Macroeconomics Assignment: Policy, Recession, and Inflation Analysis

VerifiedAdded on 2022/09/01

|16

|2969

|28

Homework Assignment

AI Summary

This macroeconomics assignment delves into the core principles of the Keynesian model, exploring how aggregate demand determines national income in the short run. It examines the paradox of thrift, where increased savings can paradoxically lead to a decline in GDP. The assignment further analyzes the impact of expansionary fiscal policy during recessions, illustrating how increased government spending can boost output and employment through the spending multiplier effect. The document also utilizes the IS-LM model to assess the relative effectiveness of monetary and fiscal policies under different circumstances. It contrasts the stagflation of the 1970s with the Great Recession of 2007-08, highlighting differences in causes, policy responses, and effectiveness. Furthermore, the assignment investigates the factors contributing to low inflation rates in the United States, even amidst low unemployment, and discusses the slow recovery of the labor market following the Great Recession. Finally, it explores the stance of monetary policy, the Phillips curve, and the state of financial conditions, providing a comprehensive overview of macroeconomic concepts and their practical implications.

Runing head: MACROECONOMICS

Macroeconomics

Name of the Student

Name of the University

Course ID

Macroeconomics

Name of the Student

Name of the University

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MACROECONOMICS

Table of Contents

Question 1..................................................................................................................................2

Question A.............................................................................................................................2

Question B..............................................................................................................................3

Question C..............................................................................................................................3

Question D.............................................................................................................................4

Question 2..................................................................................................................................5

Question A.............................................................................................................................5

Question B..............................................................................................................................6

Question C..............................................................................................................................7

Question D.............................................................................................................................8

Question 3..................................................................................................................................8

Question A.............................................................................................................................8

Question B..............................................................................................................................9

Question C............................................................................................................................10

Question D...........................................................................................................................12

References................................................................................................................................14

Table of Contents

Question 1..................................................................................................................................2

Question A.............................................................................................................................2

Question B..............................................................................................................................3

Question C..............................................................................................................................3

Question D.............................................................................................................................4

Question 2..................................................................................................................................5

Question A.............................................................................................................................5

Question B..............................................................................................................................6

Question C..............................................................................................................................7

Question D.............................................................................................................................8

Question 3..................................................................................................................................8

Question A.............................................................................................................................8

Question B..............................................................................................................................9

Question C............................................................................................................................10

Question D...........................................................................................................................12

References................................................................................................................................14

2MACROECONOMICS

Question 1

Question A

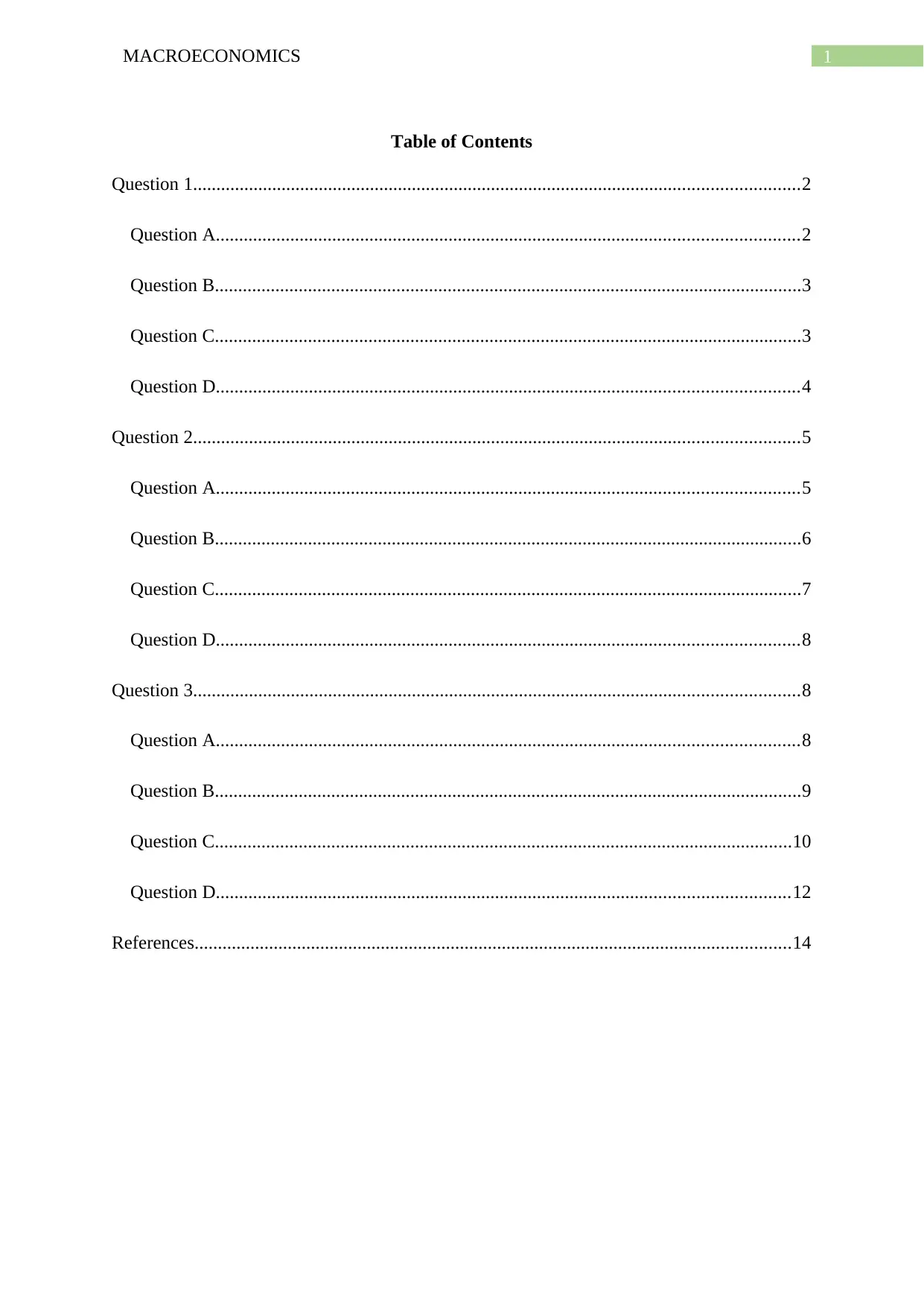

In the Keynesian model, national income in the short run is determined by aggregate

