Calculating Net Income for Tax Purposes: EASI's 2018 Business Taxation

VerifiedAdded on 2023/04/23

|16

|2918

|496

Homework Assignment

AI Summary

This assignment focuses on calculating the net income for tax purposes for Eldridge Asset Sales Inc. (EASI) for the fiscal year ended December 31, 2018, under the provisions of the Income Tax Act. The solution begins with EASI's unaudited income statement, detailing sales, cost of goods sold, and various expenses. The assignment requires a series of adjustments to the net income for accounting purposes, considering items such as deferred revenue, inventory reserves, warranty provisions, charitable donations, golf club membership fees, management bonuses, and various other expenses. The solution meticulously analyzes each item, determining whether it is deductible or requires an add-back, based on Canadian tax regulations. It also addresses capital cost allowance (CCA) calculations for different asset classes, including buildings, office furniture, trucks, passenger vehicles, leasehold improvements, and manufacturing equipment. The final answer provides the minimum net income for tax purposes, demonstrating a clear understanding of tax principles and their application to a business context. The solution also includes detailed working papers for each adjustment.

Running head: BUSINESS TAXATION IN CANADA 1

Topic: Business Taxation in Canada

By (Name of Student)

(Institutional Affiliation)

(Course Code)

(Date of Submission)

Topic: Business Taxation in Canada

By (Name of Student)

(Institutional Affiliation)

(Course Code)

(Date of Submission)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BUSINESS TAXATION IN CANADA 2

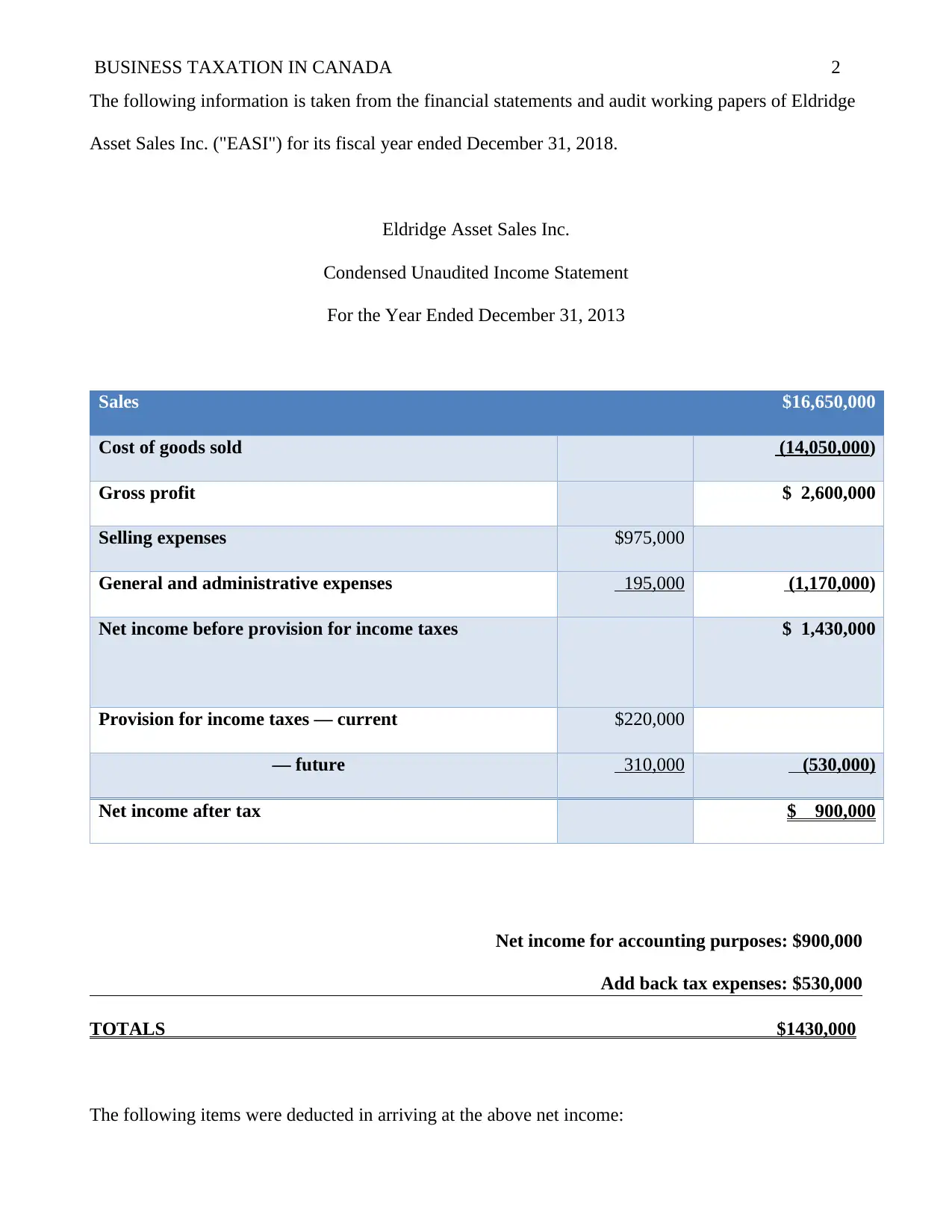

The following information is taken from the financial statements and audit working papers of Eldridge

Asset Sales Inc. ("EASI") for its fiscal year ended December 31, 2018.

Eldridge Asset Sales Inc.

Condensed Unaudited Income Statement

For the Year Ended December 31, 2013

Sales $16,650,000

Cost of goods sold (14,050,000)

Gross profit $ 2,600,000

Selling expenses $975,000

General and administrative expenses 195,000 (1,170,000)

Net income before provision for income taxes $ 1,430,000

Provision for income taxes — current $220,000

— future 310,000 (530,000)

Net income after tax $ 900,000

Net income for accounting purposes: $900,000

Add back tax expenses: $530,000

TOTALS $1430,000

The following items were deducted in arriving at the above net income:

The following information is taken from the financial statements and audit working papers of Eldridge

Asset Sales Inc. ("EASI") for its fiscal year ended December 31, 2018.

Eldridge Asset Sales Inc.

Condensed Unaudited Income Statement

For the Year Ended December 31, 2013

Sales $16,650,000

Cost of goods sold (14,050,000)

Gross profit $ 2,600,000

Selling expenses $975,000

General and administrative expenses 195,000 (1,170,000)

Net income before provision for income taxes $ 1,430,000

Provision for income taxes — current $220,000

— future 310,000 (530,000)

Net income after tax $ 900,000

Net income for accounting purposes: $900,000

Add back tax expenses: $530,000

TOTALS $1430,000

The following items were deducted in arriving at the above net income:

BUSINESS TAXATION IN CANADA 3

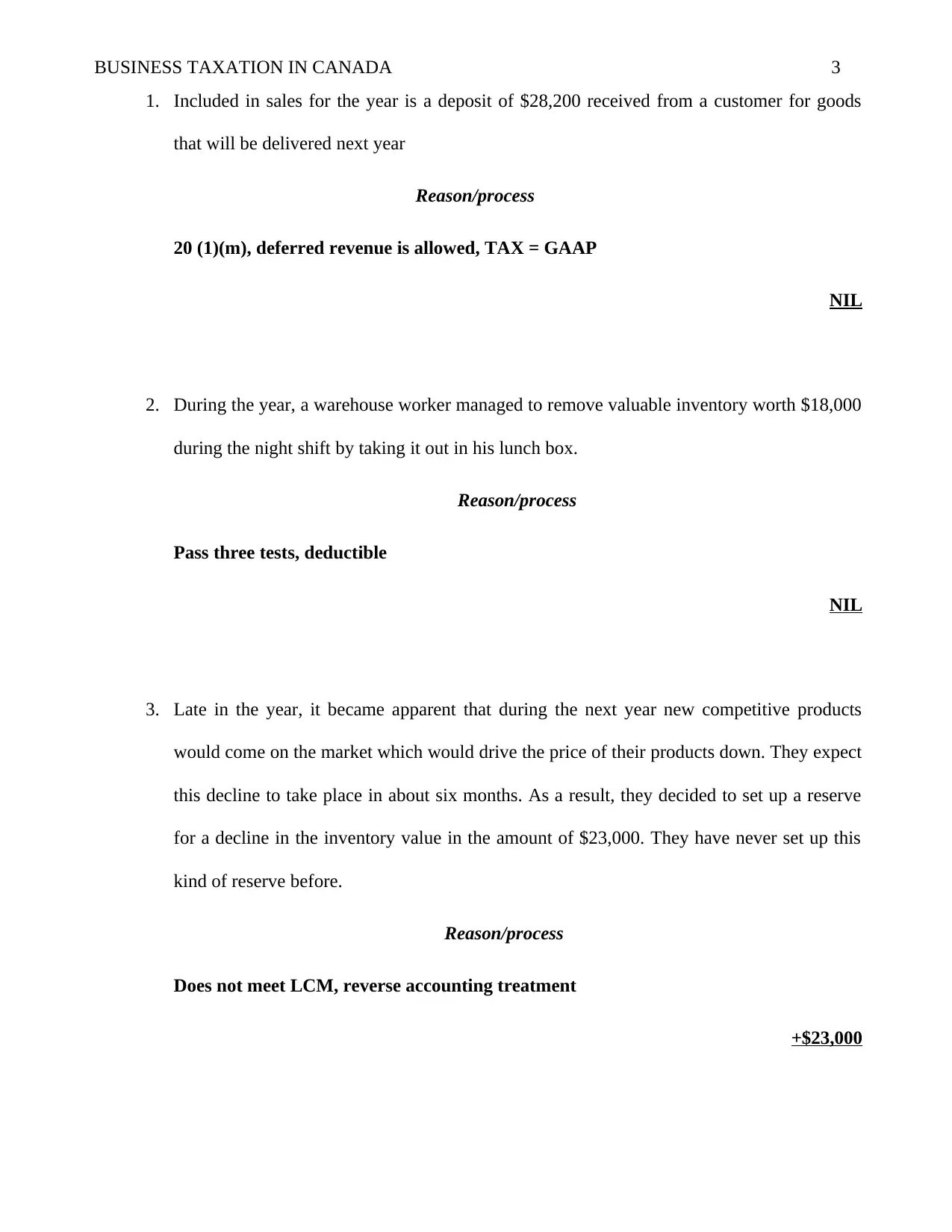

1. Included in sales for the year is a deposit of $28,200 received from a customer for goods

that will be delivered next year

Reason/process

20 (1)(m), deferred revenue is allowed, TAX = GAAP

NIL

2. During the year, a warehouse worker managed to remove valuable inventory worth $18,000

during the night shift by taking it out in his lunch box.

Reason/process

Pass three tests, deductible

NIL

3. Late in the year, it became apparent that during the next year new competitive products

would come on the market which would drive the price of their products down. They expect

this decline to take place in about six months. As a result, they decided to set up a reserve

for a decline in the inventory value in the amount of $23,000. They have never set up this

kind of reserve before.

Reason/process

Does not meet LCM, reverse accounting treatment

+$23,000

1. Included in sales for the year is a deposit of $28,200 received from a customer for goods

that will be delivered next year

Reason/process

20 (1)(m), deferred revenue is allowed, TAX = GAAP

NIL

2. During the year, a warehouse worker managed to remove valuable inventory worth $18,000

during the night shift by taking it out in his lunch box.

Reason/process

Pass three tests, deductible

NIL

3. Late in the year, it became apparent that during the next year new competitive products

would come on the market which would drive the price of their products down. They expect

this decline to take place in about six months. As a result, they decided to set up a reserve

for a decline in the inventory value in the amount of $23,000. They have never set up this

kind of reserve before.

Reason/process

Does not meet LCM, reverse accounting treatment

+$23,000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

BUSINESS TAXATION IN CANADA 4

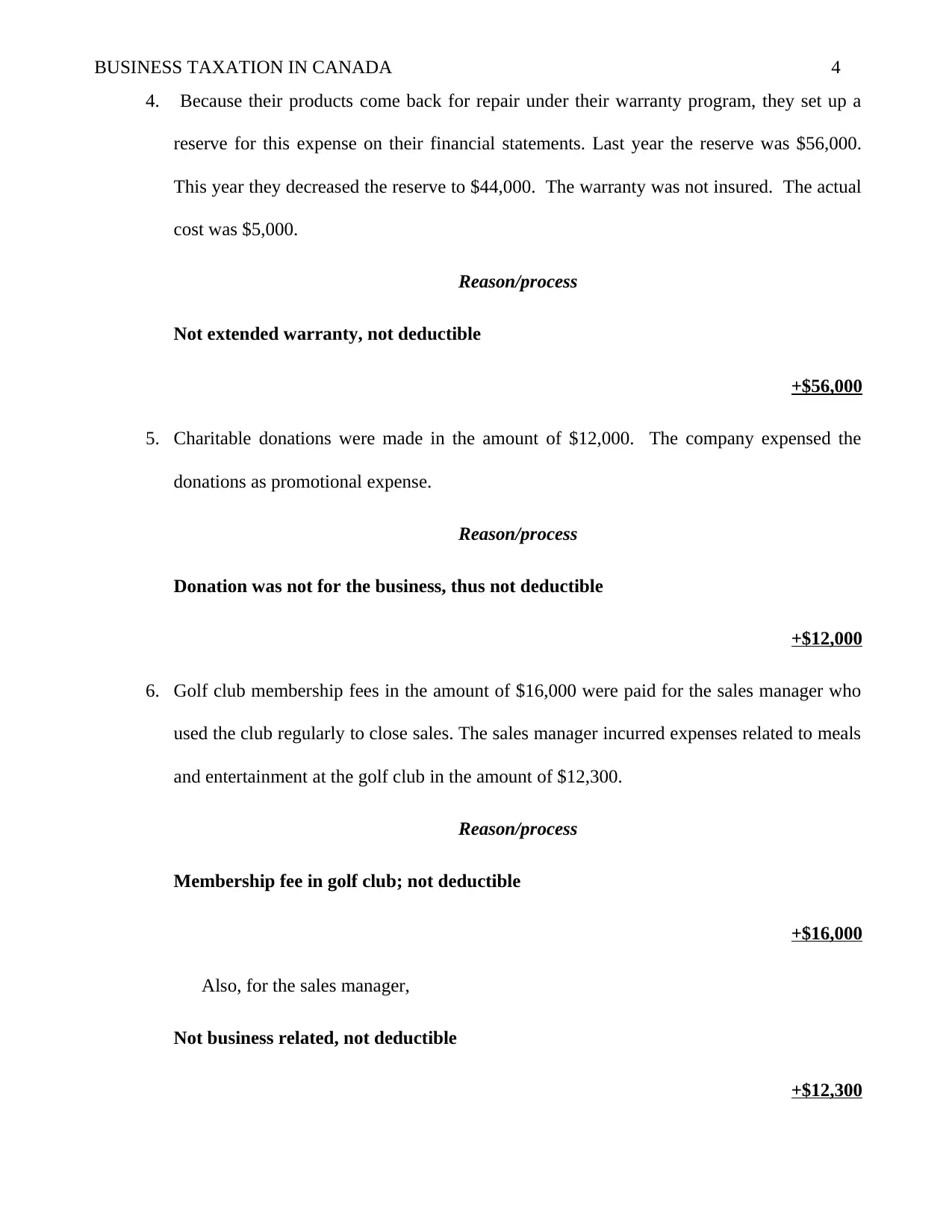

4. Because their products come back for repair under their warranty program, they set up a

reserve for this expense on their financial statements. Last year the reserve was $56,000.

