Enron: Analysis of downfall and IFRS vs US GAAP comparison

VerifiedAdded on 2023/06/06

|10

|2696

|395

AI Summary

This article provides an analysis of the downfall of Enron and a comparison between IFRS and US GAAP. It covers topics such as mark-to-market accounting, special purpose entities, and stock options. The article also includes a comparison of financial statement elements and measurement techniques used by Wesfarmer Group Limited and Mackay Golf Club.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

qwertyuiopasdfghjklzxcvbnmqwerty

uiopasdfghjklzxcvbnmqwertyuiopasd

fghjklzxcvbnmqwertyuiopasdfghjklzx

cvbnmqwertyuiopasdfghjklzxcvbnmq

wertyuiopasdfghjklzxcvbnmqwertyui

opasdfghjklzxcvbnmqwertyuiopasdfg

hjklzxcvbnmqwertyuiopasdfghjklzxc

vbnmqwertyuiopasdfghjklzxcvbnmq

wertyuiopasdfghjklzxcvbnmqwertyui

opasdfghjklzxcvbnmqwertyuiopasdfg

hjklzxcvbnmqwertyuiopasdfghjklzxc

vbnmqwertyuiopasdfghjklzxcvbnmq

wertyuiopasdfghjklzxcvbnmqwertyui

opasdfghjklzxcvbnmqwertyuiopasdfg

hjklzxcvbnmrtyuiopasdfghjklzxcvbn

mqwertyuiopasdfghjklzxcvbnmqwert

yuiopasdfghjklzxcvbnmqwertyuiopas

Advance financial accounting

uiopasdfghjklzxcvbnmqwertyuiopasd

fghjklzxcvbnmqwertyuiopasdfghjklzx

cvbnmqwertyuiopasdfghjklzxcvbnmq

wertyuiopasdfghjklzxcvbnmqwertyui

opasdfghjklzxcvbnmqwertyuiopasdfg

hjklzxcvbnmqwertyuiopasdfghjklzxc

vbnmqwertyuiopasdfghjklzxcvbnmq

wertyuiopasdfghjklzxcvbnmqwertyui

opasdfghjklzxcvbnmqwertyuiopasdfg

hjklzxcvbnmqwertyuiopasdfghjklzxc

vbnmqwertyuiopasdfghjklzxcvbnmq

wertyuiopasdfghjklzxcvbnmqwertyui

opasdfghjklzxcvbnmqwertyuiopasdfg

hjklzxcvbnmrtyuiopasdfghjklzxcvbn

mqwertyuiopasdfghjklzxcvbnmqwert

yuiopasdfghjklzxcvbnmqwertyuiopas

Advance financial accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Enron

Going by the matter provided in the article of Paul M. Healy and Krishna G. Palepu regarding

the downfall of Enron, the following can be extracted from the article:

a. Mark-to-market accounting approach can be said to be the accounting on the FV of the

assets, as well as liabilities that dwells on market price in the current scenario that links to the

assets of similar nature and liabilities. In the accounting of mark-to-market, the current

market price is considered as the base for the transactions, it is infused with high volatility

because the market price is exposed to fluctuations. This method is used by the company

when it comes to long-term contracts. when it comes to mark-to-market accounting, the

income, as well as expenses for the long-term contract, are considered residing on the PV of

the future cash flow. Hence, when the price tends to increase or decrease, the same cannot be

adjusted in the books of the company. The faults in the income, as well as profit, was huge

that resulted in misleading of the financial report. When there is a discrepancy in the income

and expenses either it exaggerate or lower the figures.

