The Impact of AI and ML on the Automobile Insurance Industry

VerifiedAdded on 2023/01/23

|13

|2516

|50

Report

AI Summary

This report investigates the transformative impact of artificial intelligence (AI) and machine learning (ML) on the automobile insurance industry, specifically focusing on Allianz Car Insurance. It explores how AI and ML are changing traditional methods of premium calculation and presenting new opportunities for insurance programs. The report outlines a high-level strategy for implementing these technologies, considering factors such as personal assistance systems, route optimization, and dynamic premium adjustments. It analyzes the motivation behind integrating AI and ML, presenting a business model for the next decade and examining value chains and organizational capabilities. Furthermore, the report addresses future states, potential risks like hacking, and provides a detailed analysis of the market, including revenue, claims, and underwriting results. The conclusion emphasizes the importance of AI and ML in reshaping the insurance landscape and highlights the need for strategic planning and comprehensive data management.

Running head: ENTERPRISE PLANNING AND IMPLEMENTATION

ENTERPRISE PLANNING AND IMPLEMENTATION

Name of the Student

Name of the University

Author Note

ENTERPRISE PLANNING AND IMPLEMENTATION

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ENTERPRISE PLANNING AND IMPLEMENTATION 1

Abstract:

The purpose of this paper is finding out how the impact of artificial intelligence

and machine learning can change the insurance of the automobile industry. The automobile

companies have used in the traditional way for the regression that is multivariate, to generate

insurance premium for the consumers. Artificial intelligence and machine learning are having

the ability to presenting some opportunities that are new for the automobile insurance

program.

Abstract:

The purpose of this paper is finding out how the impact of artificial intelligence

and machine learning can change the insurance of the automobile industry. The automobile

companies have used in the traditional way for the regression that is multivariate, to generate

insurance premium for the consumers. Artificial intelligence and machine learning are having

the ability to presenting some opportunities that are new for the automobile insurance

program.

2ENTERPRISE PLANNING AND IMPLEMENTATION

Table of Contents

Introduction:...............................................................................................................................3

Strategy:.....................................................................................................................................3

The motivation of business:.......................................................................................................4

Business model:.........................................................................................................................6

Value chains:..............................................................................................................................6

Capabilities of the organization:................................................................................................7

Future states and risks:...............................................................................................................8

Conclusion:................................................................................................................................8

Table of Contents

Introduction:...............................................................................................................................3

Strategy:.....................................................................................................................................3

The motivation of business:.......................................................................................................4

Business model:.........................................................................................................................6

Value chains:..............................................................................................................................6

Capabilities of the organization:................................................................................................7

Future states and risks:...............................................................................................................8

Conclusion:................................................................................................................................8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ENTERPRISE PLANNING AND IMPLEMENTATION

Introduction:

Already the artificial intelligence and machine learning is being used for the

automobile insurance industry as well as these two things are changing the entire scenario of

the game. The automobile insurance companies have been traditionally used for the

regression that is multivariate to generate insurance premium for the customer (Baecke and

Bocca, 2017). The artificial intelligence and machine learning both are having the ability to

presenting new opportunities and ideas for the automobile insurance program. The primary

purpose of this paper finds out how the impact of artificial intelligence and machine learning

can change the insurance of the automobile industry for Allianz Car Insurance. Presently the

automobile companies are offering auto insurance program that is too in the form of machine

learning and artificial intelligence (Blumer et al., 2015). Though machine learning and

artificial intelligence are having their infancy if their own but most of the experts are

assuming that machine learning and artificial intelligence will play an essential role in the

automobile insurance industry.

Strategy:

The automobile insurance industry is staying onto the seismic verge, which is the shift

of tech-driven. Machine learning and artificial intelligence will play an important role in the

future but for the implementation of these technologies. There has to be the existence of some

strategies, as there would be one personal assistance that is for the consumers, which shall

have, be an ability for ordering the consumer, an autonomous car for meeting up across entire

the town (Bourne et al., 2014). As looking through Scott's eyes, at the time of arriving of a

car as well as whether the customer shall make the route map himself, which would be the

route. The assistance will share the map of the route immediately with the insurance company

who must respond immediately as well as will suggest one more alternative route. It shall not

Introduction:

Already the artificial intelligence and machine learning is being used for the

automobile insurance industry as well as these two things are changing the entire scenario of

the game. The automobile insurance companies have been traditionally used for the

regression that is multivariate to generate insurance premium for the customer (Baecke and

Bocca, 2017). The artificial intelligence and machine learning both are having the ability to

presenting new opportunities and ideas for the automobile insurance program. The primary

purpose of this paper finds out how the impact of artificial intelligence and machine learning

can change the insurance of the automobile industry for Allianz Car Insurance. Presently the

automobile companies are offering auto insurance program that is too in the form of machine

learning and artificial intelligence (Blumer et al., 2015). Though machine learning and

artificial intelligence are having their infancy if their own but most of the experts are

assuming that machine learning and artificial intelligence will play an essential role in the

automobile insurance industry.

