Economics For Business And Management

VerifiedAdded on 2022/09/14

|12

|2690

|13

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: ECONOMICS FOR BUSINESS AND MANAGEMENT

Economics for Business and Management

Name of the Student

Name of the University

Author Note

Economics for Business and Management

Name of the Student

Name of the University

Author Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1ECONOMICS FOR BUSINESS AND MANAGEMENT

Table of Contents

Introduction......................................................................................................................................2

Structure of Australian Banking System.........................................................................................2

Consequence of having a Cosy Banking Oligopoly........................................................................5

Government Regulations and Policies undertaken to overcome the problems created by the

situation............................................................................................................................................6

Conclusion.......................................................................................................................................8

References......................................................................................................................................10

Table of Contents

Introduction......................................................................................................................................2

Structure of Australian Banking System.........................................................................................2

Consequence of having a Cosy Banking Oligopoly........................................................................5

Government Regulations and Policies undertaken to overcome the problems created by the

situation............................................................................................................................................6

Conclusion.......................................................................................................................................8

References......................................................................................................................................10

2ECONOMICS FOR BUSINESS AND MANAGEMENT

Introduction

Banking sector is one of the most important sectors of any economy, which plays a

crucial role in dealing with the financial system of the country. Banks are regarded as the

“lifeblood” of any nation that deal with savings, deposits, borrowing and lending activities of the

economy (Lau et al., 2013). A country’s growth, development and performance in the world

market is completely dependent on the efficiency of its banking and financial system. Australian

banking system too plays a vital role in boosting up its economy. It helps in facilitating the fund

flowing in the Australian economy and assuring that the financial resources are efficiently

allocated, thus encouraging the growth and development of the Australian economy (Salim,

Arjomandi & Seufert, 2016). Besides performing the traditional bank activities, the Australian

banks are also involved in activities like business banking, insurance management, financial

market dealing, foreign exchange purchasing and selling, stockbroking and others. They acts as

custodians as wells as distributors of the liquid capital of the nation, which in turn facilitates the

industrial and commercial activities leading towards economic prosperity and well-being of

Australia. In the last few decades the Australian banking and financial institution has undergone

a remarkable change (Joshi et al., 2013).

Structure of Australian Banking System

The banking system of Australia is mainly dominated by four important banks – Westpac

Banking Corporation, National Australia Bank, Australia and New Zealand (ANZ) Banking

Group and Common Wealth Bank of Australia. These four leading banks enjoying the “Four

Pillar Policy” (a policy of Australian Government in order to maintain the four banks’ separation

by prohibiting any merger between the banks) together account about 85% of total banking

system of Australia (Moradi-Motlagh & Babacan, 2015). In addition to these four largest banks

Introduction

Banking sector is one of the most important sectors of any economy, which plays a

crucial role in dealing with the financial system of the country. Banks are regarded as the

“lifeblood” of any nation that deal with savings, deposits, borrowing and lending activities of the

economy (Lau et al., 2013). A country’s growth, development and performance in the world

market is completely dependent on the efficiency of its banking and financial system. Australian

banking system too plays a vital role in boosting up its economy. It helps in facilitating the fund

flowing in the Australian economy and assuring that the financial resources are efficiently

allocated, thus encouraging the growth and development of the Australian economy (Salim,

Arjomandi & Seufert, 2016). Besides performing the traditional bank activities, the Australian

banks are also involved in activities like business banking, insurance management, financial

market dealing, foreign exchange purchasing and selling, stockbroking and others. They acts as

custodians as wells as distributors of the liquid capital of the nation, which in turn facilitates the

industrial and commercial activities leading towards economic prosperity and well-being of

Australia. In the last few decades the Australian banking and financial institution has undergone

a remarkable change (Joshi et al., 2013).

Structure of Australian Banking System

The banking system of Australia is mainly dominated by four important banks – Westpac

Banking Corporation, National Australia Bank, Australia and New Zealand (ANZ) Banking

Group and Common Wealth Bank of Australia. These four leading banks enjoying the “Four

Pillar Policy” (a policy of Australian Government in order to maintain the four banks’ separation

by prohibiting any merger between the banks) together account about 85% of total banking

system of Australia (Moradi-Motlagh & Babacan, 2015). In addition to these four largest banks

3ECONOMICS FOR BUSINESS AND MANAGEMENT

of the country, there exist a number of small banks which have nation-wide prevalence and

several financial institutions like mutual banks, credit unions and building societies, providing

limited banking-type facilities, known as Authorized Deposit-taking Institutions (ADIs).

Recently, fifty-three (53) banks are operating in the country, among them fourteen (14) banks are

predominantly owned by the country. The Reserve Bank of Australia (RBA) is the central bank,

which provides services to the Australian Government along with various official institutions and

central banks.