The company used to ascertain the revenue as the FV of all cash inflow in coming years, as

well as expenses, were booked. The gains, as well as losses, were unrealized in the later

years when that happened. Enron engaged into many long-term contracts of business that

depicted the PV of future cash flow as the income, as well as PV of costs to be incurred

during the entire contract as the cost of service (Healy & Palepu, 2003). There were many

contracts that failed the test of viability in the later year of the contract. In this manner, the

management of the company depicted a false picture of the financial performance while

considering the long-term contract without enabling a cushion for the alterations in income,

as well as expenses that arise in future (Ross et. al, 2014).

b. Special purpose entities can be said to be the shell firms that are developed by the

sponsor but the funding happens through independent equity investor or through debt

financing. Special purpose entities are utilized for different purposes by the businesses like

support in financing, sharing of risk, assets transfer, loan securitization, etc. When it comes to

Enron, it has made various Special Purpose entities so that the finance can be done to forward

contracts and to attain the objectives of financial reporting (Healy & Palepu, 2003). An apt

example of financial report manipulation is done with the help of SPE is being discussed in

2

Going by the matter provided in the article of Paul M. Healy and Krishna G. Palepu regarding

the downfall of Enron, the following can be extracted from the article:

a. Mark-to-market accounting approach can be said to be the accounting on the FV of the

assets, as well as liabilities that dwells on market price in the current scenario that links to the

assets of similar nature and liabilities. In the accounting of mark-to-market, the current

market price is considered as the base for the transactions, it is infused with high volatility

because the market price is exposed to fluctuations. This method is used by the company

when it comes to long-term contracts. when it comes to mark-to-market accounting, the

income, as well as expenses for the long-term contract, are considered residing on the PV of

the future cash flow. Hence, when the price tends to increase or decrease, the same cannot be

adjusted in the books of the company. The faults in the income, as well as profit, was huge

that resulted in misleading of the financial report. When there is a discrepancy in the income

and expenses either it exaggerate or lower the figures.

The company used to ascertain the revenue as the FV of all cash inflow in coming years, as

well as expenses, were booked. The gains, as well as losses, were unrealized in the later

years when that happened. Enron engaged into many long-term contracts of business that

depicted the PV of future cash flow as the income, as well as PV of costs to be incurred

during the entire contract as the cost of service (Healy & Palepu, 2003). There were many

contracts that failed the test of viability in the later year of the contract. In this manner, the

management of the company depicted a false picture of the financial performance while

considering the long-term contract without enabling a cushion for the alterations in income,

as well as expenses that arise in future (Ross et. al, 2014).

b. Special purpose entities can be said to be the shell firms that are developed by the

sponsor but the funding happens through independent equity investor or through debt

financing. Special purpose entities are utilized for different purposes by the businesses like

support in financing, sharing of risk, assets transfer, loan securitization, etc. When it comes to

Enron, it has made various Special Purpose entities so that the finance can be done to forward

contracts and to attain the objectives of financial reporting (Healy & Palepu, 2003). An apt

example of financial report manipulation is done with the help of SPE is being discussed in

2

Enron

the following. In 1997, the Enron contained an intention to purchase the partner share in a

contract of a joint venture. However, the company had no intention to disclose the debts from

the transaction of acquisition or from the JV in the financial statements. The controlling

power in an SPE was held by an executive of Enron that was named as Chewco that raised a

debt guaranteed by Chewco. Enron utilized the debt for the acquisition of the JV relationship.

The structure was framed in a fashion that nothing linked to the transaction of debt financing

was highlighted in the financial statements of Enron and hence Enron was at ease in the

acquisition of the partnership in Joint Venture (Vaitilingam, 2014). The Chewco SPE led to

the violation of various accounting standards and therefore, Enron did not consolidate the

accounts with Chewco. In this fashion, debt, as well as liabilities was understated in the

balance sheet of Enron and on the contrary, earnings, as well a equity was overstated.

