Environmental Issues and Taxes of New Zealand

VerifiedAdded on 2023/06/10

|26

|8799

|161

AI Summary

This research paper focuses on the major environmental issues and corresponding environmental taxes in New Zealand. It evaluates the beneficial influences of environmental taxation on society and the economy of New Zealand. The paper discusses the Wildlife Act, 1953, Environment Act 1986, Resource Management Act, 1991, Bio security Act, 1993, Conservation Act, 1987, and Ozone Layer Protection Act, 1996. The research questions include the predominant environmental issues in New Zealand, how to address issues related to taxes, benefits of environmental taxation, and the extent of governmental effort to maintain environmental balance in the country.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

ENVIRONMENTAL ISSUES AND TAXES OF NEW ZEALAND

1

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of content

Abstract............................................................................................................................................3

Part 1: Introduction..........................................................................................................................4

Part 2: Literature Review.................................................................................................................7

2.1 Rising environmental pressures in New Zealand-OECD research 2017...................................7

2.2 Green taxes: An initiative of the New Zealand parliament.......................................................7

2.3. Changes in environmental taxes and its impact........................................................................9

2.4 Environmental legislations of New Zealand:..........................................................................10

2.4.1 Wildlife Act, 1953................................................................................................................10

2.4.2 Environment Act 1986..........................................................................................................12

2.4.3 Bio security Act, 1993..........................................................................................................13

2.4.4. Conservation Act, 1987.......................................................................................................15

2.5.5 Resource Management Act, 1991.........................................................................................16

Part 3: Research Methodology.......................................................................................................19

Part 4: Analysis..............................................................................................................................20

Part 5: Conclusion..........................................................................................................................22

Reference list.................................................................................................................................25

2

Abstract............................................................................................................................................3

Part 1: Introduction..........................................................................................................................4

Part 2: Literature Review.................................................................................................................7

2.1 Rising environmental pressures in New Zealand-OECD research 2017...................................7

2.2 Green taxes: An initiative of the New Zealand parliament.......................................................7

2.3. Changes in environmental taxes and its impact........................................................................9

2.4 Environmental legislations of New Zealand:..........................................................................10

2.4.1 Wildlife Act, 1953................................................................................................................10

2.4.2 Environment Act 1986..........................................................................................................12

2.4.3 Bio security Act, 1993..........................................................................................................13

2.4.4. Conservation Act, 1987.......................................................................................................15

2.5.5 Resource Management Act, 1991.........................................................................................16

Part 3: Research Methodology.......................................................................................................19

Part 4: Analysis..............................................................................................................................20

Part 5: Conclusion..........................................................................................................................22

Reference list.................................................................................................................................25

2

Abstract

This entire research paper has been devised by focusing upon the content “environmental issues

and taxation”. The principal aim of this project is to emphasise on the major environmental

issues, predominant in New Zealand and on the corresponding environmental taxes.

This report will reflect on the most prevalent environmental issues in New Zealand and

corresponding taxes that will be effective for identification of most predominant issues existing

in New Zealand along with the persisting problem regarding environmental taxes. Not only that,

along with such issues, various aspects of New Zealand environmental taxes due to which the

society of New Zealand is getting benefits has also been discussed in this paper. This paper has

tried to identify the effort level of New Zealand government regarding environmental issues

management through the discussion and analysis of existing environmental taxation legislation.

In order to provide better understanding the issues and effort of New Zealand government in this

regard, a range of case laws have also been discussed and analysed in this research paper. The

key focus has been provided on Wildlife Act, 1953, Environment Act 1986, Resource

Management Act, 1991, Bio security Act, 1993, Conservation Act, 1987, Ozone Layer

Protection Act, 1996, Resource Management Act, 1991.

3

This entire research paper has been devised by focusing upon the content “environmental issues

and taxation”. The principal aim of this project is to emphasise on the major environmental

issues, predominant in New Zealand and on the corresponding environmental taxes.

This report will reflect on the most prevalent environmental issues in New Zealand and

corresponding taxes that will be effective for identification of most predominant issues existing

in New Zealand along with the persisting problem regarding environmental taxes. Not only that,

along with such issues, various aspects of New Zealand environmental taxes due to which the

society of New Zealand is getting benefits has also been discussed in this paper. This paper has

tried to identify the effort level of New Zealand government regarding environmental issues

management through the discussion and analysis of existing environmental taxation legislation.

In order to provide better understanding the issues and effort of New Zealand government in this

regard, a range of case laws have also been discussed and analysed in this research paper. The

key focus has been provided on Wildlife Act, 1953, Environment Act 1986, Resource

Management Act, 1991, Bio security Act, 1993, Conservation Act, 1987, Ozone Layer

Protection Act, 1996, Resource Management Act, 1991.

3

Part 1: Introduction

With respect to the present scenario, the countries across the globe are trying, in one way or the

other, to improve their economic as well as societal aspects. This is done in order to stay in

constant competition with other countries. However, while giving importance to this competition

several countries have started contributing towards various environmental issues like pollution,

deforestation, waste disposal, overpopulation, etc. In order to deal with these growing

environmental concerns, the governments of different countries are focusing on different

environmental taxes. In this section the persisting environmental issues in New Zealand will be

discussed. Along with the particular discussion, emphasis will be laid on the respective

approaches taken by the country’s government in the context of environmental taxation1.

A variety of taxation policies can be used by the government to reduce the level of pollution and

other environment related issues to a greater extent. This proposed research paper has focused on

the content “environmental issues and tax” in the context of New Zealand2.

Among the 34 OECD countries and 5 partner economies, New Zealand has the 9th lowest

environmentally tax related revenue as a share of the GDP of the country. In the year 2014, the

environmentally related taxes revenue in the New Zealand contributed about 1.34% of the GDP

in comparison to an average of 2% contribution to GDP among the 39 countries (34 OECD

countries and 5 partner economies). Similarly, in comparison to other nations, the taxes on

energy in New Zealand represents 55% of the total environmentally related tax revenue.

Whereas, in the other 39 countries the percentage is 70 on an average (www.oecd.org).

1Oz, Ersan, and Mahmure Esgunoglu. "Taxes in the Prevention of Environmental Pollution Are a

Means? or Aim? Alternative Methods." In Country Experiences in Economic Development,

Management and Entrepreneurship, pp. 267-280. Springer, Cham, 2017.

2Foote, Kyleisha J., Michael K. Joy, and Russell G. Death. "New Zealand dairy farming: milking

our environment for all its worth." Environmental management 56, no. 3 (2015): 709-720.

4

With respect to the present scenario, the countries across the globe are trying, in one way or the

other, to improve their economic as well as societal aspects. This is done in order to stay in

constant competition with other countries. However, while giving importance to this competition

several countries have started contributing towards various environmental issues like pollution,

deforestation, waste disposal, overpopulation, etc. In order to deal with these growing

environmental concerns, the governments of different countries are focusing on different

environmental taxes. In this section the persisting environmental issues in New Zealand will be

discussed. Along with the particular discussion, emphasis will be laid on the respective

approaches taken by the country’s government in the context of environmental taxation1.

A variety of taxation policies can be used by the government to reduce the level of pollution and

other environment related issues to a greater extent. This proposed research paper has focused on

the content “environmental issues and tax” in the context of New Zealand2.

Among the 34 OECD countries and 5 partner economies, New Zealand has the 9th lowest

environmentally tax related revenue as a share of the GDP of the country. In the year 2014, the

environmentally related taxes revenue in the New Zealand contributed about 1.34% of the GDP

in comparison to an average of 2% contribution to GDP among the 39 countries (34 OECD

countries and 5 partner economies). Similarly, in comparison to other nations, the taxes on

energy in New Zealand represents 55% of the total environmentally related tax revenue.

Whereas, in the other 39 countries the percentage is 70 on an average (www.oecd.org).

1Oz, Ersan, and Mahmure Esgunoglu. "Taxes in the Prevention of Environmental Pollution Are a

Means? or Aim? Alternative Methods." In Country Experiences in Economic Development,

Management and Entrepreneurship, pp. 267-280. Springer, Cham, 2017.

2Foote, Kyleisha J., Michael K. Joy, and Russell G. Death. "New Zealand dairy farming: milking

our environment for all its worth." Environmental management 56, no. 3 (2015): 709-720.

