Enhanced Auditor Reporting Embraced in Australia: A Rio Tinto Analysis

VerifiedAdded on 2021/01/02

|14

|3180

|201

Report

AI Summary

This report examines the adoption of enhanced auditor reporting standards in Australia through a case study of Rio Tinto Limited. It provides an overview of audit reporting, including the analysis of financial statements and the role of auditors. The report delves into key aspects such as the auditor's independence declaration, the independent auditor's report, non-audit services, key audit matters, the audit committee's functions, and audit opinions. It also discusses the diversification of responsibilities between auditors and directors, material subsequent events, and the evaluation of assurance services. The analysis includes the examination of auditor remuneration, key audit matters like impairment assessments and provisions, and the audit opinion issued by both PrincewaterhouseCoopers LLP and PrincewaterhouseCoopers. The report also covers the responsibilities of directors in preparing financial statements and the application of International Financial Reporting Standards (IFRS) within the context of Australian auditing regulations. This comprehensive analysis aims to provide insights into how enhanced auditor reporting is implemented and its implications for listed companies in Australia.

How is Enhanced Auditor

Reporting being embraced in

Australia? Background and

Context

Reporting being embraced in

Australia? Background and

Context

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

This project report is summarises that auditing is a concept which

helps in investigating the accuracy of the financial statements of an

organisation. RIO TINTO limited is an organisation which is listed on

Australian stock exchange is chosen in order to better understand the topic

of auditing. Audit report and opinions provided by its subsidiary and external

auditor Prince waterhouse Coopers are analysed and interpreted in order to

ascertain various issues regarding the process of auditing.

This project report is summarises that auditing is a concept which

helps in investigating the accuracy of the financial statements of an

organisation. RIO TINTO limited is an organisation which is listed on

Australian stock exchange is chosen in order to better understand the topic

of auditing. Audit report and opinions provided by its subsidiary and external

auditor Prince waterhouse Coopers are analysed and interpreted in order to

ascertain various issues regarding the process of auditing.

Table of Contents

EXECUTIVE SUMMARY.............................................................................................................2

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

Commentary on Revised auditing reporting standards..........................................................1

Auditor’s Independence Declaration......................................................................................2

Independent auditor’s report...................................................................................................3

Non-Audit services performed by the Auditor.......................................................................3

Key Audit Matters..................................................................................................................4

Audit Committee and its role, functions and composition ....................................................5

Audit opinion..........................................................................................................................5

Diversification between the auditors and Directors responsibilities......................................7

Material subsequent events and elements evaluated by auditors...........................................7

Evaluation of auditor’s assurance services performed for the client company......................8

Follow up questions asked to auditors in AGM.....................................................................8

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

EXECUTIVE SUMMARY.............................................................................................................2

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

Commentary on Revised auditing reporting standards..........................................................1

Auditor’s Independence Declaration......................................................................................2

Independent auditor’s report...................................................................................................3

Non-Audit services performed by the Auditor.......................................................................3

Key Audit Matters..................................................................................................................4

Audit Committee and its role, functions and composition ....................................................5

Audit opinion..........................................................................................................................5

Diversification between the auditors and Directors responsibilities......................................7

Material subsequent events and elements evaluated by auditors...........................................7

Evaluation of auditor’s assurance services performed for the client company......................8

Follow up questions asked to auditors in AGM.....................................................................8

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Audit reporting plays vital role in management reporting and decision

making. Auditing standards are reformed and changed time to time to

improve the quality and control of auditing for listed organisations and

entities. This report defines the concept of audit reporting standard that how

these standards are adopted by auditors in Australia (Pittock, Hussey and

McGlennon, 2013). Evaluation of audit report of Rio Tinto Limited that is a

material industry supplies raw material for manufacturing cars, mobiles,

planes, material for building hospitals and houses. There are type of

elements analysed by evaluating the financial reports of company as

Auditor's independence declaration, Key audit matters, non Audit services

performed performed by auditors, Auditor's remuneration, functions and

roles of audit committee, independent auditors reports to the member and

review of all key audit matters with auditing procedures.