effective demand. The model was initially based upon two sectors consisting household and

business only. Later the model was extended for four sectors where aggregate demand or

aggregate expenditure is the sum of consumption expenditure, investment expenditure,

government expenditure and net earnings from foreign sector (Goodwin et al. 2015).

Equilibrium level of national income in the model is determined where actual spending of the

economy matches with planned spending or aggregate demand. The equation of aggregate

expenditure in the model is given as

AE=C + I +G+ ( X−M )= AD

Figure 1: Determination of national income in Keynesian model

In the above figure, the 450 line shows actual expenditure of the economy. The

planned expenditure line is shown as the sum of consumption, investment, government

expenditure and net export. Equilibrium in the economy corresponds to the point E where

Question 1

Question A

In the Keynesian model, national income in the short run is determined by aggregate

effective demand. The model was initially based upon two sectors consisting household and

business only. Later the model was extended for four sectors where aggregate demand or

aggregate expenditure is the sum of consumption expenditure, investment expenditure,

government expenditure and net earnings from foreign sector (Goodwin et al. 2015).

Equilibrium level of national income in the model is determined where actual spending of the

economy matches with planned spending or aggregate demand. The equation of aggregate

expenditure in the model is given as

AE=C + I +G+ ( X−M )= AD

Figure 1: Determination of national income in Keynesian model

In the above figure, the 450 line shows actual expenditure of the economy. The

planned expenditure line is shown as the sum of consumption, investment, government

expenditure and net export. Equilibrium in the economy corresponds to the point E where

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MACROECONOMICS

aggregate expenditure or demand matches actual expenditure or aggregate supply. Changes in

any component of aggregate spending results in a change in aggregate demand and an

associated change in national income.

Question B

An increase in saving rate is often considered to increase capital formation to increase

causing an increase in GDP. This however is not the case always. Income of a household is

generally divided between consumption and saving. A higher saving propensity actually leads

to a decline in consumption level and income without any increase in rather decrease in

aggregate saving of the economy. The impact of increase in saving propensity explained as

thriftiness of people on equilibrium income, consumption and saving is known as paradox of

thrift. According to Keynes a higher saving rate though is welcome from view of individual

household, it is not good from aggregate perspective since it has a damaging impact on

national income (Uribe and Schmitt-Grohe 2017). The reason for a fall in GDP because of an

increase in saving rate is given as higher saving rate means a lower propensity to consume.

As households consume less, there is a smaller demand for production causing a fall in

induced investment. Because of decline in factor employment there is a fall in income

generation resulting in a smaller GDP.