This year they decreased the reserve to $44,000. The warranty was not insured. The actual

cost was $5,000.

Reason/process

Not extended warranty, not deductible

+$56,000

5. Charitable donations were made in the amount of $12,000. The company expensed the

donations as promotional expense.

Reason/process

Donation was not for the business, thus not deductible

+$12,000

6. Golf club membership fees in the amount of $16,000 were paid for the sales manager who

used the club regularly to close sales. The sales manager incurred expenses related to meals

and entertainment at the golf club in the amount of $12,300.

Reason/process

Membership fee in golf club; not deductible

+$16,000

Also, for the sales manager,

Not business related, not deductible

+$12,300

4. Because their products come back for repair under their warranty program, they set up a

reserve for this expense on their financial statements. Last year the reserve was $56,000.

This year they decreased the reserve to $44,000. The warranty was not insured. The actual

cost was $5,000.

Reason/process

Not extended warranty, not deductible

+$56,000

5. Charitable donations were made in the amount of $12,000. The company expensed the

donations as promotional expense.

Reason/process

Donation was not for the business, thus not deductible

+$12,000

6. Golf club membership fees in the amount of $16,000 were paid for the sales manager who

used the club regularly to close sales. The sales manager incurred expenses related to meals

and entertainment at the golf club in the amount of $12,300.

Reason/process

Membership fee in golf club; not deductible

+$16,000

Also, for the sales manager,

Not business related, not deductible

+$12,300

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BUSINESS TAXATION IN CANADA 5

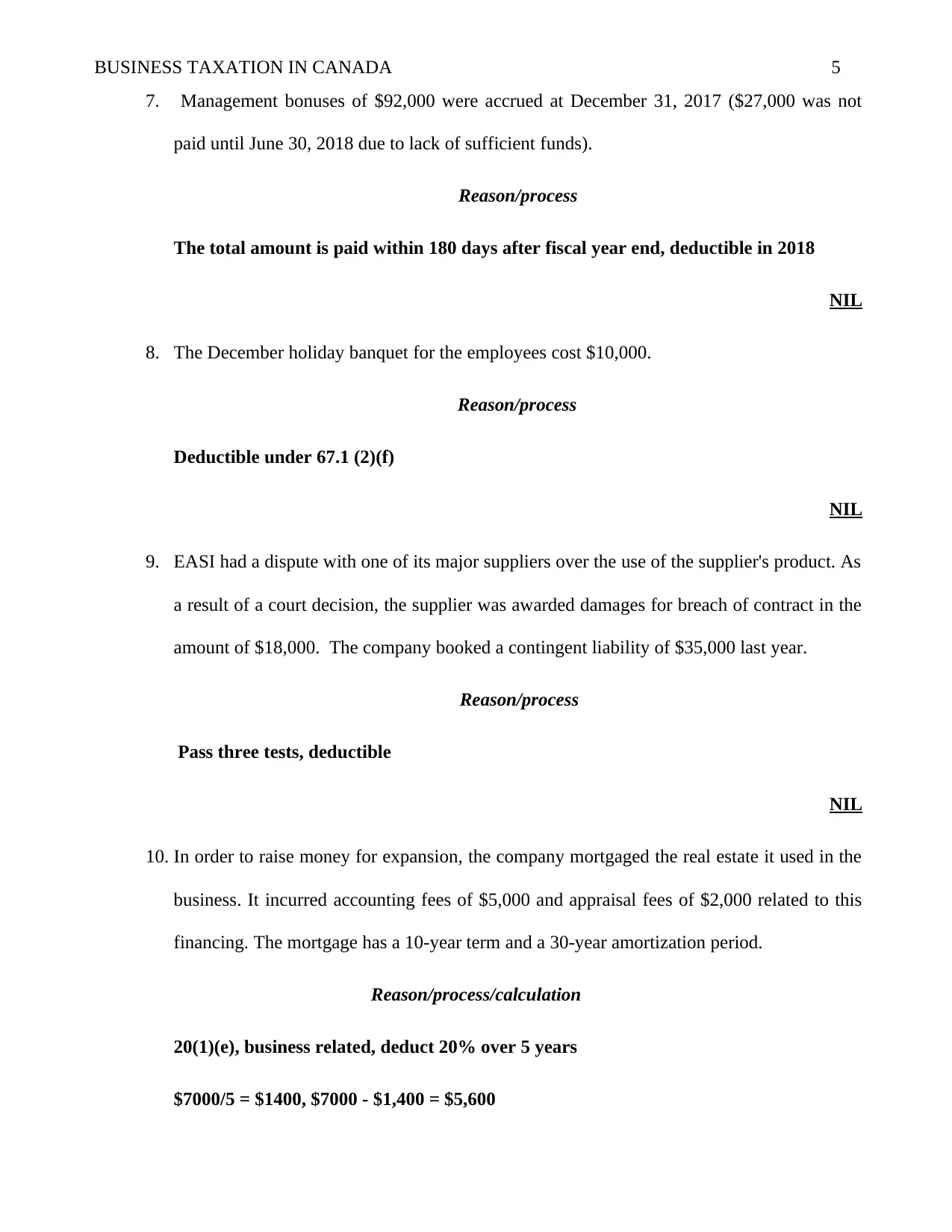

7. Management bonuses of $92,000 were accrued at December 31, 2017 ($27,000 was not

paid until June 30, 2018 due to lack of sufficient funds).

Reason/process

The total amount is paid within 180 days after fiscal year end, deductible in 2018

NIL

8. The December holiday banquet for the employees cost $10,000.

Reason/process

Deductible under 67.1 (2)(f)

NIL

9. EASI had a dispute with one of its major suppliers over the use of the supplier's product. As

a result of a court decision, the supplier was awarded damages for breach of contract in the

amount of $18,000. The company booked a contingent liability of $35,000 last year.

Reason/process

Pass three tests, deductible

NIL

10. In order to raise money for expansion, the company mortgaged the real estate it used in the

business. It incurred accounting fees of $5,000 and appraisal fees of $2,000 related to this

financing. The mortgage has a 10-year term and a 30-year amortization period.

Reason/process/calculation

20(1)(e), business related, deduct 20% over 5 years

$7000/5 = $1400, $7000 - $1,400 = $5,600

7. Management bonuses of $92,000 were accrued at December 31, 2017 ($27,000 was not

paid until June 30, 2018 due to lack of sufficient funds).

Reason/process

The total amount is paid within 180 days after fiscal year end, deductible in 2018

NIL

8. The December holiday banquet for the employees cost $10,000.

Reason/process

Deductible under 67.1 (2)(f)

NIL

9. EASI had a dispute with one of its major suppliers over the use of the supplier's product. As

a result of a court decision, the supplier was awarded damages for breach of contract in the

amount of $18,000. The company booked a contingent liability of $35,000 last year.

Reason/process

Pass three tests, deductible

NIL

10. In order to raise money for expansion, the company mortgaged the real estate it used in the

business. It incurred accounting fees of $5,000 and appraisal fees of $2,000 related to this

financing. The mortgage has a 10-year term and a 30-year amortization period.