In contrast to this, Enron led to minimum disclosures in terms of link with the SPE and a

downside risk was observed in the illiquid investment through SPE. However, no awareness

was seen among the investor that Enron allowed the usage of the stocks to SPE and the

overall debt transaction was guaranteed. Enron even involved various top officers in the

transactions and therefore was successful in funding of contracts and obtained the aims of

financial objectives (Deegan, 2012).

c. The top management of Enron was awarded high compensation that contained stock

options. The main reason for the compensation scheme of the stock option was to lure the

management, as well as a shareholder in the same interest. The main need for providing the

stock option to the employees was to bring a change in the decision making capacity and to

influence them to provide an inflated position of the company. The major noteworthy point

that can be seen is that the stock options provided were without any restriction of further

resale and was indifferent as per the other companies (Davies & Crawford, 2012). When the

stock options are provided without any restriction it leads to a massive problem as there is no

bar in terms of the transfer. Moreover, there were no particular needs for the management of

the stock option purchase. This pattern can be highlighted with the help of the agency theory.

As per the theory, both the principal, as well as the agent is driven by self-interest. The theory

dwells on the assumption that the agent works for self-interest only and to enhance personal

wealth. Therefore, to challenge the assumption it is needed from the agent that either the

work is left aside for self-interest or work in tune with the principle to maximize the wealth

3

the following. In 1997, the Enron contained an intention to purchase the partner share in a

contract of a joint venture. However, the company had no intention to disclose the debts from

the transaction of acquisition or from the JV in the financial statements. The controlling

power in an SPE was held by an executive of Enron that was named as Chewco that raised a

debt guaranteed by Chewco. Enron utilized the debt for the acquisition of the JV relationship.

The structure was framed in a fashion that nothing linked to the transaction of debt financing

was highlighted in the financial statements of Enron and hence Enron was at ease in the

acquisition of the partnership in Joint Venture (Vaitilingam, 2014). The Chewco SPE led to

the violation of various accounting standards and therefore, Enron did not consolidate the

accounts with Chewco. In this fashion, debt, as well as liabilities was understated in the

balance sheet of Enron and on the contrary, earnings, as well a equity was overstated.

In contrast to this, Enron led to minimum disclosures in terms of link with the SPE and a

downside risk was observed in the illiquid investment through SPE. However, no awareness

was seen among the investor that Enron allowed the usage of the stocks to SPE and the

overall debt transaction was guaranteed. Enron even involved various top officers in the

transactions and therefore was successful in funding of contracts and obtained the aims of

financial objectives (Deegan, 2012).

c. The top management of Enron was awarded high compensation that contained stock

options. The main reason for the compensation scheme of the stock option was to lure the

management, as well as a shareholder in the same interest. The main need for providing the

stock option to the employees was to bring a change in the decision making capacity and to

influence them to provide an inflated position of the company. The major noteworthy point

that can be seen is that the stock options provided were without any restriction of further

resale and was indifferent as per the other companies (Davies & Crawford, 2012). When the

stock options are provided without any restriction it leads to a massive problem as there is no

bar in terms of the transfer. Moreover, there were no particular needs for the management of

the stock option purchase. This pattern can be highlighted with the help of the agency theory.

As per the theory, both the principal, as well as the agent is driven by self-interest. The theory

dwells on the assumption that the agent works for self-interest only and to enhance personal

wealth. Therefore, to challenge the assumption it is needed from the agent that either the

work is left aside for self-interest or work in tune with the principle to maximize the wealth

3

Enron

together with the personal wealth (Choi & Meek, 2011). When it comes to Enron, the

management can be defined as the agents that are provided with compensation of high stature

that includes stock options. It was the need to enhance the wealth of the public however, only

the financial performance was inflated without providing any sort of growth for the company.

4

together with the personal wealth (Choi & Meek, 2011). When it comes to Enron, the

management can be defined as the agents that are provided with compensation of high stature

that includes stock options. It was the need to enhance the wealth of the public however, only

the financial performance was inflated without providing any sort of growth for the company.

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Enron

Assessment Task Part-B

As per the International IFRS Conceptual framework, the five elements of financial

statements are asset, liability, equity, income and expense. Different organization has

different level of measurement of such level like historical cost measurement basis, current

value measurement basis, realisable value and present value method.