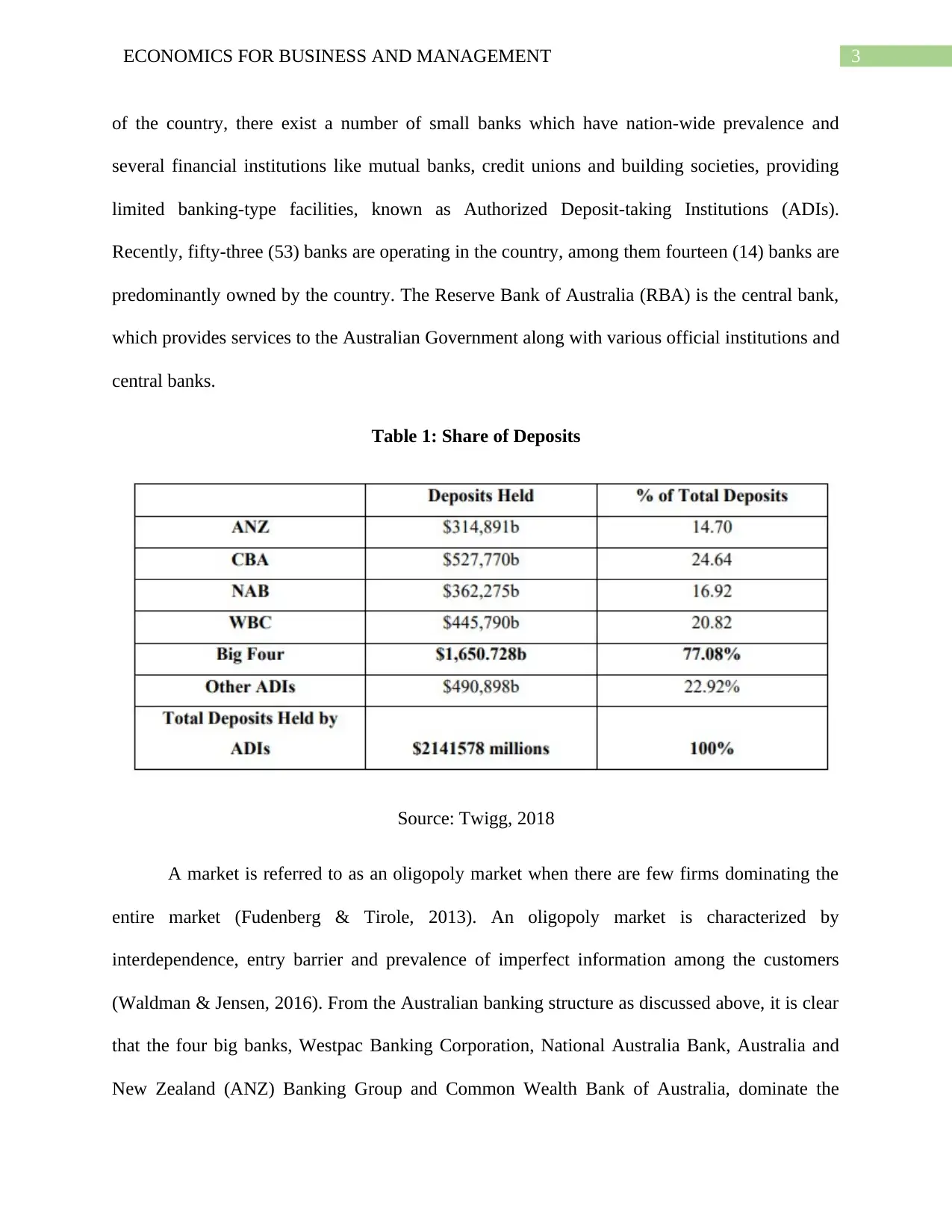

Table 1: Share of Deposits

Source: Twigg, 2018

A market is referred to as an oligopoly market when there are few firms dominating the

entire market (Fudenberg & Tirole, 2013). An oligopoly market is characterized by

interdependence, entry barrier and prevalence of imperfect information among the customers

(Waldman & Jensen, 2016). From the Australian banking structure as discussed above, it is clear

that the four big banks, Westpac Banking Corporation, National Australia Bank, Australia and

New Zealand (ANZ) Banking Group and Common Wealth Bank of Australia, dominate the

of the country, there exist a number of small banks which have nation-wide prevalence and

several financial institutions like mutual banks, credit unions and building societies, providing

limited banking-type facilities, known as Authorized Deposit-taking Institutions (ADIs).

Recently, fifty-three (53) banks are operating in the country, among them fourteen (14) banks are

predominantly owned by the country. The Reserve Bank of Australia (RBA) is the central bank,

which provides services to the Australian Government along with various official institutions and

central banks.

Table 1: Share of Deposits

Source: Twigg, 2018

A market is referred to as an oligopoly market when there are few firms dominating the

entire market (Fudenberg & Tirole, 2013). An oligopoly market is characterized by

interdependence, entry barrier and prevalence of imperfect information among the customers

(Waldman & Jensen, 2016). From the Australian banking structure as discussed above, it is clear

that the four big banks, Westpac Banking Corporation, National Australia Bank, Australia and

New Zealand (ANZ) Banking Group and Common Wealth Bank of Australia, dominate the

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4ECONOMICS FOR BUSINESS AND MANAGEMENT

entire banking industry. Hence, the banking sector acts as collusive oligopoly where the four

leading firms collude and perform together to increase their returns and divide the earned profit

among themselves. They make some agreements that helps them to restrict and regulate the

competition, therefore acting as an entry barrier for other institutions. In oligopolistic market,

either homogenous goods or differentiated products are sold and these four institutions are

selling homogenous products in the banking market. They create entry barrier, as heavy

investment is required, and the most striking feature that isolates them and make them quite

different from others is their inter-dependency. They are incapable of taking decision of their

own in isolation from other three without considering the action of their rival firms. The strong

collusive pricing policy of these dominant four banks make them an efficient player in the

oligopolistic banking sector of Australia (Dong et al., 2019). They possess dominating and

superior position in Australian banking institution and have tough entry barrier because they are

strong banks with economies of scales, assisting them to operate at low costs.