Question C

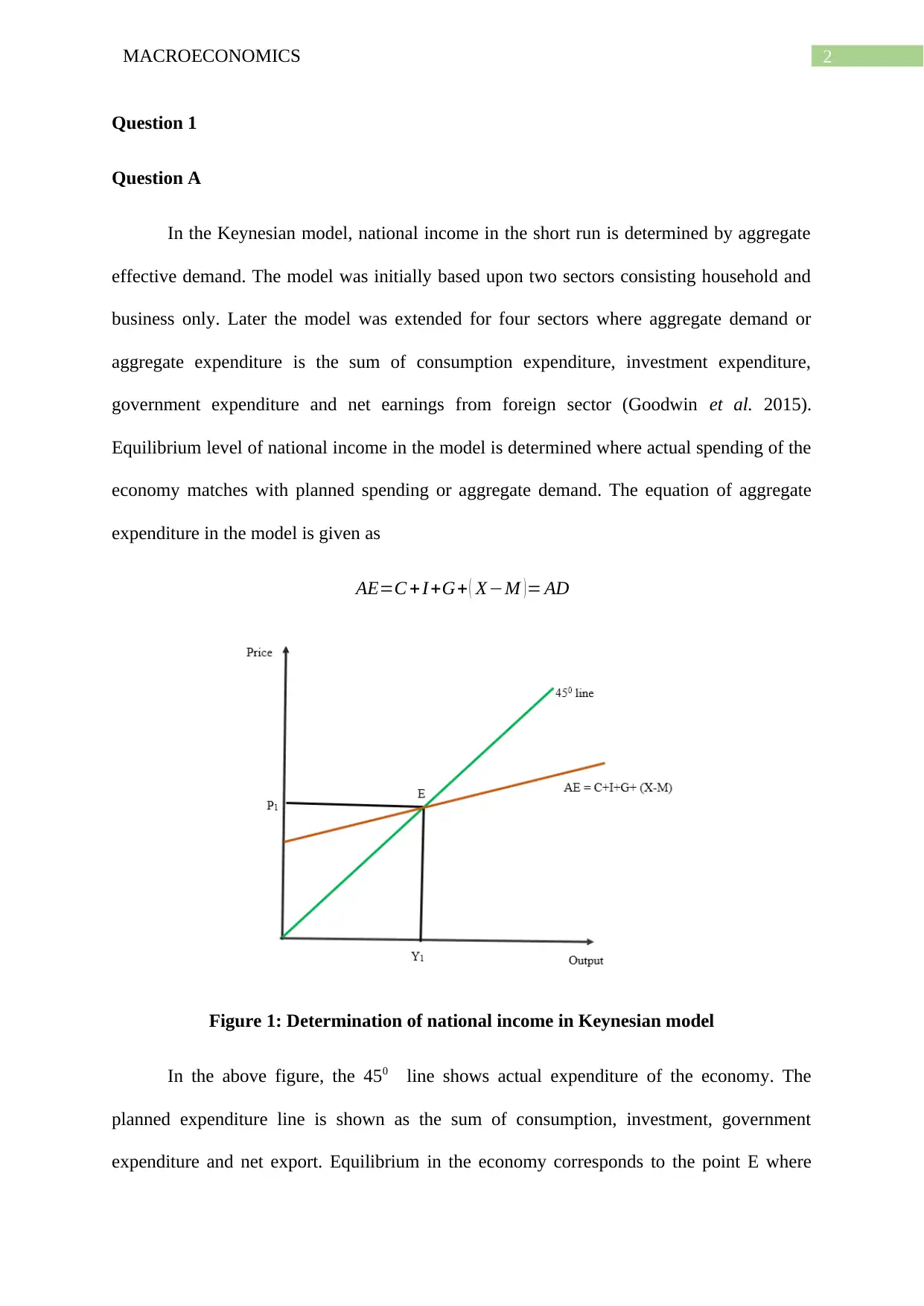

A low output and high unemployment rate indicates recessionary state of the

economy. In such a situation the economy needs necessary policy stimulus from the

government. One way to boost aggregate demand and expand output and employment is to

undertake expansionary fiscal policy by increasing spending. Government expenditure being

one important component of aggregate demand, as government spending increases there is an

aggregate expenditure or demand matches actual expenditure or aggregate supply. Changes in

any component of aggregate spending results in a change in aggregate demand and an

associated change in national income.

Question B

An increase in saving rate is often considered to increase capital formation to increase

causing an increase in GDP. This however is not the case always. Income of a household is

generally divided between consumption and saving. A higher saving propensity actually leads

to a decline in consumption level and income without any increase in rather decrease in

aggregate saving of the economy. The impact of increase in saving propensity explained as

thriftiness of people on equilibrium income, consumption and saving is known as paradox of

thrift. According to Keynes a higher saving rate though is welcome from view of individual

household, it is not good from aggregate perspective since it has a damaging impact on

national income (Uribe and Schmitt-Grohe 2017). The reason for a fall in GDP because of an

increase in saving rate is given as higher saving rate means a lower propensity to consume.

As households consume less, there is a smaller demand for production causing a fall in

induced investment. Because of decline in factor employment there is a fall in income

generation resulting in a smaller GDP.

Question C

A low output and high unemployment rate indicates recessionary state of the

economy. In such a situation the economy needs necessary policy stimulus from the

government. One way to boost aggregate demand and expand output and employment is to

undertake expansionary fiscal policy by increasing spending. Government expenditure being

one important component of aggregate demand, as government spending increases there is an

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MACROECONOMICS

increases in aggregate demand giving a boost to output and employment. This can be

explained with help of the following diagram

Figure 2: Impact of higher spending on output and employment

When government increases its spending, then aggregate demand moves outward as

shown from the rightward movement of aggregate demand from AD to AD1. Because of

expansion of aggregate demand, equilibrium shifts from E to E1. This leads to an increases in

output to Y1 and an increase in price level to P1. As output increases, there is a significant

increase in production creating opportunities for new job and lowers unemployment.

Therefore, during the phase of low output and high unemployment government should to lead

the charge and spend more.

Question D

When government spending increases, GDP increases more than the initial increase in

G. This is because of the working of spending multiplier. An autonomous expansion of

government expenditure results in multiple expansion of national income. The magnitude of

income increase depends on marginal propensity to consume or its reciprocal that is marginal

increases in aggregate demand giving a boost to output and employment. This can be

explained with help of the following diagram

Figure 2: Impact of higher spending on output and employment

When government increases its spending, then aggregate demand moves outward as

shown from the rightward movement of aggregate demand from AD to AD1. Because of

expansion of aggregate demand, equilibrium shifts from E to E1. This leads to an increases in

output to Y1 and an increase in price level to P1. As output increases, there is a significant

increase in production creating opportunities for new job and lowers unemployment.

Therefore, during the phase of low output and high unemployment government should to lead

the charge and spend more.

Question D

When government spending increases, GDP increases more than the initial increase in

G. This is because of the working of spending multiplier. An autonomous expansion of

government expenditure results in multiple expansion of national income. The magnitude of

income increase depends on marginal propensity to consume or its reciprocal that is marginal

5MACROECONOMICS

propensity to save (Agenor and Montiel 2015). The expression for government spending

multiplier can be given as

Δ Y

Δ G = 1

1−MPC = 1

MPS

Since value of MPC lies between 0 and 1, the multiplier value is greater than 1. Since, the

multiplier is larger than 1, following an increase in government expenditure, GDP increases

more than the initial increase in government expenditure. Larger the value of MPC, greater is

the value of multiplier and therefore larger is the change in national income. When

consumers are more willing to spend any increase in their income this implies the marginal

propensity to consume is higher. That means the value of multiplier is larger implying there

will be a larger increase in national income because of an increase in government spending.