(a)

There are various mechanism that can be used to ascertain the various element of financial

statements. An apt example of such a framework is that of Wesfarmer Group Limited that

uses the method prescribed below. The revenue computation is done at the consideration fair

value that is received or receivable (Wesfarmer, 2014). The inventories computation are done

at cost or net realisable value that is lower and the computation of cost is done on the basis of

weighted average cost (Melville, 2013).

From the annual report it is observed that the trade and other receivables are done at FV and

later ascertained at amortised cost utilizing the method of effective interest and in tune to this

a deduction happens for the part of an allowance. When it comes to fixed assets like PPE, the

measurement is done at cost deducting the depreciation and the computation of depreciation

happens at straight line method over the useful life for the rest of the time span of the assets

(Wesfarmer, 2014). Moreover, the valuation of the borrowings are done at FV with lesser

transaction cost and later on amortised (Merchant, 2012). The difference between the two are

reflected in the consolidated statement.

Income Statement (ahead of the borrowings)

For the purpose of comparison, another company is considered from US that implements and

make use of the GAAP for the preparation of the financial statements. Mackay Golf club is

selected for the purpose of the study. In this company, the recognition of the revenue, as well

as expenses is done in regard to the percentage of method of completion and this method is

computed as per the Input method (Mackay Golf Club, 2017).

5

Assessment Task Part-B

As per the International IFRS Conceptual framework, the five elements of financial

statements are asset, liability, equity, income and expense. Different organization has

different level of measurement of such level like historical cost measurement basis, current

value measurement basis, realisable value and present value method.

(a)

There are various mechanism that can be used to ascertain the various element of financial

statements. An apt example of such a framework is that of Wesfarmer Group Limited that

uses the method prescribed below. The revenue computation is done at the consideration fair

value that is received or receivable (Wesfarmer, 2014). The inventories computation are done

at cost or net realisable value that is lower and the computation of cost is done on the basis of

weighted average cost (Melville, 2013).

From the annual report it is observed that the trade and other receivables are done at FV and

later ascertained at amortised cost utilizing the method of effective interest and in tune to this

a deduction happens for the part of an allowance. When it comes to fixed assets like PPE, the

measurement is done at cost deducting the depreciation and the computation of depreciation

happens at straight line method over the useful life for the rest of the time span of the assets

(Wesfarmer, 2014). Moreover, the valuation of the borrowings are done at FV with lesser

transaction cost and later on amortised (Merchant, 2012). The difference between the two are

reflected in the consolidated statement.

Income Statement (ahead of the borrowings)

For the purpose of comparison, another company is considered from US that implements and

make use of the GAAP for the preparation of the financial statements. Mackay Golf club is

selected for the purpose of the study. In this company, the recognition of the revenue, as well

as expenses is done in regard to the percentage of method of completion and this method is

computed as per the Input method (Mackay Golf Club, 2017).

5

Enron

The measurement of inventories is done at cost or market price and the one with the lowest is

considered. Further, the determination of the cost happens in two steps that is Raw materials

on FIFO and WIP and Finished Goods in terms of proportionate direct and indirect

manufacturing costs (Mersland & Urgeghe, 2013). Moreover, the long term trade receivables

and other receivables is done as per their present values that is estimated. Furthermore, fixed

assets like PPE are measured at cost deducting the depreciation and the depreciation is

computed utilizing the straight line method over the left over useful life of the asset (Brigham

& Ehrhardt, 2012). The Annual report of the company projects vital information in different

areas of the annual report.