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

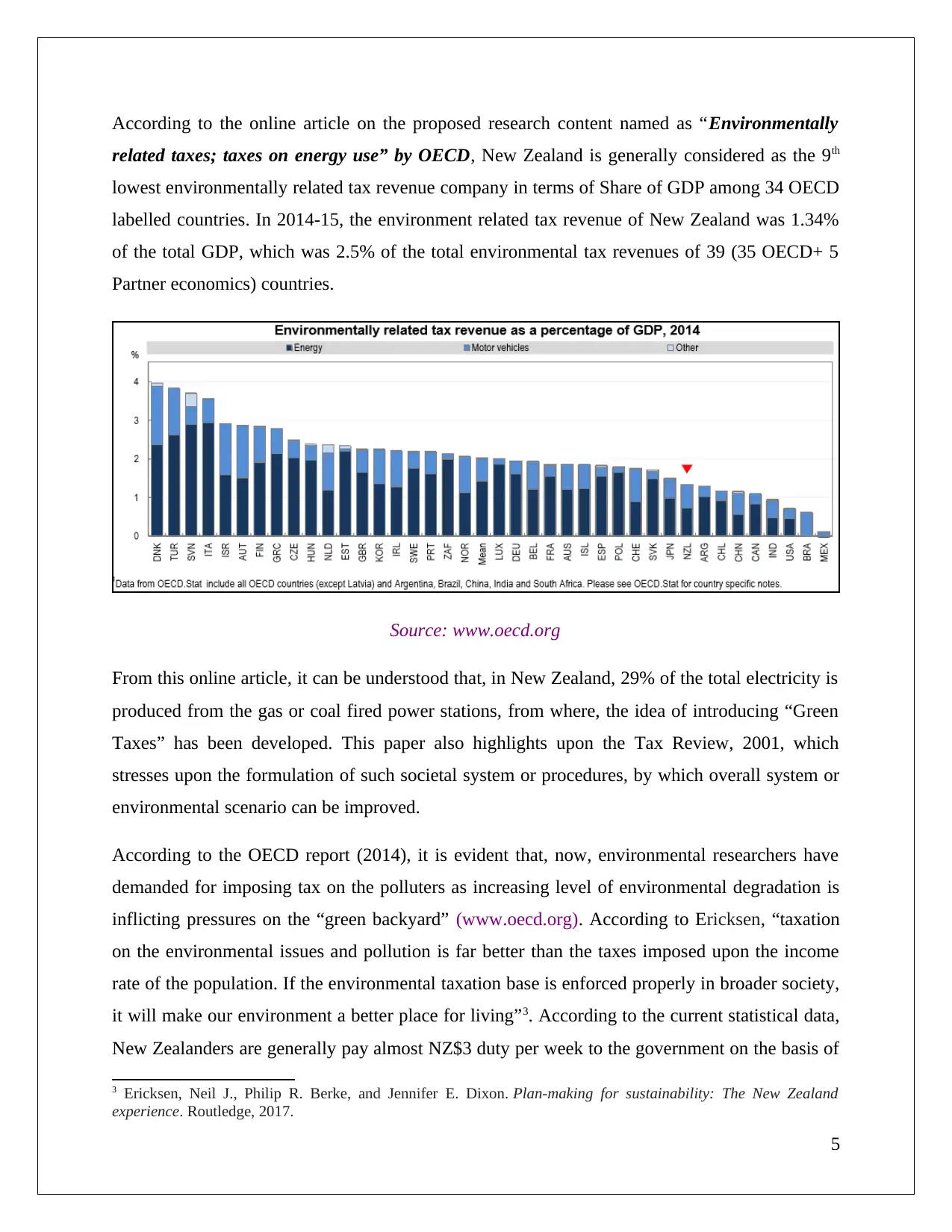

According to the online article on the proposed research content named as “Environmentally

related taxes; taxes on energy use” by OECD, New Zealand is generally considered as the 9th

lowest environmentally related tax revenue company in terms of Share of GDP among 34 OECD

labelled countries. In 2014-15, the environment related tax revenue of New Zealand was 1.34%

of the total GDP, which was 2.5% of the total environmental tax revenues of 39 (35 OECD+ 5

Partner economics) countries.

Source: www.oecd.org

From this online article, it can be understood that, in New Zealand, 29% of the total electricity is

produced from the gas or coal fired power stations, from where, the idea of introducing “Green

Taxes” has been developed. This paper also highlights upon the Tax Review, 2001, which

stresses upon the formulation of such societal system or procedures, by which overall system or

environmental scenario can be improved.

According to the OECD report (2014), it is evident that, now, environmental researchers have

demanded for imposing tax on the polluters as increasing level of environmental degradation is

inflicting pressures on the “green backyard” (www.oecd.org). According to Ericksen, “taxation

on the environmental issues and pollution is far better than the taxes imposed upon the income

rate of the population. If the environmental taxation base is enforced properly in broader society,

it will make our environment a better place for living”3. According to the current statistical data,

New Zealanders are generally pay almost NZ$3 duty per week to the government on the basis of

3 Ericksen, Neil J., Philip R. Berke, and Jennifer E. Dixon. Plan-making for sustainability: The New Zealand

experience. Routledge, 2017.

5

related taxes; taxes on energy use” by OECD, New Zealand is generally considered as the 9th

lowest environmentally related tax revenue company in terms of Share of GDP among 34 OECD

labelled countries. In 2014-15, the environment related tax revenue of New Zealand was 1.34%

of the total GDP, which was 2.5% of the total environmental tax revenues of 39 (35 OECD+ 5

Partner economics) countries.

Source: www.oecd.org

From this online article, it can be understood that, in New Zealand, 29% of the total electricity is

produced from the gas or coal fired power stations, from where, the idea of introducing “Green

Taxes” has been developed. This paper also highlights upon the Tax Review, 2001, which

stresses upon the formulation of such societal system or procedures, by which overall system or

environmental scenario can be improved.

According to the OECD report (2014), it is evident that, now, environmental researchers have

demanded for imposing tax on the polluters as increasing level of environmental degradation is

inflicting pressures on the “green backyard” (www.oecd.org). According to Ericksen, “taxation

on the environmental issues and pollution is far better than the taxes imposed upon the income

rate of the population. If the environmental taxation base is enforced properly in broader society,

it will make our environment a better place for living”3. According to the current statistical data,

New Zealanders are generally pay almost NZ$3 duty per week to the government on the basis of

3 Ericksen, Neil J., Philip R. Berke, and Jennifer E. Dixon. Plan-making for sustainability: The New Zealand

experience. Routledge, 2017.

5

consumption of electricity, gas and the use of petrol; where the country is recognised as the first

in the globe to introduce Carbon tax to keep control over the intensity of global warming

(www.theguardian .com). According to Jacinda Ardern, the minister of New Zealand,

responsible for climate change policy “if we want to tackle or keep control over the climate

change, we have to start taking our environmental cost into vigilant consideration with respect

to the economic choices we make”4.

This entire research paper has devised by focusing upon the content “environmental issues and

taxation”. The principal aim of this project is to emphasis upon the major environmental issues,

predominant in New Zealand and on the corresponding environmental taxes.

This research work has been carried out with the objective of identification of the most

predominant environmental issues in New Zealand and to address relevant environmental taxes.

Along with that this particular research work has also aimed to evaluate all the beneficial

influences of environmental taxation on society and the economy of New Zealand. Along with

that the objective of this research work also includes the identification of the degree of

governmental effort to maintain environmental balance of New Zealand via enforcement of

Environmental taxation within the border society.

Research Questions

As the research aim and objectives have been already discussed above, there are certain research

questions that can be framed based on the aims and objectives of the research study. These

research questions include:

What are the environmental issues that are predominant in New Zealand?

How can the issues related to the taxes be addressed to?

What are the benefits that are being received by the society or economy of the country

due to the environmental taxation?

To what extent is the government making efforts to maintain environmental balance in

the country via the enforcement of environmental taxation within the border society?

4

6

in the globe to introduce Carbon tax to keep control over the intensity of global warming

(www.theguardian .com). According to Jacinda Ardern, the minister of New Zealand,

responsible for climate change policy “if we want to tackle or keep control over the climate

change, we have to start taking our environmental cost into vigilant consideration with respect

to the economic choices we make”4.

This entire research paper has devised by focusing upon the content “environmental issues and

taxation”. The principal aim of this project is to emphasis upon the major environmental issues,

predominant in New Zealand and on the corresponding environmental taxes.

This research work has been carried out with the objective of identification of the most

predominant environmental issues in New Zealand and to address relevant environmental taxes.

Along with that this particular research work has also aimed to evaluate all the beneficial

influences of environmental taxation on society and the economy of New Zealand. Along with

that the objective of this research work also includes the identification of the degree of

governmental effort to maintain environmental balance of New Zealand via enforcement of

Environmental taxation within the border society.

Research Questions

As the research aim and objectives have been already discussed above, there are certain research

questions that can be framed based on the aims and objectives of the research study. These

research questions include:

What are the environmental issues that are predominant in New Zealand?

How can the issues related to the taxes be addressed to?

What are the benefits that are being received by the society or economy of the country

due to the environmental taxation?

To what extent is the government making efforts to maintain environmental balance in

the country via the enforcement of environmental taxation within the border society?