Question 2

Question A

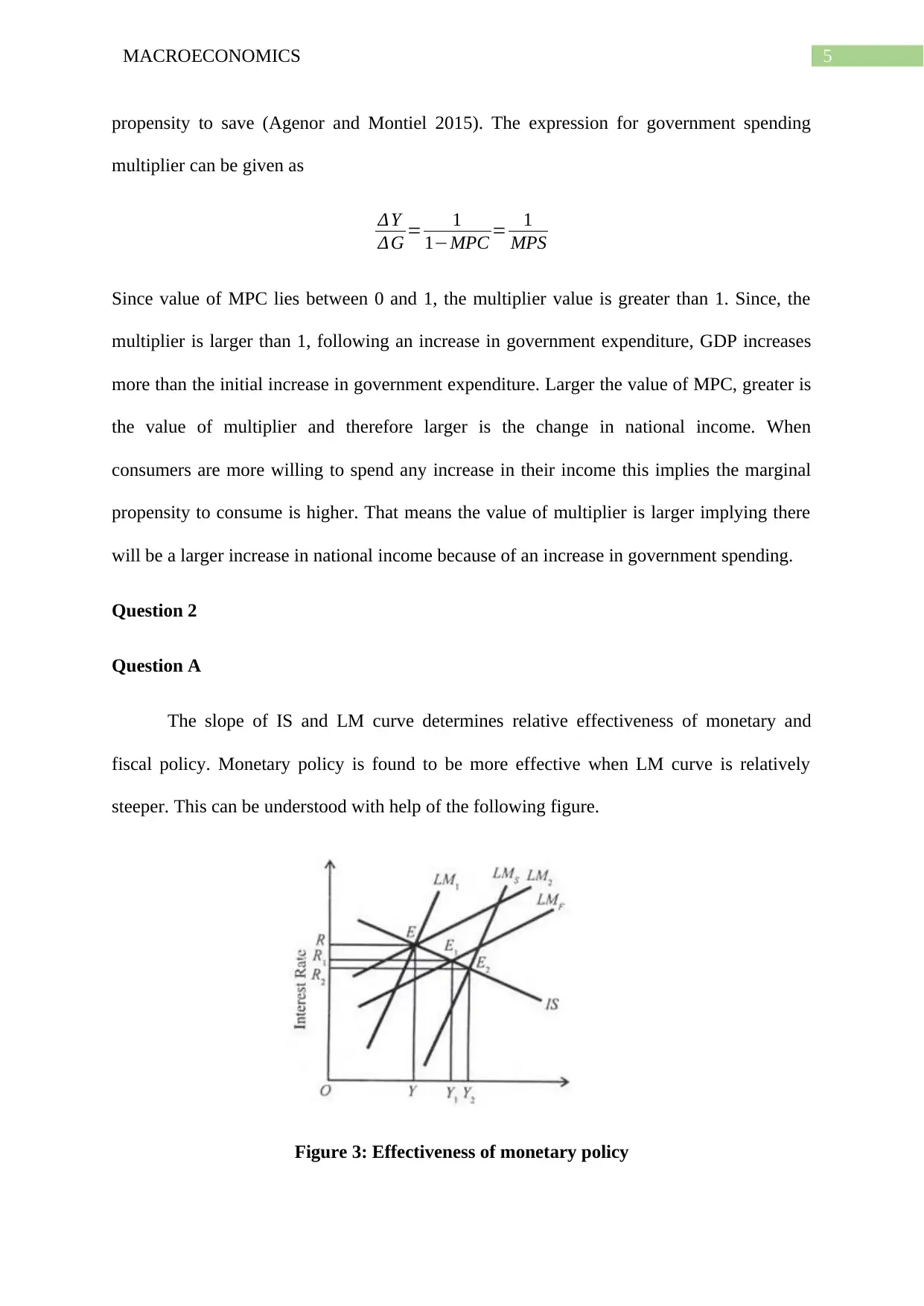

The slope of IS and LM curve determines relative effectiveness of monetary and

fiscal policy. Monetary policy is found to be more effective when LM curve is relatively

steeper. This can be understood with help of the following figure.

Figure 3: Effectiveness of monetary policy

propensity to save (Agenor and Montiel 2015). The expression for government spending

multiplier can be given as

Δ Y

Δ G = 1

1−MPC = 1

MPS

Since value of MPC lies between 0 and 1, the multiplier value is greater than 1. Since, the

multiplier is larger than 1, following an increase in government expenditure, GDP increases

more than the initial increase in government expenditure. Larger the value of MPC, greater is

the value of multiplier and therefore larger is the change in national income. When

consumers are more willing to spend any increase in their income this implies the marginal

propensity to consume is higher. That means the value of multiplier is larger implying there

will be a larger increase in national income because of an increase in government spending.

Question 2

Question A

The slope of IS and LM curve determines relative effectiveness of monetary and

fiscal policy. Monetary policy is found to be more effective when LM curve is relatively

steeper. This can be understood with help of the following figure.

Figure 3: Effectiveness of monetary policy

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MACROECONOMICS

The initial equilibrium in the above figure is at E. As shown in the above figure the

outward shift of steeper LM (LM1 to LMS) leads to a greater increase in income compared to

shift in flatter LM curve (LM2 to LMf).