Reason/process/calculation

20(1)(e), business related, deduct 20% over 5 years

$7000/5 = $1400, $7000 - $1,400 = $5,600

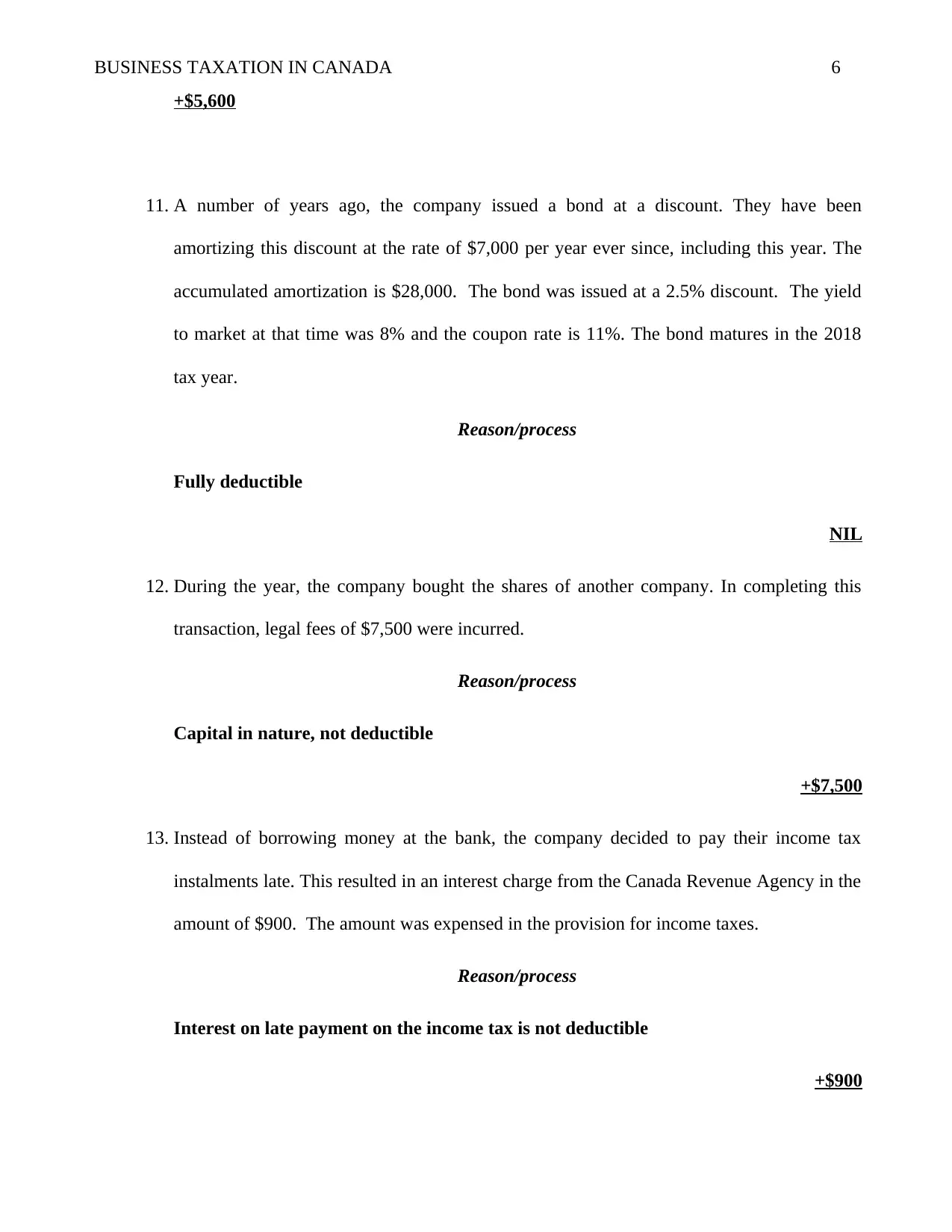

BUSINESS TAXATION IN CANADA 6

+$5,600

11. A number of years ago, the company issued a bond at a discount. They have been

amortizing this discount at the rate of $7,000 per year ever since, including this year. The

accumulated amortization is $28,000. The bond was issued at a 2.5% discount. The yield

to market at that time was 8% and the coupon rate is 11%. The bond matures in the 2018

tax year.

Reason/process

Fully deductible

NIL

12. During the year, the company bought the shares of another company. In completing this

transaction, legal fees of $7,500 were incurred.

Reason/process

Capital in nature, not deductible

+$7,500

13. Instead of borrowing money at the bank, the company decided to pay their income tax

instalments late. This resulted in an interest charge from the Canada Revenue Agency in the

amount of $900. The amount was expensed in the provision for income taxes.

Reason/process

Interest on late payment on the income tax is not deductible

+$900

+$5,600

11. A number of years ago, the company issued a bond at a discount. They have been

amortizing this discount at the rate of $7,000 per year ever since, including this year. The

accumulated amortization is $28,000. The bond was issued at a 2.5% discount. The yield

to market at that time was 8% and the coupon rate is 11%. The bond matures in the 2018

tax year.

Reason/process

Fully deductible

NIL

12. During the year, the company bought the shares of another company. In completing this

transaction, legal fees of $7,500 were incurred.

Reason/process

Capital in nature, not deductible

+$7,500

13. Instead of borrowing money at the bank, the company decided to pay their income tax

instalments late. This resulted in an interest charge from the Canada Revenue Agency in the

amount of $900. The amount was expensed in the provision for income taxes.

Reason/process

Interest on late payment on the income tax is not deductible

+$900

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

BUSINESS TAXATION IN CANADA 7

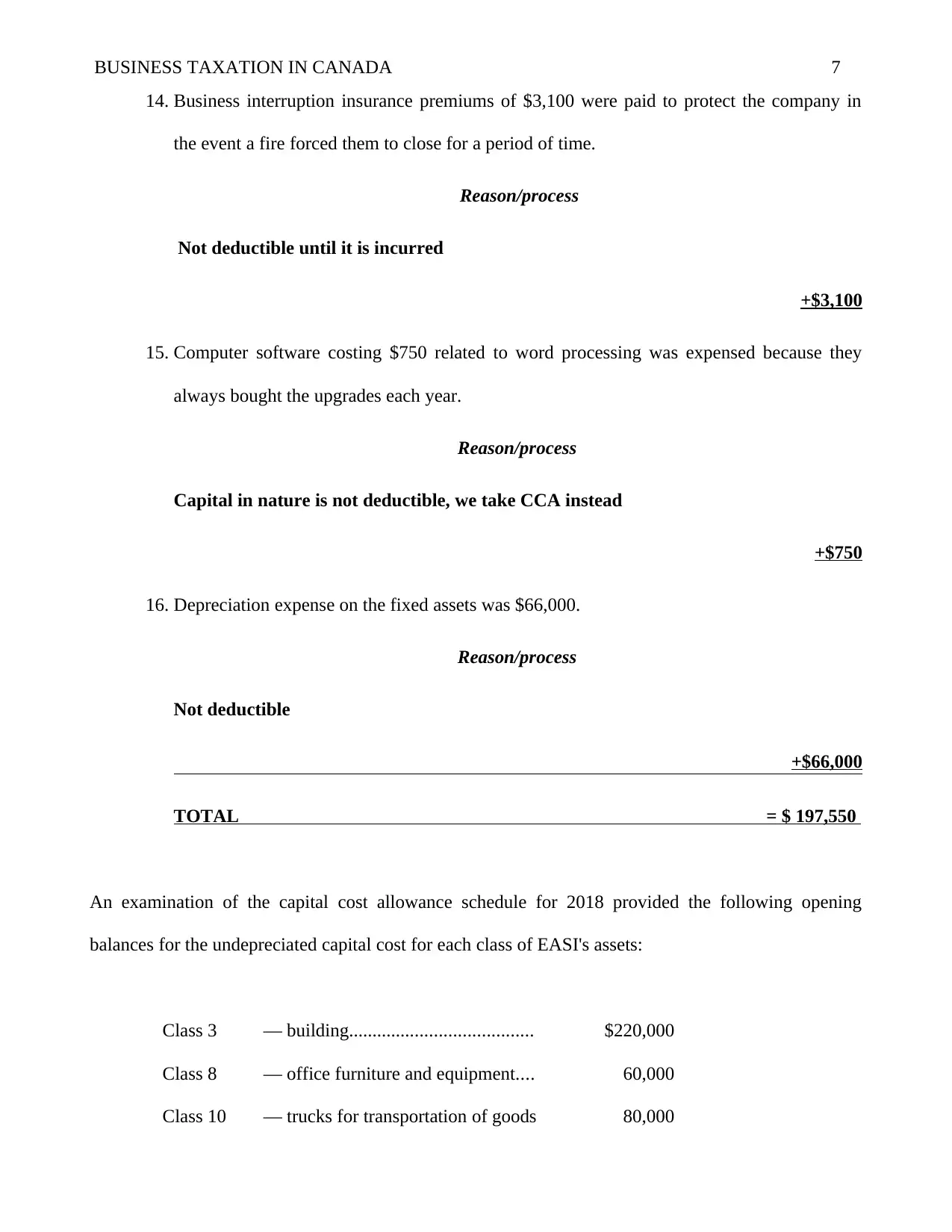

14. Business interruption insurance premiums of $3,100 were paid to protect the company in

the event a fire forced them to close for a period of time.