4

6

Part 2: Literature Review

2.1 Rising environmental pressures in New Zealand-OECD research 2017

Since 1990 the emission rate of New Zealand has been rapidly growing. The annual rate of this

growth is almost 23%. The situation of New Zealand has become a major concern for this OECD

because till now 80% of New Zealand electricity is generated from 80% renewable sources but

even after that New Zealand is facing such kind of emission hike5. In order to deal with such

unexpected incidents, the government of New Zealand have reviewed their climate policies in

such ways so that the level of carbon emission can be managed accordingly but still the

environmental requirements have not been fulfilled6. A range of research on this, has identified

that the population of New Zealand has to be made much more aware about environmental

imbalance and that their restricted social and economic behaviours can make the situation better.

In order to increase awareness among the population of New Zealand, a range of environmental

taxes have been implemented by government.

2.2 Green taxes: An initiative of the New Zealand parliament

This was the most fruitful initiative of New Zealand government regarding environmental

pollution. According to these taxes, the population of New Zealand has to pay various kinds of

charges for different social and business behaviours such as using of raw material or process that

emits carbon, production of goods that generate CFC, effluent and emission from vehicle driving

etc7. However, in order to detect the amount of such taxes a range of instruments are used and

those include the following;

5 Schaltegger, Stefan, and Roger Burritt. Contemporary environmental accounting: issues,

concepts and practice. Routledge, 2017.

6 Foote, Kyleisha J., Michael K. Joy, and Russell G. Death. "New Zealand dairy farming:

milking our environment for all its worth." Environmental management 56, no. 3 (2015): 709-

720.

7 Fairbrother, Malcolm. "When will people pay to pollute? Environmental taxes, political trust

and experimental evidence from Britain." British Journal of Political Science (2017): 1-22.

7

2.1 Rising environmental pressures in New Zealand-OECD research 2017

Since 1990 the emission rate of New Zealand has been rapidly growing. The annual rate of this

growth is almost 23%. The situation of New Zealand has become a major concern for this OECD

because till now 80% of New Zealand electricity is generated from 80% renewable sources but

even after that New Zealand is facing such kind of emission hike5. In order to deal with such

unexpected incidents, the government of New Zealand have reviewed their climate policies in

such ways so that the level of carbon emission can be managed accordingly but still the

environmental requirements have not been fulfilled6. A range of research on this, has identified

that the population of New Zealand has to be made much more aware about environmental

imbalance and that their restricted social and economic behaviours can make the situation better.

In order to increase awareness among the population of New Zealand, a range of environmental

taxes have been implemented by government.

2.2 Green taxes: An initiative of the New Zealand parliament

This was the most fruitful initiative of New Zealand government regarding environmental

pollution. According to these taxes, the population of New Zealand has to pay various kinds of

charges for different social and business behaviours such as using of raw material or process that

emits carbon, production of goods that generate CFC, effluent and emission from vehicle driving

etc7. However, in order to detect the amount of such taxes a range of instruments are used and

those include the following;

5 Schaltegger, Stefan, and Roger Burritt. Contemporary environmental accounting: issues,

concepts and practice. Routledge, 2017.

6 Foote, Kyleisha J., Michael K. Joy, and Russell G. Death. "New Zealand dairy farming:

milking our environment for all its worth." Environmental management 56, no. 3 (2015): 709-

720.

7 Fairbrother, Malcolm. "When will people pay to pollute? Environmental taxes, political trust

and experimental evidence from Britain." British Journal of Political Science (2017): 1-22.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2.2.a. Economic instruments : This type of instruments is comprised of various kinds of

additional charges, subsidies, financial enforcement incentives etc.

2.2.b. Regulatory Instruments: These include various kinds of legislation that direct and limit the

use of various kind of material that has been marked as pollutants, use of process that facilitate

environmental pollution etc.

2.2.c. Suasive instruments: These include legislations that have been implemented in order to

increase the awareness among the population New Zealand.

As a result of the green taxes, the producers or consumers will use lesser quantities of such

substances thereby lowering the level of pollution8. The key theory behind this application is that

producers lower the use of those substances upon which taxes have been levied. If the producers

are unable to do so, then they will experience reduction in their revenues or profit margins as the

customers will refrain from expending on such highly priced products. It must be noted that the

extent up to which the taxes reduce the pollution creating depends on certain factors. Often the

circumstances do not turn out to be favourable for the producers and consumers. They may not

be able to find out any alternative option on affordable price9.

2.3. Changes in environmental taxes and its impact

According to the politician Sir Michael Cullen, the changes in the environmental taxes to be

brought about by the tax working group can result in the lowering of the GST. The tax working

group is deciding to apply certain changes to the tax system. The changes are to be applied after

the elections of the year 202010. There are chances that some new taxes will get introduced along

with the modification of some exiting taxes so that the increment in taxation can be controlled

8Scrimgeour, Frank, and Ken Piddington. 2002. "Environmental Taxation In New Zealand: What

Place Does It Have?."

9Miceikiene, Astrida, Vida Ciuleviciene, Jolanta Rauluskeviciene, and Dalia Streimikiene.

"Assessment of the Effect of Environmental Taxes on Environmental Protection." Ekonomicky

Casopis 66, no. 3 (2018): 286-308.

8

additional charges, subsidies, financial enforcement incentives etc.

2.2.b. Regulatory Instruments: These include various kinds of legislation that direct and limit the

use of various kind of material that has been marked as pollutants, use of process that facilitate

environmental pollution etc.

2.2.c. Suasive instruments: These include legislations that have been implemented in order to

increase the awareness among the population New Zealand.

As a result of the green taxes, the producers or consumers will use lesser quantities of such

substances thereby lowering the level of pollution8. The key theory behind this application is that

producers lower the use of those substances upon which taxes have been levied. If the producers

are unable to do so, then they will experience reduction in their revenues or profit margins as the

customers will refrain from expending on such highly priced products. It must be noted that the

extent up to which the taxes reduce the pollution creating depends on certain factors. Often the

circumstances do not turn out to be favourable for the producers and consumers. They may not

be able to find out any alternative option on affordable price9.

2.3. Changes in environmental taxes and its impact

According to the politician Sir Michael Cullen, the changes in the environmental taxes to be

brought about by the tax working group can result in the lowering of the GST. The tax working

group is deciding to apply certain changes to the tax system. The changes are to be applied after

the elections of the year 202010. There are chances that some new taxes will get introduced along

with the modification of some exiting taxes so that the increment in taxation can be controlled

8Scrimgeour, Frank, and Ken Piddington. 2002. "Environmental Taxation In New Zealand: What

Place Does It Have?."

9Miceikiene, Astrida, Vida Ciuleviciene, Jolanta Rauluskeviciene, and Dalia Streimikiene.

"Assessment of the Effect of Environmental Taxes on Environmental Protection." Ekonomicky

Casopis 66, no. 3 (2018): 286-308.

8

and that will be carried out through lowering of GST8. Environmental taxes have been levied on

water consumption, usage of petrol and disposal of wastes on the landfills.

Presently, New Zealanders pay an extra NZ$3 as a levy per week upon consumption rate of

electricity, gas and petrol to the government11. According to the provisions of the taxation policy

in New Zealand, the business sectors or the organisations have to pay almost NZ$11 duty per

metric tonne of carbon emitted, to the government.

Kyoto Protocol: It is an important international Treaty; formulate with the aim to reduce the rate

of emission of greenhouse gas. This treaty has two parts: first one is completely based upon the

prevalent rate of global warming and second part includes human-made carbon dioxide emission

which is considered as the principle reason for global warming and environmental degradation12.

In order to highlights upon the impact of Kyoto protocol on the environmental issues in New

Zealand, it can be said that, after this agreement, the price of the polluting energy sources like

oil, coal become more expensive than the cleaner ones or natural energy resources like natural

gas, hydro energy, biogas and so on13.

Environmental tax can be considered as a tool, which includes both the incentives for the

investment on clean and eco-friendly technology and penalties for continuing environmental

degradation by the polluters, in New Zealand.

10Dogbe, Wisdom, and Jose Maria Gil. "Distributional Impacts of Green Taxes on Food

Consumption in Catalonia." (2017).

11 Sæther, Simen Rostad. "Climate policy choices: do environmental taxes work? A mixed method study of the

OECD and Norway." Master's thesis, NTNU, 2016

12Schneider, Friedrich, Andrea Kollmann, and Johannes Reichl. "The Acceptance of

Environmental Taxes: An Empirical Public Choice Investigation (Draft)." (2016).

13Grunewald, Nicole, and Inmaculada Martinez-Zarzoso. "Did the Kyoto Protocol fail? An

evaluation of the effect of the Kyoto Protocol on CO 2 emissions." Environment and

Development Economics 21, no. 1 (2016): 1-22.

9

water consumption, usage of petrol and disposal of wastes on the landfills.