(b) The above mentioned companies in the report uses two different approaches for the

preparation of the financial statements. It cannot be commented with overall accuracy that

which method ranks over another. It can be said that the measurement recognition of one

element ranks higher in the case of IFRS and another element ranks higher in U.S GAAP. For

this purpose various examples are taken into consideration that projects different method of

recognition (Brigham & Ehrhardt, 2012). If the measurement of revenue is done considering

the IFRS then it becomes easy to ascertain, as well as recognize the Income Statement instead

of the U.S GAAP because the IFRS utilizes the most common method of Revenue

Recognition (Brigham & Daves, 2012). Going by the U.S GAAP it can be seen that the

classification of the expenses are done by function while in the case of IFRS the classification

of expenses are done in two parts that is the nature of expense and function that makes it

easier in terms of understanding of the expenses feature in the Income Statement. When it

comes to the presentation of Financial statements under GAAP there are stern requirements

as compared to IFRS. Therefore, it is effective in terms of IFRS presentation. On providing

the remaining examples, the measurements, as well as recognition under the IFRS are easier

in terms of understanding in comparison to GAAP thereby ensuring a better decision making.

When the financial statements are effective then it becomes easier for the users to understand

the financial statement and leads to funding (Mackay Golf Club, 2017).

(c) IFRS and US GAAP:

If both the companies are considered for the critical evaluation considering the

effectiveness of method employed then it can be commented that proper comparability is

not ensured. One of the major reason is that both the companies have their operations in

6

The measurement of inventories is done at cost or market price and the one with the lowest is

considered. Further, the determination of the cost happens in two steps that is Raw materials

on FIFO and WIP and Finished Goods in terms of proportionate direct and indirect

manufacturing costs (Mersland & Urgeghe, 2013). Moreover, the long term trade receivables

and other receivables is done as per their present values that is estimated. Furthermore, fixed

assets like PPE are measured at cost deducting the depreciation and the depreciation is

computed utilizing the straight line method over the left over useful life of the asset (Brigham

& Ehrhardt, 2012). The Annual report of the company projects vital information in different

areas of the annual report.

(b) The above mentioned companies in the report uses two different approaches for the

preparation of the financial statements. It cannot be commented with overall accuracy that

which method ranks over another. It can be said that the measurement recognition of one

element ranks higher in the case of IFRS and another element ranks higher in U.S GAAP. For

this purpose various examples are taken into consideration that projects different method of

recognition (Brigham & Ehrhardt, 2012). If the measurement of revenue is done considering

the IFRS then it becomes easy to ascertain, as well as recognize the Income Statement instead

of the U.S GAAP because the IFRS utilizes the most common method of Revenue

Recognition (Brigham & Daves, 2012). Going by the U.S GAAP it can be seen that the

classification of the expenses are done by function while in the case of IFRS the classification

of expenses are done in two parts that is the nature of expense and function that makes it

easier in terms of understanding of the expenses feature in the Income Statement. When it

comes to the presentation of Financial statements under GAAP there are stern requirements

as compared to IFRS. Therefore, it is effective in terms of IFRS presentation. On providing

the remaining examples, the measurements, as well as recognition under the IFRS are easier

in terms of understanding in comparison to GAAP thereby ensuring a better decision making.

When the financial statements are effective then it becomes easier for the users to understand

the financial statement and leads to funding (Mackay Golf Club, 2017).

(c) IFRS and US GAAP:

If both the companies are considered for the critical evaluation considering the

effectiveness of method employed then it can be commented that proper comparability is

not ensured. One of the major reason is that both the companies have their operations in