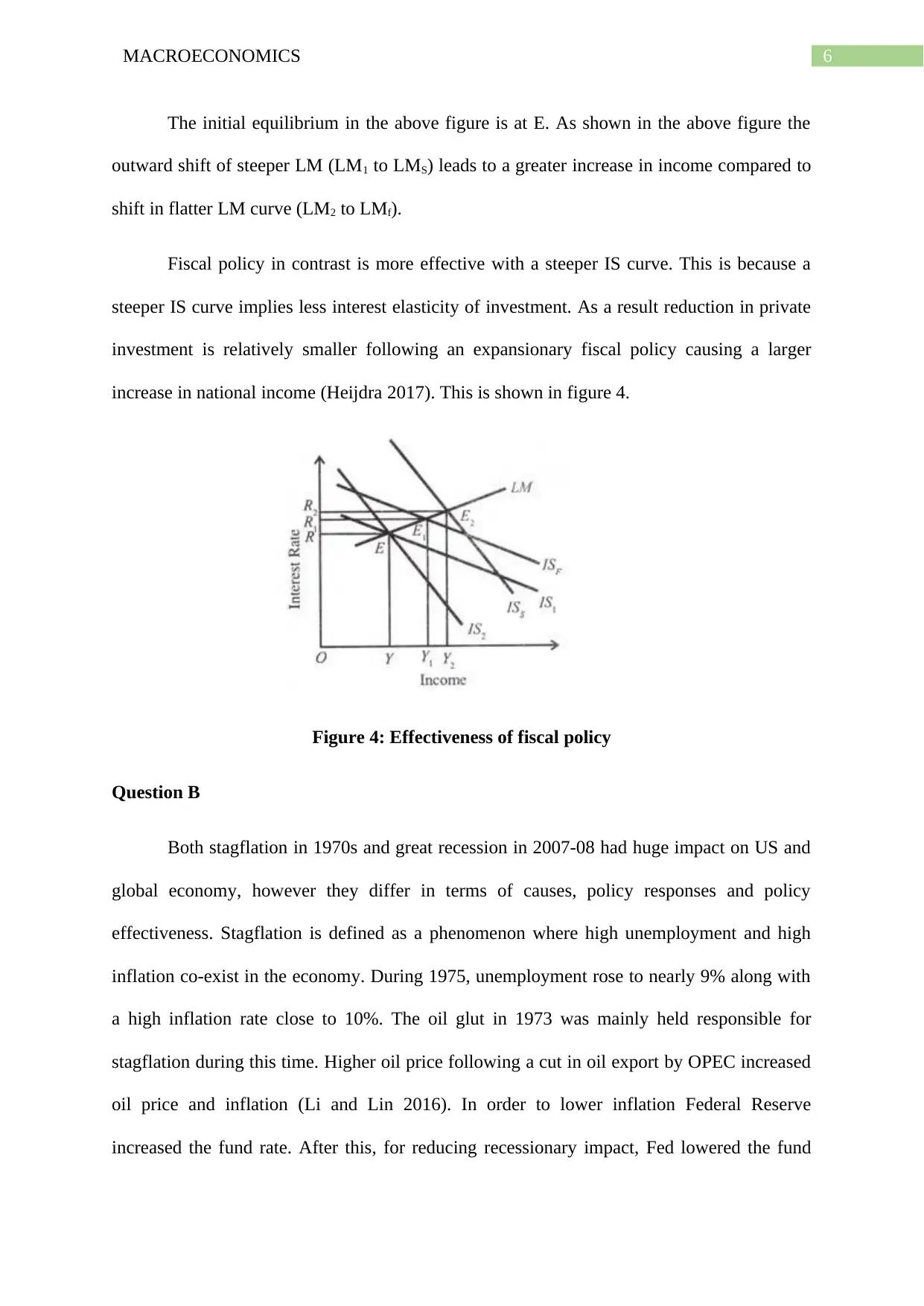

Fiscal policy in contrast is more effective with a steeper IS curve. This is because a

steeper IS curve implies less interest elasticity of investment. As a result reduction in private

investment is relatively smaller following an expansionary fiscal policy causing a larger

increase in national income (Heijdra 2017). This is shown in figure 4.

Figure 4: Effectiveness of fiscal policy

Question B

Both stagflation in 1970s and great recession in 2007-08 had huge impact on US and

global economy, however they differ in terms of causes, policy responses and policy

effectiveness. Stagflation is defined as a phenomenon where high unemployment and high

inflation co-exist in the economy. During 1975, unemployment rose to nearly 9% along with

a high inflation rate close to 10%. The oil glut in 1973 was mainly held responsible for

stagflation during this time. Higher oil price following a cut in oil export by OPEC increased

oil price and inflation (Li and Lin 2016). In order to lower inflation Federal Reserve

increased the fund rate. After this, for reducing recessionary impact, Fed lowered the fund

The initial equilibrium in the above figure is at E. As shown in the above figure the

outward shift of steeper LM (LM1 to LMS) leads to a greater increase in income compared to

shift in flatter LM curve (LM2 to LMf).

Fiscal policy in contrast is more effective with a steeper IS curve. This is because a

steeper IS curve implies less interest elasticity of investment. As a result reduction in private

investment is relatively smaller following an expansionary fiscal policy causing a larger

increase in national income (Heijdra 2017). This is shown in figure 4.

Figure 4: Effectiveness of fiscal policy

Question B

Both stagflation in 1970s and great recession in 2007-08 had huge impact on US and

global economy, however they differ in terms of causes, policy responses and policy

effectiveness. Stagflation is defined as a phenomenon where high unemployment and high

inflation co-exist in the economy. During 1975, unemployment rose to nearly 9% along with

a high inflation rate close to 10%. The oil glut in 1973 was mainly held responsible for

stagflation during this time. Higher oil price following a cut in oil export by OPEC increased

oil price and inflation (Li and Lin 2016). In order to lower inflation Federal Reserve

increased the fund rate. After this, for reducing recessionary impact, Fed lowered the fund

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MACROECONOMICS

rate. This kind of monetary policy confused businesses and worsened the situation. The Fed’s

decision to raise fund rate by 20 percent resulted in further recession in during 1980-82

(Hong-yu 2015).

In contrast to stagflation in 1970s which was the result of aggregate supply shortage

due to higher oil price, the great recession of 2007-08 caused due to subprime mortgage

crisis. The collapse of housing market in United State led to a contraction of liquidity in the

global financial market was the main cause of great recession. The cheap and easy

availability of credit resulted in a housing bubble and a worldwide financial crisis. Policy

measures were taken to revive economic growth (Rich 2019). In United State the

expansionary fiscal policy was undertaken in the form of different stimulatory packages and

tax cuts. Since the traditional stimulatory policies took a greater time government also took

non-traditional avenues. Along with fiscal stimulus, Fed also lowered the fund rate. All the

policies together resulted in a slow but gradual recovery of economic growth.

