Australia's Economic Resilience

VerifiedAdded on 2020/05/04

|10

|2460

|92

AI Summary

This assignment examines Australia's economic performance following the Global Financial Crisis (GFC) of 2008-2009. It analyzes the strategies implemented by the Australian government to mitigate the crisis's impact, explores the role of the mining boom in driving economic growth, and investigates Australia's international trade relationships, particularly with China. The goal is to understand how Australia achieved sustained economic expansion despite the global downturn.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

ECONOMICS

Growth Trends in Australia

STUDENT ID:

[Pick the date]

Growth Trends in Australia

STUDENT ID:

[Pick the date]

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

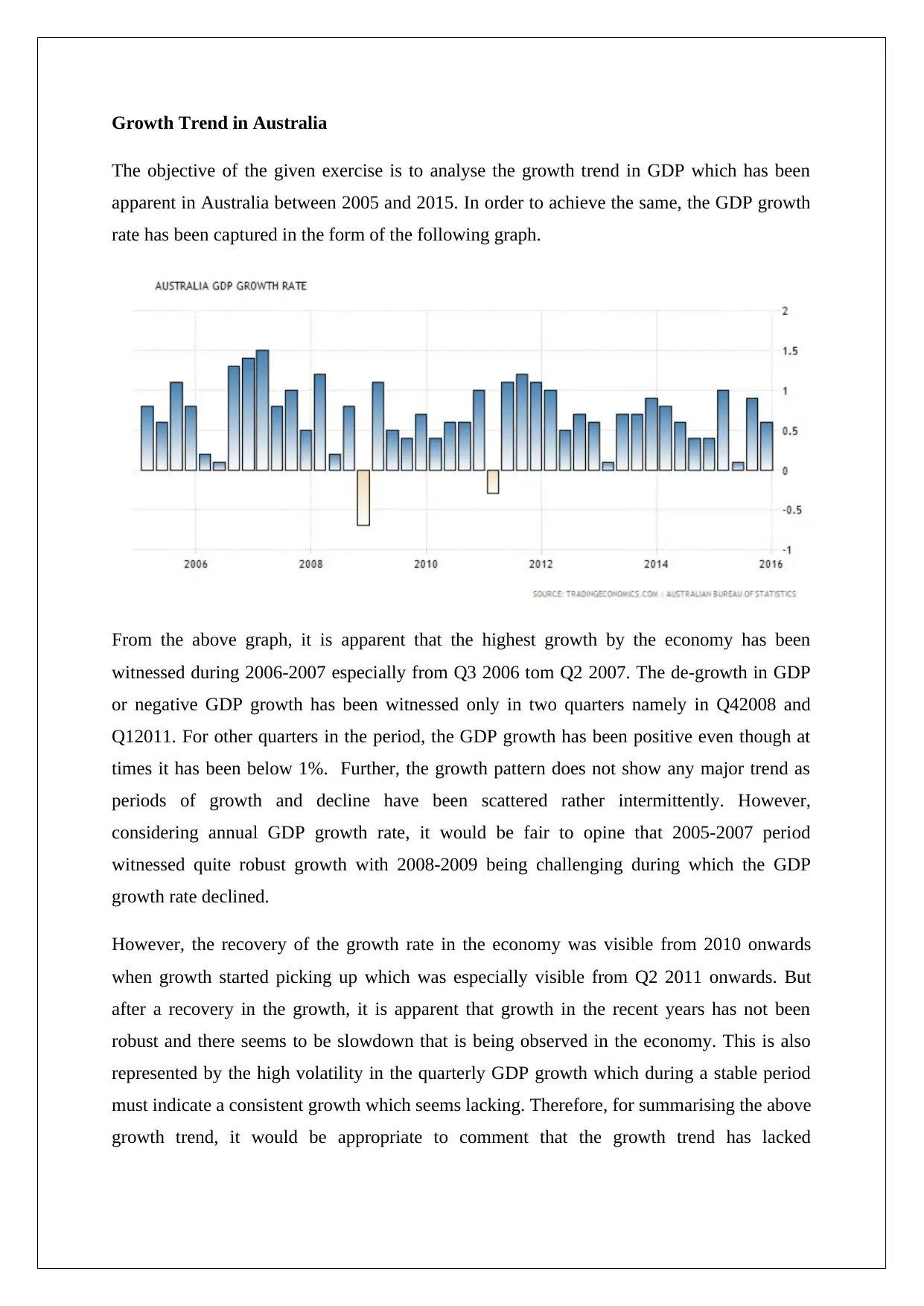

Growth Trend in Australia

The objective of the given exercise is to analyse the growth trend in GDP which has been

apparent in Australia between 2005 and 2015. In order to achieve the same, the GDP growth

rate has been captured in the form of the following graph.