6

Enron

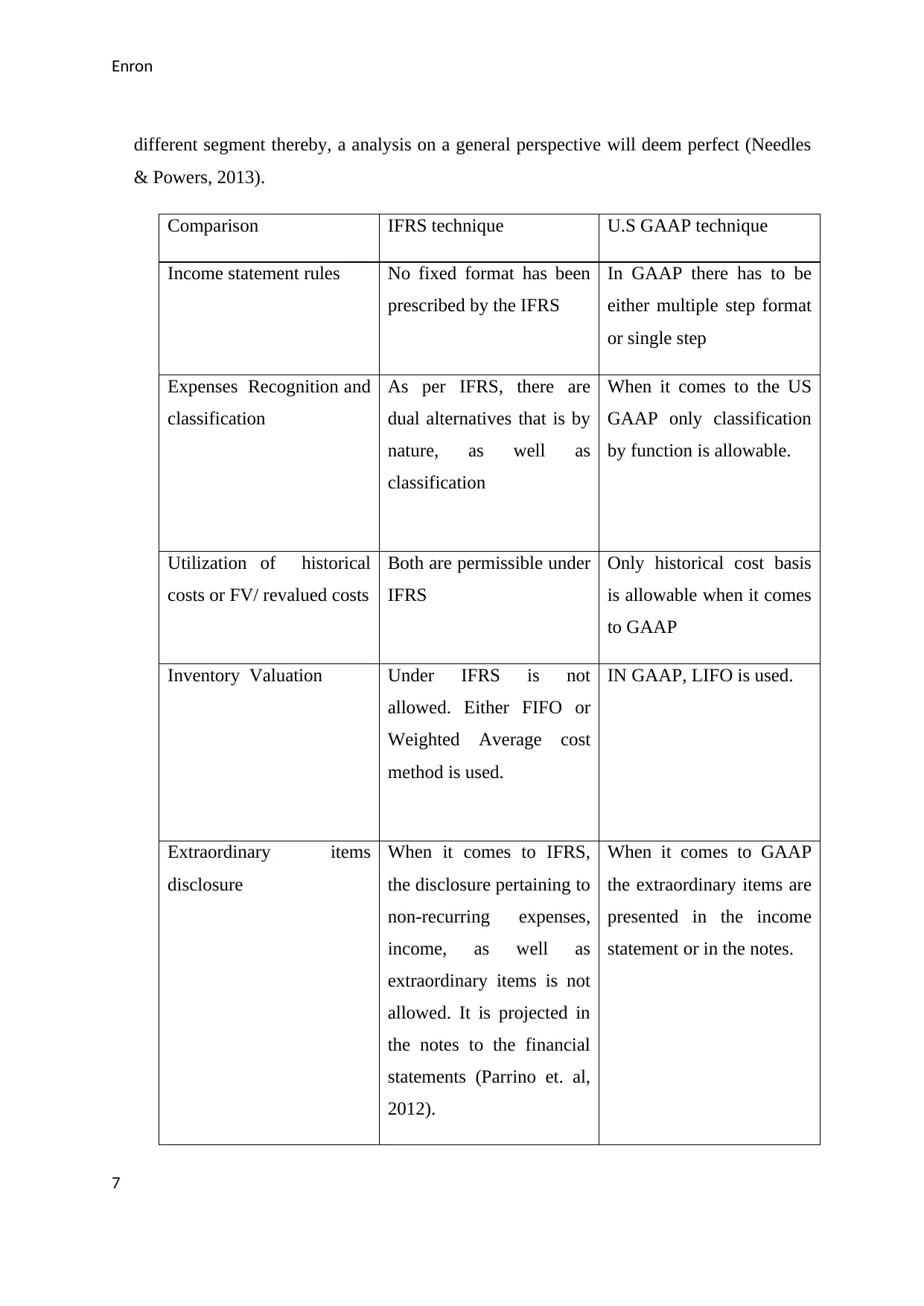

different segment thereby, a analysis on a general perspective will deem perfect (Needles

& Powers, 2013).

Comparison IFRS technique U.S GAAP technique

Income statement rules No fixed format has been

prescribed by the IFRS

In GAAP there has to be

either multiple step format

or single step

Expenses Recognition and

classification

As per IFRS, there are

dual alternatives that is by

nature, as well as

classification

When it comes to the US

GAAP only classification

by function is allowable.

Utilization of historical

costs or FV/ revalued costs

Both are permissible under

IFRS

Only historical cost basis

is allowable when it comes

to GAAP

Inventory Valuation Under IFRS is not

allowed. Either FIFO or

Weighted Average cost

method is used.

