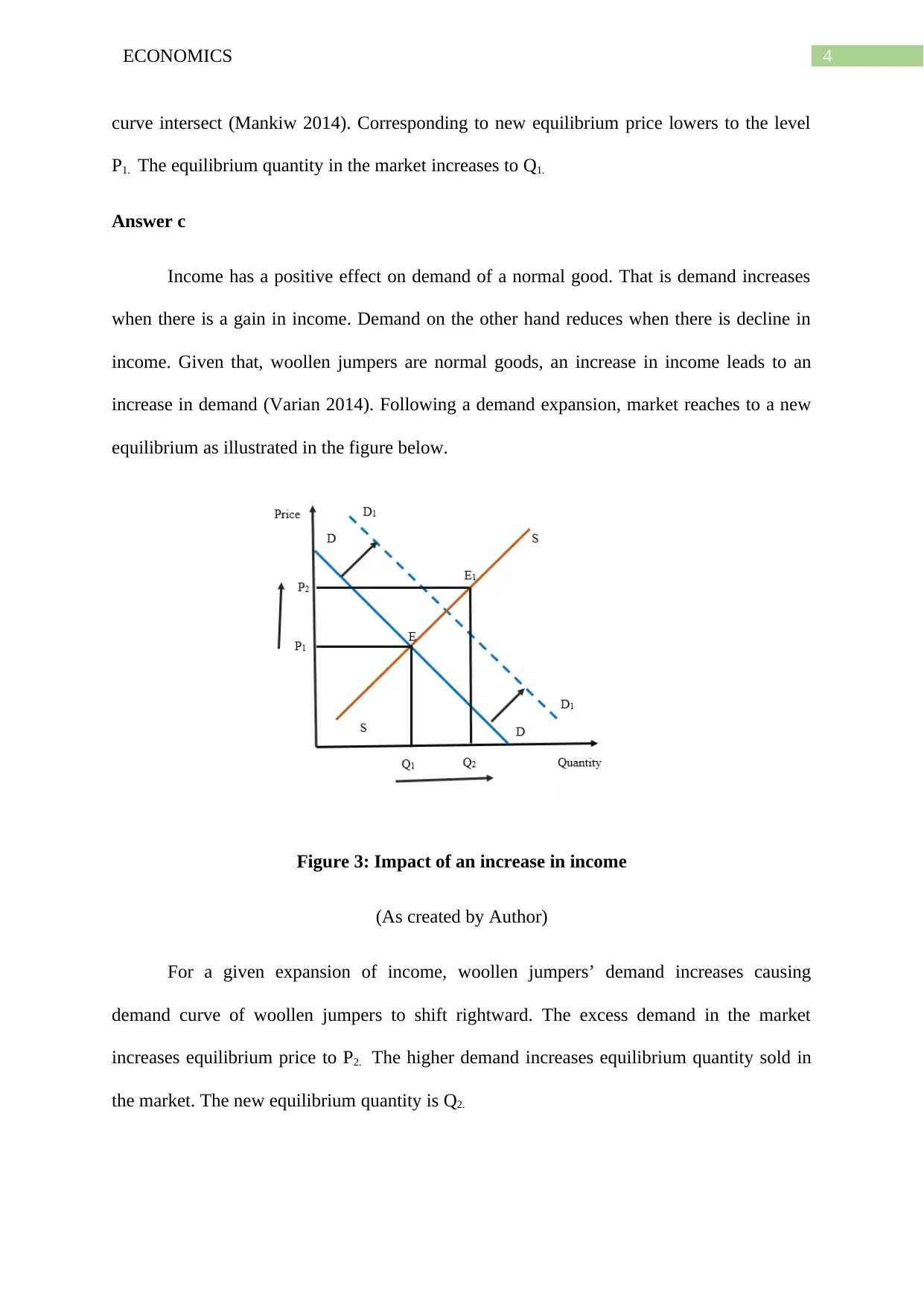

Income has a positive effect on demand of a normal good. That is demand increases

when there is a gain in income. Demand on the other hand reduces when there is decline in

income. Given that, woollen jumpers are normal goods, an increase in income leads to an

increase in demand (Varian 2014). Following a demand expansion, market reaches to a new

equilibrium as illustrated in the figure below.