Strategy:

The automobile insurance industry is staying onto the seismic verge, which is the shift

of tech-driven. Machine learning and artificial intelligence will play an important role in the

future but for the implementation of these technologies. There has to be the existence of some

strategies, as there would be one personal assistance that is for the consumers, which shall

have, be an ability for ordering the consumer, an autonomous car for meeting up across entire

the town (Bourne et al., 2014). As looking through Scott's eyes, at the time of arriving of a

car as well as whether the customer shall make the route map himself, which would be the

route. The assistance will share the map of the route immediately with the insurance company

who must respond immediately as well as will suggest one more alternative route. It shall not

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ENTERPRISE PLANNING AND IMPLEMENTATION

be having more crowd that will provide low accident as well as low risks assumptions

(Kašćelan, Kašćelan and Novović Burić, 2016). The assistance will then calculate the

monthly insurance premium as well as will notify the customer about his update of the

premium that the premium of the insurance may be increased by 6 to 9 percent (Júnior et al.,

2017). The premium shall be based on the root that is selected as well as the volume of the

motor vehicles, which will be existing on to the road at that time. That personal assistance

may also alert the consumers about the life insurance policy of them, which must be priced

based on the pay they live as well as it, will also increase by 3 percent more (Koopman and

Wagner, 2017).

The motivation of business:

The scenario may be seemed at the beyond of the horizon, the stories of the user,

which are integrated, shall emerge every line, which is related to the insurance. All the

technologies that are required have existed already as well as most of them are having the

ability to the consumers (Martinelli et al., 2018). With the techniques of the learning that are

new, are having the relation with the deep wave such as artificial intelligence, convolutional

neural networks and the machine learning have the potentiality for the living that is up to the

promise that is for learning, reasoning, attitude of problem solving and perception of the mind

of human being. The premium of the insurance shall be shifted from the repairing of the

current state as well as detecting for preventing or predict as well as transforming every

aspect of that plan of the insurance that is of the industry in the entire process (Pappalardo et

al., 2013). The change is related to the pace that will accelerate as the consumers as well as

insurers, brokers and the intermediaries of the financial. Those shall become more and more

adept at the time of using some of the much advanced technologies, for the enhancement of

the productivity and the decision making, cost that should be lower and optimising the

experience of the consumers.

be having more crowd that will provide low accident as well as low risks assumptions

(Kašćelan, Kašćelan and Novović Burić, 2016). The assistance will then calculate the

monthly insurance premium as well as will notify the customer about his update of the

premium that the premium of the insurance may be increased by 6 to 9 percent (Júnior et al.,

2017). The premium shall be based on the root that is selected as well as the volume of the

motor vehicles, which will be existing on to the road at that time. That personal assistance

may also alert the consumers about the life insurance policy of them, which must be priced

based on the pay they live as well as it, will also increase by 3 percent more (Koopman and

Wagner, 2017).

The motivation of business:

The scenario may be seemed at the beyond of the horizon, the stories of the user,

which are integrated, shall emerge every line, which is related to the insurance. All the

technologies that are required have existed already as well as most of them are having the

ability to the consumers (Martinelli et al., 2018). With the techniques of the learning that are

new, are having the relation with the deep wave such as artificial intelligence, convolutional

neural networks and the machine learning have the potentiality for the living that is up to the

promise that is for learning, reasoning, attitude of problem solving and perception of the mind

of human being. The premium of the insurance shall be shifted from the repairing of the

current state as well as detecting for preventing or predict as well as transforming every

aspect of that plan of the insurance that is of the industry in the entire process (Pappalardo et

al., 2013). The change is related to the pace that will accelerate as the consumers as well as

insurers, brokers and the intermediaries of the financial. Those shall become more and more

adept at the time of using some of the much advanced technologies, for the enhancement of

the productivity and the decision making, cost that should be lower and optimising the

experience of the consumers.

