Cost-Benefit Analysis of Proposal 1 and Proposal 2 for John Wiley Pty Ltd

VerifiedAdded on 2019/10/30

|27

|2747

|144

Report

AI Summary

Project finance costs are the risks characteristic to project financing, which can reduce the liquidity of a project's debt. The project finance costs for Proposal 1 is $69,840,386 and for Proposal 2 is $70,073,224. Cost escalation for Proposal 1 is $24,005,796 and for Proposal 2 is $39,355,932. Both proposals have varying initial yields, with Proposal 1 having a better yield. John Wiley Pty Ltd will purchase the entire facility for both proposals. The developer profit for Proposal 1 is estimated as $130,704,595 and for Proposal 2 as $117,968,291. The Net Present Value (NPV) for Proposal 1 is -$77,880,299 and for Proposal 2 is -$134,770,067, indicating that Proposal 1 is more cost-effective. The annual net cash flow for 10 years for both proposals is provided. The NPV of sale in the year 2020 at a discount rate of 9% for both proposals is $948,462,672 for Proposal 1 and $938,861,626 for Proposal 2. The Internal Rate of Return (IRR) for Option 1 and Option 2 is 10.79% and 12.53%, respectively.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Engineering Management

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Letter to the Managing Director

23 October 2017

XXX

Dear Managing Director

It is our pleasure to inform you that calculating the proposals provided to us for the Sub Division

Residential Development Complex Project located at the outer suburb of Point Cook, VIC have

been done carefully.

For a clear vision the two proposals that are provided have been financially analyzed and

accomplished to understand which proposal is more feasible. Proposal 1 has confirmed to be

more economically feasible as the profit betters that of the proposal 2.

Through the term of this report this will turn out to be clear through our utilization of

investigation apparatuses intended to analyze the two choices.

For further information kindly contact me: XXX University,

Tel: XXX

Regards,

XXX

23 October 2017

XXX

Dear Managing Director

It is our pleasure to inform you that calculating the proposals provided to us for the Sub Division

Residential Development Complex Project located at the outer suburb of Point Cook, VIC have

been done carefully.

For a clear vision the two proposals that are provided have been financially analyzed and

accomplished to understand which proposal is more feasible. Proposal 1 has confirmed to be

more economically feasible as the profit betters that of the proposal 2.

Through the term of this report this will turn out to be clear through our utilization of

investigation apparatuses intended to analyze the two choices.

For further information kindly contact me: XXX University,

Tel: XXX

Regards,

XXX

Executive Summary

This report clarifies the findings of the money related practicality ponder done in the investor’s

interest, executed by the budgetary advisor group. It noticed the key examinations between two

alternatives which propose the development of a Sub Division Residential Development

Complex Project located at the outer suburb of Point Cook, VIC. This contains an inside and out

investigation including however not restricted to a Gantt chart, yearly net income and

suggestions. We found that Proposal 1 was the better one than attempt for the financial specialist,

in any case, the designer would profit more noteworthy with Proposal 2. Overall the two

proposals are not cautious alternatives to hold for this specific undertaking.

This report clarifies the findings of the money related practicality ponder done in the investor’s

interest, executed by the budgetary advisor group. It noticed the key examinations between two

alternatives which propose the development of a Sub Division Residential Development

Complex Project located at the outer suburb of Point Cook, VIC. This contains an inside and out

investigation including however not restricted to a Gantt chart, yearly net income and

suggestions. We found that Proposal 1 was the better one than attempt for the financial specialist,

in any case, the designer would profit more noteworthy with Proposal 2. Overall the two

proposals are not cautious alternatives to hold for this specific undertaking.

Assumptions

Land all sold over 18 months

The expenses will be 30% of the gross revenue

All properties 100% leased

Land all sold over 18 months

The expenses will be 30% of the gross revenue

All properties 100% leased

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

Introduction.............................................................................................................................................4

Aim..........................................................................................................................................................5

Outline Methodology..............................................................................................................................5

Part A.......................................................................................................................................................6

Part B.....................................................................................................................................................13

Part C.....................................................................................................................................................15

Part D.....................................................................................................................................................16

Part E.....................................................................................................................................................16

Part-G....................................................................................................................................................19

Recommendations.................................................................................................................................19

References............................................................................................................................................19

Introduction.............................................................................................................................................4

Aim..........................................................................................................................................................5

Outline Methodology..............................................................................................................................5

Part A.......................................................................................................................................................6

Part B.....................................................................................................................................................13

Part C.....................................................................................................................................................15

Part D.....................................................................................................................................................16

Part E.....................................................................................................................................................16

Part-G....................................................................................................................................................19

Recommendations.................................................................................................................................19

References............................................................................................................................................19

Introduction

As a section of this task, we have been designated as monetary specialists for an

Investment Company for which we should do a budgetary attainability examination for two

proposals to construct a Sub Division Residential Development Complex Project located at the

outer suburb of Point Cook, VIC and make suggestions to the Managing Director to legitimize

the money related feasibility. From these two Proposals, we should choose which alternative will

be better for the organization through contrasting perspectives, for example, costs, incomes, and

venture salary and different distributions. The Sub Division Residential Development Complex

Project consist of Aged care Accommodation, Medical center, Shopping center, Parks and

recreation facilities. Toward the finish of the examination, an informed proposal is made to the

Managing Director in regards to which alternative is the most reasonable choice. This report

additionally contains conceivable dangers which might be experienced through the advancement.

Aim

To convey a financial feasibility study for the proposed Sub Division Residential Development

Complex Project located at the outer suburb of Point Cook, VIC and make recommendations to

the Managing Director of the Investment Company regarding which proposal has the most

financial feasibility is the aim of the project.

Outline Methodology

To analyze a feasibility study the subsequent principles or procedure are essentially taken to

completely realize the two proposals approaching to provide the client with a better

understanding about what the project is. These procedure or principles include

Computing the Sub Division Residential Development Complex Project located at the

outer suburb of Point Cook, VIC total cost.

Estimate internal rate of return.

Conclude the NPV.

Manipulating the cash flow for the given period.

The debt: equity ratio analysis.

And provide a sensitive analysis along with risk analysis.

This report sets out the Sub Division Residential Development Complex Project located

at the outer suburb of Point Cook, VIC proposals for the construction phase. The key features of

the construction stage and the proposals are developed to diminish the impacts.

In this report, the development proposal for the project is defined. The total cost of the

construction completion as per the on 1st April 2017 is being calculated in Part-A, the net

income on the completion of the project is being identified and the total development cost, cost

As a section of this task, we have been designated as monetary specialists for an

Investment Company for which we should do a budgetary attainability examination for two

proposals to construct a Sub Division Residential Development Complex Project located at the

outer suburb of Point Cook, VIC and make suggestions to the Managing Director to legitimize

the money related feasibility. From these two Proposals, we should choose which alternative will

be better for the organization through contrasting perspectives, for example, costs, incomes, and

venture salary and different distributions. The Sub Division Residential Development Complex

Project consist of Aged care Accommodation, Medical center, Shopping center, Parks and

recreation facilities. Toward the finish of the examination, an informed proposal is made to the

Managing Director in regards to which alternative is the most reasonable choice. This report

additionally contains conceivable dangers which might be experienced through the advancement.

Aim

To convey a financial feasibility study for the proposed Sub Division Residential Development

Complex Project located at the outer suburb of Point Cook, VIC and make recommendations to

the Managing Director of the Investment Company regarding which proposal has the most

financial feasibility is the aim of the project.

Outline Methodology

To analyze a feasibility study the subsequent principles or procedure are essentially taken to

completely realize the two proposals approaching to provide the client with a better

understanding about what the project is. These procedure or principles include

Computing the Sub Division Residential Development Complex Project located at the

outer suburb of Point Cook, VIC total cost.

Estimate internal rate of return.

Conclude the NPV.

Manipulating the cash flow for the given period.

The debt: equity ratio analysis.

And provide a sensitive analysis along with risk analysis.

This report sets out the Sub Division Residential Development Complex Project located

at the outer suburb of Point Cook, VIC proposals for the construction phase. The key features of

the construction stage and the proposals are developed to diminish the impacts.

In this report, the development proposal for the project is defined. The total cost of the

construction completion as per the on 1st April 2017 is being calculated in Part-A, the net

income on the completion of the project is being identified and the total development cost, cost

of the project is done. From the two given proposal, the best suit proposal is found out and the

statement is provided in Part-C. The calculation is also done for the John Wiley is done in Part-

B. In Part-D the impacts of the different equity ratios are provided. All possible risk is been

identified in Part-E and the three risky areas are specified, spider graph is provided for a clear

definition

Part A

Answer

1.

To calculate the total cost for the Sub division department as per 1st April 2017 Excel

sheet is been used for the calculation (Kubba, 2010). The following steps are done

An input table is setup in MS excel for option 1 sheet 1 is used

The construction cost that given for 1st January 2017 is take as the current vale

and the calculation is done by using the formula

statement is provided in Part-C. The calculation is also done for the John Wiley is done in Part-

B. In Part-D the impacts of the different equity ratios are provided. All possible risk is been

identified in Part-E and the three risky areas are specified, spider graph is provided for a clear

definition

Part A

Answer

1.