From the above graph, it is apparent that the highest growth by the economy has been

witnessed during 2006-2007 especially from Q3 2006 tom Q2 2007. The de-growth in GDP

or negative GDP growth has been witnessed only in two quarters namely in Q42008 and

Q12011. For other quarters in the period, the GDP growth has been positive even though at

times it has been below 1%. Further, the growth pattern does not show any major trend as

periods of growth and decline have been scattered rather intermittently. However,

considering annual GDP growth rate, it would be fair to opine that 2005-2007 period

witnessed quite robust growth with 2008-2009 being challenging during which the GDP

growth rate declined.

However, the recovery of the growth rate in the economy was visible from 2010 onwards

when growth started picking up which was especially visible from Q2 2011 onwards. But

after a recovery in the growth, it is apparent that growth in the recent years has not been

robust and there seems to be slowdown that is being observed in the economy. This is also

represented by the high volatility in the quarterly GDP growth which during a stable period

must indicate a consistent growth which seems lacking. Therefore, for summarising the above

growth trend, it would be appropriate to comment that the growth trend has lacked

The objective of the given exercise is to analyse the growth trend in GDP which has been

apparent in Australia between 2005 and 2015. In order to achieve the same, the GDP growth

rate has been captured in the form of the following graph.

From the above graph, it is apparent that the highest growth by the economy has been

witnessed during 2006-2007 especially from Q3 2006 tom Q2 2007. The de-growth in GDP

or negative GDP growth has been witnessed only in two quarters namely in Q42008 and

Q12011. For other quarters in the period, the GDP growth has been positive even though at

times it has been below 1%. Further, the growth pattern does not show any major trend as

periods of growth and decline have been scattered rather intermittently. However,

considering annual GDP growth rate, it would be fair to opine that 2005-2007 period

witnessed quite robust growth with 2008-2009 being challenging during which the GDP

growth rate declined.

However, the recovery of the growth rate in the economy was visible from 2010 onwards

when growth started picking up which was especially visible from Q2 2011 onwards. But

after a recovery in the growth, it is apparent that growth in the recent years has not been

robust and there seems to be slowdown that is being observed in the economy. This is also

represented by the high volatility in the quarterly GDP growth which during a stable period

must indicate a consistent growth which seems lacking. Therefore, for summarising the above

growth trend, it would be appropriate to comment that the growth trend has lacked

consistency and has been quite choppy with a particular broad pattern being visible for only

couple of years. Also, high variation in the quarterly growth rates is visible.