MAIN BODY

Commentary on Revised auditing reporting standards

Audit reporting is process contains entire evaluation of main Financial

data, assessment of material errors, auxiliary reports and measures taken

after by entity. The necessity of audit reporting for the most part connected

with improving the extension and expanding the congeniality of Auditors of

company. As indicated by independent declaration under section 307c of

Corporations act 2001, a review or survey must be directed of the Financial

reports for an organization for the financial year or half yearly basis (Oliver,

Vesty and Brooks, 2016). Primary aim of the alterations and changes was to

enhance the qualities and upgrade significance of the Auditor's report

through update under ISA (International standard on Auditing).

A presentation in composed that represents the combined financial

reports are evaluated by individual auditor. Further more, there is no any

contradictions of auditors reports as prerequisites of this demonstration

identified with review or survey and no contradictions of any material code of

1

Audit reporting plays vital role in management reporting and decision

making. Auditing standards are reformed and changed time to time to

improve the quality and control of auditing for listed organisations and

entities. This report defines the concept of audit reporting standard that how

these standards are adopted by auditors in Australia (Pittock, Hussey and

McGlennon, 2013). Evaluation of audit report of Rio Tinto Limited that is a

material industry supplies raw material for manufacturing cars, mobiles,

planes, material for building hospitals and houses. There are type of

elements analysed by evaluating the financial reports of company as

Auditor's independence declaration, Key audit matters, non Audit services

performed performed by auditors, Auditor's remuneration, functions and

roles of audit committee, independent auditors reports to the member and

review of all key audit matters with auditing procedures.

MAIN BODY

Commentary on Revised auditing reporting standards

Audit reporting is process contains entire evaluation of main Financial

data, assessment of material errors, auxiliary reports and measures taken

after by entity. The necessity of audit reporting for the most part connected

with improving the extension and expanding the congeniality of Auditors of

company. As indicated by independent declaration under section 307c of

Corporations act 2001, a review or survey must be directed of the Financial

reports for an organization for the financial year or half yearly basis (Oliver,

Vesty and Brooks, 2016). Primary aim of the alterations and changes was to

enhance the qualities and upgrade significance of the Auditor's report

through update under ISA (International standard on Auditing).

A presentation in composed that represents the combined financial

reports are evaluated by individual auditor. Further more, there is no any

contradictions of auditors reports as prerequisites of this demonstration

identified with review or survey and no contradictions of any material code of

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

expert lead in connection to the review or survey (Jones, 2017). Presentation

either should be given when the review report is given to managers ,enlisted

conspire and revealing element, or must fulfill the states of subsection 5(a),

additionally should be marked by the individual making the presentation.

Alterations subject to change the structure of national money related

announcing principles and rules to guarantee the key normal content with

fitting correspondence and reviewing are considered in this setting. The new

examining rules was acquainted subject with help the speculators and

partners. Sufficient changes to decide the correct money related

articulations and the data related with administration considered in

inspecting announcing norms and related accommodating corrections

(Caust, 2015).

Review and analysis of annual report of Rio Tinto limited

Annual report of company is given subejct to analyse the real position

and essential aspect associated with determining the key information

associated to audit reports.

Auditor’s Independence Declaration

An auditor's independence declaration shows the concent and

declaration of auditors that they have audited the reports adequate manner.

Leading auditors subject to audit of Rio Tinto Limited for the year ended

2017, declare that they have been

a) No dispute and conflicts occurs while analysing the independence

requirements as per the corporation act 2001 related to the audit and

b) There was no Dispute and conflicts found regarding implying the code of

professional conduct relation to the audit.

The declaration was made in respect of Rio Tinto and its subsidiary

entities to for better control in a particular financial period. The report was

controlled by the debbie smith and the partner price Waterhouse cooper that

is a liability limited by a scheme approved under professional standard

legislations.

