Environmental Pollution Assignment PDF

Added on 2021-08-31

22 Pages7195 Words104 Views

EnvironmentalPollution

Receive your Favorite Topics right in your Inbox.

Let me in now!

Term Structure of Interest Rates: Meaning, Factors and Theories

Article shared by :

In this article we will discuss about: Meaning of the Term Structure of Interest Rates 2. Factors

Determining the Term Structure of Interest Rates 3. Theories.

Meaning of the Term Structure of Interest Rates:

The term structure of interest rates refers to the relationship between market rates of interest on short-

term and long-term securities. It is the interest rate difference on fixed income securities due to

differences in time of maturity. It is, therefore, also known as time-structure or maturity-structure of

interest rates which explains the relationship between yields and maturities of the same type of

security.

If two securities are identical in every respect except maturity, it is likely that they will sell in the market

at different prices (or yields or interest rates). Generally, their prices will change in the same direction. If

the short-term securities rise in price, the long-term securities will also rise in price.

People generally hold both short-term securities and they adjust their holdings of securities depending

on the relative yields. Usually the long term securities tend to fluctuate more in price than the short-

term securities, even though their yields do not fluctuate as much.

The relationship between yields and terms to maturity is depicted graphically by a yield curve. Figure 1

shows three yield curves. When short-term interest rates are above long-term interest rates, the yield

curve slopes downward, as the curve FF. When short-term interest rates are below long-term interest

rates, the yield curve slopes upward, as the curve RR. When the short-term yields equal long-term

yields, the yield curve is flat, as the curve HL.

Factors Determining the Term Structure of Interest Rates:

Receive your Favorite Topics right in your Inbox.

Let me in now!

Term Structure of Interest Rates: Meaning, Factors and Theories

Article shared by :

In this article we will discuss about: Meaning of the Term Structure of Interest Rates 2. Factors

Determining the Term Structure of Interest Rates 3. Theories.

Meaning of the Term Structure of Interest Rates:

The term structure of interest rates refers to the relationship between market rates of interest on short-

term and long-term securities. It is the interest rate difference on fixed income securities due to

differences in time of maturity. It is, therefore, also known as time-structure or maturity-structure of

interest rates which explains the relationship between yields and maturities of the same type of

security.

If two securities are identical in every respect except maturity, it is likely that they will sell in the market

at different prices (or yields or interest rates). Generally, their prices will change in the same direction. If

the short-term securities rise in price, the long-term securities will also rise in price.

People generally hold both short-term securities and they adjust their holdings of securities depending

on the relative yields. Usually the long term securities tend to fluctuate more in price than the short-

term securities, even though their yields do not fluctuate as much.

The relationship between yields and terms to maturity is depicted graphically by a yield curve. Figure 1

shows three yield curves. When short-term interest rates are above long-term interest rates, the yield

curve slopes downward, as the curve FF. When short-term interest rates are below long-term interest

rates, the yield curve slopes upward, as the curve RR. When the short-term yields equal long-term

yields, the yield curve is flat, as the curve HL.

Factors Determining the Term Structure of Interest Rates:

What determines the shape of the yield curve? There are three factors which determine the term

structure of interest rates. They are risk preference, supply and demand of securities, and expectations

and uncertainty. These factors determine whether short-term interest rates are above or below long-

term interest rates.

We discuss these factors as under:

1. Risk Preference:

Long-term security prices are sensitive to changes in interest rates because the chances to default are

higher on long-term securities as compared to short-term securities. Therefore, lenders prefer to lend

for short-term, if short-term and long-term securities have identical yields.

This would push up short-term prices of securities and bring down their yields. Hence the yield curve

slopes upward. On the other hand, borrowers prefer to borrow for long period because they will not

have to worry about rising interest rates or to renew their loans frequently.

They are, therefore, willing to pay more for long-term securities as compared to short-term securities.