Reasons for growth rate variation

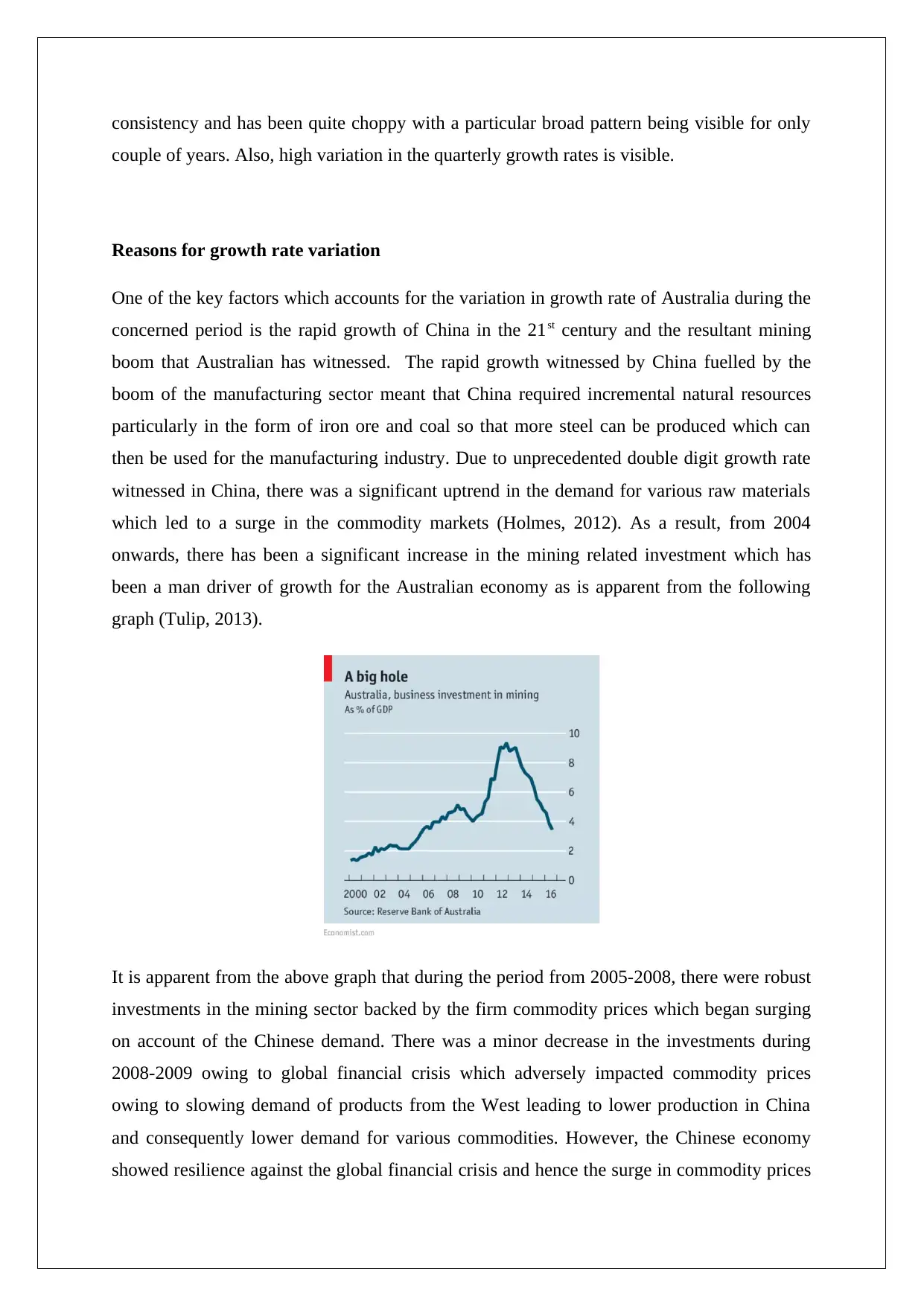

One of the key factors which accounts for the variation in growth rate of Australia during the

concerned period is the rapid growth of China in the 21st century and the resultant mining

boom that Australian has witnessed. The rapid growth witnessed by China fuelled by the

boom of the manufacturing sector meant that China required incremental natural resources

particularly in the form of iron ore and coal so that more steel can be produced which can

then be used for the manufacturing industry. Due to unprecedented double digit growth rate

witnessed in China, there was a significant uptrend in the demand for various raw materials

which led to a surge in the commodity markets (Holmes, 2012). As a result, from 2004

onwards, there has been a significant increase in the mining related investment which has

been a man driver of growth for the Australian economy as is apparent from the following

graph (Tulip, 2013).

It is apparent from the above graph that during the period from 2005-2008, there were robust

investments in the mining sector backed by the firm commodity prices which began surging

on account of the Chinese demand. There was a minor decrease in the investments during

2008-2009 owing to global financial crisis which adversely impacted commodity prices

owing to slowing demand of products from the West leading to lower production in China

and consequently lower demand for various commodities. However, the Chinese economy

showed resilience against the global financial crisis and hence the surge in commodity prices

couple of years. Also, high variation in the quarterly growth rates is visible.

Reasons for growth rate variation

One of the key factors which accounts for the variation in growth rate of Australia during the

concerned period is the rapid growth of China in the 21st century and the resultant mining

boom that Australian has witnessed. The rapid growth witnessed by China fuelled by the

boom of the manufacturing sector meant that China required incremental natural resources

particularly in the form of iron ore and coal so that more steel can be produced which can

then be used for the manufacturing industry. Due to unprecedented double digit growth rate

witnessed in China, there was a significant uptrend in the demand for various raw materials

which led to a surge in the commodity markets (Holmes, 2012). As a result, from 2004

onwards, there has been a significant increase in the mining related investment which has

been a man driver of growth for the Australian economy as is apparent from the following

graph (Tulip, 2013).

It is apparent from the above graph that during the period from 2005-2008, there were robust

investments in the mining sector backed by the firm commodity prices which began surging

on account of the Chinese demand. There was a minor decrease in the investments during

2008-2009 owing to global financial crisis which adversely impacted commodity prices

owing to slowing demand of products from the West leading to lower production in China

and consequently lower demand for various commodities. However, the Chinese economy

showed resilience against the global financial crisis and hence the surge in commodity prices

continues from 2010 onwards which led to increase in investments in mining. These

investments peaked in 2012-2013 post which there has been a decline as signs of slowdown

are visible in China owing to which the commodity demand is slowing and hence caused the

commodity prices to crash. This explains the lacklustre growth witnessed from mid-2013

onwards as the contribution of the mining industry to the GDP is quite substantial (Tulip,

2013).

