Effectiveness of Financial Statement

VerifiedAdded on 2021/06/16

|21

|2452

|19

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: FINANCIAL ACCOUNTING

Financial accounting

Name of the University

Name of the student

Authors note

Financial accounting

Name of the University

Name of the student

Authors note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1

FINANCIAL ACCOUNTING

Table of Contents

Answer to Question 1:.....................................................................................................................2

Answer to Question 2:.....................................................................................................................7

Answer to Question 3:...................................................................................................................10

Answer to Question 4:...................................................................................................................14

Answer to Question 5:...................................................................................................................15

Reference list:................................................................................................................................17

FINANCIAL ACCOUNTING

Table of Contents

Answer to Question 1:.....................................................................................................................2

Answer to Question 2:.....................................................................................................................7

Answer to Question 3:...................................................................................................................10

Answer to Question 4:...................................................................................................................14

Answer to Question 5:...................................................................................................................15

Reference list:................................................................................................................................17

2

FINANCIAL ACCOUNTING

Answer to Question 1:

To,

Chairperson

International standard accounting board (IASB)

30 cannon street, London- EC4M 6XH, United Kingdom

Date: 4th March, 2018

Subject:

Sir,

I am writing this letter that will form a part of recommendations for incorporating the

principles of effective communication in presenting the financial information in the annual report

of company. Such recommendation will help entities in improving the effectiveness of

disclosures for the financial statement users. Being an investor, currently, I am intending to make

investment in stocks of two companies that are listed on the stock exchange of Australia that is

Common wealth bank of Australia (CBA) and National Australia bank (NAB). For the purpose

of evaluation of financial position of both the banking organizations, I have reviewed and

evaluated the annual report of both organizations in respect of the disclosures they are made

regarding their financial data and information. I have come to known with some of the areas

where the disclosure is lacking on different aspects such as comparability and transparency and

have thought of submitting my response towards such disclosure evaluation. Financial

information disclosure presented by company in the annual reports as perceived by the

accounting standard are often faced with some of the issues such as disclosure of insufficient

FINANCIAL ACCOUNTING

Answer to Question 1:

To,

Chairperson

International standard accounting board (IASB)

30 cannon street, London- EC4M 6XH, United Kingdom

Date: 4th March, 2018

Subject:

Sir,

I am writing this letter that will form a part of recommendations for incorporating the

principles of effective communication in presenting the financial information in the annual report

of company. Such recommendation will help entities in improving the effectiveness of

disclosures for the financial statement users. Being an investor, currently, I am intending to make

investment in stocks of two companies that are listed on the stock exchange of Australia that is

Common wealth bank of Australia (CBA) and National Australia bank (NAB). For the purpose

of evaluation of financial position of both the banking organizations, I have reviewed and

evaluated the annual report of both organizations in respect of the disclosures they are made

regarding their financial data and information. I have come to known with some of the areas

where the disclosure is lacking on different aspects such as comparability and transparency and

have thought of submitting my response towards such disclosure evaluation. Financial

information disclosure presented by company in the annual reports as perceived by the

accounting standard are often faced with some of the issues such as disclosure of insufficient

3

FINANCIAL ACCOUNTING

information in the notes that do not provide users with accurate picture of financial position of

company (Abernathy et al., 2016). Furthermore, there might be presence of irrelevant

information in the disclosed notes that might not be beneficial for investors to make financial

decision.

While going through the disclosure initiatives as a part of principles of disclosure that is

proposed by International accounting standard, I have come across seven principles that would

help in reducing the difficulties while judging the financial statements. It is believed by the board

that such principles of disclosure would encourage entities for communicating the information in

an effective way and application of better judgment by financial statement users. The seven

principles that I have become acquainted with for increasing the effectiveness of financial

information as proposed by board are clear and simple, comparable, entity specific, organized for

highlighting important matters, information should be in an appropriate format, it should be well

organized for highlighting the important matters, information should be linked to related matters

and disclosed information should be free from any unnecessary duplication. Disclosing the

information in an appropriate manner would involve use of table, charts, lists and graphs

(Klychova et al., 2017).

Providing IASB with the feedback on the disclosure principles would have much valued

by the board as it would help in contributing to the well grounded and robust discussion on the

disclosure principles. From the analysis of the annual report of both organizations, it can be

inferred that NAB as well as CBA lacks on disclosure fronts in several aspects as there are no

sufficient and appropriate disclosures of information that are depicted in the financial statements.

There are no separate presentations of the disclosures that are made in the financial statements. It

has been ascertained from the analysis that organization has not used any segmental approach

FINANCIAL ACCOUNTING

information in the notes that do not provide users with accurate picture of financial position of

company (Abernathy et al., 2016). Furthermore, there might be presence of irrelevant

information in the disclosed notes that might not be beneficial for investors to make financial

decision.

While going through the disclosure initiatives as a part of principles of disclosure that is

proposed by International accounting standard, I have come across seven principles that would

help in reducing the difficulties while judging the financial statements. It is believed by the board

that such principles of disclosure would encourage entities for communicating the information in

an effective way and application of better judgment by financial statement users. The seven

principles that I have become acquainted with for increasing the effectiveness of financial

information as proposed by board are clear and simple, comparable, entity specific, organized for

highlighting important matters, information should be in an appropriate format, it should be well

organized for highlighting the important matters, information should be linked to related matters

and disclosed information should be free from any unnecessary duplication. Disclosing the

information in an appropriate manner would involve use of table, charts, lists and graphs

(Klychova et al., 2017).

Providing IASB with the feedback on the disclosure principles would have much valued

by the board as it would help in contributing to the well grounded and robust discussion on the

disclosure principles. From the analysis of the annual report of both organizations, it can be

inferred that NAB as well as CBA lacks on disclosure fronts in several aspects as there are no

sufficient and appropriate disclosures of information that are depicted in the financial statements.

There are no separate presentations of the disclosures that are made in the financial statements. It

has been ascertained from the analysis that organization has not used any segmental approach

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4

FINANCIAL ACCOUNTING

and has not adopted any consistent segment definition in light of some disclosed matters.

Moreover, there is no proper presentation of information as the users will not be able to create

any relationship and thereby it is required by organization to improve the navigation (Trucco,

2015). In addition to this, the information on credit and liquidity risks has been presented

separately. Nevertheless, the information presented in the table format by both the organization

are capable of being compared from year to year and determine the trend of increasing or

decreasing financial information. Therefore, investors are capable of analyzing the trend that

forms an essential part of investment decision process.

In addition to the disclosures that have been identified above from reviewing of annual

report, it is a known fact that for banking institutions that disclosure for banking requirement is

of utmost importance. This is so because Basel is the measures or the reforms that are undertaken

for strengthening the regulations of banking industry. From the annual report analysis of both the

banks, it can be seen that disclosure about requirement of Basel are disclosed adequately in the

notes to financial statements. Another important factor that has been identified in the

presentation of financial information is usage of an appropriate format (Schipper et al., 2017). It

has been identified that there is a difference in presentation of data using an appropriate format.

From the annual report of CBA, it can be seen that financial information has been presented by

making a very restricted use of charts, graphs and tables. NAB on other hand, have not made any

disclosure of financial information using graphs or charts. In addition to this, the divisional

performance of NAB is presented only in the table format and there is no detailed explanation of

the same in the annual report. On other hand, CBA have made appropriate disclosure of the

divisional performance in the notes to financial statements in addition to the table format.

FINANCIAL ACCOUNTING

and has not adopted any consistent segment definition in light of some disclosed matters.

Moreover, there is no proper presentation of information as the users will not be able to create

any relationship and thereby it is required by organization to improve the navigation (Trucco,

2015). In addition to this, the information on credit and liquidity risks has been presented

separately. Nevertheless, the information presented in the table format by both the organization

are capable of being compared from year to year and determine the trend of increasing or

decreasing financial information. Therefore, investors are capable of analyzing the trend that

forms an essential part of investment decision process.

In addition to the disclosures that have been identified above from reviewing of annual

report, it is a known fact that for banking institutions that disclosure for banking requirement is

of utmost importance. This is so because Basel is the measures or the reforms that are undertaken

for strengthening the regulations of banking industry. From the annual report analysis of both the

banks, it can be seen that disclosure about requirement of Basel are disclosed adequately in the

notes to financial statements. Another important factor that has been identified in the

presentation of financial information is usage of an appropriate format (Schipper et al., 2017). It

has been identified that there is a difference in presentation of data using an appropriate format.

From the annual report of CBA, it can be seen that financial information has been presented by

making a very restricted use of charts, graphs and tables. NAB on other hand, have not made any

disclosure of financial information using graphs or charts. In addition to this, the divisional

performance of NAB is presented only in the table format and there is no detailed explanation of

the same in the annual report. On other hand, CBA have made appropriate disclosure of the

divisional performance in the notes to financial statements in addition to the table format.

5

FINANCIAL ACCOUNTING

For improving the communication effectiveness of the presented financial information in

the report, I would like to make some recommendations after ascertaining the area where the

organizations are lacking on disclosure front. The data presentation should be specific to nature

and business of reporting entities as entity specific information’s are regarded as valuable to

investors because general information can be accessed from several sources. For disclosing the

relevant information that is considered essential for decision making of investors, organization

should make use of appropriate format. Some common form of formatting should be used by

organization depending upon the circumstance in which entity operates and their operating

conditions. In addition to this, I would recommend organizations to incorporate use of charts and

graphs for presentation of financial data pertaining to their financial conditions. This is so

because users find it suitable to analyze the financial performance of company by using such

format as it is less time consuming (Jiang et al., 2015). In addition to this, they are able to view

the trend of performance of company over a considerable time periods.