Figure 3: Impact of an increase in income

(As created by Author)

For a given expansion of income, woollen jumpers’ demand increases causing

demand curve of woollen jumpers to shift rightward. The excess demand in the market

increases equilibrium price to P2. The higher demand increases equilibrium quantity sold in

the market. The new equilibrium quantity is Q2.

curve intersect (Mankiw 2014). Corresponding to new equilibrium price lowers to the level

P1. The equilibrium quantity in the market increases to Q1.

Answer c

Income has a positive effect on demand of a normal good. That is demand increases

when there is a gain in income. Demand on the other hand reduces when there is decline in

income. Given that, woollen jumpers are normal goods, an increase in income leads to an

increase in demand (Varian 2014). Following a demand expansion, market reaches to a new

equilibrium as illustrated in the figure below.

Figure 3: Impact of an increase in income

(As created by Author)

For a given expansion of income, woollen jumpers’ demand increases causing

demand curve of woollen jumpers to shift rightward. The excess demand in the market

increases equilibrium price to P2. The higher demand increases equilibrium quantity sold in

the market. The new equilibrium quantity is Q2.

5ECONOMICS

Answer 2

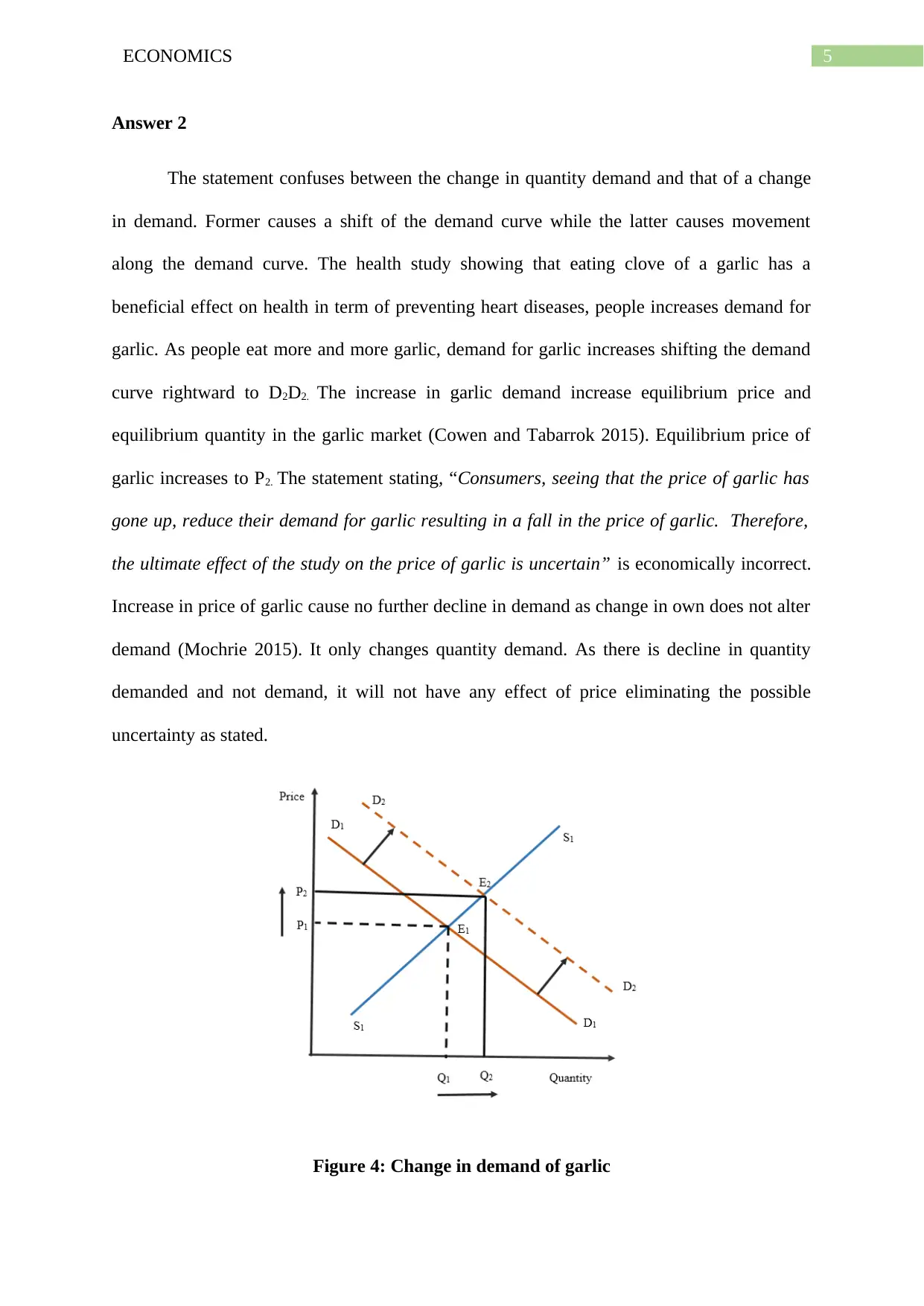

The statement confuses between the change in quantity demand and that of a change

in demand. Former causes a shift of the demand curve while the latter causes movement

along the demand curve. The health study showing that eating clove of a garlic has a

beneficial effect on health in term of preventing heart diseases, people increases demand for

garlic. As people eat more and more garlic, demand for garlic increases shifting the demand

curve rightward to D2D2. The increase in garlic demand increase equilibrium price and

equilibrium quantity in the garlic market (Cowen and Tabarrok 2015). Equilibrium price of

garlic increases to P2. The statement stating, “Consumers, seeing that the price of garlic has

gone up, reduce their demand for garlic resulting in a fall in the price of garlic. Therefore,

the ultimate effect of the study on the price of garlic is uncertain” is economically incorrect.

Increase in price of garlic cause no further decline in demand as change in own does not alter

demand (Mochrie 2015). It only changes quantity demand. As there is decline in quantity

demanded and not demand, it will not have any effect of price eliminating the possible

uncertainty as stated.

Figure 4: Change in demand of garlic

Answer 2

The statement confuses between the change in quantity demand and that of a change