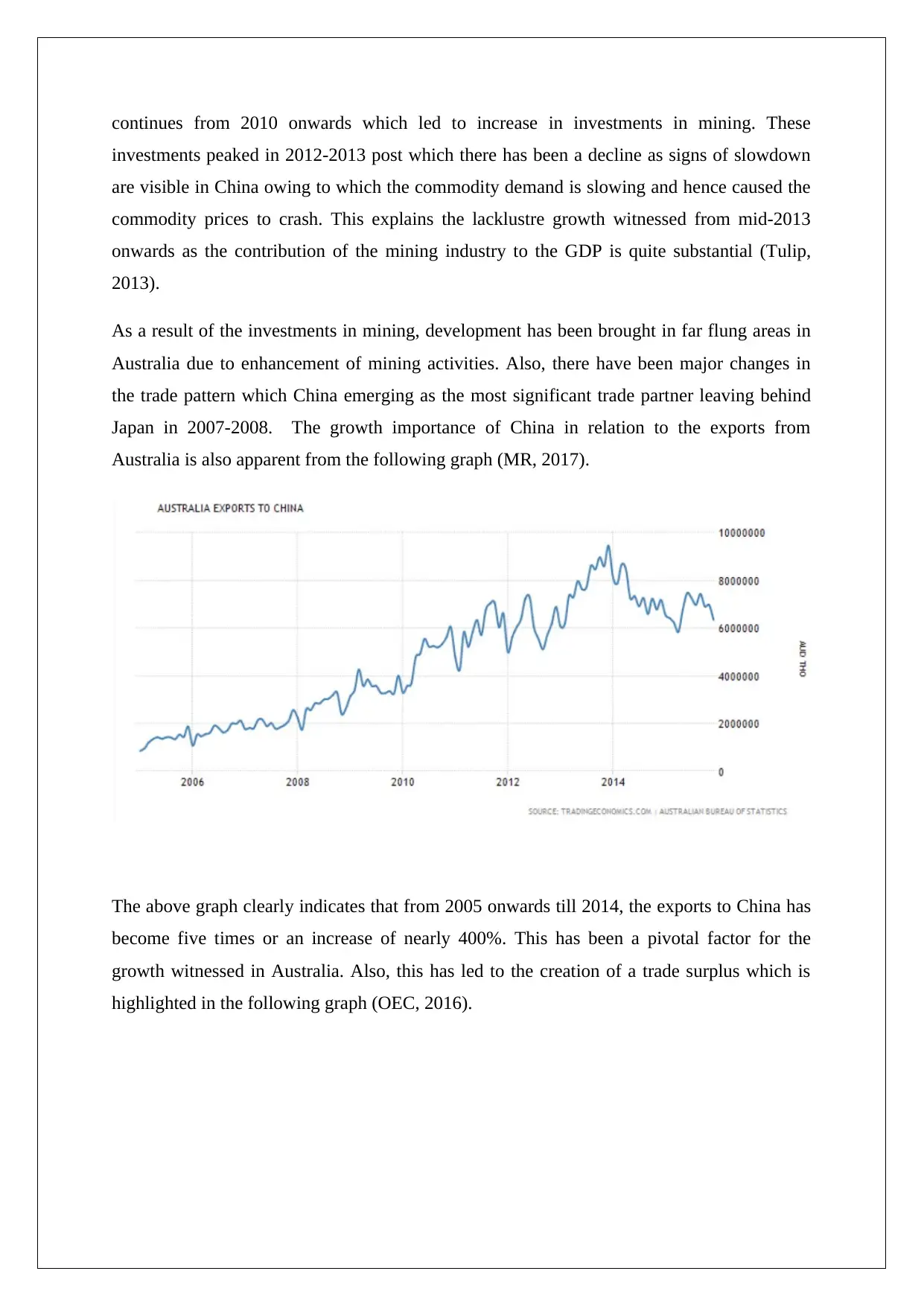

As a result of the investments in mining, development has been brought in far flung areas in

Australia due to enhancement of mining activities. Also, there have been major changes in

the trade pattern which China emerging as the most significant trade partner leaving behind

Japan in 2007-2008. The growth importance of China in relation to the exports from

Australia is also apparent from the following graph (MR, 2017).

The above graph clearly indicates that from 2005 onwards till 2014, the exports to China has

become five times or an increase of nearly 400%. This has been a pivotal factor for the

growth witnessed in Australia. Also, this has led to the creation of a trade surplus which is

highlighted in the following graph (OEC, 2016).

investments peaked in 2012-2013 post which there has been a decline as signs of slowdown

are visible in China owing to which the commodity demand is slowing and hence caused the

commodity prices to crash. This explains the lacklustre growth witnessed from mid-2013

onwards as the contribution of the mining industry to the GDP is quite substantial (Tulip,

2013).

As a result of the investments in mining, development has been brought in far flung areas in

Australia due to enhancement of mining activities. Also, there have been major changes in

the trade pattern which China emerging as the most significant trade partner leaving behind

Japan in 2007-2008. The growth importance of China in relation to the exports from

Australia is also apparent from the following graph (MR, 2017).