To calculate the total cost for the Sub division department as per 1st April 2017 Excel

sheet is been used for the calculation (Kubba, 2010). The following steps are done

An input table is setup in MS excel for option 1 sheet 1 is used

The construction cost that given for 1st January 2017 is take as the current vale

and the calculation is done by using the formula

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Total Cost for the Sub division department as per 1st April 2017

Figure 1 Total cost for Proposal 1

Figure 1 Total cost for Proposal 1

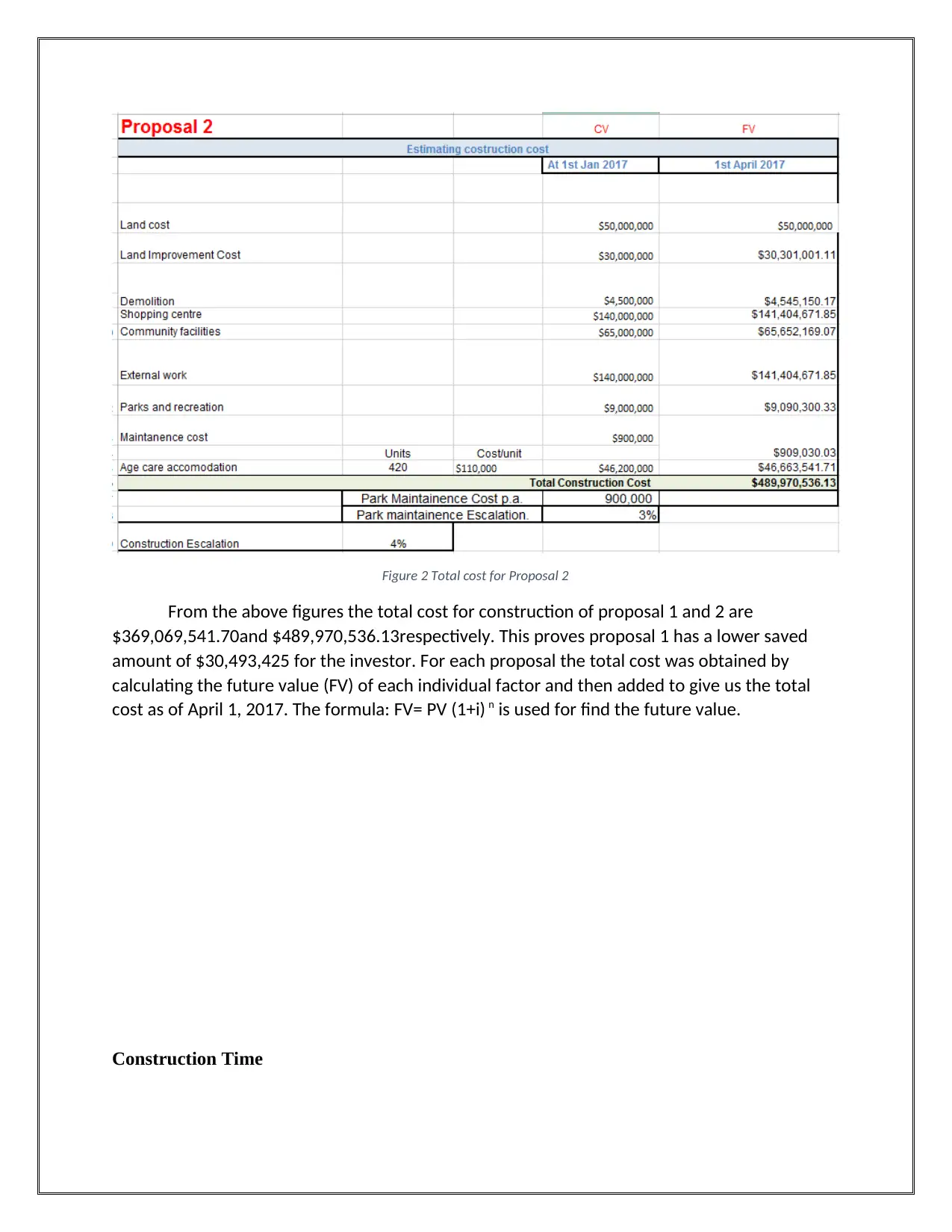

Figure 2 Total cost for Proposal 2

From the above figures the total cost for construction of proposal 1 and 2 are

$369,069,541.70and $489,970,536.13respectively. This proves proposal 1 has a lower saved

amount of $30,493,425 for the investor. For each proposal the total cost was obtained by

calculating the future value (FV) of each individual factor and then added to give us the total

cost as of April 1, 2017. The formula: FV= PV (1+i) n is used for find the future value.

Construction Time

From the above figures the total cost for construction of proposal 1 and 2 are

$369,069,541.70and $489,970,536.13respectively. This proves proposal 1 has a lower saved

amount of $30,493,425 for the investor. For each proposal the total cost was obtained by

calculating the future value (FV) of each individual factor and then added to give us the total

cost as of April 1, 2017. The formula: FV= PV (1+i) n is used for find the future value.

Construction Time

Figure 3 construction time for Proposal 1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Figure 4 construction time for Proposal 2

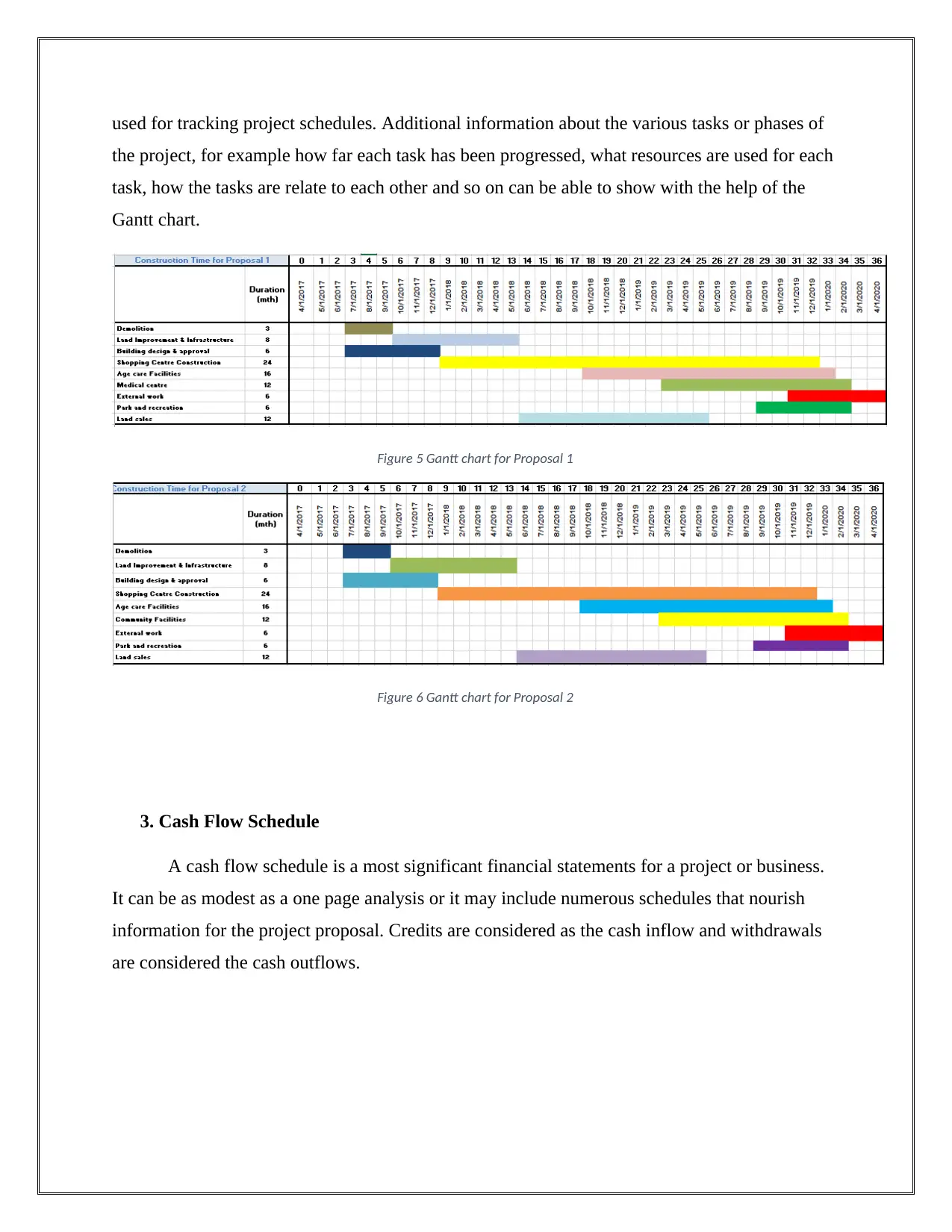

2. Gantt Chart

A development plan has a set of documents that is used to set out the local authority's

policies and proposals for the developing and using the land in their area. Development plan

details the complete strategy of the council and makes for the suitable planning and ecological

development of an area and generally it consists of a written statement and accompanied with

maps. The broad aims of council on topics like infrastructure, housing, community facilities that

will be strengthened by more detailed objectives, procedures and policies are included in the

plan.

The main statement of the public planning policies and objectives are provided by the

development plan. The procedures, policies and objectives are serious in determining the suitable

location and form of different categories of development because the development plan is one of

the issues in contradiction of which planning applications are evaluated. For the development

plan work breakdown structure is essential to achieve this Gantt charts are used. Gantt charts are

2. Gantt Chart

A development plan has a set of documents that is used to set out the local authority's

policies and proposals for the developing and using the land in their area. Development plan

details the complete strategy of the council and makes for the suitable planning and ecological

development of an area and generally it consists of a written statement and accompanied with

maps. The broad aims of council on topics like infrastructure, housing, community facilities that

will be strengthened by more detailed objectives, procedures and policies are included in the

plan.