5ENTERPRISE PLANNING AND IMPLEMENTATION

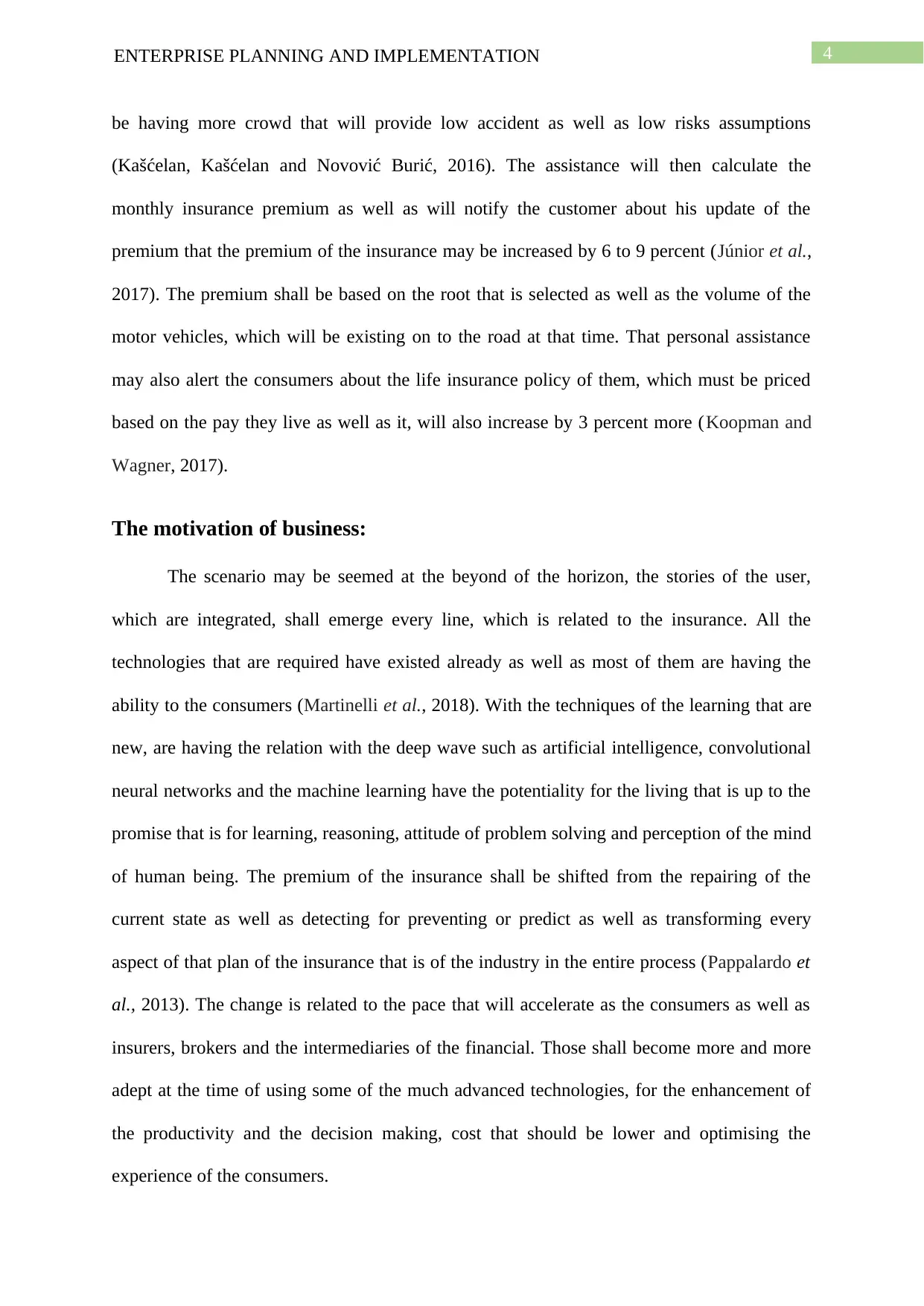

The module for the business of the next ten years should be as follows:

2020 2021 2022 2023 2024 2025 2026 2027

Net premium

revenue ($m)

14,155 19,989 20,354 21,311 21,310 22,433 22,898 24,773

Net incurred

claims ($m)

11,787 11,577 12,234 12,91 12,181 13,203 16,521 16,289

Underwriting

result ($m)

-885 3,069 3,141 2,894 3,469 3,250 -21 1,893

Investment

income ($m)

2,433 2,248 4,028 4,431 4,272 4,660 3,792 3,179

Net profit /

loss ($m)