The information presented in the annual report should be linked to other information and

thereby improving navigation so that relationship between pieces of information’s are

highlighted properly. Usefulness of presented information can be increased by easing the

comparability across the reporting period and among the entities. Therefore, as an investor, I

would recommend to the board to make improvement in the disclosures of the financial

information by reporting entity. The recommended principles for enhancing the effectiveness of

communication of financial information are easing comparability, using an appropriate format,

creating linkage to related information, information should be organization specific. It is

essential for board to address the disclosure issues by recommending on using the effective

FINANCIAL ACCOUNTING

For improving the communication effectiveness of the presented financial information in

the report, I would like to make some recommendations after ascertaining the area where the

organizations are lacking on disclosure front. The data presentation should be specific to nature

and business of reporting entities as entity specific information’s are regarded as valuable to

investors because general information can be accessed from several sources. For disclosing the

relevant information that is considered essential for decision making of investors, organization

should make use of appropriate format. Some common form of formatting should be used by

organization depending upon the circumstance in which entity operates and their operating

conditions. In addition to this, I would recommend organizations to incorporate use of charts and

graphs for presentation of financial data pertaining to their financial conditions. This is so

because users find it suitable to analyze the financial performance of company by using such

format as it is less time consuming (Jiang et al., 2015). In addition to this, they are able to view

the trend of performance of company over a considerable time periods.

The information presented in the annual report should be linked to other information and

thereby improving navigation so that relationship between pieces of information’s are

highlighted properly. Usefulness of presented information can be increased by easing the

comparability across the reporting period and among the entities. Therefore, as an investor, I

would recommend to the board to make improvement in the disclosures of the financial

information by reporting entity. The recommended principles for enhancing the effectiveness of

communication of financial information are easing comparability, using an appropriate format,

creating linkage to related information, information should be organization specific. It is

essential for board to address the disclosure issues by recommending on using the effective

6

FINANCIAL ACCOUNTING

disclosure principles so that investors can have proper understanding of the financial information

(Barth, 2015).

Therefore, it is essential for reporting entities to take into account all the issues pertaining

to lack of disclosure of financial information’s. Banking institutions such as CBA and NAB

should improve their effectiveness of disclosed information by adopting the principles of

disclosure initiatives as recommended by the board.

FINANCIAL ACCOUNTING

disclosure principles so that investors can have proper understanding of the financial information

(Barth, 2015).

Therefore, it is essential for reporting entities to take into account all the issues pertaining

to lack of disclosure of financial information’s. Banking institutions such as CBA and NAB

should improve their effectiveness of disclosed information by adopting the principles of

disclosure initiatives as recommended by the board.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

FINANCIAL ACCOUNTING

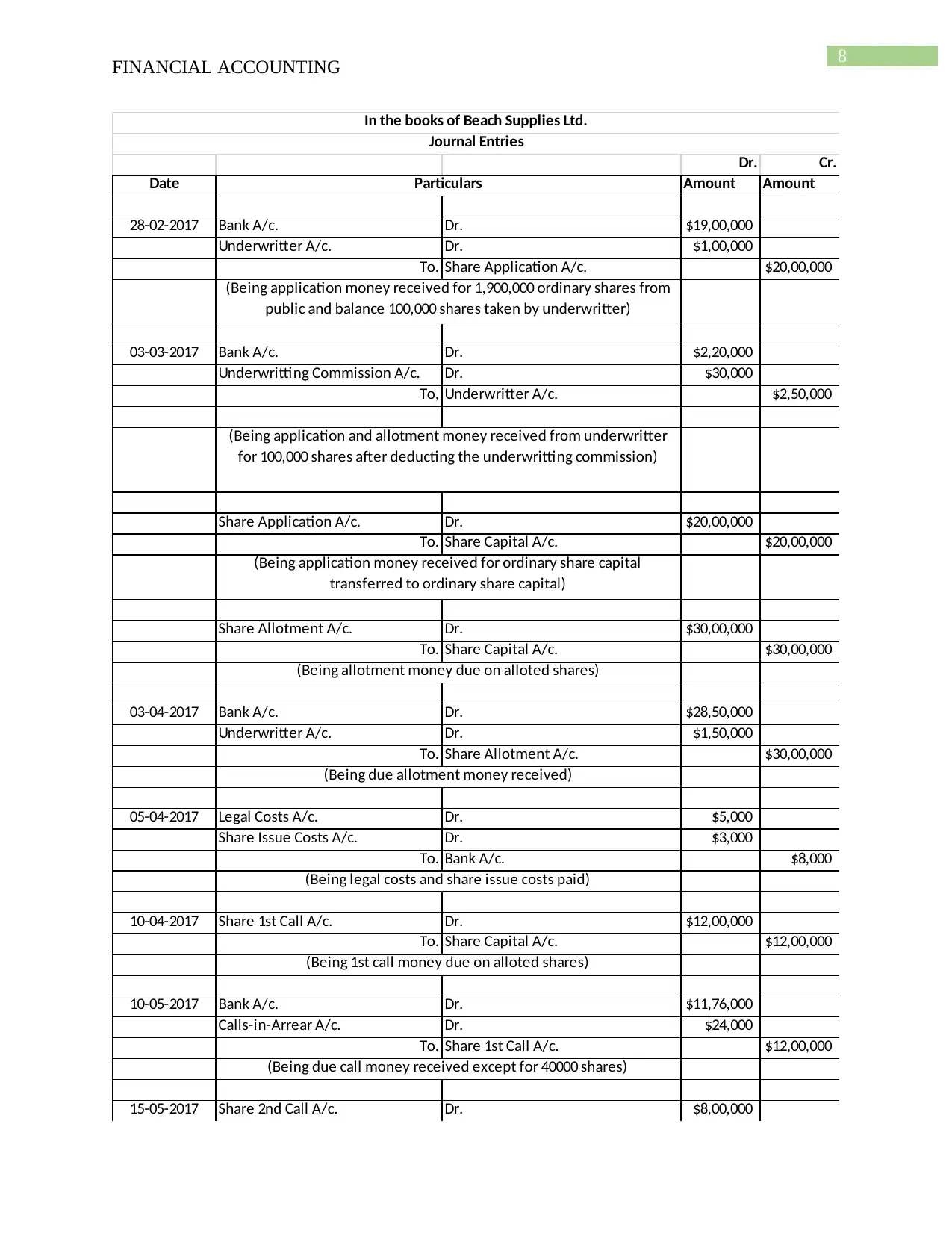

Answer to Question 2:

FINANCIAL ACCOUNTING

Answer to Question 2:

8

FINANCIAL ACCOUNTING

Dr. Cr.

Date Amount Amount

28-02-2017 Bank A/c. Dr. $19,00,000

Underwritter A/c. Dr. $1,00,000

To. Share Application A/c. $20,00,000

03-03-2017 Bank A/c. Dr. $2,20,000

Underwritting Commission A/c. Dr. $30,000

To, Underwritter A/c. $2,50,000

Share Application A/c. Dr. $20,00,000

To. Share Capital A/c. $20,00,000

Share Allotment A/c. Dr. $30,00,000

To. Share Capital A/c. $30,00,000

03-04-2017 Bank A/c. Dr. $28,50,000

Underwritter A/c. Dr. $1,50,000

To. Share Allotment A/c. $30,00,000

05-04-2017 Legal Costs A/c. Dr. $5,000

Share Issue Costs A/c. Dr. $3,000

To. Bank A/c. $8,000

10-04-2017 Share 1st Call A/c. Dr. $12,00,000

To. Share Capital A/c. $12,00,000

10-05-2017 Bank A/c. Dr. $11,76,000

Calls-in-Arrear A/c. Dr. $24,000

To. Share 1st Call A/c. $12,00,000

15-05-2017 Share 2nd Call A/c. Dr. $8,00,000

Particulars

(Being application money received for 1,900,000 ordinary shares from

public and balance 100,000 shares taken by underwritter)

(Being application and allotment money received from underwritter

for 100,000 shares after deducting the underwritting commission)

(Being application money received for ordinary share capital

transferred to ordinary share capital)

(Being allotment money due on alloted shares)

(Being due allotment money received)

(Being 1st call money due on alloted shares)

(Being due call money received except for 40000 shares)

(Being legal costs and share issue costs paid)

In the books of Beach Supplies Ltd.

Journal Entries

FINANCIAL ACCOUNTING

Dr. Cr.

Date Amount Amount

28-02-2017 Bank A/c. Dr. $19,00,000

Underwritter A/c. Dr. $1,00,000

To. Share Application A/c. $20,00,000

03-03-2017 Bank A/c. Dr. $2,20,000

Underwritting Commission A/c. Dr. $30,000

To, Underwritter A/c. $2,50,000

Share Application A/c. Dr. $20,00,000

To. Share Capital A/c. $20,00,000

Share Allotment A/c. Dr. $30,00,000

To. Share Capital A/c. $30,00,000

03-04-2017 Bank A/c. Dr. $28,50,000

Underwritter A/c. Dr. $1,50,000

To. Share Allotment A/c. $30,00,000

05-04-2017 Legal Costs A/c. Dr. $5,000

Share Issue Costs A/c. Dr. $3,000

To. Bank A/c. $8,000

10-04-2017 Share 1st Call A/c. Dr. $12,00,000

To. Share Capital A/c. $12,00,000

10-05-2017 Bank A/c. Dr. $11,76,000

Calls-in-Arrear A/c. Dr. $24,000

To. Share 1st Call A/c. $12,00,000

15-05-2017 Share 2nd Call A/c. Dr. $8,00,000

Particulars

(Being application money received for 1,900,000 ordinary shares from

public and balance 100,000 shares taken by underwritter)

(Being application and allotment money received from underwritter

for 100,000 shares after deducting the underwritting commission)

(Being application money received for ordinary share capital

transferred to ordinary share capital)

(Being allotment money due on alloted shares)

(Being due allotment money received)

(Being 1st call money due on alloted shares)

(Being due call money received except for 40000 shares)

(Being legal costs and share issue costs paid)

In the books of Beach Supplies Ltd.