Question C

Over the last decade, inflation rate in United State was adjusted just above 1-0.5

percent which is well below the Fed’s inflation target of 2 percent. The trend is surprising

since unemployment rate also remained at a historically low level contradicting Phillips curve

relation. Economists have given several possible reasons behind a low inflation since the

global financial crisis. The low inflation expectation is the primary factor that lowered

inflation expectation. With stability in inflation expectation factors such as low level of

unemployment or rise in energy price failed to boost price level (Gkanoutas-Leventis and

Nesvetailova 2015). The decline in oil prices by almost 60 percent had the direct impact of

lowering inflation through a lower price of gasoline and associated energy price. Rapid

spread of globalization is another factor that restrained price level or inflation. With increased

rate. This kind of monetary policy confused businesses and worsened the situation. The Fed’s

decision to raise fund rate by 20 percent resulted in further recession in during 1980-82

(Hong-yu 2015).

In contrast to stagflation in 1970s which was the result of aggregate supply shortage

due to higher oil price, the great recession of 2007-08 caused due to subprime mortgage

crisis. The collapse of housing market in United State led to a contraction of liquidity in the

global financial market was the main cause of great recession. The cheap and easy

availability of credit resulted in a housing bubble and a worldwide financial crisis. Policy

measures were taken to revive economic growth (Rich 2019). In United State the

expansionary fiscal policy was undertaken in the form of different stimulatory packages and

tax cuts. Since the traditional stimulatory policies took a greater time government also took

non-traditional avenues. Along with fiscal stimulus, Fed also lowered the fund rate. All the

policies together resulted in a slow but gradual recovery of economic growth.

Question C

Over the last decade, inflation rate in United State was adjusted just above 1-0.5

percent which is well below the Fed’s inflation target of 2 percent. The trend is surprising

since unemployment rate also remained at a historically low level contradicting Phillips curve

relation. Economists have given several possible reasons behind a low inflation since the

global financial crisis. The low inflation expectation is the primary factor that lowered

inflation expectation. With stability in inflation expectation factors such as low level of

unemployment or rise in energy price failed to boost price level (Gkanoutas-Leventis and

Nesvetailova 2015). The decline in oil prices by almost 60 percent had the direct impact of

lowering inflation through a lower price of gasoline and associated energy price. Rapid

spread of globalization is another factor that restrained price level or inflation. With increased

8MACROECONOMICS

linkage among countries, inflation in US no longer determined by domestic factors. The

ongoing economic slow-down is one factor for core inflation to be low.

Given stability in inflation expectation, it is believed that inflation in United State will

pick up. Some of the forces holding down inflation has started to fade away. With a

diminishing state of labor market slack further downward pressure on labor market will be

diminished from this channel.

Question D

After the great recession during 2007-08, the economy experienced a significant

downfall. Contraction of economic activity during this time reduced labor demand

considerably pushing up the unemployment rate to the peak level of 10 percent. With

economic recovery unemployment though lowered it however took a relatively larger time

for unemployment to get back to pre-recession level (Orhangazi 2015). The main reason for

slow recovery of labor market was inadequate labor demand for a considerably long period.

Wage was also stagnated for working and middle class workers. Because of a very little

structural change in the economy causing inadequate labor demand.

The easing fiscal policy lower private investment through the crowding out effect.

With a high level of private investment there would have a faster expansion of private sectors

causing unemployment rate to fall faster. The ease fiscal policy further resulted in a deficit in

government budget resulting in a lack of funds for further employment opportunity.

Question 3

Question A

The stance of monetary policy is likely to be evaluated depending on a particular

variable or set of variables that are able to capture transmission mechanism of monetary

linkage among countries, inflation in US no longer determined by domestic factors. The

ongoing economic slow-down is one factor for core inflation to be low.

Given stability in inflation expectation, it is believed that inflation in United State will

pick up. Some of the forces holding down inflation has started to fade away. With a

diminishing state of labor market slack further downward pressure on labor market will be

diminished from this channel.

Question D

After the great recession during 2007-08, the economy experienced a significant

downfall. Contraction of economic activity during this time reduced labor demand

considerably pushing up the unemployment rate to the peak level of 10 percent. With

economic recovery unemployment though lowered it however took a relatively larger time

for unemployment to get back to pre-recession level (Orhangazi 2015). The main reason for

slow recovery of labor market was inadequate labor demand for a considerably long period.

Wage was also stagnated for working and middle class workers. Because of a very little

structural change in the economy causing inadequate labor demand.

The easing fiscal policy lower private investment through the crowding out effect.

With a high level of private investment there would have a faster expansion of private sectors

causing unemployment rate to fall faster. The ease fiscal policy further resulted in a deficit in

government budget resulting in a lack of funds for further employment opportunity.

Question 3

Question A

The stance of monetary policy is likely to be evaluated depending on a particular

variable or set of variables that are able to capture transmission mechanism of monetary

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MACROECONOMICS

policy. The variable particularly explaining stance of monetary policy is the short term

interest rate. If actual inflation rate overshoots the targeted rate, then Central bank increases

the interest rate to curb demand and inflation. This is called tight monetary policy. In

contrast, when inflation rate is below the central bank’s targeted rate, Central bank lowers the

interest rate to boost economic activity to push the price level up (Mankiw 2019). This is

known as ease or loose monetary policy. Monetary policy is said to be neutral when Central

bank neither increases nor decreases the interest rate. This happens when inflation rate is line

with targeted inflation rate.