The chairperson of Australian Competition and Consumer Commission (ACCC), Rod

Sims, stated that Australian finance sector is ‘a cosy banking oligopoly”. The main reason behind

this statement is the domination and the powerful position the four major banks hold in the

Australian bank market. The four massive banks of Australia that follows oligopolistic approach,

are continuously trying to maximize their profit, thereby intensifying the level of competition in

the banking sector. They hold a control to over 75% of the national banking market and have

covered beyond Australian $4.7 trillion banking sector (Twigg, 2018).

entire banking industry. Hence, the banking sector acts as collusive oligopoly where the four

leading firms collude and perform together to increase their returns and divide the earned profit

among themselves. They make some agreements that helps them to restrict and regulate the

competition, therefore acting as an entry barrier for other institutions. In oligopolistic market,

either homogenous goods or differentiated products are sold and these four institutions are

selling homogenous products in the banking market. They create entry barrier, as heavy

investment is required, and the most striking feature that isolates them and make them quite

different from others is their inter-dependency. They are incapable of taking decision of their

own in isolation from other three without considering the action of their rival firms. The strong

collusive pricing policy of these dominant four banks make them an efficient player in the

oligopolistic banking sector of Australia (Dong et al., 2019). They possess dominating and

superior position in Australian banking institution and have tough entry barrier because they are

strong banks with economies of scales, assisting them to operate at low costs.

The chairperson of Australian Competition and Consumer Commission (ACCC), Rod

Sims, stated that Australian finance sector is ‘a cosy banking oligopoly”. The main reason behind

this statement is the domination and the powerful position the four major banks hold in the

Australian bank market. The four massive banks of Australia that follows oligopolistic approach,

are continuously trying to maximize their profit, thereby intensifying the level of competition in

the banking sector. They hold a control to over 75% of the national banking market and have

covered beyond Australian $4.7 trillion banking sector (Twigg, 2018).