The main statement of the public planning policies and objectives are provided by the

development plan. The procedures, policies and objectives are serious in determining the suitable

location and form of different categories of development because the development plan is one of

the issues in contradiction of which planning applications are evaluated. For the development

plan work breakdown structure is essential to achieve this Gantt charts are used. Gantt charts are

used for tracking project schedules. Additional information about the various tasks or phases of

the project, for example how far each task has been progressed, what resources are used for each

task, how the tasks are relate to each other and so on can be able to show with the help of the

Gantt chart.

Figure 5 Gantt chart for Proposal 1

Figure 6 Gantt chart for Proposal 2

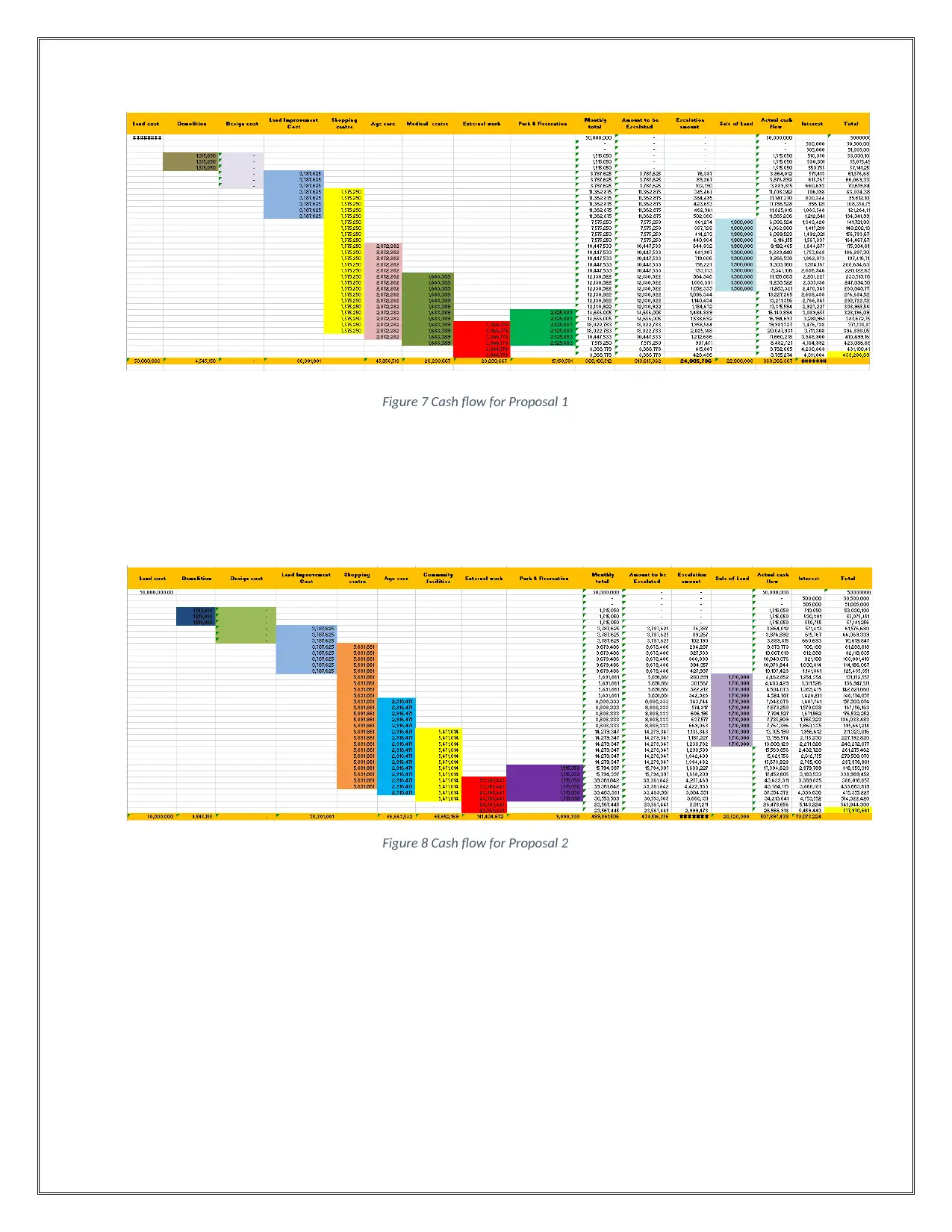

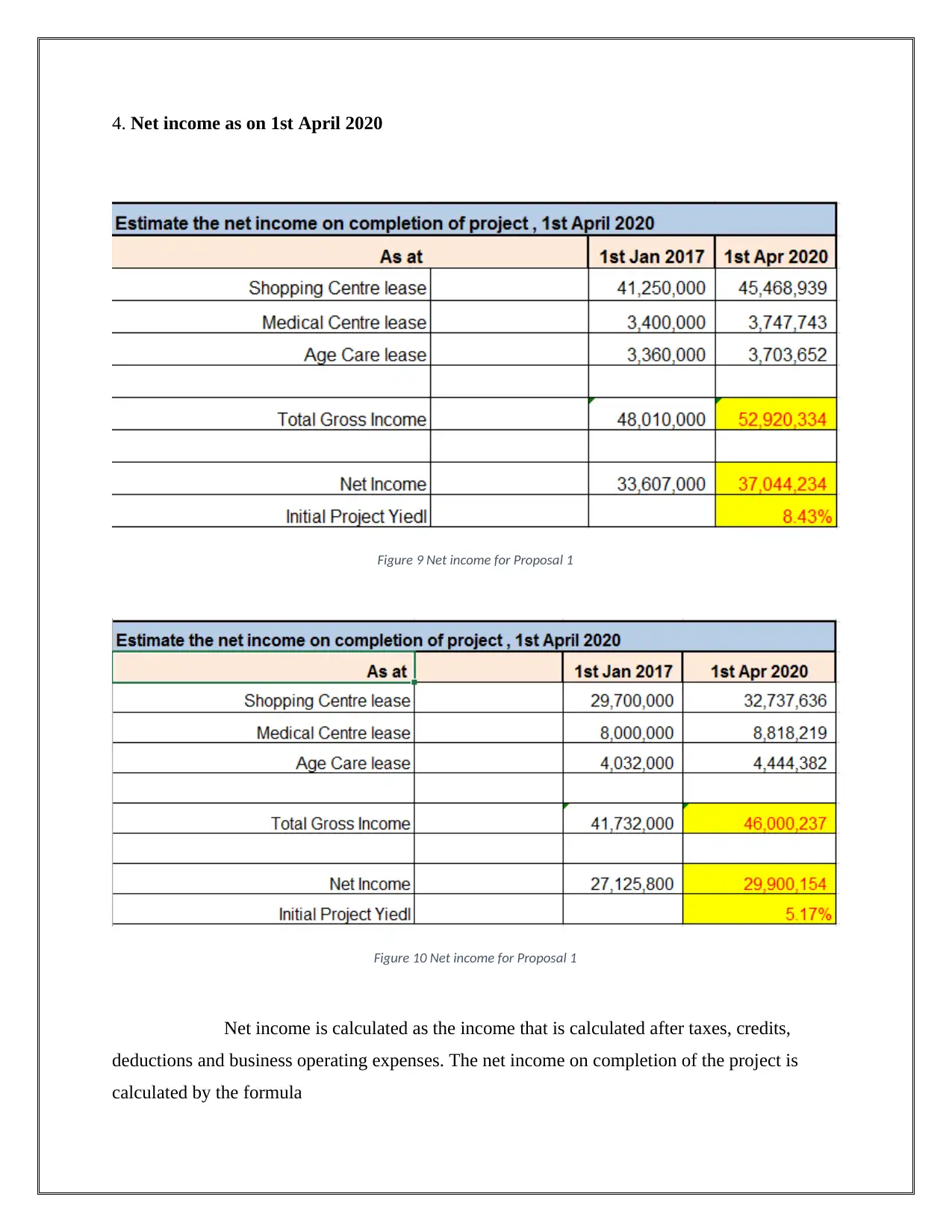

3. Cash Flow Schedule

A cash flow schedule is a most significant financial statements for a project or business.

It can be as modest as a one page analysis or it may include numerous schedules that nourish

information for the project proposal. Credits are considered as the cash inflow and withdrawals

are considered the cash outflows.

the project, for example how far each task has been progressed, what resources are used for each

task, how the tasks are relate to each other and so on can be able to show with the help of the

Gantt chart.

Figure 5 Gantt chart for Proposal 1

Figure 6 Gantt chart for Proposal 2

3. Cash Flow Schedule

A cash flow schedule is a most significant financial statements for a project or business.

It can be as modest as a one page analysis or it may include numerous schedules that nourish

information for the project proposal. Credits are considered as the cash inflow and withdrawals

are considered the cash outflows.