Journal Entries

9

FINANCIAL ACCOUNTING

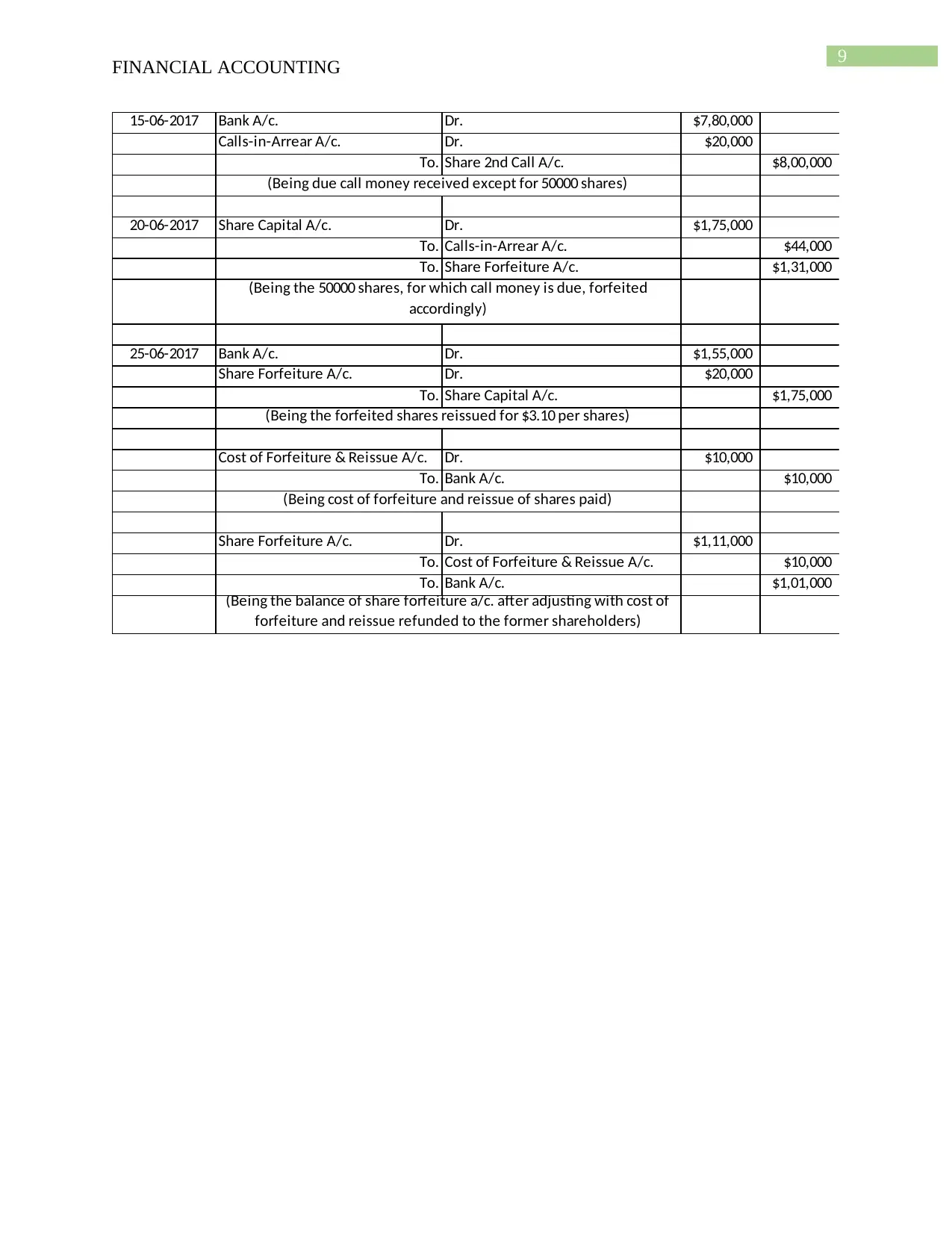

15-06-2017 Bank A/c. Dr. $7,80,000

Calls-in-Arrear A/c. Dr. $20,000

To. Share 2nd Call A/c. $8,00,000

20-06-2017 Share Capital A/c. Dr. $1,75,000

To. Calls-in-Arrear A/c. $44,000

To. Share Forfeiture A/c. $1,31,000

25-06-2017 Bank A/c. Dr. $1,55,000

Share Forfeiture A/c. Dr. $20,000

To. Share Capital A/c. $1,75,000

Cost of Forfeiture & Reissue A/c. Dr. $10,000

To. Bank A/c. $10,000

Share Forfeiture A/c. Dr. $1,11,000

To. Cost of Forfeiture & Reissue A/c. $10,000

To. Bank A/c. $1,01,000

(Being the balance of share forfeiture a/c. after adjusting with cost of

forfeiture and reissue refunded to the former shareholders)

(Being the 50000 shares, for which call money is due, forfeited

accordingly)

(Being the forfeited shares reissued for $3.10 per shares)

(Being cost of forfeiture and reissue of shares paid)

(Being due call money received except for 50000 shares)

FINANCIAL ACCOUNTING

15-06-2017 Bank A/c. Dr. $7,80,000

Calls-in-Arrear A/c. Dr. $20,000

To. Share 2nd Call A/c. $8,00,000

20-06-2017 Share Capital A/c. Dr. $1,75,000

To. Calls-in-Arrear A/c. $44,000

To. Share Forfeiture A/c. $1,31,000

25-06-2017 Bank A/c. Dr. $1,55,000

Share Forfeiture A/c. Dr. $20,000

To. Share Capital A/c. $1,75,000

Cost of Forfeiture & Reissue A/c. Dr. $10,000

To. Bank A/c. $10,000

Share Forfeiture A/c. Dr. $1,11,000

To. Cost of Forfeiture & Reissue A/c. $10,000

To. Bank A/c. $1,01,000

(Being the balance of share forfeiture a/c. after adjusting with cost of

forfeiture and reissue refunded to the former shareholders)

(Being the 50000 shares, for which call money is due, forfeited

accordingly)

(Being the forfeited shares reissued for $3.10 per shares)

(Being cost of forfeiture and reissue of shares paid)

(Being due call money received except for 50000 shares)

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10

FINANCIAL ACCOUNTING

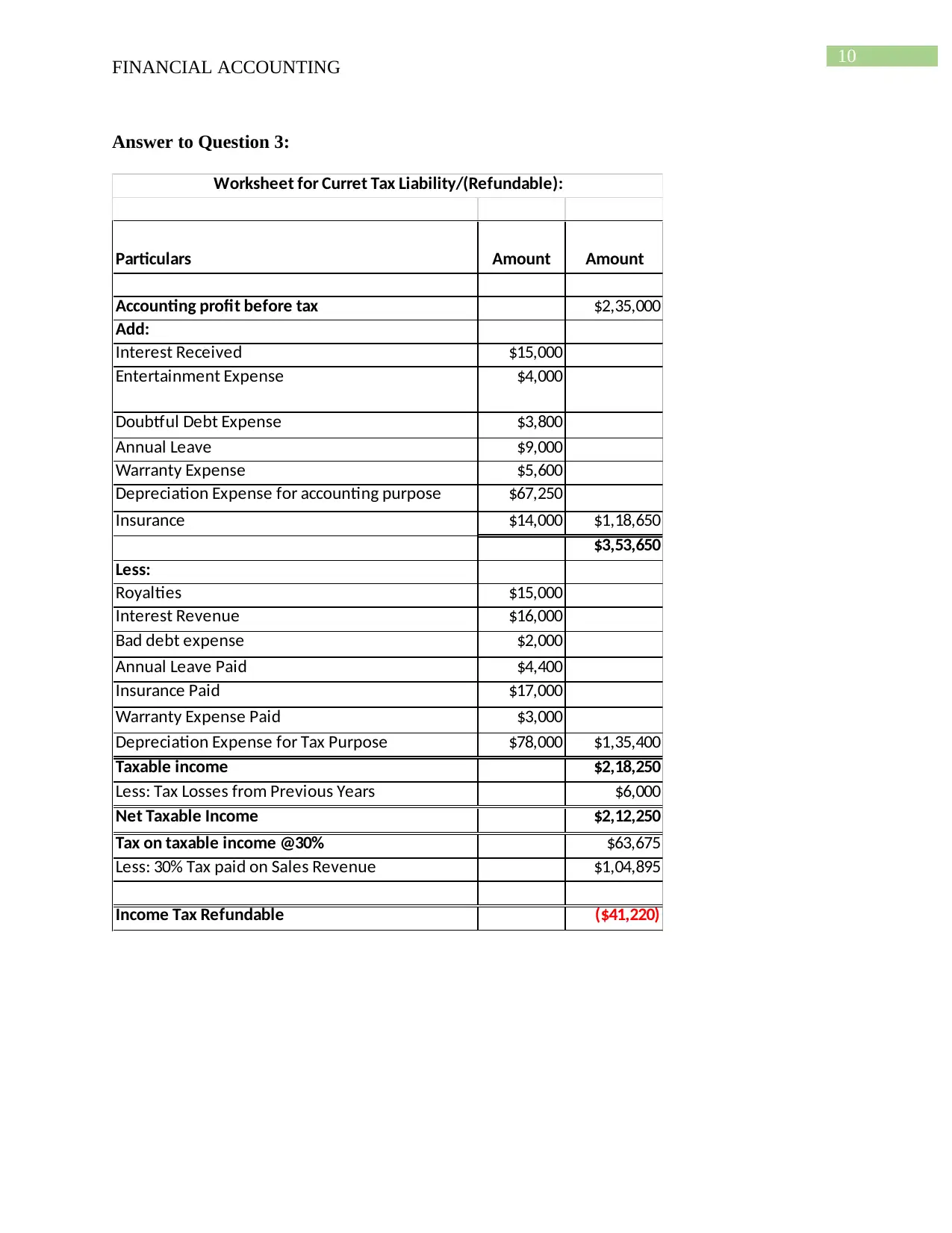

Answer to Question 3:

Particulars Amount Amount

Accounting profit before tax $2,35,000

Add:

Interest Received $15,000

Entertainment Expense $4,000

Doubtful Debt Expense $3,800

Annual Leave $9,000

Warranty Expense $5,600

Depreciation Expense for accounting purpose $67,250

Insurance $14,000 $1,18,650

$3,53,650

Less:

Royalties $15,000

Interest Revenue $16,000

Bad debt expense $2,000

Annual Leave Paid $4,400

Insurance Paid $17,000

Warranty Expense Paid $3,000

Depreciation Expense for Tax Purpose $78,000 $1,35,400

Taxable income $2,18,250

Less: Tax Losses from Previous Years $6,000

Net Taxable Income $2,12,250

Tax on taxable income @30% $63,675

Less: 30% Tax paid on Sales Revenue $1,04,895

Income Tax Refundable ($41,220)

Worksheet for Curret Tax Liability/(Refundable):

FINANCIAL ACCOUNTING

Answer to Question 3:

Particulars Amount Amount

Accounting profit before tax $2,35,000

Add:

Interest Received $15,000

Entertainment Expense $4,000

Doubtful Debt Expense $3,800

Annual Leave $9,000

Warranty Expense $5,600

Depreciation Expense for accounting purpose $67,250

Insurance $14,000 $1,18,650

$3,53,650

Less:

Royalties $15,000

Interest Revenue $16,000

Bad debt expense $2,000

Annual Leave Paid $4,400

Insurance Paid $17,000

Warranty Expense Paid $3,000

Depreciation Expense for Tax Purpose $78,000 $1,35,400

Taxable income $2,18,250

Less: Tax Losses from Previous Years $6,000

Net Taxable Income $2,12,250

Tax on taxable income @30% $63,675

Less: 30% Tax paid on Sales Revenue $1,04,895

Income Tax Refundable ($41,220)

Worksheet for Curret Tax Liability/(Refundable):

11

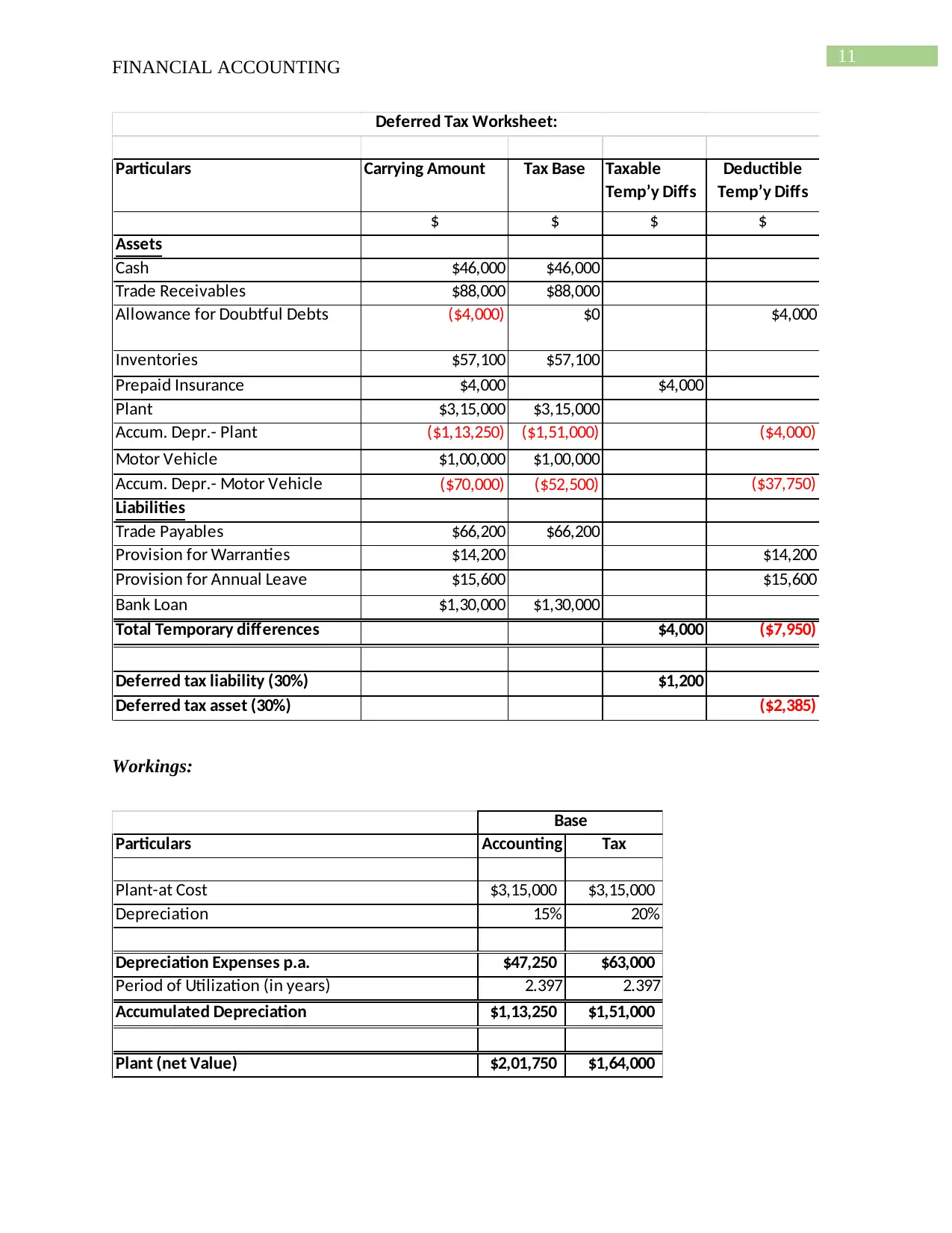

FINANCIAL ACCOUNTING

Particulars Carrying Amount Tax Base Taxable

Temp’y Diffs

Deductible

Temp’y Diffs

$ $ $ $

Assets

Cash $46,000 $46,000

Trade Receivables $88,000 $88,000

Allowance for Doubtful Debts ($4,000) $0 $4,000

Inventories $57,100 $57,100

Prepaid Insurance $4,000 $4,000

Plant $3,15,000 $3,15,000

Accum. Depr.- Plant ($1,13,250) ($1,51,000) ($4,000)

Motor Vehicle $1,00,000 $1,00,000

Accum. Depr.- Motor Vehicle ($70,000) ($52,500) ($37,750)

Liabilities

Trade Payables $66,200 $66,200

Provision for Warranties $14,200 $14,200

Provision for Annual Leave $15,600 $15,600

Bank Loan $1,30,000 $1,30,000

Total Temporary differences $4,000 ($7,950)

Deferred tax liability (30%) $1,200

Deferred tax asset (30%) ($2,385)

Deferred Tax Worksheet:

Workings:

Particulars Accounting Tax

Plant-at Cost $3,15,000 $3,15,000

Depreciation 15% 20%

Depreciation Expenses p.a. $47,250 $63,000

Period of Utilization (in years) 2.397 2.397

Accumulated Depreciation $1,13,250 $1,51,000

Plant (net Value) $2,01,750 $1,64,000

Base

FINANCIAL ACCOUNTING

Particulars Carrying Amount Tax Base Taxable

Temp’y Diffs

Deductible

Temp’y Diffs

$ $ $ $

Assets

Cash $46,000 $46,000

Trade Receivables $88,000 $88,000

Allowance for Doubtful Debts ($4,000) $0 $4,000

Inventories $57,100 $57,100

Prepaid Insurance $4,000 $4,000

Plant $3,15,000 $3,15,000

Accum. Depr.- Plant ($1,13,250) ($1,51,000) ($4,000)

Motor Vehicle $1,00,000 $1,00,000

Accum. Depr.- Motor Vehicle ($70,000) ($52,500) ($37,750)

Liabilities

Trade Payables $66,200 $66,200

Provision for Warranties $14,200 $14,200

Provision for Annual Leave $15,600 $15,600

Bank Loan $1,30,000 $1,30,000

Total Temporary differences $4,000 ($7,950)

Deferred tax liability (30%) $1,200

Deferred tax asset (30%) ($2,385)

Deferred Tax Worksheet:

Workings:

Particulars Accounting Tax

Plant-at Cost $3,15,000 $3,15,000

Depreciation 15% 20%

Depreciation Expenses p.a. $47,250 $63,000

Period of Utilization (in years) 2.397 2.397

Accumulated Depreciation $1,13,250 $1,51,000

Plant (net Value) $2,01,750 $1,64,000

Base

12

FINANCIAL ACCOUNTING

Base

Particulars Accounting Tax

Motor Vehicles-at Cost $1,00,000 $1,00,000

Depreciation 20% 15%

Depreciation Expenses p.a. $20,000 $15,000

Period of Utilization (in years) 3.500 3.500

Accumulated Depreciation $70,000 $52,500

Motor Vehicle (Net Value) $30,000 $47,500

Particulars Amount

Doubtful Debt Expense $3,800

Add: Allownace for Doubtful Debts on 2016 $2,200

Less: Allownace for Doubtful Debts on 2017 $4,000

Bad Debt Expense $2,000

Annual Leave Expenses $9,000

Add: Prov. For Annual Leaves on 2016 $11,000

Less: Prov. For Annual Leaves on 2017 $15,600

Annual Leave Paid $4,400

Warranty Expense $5,600

Add: Prov. For Warranty for 2016 $11,600

Less: Prov. For Warranty for 2017 $14,200

Warranty Expense Paid $3,000

Insurance Expense $14,000

Add: Prepaid Insurance for 2017 $4,000

Less: Prepaid Insurance for 2016 $1,000

Insurance Paid $17,000

Interest Revenue $16,000

Add: Interesr Receivable for 2016 $1,000

Less: Interesr Receivable for 2017 $2,000

Interest received $15,000

FINANCIAL ACCOUNTING

Base

Particulars Accounting Tax

Motor Vehicles-at Cost $1,00,000 $1,00,000

Depreciation 20% 15%

Depreciation Expenses p.a. $20,000 $15,000

Period of Utilization (in years) 3.500 3.500

Accumulated Depreciation $70,000 $52,500

Motor Vehicle (Net Value) $30,000 $47,500

Particulars Amount

Doubtful Debt Expense $3,800

Add: Allownace for Doubtful Debts on 2016 $2,200

Less: Allownace for Doubtful Debts on 2017 $4,000

Bad Debt Expense $2,000

Annual Leave Expenses $9,000

Add: Prov. For Annual Leaves on 2016 $11,000

Less: Prov. For Annual Leaves on 2017 $15,600

Annual Leave Paid $4,400

Warranty Expense $5,600

Add: Prov. For Warranty for 2016 $11,600

Less: Prov. For Warranty for 2017 $14,200

Warranty Expense Paid $3,000

Insurance Expense $14,000

Add: Prepaid Insurance for 2017 $4,000

Less: Prepaid Insurance for 2016 $1,000

Insurance Paid $17,000

Interest Revenue $16,000

Add: Interesr Receivable for 2016 $1,000

Less: Interesr Receivable for 2017 $2,000

Interest received $15,000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13

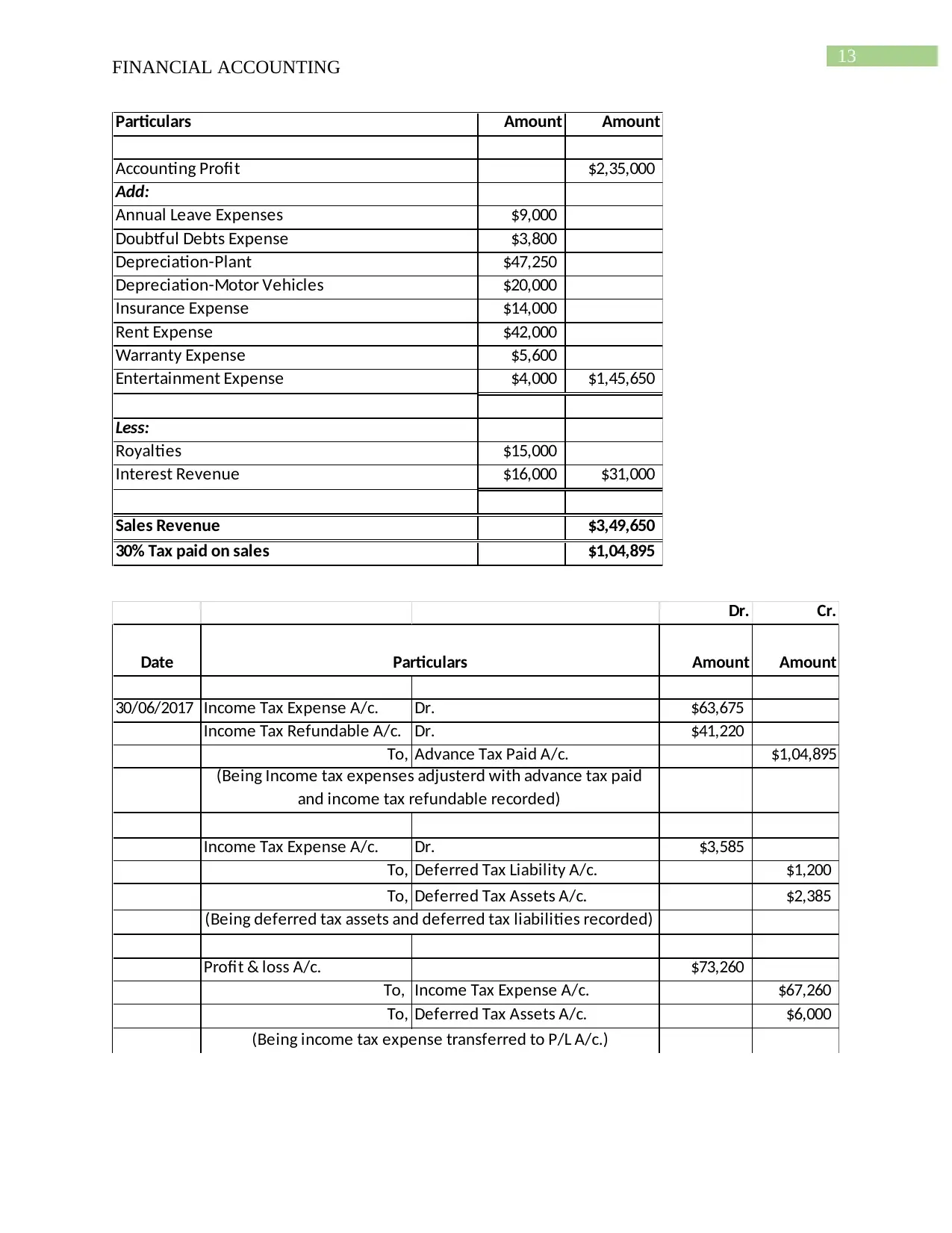

FINANCIAL ACCOUNTING

Particulars Amount Amount

Accounting Profit $2,35,000

Add:

Annual Leave Expenses $9,000

Doubtful Debts Expense $3,800

Depreciation-Plant $47,250

Depreciation-Motor Vehicles $20,000

Insurance Expense $14,000

Rent Expense $42,000

Warranty Expense $5,600

Entertainment Expense $4,000 $1,45,650

Less:

Royalties $15,000

Interest Revenue $16,000 $31,000

Sales Revenue $3,49,650

30% Tax paid on sales $1,04,895

Dr. Cr.

Date Amount Amount

30/06/2017 Income Tax Expense A/c. Dr. $63,675

Income Tax Refundable A/c. Dr. $41,220

To, Advance Tax Paid A/c. $1,04,895

Income Tax Expense A/c. Dr. $3,585

To, Deferred Tax Liability A/c. $1,200

To, Deferred Tax Assets A/c. $2,385

Profit & loss A/c. $73,260

To, Income Tax Expense A/c. $67,260

To, Deferred Tax Assets A/c. $6,000

(Being deferred tax assets and deferred tax liabilities recorded)

Particulars

(Being Income tax expenses adjusterd with advance tax paid

and income tax refundable recorded)

(Being income tax expense transferred to P/L A/c.)

FINANCIAL ACCOUNTING

Particulars Amount Amount

Accounting Profit $2,35,000

Add:

Annual Leave Expenses $9,000

Doubtful Debts Expense $3,800

Depreciation-Plant $47,250

Depreciation-Motor Vehicles $20,000

Insurance Expense $14,000

Rent Expense $42,000

Warranty Expense $5,600

Entertainment Expense $4,000 $1,45,650

Less:

Royalties $15,000

Interest Revenue $16,000 $31,000

Sales Revenue $3,49,650

30% Tax paid on sales $1,04,895

Dr. Cr.

Date Amount Amount

30/06/2017 Income Tax Expense A/c. Dr. $63,675

Income Tax Refundable A/c. Dr. $41,220

To, Advance Tax Paid A/c. $1,04,895

Income Tax Expense A/c. Dr. $3,585

To, Deferred Tax Liability A/c. $1,200

To, Deferred Tax Assets A/c. $2,385

Profit & loss A/c. $73,260

To, Income Tax Expense A/c. $67,260

To, Deferred Tax Assets A/c. $6,000

(Being deferred tax assets and deferred tax liabilities recorded)

Particulars

(Being Income tax expenses adjusterd with advance tax paid

and income tax refundable recorded)

(Being income tax expense transferred to P/L A/c.)

14

FINANCIAL ACCOUNTING

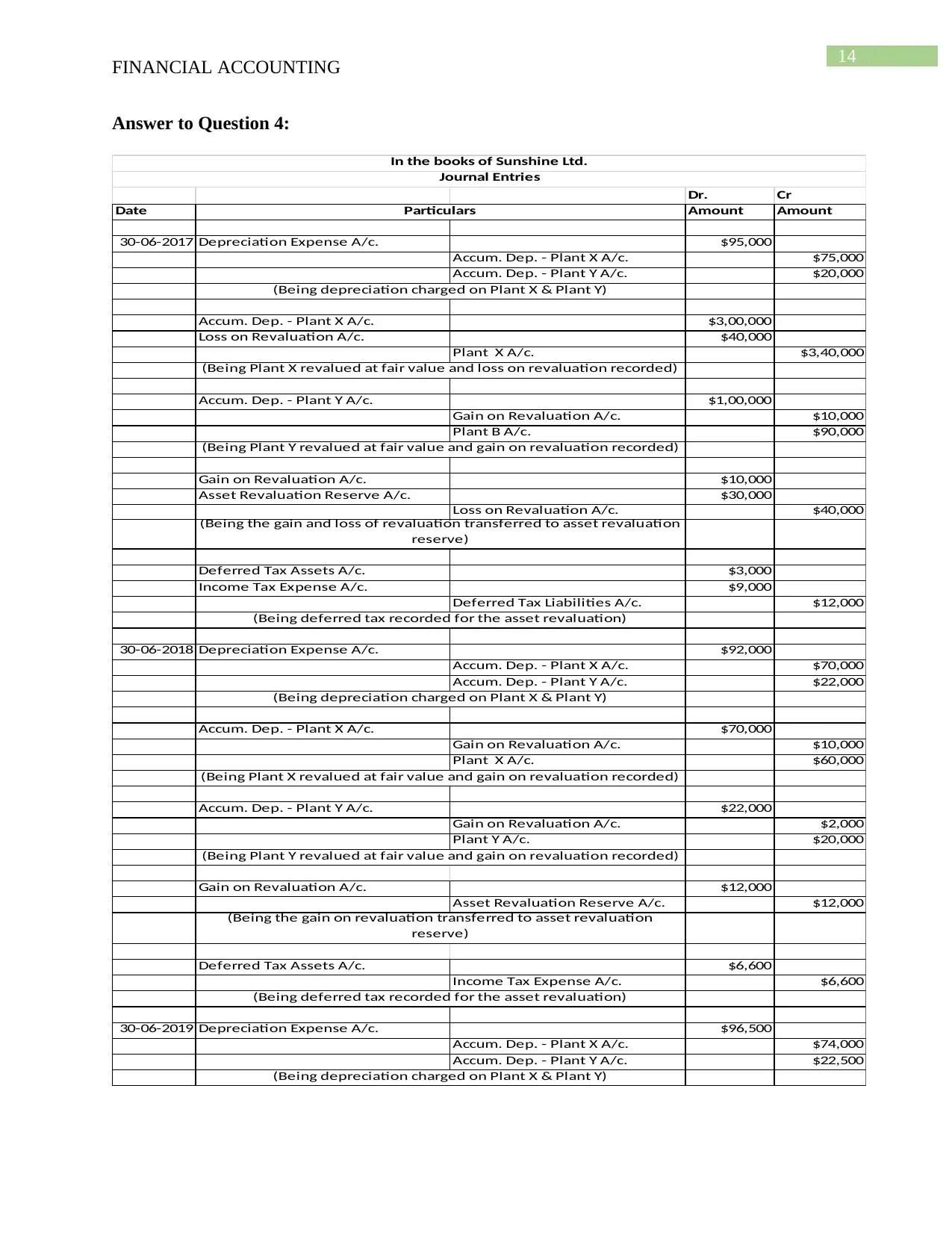

Answer to Question 4:

Dr. Cr

Date Amount Amount

30-06-2017 Depreciation Expense A/c. $95,000

Accum. Dep. - Plant X A/c. $75,000

Accum. Dep. - Plant Y A/c. $20,000

Accum. Dep. - Plant X A/c. $3,00,000

Loss on Revaluation A/c. $40,000

Plant X A/c. $3,40,000

Accum. Dep. - Plant Y A/c. $1,00,000

Gain on Revaluation A/c. $10,000

Plant B A/c. $90,000

Gain on Revaluation A/c. $10,000

Asset Revaluation Reserve A/c. $30,000

Loss on Revaluation A/c. $40,000

Deferred Tax Assets A/c. $3,000

Income Tax Expense A/c. $9,000

Deferred Tax Liabilities A/c. $12,000

30-06-2018 Depreciation Expense A/c. $92,000

Accum. Dep. - Plant X A/c. $70,000

Accum. Dep. - Plant Y A/c. $22,000

Accum. Dep. - Plant X A/c. $70,000

Gain on Revaluation A/c. $10,000

Plant X A/c. $60,000

Accum. Dep. - Plant Y A/c. $22,000

Gain on Revaluation A/c. $2,000

Plant Y A/c. $20,000

Gain on Revaluation A/c. $12,000

Asset Revaluation Reserve A/c. $12,000

Deferred Tax Assets A/c. $6,600

Income Tax Expense A/c. $6,600

30-06-2019 Depreciation Expense A/c. $96,500

Accum. Dep. - Plant X A/c. $74,000

Accum. Dep. - Plant Y A/c. $22,500

(Being depreciation charged on Plant X & Plant Y)

(Being Plant Y revalued at fair value and gain on revaluation recorded)

(Being the gain on revaluation transferred to asset revaluation

reserve)

(Being deferred tax recorded for the asset revaluation)

Journal Entries

(Being deferred tax recorded for the asset revaluation)

(Being depreciation charged on Plant X & Plant Y)

(Being depreciation charged on Plant X & Plant Y)

(Being Plant X revalued at fair value and loss on revaluation recorded)

(Being Plant Y revalued at fair value and gain on revaluation recorded)

(Being the gain and loss of revaluation transferred to asset revaluation

reserve)

(Being Plant X revalued at fair value and gain on revaluation recorded)

Particulars

In the books of Sunshine Ltd.

FINANCIAL ACCOUNTING

Answer to Question 4:

Dr. Cr

Date Amount Amount

30-06-2017 Depreciation Expense A/c. $95,000

Accum. Dep. - Plant X A/c. $75,000

Accum. Dep. - Plant Y A/c. $20,000

Accum. Dep. - Plant X A/c. $3,00,000

Loss on Revaluation A/c. $40,000

Plant X A/c. $3,40,000

Accum. Dep. - Plant Y A/c. $1,00,000

Gain on Revaluation A/c. $10,000

Plant B A/c. $90,000

Gain on Revaluation A/c. $10,000

Asset Revaluation Reserve A/c. $30,000

Loss on Revaluation A/c. $40,000

Deferred Tax Assets A/c. $3,000

Income Tax Expense A/c. $9,000

Deferred Tax Liabilities A/c. $12,000

30-06-2018 Depreciation Expense A/c. $92,000

Accum. Dep. - Plant X A/c. $70,000

Accum. Dep. - Plant Y A/c. $22,000

Accum. Dep. - Plant X A/c. $70,000

Gain on Revaluation A/c. $10,000

Plant X A/c. $60,000

Accum. Dep. - Plant Y A/c. $22,000

Gain on Revaluation A/c. $2,000

Plant Y A/c. $20,000

Gain on Revaluation A/c. $12,000

Asset Revaluation Reserve A/c. $12,000

Deferred Tax Assets A/c. $6,600

Income Tax Expense A/c. $6,600

30-06-2019 Depreciation Expense A/c. $96,500

Accum. Dep. - Plant X A/c. $74,000

Accum. Dep. - Plant Y A/c. $22,500

(Being depreciation charged on Plant X & Plant Y)

(Being Plant Y revalued at fair value and gain on revaluation recorded)

(Being the gain on revaluation transferred to asset revaluation

reserve)

(Being deferred tax recorded for the asset revaluation)

Journal Entries

(Being deferred tax recorded for the asset revaluation)

(Being depreciation charged on Plant X & Plant Y)

(Being depreciation charged on Plant X & Plant Y)

(Being Plant X revalued at fair value and loss on revaluation recorded)

(Being Plant Y revalued at fair value and gain on revaluation recorded)

(Being the gain and loss of revaluation transferred to asset revaluation

reserve)

(Being Plant X revalued at fair value and gain on revaluation recorded)

Particulars

In the books of Sunshine Ltd.

15

FINANCIAL ACCOUNTING

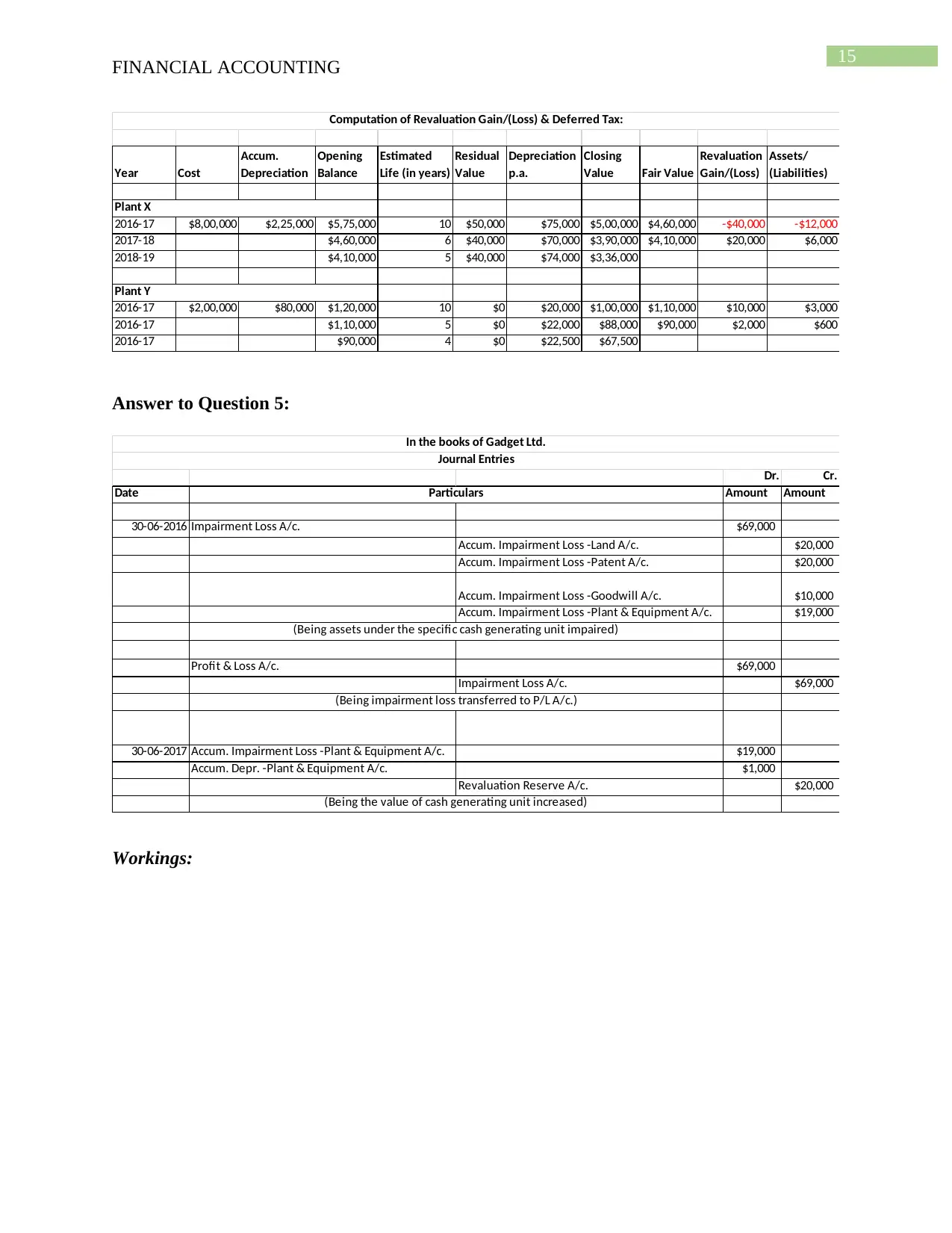

Year Cost

Accum.

Depreciation

Opening

Balance

Estimated

Life (in years)

Residual

Value

Depreciation

p.a.