856 3,397 4,774 5,093 5,364 5,414 2,054 3,086

Net loss ratio 79% 60% 61% 61% 57% 59% 72% 66%

Total assets

($m)

60,013 77,091 78,736 81,536 83,605 92,017 92,650 96,278

Shareholders'

equity ($m)

15,066 21,291 24,007 24,938 24,786 25,984 25,821 29,807

Return on

assets

1.5% 4.6% 6.1% 6.4% 6.5% 6.2% 2.2% 3.3%

Return on

equity

5.5% 17.1% 21.1% 20.8% 21.6% 21.3% 7.9% 11.1%

Solvency 2.75 2.14 2.19 2.44 2.08 2.04 1.85 1.91

The module for the business of the next ten years should be as follows:

2020 2021 2022 2023 2024 2025 2026 2027

Net premium

revenue ($m)

14,155 19,989 20,354 21,311 21,310 22,433 22,898 24,773

Net incurred

claims ($m)

11,787 11,577 12,234 12,91 12,181 13,203 16,521 16,289

Underwriting

result ($m)

-885 3,069 3,141 2,894 3,469 3,250 -21 1,893

Investment

income ($m)

2,433 2,248 4,028 4,431 4,272 4,660 3,792 3,179

Net profit /

loss ($m)

856 3,397 4,774 5,093 5,364 5,414 2,054 3,086

Net loss ratio 79% 60% 61% 61% 57% 59% 72% 66%

Total assets

($m)

60,013 77,091 78,736 81,536 83,605 92,017 92,650 96,278

Shareholders'

equity ($m)

15,066 21,291 24,007 24,938 24,786 25,984 25,821 29,807

Return on

assets

1.5% 4.6% 6.1% 6.4% 6.5% 6.2% 2.2% 3.3%

Return on

equity

5.5% 17.1% 21.1% 20.8% 21.6% 21.3% 7.9% 11.1%

Solvency 2.75 2.14 2.19 2.44 2.08 2.04 1.85 1.91

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ENTERPRISE PLANNING AND IMPLEMENTATION

coverage

Table: Insurance at a glance

Business model:

As the machine, learning and artificial intelligence are becoming more and more type

of the integrated into the industry of the insurance, have to position themselves to respond for

the landscape of the business that is changing day after day. The executive who has the

ability for handling the policies of the insurance must also be having the understanding about

those factors that may contribute for the changes and how the machine learning and artificial

intelligence will reshape the claims, pricing, underwriting and the distribution (Patil et al.,

2017). The machine learning and artificial intelligence are underlying all the technologies,

which have already been deployed in the homes, businesses as well as in the vehicles. The

machine learning and artificial intelligence shall also reshape the industry that is based on

insurance over the coming decade. These kinds of fields are related to the robotics where so

many achievements have seen in recent years.

coverage

Table: Insurance at a glance

Business model:

As the machine, learning and artificial intelligence are becoming more and more type

of the integrated into the industry of the insurance, have to position themselves to respond for

the landscape of the business that is changing day after day. The executive who has the

ability for handling the policies of the insurance must also be having the understanding about

those factors that may contribute for the changes and how the machine learning and artificial

intelligence will reshape the claims, pricing, underwriting and the distribution (Patil et al.,

2017). The machine learning and artificial intelligence are underlying all the technologies,

which have already been deployed in the homes, businesses as well as in the vehicles. The

machine learning and artificial intelligence shall also reshape the industry that is based on

insurance over the coming decade. These kinds of fields are related to the robotics where so

many achievements have seen in recent years.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ENTERPRISE PLANNING AND IMPLEMENTATION

Figure: Business canvas model

Value chains:

The information systems have been made more and more adaptive by the technologies that

are related to the machine learning and artificial intelligence to the human being as well as it

is having the ability for improving the interaction that is between the human being and the

computers (Sanchez et al., 2015). After doing these, the machine was leaning, and artificial

intelligence gives the insurance companies one, edge that how the companies can have the

ability to manage the claiming of the management via using the technologies in some decent

ways.

For the prediction of claiming of the patterns of volume.

For enabling the automated claims for detecting the frauds through using the data,

analytics that is enriched.

In dollars 2009 2010 2011 2012 2013 2014 2015 2016 2018

Figure: Business canvas model

Value chains:

The information systems have been made more and more adaptive by the technologies that

are related to the machine learning and artificial intelligence to the human being as well as it

is having the ability for improving the interaction that is between the human being and the

computers (Sanchez et al., 2015). After doing these, the machine was leaning, and artificial

intelligence gives the insurance companies one, edge that how the companies can have the

ability to manage the claiming of the management via using the technologies in some decent

ways.