Presently, New Zealanders pay an extra NZ$3 as a levy per week upon consumption rate of

electricity, gas and petrol to the government11. According to the provisions of the taxation policy

in New Zealand, the business sectors or the organisations have to pay almost NZ$11 duty per

metric tonne of carbon emitted, to the government.

Kyoto Protocol: It is an important international Treaty; formulate with the aim to reduce the rate

of emission of greenhouse gas. This treaty has two parts: first one is completely based upon the

prevalent rate of global warming and second part includes human-made carbon dioxide emission

which is considered as the principle reason for global warming and environmental degradation12.

In order to highlights upon the impact of Kyoto protocol on the environmental issues in New

Zealand, it can be said that, after this agreement, the price of the polluting energy sources like

oil, coal become more expensive than the cleaner ones or natural energy resources like natural

gas, hydro energy, biogas and so on13.

Environmental tax can be considered as a tool, which includes both the incentives for the

investment on clean and eco-friendly technology and penalties for continuing environmental

degradation by the polluters, in New Zealand.

10Dogbe, Wisdom, and Jose Maria Gil. "Distributional Impacts of Green Taxes on Food

Consumption in Catalonia." (2017).

11 Sæther, Simen Rostad. "Climate policy choices: do environmental taxes work? A mixed method study of the

OECD and Norway." Master's thesis, NTNU, 2016

12Schneider, Friedrich, Andrea Kollmann, and Johannes Reichl. "The Acceptance of

Environmental Taxes: An Empirical Public Choice Investigation (Draft)." (2016).

13Grunewald, Nicole, and Inmaculada Martinez-Zarzoso. "Did the Kyoto Protocol fail? An

evaluation of the effect of the Kyoto Protocol on CO 2 emissions." Environment and

Development Economics 21, no. 1 (2016): 1-22.

9

2.4 Environmental legislations of New Zealand:

2.4.1 Wildlife Act, 1953

In order protect some rare species of New Zealand this Act was introduced in 1953.

According to this act if an individual violates the session of this act then accused individual

will be punished by charging NZ $ 100,000. This Act is divided into total of five parts and

part 1 is subdivided into 6 schedules. All theses schedules ensure that the species that are

enlisted under the list of rare species according to New Zealand government can’t be hunted

or eaten. Not only that the key objective of Part 1 of this act is to classify the all available

wildlife species of New Zealand into different category to make the legislative action more

specific and easily identifiable. The 7 classifications are ‘Wildlife declared to be game’,

‘partially protected wildlife’, ‘wildlife that can be haunted or killed in accordance with the

situation’, ‘wild life not protected, except in areas and during specified in minister’s

notification ’, ‘Non protected wild life’, ‘Animals declared to be noxious animal subject to

the Noxious Animal Act 1956’ and the last one is the ‘Terrestrial and freshwater

invertebrates declared to be animals’. Section 7 that means the legislations about freshwater

vertebrates was amended to 7A and according to that marine species were also declared as

animals.

Analysis of social and cultural life of New Zealand it can be seen that bird hunting is

considered as a traditional game in New Zealand society, hence in order to preserve the birds

Part II of this legislation have outlined a range of provision under which the game birds can

haunted. However in order to ensure well-being of New Zealand population of bird species

Part II, IV and V have also been included under wild life Act and that focus on administrative

matters, dealing with injurious species of birds and general provision for ownership and

preservation of various wildlife specimens.

Case law

Incorporated v Director-General of Conservation Case [2017]

10

2.4.1 Wildlife Act, 1953

In order protect some rare species of New Zealand this Act was introduced in 1953.

According to this act if an individual violates the session of this act then accused individual

will be punished by charging NZ $ 100,000. This Act is divided into total of five parts and

part 1 is subdivided into 6 schedules. All theses schedules ensure that the species that are

enlisted under the list of rare species according to New Zealand government can’t be hunted

or eaten. Not only that the key objective of Part 1 of this act is to classify the all available

wildlife species of New Zealand into different category to make the legislative action more

specific and easily identifiable. The 7 classifications are ‘Wildlife declared to be game’,

‘partially protected wildlife’, ‘wildlife that can be haunted or killed in accordance with the

situation’, ‘wild life not protected, except in areas and during specified in minister’s

notification ’, ‘Non protected wild life’, ‘Animals declared to be noxious animal subject to

the Noxious Animal Act 1956’ and the last one is the ‘Terrestrial and freshwater

invertebrates declared to be animals’. Section 7 that means the legislations about freshwater

vertebrates was amended to 7A and according to that marine species were also declared as

animals.

Analysis of social and cultural life of New Zealand it can be seen that bird hunting is

considered as a traditional game in New Zealand society, hence in order to preserve the birds

Part II of this legislation have outlined a range of provision under which the game birds can

haunted. However in order to ensure well-being of New Zealand population of bird species

Part II, IV and V have also been included under wild life Act and that focus on administrative

matters, dealing with injurious species of birds and general provision for ownership and

preservation of various wildlife specimens.

Case law

Incorporated v Director-General of Conservation Case [2017]

10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

In Incorporated v Director-General of Conservation Case [2017] 14regarding wild life has

been raised few years back. Shark cage diving is one of the most popular water game in New

Zealand and PanuaMACC5 is the most popular commercial fishing organisation that

arranges such diving for interested individuals15. However as with increasing numbers of

cage drivers this area is getting riskier regarding shark attack, due to which some sharks have

been killed in order to save human life. The PaumMAC5 authorities have argued that they

have killed those sharks according to the permit issued under S 53(1) under the Wildlife Act

which allows the Minister to authorise any “catch alive or kill” of protected wildlife that was

granted in December 2014. However, some judges of this case argued that the shark cage

diving falls under the offences session that means S63 and 63A session of Wild Life Act.

According to S63 and 63A, cage diving disturb the life of shark which was established from

the case of Solid Energy New Zealand Ltd v Minister of Energy [2008].16 After long

arguments the Cage diving activity of New Zealand has been finally regulated under Marin

Mammals Projection Act 197817.

2.4.2 Environment Act 1986

This Act set out the functions of ministry for environment that includes management of

natural as well as physical resources of New Zealand. The legislation associated with this act

controls the use and access of hazardous substances, reduction of natural hazards etc. the

session associated with this act classify the hazardous in terms of natural and artificial, not

only that this also regulate a range of policies that provide the scope of penalties and

legislative obligation in terms of hazardous material usage, production and accesses or even

the cases of environmental balance violation.

Case law

Environmental Defence Society Inc v New Zealand King Salmon Co Ltd

14 Incorporated v Director-General of Conservation [2017] NZHC 1182

15 Nicola Wheen, 'Case Update: Shark Cage Diving And The Wildlife Act 1953 – Pauamac5 Incorporated V

Director-General Of Conservation [2017] NZHC 1182 – RMLA' (Rmla.org.nz, 2017)

<https://www.rmla.org.nz/2017/08/23/case-update-shark-cage-diving-and-the-wildlife-act-1953-pauamac5-

incorporated-v-director-general-of-conservation-2017-nzhc-1182/> accessed 6 September 2018.

16 Solid Energy New Zealand Ltd v Minister of Energy [2008] NZHC 1979

17 'Marine Mammals Protection Act 1978 No 80 (As At 26 March 2015), Public Act Contents – New Zealand

Legislation' (Legislation.govt.nz, 2018)

<http://www.legislation.govt.nz/act/public/1978/0080/latest/DLM25111.html> accessed 6 September 2018.

11

been raised few years back. Shark cage diving is one of the most popular water game in New

Zealand and PanuaMACC5 is the most popular commercial fishing organisation that

arranges such diving for interested individuals15. However as with increasing numbers of

cage drivers this area is getting riskier regarding shark attack, due to which some sharks have

been killed in order to save human life. The PaumMAC5 authorities have argued that they

have killed those sharks according to the permit issued under S 53(1) under the Wildlife Act

which allows the Minister to authorise any “catch alive or kill” of protected wildlife that was

granted in December 2014. However, some judges of this case argued that the shark cage

diving falls under the offences session that means S63 and 63A session of Wild Life Act.

According to S63 and 63A, cage diving disturb the life of shark which was established from

the case of Solid Energy New Zealand Ltd v Minister of Energy [2008].16 After long

arguments the Cage diving activity of New Zealand has been finally regulated under Marin

Mammals Projection Act 197817.

2.4.2 Environment Act 1986

This Act set out the functions of ministry for environment that includes management of

natural as well as physical resources of New Zealand. The legislation associated with this act

controls the use and access of hazardous substances, reduction of natural hazards etc. the

session associated with this act classify the hazardous in terms of natural and artificial, not

only that this also regulate a range of policies that provide the scope of penalties and

legislative obligation in terms of hazardous material usage, production and accesses or even

the cases of environmental balance violation.

