Equifax Data Breach Analysis and Facebook Target Price Valuation

VerifiedAdded on 2020/05/28

|5

|1384

|319

Report

AI Summary

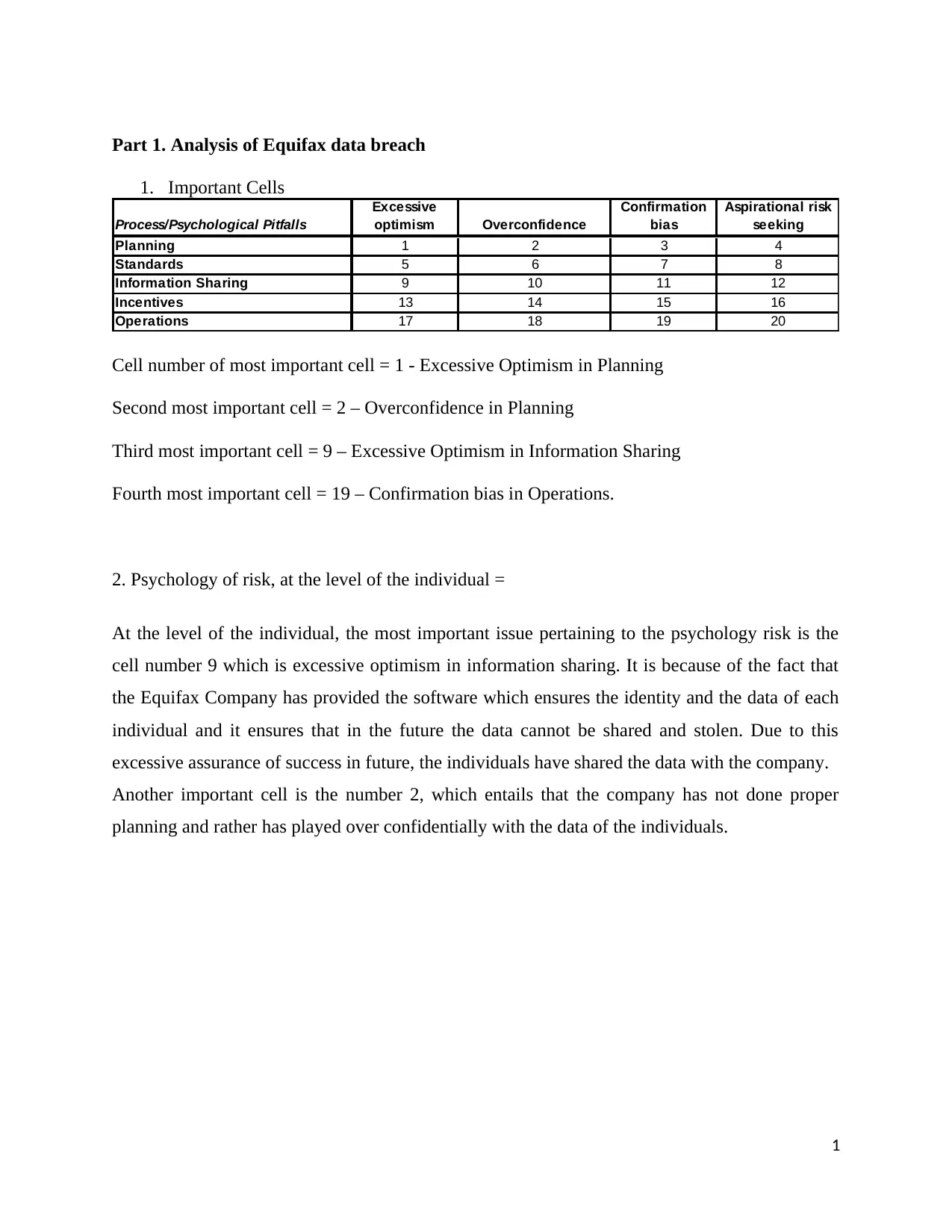

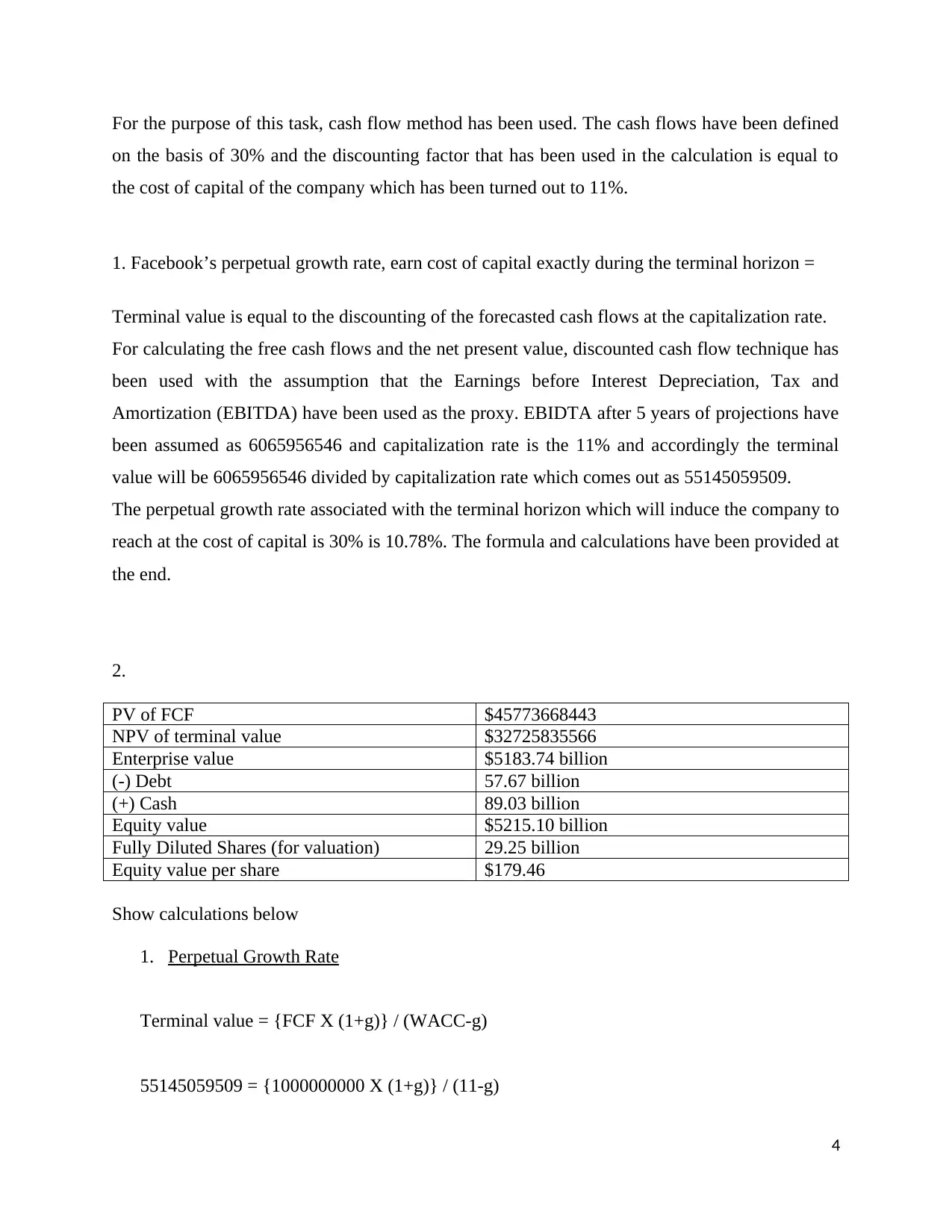

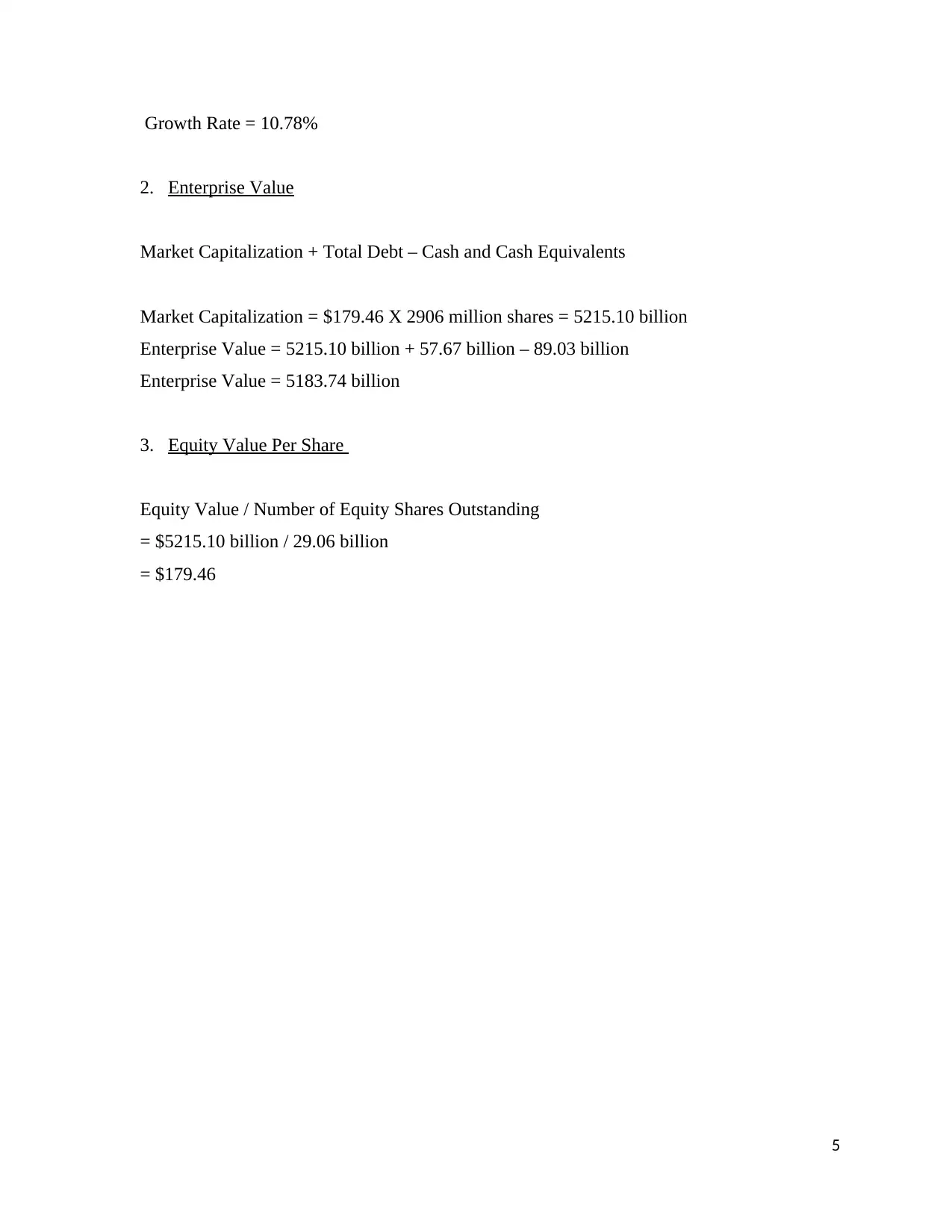

This report provides a comprehensive analysis of the Equifax data breach, examining the psychological factors contributing to the security failure and the application of conceptual frameworks for risk management. It identifies key issues such as excessive optimism in planning and information sharing, confirmation bias, and overconfidence. The report further delves into the financial analysis of Facebook, utilizing the Discounted Cash Flow (DCF) technique to determine a target price. It outlines the methodology, assumptions, and calculations, including the perpetual growth rate, enterprise value, and equity value per share. The report also incorporates the context of Facebook's growth, valuation, and the impact of significant events like acquisitions and stock performance, providing a detailed financial perspective.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.