2

either should be given when the review report is given to managers ,enlisted

conspire and revealing element, or must fulfill the states of subsection 5(a),

additionally should be marked by the individual making the presentation.

Alterations subject to change the structure of national money related

announcing principles and rules to guarantee the key normal content with

fitting correspondence and reviewing are considered in this setting. The new

examining rules was acquainted subject with help the speculators and

partners. Sufficient changes to decide the correct money related

articulations and the data related with administration considered in

inspecting announcing norms and related accommodating corrections

(Caust, 2015).

Review and analysis of annual report of Rio Tinto limited

Annual report of company is given subejct to analyse the real position

and essential aspect associated with determining the key information

associated to audit reports.

Auditor’s Independence Declaration

An auditor's independence declaration shows the concent and

declaration of auditors that they have audited the reports adequate manner.

Leading auditors subject to audit of Rio Tinto Limited for the year ended

2017, declare that they have been

a) No dispute and conflicts occurs while analysing the independence

requirements as per the corporation act 2001 related to the audit and

b) There was no Dispute and conflicts found regarding implying the code of

professional conduct relation to the audit.

The declaration was made in respect of Rio Tinto and its subsidiary

entities to for better control in a particular financial period. The report was

controlled by the debbie smith and the partner price Waterhouse cooper that

is a liability limited by a scheme approved under professional standard

legislations.

2

Independent auditor’s report

The price-water house coopers LLP giving opinion on the financial statements of the

members of Rio Tinto Plc

On 31 December 2017 the financial statement define as a true and fair view of Rio's

tinto affairs and the group in the year ended group's profit and cash flows.

On the behalf of international financial reporting standards prepared group's financial

statement by the European union

In accordance with united kingdom generally accounting practice prepared Rio Tinto Plc

financial statement

It is considered that the financial statements are consolidated with effect of relevant

rules and legislation related to European union. There are type of accounting rules and

objectives are evaluated with effect of GAAP and IFRS (Annual report of RIO TINTO

Limted, 2017).

Financial statement also prepare according to requirements of the companies act 2006

the audit reporting structure and the international accordance with IFRS and the

reformed rules of 2016/17.

Non-Audit services performed by the Auditor

Role of non- auditing services was also found subject to audit of non

financial services. It is required to analyse the occasionally events and

transactions while considering the knowledge and facts. The efficient use of

auditing reports and evaluation of different type of financial records were

undertaken to simply the information and utile the auditing standards.

Safeguards and legislations were followed by external auditors for managing

the management (Armstrong, Brown and Smith, 2014).

There are type of transactions was made in terms of assessing the

audit program as managing the flow of operations and management. Setting

the criteria of audit for financial and non financial transactions.

3

The price-water house coopers LLP giving opinion on the financial statements of the

members of Rio Tinto Plc

On 31 December 2017 the financial statement define as a true and fair view of Rio's

tinto affairs and the group in the year ended group's profit and cash flows.

On the behalf of international financial reporting standards prepared group's financial

statement by the European union

In accordance with united kingdom generally accounting practice prepared Rio Tinto Plc

financial statement

It is considered that the financial statements are consolidated with effect of relevant

rules and legislation related to European union. There are type of accounting rules and

objectives are evaluated with effect of GAAP and IFRS (Annual report of RIO TINTO

Limted, 2017).

Financial statement also prepare according to requirements of the companies act 2006

the audit reporting structure and the international accordance with IFRS and the

reformed rules of 2016/17.

Non-Audit services performed by the Auditor

Role of non- auditing services was also found subject to audit of non

financial services. It is required to analyse the occasionally events and

transactions while considering the knowledge and facts. The efficient use of

auditing reports and evaluation of different type of financial records were

undertaken to simply the information and utile the auditing standards.

Safeguards and legislations were followed by external auditors for managing

the management (Armstrong, Brown and Smith, 2014).