The above graph clearly indicates that from 2005 onwards till 2014, the exports to China has

become five times or an increase of nearly 400%. This has been a pivotal factor for the

growth witnessed in Australia. Also, this has led to the creation of a trade surplus which is

highlighted in the following graph (OEC, 2016).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

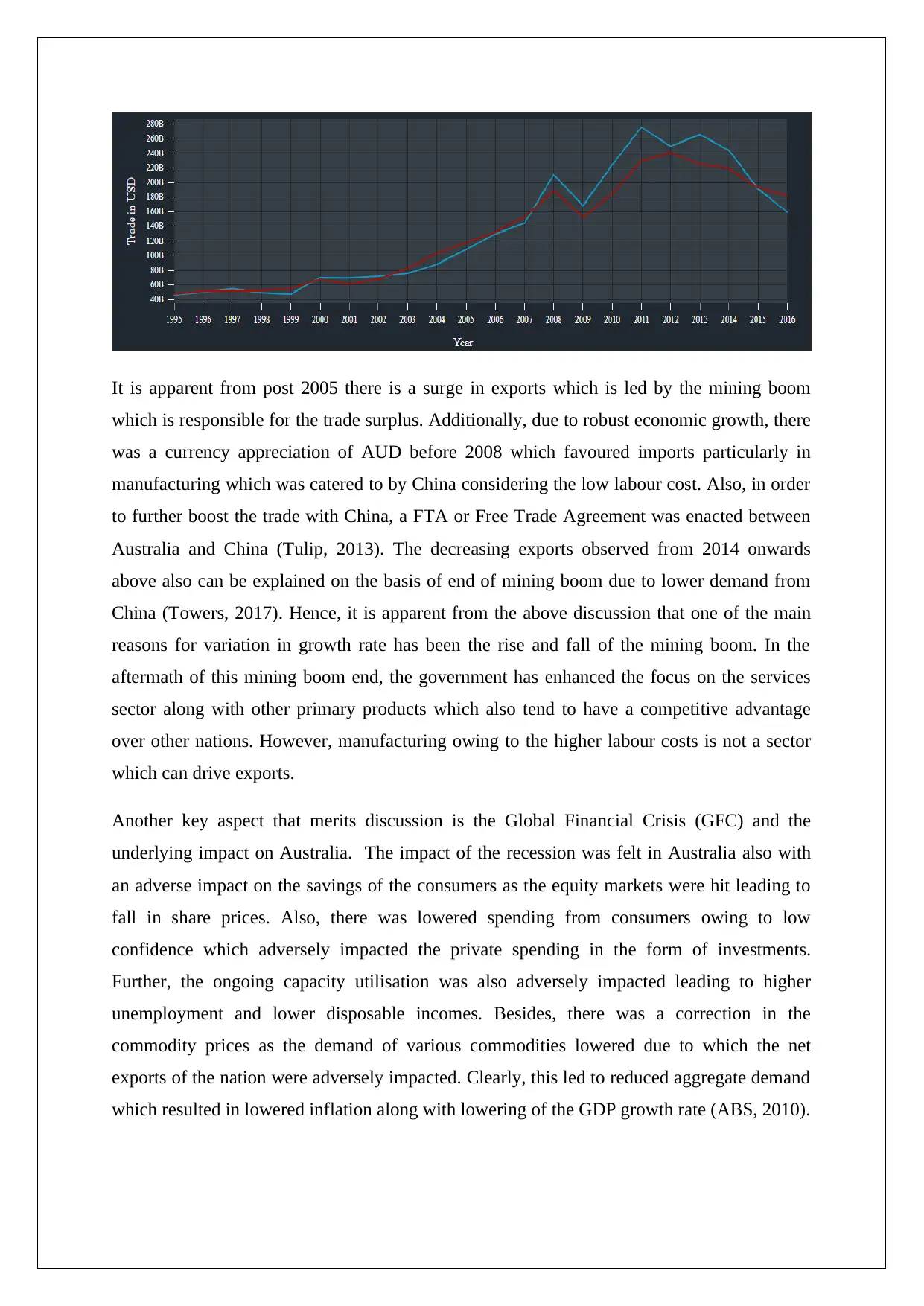

It is apparent from post 2005 there is a surge in exports which is led by the mining boom

which is responsible for the trade surplus. Additionally, due to robust economic growth, there

was a currency appreciation of AUD before 2008 which favoured imports particularly in

manufacturing which was catered to by China considering the low labour cost. Also, in order

to further boost the trade with China, a FTA or Free Trade Agreement was enacted between

Australia and China (Tulip, 2013). The decreasing exports observed from 2014 onwards

above also can be explained on the basis of end of mining boom due to lower demand from

China (Towers, 2017). Hence, it is apparent from the above discussion that one of the main

reasons for variation in growth rate has been the rise and fall of the mining boom. In the

aftermath of this mining boom end, the government has enhanced the focus on the services

sector along with other primary products which also tend to have a competitive advantage

over other nations. However, manufacturing owing to the higher labour costs is not a sector

which can drive exports.

Another key aspect that merits discussion is the Global Financial Crisis (GFC) and the

underlying impact on Australia. The impact of the recession was felt in Australia also with

an adverse impact on the savings of the consumers as the equity markets were hit leading to

fall in share prices. Also, there was lowered spending from consumers owing to low

confidence which adversely impacted the private spending in the form of investments.