Closing

Value Fair Value

Revaluation

Gain/(Loss)

Deferred Tax

Assets/

(Liabilities)

2016-17 $8,00,000 $2,25,000 $5,75,000 10 $50,000 $75,000 $5,00,000 $4,60,000 -$40,000 -$12,000

2017-18 $4,60,000 6 $40,000 $70,000 $3,90,000 $4,10,000 $20,000 $6,000

2018-19 $4,10,000 5 $40,000 $74,000 $3,36,000

2016-17 $2,00,000 $80,000 $1,20,000 10 $0 $20,000 $1,00,000 $1,10,000 $10,000 $3,000

2016-17 $1,10,000 5 $0 $22,000 $88,000 $90,000 $2,000 $600

2016-17 $90,000 4 $0 $22,500 $67,500

Plant X

Plant Y

Computation of Revaluation Gain/(Loss) & Deferred Tax:

Answer to Question 5:

Dr. Cr.

Date Amount Amount

30-06-2016 Impairment Loss A/c. $69,000

Accum. Impairment Loss -Land A/c. $20,000

Accum. Impairment Loss -Patent A/c. $20,000

Accum. Impairment Loss -Goodwill A/c. $10,000

Accum. Impairment Loss -Plant & Equipment A/c. $19,000

Profit & Loss A/c. $69,000

Impairment Loss A/c. $69,000

30-06-2017 Accum. Impairment Loss -Plant & Equipment A/c. $19,000

Accum. Depr. -Plant & Equipment A/c. $1,000

Revaluation Reserve A/c. $20,000

In the books of Gadget Ltd.

Journal Entries

Particulars

(Being assets under the specific cash generating unit impaired)

(Being impairment loss transferred to P/L A/c.)

(Being the value of cash generating unit increased)

Workings:

FINANCIAL ACCOUNTING

Year Cost

Accum.

Depreciation

Opening

Balance

Estimated

Life (in years)

Residual

Value

Depreciation

p.a.

Closing

Value Fair Value

Revaluation

Gain/(Loss)

Deferred Tax

Assets/

(Liabilities)

2016-17 $8,00,000 $2,25,000 $5,75,000 10 $50,000 $75,000 $5,00,000 $4,60,000 -$40,000 -$12,000

2017-18 $4,60,000 6 $40,000 $70,000 $3,90,000 $4,10,000 $20,000 $6,000

2018-19 $4,10,000 5 $40,000 $74,000 $3,36,000

2016-17 $2,00,000 $80,000 $1,20,000 10 $0 $20,000 $1,00,000 $1,10,000 $10,000 $3,000

2016-17 $1,10,000 5 $0 $22,000 $88,000 $90,000 $2,000 $600

2016-17 $90,000 4 $0 $22,500 $67,500

Plant X

Plant Y

Computation of Revaluation Gain/(Loss) & Deferred Tax:

Answer to Question 5:

Dr. Cr.

Date Amount Amount

30-06-2016 Impairment Loss A/c. $69,000

Accum. Impairment Loss -Land A/c. $20,000

Accum. Impairment Loss -Patent A/c. $20,000

Accum. Impairment Loss -Goodwill A/c. $10,000

Accum. Impairment Loss -Plant & Equipment A/c. $19,000

Profit & Loss A/c. $69,000

Impairment Loss A/c. $69,000

30-06-2017 Accum. Impairment Loss -Plant & Equipment A/c. $19,000

Accum. Depr. -Plant & Equipment A/c. $1,000

Revaluation Reserve A/c. $20,000

In the books of Gadget Ltd.

Journal Entries

Particulars

(Being assets under the specific cash generating unit impaired)

(Being impairment loss transferred to P/L A/c.)

(Being the value of cash generating unit increased)

Workings:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

16

FINANCIAL ACCOUNTING

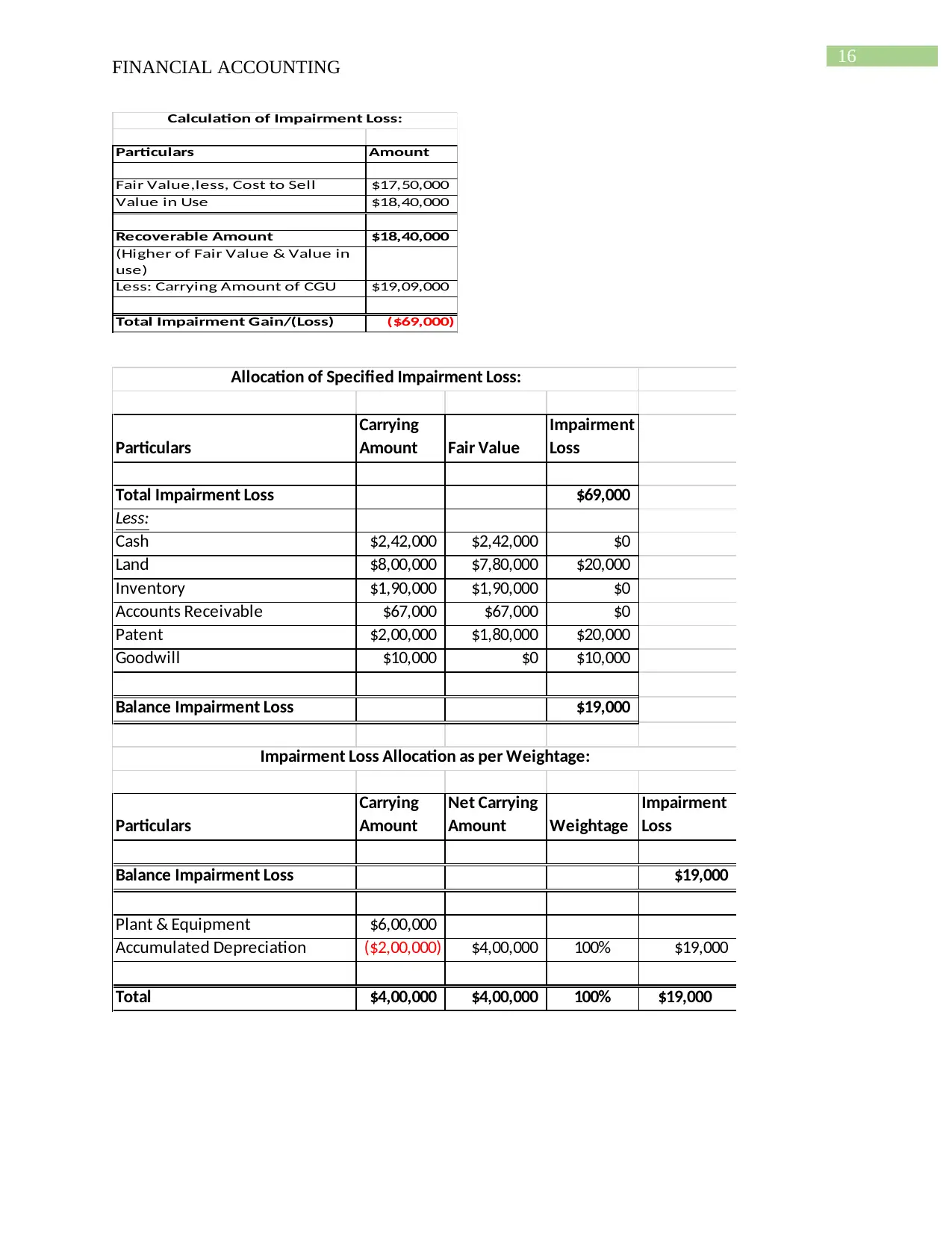

Particulars Amount

Fair Value,less, Cost to Sell $17,50,000

Value in Use $18,40,000

Recoverable Amount $18,40,000

(Higher of Fair Value & Value in

use)

Less: Carrying Amount of CGU $19,09,000

Total Impairment Gain/(Loss) ($69,000)

Calculation of Impairment Loss:

Particulars

Carrying

Amount Fair Value

Impairment

Loss

Total Impairment Loss $69,000

Less:

Cash $2,42,000 $2,42,000 $0

Land $8,00,000 $7,80,000 $20,000

Inventory $1,90,000 $1,90,000 $0

Accounts Receivable $67,000 $67,000 $0

Patent $2,00,000 $1,80,000 $20,000

Goodwill $10,000 $0 $10,000

Balance Impairment Loss $19,000

Particulars

Carrying

Amount

Net Carrying

Amount Weightage

Impairment

Loss

Balance Impairment Loss $19,000

Plant & Equipment $6,00,000

Accumulated Depreciation ($2,00,000) $4,00,000 100% $19,000

Total $4,00,000 $4,00,000 100% $19,000

Impairment Loss Allocation as per Weightage:

Allocation of Specified Impairment Loss:

FINANCIAL ACCOUNTING

Particulars Amount

Fair Value,less, Cost to Sell $17,50,000

Value in Use $18,40,000

Recoverable Amount $18,40,000

(Higher of Fair Value & Value in

use)

Less: Carrying Amount of CGU $19,09,000

Total Impairment Gain/(Loss) ($69,000)

Calculation of Impairment Loss:

Particulars

Carrying

Amount Fair Value

Impairment

Loss

Total Impairment Loss $69,000

Less:

Cash $2,42,000 $2,42,000 $0

Land $8,00,000 $7,80,000 $20,000

Inventory $1,90,000 $1,90,000 $0

Accounts Receivable $67,000 $67,000 $0

Patent $2,00,000 $1,80,000 $20,000

Goodwill $10,000 $0 $10,000

Balance Impairment Loss $19,000

Particulars

Carrying

Amount

Net Carrying

Amount Weightage

Impairment

Loss

Balance Impairment Loss $19,000

Plant & Equipment $6,00,000

Accumulated Depreciation ($2,00,000) $4,00,000 100% $19,000

Total $4,00,000 $4,00,000 100% $19,000

Impairment Loss Allocation as per Weightage:

Allocation of Specified Impairment Loss:

17

FINANCIAL ACCOUNTING

Reference list and Bibliography:

Abernathy, J. L., Beyer, B., Masli, A., & Stefaniak, C. M. (2015). How the source of audit

committee accounting expertise influences financial reporting timeliness. Current Issues

in Auditing, 9(1), P1-P9.