There are type of transactions was made in terms of assessing the

audit program as managing the flow of operations and management. Setting

the criteria of audit for financial and non financial transactions.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

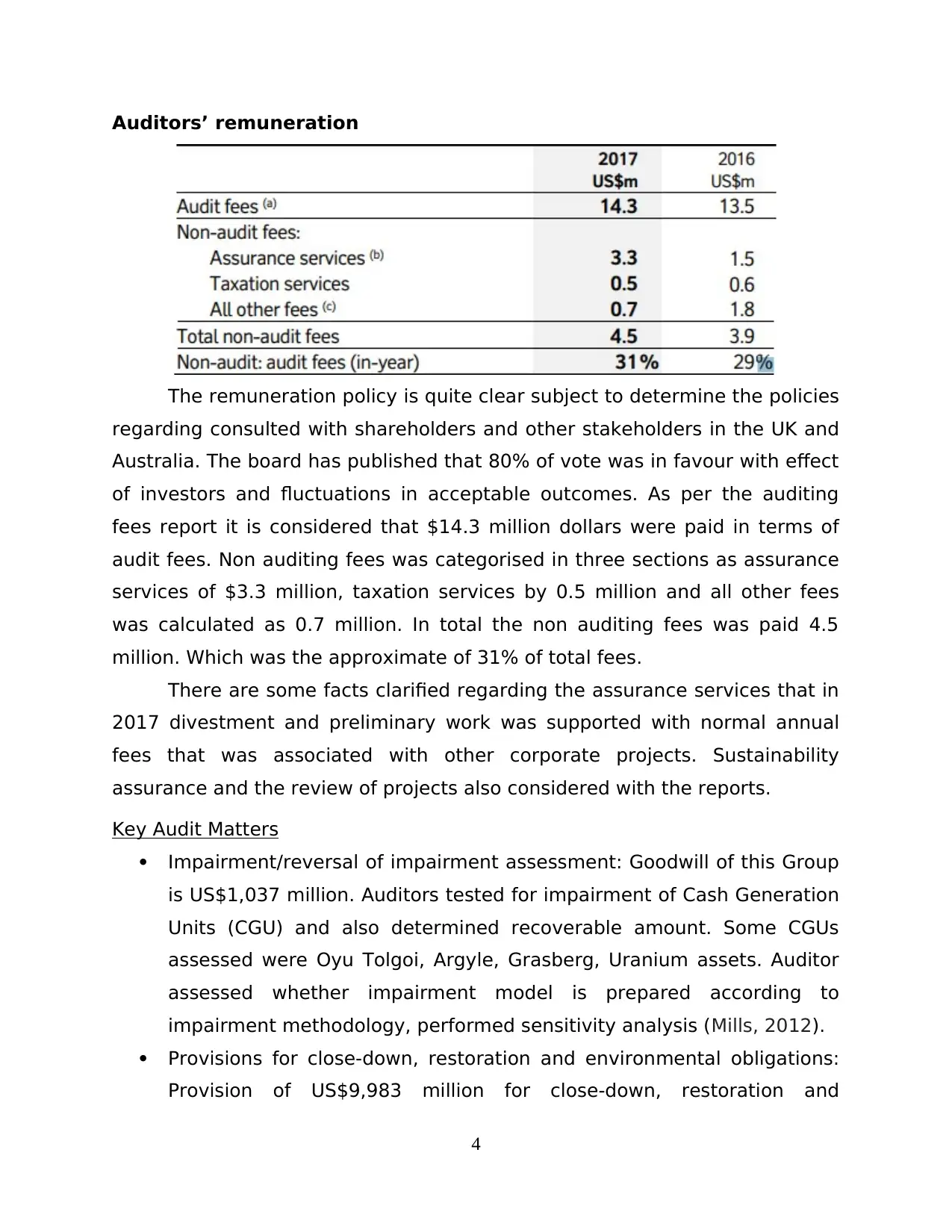

Auditors’ remuneration

The remuneration policy is quite clear subject to determine the policies

regarding consulted with shareholders and other stakeholders in the UK and

Australia. The board has published that 80% of vote was in favour with effect

of investors and fluctuations in acceptable outcomes. As per the auditing

fees report it is considered that $14.3 million dollars were paid in terms of

audit fees. Non auditing fees was categorised in three sections as assurance

services of $3.3 million, taxation services by 0.5 million and all other fees

was calculated as 0.7 million. In total the non auditing fees was paid 4.5

million. Which was the approximate of 31% of total fees.