Case law

Environmental Defence Society Inc v New Zealand King Salmon Co Ltd

14 Incorporated v Director-General of Conservation [2017] NZHC 1182

15 Nicola Wheen, 'Case Update: Shark Cage Diving And The Wildlife Act 1953 – Pauamac5 Incorporated V

Director-General Of Conservation [2017] NZHC 1182 – RMLA' (Rmla.org.nz, 2017)

<https://www.rmla.org.nz/2017/08/23/case-update-shark-cage-diving-and-the-wildlife-act-1953-pauamac5-

incorporated-v-director-general-of-conservation-2017-nzhc-1182/> accessed 6 September 2018.

16 Solid Energy New Zealand Ltd v Minister of Energy [2008] NZHC 1979

17 'Marine Mammals Protection Act 1978 No 80 (As At 26 March 2015), Public Act Contents – New Zealand

Legislation' (Legislation.govt.nz, 2018)

<http://www.legislation.govt.nz/act/public/1978/0080/latest/DLM25111.html> accessed 6 September 2018.

11

This is the case law that was associated with the interpretation of Resources Management Act

1991 (Environmental Defence Society Incorporated v The New Zealand King Salmon

Company Limited & Ors [2014])18. The reason of this case was that Marlborough sound

resource Management plan of King Salmon Co Ltd got changed and appealed for

undertaking some sites those are under government prohibition in terms of resource use. His

appeal was argued by the Supreme Court of New Zealand on the basis of 67(3) of RMA that

required proper regional plan to access those prohibited areas for resource usage. Finally

their appeal was rejected in 2014 by Supreme Court as this would provide “adverse effect”

on environmental balance of those area19.

The Aoraki Water Trust v Meridian Energy Ltd [2005] 2 NZLR 268, can be referred to in this

specific context regarding the principle of non-derogation from grant20. In this case, it was held

by the court that it would have been an unlawful matter for the concerned authority to grant for

the permission to another operator regarding a water permit where this resource was allocated in

full and added to that doing so would also in turn reduce for the total amount of water that was

available regarding the satisfaction of the consents that were then presently. Although this case is

concerned to the property but the same also brings about the concern for the respect for the value

of the natural resources as per the laws in the New Zealand and that brings about the concern that

the resources are planned to be effectively used within the nation which is a better sign towards

the development of the concerns of the environment21.

Also in the Quarantine Waste NZ Ltd v. Waste Resources Ltd [1994] NZRMA 529 the

permission was granted to the Waste Resources Ltd regarding the usage of the excess capacity of

the carbonize the waste from even outside the premises of the airport with subject to certain

restriction. The authority that provided for the consent in this case was however much sure

regarding the fact that the adverse effect of such activities would be very minimal in regards to

18 Environmental Defence Society Incorporated v The New Zealand King Salmon Company Limited & Ors [2014]

NZSC 38

19 'Environmental Defence Society Incorporated V The New Zealand King Salmon Company Limited & Ors —

Courts Of New Zealand' (Courtsofnz.govt.nz, 2018) <https://www.courtsofnz.govt.nz/cases/environmental-defence-

society-incorporated-v-the-new-zealand-king-salmon-company-limited-ors> accessed 6 September 2018.

20Salmon, Peter Maxwell, and David Paul Grinlinton, eds. Environmental Law in New Zealand. Wellington:

Thomson Reuters, 2015.

21Christensen, Sharon, Pamela O'Connor, William D. Duncan, and Anna Lark. "Statutory licences and third party

dealings: Property analysis v statutory interpretation." New Zealand Law Review 2015, no. 4 (2015): 585-615.

12

1991 (Environmental Defence Society Incorporated v The New Zealand King Salmon

Company Limited & Ors [2014])18. The reason of this case was that Marlborough sound

resource Management plan of King Salmon Co Ltd got changed and appealed for

undertaking some sites those are under government prohibition in terms of resource use. His

appeal was argued by the Supreme Court of New Zealand on the basis of 67(3) of RMA that

required proper regional plan to access those prohibited areas for resource usage. Finally

their appeal was rejected in 2014 by Supreme Court as this would provide “adverse effect”

on environmental balance of those area19.

The Aoraki Water Trust v Meridian Energy Ltd [2005] 2 NZLR 268, can be referred to in this

specific context regarding the principle of non-derogation from grant20. In this case, it was held

by the court that it would have been an unlawful matter for the concerned authority to grant for

the permission to another operator regarding a water permit where this resource was allocated in

full and added to that doing so would also in turn reduce for the total amount of water that was

available regarding the satisfaction of the consents that were then presently. Although this case is

concerned to the property but the same also brings about the concern for the respect for the value

of the natural resources as per the laws in the New Zealand and that brings about the concern that

the resources are planned to be effectively used within the nation which is a better sign towards

the development of the concerns of the environment21.

Also in the Quarantine Waste NZ Ltd v. Waste Resources Ltd [1994] NZRMA 529 the

permission was granted to the Waste Resources Ltd regarding the usage of the excess capacity of

the carbonize the waste from even outside the premises of the airport with subject to certain

restriction. The authority that provided for the consent in this case was however much sure

regarding the fact that the adverse effect of such activities would be very minimal in regards to

18 Environmental Defence Society Incorporated v The New Zealand King Salmon Company Limited & Ors [2014]

NZSC 38

19 'Environmental Defence Society Incorporated V The New Zealand King Salmon Company Limited & Ors —

Courts Of New Zealand' (Courtsofnz.govt.nz, 2018) <https://www.courtsofnz.govt.nz/cases/environmental-defence-

society-incorporated-v-the-new-zealand-king-salmon-company-limited-ors> accessed 6 September 2018.

20Salmon, Peter Maxwell, and David Paul Grinlinton, eds. Environmental Law in New Zealand. Wellington:

Thomson Reuters, 2015.

21Christensen, Sharon, Pamela O'Connor, William D. Duncan, and Anna Lark. "Statutory licences and third party

dealings: Property analysis v statutory interpretation." New Zealand Law Review 2015, no. 4 (2015): 585-615.

12

the hampering of the environment22. But the Quarantine Waste felt that this would in a manner

affect the environment and brought the entire decision to be judicially reviewed. Also, in case of

the Rural Management Ltd v Banks Peninsula District Council, the appellant started discharging

the sewage into the sea water some years prior to passing of the Resource Management Act of

1991. But with the advent of this act, this entire activity of discharge of the sewage was

cancelled as that harmed the environment in turn.

2.4.3 Bio security Act, 1993

Bio security act, 1993 is a legislation enacted by the parliament of New Zealand before

any other country. The main objective of this statutory legislation is to remove and

eradicate pests and other unwanted organisms which might be harmful for other living

organisms by effective management of the same23. The provisions incorporated in the Act

provides the mechanism of preventing unwanted and harmful organisms entering any

region, undertaking various surveys for the purpose of detection of these pests once they

had already entered and implementing measures to fully eradicate them or make them

ineffective. It also undertakes steps for the development and flourishment of management

plans for pest control. The bio security functions are divided MPI, governmental agencies

and departments and with the regional councils. At present in New Zealand very few

regional councils are operating who are undertaking the role of monitoring and preparing

pest management strategies.

Case law:

Strathboss kiwifruit limited vs. Attorney general

In this case during the year 2010 there was an outbreak of bacteria named Psa in Te Puke,

New Zealand. These bacteria infested two neighbouring kiwifruits orchards. Due to its

outbreak in New Zealand the kiwifruit industry was getting hugely affected. At the initial

stage of the infection the orchardists tried their best of eradicating the bacteria by

22Rodgers, Christopher. "A new approach to protecting ecosystems: The Te Awa Tupua (Whanganui River Claims

Settlement) Act 2017." Environmental Law Review 19, no. 4 (2017): 266-279.

23 'Biosecurity Act 1993 • Environment Guide' (Environmentguide.org.nz, 2018)

<http://www.environmentguide.org.nz/issues/marine/marine-biosecurity/biosecurity-act-1993/> accessed 6

September 2018.

13

affect the environment and brought the entire decision to be judicially reviewed. Also, in case of

the Rural Management Ltd v Banks Peninsula District Council, the appellant started discharging

the sewage into the sea water some years prior to passing of the Resource Management Act of

1991. But with the advent of this act, this entire activity of discharge of the sewage was

cancelled as that harmed the environment in turn.

2.4.3 Bio security Act, 1993

Bio security act, 1993 is a legislation enacted by the parliament of New Zealand before

any other country. The main objective of this statutory legislation is to remove and

eradicate pests and other unwanted organisms which might be harmful for other living

organisms by effective management of the same23. The provisions incorporated in the Act

provides the mechanism of preventing unwanted and harmful organisms entering any

region, undertaking various surveys for the purpose of detection of these pests once they

had already entered and implementing measures to fully eradicate them or make them

ineffective. It also undertakes steps for the development and flourishment of management

plans for pest control. The bio security functions are divided MPI, governmental agencies

and departments and with the regional councils. At present in New Zealand very few

regional councils are operating who are undertaking the role of monitoring and preparing

pest management strategies.