Reason/process

Not deductible until it is incurred

+$3,100

15. Computer software costing $750 related to word processing was expensed because they

always bought the upgrades each year.

Reason/process

Capital in nature is not deductible, we take CCA instead

+$750

16. Depreciation expense on the fixed assets was $66,000.

Reason/process

Not deductible

+$66,000

TOTAL = $ 197,550

An examination of the capital cost allowance schedule for 2018 provided the following opening

balances for the undepreciated capital cost for each class of EASI's assets:

Class 3 — building....................................... $220,000

Class 8 — office furniture and equipment.... 60,000

Class 10 — trucks for transportation of goods 80,000

14. Business interruption insurance premiums of $3,100 were paid to protect the company in

the event a fire forced them to close for a period of time.

Reason/process

Not deductible until it is incurred

+$3,100

15. Computer software costing $750 related to word processing was expensed because they

always bought the upgrades each year.

Reason/process

Capital in nature is not deductible, we take CCA instead

+$750

16. Depreciation expense on the fixed assets was $66,000.

Reason/process

Not deductible

+$66,000

TOTAL = $ 197,550

An examination of the capital cost allowance schedule for 2018 provided the following opening

balances for the undepreciated capital cost for each class of EASI's assets:

Class 3 — building....................................... $220,000

Class 8 — office furniture and equipment.... 60,000

Class 10 — trucks for transportation of goods 80,000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BUSINESS TAXATION IN CANADA 8

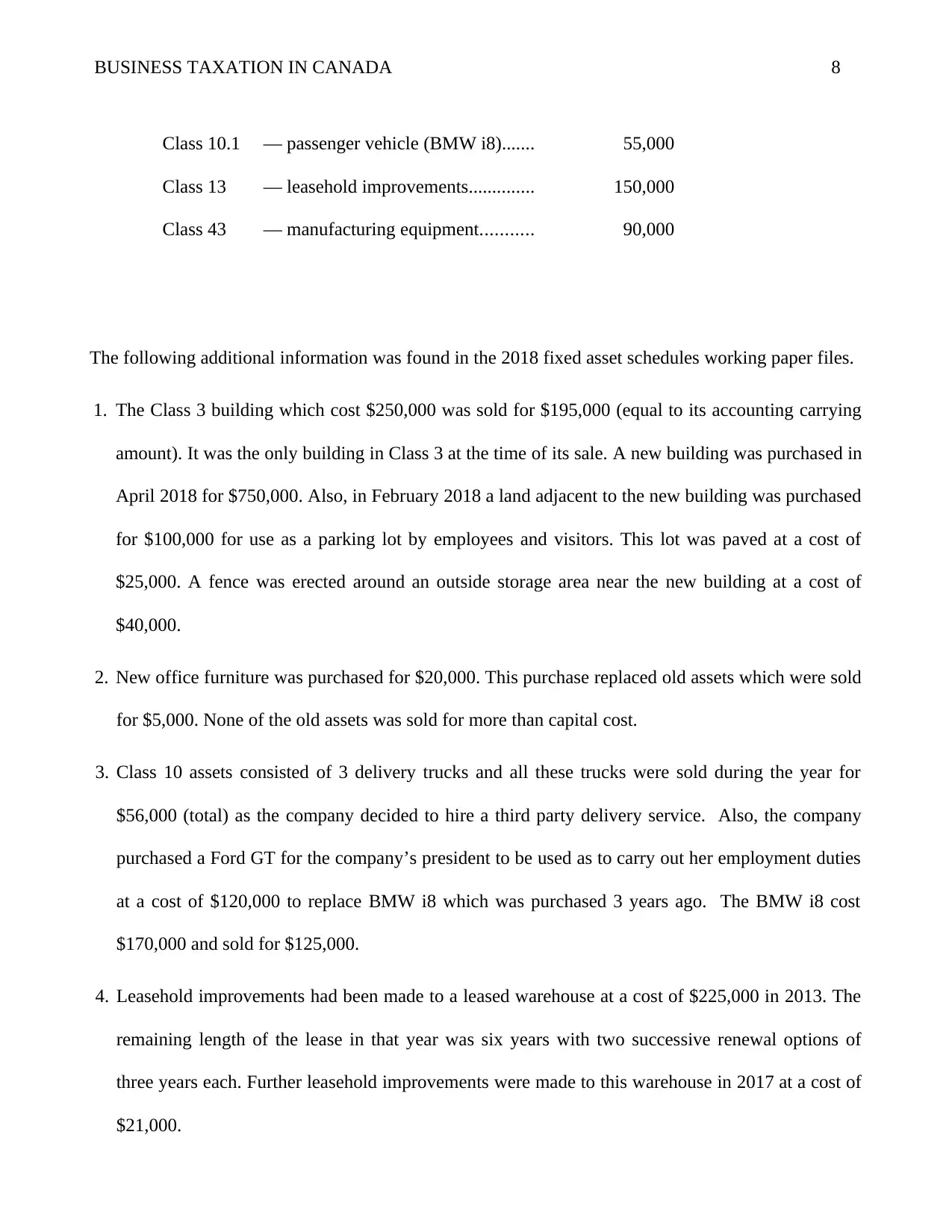

Class 10.1 — passenger vehicle (BMW i8)....... 55,000

Class 13 — leasehold improvements.............. 150,000

Class 43 — manufacturing equipment........... 90,000

The following additional information was found in the 2018 fixed asset schedules working paper files.

1. The Class 3 building which cost $250,000 was sold for $195,000 (equal to its accounting carrying

amount). It was the only building in Class 3 at the time of its sale. A new building was purchased in

April 2018 for $750,000. Also, in February 2018 a land adjacent to the new building was purchased

for $100,000 for use as a parking lot by employees and visitors. This lot was paved at a cost of

$25,000. A fence was erected around an outside storage area near the new building at a cost of

$40,000.

2. New office furniture was purchased for $20,000. This purchase replaced old assets which were sold

for $5,000. None of the old assets was sold for more than capital cost.

3. Class 10 assets consisted of 3 delivery trucks and all these trucks were sold during the year for

$56,000 (total) as the company decided to hire a third party delivery service. Also, the company

purchased a Ford GT for the company’s president to be used as to carry out her employment duties

at a cost of $120,000 to replace BMW i8 which was purchased 3 years ago. The BMW i8 cost

$170,000 and sold for $125,000.

4. Leasehold improvements had been made to a leased warehouse at a cost of $225,000 in 2013. The

remaining length of the lease in that year was six years with two successive renewal options of

three years each. Further leasehold improvements were made to this warehouse in 2017 at a cost of

$21,000.

Class 10.1 — passenger vehicle (BMW i8)....... 55,000

Class 13 — leasehold improvements.............. 150,000

Class 43 — manufacturing equipment........... 90,000

The following additional information was found in the 2018 fixed asset schedules working paper files.

1. The Class 3 building which cost $250,000 was sold for $195,000 (equal to its accounting carrying

amount). It was the only building in Class 3 at the time of its sale. A new building was purchased in

April 2018 for $750,000. Also, in February 2018 a land adjacent to the new building was purchased

for $100,000 for use as a parking lot by employees and visitors. This lot was paved at a cost of

$25,000. A fence was erected around an outside storage area near the new building at a cost of

$40,000.