5ECONOMICS FOR BUSINESS AND MANAGEMENT

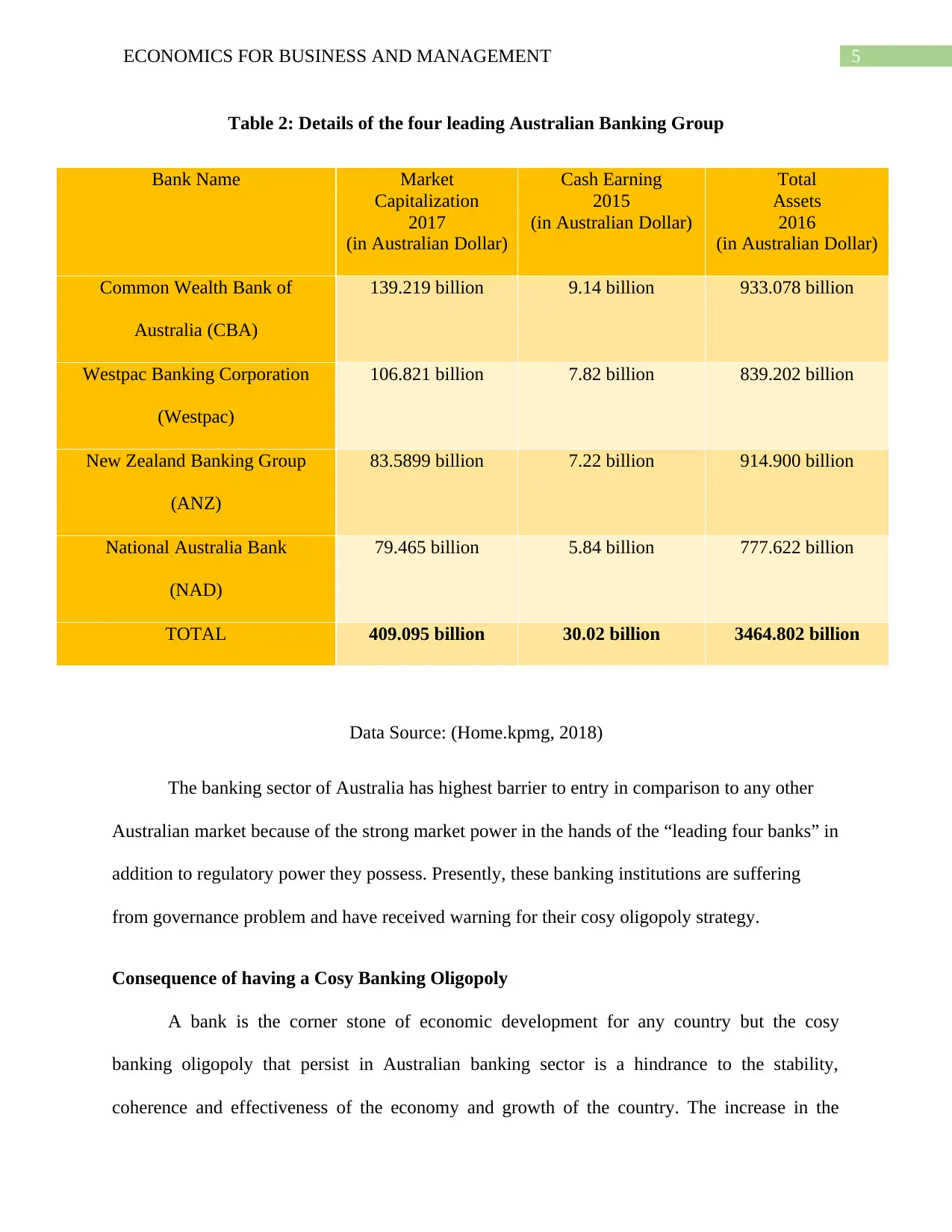

Table 2: Details of the four leading Australian Banking Group

Bank Name Market

Capitalization

2017

(in Australian Dollar)

Cash Earning

2015

(in Australian Dollar)

Total

Assets

2016

(in Australian Dollar)

Common Wealth Bank of

Australia (CBA)

139.219 billion 9.14 billion 933.078 billion

Westpac Banking Corporation

(Westpac)

106.821 billion 7.82 billion 839.202 billion

New Zealand Banking Group

(ANZ)

83.5899 billion 7.22 billion 914.900 billion

National Australia Bank

(NAD)

79.465 billion 5.84 billion 777.622 billion

TOTAL 409.095 billion 30.02 billion 3464.802 billion

Data Source: (Home.kpmg, 2018)

The banking sector of Australia has highest barrier to entry in comparison to any other

Australian market because of the strong market power in the hands of the “leading four banks” in

addition to regulatory power they possess. Presently, these banking institutions are suffering

from governance problem and have received warning for their cosy oligopoly strategy.

Consequence of having a Cosy Banking Oligopoly

A bank is the corner stone of economic development for any country but the cosy

banking oligopoly that persist in Australian banking sector is a hindrance to the stability,

coherence and effectiveness of the economy and growth of the country. The increase in the

Table 2: Details of the four leading Australian Banking Group

Bank Name Market

Capitalization

2017

(in Australian Dollar)

Cash Earning

2015

(in Australian Dollar)

Total

Assets

2016

(in Australian Dollar)

Common Wealth Bank of

Australia (CBA)

139.219 billion 9.14 billion 933.078 billion

Westpac Banking Corporation

(Westpac)

106.821 billion 7.82 billion 839.202 billion

New Zealand Banking Group

(ANZ)

83.5899 billion 7.22 billion 914.900 billion

National Australia Bank

(NAD)

79.465 billion 5.84 billion 777.622 billion

TOTAL 409.095 billion 30.02 billion 3464.802 billion

Data Source: (Home.kpmg, 2018)

The banking sector of Australia has highest barrier to entry in comparison to any other

Australian market because of the strong market power in the hands of the “leading four banks” in

addition to regulatory power they possess. Presently, these banking institutions are suffering

from governance problem and have received warning for their cosy oligopoly strategy.

Consequence of having a Cosy Banking Oligopoly

A bank is the corner stone of economic development for any country but the cosy

banking oligopoly that persist in Australian banking sector is a hindrance to the stability,

coherence and effectiveness of the economy and growth of the country. The increase in the

6ECONOMICS FOR BUSINESS AND MANAGEMENT

concentration, might lead to a plethora of incompetence in the banking market due to the shifting

of the market away from the necessary competitive outcome. The inefficient economic condition

prevails in the banking system of Australia due to the presence of lack of competition in the

system that is supposed to exist. Absence of proper competition in the banking areas of Australia

creates an unfavorable consequence for the country’s frugality and people. This gives rise to

moral hazards and lowers the interest of the banks to chalk out innovative plans and invest for

building up new infrastructure. The insufficiency of adequate competition creates dead weight

loss to the bank market since the banking structure is not at all Pareteo Efficient (Iancu &

Trichakis, 2013). As the four large banks (Westpac Banking Corporation, National Australia

Bank, Australia and New Zealand (ANZ) Banking Group and Common Wealth Bank of

Australia) together behave in a monopolistic way and creates a high barrier to entry so, there can

an issue regarding social welfare. The Consumer Surplus (CS) will get replaced by Producer

Surplus (PS), thus affecting the customers’ interest. The banks are using their power of pricing

for extracting excessive extra profit which has a detrimental effect on the common people

(Zhang et al., 2016). The combined effect of the four prime banks’ co-ownership, the “four pillar

policy” protection of the Australian government and high market entry barrier has made the

banking system less competitive, is creating a substantial dead weight loss to the society. This

will in turn act as a fuel for increasing and intensifying the profit of the banks, generating a

hazardous effect on the Australian economy and society.