This will also cause the yield curve to slope upward. Thus the preferences of both lenders and borrowers

lead to low rates on short-term securities and high rates on long-term securities, thereby bringing about

an upward sloping yield curve.

2. Supply-Demand Conditions:

When the supply of short-term securities falls and that of long-term securities rises, the short-term

interest rate comes down and the long-term interest rate is pushed up. The yield curve is upward

sloping and vice versa.

If the demand for securities is more in the short-run market and the supply is more in the long-run

market, this will lead to high short-term and low long-term interest rates, and the yield curve will be

downward sloping. The opposite supply-demand conditions will lead to an upward sloping yield curve.

3. Expectations and Uncertainty:

structure of interest rates. They are risk preference, supply and demand of securities, and expectations

and uncertainty. These factors determine whether short-term interest rates are above or below long-

term interest rates.

We discuss these factors as under:

1. Risk Preference:

Long-term security prices are sensitive to changes in interest rates because the chances to default are

higher on long-term securities as compared to short-term securities. Therefore, lenders prefer to lend

for short-term, if short-term and long-term securities have identical yields.

This would push up short-term prices of securities and bring down their yields. Hence the yield curve

slopes upward. On the other hand, borrowers prefer to borrow for long period because they will not

have to worry about rising interest rates or to renew their loans frequently.

They are, therefore, willing to pay more for long-term securities as compared to short-term securities.

This will also cause the yield curve to slope upward. Thus the preferences of both lenders and borrowers

lead to low rates on short-term securities and high rates on long-term securities, thereby bringing about

an upward sloping yield curve.

2. Supply-Demand Conditions:

When the supply of short-term securities falls and that of long-term securities rises, the short-term

interest rate comes down and the long-term interest rate is pushed up. The yield curve is upward

sloping and vice versa.

If the demand for securities is more in the short-run market and the supply is more in the long-run

market, this will lead to high short-term and low long-term interest rates, and the yield curve will be

downward sloping. The opposite supply-demand conditions will lead to an upward sloping yield curve.

3. Expectations and Uncertainty:

Other factors affecting the yield curve are expectations and uncertainty. The expectation of the rise in

the long-term interest rate explains that the short-term interest rate remains much below the long-term

interest rate for any length of time. This produces an upward sloping yield curve.

Further, certain risks and uncertainties may lead to the same results. For instance, if people expect war,

social disturbances, political upheavals, uncertainties, inflationary pressures, etc., they will not purchase

long-term securities except at a low price or low current yield.

Theories of Term Structure of Interest Rates:

Many theories have been put forth by economists to explain differences in the structure of interest rates

on short-term and long-term securities.

They are discussed as under:

1. The Expectations Theory:

The expectations theory regards future interest rates as the principal determinant of the present

structure of interest rates. The theory originated with Irving Fisher, was perfected by Hicks in his Value

and Capital, and is closely identified with Lutz.

Its Assumptions:

The expectations theory is based on the following assumptions:

1. All investors have definite expectations with respect to future short-term interest rates, and these

expectations are held with complete confidence.

2. The objective of investors is to maximise expected profits, and they are prepared to transfer funds

freely from one maturity to another in order to achieve this objective.

the long-term interest rate explains that the short-term interest rate remains much below the long-term

interest rate for any length of time. This produces an upward sloping yield curve.

Further, certain risks and uncertainties may lead to the same results. For instance, if people expect war,

social disturbances, political upheavals, uncertainties, inflationary pressures, etc., they will not purchase

long-term securities except at a low price or low current yield.

Theories of Term Structure of Interest Rates:

Many theories have been put forth by economists to explain differences in the structure of interest rates

on short-term and long-term securities.

They are discussed as under:

1. The Expectations Theory:

The expectations theory regards future interest rates as the principal determinant of the present

structure of interest rates. The theory originated with Irving Fisher, was perfected by Hicks in his Value

and Capital, and is closely identified with Lutz.