Case law:

Strathboss kiwifruit limited vs. Attorney general

In this case during the year 2010 there was an outbreak of bacteria named Psa in Te Puke,

New Zealand. These bacteria infested two neighbouring kiwifruits orchards. Due to its

outbreak in New Zealand the kiwifruit industry was getting hugely affected. At the initial

stage of the infection the orchardists tried their best of eradicating the bacteria by

22Rodgers, Christopher. "A new approach to protecting ecosystems: The Te Awa Tupua (Whanganui River Claims

Settlement) Act 2017." Environmental Law Review 19, no. 4 (2017): 266-279.

23 'Biosecurity Act 1993 • Environment Guide' (Environmentguide.org.nz, 2018)

<http://www.environmentguide.org.nz/issues/marine/marine-biosecurity/biosecurity-act-1993/> accessed 6

September 2018.

13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

undertaking various measures but all such measures went in vain (Strathboss kiwifruit

limited vs. Attorney general [2018])24.Then the government decided to compensate those

who had suffered losses due to this infestation. But the damages were not adequate in

nature so the plaintiffs of the case instituted a proceeding against the government due to

the incursion of Psa. They contended that MAF had an express authority and duty to take

reasonable care while permitting the kiwi pollen from china. The rules and regulations

were not followed clearly by the concerned authority. Under the Act it was their

responsibility to protect the New Zealand’s border. On the other hand the crown

contented that they were under no duty to take care towards the plaintiff as Bio security

issues are not the appropriate kinds of allegations for which the crown can be held

responsible. Ultimately it was held by the judge that MAF did had the duty to take the

reasonable amount of care and that there was negligence on the part of the authorities

actions. With the entry of this kiwifruit vine disease the impact on the industry was very

devastating as a result of which the kiwifruit growers have run into huge losses so ample

amount of compensation needs to be granted.

2.4.4. Conservation Act, 1987

The conservation Act 1987 was usually promulgated for the purpose of protection and

conservation of New Zealand’s natural resources along with the varieties of flora and

faunas developing in the region. Under this Act different departments are established in

order to undertake the process and functions of conservation which were formerly done

and controlled by the governmental agencies25. The Act has defined the areas which are

to be conserved specifically in the interest of the development of the country. Part IV of

the Act categorises the areas that are to be protected and preserved, sections 18 – 23 deals

with the same. The main area over which the Act focuses is the preservation of the

indigenous fisheries and adopting measures for the purpose of recreation.

Case laws:

24 Strathboss kiwifruit limited vs. Attorney general [2018] NZHC 155)

25 'Legislation' (Doc.govt.nz, 2018) <https://www.doc.govt.nz/about-us/our-role/legislation/> accessed 6 September

2018.

14

limited vs. Attorney general [2018])24.Then the government decided to compensate those

who had suffered losses due to this infestation. But the damages were not adequate in

nature so the plaintiffs of the case instituted a proceeding against the government due to

the incursion of Psa. They contended that MAF had an express authority and duty to take

reasonable care while permitting the kiwi pollen from china. The rules and regulations

were not followed clearly by the concerned authority. Under the Act it was their

responsibility to protect the New Zealand’s border. On the other hand the crown

contented that they were under no duty to take care towards the plaintiff as Bio security

issues are not the appropriate kinds of allegations for which the crown can be held

responsible. Ultimately it was held by the judge that MAF did had the duty to take the

reasonable amount of care and that there was negligence on the part of the authorities

actions. With the entry of this kiwifruit vine disease the impact on the industry was very

devastating as a result of which the kiwifruit growers have run into huge losses so ample

amount of compensation needs to be granted.

2.4.4. Conservation Act, 1987

The conservation Act 1987 was usually promulgated for the purpose of protection and

conservation of New Zealand’s natural resources along with the varieties of flora and

faunas developing in the region. Under this Act different departments are established in

order to undertake the process and functions of conservation which were formerly done

and controlled by the governmental agencies25. The Act has defined the areas which are

to be conserved specifically in the interest of the development of the country. Part IV of

the Act categorises the areas that are to be protected and preserved, sections 18 – 23 deals

with the same. The main area over which the Act focuses is the preservation of the

indigenous fisheries and adopting measures for the purpose of recreation.

Case laws:

24 Strathboss kiwifruit limited vs. Attorney general [2018] NZHC 155)

25 'Legislation' (Doc.govt.nz, 2018) <https://www.doc.govt.nz/about-us/our-role/legislation/> accessed 6 September

2018.

14

Royal forest and bird protection society of new Zealand incorporated vs. Minister of

conservation

In this case an appeal was put before the supreme court of New Zealand regarding the

revocation of the special conservation status of a portion of the Ruahine Forest Park

(RFP) given by the director general of conservation department for acquisition of more

land for the purpose of the Ruataniwha Water Storage Program. The land that was

revoked forms part of the conservation park allotted under the conservation act 1987. The

appellate court went for the judicial review of the judgment given by the high court

(MERIDIAN ENERGY LIMITED V CENTRAL OTAGO DISTRICT COUNCIL And Ors

HC DUN CIV [2009])26. It was concluded that the decision was not rendered at par with

the conservation Act and directed the director general to set aside the previous decision as

it was considered ultra vires. A central inquiry was instituted to declare the purposes for

which the power of revocation of the special protection can be exercised. It was held by

majority view that in order to exercise the discretionary power of revocation of special

protection the director general is first required to judge and verify that the land which was

previously under the scope of special protection under the Act does not require any more

further conservation which was not done in this case. Hence the decision rendered

formerly for the expulsion of the park area was set aside with the additional task on the

part of director general for reconsideration of the issue.

2.5.5 Resource Management Act, 1991

The resource management act 1991(RMA) was passed in the year 1991 in order to

promote the sustainable development and progress of the environment in New Zealand. It

is one of the significant acts that were being developed to keep a check on the

environment and natural resources of the country. The RMA Act provides the mechanism

of an integrated framework which is different from the processes that were previously

followed for the purpose of environmental resources protection. With the incorporation of

an integrated framework all the policies, rules and regulations are completely focused at

raising the standard of the environment. The RMA Act provides all the necessary

26 MERIDIAN ENERGY LIMITED V CENTRAL OTAGO DISTRICT COUNCIL And Ors HC DUN CIV [2009]

15

conservation

In this case an appeal was put before the supreme court of New Zealand regarding the

revocation of the special conservation status of a portion of the Ruahine Forest Park

(RFP) given by the director general of conservation department for acquisition of more

land for the purpose of the Ruataniwha Water Storage Program. The land that was

revoked forms part of the conservation park allotted under the conservation act 1987. The

appellate court went for the judicial review of the judgment given by the high court

(MERIDIAN ENERGY LIMITED V CENTRAL OTAGO DISTRICT COUNCIL And Ors

HC DUN CIV [2009])26. It was concluded that the decision was not rendered at par with

the conservation Act and directed the director general to set aside the previous decision as

it was considered ultra vires. A central inquiry was instituted to declare the purposes for

which the power of revocation of the special protection can be exercised. It was held by

majority view that in order to exercise the discretionary power of revocation of special

protection the director general is first required to judge and verify that the land which was

previously under the scope of special protection under the Act does not require any more

further conservation which was not done in this case. Hence the decision rendered

formerly for the expulsion of the park area was set aside with the additional task on the

part of director general for reconsideration of the issue.

2.5.5 Resource Management Act, 1991

The resource management act 1991(RMA) was passed in the year 1991 in order to

promote the sustainable development and progress of the environment in New Zealand. It

is one of the significant acts that were being developed to keep a check on the

environment and natural resources of the country. The RMA Act provides the mechanism

of an integrated framework which is different from the processes that were previously

followed for the purpose of environmental resources protection. With the incorporation of

an integrated framework all the policies, rules and regulations are completely focused at

raising the standard of the environment. The RMA Act provides all the necessary

26 MERIDIAN ENERGY LIMITED V CENTRAL OTAGO DISTRICT COUNCIL And Ors HC DUN CIV [2009]

15

legislations for the purpose sustainable management of resources relating to water, land

and coastal regions, preserving the landscapes historic heritages etc.

Case laws:

Meridian Energy Limited vs. Central Otago District Council and Others.