Government Regulations and Policies undertaken to overcome the problems created by the

situation

To handle and overcome the negative effects of the cosy banking oligopoly, the

Australian government has adopted several policies and regulations. A number of regulations

concentration, might lead to a plethora of incompetence in the banking market due to the shifting

of the market away from the necessary competitive outcome. The inefficient economic condition

prevails in the banking system of Australia due to the presence of lack of competition in the

system that is supposed to exist. Absence of proper competition in the banking areas of Australia

creates an unfavorable consequence for the country’s frugality and people. This gives rise to

moral hazards and lowers the interest of the banks to chalk out innovative plans and invest for

building up new infrastructure. The insufficiency of adequate competition creates dead weight

loss to the bank market since the banking structure is not at all Pareteo Efficient (Iancu &

Trichakis, 2013). As the four large banks (Westpac Banking Corporation, National Australia

Bank, Australia and New Zealand (ANZ) Banking Group and Common Wealth Bank of

Australia) together behave in a monopolistic way and creates a high barrier to entry so, there can

an issue regarding social welfare. The Consumer Surplus (CS) will get replaced by Producer

Surplus (PS), thus affecting the customers’ interest. The banks are using their power of pricing

for extracting excessive extra profit which has a detrimental effect on the common people

(Zhang et al., 2016). The combined effect of the four prime banks’ co-ownership, the “four pillar

policy” protection of the Australian government and high market entry barrier has made the

banking system less competitive, is creating a substantial dead weight loss to the society. This

will in turn act as a fuel for increasing and intensifying the profit of the banks, generating a

hazardous effect on the Australian economy and society.

Government Regulations and Policies undertaken to overcome the problems created by the

situation

To handle and overcome the negative effects of the cosy banking oligopoly, the

Australian government has adopted several policies and regulations. A number of regulations

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ECONOMICS FOR BUSINESS AND MANAGEMENT

and policies are undertaken for better governance and monitoring of the Australian banks in

relation to licensing, international standards, protecting the interest of the customers, foreign

investment, rules on liquidity, liquidity regimes, and so on. Different authorities, committees and

commissions of the nation like Australian Securities and Investment Commission (ASIC),

Australian Prudential Regulation Authority (APRA), Australian Competition and Consumer

Commission (ACCC) are entitled to look after and supervise the various areas that affects a

banks’ activity along with the Reserve Bank of Australia (RBA) (Middleton, 2015). The RBA

takes care of the financial stability of the organization by setting Monetary Policies (MP) and

regulating the system of payment, while ASIC ensures consumers’ protection and market

integrity, APRA is primarily concerned with the prudential policies and ACCC enforces the

competition laws (Lim, Tsiaplias & Chua, 2013). APRA monitors ADIs (authorized deposit-

taking institutions), insurance (general insurance or life insurance) companies and

superannuation industries in addition to ascertaining that all the APRA supervised banking

institution are meeting their promises in terms of efficiency, stability and market competition

(Pearson, 2016). ASIC acts as a regular of financial services, corporate and markets by looking

after the market behavior and protection of the investors (Lui, 2016). The Australian committee

recommends that, to monitor and check the level of competition in the Australian banking

system, a team will be entitled for the job and the selection of the team members will be carried

out by ACCC. The team will have the power to suggest and recommend numerous policies for

raising and boosting up the competition in the banking market.

and policies are undertaken for better governance and monitoring of the Australian banks in

relation to licensing, international standards, protecting the interest of the customers, foreign

investment, rules on liquidity, liquidity regimes, and so on. Different authorities, committees and

commissions of the nation like Australian Securities and Investment Commission (ASIC),

Australian Prudential Regulation Authority (APRA), Australian Competition and Consumer

Commission (ACCC) are entitled to look after and supervise the various areas that affects a

banks’ activity along with the Reserve Bank of Australia (RBA) (Middleton, 2015). The RBA

takes care of the financial stability of the organization by setting Monetary Policies (MP) and

regulating the system of payment, while ASIC ensures consumers’ protection and market

integrity, APRA is primarily concerned with the prudential policies and ACCC enforces the

competition laws (Lim, Tsiaplias & Chua, 2013). APRA monitors ADIs (authorized deposit-

taking institutions), insurance (general insurance or life insurance) companies and

superannuation industries in addition to ascertaining that all the APRA supervised banking

institution are meeting their promises in terms of efficiency, stability and market competition

(Pearson, 2016). ASIC acts as a regular of financial services, corporate and markets by looking

after the market behavior and protection of the investors (Lui, 2016). The Australian committee

recommends that, to monitor and check the level of competition in the Australian banking

system, a team will be entitled for the job and the selection of the team members will be carried

out by ACCC. The team will have the power to suggest and recommend numerous policies for

raising and boosting up the competition in the banking market.