Its Assumptions:

The expectations theory is based on the following assumptions:

1. All investors have definite expectations with respect to future short-term interest rates, and these

expectations are held with complete confidence.

2. The objective of investors is to maximise expected profits, and they are prepared to transfer funds

freely from one maturity to another in order to achieve this objective.

3. There are no costs associated with investment and disinvestment in securities. It means that there are

no transaction costs.

4. The short-term and long-term interest rates are adjusted for any differences due to risk and liquidity.

5. ‘Safe’ securities of various maturities are perfect substitutes in the portfolios of investors.

6. Investors are profit maximisers who hold such financial assets in their portfolios which maximize

return over a period they are held.

7. All investors hold with certainty the same expectations of how future rates are going to behave.

Explanation:

Given these assumptions, the theory states that the long-term interest rate at any point in time

represents an average of expected short-time interest rates. Suppose a long-term security maturing

after three years sells at the short-term interest rate of 2 per cent in the first year, and that the expected

short-term interest rates in the second and third years are 3 per cent and 4 per cent respectively.

The long-term interest rate on this security will be the average of the short-term interest rates over the

three years, that is 3 per cent (=2 per cent + 3 per cent+4 per cent=9 per cent/3). If the interest rate on

the short-term security for the first year is expected to decline by 1 per cent the long-term yield on the

three-year security will be 2.67 per cent (=1 per cent+3 per cent+4 per cent=8 per cent/3). On the other

hand, if the interest rate is expected to increase by 1 per cent on the three-year security, then the long-

term yield will be 3.33 per cent (=2 per cent+3 per cent+5 per cent=10 per cent/3).

The expectations theory holds that differences in yields on securities of different maturities are due to

the fact that the market expects the interest rates on different securities to be the same over an equal

period of time.

no transaction costs.

4. The short-term and long-term interest rates are adjusted for any differences due to risk and liquidity.

5. ‘Safe’ securities of various maturities are perfect substitutes in the portfolios of investors.

6. Investors are profit maximisers who hold such financial assets in their portfolios which maximize

return over a period they are held.

7. All investors hold with certainty the same expectations of how future rates are going to behave.

Explanation:

Given these assumptions, the theory states that the long-term interest rate at any point in time

represents an average of expected short-time interest rates. Suppose a long-term security maturing

after three years sells at the short-term interest rate of 2 per cent in the first year, and that the expected

short-term interest rates in the second and third years are 3 per cent and 4 per cent respectively.

The long-term interest rate on this security will be the average of the short-term interest rates over the

three years, that is 3 per cent (=2 per cent + 3 per cent+4 per cent=9 per cent/3). If the interest rate on

the short-term security for the first year is expected to decline by 1 per cent the long-term yield on the

three-year security will be 2.67 per cent (=1 per cent+3 per cent+4 per cent=8 per cent/3). On the other

hand, if the interest rate is expected to increase by 1 per cent on the three-year security, then the long-

term yield will be 3.33 per cent (=2 per cent+3 per cent+5 per cent=10 per cent/3).

The expectations theory holds that differences in yields on securities of different maturities are due to

the fact that the market expects the interest rates on different securities to be the same over an equal

period of time.

If this is not the case, the investor will buy security of one maturity by selling security of another

maturity that he expects to provide him the highest yield. It is this “arbitrage procedure” (buying

security of one maturity and selling of another maturity) which brings the equality of expected yields of

different maturities.

According to Warren L. Smith, “Investors generally have repressive interest rate expectations. That is to

say, at any particular time they have an opinion regarding the level of interest rates they regard as

normal, and as short-term rates rise above or fall below this level, they expect them to regress back

towards this normal level. Thus, as rates rise above normal, investors expect them to fall; and as rates

fall below normal, investors expect them to rise.”