Further, the ongoing capacity utilisation was also adversely impacted leading to higher

unemployment and lower disposable incomes. Besides, there was a correction in the

commodity prices as the demand of various commodities lowered due to which the net

exports of the nation were adversely impacted. Clearly, this led to reduced aggregate demand

which resulted in lowered inflation along with lowering of the GDP growth rate (ABS, 2010).

which is responsible for the trade surplus. Additionally, due to robust economic growth, there

was a currency appreciation of AUD before 2008 which favoured imports particularly in

manufacturing which was catered to by China considering the low labour cost. Also, in order

to further boost the trade with China, a FTA or Free Trade Agreement was enacted between

Australia and China (Tulip, 2013). The decreasing exports observed from 2014 onwards

above also can be explained on the basis of end of mining boom due to lower demand from

China (Towers, 2017). Hence, it is apparent from the above discussion that one of the main

reasons for variation in growth rate has been the rise and fall of the mining boom. In the

aftermath of this mining boom end, the government has enhanced the focus on the services

sector along with other primary products which also tend to have a competitive advantage

over other nations. However, manufacturing owing to the higher labour costs is not a sector

which can drive exports.

Another key aspect that merits discussion is the Global Financial Crisis (GFC) and the

underlying impact on Australia. The impact of the recession was felt in Australia also with

an adverse impact on the savings of the consumers as the equity markets were hit leading to

fall in share prices. Also, there was lowered spending from consumers owing to low

confidence which adversely impacted the private spending in the form of investments.

Further, the ongoing capacity utilisation was also adversely impacted leading to higher

unemployment and lower disposable incomes. Besides, there was a correction in the

commodity prices as the demand of various commodities lowered due to which the net

exports of the nation were adversely impacted. Clearly, this led to reduced aggregate demand

which resulted in lowered inflation along with lowering of the GDP growth rate (ABS, 2010).

However, the impact of GFC was rather limited on Australia in comparison to other

developed countries primarily because of two main factors. One was the strong fiscal

situation of the country going into the crisis. The fiscal deficits owing to the trade surpluses

were quite lower in comparison to other nations. Also, the sovereign debt was maintained at a

much lower level which provided the government with higher flexibility in providing higher

economic stimulus (Pickering, 2014). Further, the banking system of Australia was quite

robust due to which there was no need for the government to provide fiscal stimulus and

hence the government could instead focus on the economy as a whole rather than a sector in

particular. The second factor was the quick recovery of China which was responsible for the

high growth observed from Q2 in 2010 to Q1 2011 (Alexander, 2013).

The response of the government to the crisis was measured and the government aimed to

maintain a balance between inflation and the downside risks posed by the GFC. As a result,

the government proposed a 2008-2009 budget which had a projected surplus of A$ 20 billion

so that the future ability to avert the crisis is not jeopardised. Further, a slew of measures

were taken to provide confidence to the financial sector. This included government

guarantees in relation to the deposits, wholesale funding, purchase of mortgage based

securities to the extent of A$8 billion and also banning short sales in certain financial

instruments. This ensured that the confidence of the people in the financial sector did not

dwindle and also there were not any financial defaults in this regards (Kennedy, 2009).

Further, measures were undertaken to enhance the overall consumer confidence so as to

enhance the demand from consumers and thereby ensure that economic growth is maintained.

This included payment of $ 4.9 billion to pensioners along with $ 3.9 billion to families

belonging to low and middle income group so that they can continue their purchases of basic

necessities. Further, the traditional monetary policy tools and fiscal stimulus was also

observed. The policy rates were lowered so as to ensure that liquidity remains in the system

and also the loan rates are low. Also, fiscal stimulus to ailing businesses in the form of tax

rebates was extended so that they can witness the difficult times. Overall, the financial

policies exhibited by the government during the crisis were quite effective and free from

excesses which ensured quick recovery unlike other western nations (Australian Government,

2009).

Major Challenges

developed countries primarily because of two main factors. One was the strong fiscal

situation of the country going into the crisis. The fiscal deficits owing to the trade surpluses

were quite lower in comparison to other nations. Also, the sovereign debt was maintained at a

much lower level which provided the government with higher flexibility in providing higher

economic stimulus (Pickering, 2014). Further, the banking system of Australia was quite

robust due to which there was no need for the government to provide fiscal stimulus and

hence the government could instead focus on the economy as a whole rather than a sector in

particular. The second factor was the quick recovery of China which was responsible for the

high growth observed from Q2 in 2010 to Q1 2011 (Alexander, 2013).

The response of the government to the crisis was measured and the government aimed to

maintain a balance between inflation and the downside risks posed by the GFC. As a result,

the government proposed a 2008-2009 budget which had a projected surplus of A$ 20 billion

so that the future ability to avert the crisis is not jeopardised. Further, a slew of measures

were taken to provide confidence to the financial sector. This included government

guarantees in relation to the deposits, wholesale funding, purchase of mortgage based

securities to the extent of A$8 billion and also banning short sales in certain financial

instruments. This ensured that the confidence of the people in the financial sector did not

dwindle and also there were not any financial defaults in this regards (Kennedy, 2009).