There are some facts clarified regarding the assurance services that in

2017 divestment and preliminary work was supported with normal annual

fees that was associated with other corporate projects. Sustainability

assurance and the review of projects also considered with the reports.

Key Audit Matters

Impairment/reversal of impairment assessment: Goodwill of this Group

is US$1,037 million. Auditors tested for impairment of Cash Generation

Units (CGU) and also determined recoverable amount. Some CGUs

assessed were Oyu Tolgoi, Argyle, Grasberg, Uranium assets. Auditor

assessed whether impairment model is prepared according to

impairment methodology, performed sensitivity analysis (Mills, 2012).

Provisions for close-down, restoration and environmental obligations:

Provision of US$9,983 million for close-down, restoration and

4

The remuneration policy is quite clear subject to determine the policies

regarding consulted with shareholders and other stakeholders in the UK and

Australia. The board has published that 80% of vote was in favour with effect

of investors and fluctuations in acceptable outcomes. As per the auditing

fees report it is considered that $14.3 million dollars were paid in terms of

audit fees. Non auditing fees was categorised in three sections as assurance

services of $3.3 million, taxation services by 0.5 million and all other fees

was calculated as 0.7 million. In total the non auditing fees was paid 4.5

million. Which was the approximate of 31% of total fees.

There are some facts clarified regarding the assurance services that in

2017 divestment and preliminary work was supported with normal annual

fees that was associated with other corporate projects. Sustainability

assurance and the review of projects also considered with the reports.

Key Audit Matters

Impairment/reversal of impairment assessment: Goodwill of this Group

is US$1,037 million. Auditors tested for impairment of Cash Generation

Units (CGU) and also determined recoverable amount. Some CGUs

assessed were Oyu Tolgoi, Argyle, Grasberg, Uranium assets. Auditor

assessed whether impairment model is prepared according to

impairment methodology, performed sensitivity analysis (Mills, 2012).

Provisions for close-down, restoration and environmental obligations:

Provision of US$9,983 million for close-down, restoration and

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

environmental obligations has been maintained by the Group. Auditors

tested objectivity of cos estimates, checked mathematical accuracy,

consistency of provisions relating to close-down, restoration and

environmental obligations.

Provisions for uncertain tax positions: The Group has current and non-

current taxes payable of about US$2,248 million.

Review all Key Audit Matters noted and the associated audit

procedures

There are two separate opinions of auditors for the company. Prince

waterhouse Coopers LLP give opinion on the financial statements of Rio Tinto

plc and PrincewaterhouseCoopers to the members of Rio Tinto Limited.

Group financial statements are prepared for Rio Tinto plc and Rio Tinto

Limited as parent companies and their subsidiaries (Tepalagul and Lin,

2015).

Audit Committee and its role, functions and composition

Audit committee of Rio Tinto Limited contains the criteria of evaluation,

control and management of audit program. This committee keep changes as

on specific financial period (Whitaker, 2013). The committee contain the

board members, internal and external auditors and subsidiary group

partners. There are five main members are the part of audit committee of

company as Ann Godbehere (Chairman), Paul Tellier, Simon Henry, Simon

Thompson, John Varley and Robert Brown.

Key functions of Audit Committee

The committee mainly assist managers to assess the main objective of

organisation to correlate the functions. The key responsibilities contains;

Integrity policy of financial reporting process and providing

recommendations regarding financial statements and reports.

Management of risk and fractionate the activities of the audit report.

Internal control and financial reports consolidation for internal audit

program

5

tested objectivity of cos estimates, checked mathematical accuracy,

consistency of provisions relating to close-down, restoration and

environmental obligations.