in demand. Former causes a shift of the demand curve while the latter causes movement

along the demand curve. The health study showing that eating clove of a garlic has a

beneficial effect on health in term of preventing heart diseases, people increases demand for

garlic. As people eat more and more garlic, demand for garlic increases shifting the demand

curve rightward to D2D2. The increase in garlic demand increase equilibrium price and

equilibrium quantity in the garlic market (Cowen and Tabarrok 2015). Equilibrium price of

garlic increases to P2. The statement stating, “Consumers, seeing that the price of garlic has

gone up, reduce their demand for garlic resulting in a fall in the price of garlic. Therefore,

the ultimate effect of the study on the price of garlic is uncertain” is economically incorrect.

Increase in price of garlic cause no further decline in demand as change in own does not alter

demand (Mochrie 2015). It only changes quantity demand. As there is decline in quantity

demanded and not demand, it will not have any effect of price eliminating the possible

uncertainty as stated.

Figure 4: Change in demand of garlic

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ECONOMICS

(As created by Author)

Answer 3

The combined forces of demand and supply determines equilibrium in the market.

Change in either demand or supply or both change the equilibrium position altering

equilibrium price and quantity. The demand for chicken in Sweden decrease due to the

discovery of bird flu. Contraction in demand causes the demand cure to shifts to left. Decline

in demand likely to cause a decline in both equilibrium price and equilibrium quantity

(Kolmar 2017). At the same time, precautionary measures taken by the government reduces

the stick of chicken in the country. The fall in supply causes equilibrium quantity to increase

while equilibrium quantity falls. As both demand and supply, push equilibrium quantity of

chicken downward, the equilibrium quantity of live chicken decreases at the new equilibrium.

The effect on equilibrium price however is ambiguous. The decline in demand pushes down

equilibrium price while a fall in supply creates an upward pressure on equilibrium price.

Price can either increase or decrease or stays same. The net effect on price depends on the

magnitude of forces of demand and supply. The three possible change in the market for live

chicken is described below.

Case 1: Demand changes more than supply

Figure 5: Demand changes more than supply

(As created by Author)

Answer 3

The combined forces of demand and supply determines equilibrium in the market.