This relationship implies that:

(a) When short- term rates are expected to fall, current short-term rates will be above long-term rates

and the yield curve will be negatively sloped, and

(b) When rates are expected to rise, current short-term rates will be below long-term rates and the yield

curve will be positively sloped. By the same reasoning, when the short-term rate is at approximately the

level judged to be normal and is expected neither to rise nor to fall, rates for all maturities will

approximate a horizontal line.

These relationships between short-term and long-term interest rates are illustrated in Figure 1 where

time to maturity, short or long-term, is taken on the horizontal axis, and yield or interest rate is taken on

the vertical axis.

In the first case, when the current short-term rates are above the long-term rates and are expected to

fall, the yield curve FF is negatively sloped. In the second case, when the current short- term rates are

below the long-term rates, and are expected to rise, the yield curve RR is positively sloped. In the third

case, when the current short-term rates equal the long-term rates and the short-term rates are

expected neither to rise nor to fall, the yield curve HL is a horizontal line.

Time to Maturity and Yield

maturity that he expects to provide him the highest yield. It is this “arbitrage procedure” (buying

security of one maturity and selling of another maturity) which brings the equality of expected yields of

different maturities.

According to Warren L. Smith, “Investors generally have repressive interest rate expectations. That is to

say, at any particular time they have an opinion regarding the level of interest rates they regard as

normal, and as short-term rates rise above or fall below this level, they expect them to regress back

towards this normal level. Thus, as rates rise above normal, investors expect them to fall; and as rates

fall below normal, investors expect them to rise.”

This relationship implies that:

(a) When short- term rates are expected to fall, current short-term rates will be above long-term rates

and the yield curve will be negatively sloped, and

(b) When rates are expected to rise, current short-term rates will be below long-term rates and the yield

curve will be positively sloped. By the same reasoning, when the short-term rate is at approximately the

level judged to be normal and is expected neither to rise nor to fall, rates for all maturities will

approximate a horizontal line.

These relationships between short-term and long-term interest rates are illustrated in Figure 1 where

time to maturity, short or long-term, is taken on the horizontal axis, and yield or interest rate is taken on

the vertical axis.

In the first case, when the current short-term rates are above the long-term rates and are expected to

fall, the yield curve FF is negatively sloped. In the second case, when the current short- term rates are

below the long-term rates, and are expected to rise, the yield curve RR is positively sloped. In the third

case, when the current short-term rates equal the long-term rates and the short-term rates are

expected neither to rise nor to fall, the yield curve HL is a horizontal line.

Time to Maturity and Yield

Prof. Lutz calls these yield curves as expectations curves which represent “the line up of the’ subjective’

long rates which correspond to people’s expectations after the latter have changed.” The key to the

expectations theory is that both short and long-term securities are perfect substitutes for each other in

the portfolios of investors.

If the supply of long-term securities goes up and that of short-term securities goes down, it makes no

difference as far as yields are concerned. Long- term securities will be exchanged for short-term

securities with no change in yields as long as expected future short-term rates are unchanged.

Its Policy Implications:

The policy implications of this theory are that if the government wishes to replace a given amount of

long-term debt with an equivalent amount of short-term debt, such a policy will have no impact on the

Structure of interest rates. This is because both long-term and short-term debts are regarded as perfect

substitutes in the portfolio of investors.