Further, measures were undertaken to enhance the overall consumer confidence so as to

enhance the demand from consumers and thereby ensure that economic growth is maintained.

This included payment of $ 4.9 billion to pensioners along with $ 3.9 billion to families

belonging to low and middle income group so that they can continue their purchases of basic

necessities. Further, the traditional monetary policy tools and fiscal stimulus was also

observed. The policy rates were lowered so as to ensure that liquidity remains in the system

and also the loan rates are low. Also, fiscal stimulus to ailing businesses in the form of tax

rebates was extended so that they can witness the difficult times. Overall, the financial

policies exhibited by the government during the crisis were quite effective and free from

excesses which ensured quick recovery unlike other western nations (Australian Government,

2009).

Major Challenges

While the Australian economy remained quite unscathed in relative terms during the GFC,

however, a bigger crisis seems to be looming at the present for the Australian economy. The

major reason for the same is the temporary end in mining boom and the need to find

alternatives to fill the gap which is pivotal considering the cyclical fluctuations in price of

various commodities. Since finding alternative customers to China is next to impossible,

hence the policymakers feel that there is a strong case for diversifying the economy lowering

the dependence on mining. However, this is easier said than done.

One of the major challenges in this regard is the ailing manufacturing industry which over the

decade has largely been overrun by Chinese goods due to which the industry has further

dwindled Owing to the FTA with China, the trade barriers have been practically nullified

which has led to surge in imports of textile and electronic goods particularly computed. Also,

the car industry is at the verge of closing down with the government not willing to extend

financial support any longer. Also, considering the low population of Australia coupled with

the geographical isolation, it is apparent that the manufacturing industry would find it

difficult to thrive without government support. The economies to scale are difficult to achieve

and hence companies worried about costs set their plants in Asia while the high end

manufacturing happens in US and Europe where market availability is plenty (Tulip, 2013).

Coming to services, the local markets seem quite saturated and the potential source of growth

seems to be only foreign markets. Again penetration in the foreign markets (both developed

and developing world) is quite difficult owing to the existence of a number of players. One

service where Australia has an edge is education which needs to be promoted further but it is

unlikely that would bring in so huge gains that the economy can be transformed. Also,

considering the geographical isolation, the export of services would involve migration of

trained manpower to far off countries with significant differences in culture and history. The

primary sector with livestock products also has potential but owing to the increasing changes

in climate, this is increasingly a challenge as there is inconsistency in the production. Further,

there are alternate players from the developed and developing world from which Australia

has to be face fierce competition coupled with higher logistics cost which leaves the Australia

exporters at a disadvantage.

Hence, on the basis of the above discussion, it is apparent that while GFC has been averted

by the economy but going forward there is a need to diversify the economy which is quite

difficult. The local demand remains saturated owing to limited population and the

however, a bigger crisis seems to be looming at the present for the Australian economy. The

major reason for the same is the temporary end in mining boom and the need to find

alternatives to fill the gap which is pivotal considering the cyclical fluctuations in price of

various commodities. Since finding alternative customers to China is next to impossible,

hence the policymakers feel that there is a strong case for diversifying the economy lowering

the dependence on mining. However, this is easier said than done.

One of the major challenges in this regard is the ailing manufacturing industry which over the

decade has largely been overrun by Chinese goods due to which the industry has further

dwindled Owing to the FTA with China, the trade barriers have been practically nullified

which has led to surge in imports of textile and electronic goods particularly computed. Also,

the car industry is at the verge of closing down with the government not willing to extend

financial support any longer. Also, considering the low population of Australia coupled with

the geographical isolation, it is apparent that the manufacturing industry would find it

difficult to thrive without government support. The economies to scale are difficult to achieve

and hence companies worried about costs set their plants in Asia while the high end

manufacturing happens in US and Europe where market availability is plenty (Tulip, 2013).

Coming to services, the local markets seem quite saturated and the potential source of growth

seems to be only foreign markets. Again penetration in the foreign markets (both developed

and developing world) is quite difficult owing to the existence of a number of players. One

service where Australia has an edge is education which needs to be promoted further but it is

unlikely that would bring in so huge gains that the economy can be transformed. Also,

considering the geographical isolation, the export of services would involve migration of

trained manpower to far off countries with significant differences in culture and history. The

primary sector with livestock products also has potential but owing to the increasing changes

in climate, this is increasingly a challenge as there is inconsistency in the production. Further,

there are alternate players from the developed and developing world from which Australia

has to be face fierce competition coupled with higher logistics cost which leaves the Australia

exporters at a disadvantage.

Hence, on the basis of the above discussion, it is apparent that while GFC has been averted

by the economy but going forward there is a need to diversify the economy which is quite

difficult. The local demand remains saturated owing to limited population and the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

geographical isolation of the countries implies that tapping the export markets is a challenge.

Going forward, the policy makers would have to work out sustainable solutions to these

issues so as to push the Australian economy forward and reduce their inherent dependence on

mining and China.