Change in either demand or supply or both change the equilibrium position altering

equilibrium price and quantity. The demand for chicken in Sweden decrease due to the

discovery of bird flu. Contraction in demand causes the demand cure to shifts to left. Decline

in demand likely to cause a decline in both equilibrium price and equilibrium quantity

(Kolmar 2017). At the same time, precautionary measures taken by the government reduces

the stick of chicken in the country. The fall in supply causes equilibrium quantity to increase

while equilibrium quantity falls. As both demand and supply, push equilibrium quantity of

chicken downward, the equilibrium quantity of live chicken decreases at the new equilibrium.

The effect on equilibrium price however is ambiguous. The decline in demand pushes down

equilibrium price while a fall in supply creates an upward pressure on equilibrium price.

Price can either increase or decrease or stays same. The net effect on price depends on the

magnitude of forces of demand and supply. The three possible change in the market for live

chicken is described below.

Case 1: Demand changes more than supply

Figure 5: Demand changes more than supply

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ECONOMICS

(As created by Author)

In this situation, the decline in demand exceeds that of the supply contraction.

Accordingly, demand curve shifts from DD to D1D1. The shift n supply curve is relatively

small from SS to S1S1. As the demand effect dominates, there is a decline in equilibrium price

and quantity.

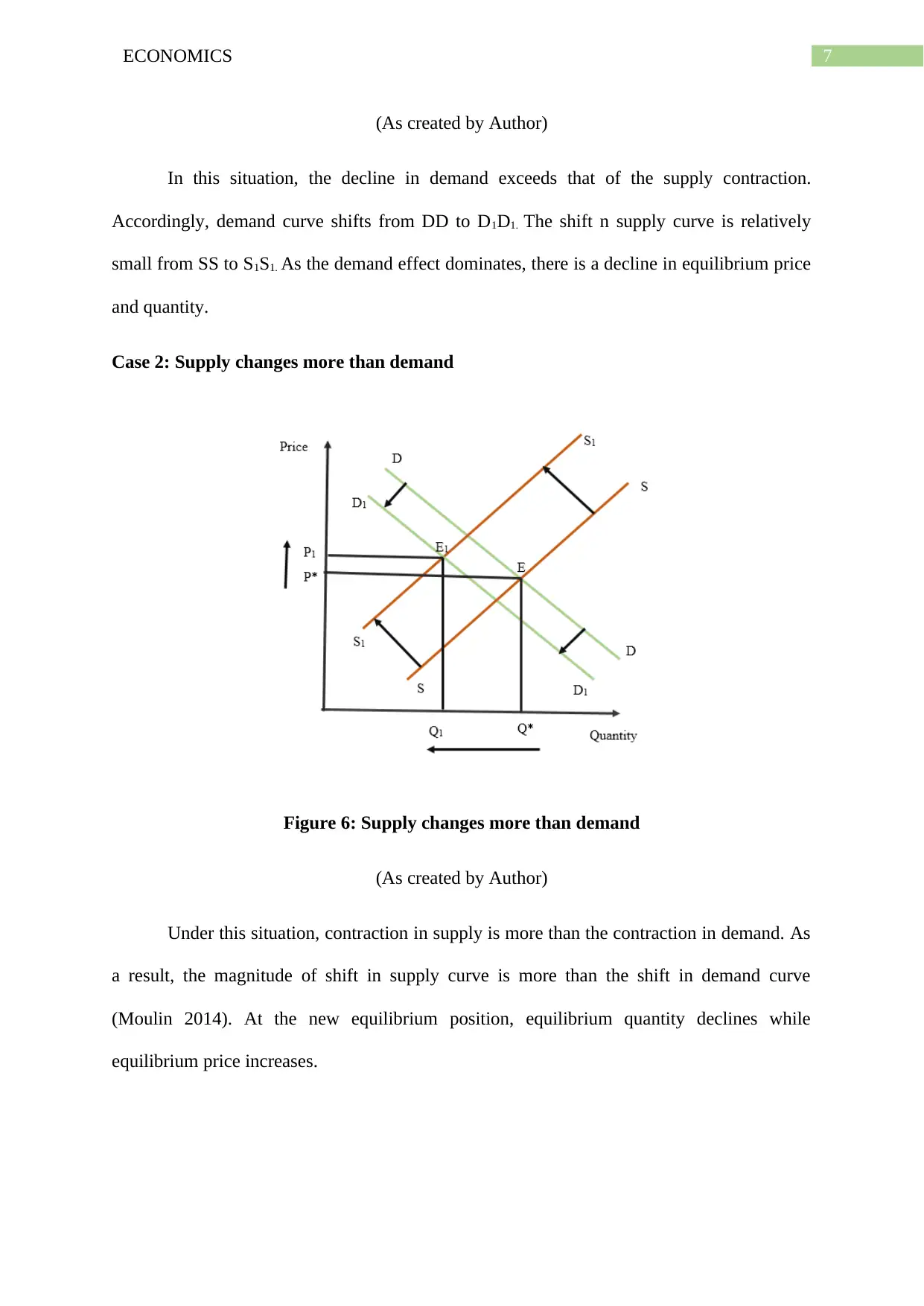

Case 2: Supply changes more than demand

Figure 6: Supply changes more than demand

(As created by Author)

Under this situation, contraction in supply is more than the contraction in demand. As

a result, the magnitude of shift in supply curve is more than the shift in demand curve

(Moulin 2014). At the new equilibrium position, equilibrium quantity declines while

equilibrium price increases.

(As created by Author)

In this situation, the decline in demand exceeds that of the supply contraction.

Accordingly, demand curve shifts from DD to D1D1. The shift n supply curve is relatively

small from SS to S1S1. As the demand effect dominates, there is a decline in equilibrium price

and quantity.

Case 2: Supply changes more than demand

Figure 6: Supply changes more than demand

(As created by Author)

Under this situation, contraction in supply is more than the contraction in demand. As

a result, the magnitude of shift in supply curve is more than the shift in demand curve

(Moulin 2014). At the new equilibrium position, equilibrium quantity declines while

equilibrium price increases.