Provisions for uncertain tax positions: The Group has current and non-

current taxes payable of about US$2,248 million.

Review all Key Audit Matters noted and the associated audit

procedures

There are two separate opinions of auditors for the company. Prince

waterhouse Coopers LLP give opinion on the financial statements of Rio Tinto

plc and PrincewaterhouseCoopers to the members of Rio Tinto Limited.

Group financial statements are prepared for Rio Tinto plc and Rio Tinto

Limited as parent companies and their subsidiaries (Tepalagul and Lin,

2015).

Audit Committee and its role, functions and composition

Audit committee of Rio Tinto Limited contains the criteria of evaluation,

control and management of audit program. This committee keep changes as

on specific financial period (Whitaker, 2013). The committee contain the

board members, internal and external auditors and subsidiary group

partners. There are five main members are the part of audit committee of

company as Ann Godbehere (Chairman), Paul Tellier, Simon Henry, Simon

Thompson, John Varley and Robert Brown.

Key functions of Audit Committee

The committee mainly assist managers to assess the main objective of

organisation to correlate the functions. The key responsibilities contains;

Integrity policy of financial reporting process and providing

recommendations regarding financial statements and reports.

Management of risk and fractionate the activities of the audit report.

Internal control and financial reports consolidation for internal audit

program

5

Managing the flow of information among internal and external

auditors.

Granting access to internal and external auditors to access audit

records.

Audit opinion

Separate opinion

The group applying IFRS adopted as the European union and issued by the IASB

(Fiolleau and et. al ., 2013). The separate opinion contains the financial statements of

determining the policies and plans with applied rules and legislation under IASB. The other

ethical responsibilities subject to separate opinion measured as APES 110.

Opinion on the financial report

it is considered that the financial reports mainly assisted to advise rules and policies

according to Corporation Act 2001 (Knechel and Salterio, 2016). the corporations act

2001 has accompanying the financial report define below:

As per the annual report the opinion reading financial statements presents fair and clear

view of the group of financial position as on 31st December 2017.

The rules are complied in respect of understanding the Australian Standards and as per

the corporation regulation act 2001.

Basis of opinion

Australian auditing rules and standards on auditing, ISA and IASB rules

are determined in respect of standards are further described with audit

responsibilities. Auditor's responsibilities for the audit financial statements

are compressed with audit evidence and explanatory reports. The subsidiary

documents and evidences are also considered to explain the financial

records (Yates and et. al., 2016).

Opinion of PrincewaterhouseCoopers LLP to Rio Tinto plc:

Financial statements are prepared in accordance with IFRS

(International Financial Reporting Standards) by European Union and also

applied IFRSs issued by IASB(International Accounting Standards Boards),

6

auditors.

Granting access to internal and external auditors to access audit

records.

Audit opinion

Separate opinion

The group applying IFRS adopted as the European union and issued by the IASB

(Fiolleau and et. al ., 2013). The separate opinion contains the financial statements of

determining the policies and plans with applied rules and legislation under IASB. The other

ethical responsibilities subject to separate opinion measured as APES 110.

Opinion on the financial report

it is considered that the financial reports mainly assisted to advise rules and policies

according to Corporation Act 2001 (Knechel and Salterio, 2016). the corporations act

2001 has accompanying the financial report define below:

As per the annual report the opinion reading financial statements presents fair and clear

view of the group of financial position as on 31st December 2017.

The rules are complied in respect of understanding the Australian Standards and as per

the corporation regulation act 2001.

Basis of opinion

Australian auditing rules and standards on auditing, ISA and IASB rules

are determined in respect of standards are further described with audit

responsibilities. Auditor's responsibilities for the audit financial statements

are compressed with audit evidence and explanatory reports. The subsidiary

documents and evidences are also considered to explain the financial

records (Yates and et. al., 2016).