IN GAAP, LIFO is used.

Extraordinary items

disclosure

When it comes to IFRS,

the disclosure pertaining to

non-recurring expenses,

income, as well as

extraordinary items is not

allowed. It is projected in

the notes to the financial

statements (Parrino et. al,

2012).

When it comes to GAAP

the extraordinary items are

presented in the income

statement or in the notes.

7

different segment thereby, a analysis on a general perspective will deem perfect (Needles

& Powers, 2013).

Comparison IFRS technique U.S GAAP technique

Income statement rules No fixed format has been

prescribed by the IFRS

In GAAP there has to be

either multiple step format

or single step

Expenses Recognition and

classification

As per IFRS, there are

dual alternatives that is by

nature, as well as

classification

When it comes to the US

GAAP only classification

by function is allowable.

Utilization of historical

costs or FV/ revalued costs

Both are permissible under

IFRS

Only historical cost basis

is allowable when it comes

to GAAP

Inventory Valuation Under IFRS is not

allowed. Either FIFO or

Weighted Average cost

method is used.

IN GAAP, LIFO is used.

Extraordinary items

disclosure

When it comes to IFRS,

the disclosure pertaining to

non-recurring expenses,

income, as well as

extraordinary items is not

allowed. It is projected in

the notes to the financial

statements (Parrino et. al,

2012).

When it comes to GAAP

the extraordinary items are

presented in the income

statement or in the notes.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Enron

The above comparison pertains to the examples that derives from the financial

statements and are selective in nature. As seen from the table of comparison that the

methods, as well as techniques utilized under IFRS are easier in terms of

understanding, as well as implementation. Further, the valuation, as well as

measurement of financial statements can be done in an in-depth manner when the

restrictions or limitations are less (Parrino et. al, 2012). Therefore, it can be

commented that the IFRS is a better standard when it comes to the usage of US

GAAP as the understanding is easier and measuring in simpler in nature thereby the

recognition of the elements portrayed in the financial statements are easier in nature.

The overall discussion sheds light on the benefit provided by the IFRS and hence

ranks above the GAAP.

8

The above comparison pertains to the examples that derives from the financial

statements and are selective in nature. As seen from the table of comparison that the

methods, as well as techniques utilized under IFRS are easier in terms of

understanding, as well as implementation. Further, the valuation, as well as

measurement of financial statements can be done in an in-depth manner when the

restrictions or limitations are less (Parrino et. al, 2012). Therefore, it can be

commented that the IFRS is a better standard when it comes to the usage of US

GAAP as the understanding is easier and measuring in simpler in nature thereby the

recognition of the elements portrayed in the financial statements are easier in nature.

The overall discussion sheds light on the benefit provided by the IFRS and hence

ranks above the GAAP.

8

Enron

References

Brigham, E., & Daves, P. (2012). Intermediate Financial Management. USA: Cengage

Learning.

Brigham, E.F. & Ehrhardt, M.C. (2011) Financial Management: Theory and Practice, USA:

Cengage Learning.

Choi, R.D. and Meek, G.K. (2011) International accounting. Pearson .

Davies, T. and Crawford, I. (2012) Financial accounting. Harlow, England: Pearson.

Deegan, C. M. (2011) In Financial accounting theory. North Ryde, N.S.W: McGraw-Hill

Mackay Golf Club. (2017) Mackay Golf Club 2017 annual report & accounts. Available

from: http://mackaygolf.com.au/beta/wp-content/uploads/2017/11/Annual-Report-2017-Final-.pdf

[Accessed 22 September 2018]

Melville, A. (2013) International Financial Reporting – A Practical Guide. 4th edition.