8ECONOMICS

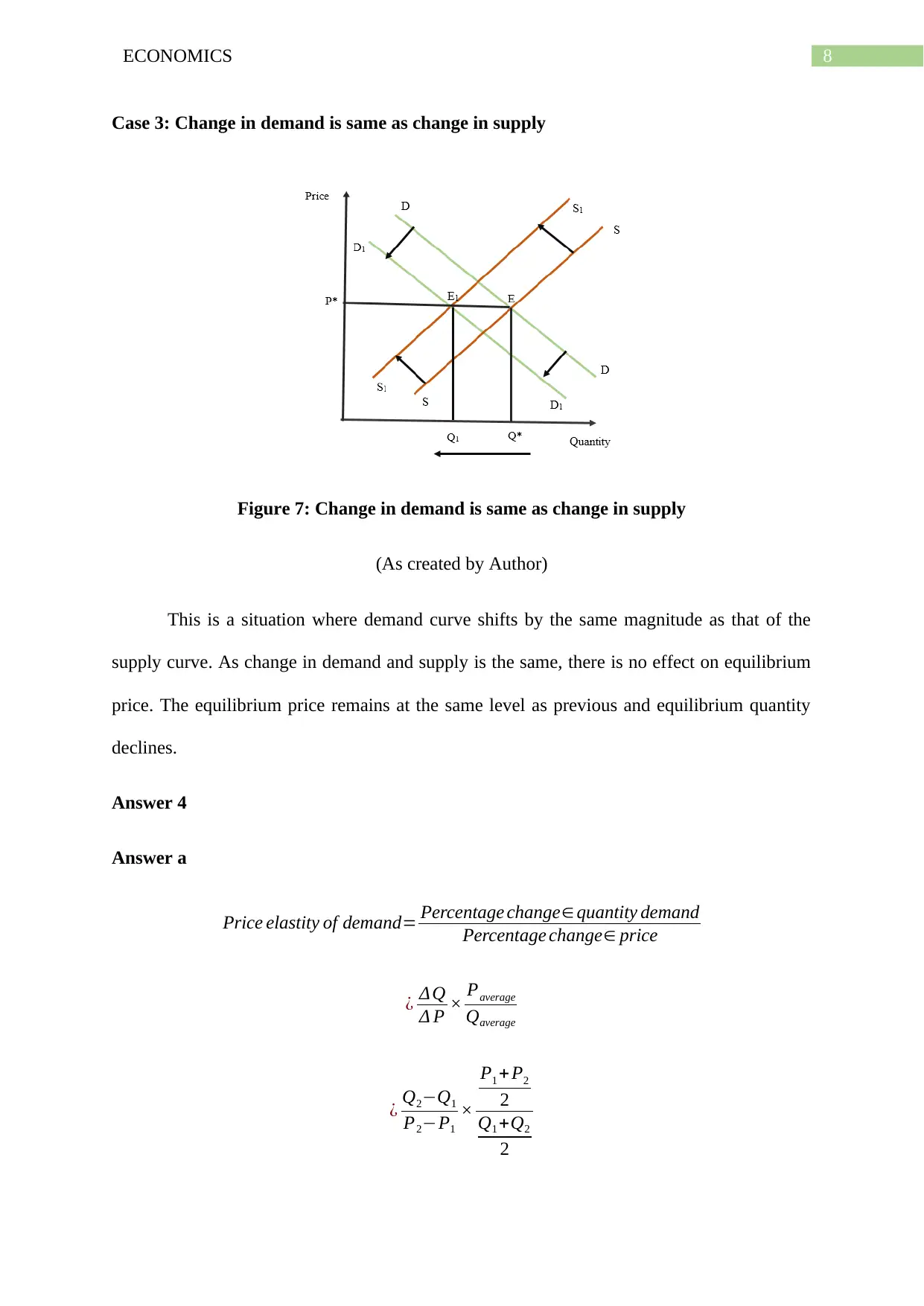

Case 3: Change in demand is same as change in supply

Figure 7: Change in demand is same as change in supply

(As created by Author)

This is a situation where demand curve shifts by the same magnitude as that of the

supply curve. As change in demand and supply is the same, there is no effect on equilibrium

price. The equilibrium price remains at the same level as previous and equilibrium quantity

declines.