2. New office furniture was purchased for $20,000. This purchase replaced old assets which were sold

for $5,000. None of the old assets was sold for more than capital cost.

3. Class 10 assets consisted of 3 delivery trucks and all these trucks were sold during the year for

$56,000 (total) as the company decided to hire a third party delivery service. Also, the company

purchased a Ford GT for the company’s president to be used as to carry out her employment duties

at a cost of $120,000 to replace BMW i8 which was purchased 3 years ago. The BMW i8 cost

$170,000 and sold for $125,000.

4. Leasehold improvements had been made to a leased warehouse at a cost of $225,000 in 2013. The

remaining length of the lease in that year was six years with two successive renewal options of

three years each. Further leasehold improvements were made to this warehouse in 2017 at a cost of

$21,000.

BUSINESS TAXATION IN CANADA 9

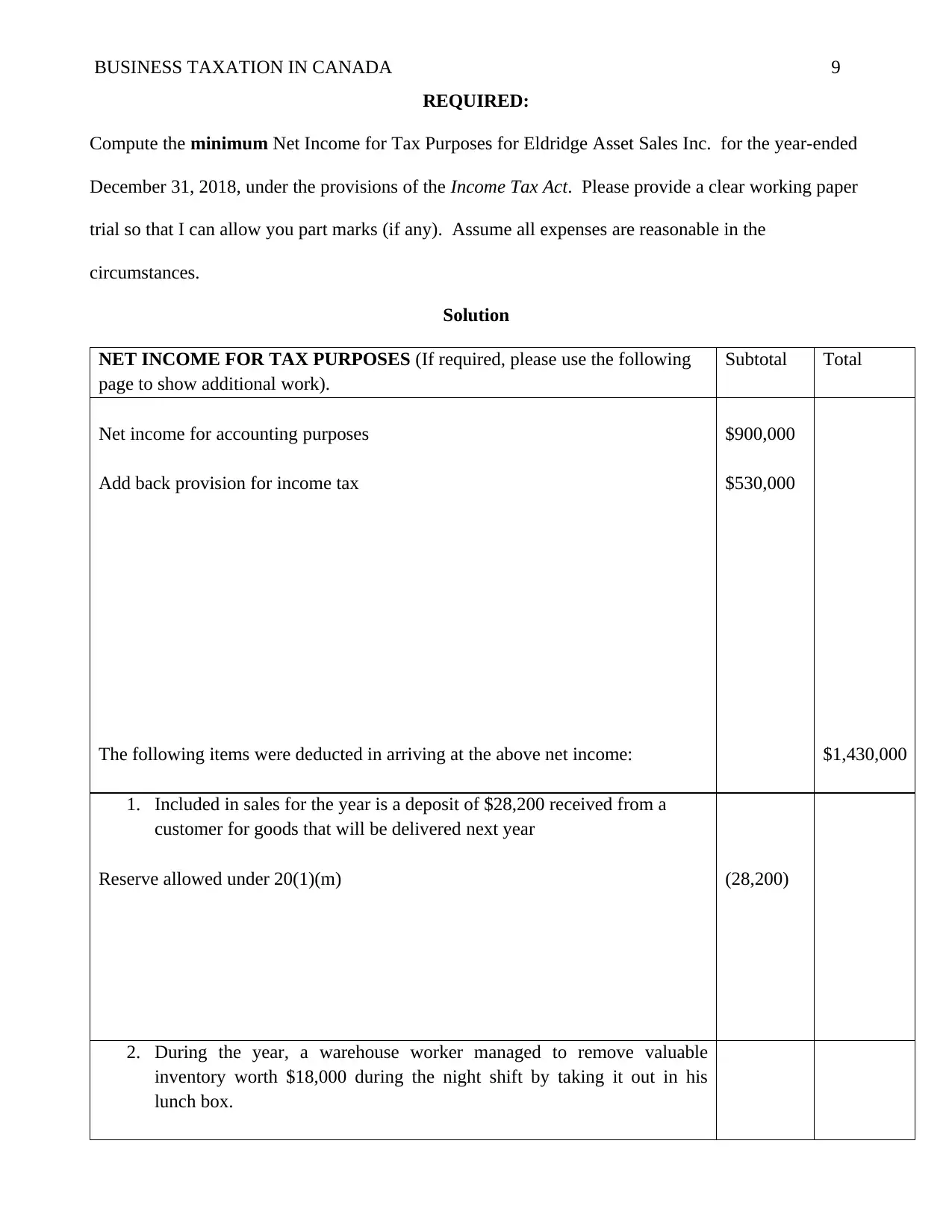

REQUIRED:

Compute the minimum Net Income for Tax Purposes for Eldridge Asset Sales Inc. for the year-ended

December 31, 2018, under the provisions of the Income Tax Act. Please provide a clear working paper

trial so that I can allow you part marks (if any). Assume all expenses are reasonable in the

circumstances.

Solution

NET INCOME FOR TAX PURPOSES (If required, please use the following

page to show additional work).

Subtotal Total

Net income for accounting purposes

Add back provision for income tax

The following items were deducted in arriving at the above net income:

$900,000

$530,000

$1,430,000

1. Included in sales for the year is a deposit of $28,200 received from a

customer for goods that will be delivered next year

Reserve allowed under 20(1)(m) (28,200)

2. During the year, a warehouse worker managed to remove valuable

inventory worth $18,000 during the night shift by taking it out in his

lunch box.

REQUIRED:

Compute the minimum Net Income for Tax Purposes for Eldridge Asset Sales Inc. for the year-ended

December 31, 2018, under the provisions of the Income Tax Act. Please provide a clear working paper

trial so that I can allow you part marks (if any). Assume all expenses are reasonable in the

circumstances.

Solution

NET INCOME FOR TAX PURPOSES (If required, please use the following

page to show additional work).

Subtotal Total

Net income for accounting purposes

Add back provision for income tax

The following items were deducted in arriving at the above net income:

$900,000

$530,000

$1,430,000

1. Included in sales for the year is a deposit of $28,200 received from a

customer for goods that will be delivered next year

Reserve allowed under 20(1)(m) (28,200)