For the prediction of claiming of the patterns of volume.

For enabling the automated claims for detecting the frauds through using the data,

analytics that is enriched.

In dollars 2009 2010 2011 2012 2013 2014 2015 2016 2018

8ENTERPRISE PLANNING AND IMPLEMENTATION

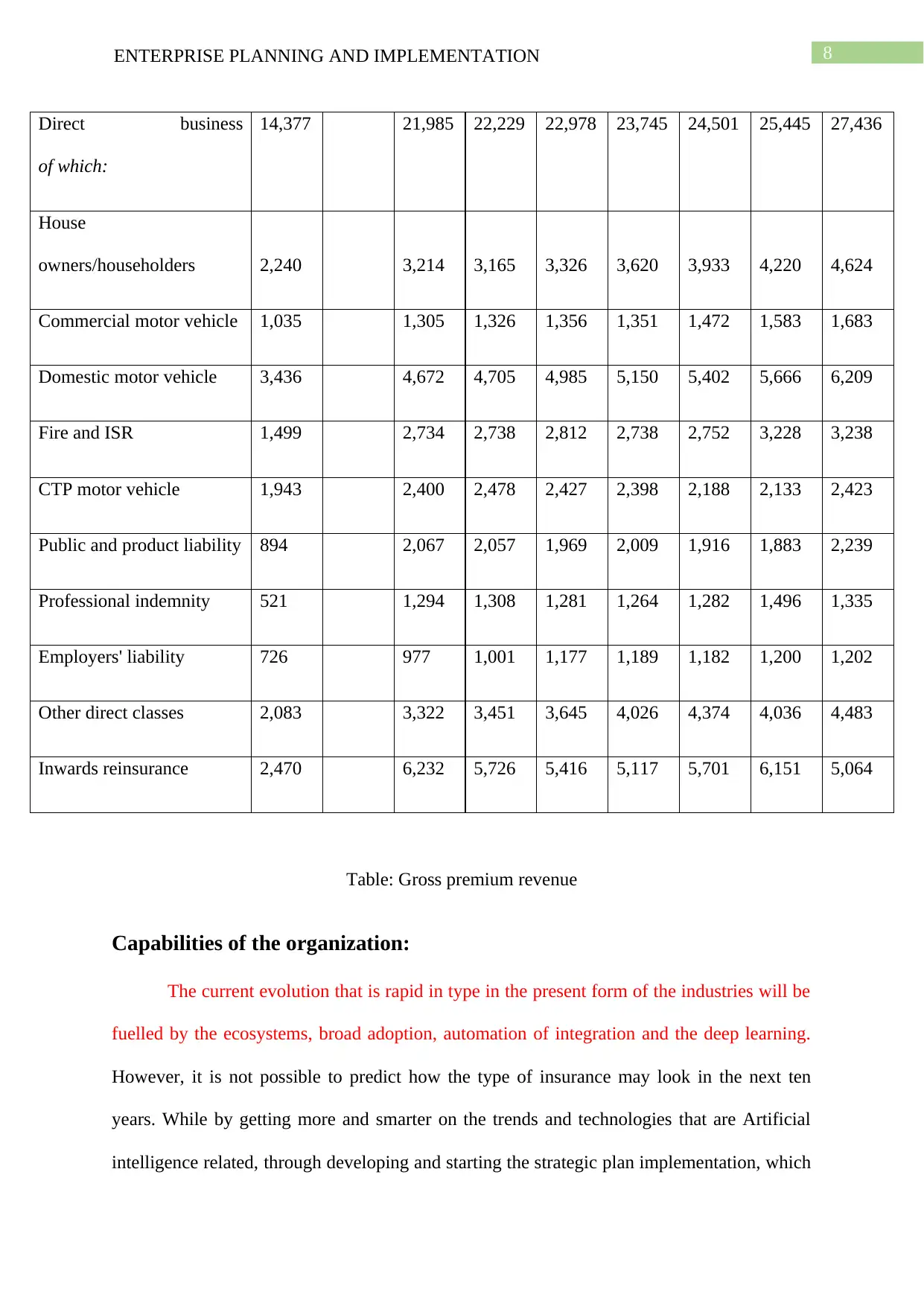

Direct business

of which:

14,377 21,985 22,229 22,978 23,745 24,501 25,445 27,436

House

owners/householders 2,240 3,214 3,165 3,326 3,620 3,933 4,220 4,624

Commercial motor vehicle 1,035 1,305 1,326 1,356 1,351 1,472 1,583 1,683

Domestic motor vehicle 3,436 4,672 4,705 4,985 5,150 5,402 5,666 6,209

Fire and ISR 1,499 2,734 2,738 2,812 2,738 2,752 3,228 3,238

CTP motor vehicle 1,943 2,400 2,478 2,427 2,398 2,188 2,133 2,423

Public and product liability 894 2,067 2,057 1,969 2,009 1,916 1,883 2,239

Professional indemnity 521 1,294 1,308 1,281 1,264 1,282 1,496 1,335

Employers' liability 726 977 1,001 1,177 1,189 1,182 1,200 1,202

Other direct classes 2,083 3,322 3,451 3,645 4,026 4,374 4,036 4,483

Inwards reinsurance 2,470 6,232 5,726 5,416 5,117 5,701 6,151 5,064

Table: Gross premium revenue

Capabilities of the organization:

The current evolution that is rapid in type in the present form of the industries will be

fuelled by the ecosystems, broad adoption, automation of integration and the deep learning.

However, it is not possible to predict how the type of insurance may look in the next ten

years. While by getting more and smarter on the trends and technologies that are Artificial

intelligence related, through developing and starting the strategic plan implementation, which

Direct business

of which:

14,377 21,985 22,229 22,978 23,745 24,501 25,445 27,436

House

owners/householders 2,240 3,214 3,165 3,326 3,620 3,933 4,220 4,624

Commercial motor vehicle 1,035 1,305 1,326 1,356 1,351 1,472 1,583 1,683

Domestic motor vehicle 3,436 4,672 4,705 4,985 5,150 5,402 5,666 6,209

Fire and ISR 1,499 2,734 2,738 2,812 2,738 2,752 3,228 3,238

CTP motor vehicle 1,943 2,400 2,478 2,427 2,398 2,188 2,133 2,423

Public and product liability 894 2,067 2,057 1,969 2,009 1,916 1,883 2,239

Professional indemnity 521 1,294 1,308 1,281 1,264 1,282 1,496 1,335

Employers' liability 726 977 1,001 1,177 1,189 1,182 1,200 1,202

Other direct classes 2,083 3,322 3,451 3,645 4,026 4,374 4,036 4,483

Inwards reinsurance 2,470 6,232 5,726 5,416 5,117 5,701 6,151 5,064

Table: Gross premium revenue

Capabilities of the organization:

The current evolution that is rapid in type in the present form of the industries will be

fuelled by the ecosystems, broad adoption, automation of integration and the deep learning.

However, it is not possible to predict how the type of insurance may look in the next ten

years. While by getting more and smarter on the trends and technologies that are Artificial

intelligence related, through developing and starting the strategic plan implementation, which

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ENTERPRISE PLANNING AND IMPLEMENTATION

is coherent, the insurance companies can be improved (Rubinstein and Kroese, 2013). The

insurance companies will have to create a strategy of the data, which is comprehensive as

well as the technology that is right, as well as talent infrastructure.

Current and Future states and risks:

The automobile insurance industry has steadily grown over the past 5 years, and it has

been characterised through the returns of falling investments as well as burdened with the

damages that are rising from the disasters that are natural. There would be one personal

assistance that is for the consumers, which shall have, be the ability for ordering the

consumer, an autonomous car for meeting up across entire the town. As looking through the

Scott's eyes, at the time of arriving of a car as well as whether the customer shall make the

route map himself, which would be the route (Ritov, Sun and Zhao, 2017). The assistance

will share the map of the route immediately with the insurance company who must respond

immediately as well as will suggest one more alternative route which shall not be having

more crowd that will provide low accident as well as low risks assumptions. However, there

are some risks too as the hacking can be one of the biggest issues in the machine learning

based motor vehicle insurance, as the hackers may be able to track the data of the user after

accessing the entire information database.

Conclusion:

The artificial intelligence and machine learning both are having the ability to

presenting new opportunities and ideas for the automobile insurance program. Already the

artificial intelligence and machine learning is being used for the automobile insurance

industry as well as these two things are changing the entire scenario of the game. The

automobile insurance companies have been traditionally used for the regression that is

multivariate to generate insurance premium for the customer. Artificial intelligence and

is coherent, the insurance companies can be improved (Rubinstein and Kroese, 2013). The

insurance companies will have to create a strategy of the data, which is comprehensive as

well as the technology that is right, as well as talent infrastructure.