Answer 4

Answer a

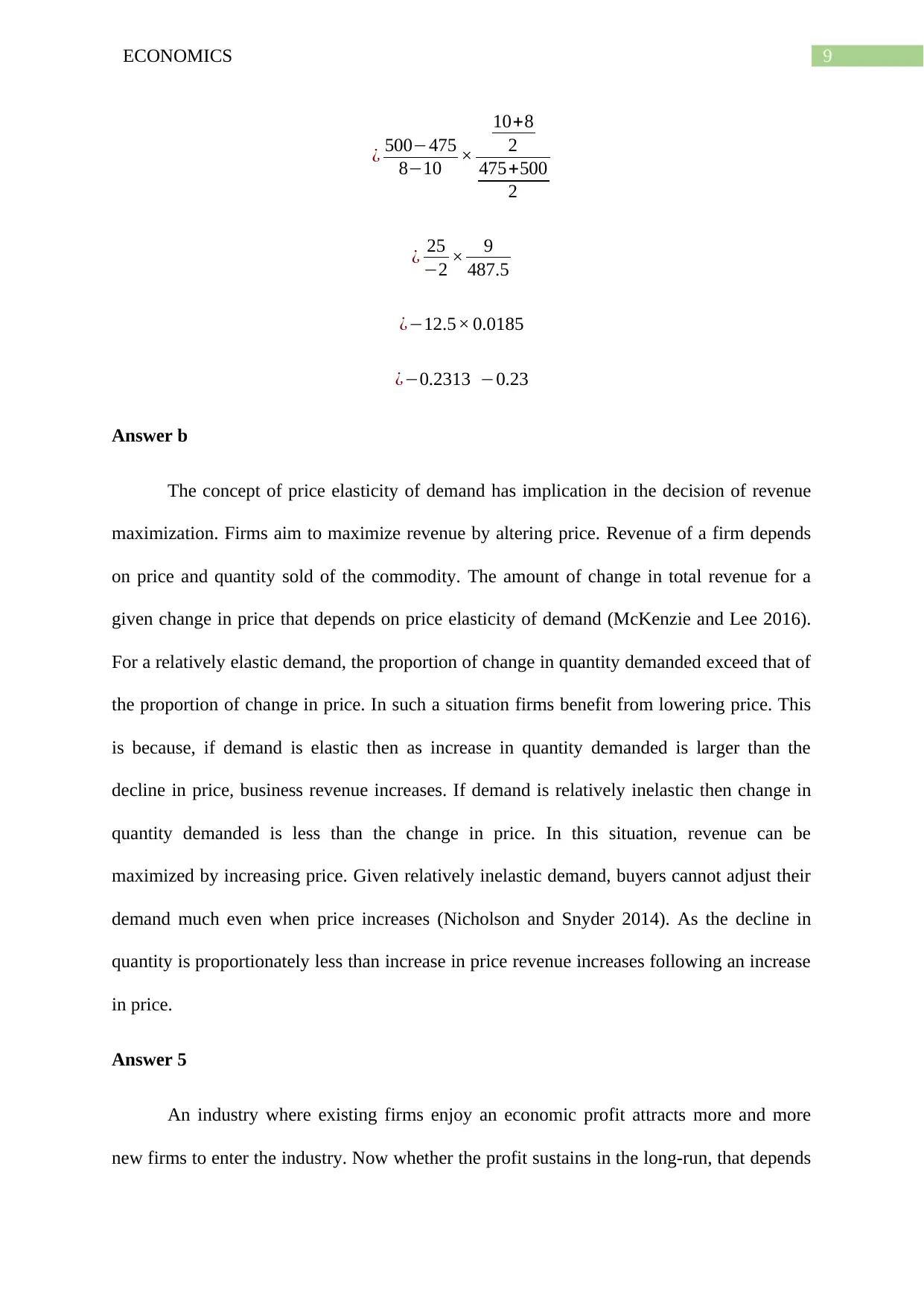

Price elastity of demand= Percentage change∈ quantity demand

Percentage change∈ price

¿ Δ Q

Δ P × Paverage

Qaverage

¿ Q2−Q1

P2−P1

×

P1 + P2

2

Q1 +Q2

2

Case 3: Change in demand is same as change in supply

Figure 7: Change in demand is same as change in supply

(As created by Author)

This is a situation where demand curve shifts by the same magnitude as that of the

supply curve. As change in demand and supply is the same, there is no effect on equilibrium

price. The equilibrium price remains at the same level as previous and equilibrium quantity

declines.

Answer 4

Answer a

Price elastity of demand= Percentage change∈ quantity demand

Percentage change∈ price

¿ Δ Q

Δ P × Paverage

Qaverage

¿ Q2−Q1

P2−P1

×

P1 + P2

2

Q1 +Q2

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ECONOMICS

¿ 500−475

8−10 ×

10+8

2

475+500

2

¿ 25

−2 × 9

487.5

¿−12.5× 0.0185

¿−0.2313 −0.23

Answer b

The concept of price elasticity of demand has implication in the decision of revenue

maximization. Firms aim to maximize revenue by altering price. Revenue of a firm depends

on price and quantity sold of the commodity. The amount of change in total revenue for a

given change in price that depends on price elasticity of demand (McKenzie and Lee 2016).

For a relatively elastic demand, the proportion of change in quantity demanded exceed that of

the proportion of change in price. In such a situation firms benefit from lowering price. This

is because, if demand is elastic then as increase in quantity demanded is larger than the

decline in price, business revenue increases. If demand is relatively inelastic then change in

quantity demanded is less than the change in price. In this situation, revenue can be

maximized by increasing price. Given relatively inelastic demand, buyers cannot adjust their

demand much even when price increases (Nicholson and Snyder 2014). As the decline in

quantity is proportionately less than increase in price revenue increases following an increase

in price.

Answer 5

An industry where existing firms enjoy an economic profit attracts more and more

new firms to enter the industry. Now whether the profit sustains in the long-run, that depends

¿ 500−475

8−10 ×

10+8

2

475+500

2

¿ 25

−2 × 9

487.5

¿−12.5× 0.0185

¿−0.2313 −0.23

Answer b

The concept of price elasticity of demand has implication in the decision of revenue

maximization. Firms aim to maximize revenue by altering price. Revenue of a firm depends

on price and quantity sold of the commodity. The amount of change in total revenue for a

given change in price that depends on price elasticity of demand (McKenzie and Lee 2016).