In this present case, meridian energy limited is one of the state owned enterprise and a

popular energy company, for the purpose of resource consents applied to the central

Otago district council (COCD) in order to get a permission to operate a substantial wind

farm to generate electricity in central Otago. Eventually consent was granted to the

company (MERIDIAN ENERGY LIMITED V CENTRAL OTAGO DISTRICT COUNCIL

And Ors HC DUN CIV [2009])27. Aggrieved by the decision of the court the other

respondents of the case appealed to the environment court. The decision of the

environment court didn’t went in favour of the company and the project was declared to

be incorrect under section 5 of the RMA Act 1991 as it was not complying with the

features of the sustainable management. Against this decision of the court meridian went

for an appeal under section 299 of the Act alleging that the environmental court’s

decision was not in accordance with the provisions of the act. Under the second appeal

sought by the company the adverse judgment of the court was set aside leading to

reconsideration of the facts once again by the concerned court. Ultimately the final

decision was rendered on 6 November 2009. Two points were discussed in the final

judgment that is the economic reasons and viability which implies specific costs and

benefits of the proposal and any matter of national importance under section 6 of the Act.

The conclusion of the court stated that the company has to give a cost benefit analysis in

which non market techniques are to be used and put up a plan which complies with the

provisions of the act.

Lower Waitaki river Management Society Incorporated vs. Canterbury regional

council

In this present case efficiency of under section 7(b) of the RMA Act is analysed. The

provision under this section requires an authority to provide consent regarding the use

27 (MERIDIAN ENERGY LIMITED V CENTRAL OTAGO DISTRICT COUNCIL And Ors HC DUN CIV

[2009]) 412 000980 (16 August 2010)]

16

and coastal regions, preserving the landscapes historic heritages etc.

Case laws:

Meridian Energy Limited vs. Central Otago District Council and Others.

In this present case, meridian energy limited is one of the state owned enterprise and a

popular energy company, for the purpose of resource consents applied to the central

Otago district council (COCD) in order to get a permission to operate a substantial wind

farm to generate electricity in central Otago. Eventually consent was granted to the

company (MERIDIAN ENERGY LIMITED V CENTRAL OTAGO DISTRICT COUNCIL

And Ors HC DUN CIV [2009])27. Aggrieved by the decision of the court the other

respondents of the case appealed to the environment court. The decision of the

environment court didn’t went in favour of the company and the project was declared to

be incorrect under section 5 of the RMA Act 1991 as it was not complying with the

features of the sustainable management. Against this decision of the court meridian went

for an appeal under section 299 of the Act alleging that the environmental court’s

decision was not in accordance with the provisions of the act. Under the second appeal

sought by the company the adverse judgment of the court was set aside leading to

reconsideration of the facts once again by the concerned court. Ultimately the final

decision was rendered on 6 November 2009. Two points were discussed in the final

judgment that is the economic reasons and viability which implies specific costs and

benefits of the proposal and any matter of national importance under section 6 of the Act.

The conclusion of the court stated that the company has to give a cost benefit analysis in

which non market techniques are to be used and put up a plan which complies with the

provisions of the act.

Lower Waitaki river Management Society Incorporated vs. Canterbury regional

council

In this present case efficiency of under section 7(b) of the RMA Act is analysed. The

provision under this section requires an authority to provide consent regarding the use

27 (MERIDIAN ENERGY LIMITED V CENTRAL OTAGO DISTRICT COUNCIL And Ors HC DUN CIV

[2009]) 412 000980 (16 August 2010)]

16

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

and applicability of the relevant resources with their existing benefits and costs (Lower

Waitaki River Management Society Inc V Canterbury Regional Council [2010])28. If this

process is not complied with then the consideration of the benefits of resources involved

through artificial weighing under sections 5 to 8 of the Act will be of no use. Hence in

order to be in proportion of the statute this cost analysis very essential.

Also we can take a considerable look at the Hampton v Canterbury Regional Council

(Environment Canterbury) [2015] NZCA 509. This was the case where the appeal was

made by Simon Moffatt in the High Court against the decision that granted the cousin of

Simon Moffatt, Robert Moffatt the specific right to take and utilize the water resource to

the extent that the water rights of Simon Moffatt regarding the irrigation of the farmland

of Robert Moffatt were not at all exercised29. However, contrary to the case that is

mentioned above, this time the appeal was reject and the court emphasised for the fact

that while proceeding with the application of irrigation of both the land of the appellant

and that of the land of his cousin, it was much inconsistent for the appellant to argue for

the fact that even his consent must be varied regarding the land of any other third party.

Also in regards to the impacts on the environment in New Zealand, the WEST COAST

ENT INCORPORATED v BULLER COAL LIMITED [2013] NZSC 87 can be referred

to. In this case, the Buller Coal Ltd. and Solid Energy Ltd. applied to the Buller District

Court and that of the West Coast Regional Council regarding getting the consents for the

resource as mentioned within the Resource Management Act of 1991 for being able to

mine the coal resources for the purposes of continuing the exports30. However, the

Supreme Court had dismissed this specific appeal citing to the fact that 2004 Amendment

Act prevented the consent authorities regarding taking into the specific account regarding

the indirect discharges of the discharges of the greenhouse gases regarding providing the

consent for the applications that are associated with the consents for the resources31.

28 Lower Waitaki River Management Society Inc V Canterbury Regional Council [2010] NZEnvC 257 (27 July 2010)

29Sharpe, Susannah. "Water Trading in New Zealand." (2016).

30Ross, Nathan Jon. "Climate change and the resource management act 1991: A Critique of West Coast ENT Inc v

Buller Coal Ltd." Victoria U. Wellington L. Rev. 46 (2015): 1111.

31 Palmer, Geoffrey. "New Zealand's defective law on climate change." NZJPIL 13 (2015): 115.

17

Waitaki River Management Society Inc V Canterbury Regional Council [2010])28. If this

process is not complied with then the consideration of the benefits of resources involved

through artificial weighing under sections 5 to 8 of the Act will be of no use. Hence in

order to be in proportion of the statute this cost analysis very essential.

Also we can take a considerable look at the Hampton v Canterbury Regional Council

(Environment Canterbury) [2015] NZCA 509. This was the case where the appeal was

made by Simon Moffatt in the High Court against the decision that granted the cousin of

Simon Moffatt, Robert Moffatt the specific right to take and utilize the water resource to

the extent that the water rights of Simon Moffatt regarding the irrigation of the farmland

of Robert Moffatt were not at all exercised29. However, contrary to the case that is

mentioned above, this time the appeal was reject and the court emphasised for the fact

that while proceeding with the application of irrigation of both the land of the appellant

and that of the land of his cousin, it was much inconsistent for the appellant to argue for

the fact that even his consent must be varied regarding the land of any other third party.

Also in regards to the impacts on the environment in New Zealand, the WEST COAST

ENT INCORPORATED v BULLER COAL LIMITED [2013] NZSC 87 can be referred

to. In this case, the Buller Coal Ltd. and Solid Energy Ltd. applied to the Buller District

Court and that of the West Coast Regional Council regarding getting the consents for the

resource as mentioned within the Resource Management Act of 1991 for being able to

mine the coal resources for the purposes of continuing the exports30. However, the

Supreme Court had dismissed this specific appeal citing to the fact that 2004 Amendment

Act prevented the consent authorities regarding taking into the specific account regarding

the indirect discharges of the discharges of the greenhouse gases regarding providing the

consent for the applications that are associated with the consents for the resources31.

28 Lower Waitaki River Management Society Inc V Canterbury Regional Council [2010] NZEnvC 257 (27 July 2010)

29Sharpe, Susannah. "Water Trading in New Zealand." (2016).

30Ross, Nathan Jon. "Climate change and the resource management act 1991: A Critique of West Coast ENT Inc v

Buller Coal Ltd." Victoria U. Wellington L. Rev. 46 (2015): 1111.