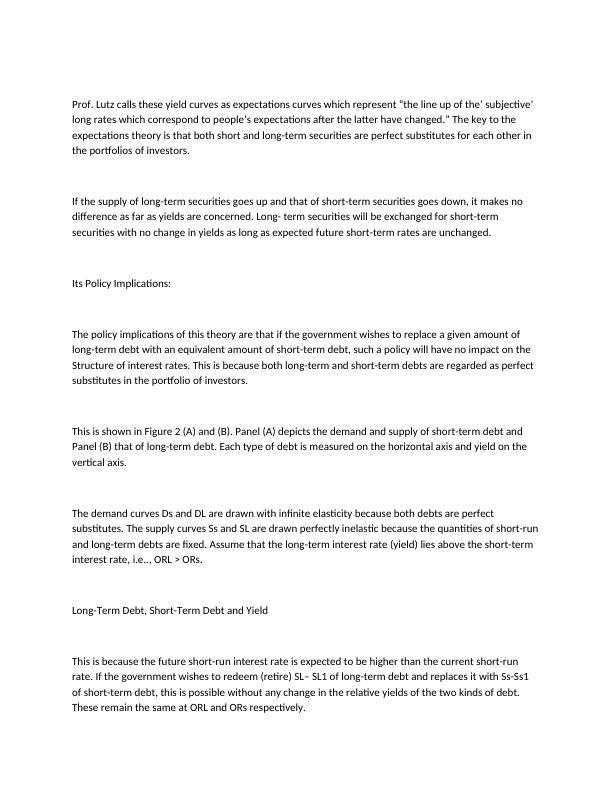

This is shown in Figure 2 (A) and (B). Panel (A) depicts the demand and supply of short-term debt and

Panel (B) that of long-term debt. Each type of debt is measured on the horizontal axis and yield on the

vertical axis.

The demand curves Ds and DL are drawn with infinite elasticity because both debts are perfect

substitutes. The supply curves Ss and SL are drawn perfectly inelastic because the quantities of short-run

and long-term debts are fixed. Assume that the long-term interest rate (yield) lies above the short-term

interest rate, i.e.., ORL > ORs.

Long-Term Debt, Short-Term Debt and Yield

This is because the future short-run interest rate is expected to be higher than the current short-run

rate. If the government wishes to redeem (retire) SL– SL1 of long-term debt and replaces it with Ss-Ss1

of short-term debt, this is possible without any change in the relative yields of the two kinds of debt.

These remain the same at ORL and ORs respectively.

long rates which correspond to people’s expectations after the latter have changed.” The key to the

expectations theory is that both short and long-term securities are perfect substitutes for each other in

the portfolios of investors.

If the supply of long-term securities goes up and that of short-term securities goes down, it makes no

difference as far as yields are concerned. Long- term securities will be exchanged for short-term

securities with no change in yields as long as expected future short-term rates are unchanged.

Its Policy Implications:

The policy implications of this theory are that if the government wishes to replace a given amount of

long-term debt with an equivalent amount of short-term debt, such a policy will have no impact on the

Structure of interest rates. This is because both long-term and short-term debts are regarded as perfect

substitutes in the portfolio of investors.

This is shown in Figure 2 (A) and (B). Panel (A) depicts the demand and supply of short-term debt and

Panel (B) that of long-term debt. Each type of debt is measured on the horizontal axis and yield on the

vertical axis.

The demand curves Ds and DL are drawn with infinite elasticity because both debts are perfect

substitutes. The supply curves Ss and SL are drawn perfectly inelastic because the quantities of short-run

and long-term debts are fixed. Assume that the long-term interest rate (yield) lies above the short-term

interest rate, i.e.., ORL > ORs.

Long-Term Debt, Short-Term Debt and Yield

This is because the future short-run interest rate is expected to be higher than the current short-run

rate. If the government wishes to redeem (retire) SL– SL1 of long-term debt and replaces it with Ss-Ss1

of short-term debt, this is possible without any change in the relative yields of the two kinds of debt.

These remain the same at ORL and ORs respectively.

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

MAF 202 - Money & Capital Marketslg...

|9

|1003

|62

Euro Yield Curve Fluctuations: Market Fluctuation and Forecastlg...

|7

|1118

|431

Accounting & Finance Question Answer 2022lg...

|11

|1288

|19

Yield Curve and Relationship Between Interest Rates and Inflationlg...

|8

|2008

|450

International Financial Markets and Institution | Q&Alg...

|15

|2749

|16

Macroeconomics Study Materiallg...

|5

|766

|304