Bach, L. T., & Hang, N. T. (2016). Accounting information quality in emerging markets:

Conservatism in financial reporting of Vietnamese firms in the context of international

economic integration. International Journal of Economics and Financial Issues, 6(6S).

Barth, M. E. (2015). Commentary on Prospects for Global Financial Reporting. Accounting

Perspectives, 14(3), 154-167.

Beatty, A., & Liao, S. (2014). Financial accounting in the banking industry: A review of the

empirical literature. Journal of Accounting and Economics, 58(2-3), 339-383.

Brausch, J. (2017). The path forward in accounting: Lev and Gu propose a new vision that

begins with simplified accounting regulations. Strategic Finance, 98(9), 17-18.

Brown, R., & Jones, M. (2015). Mapping and exploring the topography of contemporary

financial accounting research. The British Accounting Review, 47(3), 237-261.

Bublitz, B., Philipich, K., & Blatz, R. (2015). An example of the use of research methods and

findings as an experiential learning exercise in an accounting theory course. Journal of

Instructional Pedagogies, 16.

Bushman, R. M. (2014). Thoughts on financial accounting and the banking industry. Journal of

Accounting and Economics, 58(2-3), 384-395.

FINANCIAL ACCOUNTING

Reference list and Bibliography:

Abernathy, J. L., Beyer, B., Masli, A., & Stefaniak, C. M. (2015). How the source of audit

committee accounting expertise influences financial reporting timeliness. Current Issues

in Auditing, 9(1), P1-P9.

Bach, L. T., & Hang, N. T. (2016). Accounting information quality in emerging markets:

Conservatism in financial reporting of Vietnamese firms in the context of international

economic integration. International Journal of Economics and Financial Issues, 6(6S).

Barth, M. E. (2015). Commentary on Prospects for Global Financial Reporting. Accounting

Perspectives, 14(3), 154-167.

Beatty, A., & Liao, S. (2014). Financial accounting in the banking industry: A review of the

empirical literature. Journal of Accounting and Economics, 58(2-3), 339-383.

Brausch, J. (2017). The path forward in accounting: Lev and Gu propose a new vision that

begins with simplified accounting regulations. Strategic Finance, 98(9), 17-18.

Brown, R., & Jones, M. (2015). Mapping and exploring the topography of contemporary

financial accounting research. The British Accounting Review, 47(3), 237-261.

Bublitz, B., Philipich, K., & Blatz, R. (2015). An example of the use of research methods and

findings as an experiential learning exercise in an accounting theory course. Journal of

Instructional Pedagogies, 16.

Bushman, R. M. (2014). Thoughts on financial accounting and the banking industry. Journal of

Accounting and Economics, 58(2-3), 384-395.

18

FINANCIAL ACCOUNTING

Caria, A. A., & Rodrigues, L. L. (2014). The evolution of financial accounting in Portugal since

the 1960s: A new institutional economics perspective. Accounting History, 19(1-2), 227-

254.

Crawley, M., & Wahlen, J. (2014). Analytics in empirical/archival financial accounting

research. Business Horizons, 57(5), 583-593.

Dutta, S., & Patatoukas, P. N. (2016). Identifying Conditional Conservatism in Financial

Accounting Data: Theory and Evidence. The Accounting Review, 92(4), 191-216.

Henderson, S., Peirson, G., Herbohn, K., & Howieson, B. (2015). Issues in financial accounting.

Pearson Higher Education AU.

Hoggett, J., Edwards, L., Medlin, J., Chalmers, K., Hellmann, A., Beattie, C., & Maxfield, J.

(2014). Financial accounting.

Horton, J. (2018). Advanced Financial Accounting and Reporting: Theory, Practice and

Evidence. Routledge.

Jiang, J., Wang, I. Y., & Xie, Y. (2015). Does it matter who serves on the Financial Accounting

Standards Board? Bob Herz’s resignation and fair value accounting for loans. Review of

Accounting Studies, 20(1), 371-394.

Klychova, G. S., Fakhretdinova, E. N., Klychova, A. S., & Antonova, N. V. (2015).

Development of accounting and financial reporting for small and medium-sized

businesses in accordance with international financial reporting standards. Asian Social

Science, 11(11), 318.

FINANCIAL ACCOUNTING

Caria, A. A., & Rodrigues, L. L. (2014). The evolution of financial accounting in Portugal since

the 1960s: A new institutional economics perspective. Accounting History, 19(1-2), 227-

254.

Crawley, M., & Wahlen, J. (2014). Analytics in empirical/archival financial accounting

research. Business Horizons, 57(5), 583-593.

Dutta, S., & Patatoukas, P. N. (2016). Identifying Conditional Conservatism in Financial

Accounting Data: Theory and Evidence. The Accounting Review, 92(4), 191-216.

Henderson, S., Peirson, G., Herbohn, K., & Howieson, B. (2015). Issues in financial accounting.

Pearson Higher Education AU.

Hoggett, J., Edwards, L., Medlin, J., Chalmers, K., Hellmann, A., Beattie, C., & Maxfield, J.

(2014). Financial accounting.

Horton, J. (2018). Advanced Financial Accounting and Reporting: Theory, Practice and

Evidence. Routledge.

Jiang, J., Wang, I. Y., & Xie, Y. (2015). Does it matter who serves on the Financial Accounting

Standards Board? Bob Herz’s resignation and fair value accounting for loans. Review of

Accounting Studies, 20(1), 371-394.

Klychova, G. S., Fakhretdinova, E. N., Klychova, A. S., & Antonova, N. V. (2015).

Development of accounting and financial reporting for small and medium-sized

businesses in accordance with international financial reporting standards. Asian Social

Science, 11(11), 318.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

19

FINANCIAL ACCOUNTING

Macve, R. (2015). A Conceptual Framework for Financial Accounting and Reporting:

Vision. Tool, Or Threat.

Macve, R. (2015). A Conceptual Framework for Financial Accounting and Reporting: Vision,

Tool, Or Threat?. Routledge.

May, R. A. (2017). An Investigation of Financial Accounting Statements and Reporting

Techniques (Doctoral dissertation, University of Mississippi).

Narayanaswamy, R. (2017). Financial accounting: a managerial perspective. PHI Learning Pvt.

Ltd..

Nilsson, F., & Stockenstrand, A. K. (2016). Financial Accounting and Management Control.

Springer International Publishing: Imprint: Springer,.

Reeve, J. M., Warren, C. S., Duchac, J. E., & Wang, W. (2014). Principles of financial

accounting with conceptual emphasis on IFRS. Cengage Learning Asia Pte Limited.

Rutherford, B. A. (2016). Articulating accounting principles: Classical accounting theory as the

pursuit of “explanation by embodiment”. Journal of Applied Accounting Research, 17(2),

118-135

Salako, M. A., & Yusuf, S. A. (2016). Cost accounting: A pivotal factor of entrepreneurial

success.

Schipper, K., Francis, J., & Weil, R. (2017). Financial Accounting: Introduction to Concepts,

Methods and Uses. Cengage Learning.

Scott, W. R. (2015). Financial accounting theory (Vol. 2, No. 0, p. 0). Prentice Hall.

FINANCIAL ACCOUNTING

Macve, R. (2015). A Conceptual Framework for Financial Accounting and Reporting:

Vision. Tool, Or Threat.

Macve, R. (2015). A Conceptual Framework for Financial Accounting and Reporting: Vision,

Tool, Or Threat?. Routledge.

May, R. A. (2017). An Investigation of Financial Accounting Statements and Reporting

Techniques (Doctoral dissertation, University of Mississippi).

Narayanaswamy, R. (2017). Financial accounting: a managerial perspective. PHI Learning Pvt.

Ltd..

Nilsson, F., & Stockenstrand, A. K. (2016). Financial Accounting and Management Control.

Springer International Publishing: Imprint: Springer,.

Reeve, J. M., Warren, C. S., Duchac, J. E., & Wang, W. (2014). Principles of financial

accounting with conceptual emphasis on IFRS. Cengage Learning Asia Pte Limited.

Rutherford, B. A. (2016). Articulating accounting principles: Classical accounting theory as the

pursuit of “explanation by embodiment”. Journal of Applied Accounting Research, 17(2),

118-135

Salako, M. A., & Yusuf, S. A. (2016). Cost accounting: A pivotal factor of entrepreneurial

success.

Schipper, K., Francis, J., & Weil, R. (2017). Financial Accounting: Introduction to Concepts,

Methods and Uses. Cengage Learning.

Scott, W. R. (2015). Financial accounting theory (Vol. 2, No. 0, p. 0). Prentice Hall.

20

FINANCIAL ACCOUNTING

Trucco, S. (2015). Premises for the Convergence of Financial Accounting and Management

Accounting. In Financial Accounting (pp. 41-64). Springer, Cham.

Tschopp, D., & Huefner, R. J. (2015). Comparing the Evolution of CSR Reporting to that of

Financial Reporting. Journal of Business Ethics, 127(3), 565-577.

Warren, C. S., & Jones, J. (2018). Corporate financial accounting. Cengage Learning.

Wild, J. (2015). Financial accounting fundamentals. McGraw-Hill Higher Education.

FINANCIAL ACCOUNTING

Trucco, S. (2015). Premises for the Convergence of Financial Accounting and Management

Accounting. In Financial Accounting (pp. 41-64). Springer, Cham.

Tschopp, D., & Huefner, R. J. (2015). Comparing the Evolution of CSR Reporting to that of

Financial Reporting. Journal of Business Ethics, 127(3), 565-577.

Warren, C. S., & Jones, J. (2018). Corporate financial accounting. Cengage Learning.

Wild, J. (2015). Financial accounting fundamentals. McGraw-Hill Higher Education.

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.