Going forward, the policy makers would have to work out sustainable solutions to these

issues so as to push the Australian economy forward and reduce their inherent dependence on

mining and China.

References

ABS (2010) FEATURES ARTICLE: THEGLOBAL FINANCIAL CRISES ANDITS IMPACT

ON AUSTRALIA. Retrieved on October 22, 2017 from

http://www.abs.gov.au/AUSSTATS/abs@.nsf/Lookup/1301.0Chapter27092009%E2

%80%9310

Alexander, D. (2013) How Australia weathered the global financial crisis while Europe

failed. Retrieved on October 22, 2017 from

https://www.theguardian.com/commentisfree/2013/aug/28/australia-global-economic-

crisis

Australian Government, (2009) PART 2: THE GOVERNMENT’S RESPONSE TO THE

GLOBAL FINANCIAL CRISIS. Retrieved on October 22, 2017 from

http://www.budget.gov.au/2008-09/content/myefo/html/part_2.htm

Holmes, A. (2012) Australia’s economic relationships with China. Retrieved on October 22,

2017 from https://www.aph.gov.au/About_Parliament/Parliamentary_Departments/

Parliamentary_Library/pubs/BriefingBook44p/China

Kennedy, S. (2009) AUSTRALIA’S RESPONSE TO THE GLOBAL FINANCIAL CRISIS.

Retrieved on October 22, 2017 from

https://static.treasury.gov.au/uploads/sites/1/2017/06/Australia_Israel_Leadership_For

um.pdf

M.R. (2017) How Australia has gone 25 years without a recession. Retrieved on October 22,

2017 from https://www.economist.com/blogs/economist-explains/2017/03/economist-

explains-11

OEC, (2016) Australia. Retrieved on October 22, 2017 from

http://atlas.media.mit.edu/en/profile/country/aus/

Pickering, C. (2014) Lessons for Australia from the GFC. Retrieved on October 22, 2017

from http://www.theaustralian.com.au/business/business-spectator/lessons-for-

australia-from-the-gfc/news-story/f6a0682272988717ad5b5d7c919190d7

Towers, C. (2017) The end of a mining boom leaves Australia’s economy surprisingly intact.

Retrieved on October 22, 2017 from

ABS (2010) FEATURES ARTICLE: THEGLOBAL FINANCIAL CRISES ANDITS IMPACT

ON AUSTRALIA. Retrieved on October 22, 2017 from

http://www.abs.gov.au/AUSSTATS/abs@.nsf/Lookup/1301.0Chapter27092009%E2

%80%9310

Alexander, D. (2013) How Australia weathered the global financial crisis while Europe

failed. Retrieved on October 22, 2017 from

https://www.theguardian.com/commentisfree/2013/aug/28/australia-global-economic-

crisis

Australian Government, (2009) PART 2: THE GOVERNMENT’S RESPONSE TO THE

GLOBAL FINANCIAL CRISIS. Retrieved on October 22, 2017 from

http://www.budget.gov.au/2008-09/content/myefo/html/part_2.htm

Holmes, A. (2012) Australia’s economic relationships with China. Retrieved on October 22,

2017 from https://www.aph.gov.au/About_Parliament/Parliamentary_Departments/

Parliamentary_Library/pubs/BriefingBook44p/China

Kennedy, S. (2009) AUSTRALIA’S RESPONSE TO THE GLOBAL FINANCIAL CRISIS.

Retrieved on October 22, 2017 from

https://static.treasury.gov.au/uploads/sites/1/2017/06/Australia_Israel_Leadership_For

um.pdf

M.R. (2017) How Australia has gone 25 years without a recession. Retrieved on October 22,

2017 from https://www.economist.com/blogs/economist-explains/2017/03/economist-

explains-11

OEC, (2016) Australia. Retrieved on October 22, 2017 from

http://atlas.media.mit.edu/en/profile/country/aus/

Pickering, C. (2014) Lessons for Australia from the GFC. Retrieved on October 22, 2017

from http://www.theaustralian.com.au/business/business-spectator/lessons-for-

australia-from-the-gfc/news-story/f6a0682272988717ad5b5d7c919190d7

Towers, C. (2017) The end of a mining boom leaves Australia’s economy surprisingly intact.

Retrieved on October 22, 2017 from

https://www.economist.com/news/asia/21718521-investment-mines-dries-up-

property-takes-up-slack-end-mining-boom-leaves

Tulip, P. (2013) The effect of the mining boom on the Australian Economy. Retrieved on

October 22, 2017 from https://www.rba.gov.au/publications/bulletin/2014/dec/pdf/bu-

1214-3.pdf

property-takes-up-slack-end-mining-boom-leaves

Tulip, P. (2013) The effect of the mining boom on the Australian Economy. Retrieved on

October 22, 2017 from https://www.rba.gov.au/publications/bulletin/2014/dec/pdf/bu-

1214-3.pdf

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.