2. During the year, a warehouse worker managed to remove valuable

inventory worth $18,000 during the night shift by taking it out in his

lunch box.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

BUSINESS TAXATION IN CANADA 10

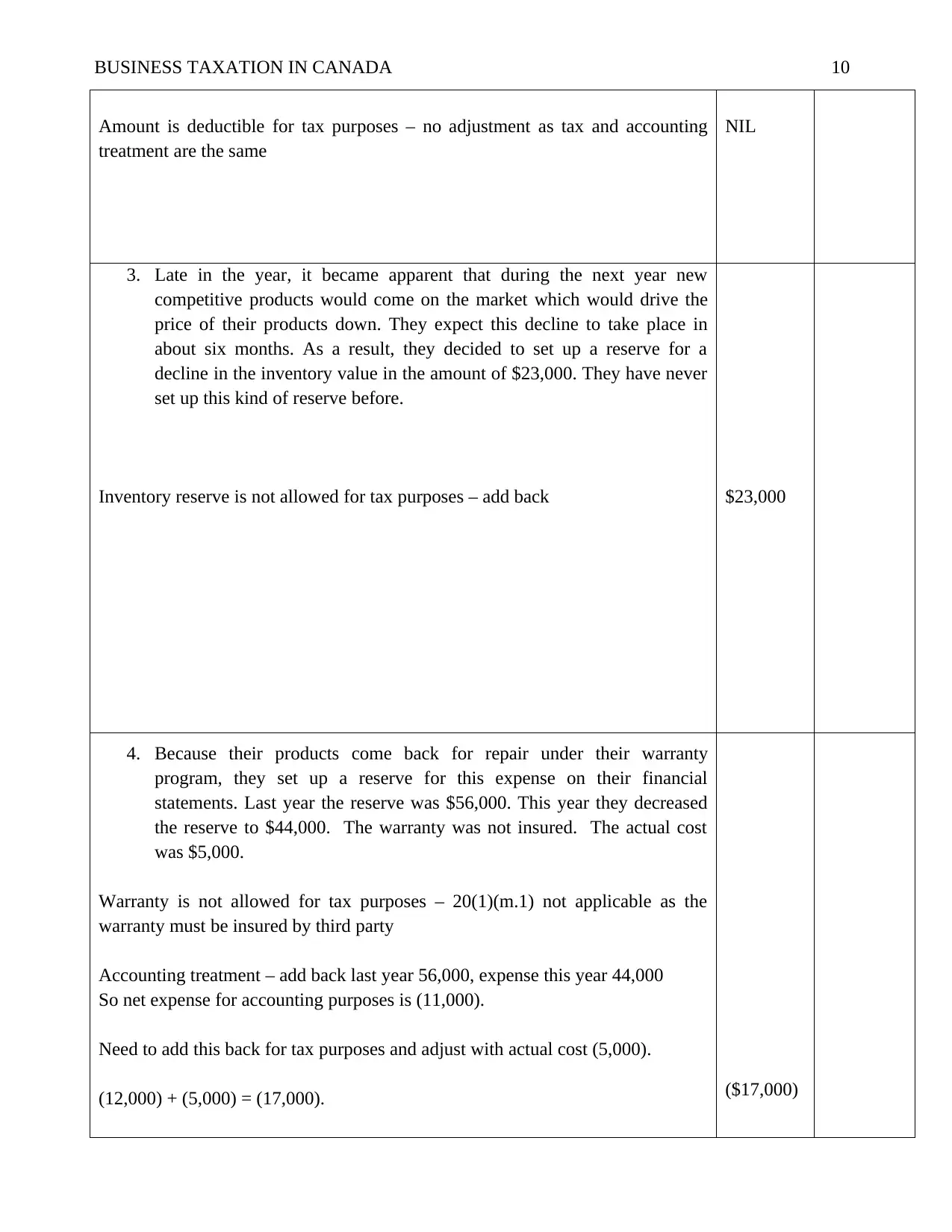

Amount is deductible for tax purposes – no adjustment as tax and accounting

treatment are the same

NIL

3. Late in the year, it became apparent that during the next year new

competitive products would come on the market which would drive the

price of their products down. They expect this decline to take place in

about six months. As a result, they decided to set up a reserve for a

decline in the inventory value in the amount of $23,000. They have never

set up this kind of reserve before.

Inventory reserve is not allowed for tax purposes – add back $23,000

4. Because their products come back for repair under their warranty

program, they set up a reserve for this expense on their financial

statements. Last year the reserve was $56,000. This year they decreased

the reserve to $44,000. The warranty was not insured. The actual cost

was $5,000.

Warranty is not allowed for tax purposes – 20(1)(m.1) not applicable as the

warranty must be insured by third party

Accounting treatment – add back last year 56,000, expense this year 44,000

So net expense for accounting purposes is (11,000).

Need to add this back for tax purposes and adjust with actual cost (5,000).

(12,000) + (5,000) = (17,000). ($17,000)

Amount is deductible for tax purposes – no adjustment as tax and accounting

treatment are the same

NIL

3. Late in the year, it became apparent that during the next year new

competitive products would come on the market which would drive the

price of their products down. They expect this decline to take place in

about six months. As a result, they decided to set up a reserve for a

decline in the inventory value in the amount of $23,000. They have never

set up this kind of reserve before.

Inventory reserve is not allowed for tax purposes – add back $23,000

4. Because their products come back for repair under their warranty

program, they set up a reserve for this expense on their financial

statements. Last year the reserve was $56,000. This year they decreased

the reserve to $44,000. The warranty was not insured. The actual cost

was $5,000.

Warranty is not allowed for tax purposes – 20(1)(m.1) not applicable as the

warranty must be insured by third party

Accounting treatment – add back last year 56,000, expense this year 44,000

So net expense for accounting purposes is (11,000).

Need to add this back for tax purposes and adjust with actual cost (5,000).

(12,000) + (5,000) = (17,000). ($17,000)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BUSINESS TAXATION IN CANADA 11

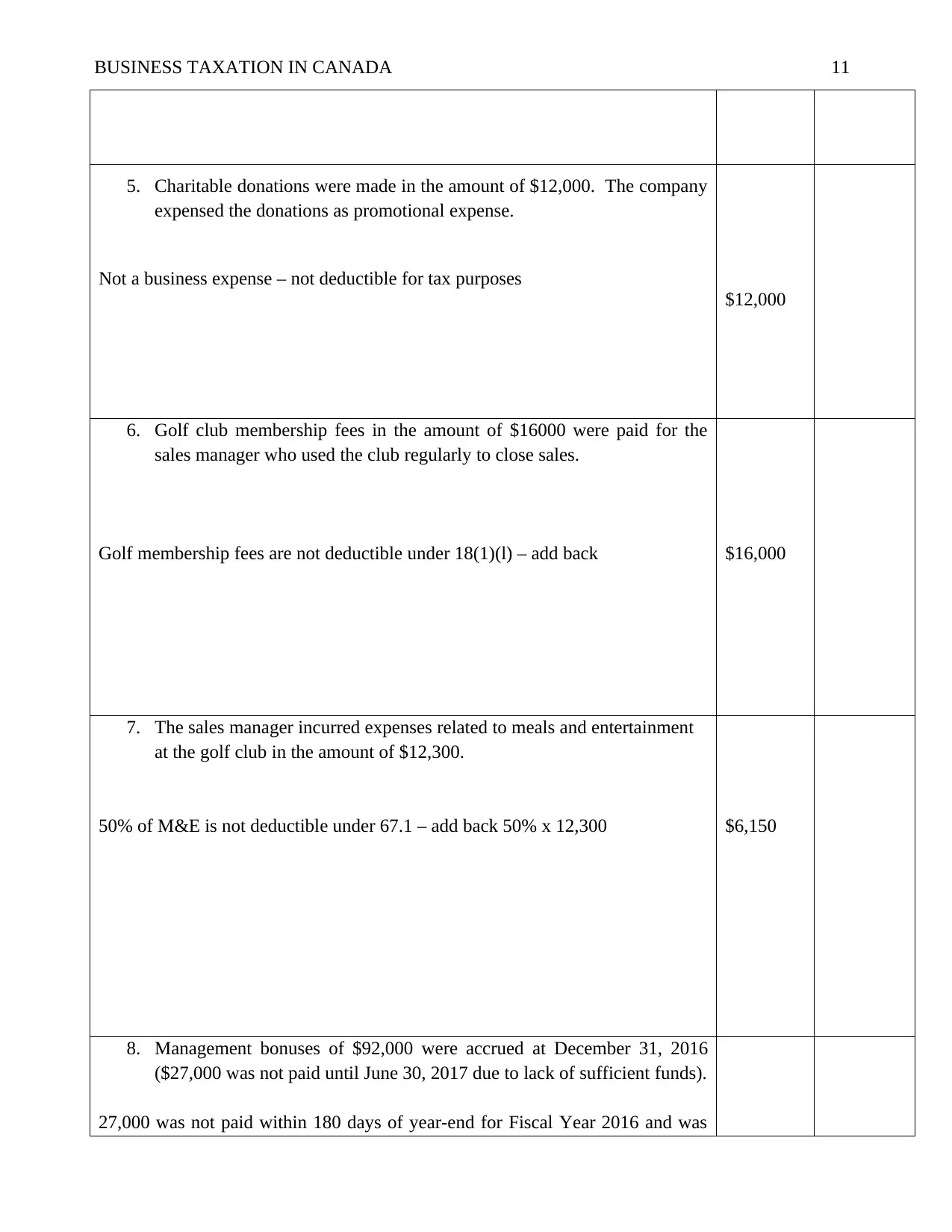

5. Charitable donations were made in the amount of $12,000. The company

expensed the donations as promotional expense.