Figure 7 Cash flow for Proposal 1

Figure 8 Cash flow for Proposal 2

Figure 8 Cash flow for Proposal 2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

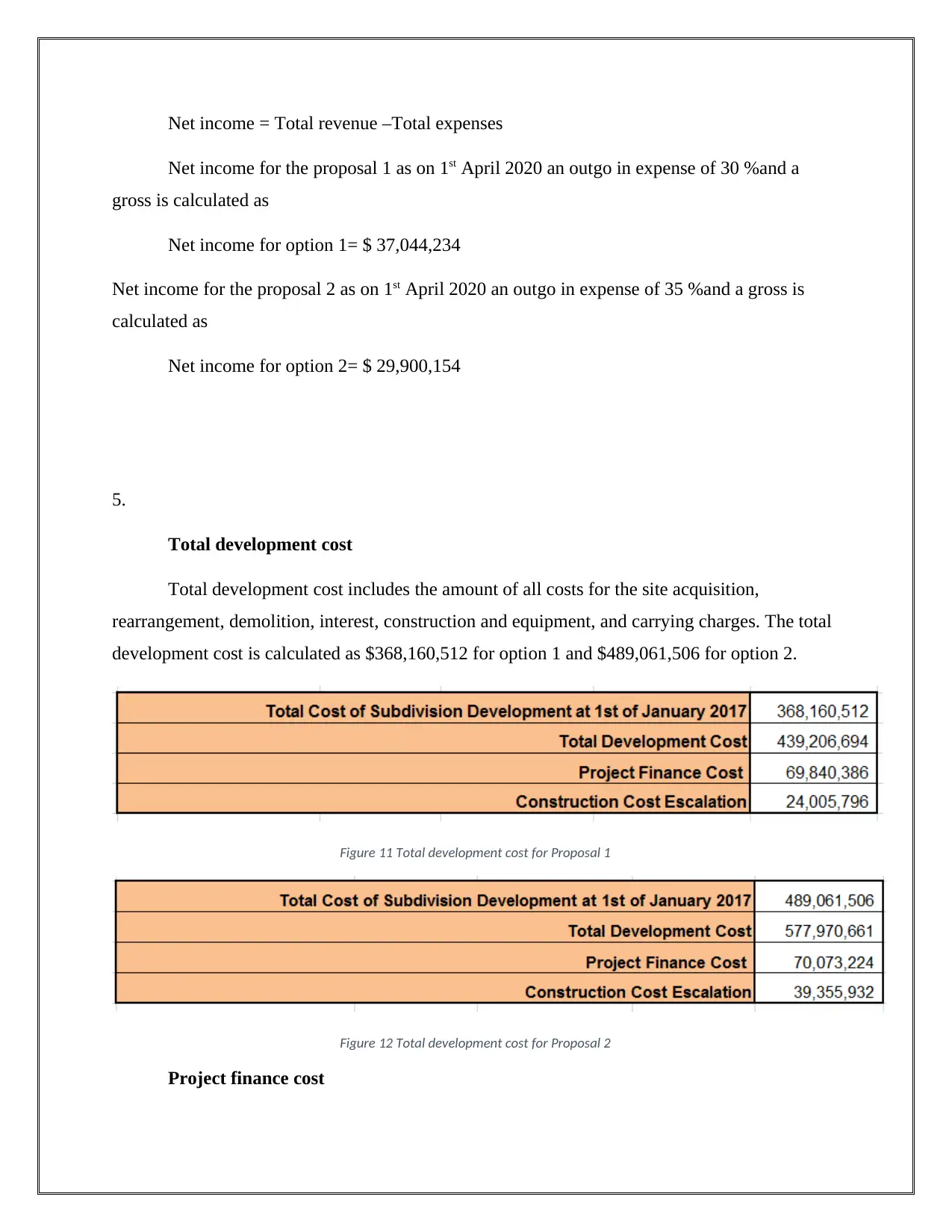

4. Net income as on 1st April 2020

Figure 9 Net income for Proposal 1

Figure 10 Net income for Proposal 1

Net income is calculated as the income that is calculated after taxes, credits,

deductions and business operating expenses. The net income on completion of the project is

calculated by the formula

Figure 9 Net income for Proposal 1

Figure 10 Net income for Proposal 1

Net income is calculated as the income that is calculated after taxes, credits,

deductions and business operating expenses. The net income on completion of the project is

calculated by the formula

Net income = Total revenue –Total expenses

Net income for the proposal 1 as on 1st April 2020 an outgo in expense of 30 %and a

gross is calculated as

Net income for option 1= $ 37,044,234

Net income for the proposal 2 as on 1st April 2020 an outgo in expense of 35 %and a gross is

calculated as

Net income for option 2= $ 29,900,154

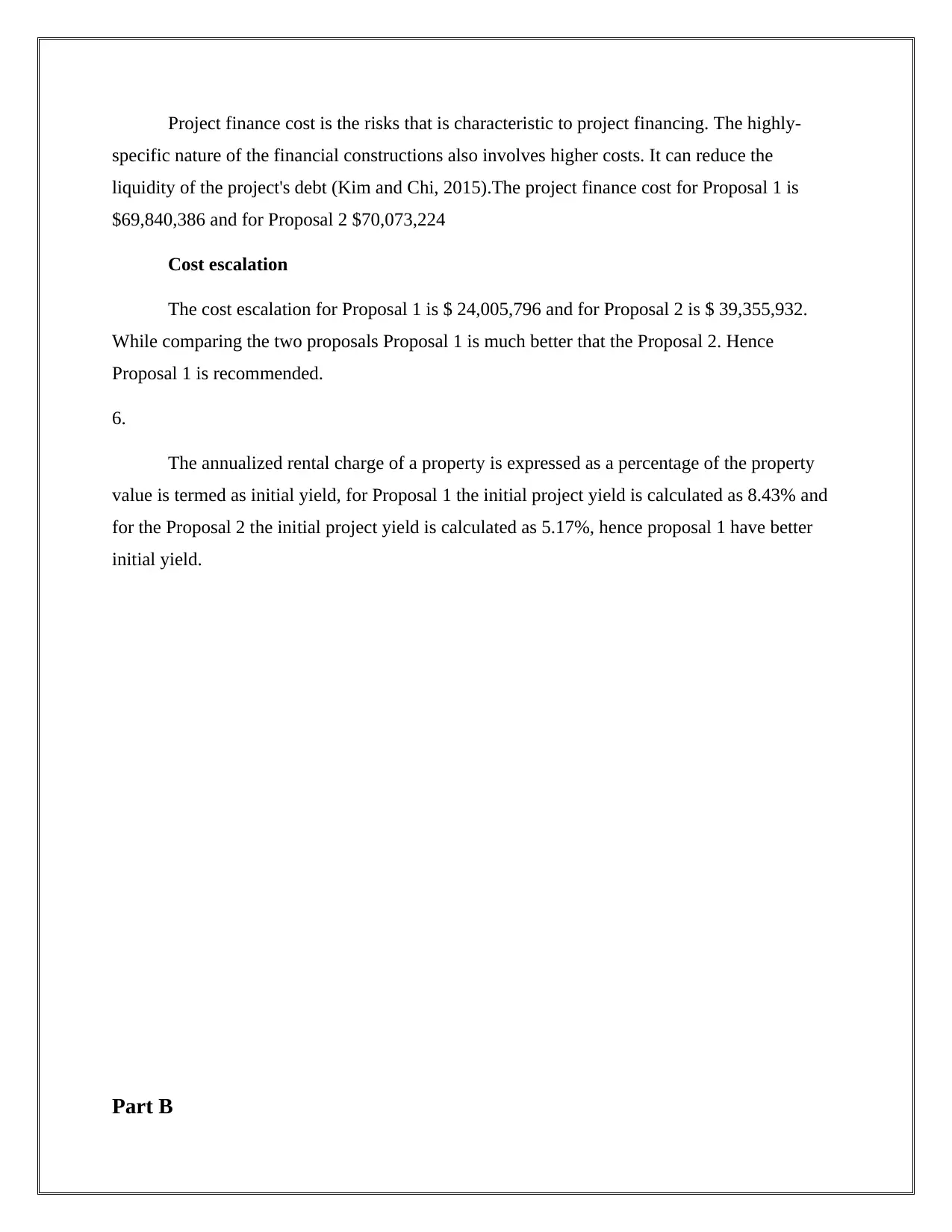

5.

Total development cost

Total development cost includes the amount of all costs for the site acquisition,

rearrangement, demolition, interest, construction and equipment, and carrying charges. The total

development cost is calculated as $368,160,512 for option 1 and $489,061,506 for option 2.

Figure 11 Total development cost for Proposal 1

Figure 12 Total development cost for Proposal 2

Project finance cost

Net income for the proposal 1 as on 1st April 2020 an outgo in expense of 30 %and a

gross is calculated as

Net income for option 1= $ 37,044,234

Net income for the proposal 2 as on 1st April 2020 an outgo in expense of 35 %and a gross is

calculated as

Net income for option 2= $ 29,900,154

5.

Total development cost

Total development cost includes the amount of all costs for the site acquisition,

rearrangement, demolition, interest, construction and equipment, and carrying charges. The total

development cost is calculated as $368,160,512 for option 1 and $489,061,506 for option 2.

Figure 11 Total development cost for Proposal 1

Figure 12 Total development cost for Proposal 2

Project finance cost

Project finance cost is the risks that is characteristic to project financing. The highly-

specific nature of the financial constructions also involves higher costs. It can reduce the

liquidity of the project's debt (Kim and Chi, 2015).The project finance cost for Proposal 1 is

$69,840,386 and for Proposal 2 $70,073,224

Cost escalation

The cost escalation for Proposal 1 is $ 24,005,796 and for Proposal 2 is $ 39,355,932.

While comparing the two proposals Proposal 1 is much better that the Proposal 2. Hence

Proposal 1 is recommended.

6.

The annualized rental charge of a property is expressed as a percentage of the property

value is termed as initial yield, for Proposal 1 the initial project yield is calculated as 8.43% and

for the Proposal 2 the initial project yield is calculated as 5.17%, hence proposal 1 have better

initial yield.