For a relatively elastic demand, the proportion of change in quantity demanded exceed that of

the proportion of change in price. In such a situation firms benefit from lowering price. This

is because, if demand is elastic then as increase in quantity demanded is larger than the

decline in price, business revenue increases. If demand is relatively inelastic then change in

quantity demanded is less than the change in price. In this situation, revenue can be

maximized by increasing price. Given relatively inelastic demand, buyers cannot adjust their

demand much even when price increases (Nicholson and Snyder 2014). As the decline in

quantity is proportionately less than increase in price revenue increases following an increase

in price.

Answer 5

An industry where existing firms enjoy an economic profit attracts more and more

new firms to enter the industry. Now whether the profit sustains in the long-run, that depends

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ECONOMICS

on entry barriers in the industry. If new firms are free to enter the industry then new firms

continue to enter. As more firms supply the industry, there is an increase in market supply.

Excess supply in the market then creates a downward pressure on price (Mahanty 2014).

With decline in price, profit gradually reduces. Entry stops when profit goes down to normal

profit. In contrast, if there are strict barriers to entry in the industry then firms can sustain the

economic profit even in the long run.

Firms in the given industry are enjoying an economic profit. Creation of internet

platform has broken down all the entry barriers allowing large number of firms to enter the

industry. The entry of large number of firms reduces industry supply largely. The resulted

increase in market supply shifts the supply curve to the right. This leads to a decline in

market price that firm face. With a lower price, profit of the existing firms reduce. Entry in

the market continues to occur until profit declines to normal profit or zero economic profit

(Jain and Ohri 2015). The market adjustment process in shown in the following figure.

Figure 8: Impact of entry of new firms

(As created by Author)

on entry barriers in the industry. If new firms are free to enter the industry then new firms

continue to enter. As more firms supply the industry, there is an increase in market supply.

Excess supply in the market then creates a downward pressure on price (Mahanty 2014).

With decline in price, profit gradually reduces. Entry stops when profit goes down to normal

profit. In contrast, if there are strict barriers to entry in the industry then firms can sustain the

economic profit even in the long run.

Firms in the given industry are enjoying an economic profit. Creation of internet

platform has broken down all the entry barriers allowing large number of firms to enter the

industry. The entry of large number of firms reduces industry supply largely. The resulted

increase in market supply shifts the supply curve to the right. This leads to a decline in

market price that firm face. With a lower price, profit of the existing firms reduce. Entry in

the market continues to occur until profit declines to normal profit or zero economic profit

(Jain and Ohri 2015). The market adjustment process in shown in the following figure.

Figure 8: Impact of entry of new firms

(As created by Author)

11ECONOMICS

The market demand and market supply in the industry are shown by the respective

curve of DD and SS. Current equilibrium is at E. The industry operates with an equilibrium

price of P* along with an equilibrium quantity of Q*. Now suppose, the market price is above

the average cost of the operating firms resulting in an economic profit for the firms. The

resulting economic profit attracts new firm. Given no entry barriers (as internet has broken

down all the entry barriers), new firms enter the industry. As industry supply increases, the

supply curve shift to the right (Sloman and Jones 2017). The new market supply curve in the

industry S1S1. The equilibrium price declines to P1 and equilibrium quantity in the industry

increases to Q1. The lower price reduces profit of the existing firms. New firms will stop

entering the industry as the profit falls to zero.

The market demand and market supply in the industry are shown by the respective

curve of DD and SS. Current equilibrium is at E. The industry operates with an equilibrium

price of P* along with an equilibrium quantity of Q*. Now suppose, the market price is above

the average cost of the operating firms resulting in an economic profit for the firms. The

resulting economic profit attracts new firm. Given no entry barriers (as internet has broken

down all the entry barriers), new firms enter the industry. As industry supply increases, the

supply curve shift to the right (Sloman and Jones 2017). The new market supply curve in the

industry S1S1. The equilibrium price declines to P1 and equilibrium quantity in the industry

increases to Q1. The lower price reduces profit of the existing firms. New firms will stop

entering the industry as the profit falls to zero.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.