Opinion of PrincewaterhouseCoopers LLP to Rio Tinto plc:

Financial statements are prepared in accordance with IFRS

(International Financial Reporting Standards) by European Union and also

applied IFRSs issued by IASB(International Accounting Standards Boards),

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

United Kingdom Generally Accepted Accounting Principles, Companies Act

2006 , also they give a true and fair view of financial position.

Opinion of Prince waterhouse Coopers to Rio Tinto Limited:

Financial Reports are made according to Corporations Act 2001 and

also showing true and fair view of financial position for the year ended 31

December 2017 following Australian Accounting Standards and Corporations

Regulations 2001.

They audited Director's Remuneration Report, Group cash flow statements,

changes in equity, significant accounting policies.

Independence:

Both Prince Waterhouse Coopers LLP and Prince waterhouse Coopers,

as independent auditors fulfilled their ethical responsibilities in accordance

with FRC's Ethical Standard. And they did not provided non-audit services to

the Group.

Audit approach:

Group of Rio Tinto plc engaged in production activities of minerals and

metal exploration. Materiality of overall Group is US$350 million (2016:

US$275 million) and of Rio Tinto plc is US$ 325 million (2016: US$250

million). There are 49 business units of this Group and done special audit of

Pilbara business unit due to its financial significance. Key audit matters are

those which are most important in financial statements and financial

reports. Audit report is mainly focussed on assessing risks of material

misstatements.

Diversification between the auditors and Directors responsibilities

Responsibilities of Director

They are responsible for preparing financial statements and reports on

the basis of financial statements frameworks.

It is essential for director to possess internal control while preparing

financial statements and reports.

7

2006 , also they give a true and fair view of financial position.

Opinion of Prince waterhouse Coopers to Rio Tinto Limited:

Financial Reports are made according to Corporations Act 2001 and

also showing true and fair view of financial position for the year ended 31

December 2017 following Australian Accounting Standards and Corporations

Regulations 2001.

They audited Director's Remuneration Report, Group cash flow statements,

changes in equity, significant accounting policies.

Independence:

Both Prince Waterhouse Coopers LLP and Prince waterhouse Coopers,

as independent auditors fulfilled their ethical responsibilities in accordance

with FRC's Ethical Standard. And they did not provided non-audit services to

the Group.

Audit approach:

Group of Rio Tinto plc engaged in production activities of minerals and

metal exploration. Materiality of overall Group is US$350 million (2016:

US$275 million) and of Rio Tinto plc is US$ 325 million (2016: US$250

million). There are 49 business units of this Group and done special audit of

Pilbara business unit due to its financial significance. Key audit matters are

those which are most important in financial statements and financial

reports. Audit report is mainly focussed on assessing risks of material

misstatements.

Diversification between the auditors and Directors responsibilities

Responsibilities of Director

They are responsible for preparing financial statements and reports on

the basis of financial statements frameworks.

It is essential for director to possess internal control while preparing

financial statements and reports.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

They ensure that all the information presented in financial statements

and reports required to be fraud free.

It is the responsibility of director to assess the parent company ability

to continue as going concern.

Auditors responsibilities

They have the responsibility to provide assurance that financial

statements are free from material misstatements

They have the responsibility to provide true and fair opinion through

which decisions are taken by investors

Material subsequent events and elements evaluated by auditors

There are type of factors and elements were audited while preparing the financial

statements of organization. It is audited that the reports of subsidiary and group of Rio Tinto

Limited are disclosed with proper procedure and aspects. The financial reports are prepared for

the year 2017. group of financial statements, comprehensive income statements,c ash floes and

the group segments are considered to elaborate the financial reports of group.

On 31 DEC 2017 financial report for the year ended including that the directors report

and directors remuneration.

The group financial statement including description of the significant accounting policies

and other information.

Rio Tinto plc financial statement include explanatory information and

significant accounting policies description.

Evaluation of auditor’s assurance services performed for the client company

It is analysed that type of figures are considered to assess the internal

program and assurance engagements for revising the financial information.