Part B

specific nature of the financial constructions also involves higher costs. It can reduce the

liquidity of the project's debt (Kim and Chi, 2015).The project finance cost for Proposal 1 is

$69,840,386 and for Proposal 2 $70,073,224

Cost escalation

The cost escalation for Proposal 1 is $ 24,005,796 and for Proposal 2 is $ 39,355,932.

While comparing the two proposals Proposal 1 is much better that the Proposal 2. Hence

Proposal 1 is recommended.

6.

The annualized rental charge of a property is expressed as a percentage of the property

value is termed as initial yield, for Proposal 1 the initial project yield is calculated as 8.43% and

for the Proposal 2 the initial project yield is calculated as 5.17%, hence proposal 1 have better

initial yield.

Part B

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Answers

Calculation for John Wiley Pty Ltd on completion

1.

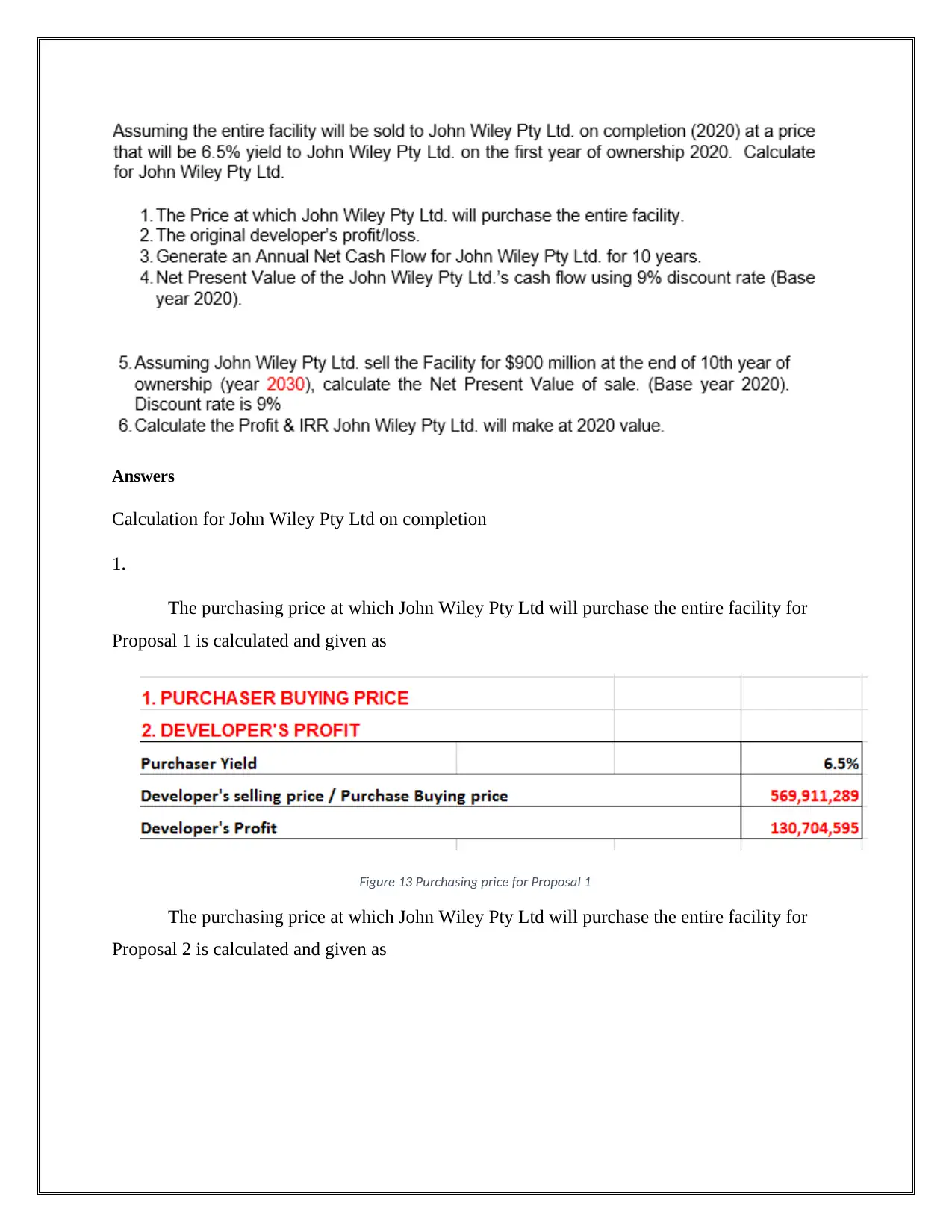

The purchasing price at which John Wiley Pty Ltd will purchase the entire facility for

Proposal 1 is calculated and given as

Figure 13 Purchasing price for Proposal 1

The purchasing price at which John Wiley Pty Ltd will purchase the entire facility for

Proposal 2 is calculated and given as

Calculation for John Wiley Pty Ltd on completion

1.

The purchasing price at which John Wiley Pty Ltd will purchase the entire facility for

Proposal 1 is calculated and given as

Figure 13 Purchasing price for Proposal 1

The purchasing price at which John Wiley Pty Ltd will purchase the entire facility for

Proposal 2 is calculated and given as

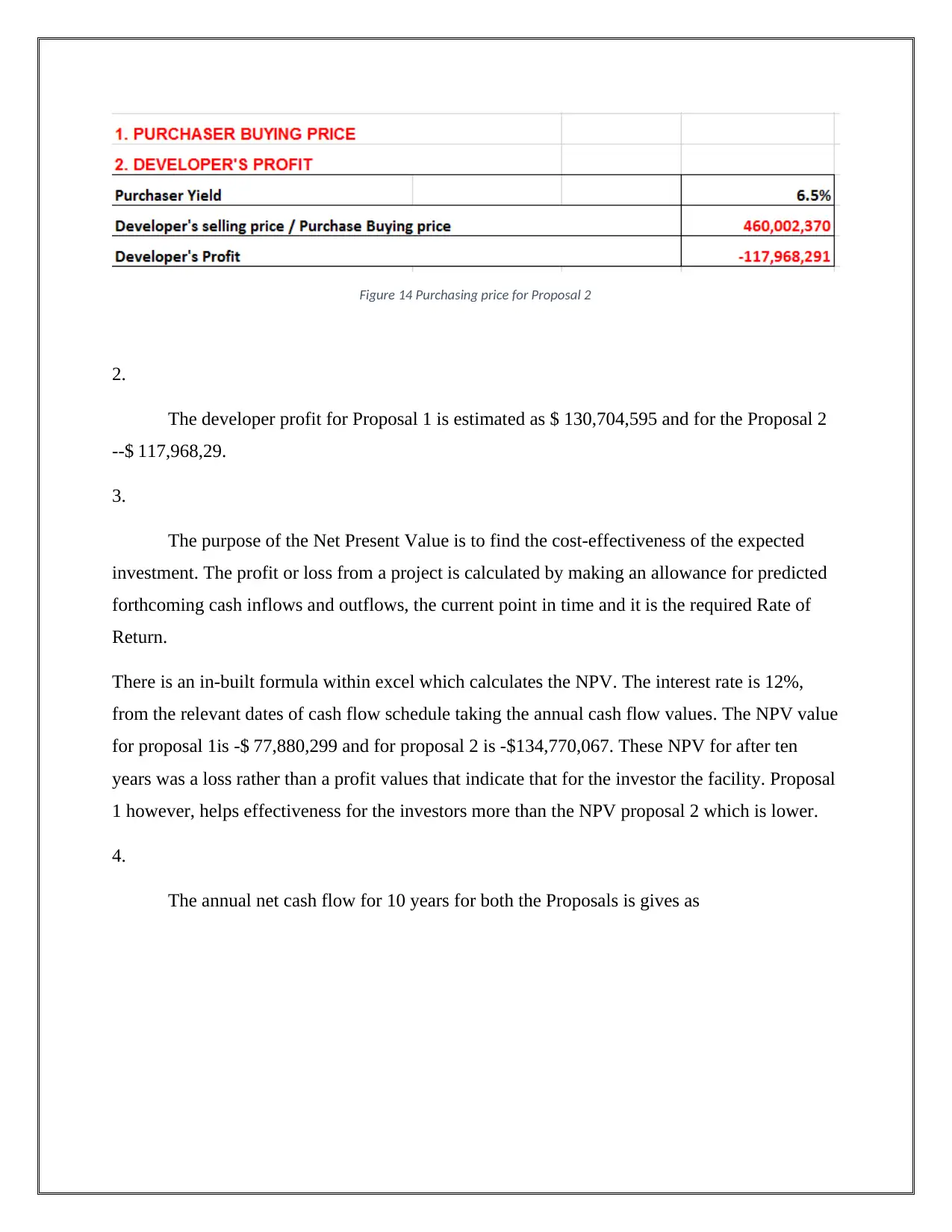

Figure 14 Purchasing price for Proposal 2

2.

The developer profit for Proposal 1 is estimated as $ 130,704,595 and for the Proposal 2

--$ 117,968,29.

3.

The purpose of the Net Present Value is to find the cost-effectiveness of the expected

investment. The profit or loss from a project is calculated by making an allowance for predicted

forthcoming cash inflows and outflows, the current point in time and it is the required Rate of

Return.

There is an in-built formula within excel which calculates the NPV. The interest rate is 12%,

from the relevant dates of cash flow schedule taking the annual cash flow values. The NPV value

for proposal 1is -$ 77,880,299 and for proposal 2 is -$134,770,067. These NPV for after ten

years was a loss rather than a profit values that indicate that for the investor the facility. Proposal

1 however, helps effectiveness for the investors more than the NPV proposal 2 which is lower.