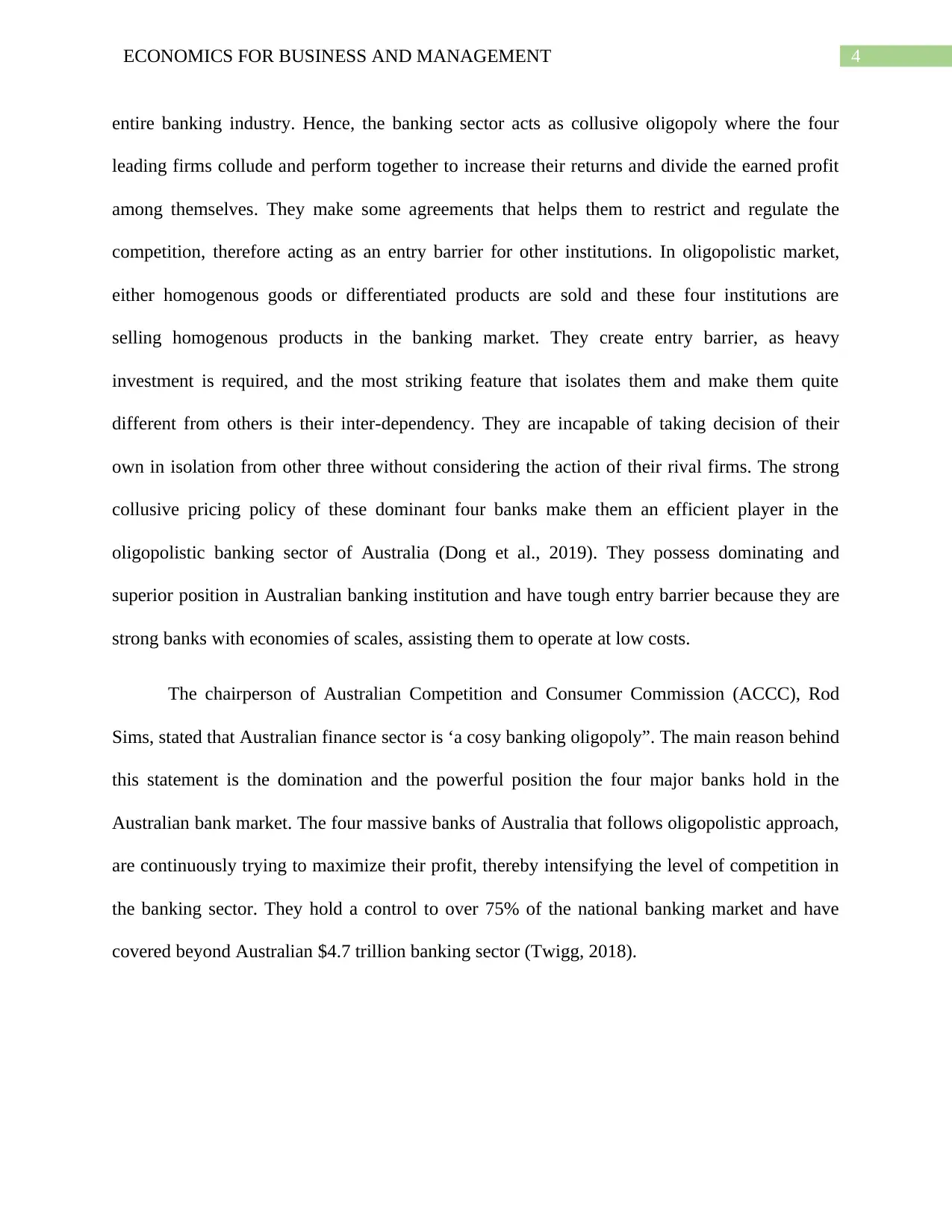

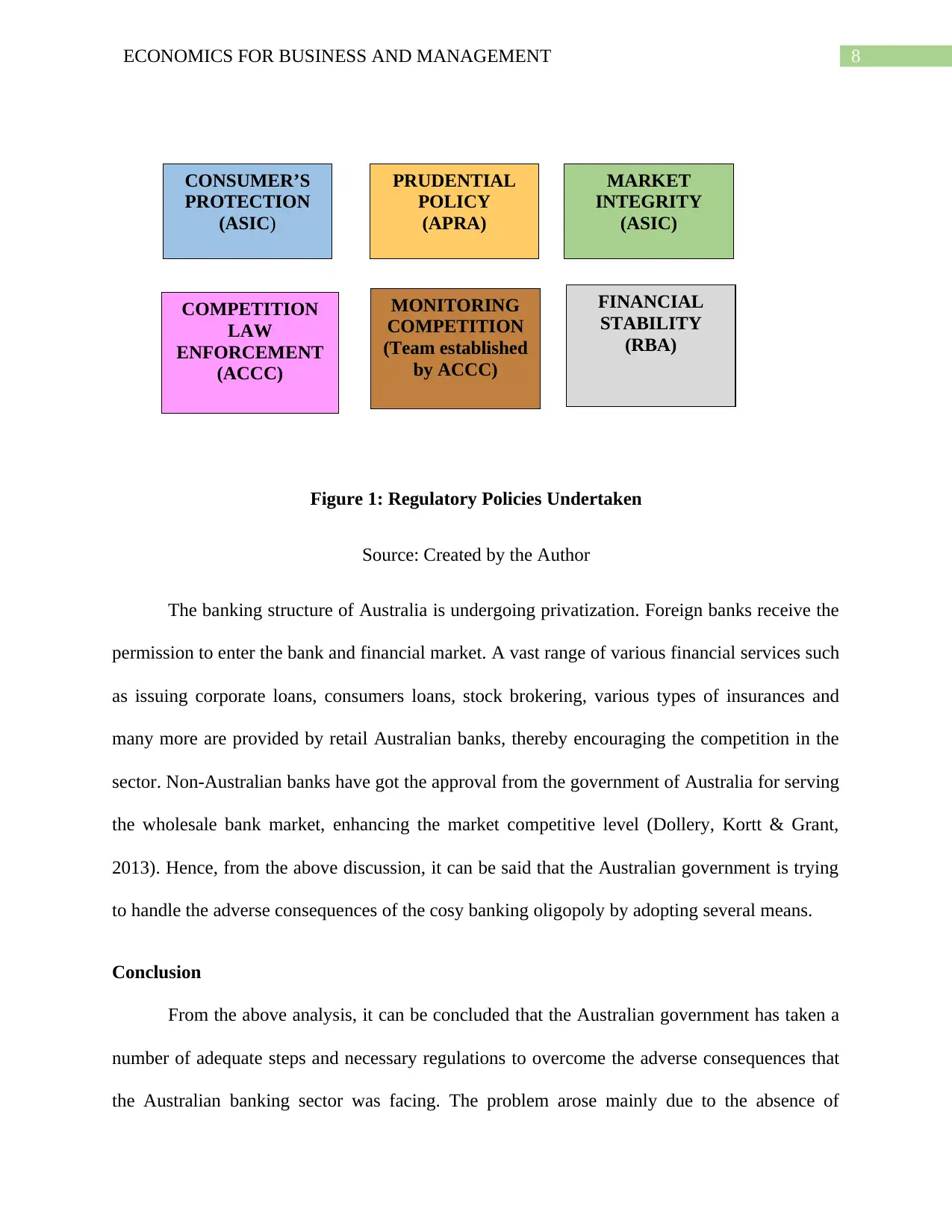

8ECONOMICS FOR BUSINESS AND MANAGEMENT

CONSUMER’S

PROTECTION

(ASIC)

PRUDENTIAL

POLICY

(APRA)

MARKET

INTEGRITY

(ASIC)

COMPETITION

LAW

ENFORCEMENT

(ACCC)

MONITORING

COMPETITION

(Team established

by ACCC)

FINANCIAL

STABILITY

(RBA)

Figure 1: Regulatory Policies Undertaken

Source: Created by the Author

The banking structure of Australia is undergoing privatization. Foreign banks receive the

permission to enter the bank and financial market. A vast range of various financial services such

as issuing corporate loans, consumers loans, stock brokering, various types of insurances and

many more are provided by retail Australian banks, thereby encouraging the competition in the

sector. Non-Australian banks have got the approval from the government of Australia for serving

the wholesale bank market, enhancing the market competitive level (Dollery, Kortt & Grant,

2013). Hence, from the above discussion, it can be said that the Australian government is trying

to handle the adverse consequences of the cosy banking oligopoly by adopting several means.

Conclusion

From the above analysis, it can be concluded that the Australian government has taken a

number of adequate steps and necessary regulations to overcome the adverse consequences that

the Australian banking sector was facing. The problem arose mainly due to the absence of

CONSUMER’S

PROTECTION

(ASIC)

PRUDENTIAL

POLICY

(APRA)

MARKET

INTEGRITY

(ASIC)

COMPETITION

LAW

ENFORCEMENT

(ACCC)

MONITORING

COMPETITION

(Team established

by ACCC)

FINANCIAL

STABILITY

(RBA)

Figure 1: Regulatory Policies Undertaken

Source: Created by the Author

The banking structure of Australia is undergoing privatization. Foreign banks receive the

permission to enter the bank and financial market. A vast range of various financial services such