Not a business expense – not deductible for tax purposes

$12,000

6. Golf club membership fees in the amount of $16000 were paid for the

sales manager who used the club regularly to close sales.

Golf membership fees are not deductible under 18(1)(l) – add back $16,000

7. The sales manager incurred expenses related to meals and entertainment

at the golf club in the amount of $12,300.

50% of M&E is not deductible under 67.1 – add back 50% x 12,300 $6,150

8. Management bonuses of $92,000 were accrued at December 31, 2016

($27,000 was not paid until June 30, 2017 due to lack of sufficient funds).

27,000 was not paid within 180 days of year-end for Fiscal Year 2016 and was

5. Charitable donations were made in the amount of $12,000. The company

expensed the donations as promotional expense.

Not a business expense – not deductible for tax purposes

$12,000

6. Golf club membership fees in the amount of $16000 were paid for the

sales manager who used the club regularly to close sales.

Golf membership fees are not deductible under 18(1)(l) – add back $16,000

7. The sales manager incurred expenses related to meals and entertainment

at the golf club in the amount of $12,300.

50% of M&E is not deductible under 67.1 – add back 50% x 12,300 $6,150

8. Management bonuses of $92,000 were accrued at December 31, 2016

($27,000 was not paid until June 30, 2017 due to lack of sufficient funds).

27,000 was not paid within 180 days of year-end for Fiscal Year 2016 and was

BUSINESS TAXATION IN CANADA 12

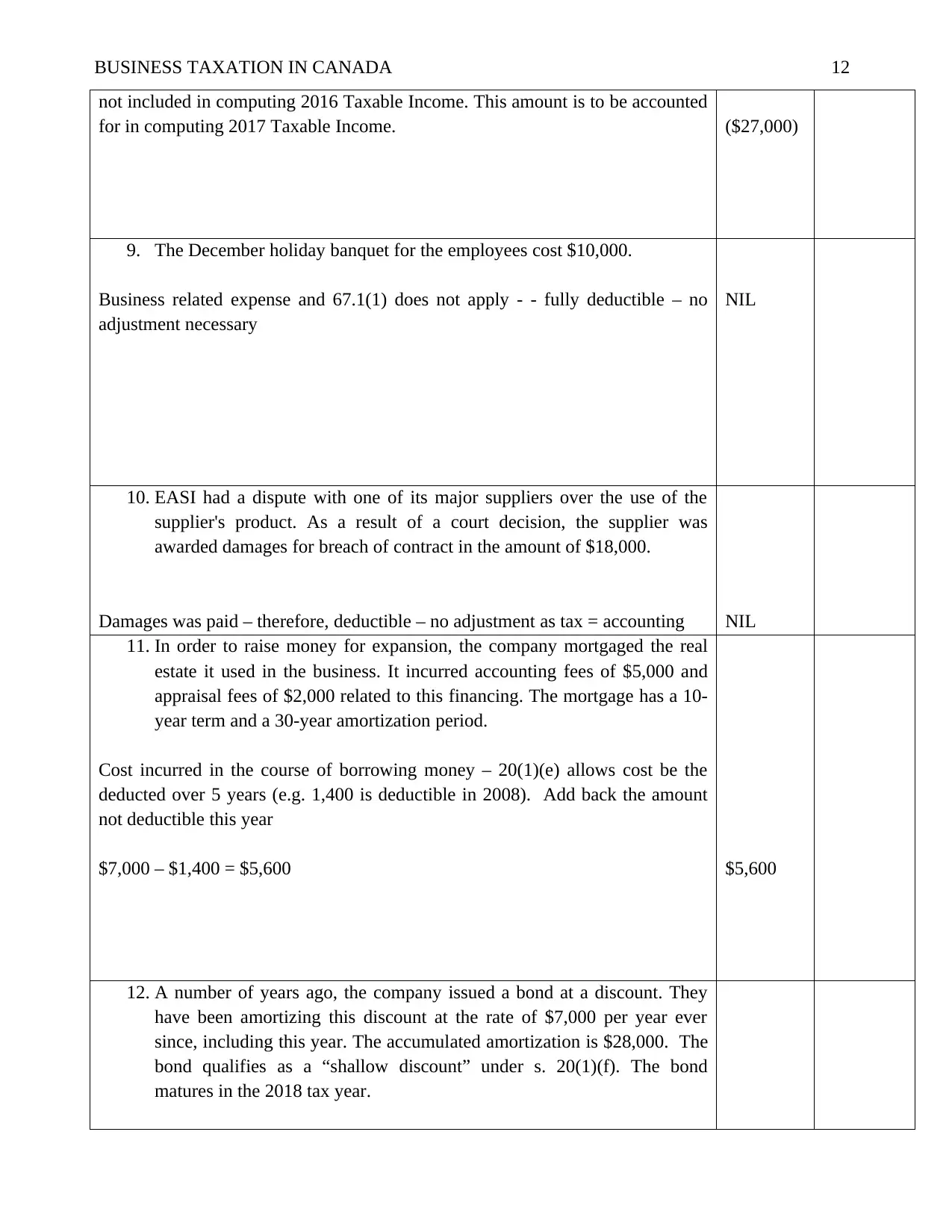

not included in computing 2016 Taxable Income. This amount is to be accounted

for in computing 2017 Taxable Income. ($27,000)

9. The December holiday banquet for the employees cost $10,000.

Business related expense and 67.1(1) does not apply - - fully deductible – no

adjustment necessary

NIL

10. EASI had a dispute with one of its major suppliers over the use of the

supplier's product. As a result of a court decision, the supplier was

awarded damages for breach of contract in the amount of $18,000.

Damages was paid – therefore, deductible – no adjustment as tax = accounting NIL

11. In order to raise money for expansion, the company mortgaged the real

estate it used in the business. It incurred accounting fees of $5,000 and

appraisal fees of $2,000 related to this financing. The mortgage has a 10-

year term and a 30-year amortization period.

Cost incurred in the course of borrowing money – 20(1)(e) allows cost be the

deducted over 5 years (e.g. 1,400 is deductible in 2008). Add back the amount

not deductible this year

$7,000 – $1,400 = $5,600 $5,600

12. A number of years ago, the company issued a bond at a discount. They

have been amortizing this discount at the rate of $7,000 per year ever

since, including this year. The accumulated amortization is $28,000. The

bond qualifies as a “shallow discount” under s. 20(1)(f). The bond

matures in the 2018 tax year.

not included in computing 2016 Taxable Income. This amount is to be accounted

for in computing 2017 Taxable Income. ($27,000)

9. The December holiday banquet for the employees cost $10,000.

Business related expense and 67.1(1) does not apply - - fully deductible – no

adjustment necessary

NIL

10. EASI had a dispute with one of its major suppliers over the use of the

supplier's product. As a result of a court decision, the supplier was

awarded damages for breach of contract in the amount of $18,000.

Damages was paid – therefore, deductible – no adjustment as tax = accounting NIL

11. In order to raise money for expansion, the company mortgaged the real

estate it used in the business. It incurred accounting fees of $5,000 and

appraisal fees of $2,000 related to this financing. The mortgage has a 10-

year term and a 30-year amortization period.

Cost incurred in the course of borrowing money – 20(1)(e) allows cost be the

deducted over 5 years (e.g. 1,400 is deductible in 2008). Add back the amount

not deductible this year

$7,000 – $1,400 = $5,600 $5,600

12. A number of years ago, the company issued a bond at a discount. They

have been amortizing this discount at the rate of $7,000 per year ever

since, including this year. The accumulated amortization is $28,000. The

bond qualifies as a “shallow discount” under s. 20(1)(f). The bond

matures in the 2018 tax year.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.