4.

The annual net cash flow for 10 years for both the Proposals is gives as

2.

The developer profit for Proposal 1 is estimated as $ 130,704,595 and for the Proposal 2

--$ 117,968,29.

3.

The purpose of the Net Present Value is to find the cost-effectiveness of the expected

investment. The profit or loss from a project is calculated by making an allowance for predicted

forthcoming cash inflows and outflows, the current point in time and it is the required Rate of

Return.

There is an in-built formula within excel which calculates the NPV. The interest rate is 12%,

from the relevant dates of cash flow schedule taking the annual cash flow values. The NPV value

for proposal 1is -$ 77,880,299 and for proposal 2 is -$134,770,067. These NPV for after ten

years was a loss rather than a profit values that indicate that for the investor the facility. Proposal

1 however, helps effectiveness for the investors more than the NPV proposal 2 which is lower.

4.

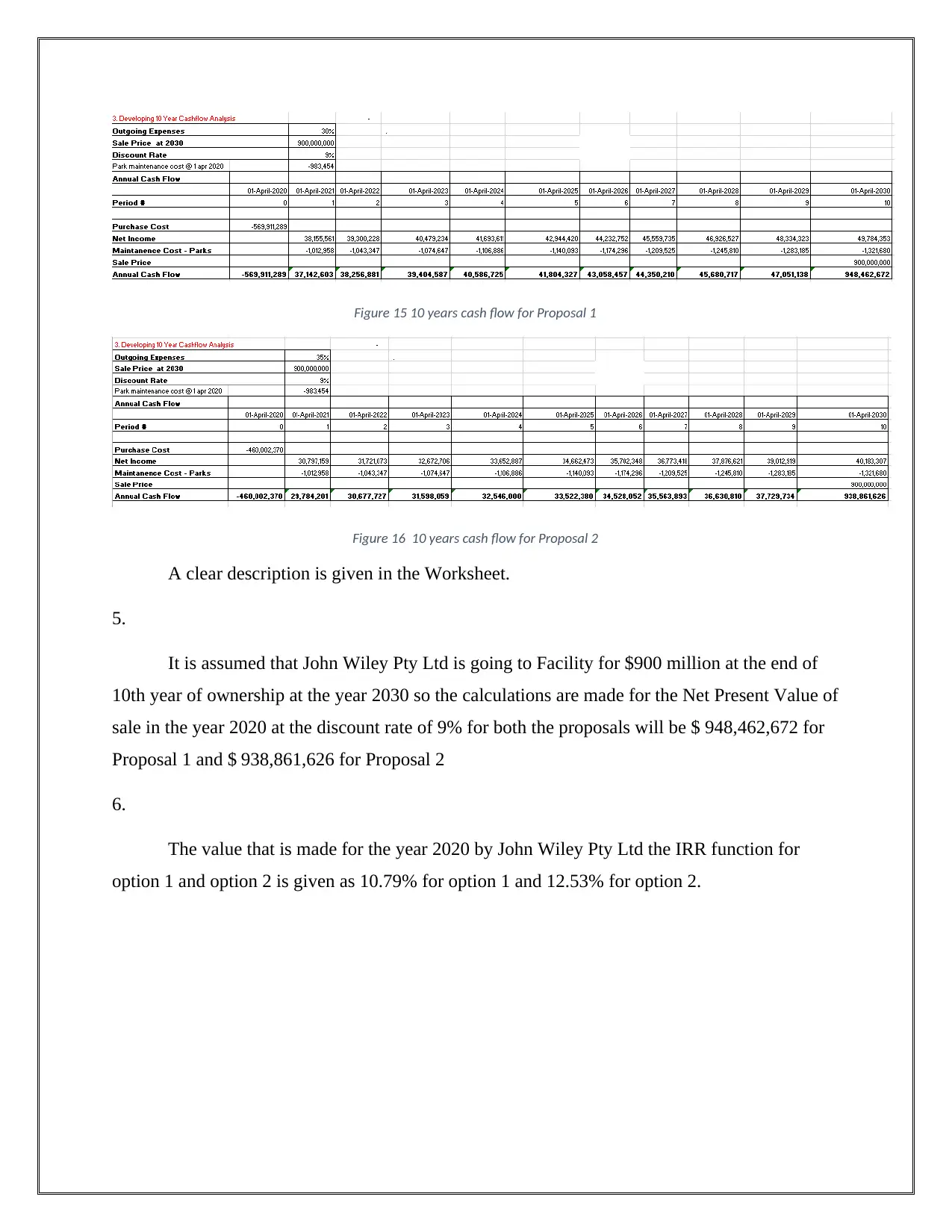

The annual net cash flow for 10 years for both the Proposals is gives as

Figure 15 10 years cash flow for Proposal 1

Figure 16 10 years cash flow for Proposal 2

A clear description is given in the Worksheet.

5.

It is assumed that John Wiley Pty Ltd is going to Facility for $900 million at the end of

10th year of ownership at the year 2030 so the calculations are made for the Net Present Value of

sale in the year 2020 at the discount rate of 9% for both the proposals will be $ 948,462,672 for

Proposal 1 and $ 938,861,626 for Proposal 2

6.

The value that is made for the year 2020 by John Wiley Pty Ltd the IRR function for

option 1 and option 2 is given as 10.79% for option 1 and 12.53% for option 2.

Figure 16 10 years cash flow for Proposal 2

A clear description is given in the Worksheet.

5.

It is assumed that John Wiley Pty Ltd is going to Facility for $900 million at the end of

10th year of ownership at the year 2030 so the calculations are made for the Net Present Value of

sale in the year 2020 at the discount rate of 9% for both the proposals will be $ 948,462,672 for

Proposal 1 and $ 938,861,626 for Proposal 2

6.

The value that is made for the year 2020 by John Wiley Pty Ltd the IRR function for

option 1 and option 2 is given as 10.79% for option 1 and 12.53% for option 2.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Part C

Answer

While comparing the two proposals, Proposal 1 is yielding more profitable benefits that

Proposal 2, hence Proposal l is recommended.

Part D

Answer

If the debt equity ratio changes from 80:20 it means that 80% of the funds are contributed

by the lenders and 20% are contributed by the equity shareholders. Then the debt equity ratio is

4:1. In this case the bankers support will not be provided. If the debt equity ratio changes from

50:50 it means that 50% of the funds are contributed by the lenders and 50% are contributed by

the equity shareholders. Then the debt equity ratio is 1:1. This has a good impact.

Part E

Answer

While comparing the two proposals, Proposal 1 is yielding more profitable benefits that

Proposal 2, hence Proposal l is recommended.

Part D

Answer

If the debt equity ratio changes from 80:20 it means that 80% of the funds are contributed

by the lenders and 20% are contributed by the equity shareholders. Then the debt equity ratio is

4:1. In this case the bankers support will not be provided. If the debt equity ratio changes from

50:50 it means that 50% of the funds are contributed by the lenders and 50% are contributed by

the equity shareholders. Then the debt equity ratio is 1:1. This has a good impact.

Part E

Answer

Giving a hazard investigation can significantly diminish the odds of a potential issue or

unanticipated conditions from happening. Considering these dangers will guarantee that the

venture can continue with no strains or misfortunes.

1. Cost of Capital: This variable could totally change the elements of the report

regardless of the possibility that a little sum is changed. Because of unexpected conditions this

cost can without much of a stretch change

2. Profit forecasts: - anticipating benefits is never a beyond any doubt approach to guarantee

that costs will be returned, however exact investigations can assess the income that will be

returned after some time.

3. Yield: The venture yield greatly affects the undertaking as it can demonstrate financial

specialists whether the task is practical or not.

4. Outgoing-During the course of the undertaking there are active money streams which can

significantly influence the basic leadership viewpoints.

5. Fluctuations in Escalation rate: - because of unanticipated conditions, heightening rate may

change contingent upon what type of issue emerges amid the tasks development. An adjustment

in heightening rate will modify the whole cost of the undertaking putting financial specialists at

danger. An investigation has been done to predict the qualities if this somehow managed to

happen as found in the bug graph.

2.

Giving a hazard investigation can significantly diminish the odds of a potential issue or

unanticipated conditions from happening. Considering these dangers will guarantee that the

venture can continue with no strains or misfortunes.

1. Cost of Capital: This variable could totally change the elements of the report

regardless of the possibility that a little sum is changed. Because of unexpected conditions this

cost can without much of a stretch change

2. Profit forecasts: - anticipating benefits is never a beyond any doubt approach to guarantee

that costs will be returned, however exact investigations can assess the income that will be

returned after some time.

3. Yield: The venture yield greatly affects the undertaking as it can demonstrate financial

specialists whether the task is practical or not.

4. Outgoing-During the course of the undertaking there are active money streams which can

significantly influence the basic leadership viewpoints.

5. Fluctuations in Escalation rate: - because of unanticipated conditions, heightening rate may

change contingent upon what type of issue emerges amid the tasks development. An adjustment

in heightening rate will modify the whole cost of the undertaking putting financial specialists at

danger. An investigation has been done to predict the qualities if this somehow managed to

happen as found in the bug graph.

2.

Three Risk Areas for Future Evaluation

1. Cost of Capital

2. Outgoing

3. Escalation rate

The motivation to additionally explore these hazard zones for what's to come are essentially

in light of the fact that we have arrived at a conclusion that these dangers can impact the

undertaking the most through even the littlest change. So we have chosen that with legitimate

research and assessment of these dangers we can outfit ourselves with the vital instruments to

battle any negative effects that they make on the undertaking. (Kubba, 2010).