as issuing corporate loans, consumers loans, stock brokering, various types of insurances and

many more are provided by retail Australian banks, thereby encouraging the competition in the

sector. Non-Australian banks have got the approval from the government of Australia for serving

the wholesale bank market, enhancing the market competitive level (Dollery, Kortt & Grant,

2013). Hence, from the above discussion, it can be said that the Australian government is trying

to handle the adverse consequences of the cosy banking oligopoly by adopting several means.

Conclusion

From the above analysis, it can be concluded that the Australian government has taken a

number of adequate steps and necessary regulations to overcome the adverse consequences that

the Australian banking sector was facing. The problem arose mainly due to the absence of

9ECONOMICS FOR BUSINESS AND MANAGEMENT

enough competition, high and strong barriers to entry to the market and tendency of the four big

banks to earn excess profit at the cost of decrementing the consumers. However, the measures

taken are quite good and note-worthy but more attention should be given in improving the sector

because this sector is the heart of any economy.

enough competition, high and strong barriers to entry to the market and tendency of the four big

banks to earn excess profit at the cost of decrementing the consumers. However, the measures

taken are quite good and note-worthy but more attention should be given in improving the sector

because this sector is the heart of any economy.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10ECONOMICS FOR BUSINESS AND MANAGEMENT

References

Dollery, B. E., Kortt, M. A., & Grant, B. J. (2013). Funding the future: Financial sustainability

and infrastructure finance in Australian local government.

Dong, M., Huangfu, S., Sun, H., & Zhou, C. (2019). A Macroeconomic Theory of Banking

Oligopoly [Ebook].

Fudenberg, D., & Tirole, J. (2013). Dynamic models of oligopoly. Routledge.