Current and Future states and risks:

The automobile insurance industry has steadily grown over the past 5 years, and it has

been characterised through the returns of falling investments as well as burdened with the

damages that are rising from the disasters that are natural. There would be one personal

assistance that is for the consumers, which shall have, be the ability for ordering the

consumer, an autonomous car for meeting up across entire the town. As looking through the

Scott's eyes, at the time of arriving of a car as well as whether the customer shall make the

route map himself, which would be the route (Ritov, Sun and Zhao, 2017). The assistance

will share the map of the route immediately with the insurance company who must respond

immediately as well as will suggest one more alternative route which shall not be having

more crowd that will provide low accident as well as low risks assumptions. However, there

are some risks too as the hacking can be one of the biggest issues in the machine learning

based motor vehicle insurance, as the hackers may be able to track the data of the user after

accessing the entire information database.

Conclusion:

The artificial intelligence and machine learning both are having the ability to

presenting new opportunities and ideas for the automobile insurance program. Already the

artificial intelligence and machine learning is being used for the automobile insurance

industry as well as these two things are changing the entire scenario of the game. The

automobile insurance companies have been traditionally used for the regression that is

multivariate to generate insurance premium for the customer. Artificial intelligence and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ENTERPRISE PLANNING AND IMPLEMENTATION

machine learning are having the ability to presenting some opportunities that are new for the

automobile insurance program.

machine learning are having the ability to presenting some opportunities that are new for the

automobile insurance program.