Question B

Phillips curve as given by A.W. Phillips depicts an inverse relation between

unemployment and inflation rate. That is inflation increases with fall in unemployment and

vice-versa.

Because of the inverse relation between inflation and unemployment, Phillips curve

slopes downward. This is because during economic boom, labor demand increases resulting

in a fall in unemployment rate. A higher labor demand in turn increases bargaining power of

workers pushing up wage inflation.

A flatter Phillips curve implies that there is a relatively softer relation between wage

inflation and unemployment. This in turn suggests that unemployment rate can further be

reduced without upward pressure on price level.

A flat Phillips curve means a softer relation between output and price level implying a

steeper Aggregate Supply curve.

When Phillips curve is flatter the combination of output variability and inflation

become less favorable. The central bank therefore needs to generate a greater variability in

the domestic demand for achieving the desired inflation target. The softer relation between

policy. The variable particularly explaining stance of monetary policy is the short term

interest rate. If actual inflation rate overshoots the targeted rate, then Central bank increases

the interest rate to curb demand and inflation. This is called tight monetary policy. In

contrast, when inflation rate is below the central bank’s targeted rate, Central bank lowers the

interest rate to boost economic activity to push the price level up (Mankiw 2019). This is

known as ease or loose monetary policy. Monetary policy is said to be neutral when Central

bank neither increases nor decreases the interest rate. This happens when inflation rate is line

with targeted inflation rate.

Question B

Phillips curve as given by A.W. Phillips depicts an inverse relation between

unemployment and inflation rate. That is inflation increases with fall in unemployment and

vice-versa.

Because of the inverse relation between inflation and unemployment, Phillips curve

slopes downward. This is because during economic boom, labor demand increases resulting

in a fall in unemployment rate. A higher labor demand in turn increases bargaining power of

workers pushing up wage inflation.

A flatter Phillips curve implies that there is a relatively softer relation between wage

inflation and unemployment. This in turn suggests that unemployment rate can further be

reduced without upward pressure on price level.

A flat Phillips curve means a softer relation between output and price level implying a

steeper Aggregate Supply curve.

When Phillips curve is flatter the combination of output variability and inflation

become less favorable. The central bank therefore needs to generate a greater variability in

the domestic demand for achieving the desired inflation target. The softer relation between

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MACROECONOMICS

inflation and unemployment makes it easier for central bank to take policies to boost

employment since it does not increase inflationary pressure much.

Question C

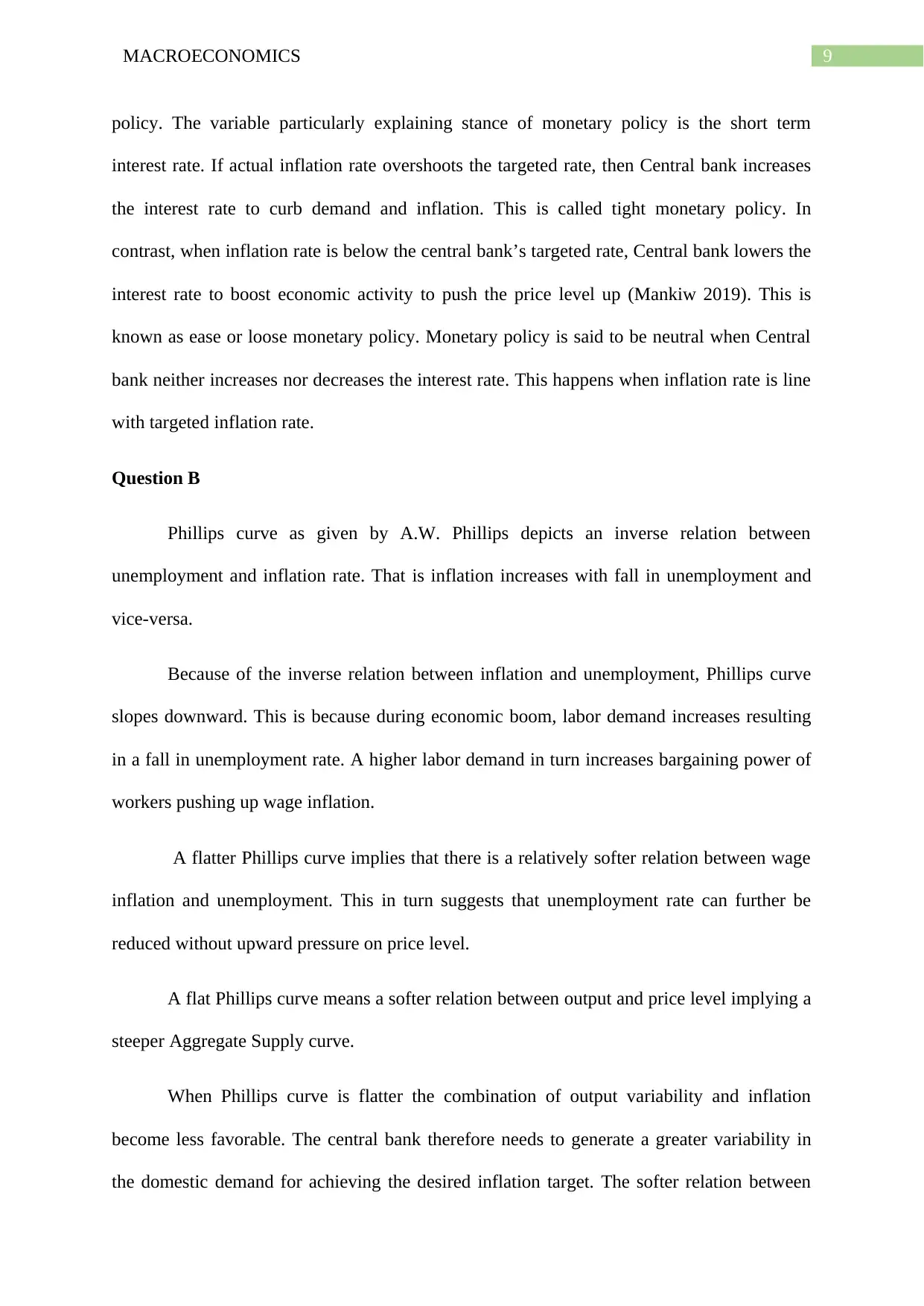

The financial condition refers to state of different components related to overall

financial health of the economy. The four important components for analyzing financial

conditions are US dollar, corporate bonds spread, equity market level and level of interest in

different maturities.