Home.kpmg. (2018). Major Australian Banks. Retrieved 28 August 2019, from

https://home.kpmg/content/dam/kpmg/au/pdf/2018/major-australian-banks-full-year-

2018-results-analysis.pdf

Iancu, D. A., & Trichakis, N. (2013). Pareto efficiency in robust optimization. Management

Science, 60(1), 130-147.

Joshi, M., Cahill, D., Sidhu, J., & Kansal, M. (2013). Intellectual capital and financial

performance: an evaluation of the Australian financial sector. Journal of intellectual

capital, 14(2), 264-285.

Lau, M. M., Cheung, R., Lam, A. Y., & Chu, Y. T. (2013). Measuring service quality in the

banking industry: a Hong Kong based study. Contemporary Management Research, 9(3).

Lim, G. C., Tsiaplias, S., & Chua, C. L. (2013). Bank and official interest rates: how do they

interact over time?. Economic Record, 89(285), 160-174.

Lui, A. (2016). Financial stability and prudential regulation: a comparative approach to the

UK, US, Canada, Australia and Germany. Routledge.

References

Dollery, B. E., Kortt, M. A., & Grant, B. J. (2013). Funding the future: Financial sustainability

and infrastructure finance in Australian local government.

Dong, M., Huangfu, S., Sun, H., & Zhou, C. (2019). A Macroeconomic Theory of Banking

Oligopoly [Ebook].

Fudenberg, D., & Tirole, J. (2013). Dynamic models of oligopoly. Routledge.

Home.kpmg. (2018). Major Australian Banks. Retrieved 28 August 2019, from

https://home.kpmg/content/dam/kpmg/au/pdf/2018/major-australian-banks-full-year-

2018-results-analysis.pdf

Iancu, D. A., & Trichakis, N. (2013). Pareto efficiency in robust optimization. Management

Science, 60(1), 130-147.

Joshi, M., Cahill, D., Sidhu, J., & Kansal, M. (2013). Intellectual capital and financial

performance: an evaluation of the Australian financial sector. Journal of intellectual

capital, 14(2), 264-285.

Lau, M. M., Cheung, R., Lam, A. Y., & Chu, Y. T. (2013). Measuring service quality in the

banking industry: a Hong Kong based study. Contemporary Management Research, 9(3).

Lim, G. C., Tsiaplias, S., & Chua, C. L. (2013). Bank and official interest rates: how do they

interact over time?. Economic Record, 89(285), 160-174.

Lui, A. (2016). Financial stability and prudential regulation: a comparative approach to the

UK, US, Canada, Australia and Germany. Routledge.

11ECONOMICS FOR BUSINESS AND MANAGEMENT

Middleton, T. (2015). Banning, disqualification and licensing powers: ACCC, APRA, ASIC and

the ATO–regulatory overlap, penalty privilege and law reform. Company and Securities

Law Journal, 33, 555-580.

Moradi-Motlagh, A., & Babacan, A. (2015). The impact of the global financial crisis on the

efficiency of Australian banks. Economic Modelling, 46, 397-406.

Pearson, G. (2016). Financial literacy and the creation of financial citizens. In The Future of

Consumer Credit Regulation (pp. 21-46). Routledge.

Salim, R., Arjomandi, A., & Seufert, J. H. (2016). Does corporate governance affect Australian

banks' performance?. Journal of International Financial Markets, Institutions and

Money, 43, 113-125.

Twigg, P. (2018). A Theory & Evidence Based Assessment of Competition in the Australian

Banking System [Ebook].

Waldman, D. E., & Jensen, E. J. (2016). Industrial organization: theory and practice. Routledge.

Zhang, Y., Zhao, Q., Zhang, Y., Friedman, D., Zhang, M., Liu, Y., & Ma, S. (2016, April).

Economic recommendation with surplus maximization. In Proceedings of the 25th

International Conference on World Wide Web (pp. 73-83). International World Wide

Web Conferences Steering Committee.

Middleton, T. (2015). Banning, disqualification and licensing powers: ACCC, APRA, ASIC and

the ATO–regulatory overlap, penalty privilege and law reform. Company and Securities

Law Journal, 33, 555-580.

Moradi-Motlagh, A., & Babacan, A. (2015). The impact of the global financial crisis on the

efficiency of Australian banks. Economic Modelling, 46, 397-406.

Pearson, G. (2016). Financial literacy and the creation of financial citizens. In The Future of

Consumer Credit Regulation (pp. 21-46). Routledge.

Salim, R., Arjomandi, A., & Seufert, J. H. (2016). Does corporate governance affect Australian

banks' performance?. Journal of International Financial Markets, Institutions and

Money, 43, 113-125.

Twigg, P. (2018). A Theory & Evidence Based Assessment of Competition in the Australian

Banking System [Ebook].

Waldman, D. E., & Jensen, E. J. (2016). Industrial organization: theory and practice. Routledge.

Zhang, Y., Zhao, Q., Zhang, Y., Friedman, D., Zhang, M., Liu, Y., & Ma, S. (2016, April).

Economic recommendation with surplus maximization. In Proceedings of the 25th

International Conference on World Wide Web (pp. 73-83). International World Wide

Web Conferences Steering Committee.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.