31 Palmer, Geoffrey. "New Zealand's defective law on climate change." NZJPIL 13 (2015): 115.

17

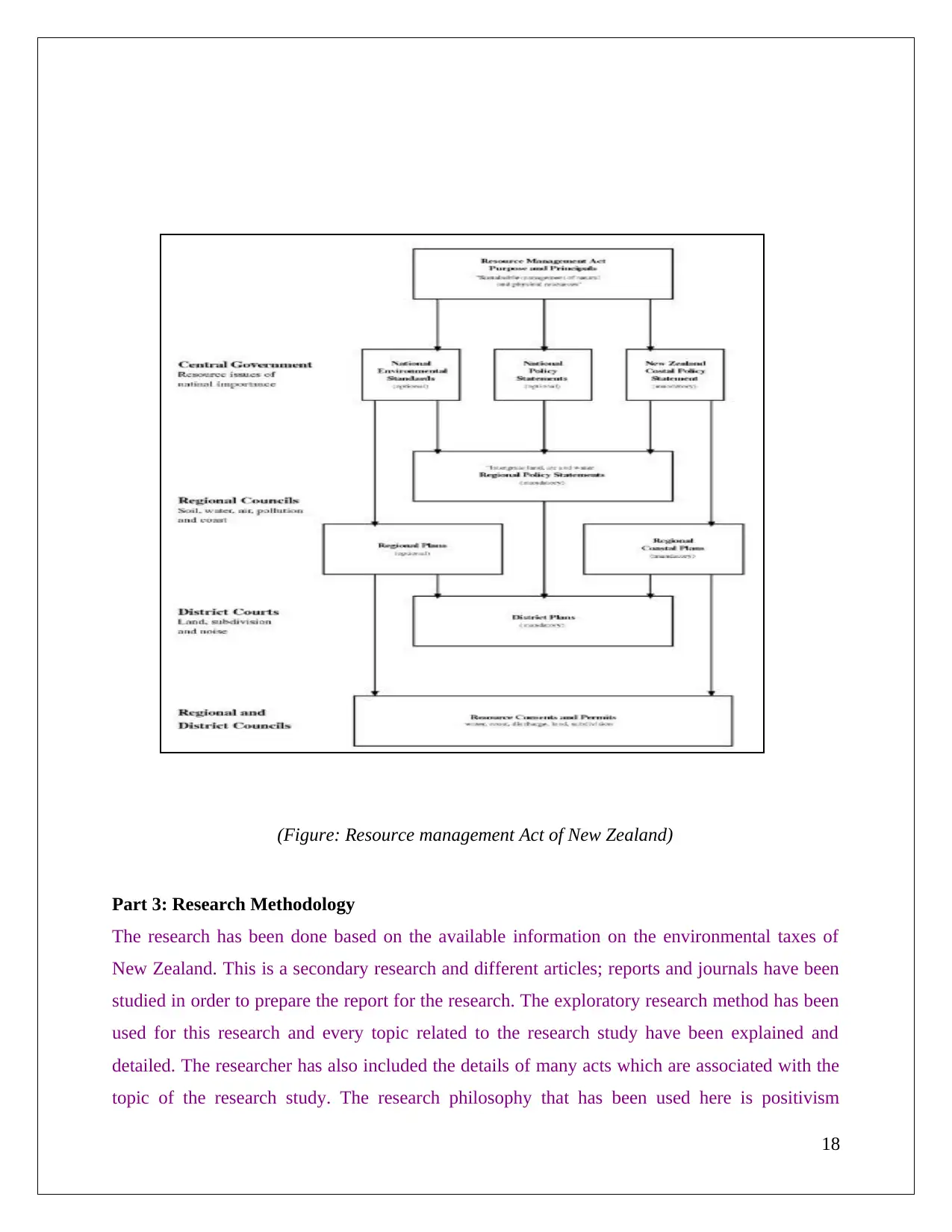

(Figure: Resource management Act of New Zealand)

Part 3: Research Methodology

The research has been done based on the available information on the environmental taxes of

New Zealand. This is a secondary research and different articles; reports and journals have been

studied in order to prepare the report for the research. The exploratory research method has been

used for this research and every topic related to the research study have been explained and

detailed. The researcher has also included the details of many acts which are associated with the

topic of the research study. The research philosophy that has been used here is positivism

18

Part 3: Research Methodology

The research has been done based on the available information on the environmental taxes of

New Zealand. This is a secondary research and different articles; reports and journals have been

studied in order to prepare the report for the research. The exploratory research method has been

used for this research and every topic related to the research study have been explained and

detailed. The researcher has also included the details of many acts which are associated with the

topic of the research study. The research philosophy that has been used here is positivism

18

research philosophy as the researcher is an independent researcher studying the various data and

information available on the environmental issues of New Zealand. The information that has

been used here has been simplified from the information available in a proper manner so that the

details that the research wants to convey clear, interpretable and understandable.

Part 4: Analysis

Secondary data analysis:

According to the research paper “environmental taxation in New Zealand: what place does it

have?” written by Frank Scrimgeour and Ken Piddington, in order to get positive

environmental impact, implication of environmental taxes on society cannot be denied. This

review is based upon the 2001 Tax Review in New Zealand. The principle aim of this paper is to

highlight upon, decarbonised the society in the context of environmental issues and current

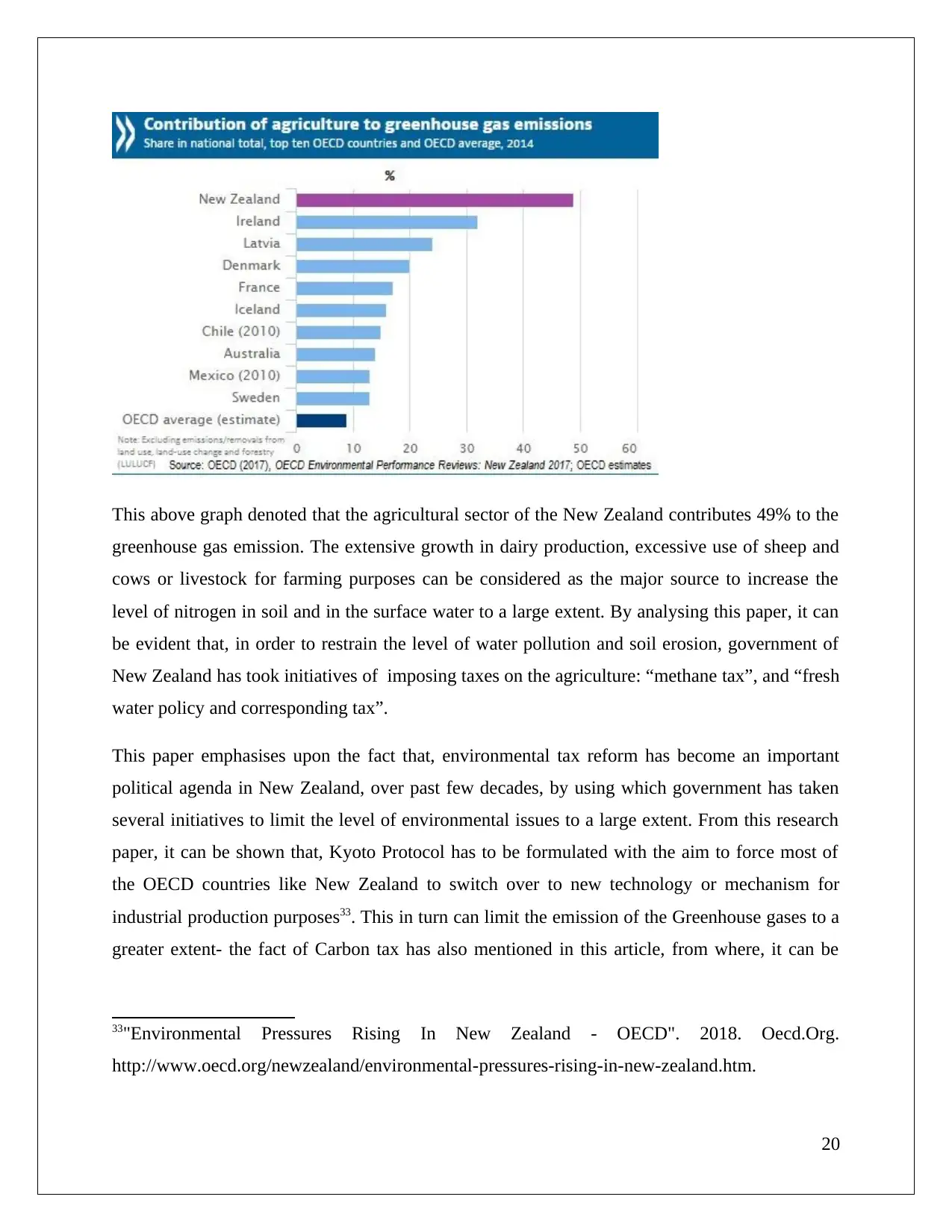

scenario of New Zealand32. By analysing this paper, it can be understood that, in order to

decarbonise the society, New Zealand government has the necessity to implicate climate policies

within the country’s energy manufacturing sectors to curb the carbon-dioxide emission to a

greater extent. This research paper mostly include the transport and agricultural sectors of the

New Zealand, as the majority of the population of this country depend upon the dairy firm and

agricultural profession and, the flatulence of the cattle or live stock are considered as the prime

responsible for increasing the greenhouse gas emission up to 50%.

32Scrimgeour, Frank, and Ken Piddington. 2002. "Environmental Taxation In New Zealand:

What Place Does It Have?."

19

information available on the environmental issues of New Zealand. The information that has

been used here has been simplified from the information available in a proper manner so that the

details that the research wants to convey clear, interpretable and understandable.

Part 4: Analysis

Secondary data analysis:

According to the research paper “environmental taxation in New Zealand: what place does it

have?” written by Frank Scrimgeour and Ken Piddington, in order to get positive

environmental impact, implication of environmental taxes on society cannot be denied. This

review is based upon the 2001 Tax Review in New Zealand. The principle aim of this paper is to

highlight upon, decarbonised the society in the context of environmental issues and current