1. Cost of Capital

2. Outgoing

3. Escalation rate

The motivation to additionally explore these hazard zones for what's to come are essentially

in light of the fact that we have arrived at a conclusion that these dangers can impact the

undertaking the most through even the littlest change. So we have chosen that with legitimate

research and assessment of these dangers we can outfit ourselves with the vital instruments to

battle any negative effects that they make on the undertaking. (Kubba, 2010).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

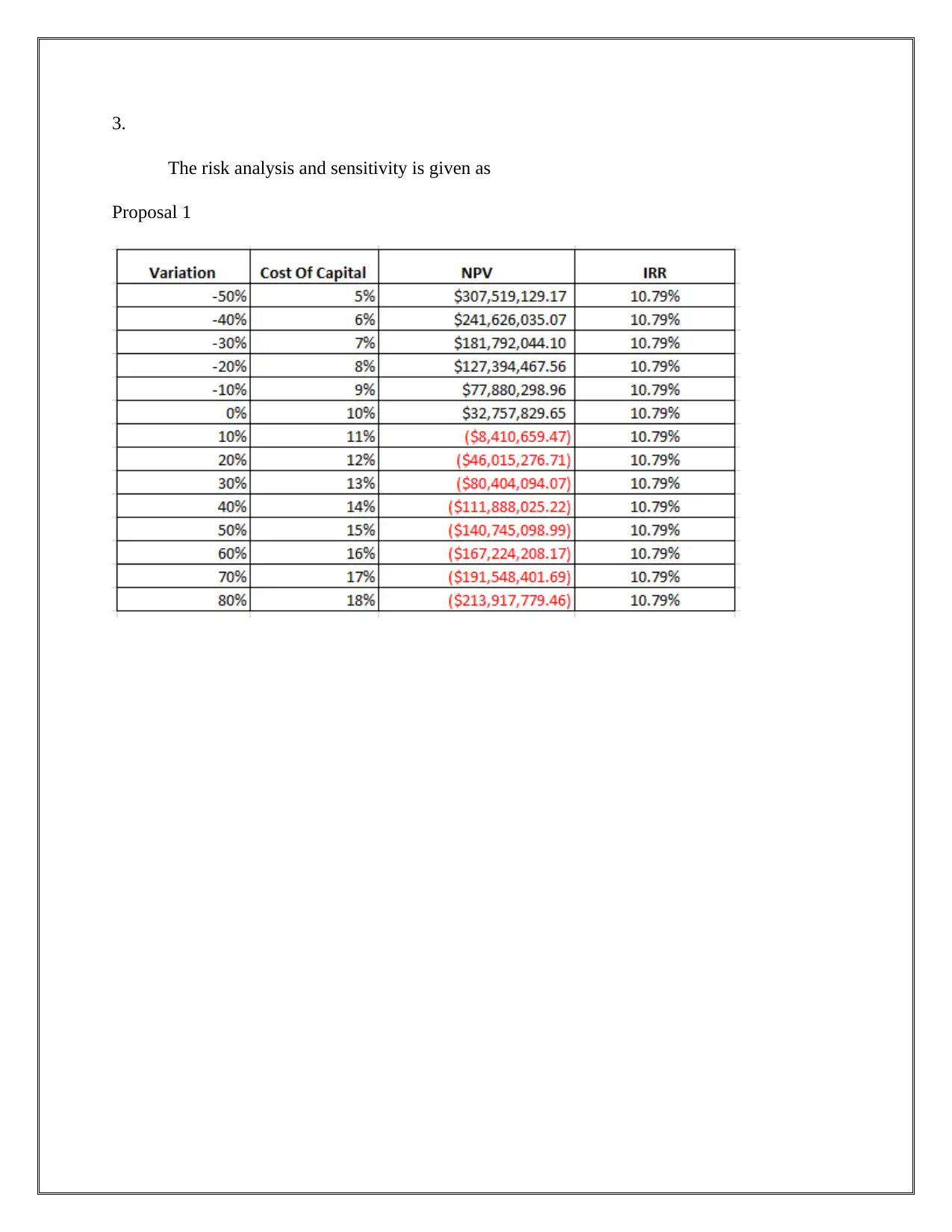

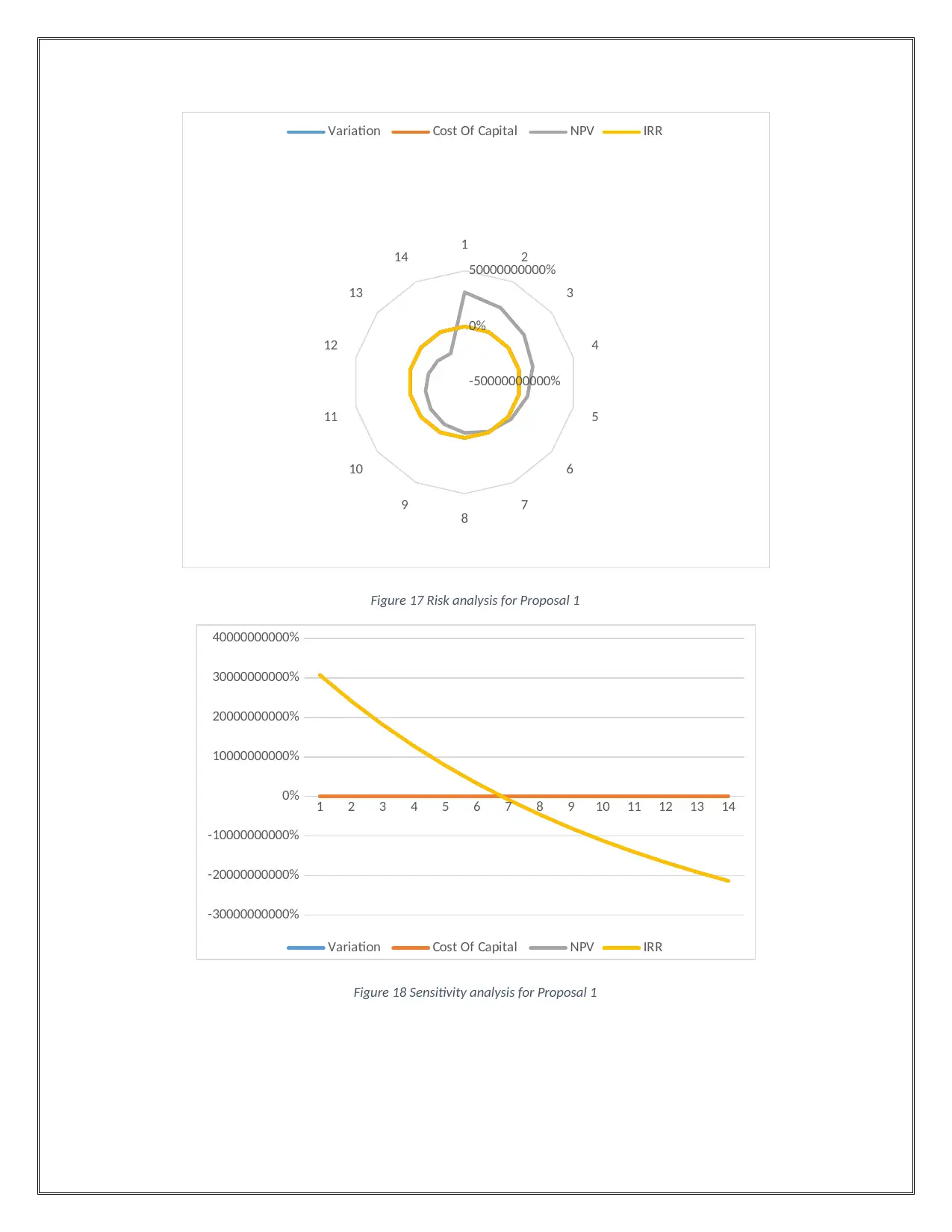

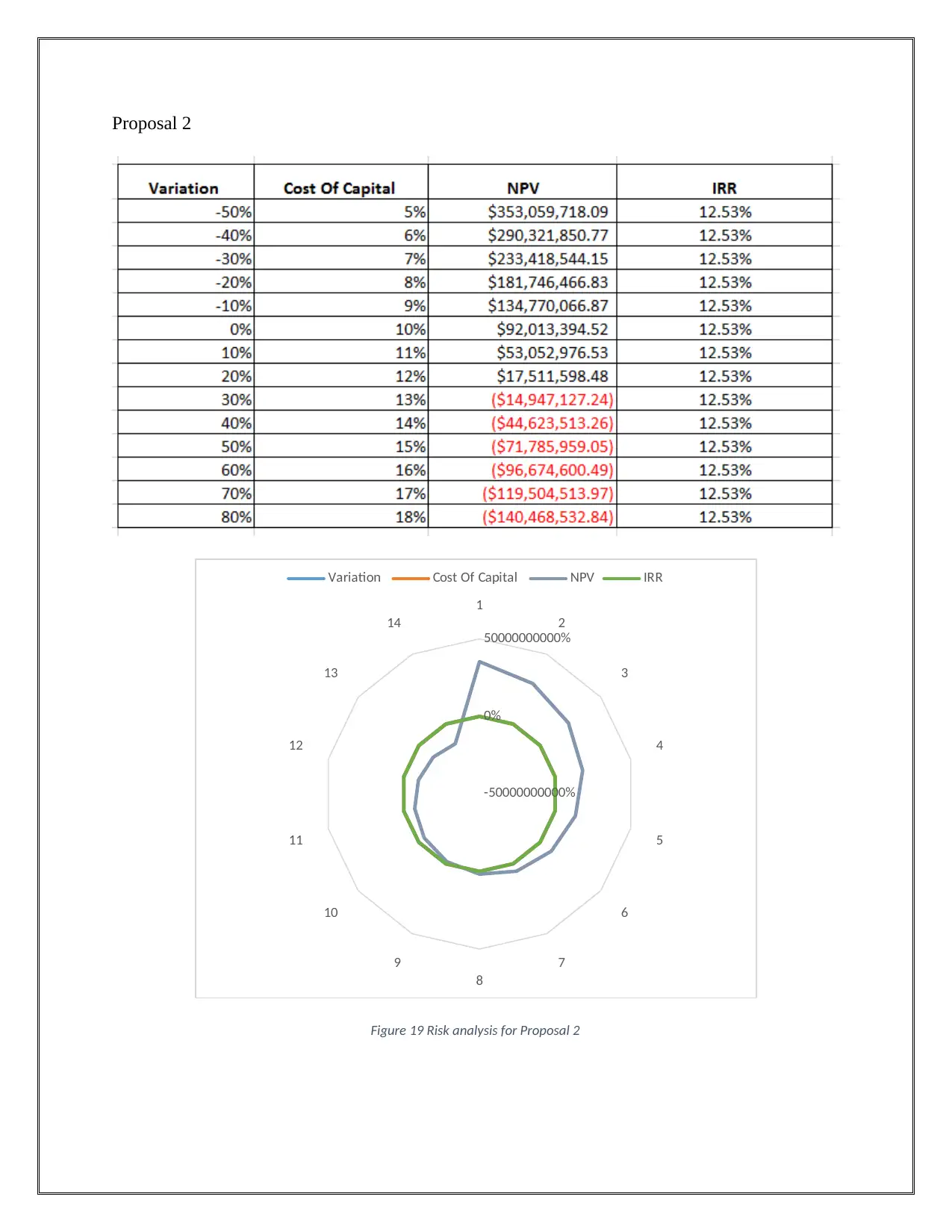

3.

The risk analysis and sensitivity is given as

Proposal 1

The risk analysis and sensitivity is given as

Proposal 1

1 2

3

4

5

6

7

8

9

10

11

12

13

14

-50000000000%

0%

50000000000%

Variation Cost Of Capital NPV IRR

Figure 17 Risk analysis for Proposal 1

1 2 3 4 5 6 7 8 9 10 11 12 13 14

-30000000000%

-20000000000%

-10000000000%

0%

10000000000%

20000000000%

30000000000%

40000000000%

Variation Cost Of Capital NPV IRR

Figure 18 Sensitivity analysis for Proposal 1

3

4

5

6

7

8

9

10

11

12

13

14

-50000000000%

0%

50000000000%

Variation Cost Of Capital NPV IRR

Figure 17 Risk analysis for Proposal 1

1 2 3 4 5 6 7 8 9 10 11 12 13 14

-30000000000%

-20000000000%

-10000000000%

0%

10000000000%

20000000000%

30000000000%

40000000000%

Variation Cost Of Capital NPV IRR

Figure 18 Sensitivity analysis for Proposal 1

Proposal 2

1

2

3

4

5

6

7

8

9

10

11

12

13

14

-50000000000%

0%

50000000000%

Variation Cost Of Capital NPV IRR

Figure 19 Risk analysis for Proposal 2

1

2

3

4

5

6

7

8

9

10

11

12

13

14

-50000000000%

0%

50000000000%

Variation Cost Of Capital NPV IRR

Figure 19 Risk analysis for Proposal 2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1 2 3 4 5 6 7 8 9 10 11 12 13 14

-20000000000%

-10000000000%

0%

10000000000%

20000000000%

30000000000%

40000000000%

Variation Cost Of Capital NPV IRR

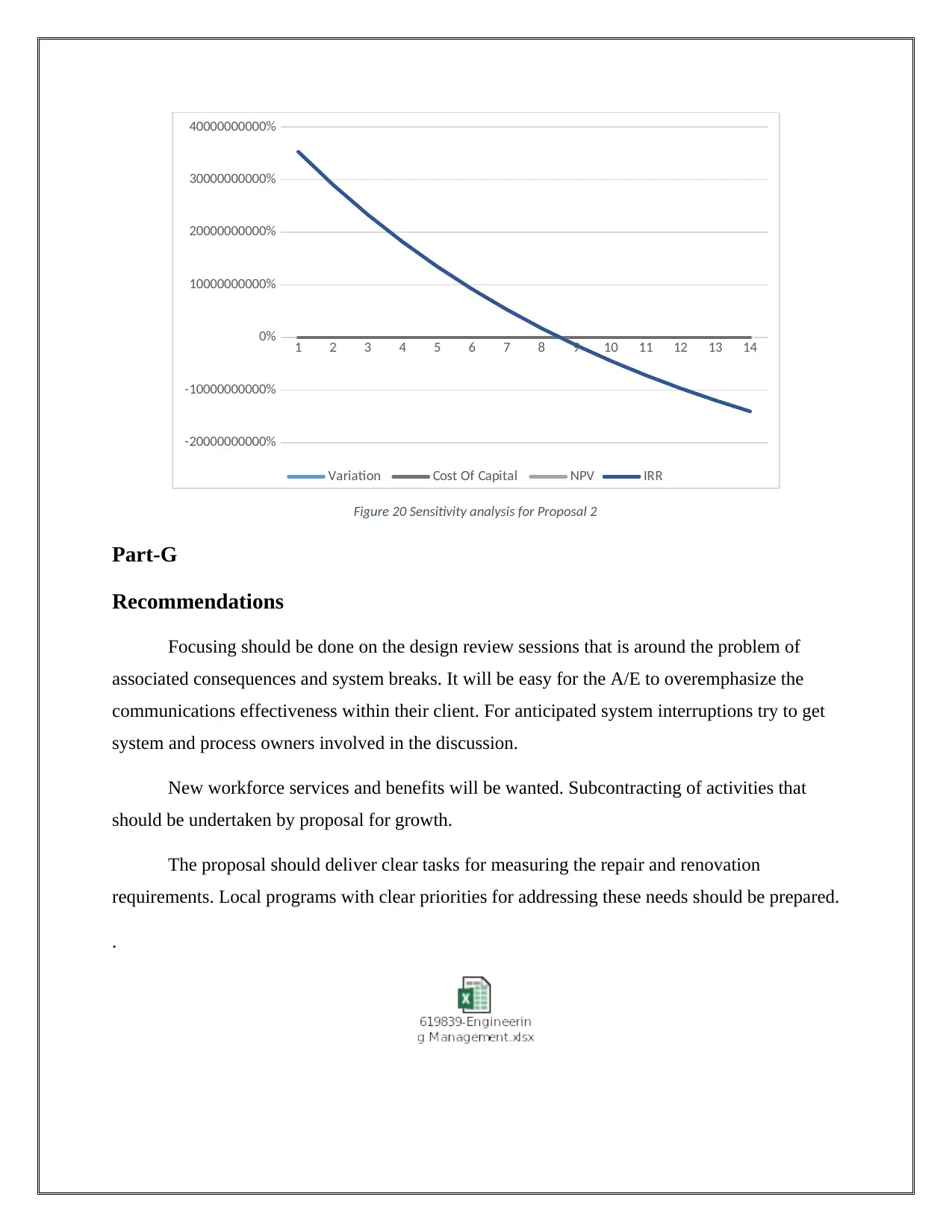

Figure 20 Sensitivity analysis for Proposal 2

Part-G