Figure 5: Trend in US dollar index

(Tradingeconomics.com. 2020)

As shown in the above figure in the beginning of 2019, the value of US dollar though

increased it however started to decline since October and continues to fall.

inflation and unemployment makes it easier for central bank to take policies to boost

employment since it does not increase inflationary pressure much.

Question C

The financial condition refers to state of different components related to overall

financial health of the economy. The four important components for analyzing financial

conditions are US dollar, corporate bonds spread, equity market level and level of interest in

different maturities.

Figure 5: Trend in US dollar index

(Tradingeconomics.com. 2020)

As shown in the above figure in the beginning of 2019, the value of US dollar though

increased it however started to decline since October and continues to fall.

11MACROECONOMICS

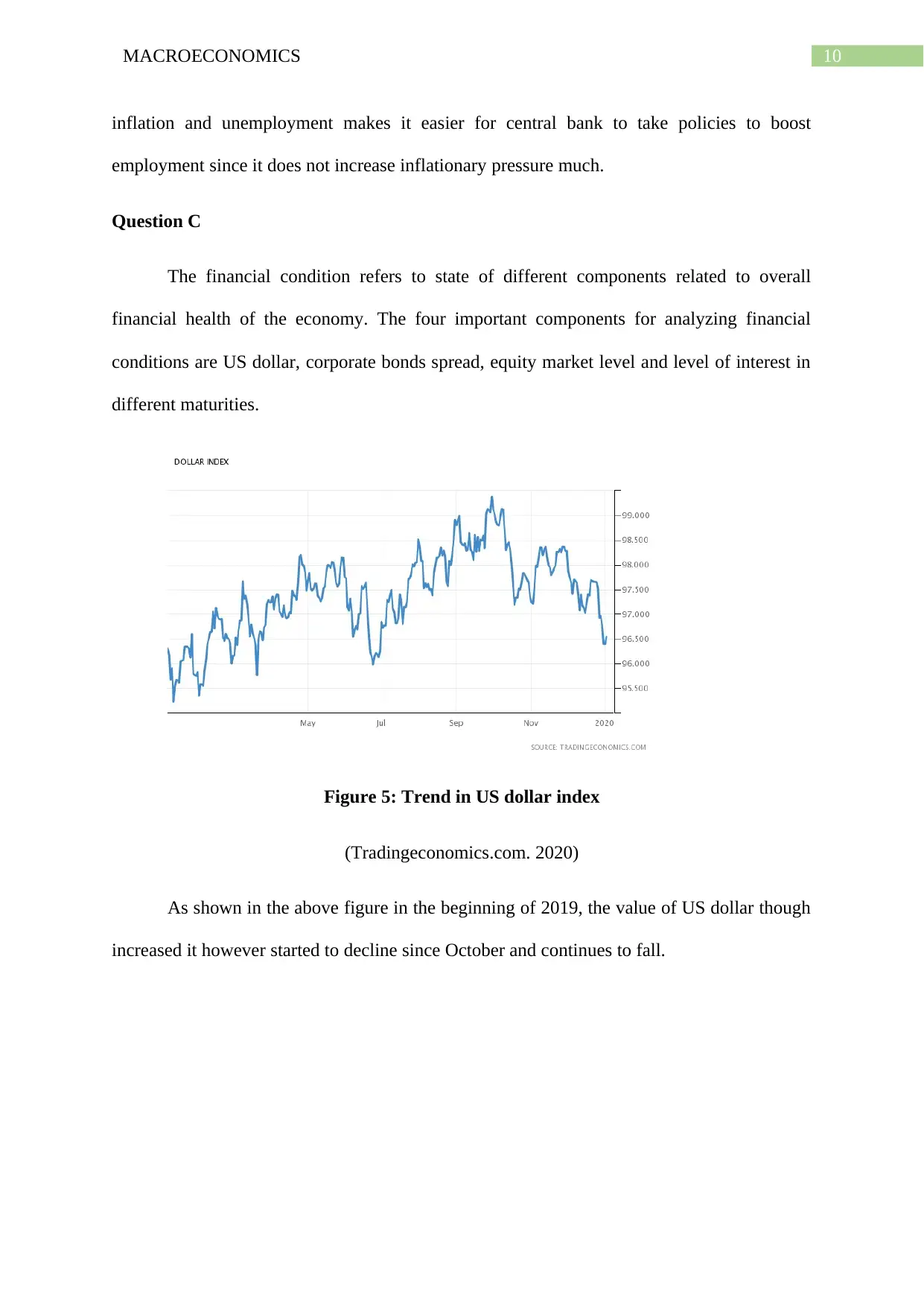

Figure 6: Trend in bond yield

(markets.businessinsider.com 2020)

The bond market yield shows that there is a decline in bond market yield in the last 1

year indicating a weak performance.

Figure 6: Trend in bond yield

(markets.businessinsider.com 2020)

The bond market yield shows that there is a decline in bond market yield in the last 1

year indicating a weak performance.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.