Pearson, Education Limited, UK

Merchant, K. A. (2012) Making Management Accounting Research More Useful. Pacific

Accounting Review. [online]. 24(3), 1-34. Available from

https://pdfs.semanticscholar.org/6ccf/f78a452763f17ed5e4f4ddc6b96703801403.pdf

Mersland, R., & Urgeghe, L. (2013) International Debt Financing and Performance of

Microfinance Institutions. Strategic Change. [online]. 22. Doi:10.1002/jsc.1919.

Needles, B.E. & Powers, M. (2013) Principles of Financial Accounting. Financial

Accounting Series: Cengage Learning.

Parrino, R, Kidwell, D. & Bates, T. (2012) Fundamentals of corporate finance. Hoboken

Healy, P.M & Palepu, K.G. (2003) The Fall of Enron. Journal of Economic Perspectives.

17(2), 3-26. Available from: https://www.aeaweb.org/articles?

id=10.1257/089533003765888403

Ross, S., Christensen, M., Drew, M., Bianchi, R., Westerfield, R. an Jordan, B.(2014)

Fundamentals of Corporate Finance, 7th ed. North Ryde: McGraw-Hill Australia Pty Ltd.

Vaitilingam, R. (2014) The Financial Times Guide to Using the Financial Pages. London: FT

Prentice Hall

9

References

Brigham, E., & Daves, P. (2012). Intermediate Financial Management. USA: Cengage

Learning.

Brigham, E.F. & Ehrhardt, M.C. (2011) Financial Management: Theory and Practice, USA:

Cengage Learning.

Choi, R.D. and Meek, G.K. (2011) International accounting. Pearson .

Davies, T. and Crawford, I. (2012) Financial accounting. Harlow, England: Pearson.

Deegan, C. M. (2011) In Financial accounting theory. North Ryde, N.S.W: McGraw-Hill

Mackay Golf Club. (2017) Mackay Golf Club 2017 annual report & accounts. Available

from: http://mackaygolf.com.au/beta/wp-content/uploads/2017/11/Annual-Report-2017-Final-.pdf

[Accessed 22 September 2018]

Melville, A. (2013) International Financial Reporting – A Practical Guide. 4th edition.

Pearson, Education Limited, UK

Merchant, K. A. (2012) Making Management Accounting Research More Useful. Pacific

Accounting Review. [online]. 24(3), 1-34. Available from

https://pdfs.semanticscholar.org/6ccf/f78a452763f17ed5e4f4ddc6b96703801403.pdf

Mersland, R., & Urgeghe, L. (2013) International Debt Financing and Performance of

Microfinance Institutions. Strategic Change. [online]. 22. Doi:10.1002/jsc.1919.

Needles, B.E. & Powers, M. (2013) Principles of Financial Accounting. Financial

Accounting Series: Cengage Learning.

Parrino, R, Kidwell, D. & Bates, T. (2012) Fundamentals of corporate finance. Hoboken

Healy, P.M & Palepu, K.G. (2003) The Fall of Enron. Journal of Economic Perspectives.

17(2), 3-26. Available from: https://www.aeaweb.org/articles?

id=10.1257/089533003765888403

Ross, S., Christensen, M., Drew, M., Bianchi, R., Westerfield, R. an Jordan, B.(2014)

Fundamentals of Corporate Finance, 7th ed. North Ryde: McGraw-Hill Australia Pty Ltd.

Vaitilingam, R. (2014) The Financial Times Guide to Using the Financial Pages. London: FT

Prentice Hall

9

Enron

Wesfarmer. (2017) Wesfarmer annual report and accounts 2017 [online]. Available from:

https://www.wesfarmers.com.au/docs/default-source/default-document-library/2017-annual-

report.pdf?sfvrsn=0 [Accessed 23 September 2018]

10

Wesfarmer. (2017) Wesfarmer annual report and accounts 2017 [online]. Available from:

https://www.wesfarmers.com.au/docs/default-source/default-document-library/2017-annual-

report.pdf?sfvrsn=0 [Accessed 23 September 2018]

10

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.