The internal standard on Assurance engagement 3401 contains the

statements as the complying the independence for ethical requirements for

plans performance and effectively (Ryan and et. al., 2012). Process and

control are considered the capturing the collating and summarised the

performance of reports to the design. Mattes and evaluating the design the

process and control.

8

and reports required to be fraud free.

It is the responsibility of director to assess the parent company ability

to continue as going concern.

Auditors responsibilities

They have the responsibility to provide assurance that financial

statements are free from material misstatements

They have the responsibility to provide true and fair opinion through

which decisions are taken by investors

Material subsequent events and elements evaluated by auditors

There are type of factors and elements were audited while preparing the financial

statements of organization. It is audited that the reports of subsidiary and group of Rio Tinto

Limited are disclosed with proper procedure and aspects. The financial reports are prepared for

the year 2017. group of financial statements, comprehensive income statements,c ash floes and

the group segments are considered to elaborate the financial reports of group.

On 31 DEC 2017 financial report for the year ended including that the directors report

and directors remuneration.

The group financial statement including description of the significant accounting policies

and other information.

Rio Tinto plc financial statement include explanatory information and

significant accounting policies description.

Evaluation of auditor’s assurance services performed for the client company

It is analysed that type of figures are considered to assess the internal

program and assurance engagements for revising the financial information.

The internal standard on Assurance engagement 3401 contains the

statements as the complying the independence for ethical requirements for

plans performance and effectively (Ryan and et. al., 2012). Process and

control are considered the capturing the collating and summarised the

performance of reports to the design. Mattes and evaluating the design the

process and control.

8

Accuracy subject to analyse the injury regarding the accuracy of

classification applied for a samples. Athematic accuracy and sample of

multiple computations were performed with the Green House gas and

emission subject to intensity. Undertaking related to analytical procedures

with performance of data. There are type of commitment to include the

diversities for determining the background and reflect the procedures related

to policies and the availability of resources (Prempeh, Twumas and

Kyeremeh, 2015).

Follow up questions asked to auditors in AGM

Q1 how much share of profits will be proposed for auditors and

directors remuneration?

Q2 Did organisation comply the Australian Auditing standards and

corporate rules 2001 ?

Q3 whether any modified opinion was produced by non auditing

services?

Q4 whether the management committee and department provide

adequate support to auditors?

CONCLUSION

From the above project report, it has been concluded that in order to

enhanced auditor reporting there are various key application are needed

to be taken into account. for this purpose, various auditor independence

declaration as well as report is used in context to the “Rio Tinto Ltd”

is examine effectively. Certain non-audit services are performed through

the auditor point of view are analysed properly. Some other information

such as audit remuneration, role, function and overall composition of

audit committee is also being evaluated clearly provided in this report.

Various key audit matters and its related procedure are used in

accordance with the company to take future decision more profitable in

near future time.

9

classification applied for a samples. Athematic accuracy and sample of

multiple computations were performed with the Green House gas and

emission subject to intensity. Undertaking related to analytical procedures

with performance of data. There are type of commitment to include the

diversities for determining the background and reflect the procedures related

to policies and the availability of resources (Prempeh, Twumas and

Kyeremeh, 2015).

Follow up questions asked to auditors in AGM

Q1 how much share of profits will be proposed for auditors and

directors remuneration?

Q2 Did organisation comply the Australian Auditing standards and

corporate rules 2001 ?

Q3 whether any modified opinion was produced by non auditing

services?

Q4 whether the management committee and department provide

adequate support to auditors?

CONCLUSION

From the above project report, it has been concluded that in order to

enhanced auditor reporting there are various key application are needed

to be taken into account. for this purpose, various auditor independence

declaration as well as report is used in context to the “Rio Tinto Ltd”

is examine effectively. Certain non-audit services are performed through

the auditor point of view are analysed properly. Some other information

such as audit remuneration, role, function and overall composition of

audit committee is also being evaluated clearly provided in this report.

Various key audit matters and its related procedure are used in

accordance with the company to take future decision more profitable in

near future time.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.