11ENTERPRISE PLANNING AND IMPLEMENTATION

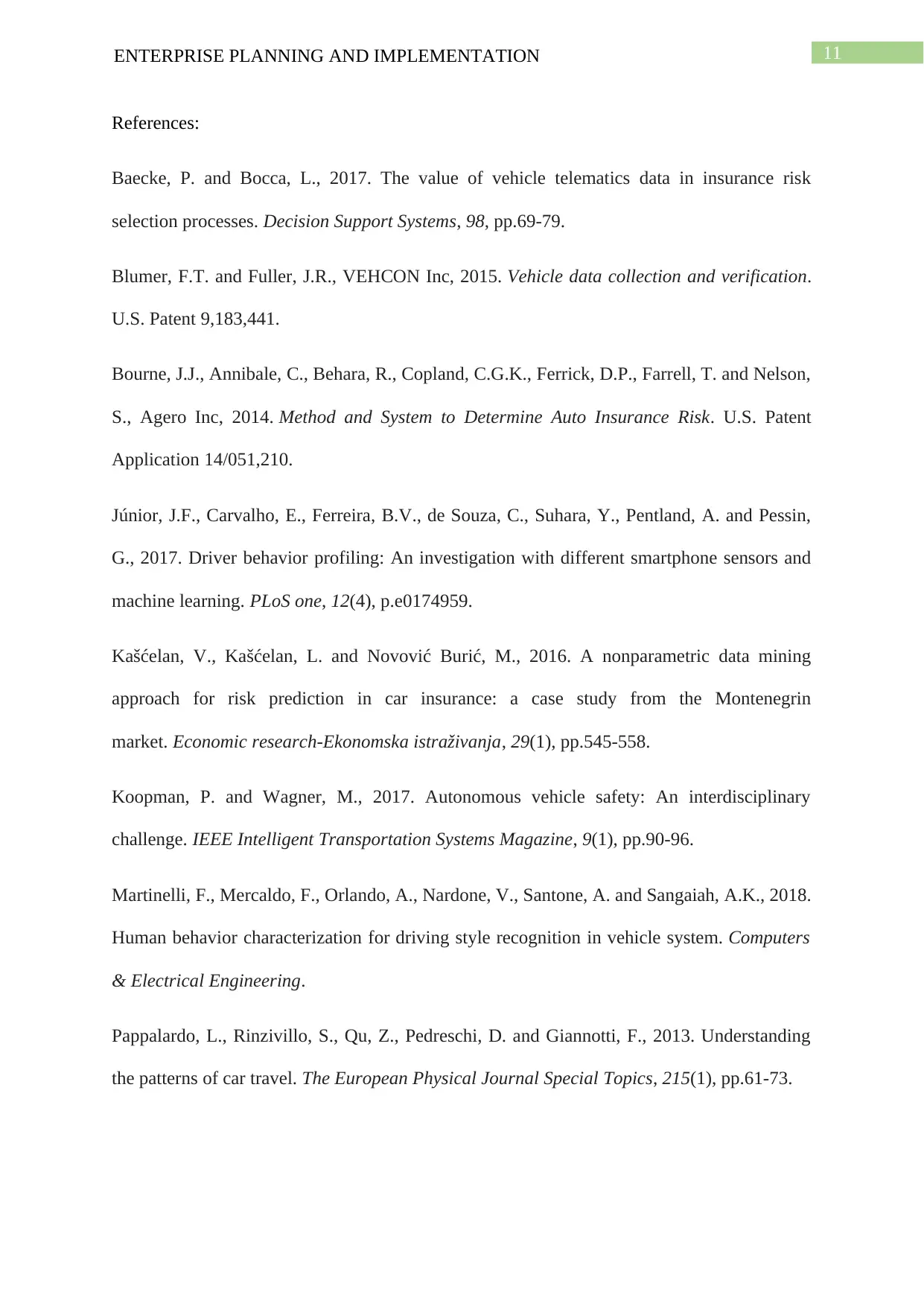

References:

Baecke, P. and Bocca, L., 2017. The value of vehicle telematics data in insurance risk

selection processes. Decision Support Systems, 98, pp.69-79.

Blumer, F.T. and Fuller, J.R., VEHCON Inc, 2015. Vehicle data collection and verification.

U.S. Patent 9,183,441.

Bourne, J.J., Annibale, C., Behara, R., Copland, C.G.K., Ferrick, D.P., Farrell, T. and Nelson,

S., Agero Inc, 2014. Method and System to Determine Auto Insurance Risk. U.S. Patent

Application 14/051,210.

Júnior, J.F., Carvalho, E., Ferreira, B.V., de Souza, C., Suhara, Y., Pentland, A. and Pessin,

G., 2017. Driver behavior profiling: An investigation with different smartphone sensors and

machine learning. PLoS one, 12(4), p.e0174959.

Kašćelan, V., Kašćelan, L. and Novović Burić, M., 2016. A nonparametric data mining

approach for risk prediction in car insurance: a case study from the Montenegrin

market. Economic research-Ekonomska istraživanja, 29(1), pp.545-558.

Koopman, P. and Wagner, M., 2017. Autonomous vehicle safety: An interdisciplinary

challenge. IEEE Intelligent Transportation Systems Magazine, 9(1), pp.90-96.

Martinelli, F., Mercaldo, F., Orlando, A., Nardone, V., Santone, A. and Sangaiah, A.K., 2018.

Human behavior characterization for driving style recognition in vehicle system. Computers

& Electrical Engineering.

Pappalardo, L., Rinzivillo, S., Qu, Z., Pedreschi, D. and Giannotti, F., 2013. Understanding

the patterns of car travel. The European Physical Journal Special Topics, 215(1), pp.61-73.

References:

Baecke, P. and Bocca, L., 2017. The value of vehicle telematics data in insurance risk

selection processes. Decision Support Systems, 98, pp.69-79.

Blumer, F.T. and Fuller, J.R., VEHCON Inc, 2015. Vehicle data collection and verification.

U.S. Patent 9,183,441.

Bourne, J.J., Annibale, C., Behara, R., Copland, C.G.K., Ferrick, D.P., Farrell, T. and Nelson,

S., Agero Inc, 2014. Method and System to Determine Auto Insurance Risk. U.S. Patent

Application 14/051,210.

Júnior, J.F., Carvalho, E., Ferreira, B.V., de Souza, C., Suhara, Y., Pentland, A. and Pessin,

G., 2017. Driver behavior profiling: An investigation with different smartphone sensors and

machine learning. PLoS one, 12(4), p.e0174959.

Kašćelan, V., Kašćelan, L. and Novović Burić, M., 2016. A nonparametric data mining

approach for risk prediction in car insurance: a case study from the Montenegrin

market. Economic research-Ekonomska istraživanja, 29(1), pp.545-558.

Koopman, P. and Wagner, M., 2017. Autonomous vehicle safety: An interdisciplinary

challenge. IEEE Intelligent Transportation Systems Magazine, 9(1), pp.90-96.

Martinelli, F., Mercaldo, F., Orlando, A., Nardone, V., Santone, A. and Sangaiah, A.K., 2018.

Human behavior characterization for driving style recognition in vehicle system. Computers

& Electrical Engineering.

Pappalardo, L., Rinzivillo, S., Qu, Z., Pedreschi, D. and Giannotti, F., 2013. Understanding

the patterns of car travel. The European Physical Journal Special Topics, 215(1), pp.61-73.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.