Recommendations

Focusing should be done on the design review sessions that is around the problem of

associated consequences and system breaks. It will be easy for the A/E to overemphasize the

communications effectiveness within their client. For anticipated system interruptions try to get

system and process owners involved in the discussion.

New workforce services and benefits will be wanted. Subcontracting of activities that

should be undertaken by proposal for growth.

The proposal should deliver clear tasks for measuring the repair and renovation

requirements. Local programs with clear priorities for addressing these needs should be prepared.

.

-20000000000%

-10000000000%

0%

10000000000%

20000000000%

30000000000%

40000000000%

Variation Cost Of Capital NPV IRR

Figure 20 Sensitivity analysis for Proposal 2

Part-G

Recommendations

Focusing should be done on the design review sessions that is around the problem of

associated consequences and system breaks. It will be easy for the A/E to overemphasize the

communications effectiveness within their client. For anticipated system interruptions try to get

system and process owners involved in the discussion.

New workforce services and benefits will be wanted. Subcontracting of activities that

should be undertaken by proposal for growth.

The proposal should deliver clear tasks for measuring the repair and renovation

requirements. Local programs with clear priorities for addressing these needs should be prepared.

.

References

Kim, D. and Chi, S. (2015). Causes of Schedule Delays in Building Construction

Projects in Vanuatu. Journal of the Korea Institute of Building Construction,

15(6), pp.641-651.

Kubba, S. (2010). Green construction project management and cost oversight.

Amsterdam: Elsevier/Architectural Press.

Kim, D. and Chi, S. (2015). Causes of Schedule Delays in Building Construction

Projects in Vanuatu. Journal of the Korea Institute of Building Construction,

15(6), pp.641-651.

Kubba, S. (2010). Green construction project management and cost oversight.

Amsterdam: Elsevier/Architectural Press.

1 out of 27

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.