HI5020 Corporate Accounting: Comparative Report of Two Companies

VerifiedAdded on 2023/06/04

|23

|4282

|457

Report

AI Summary

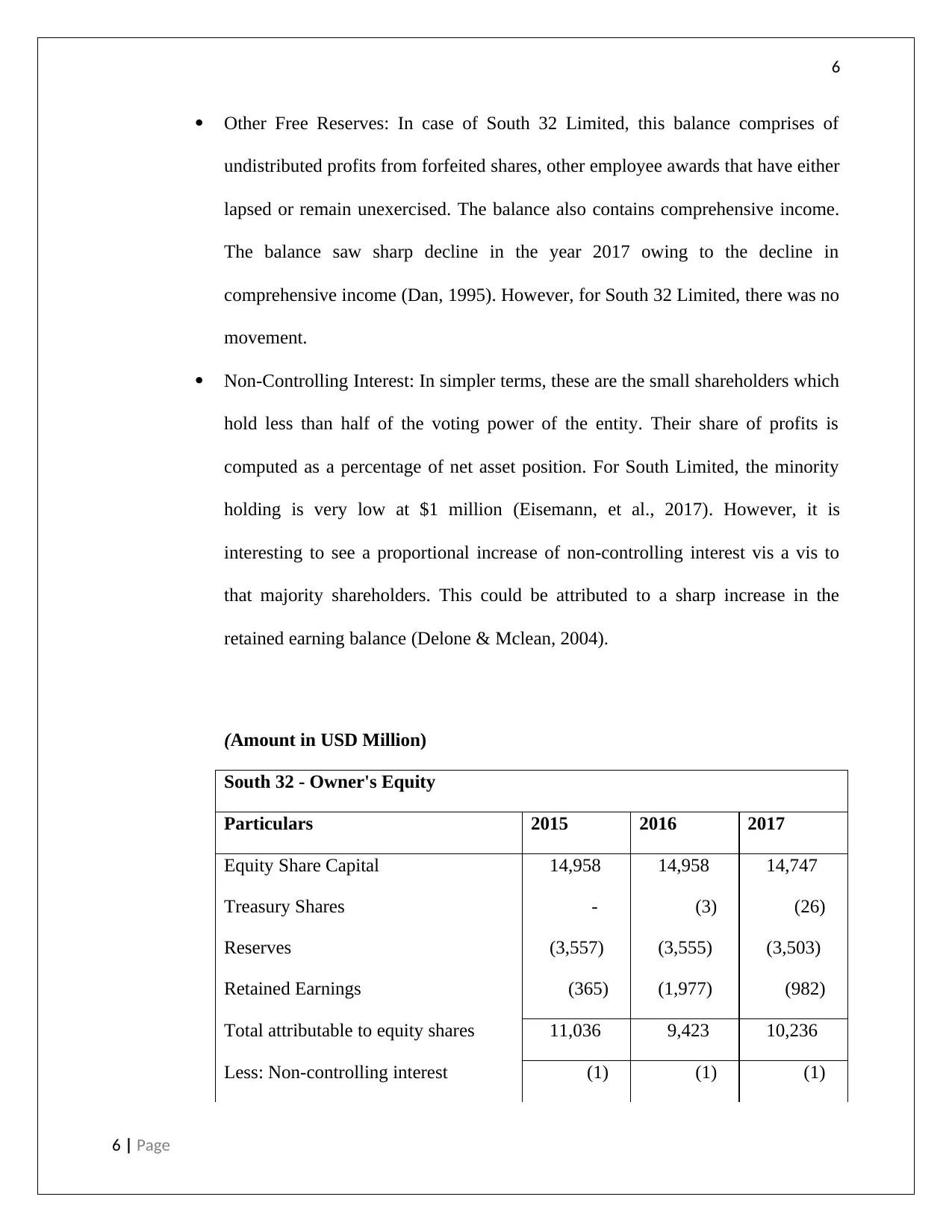

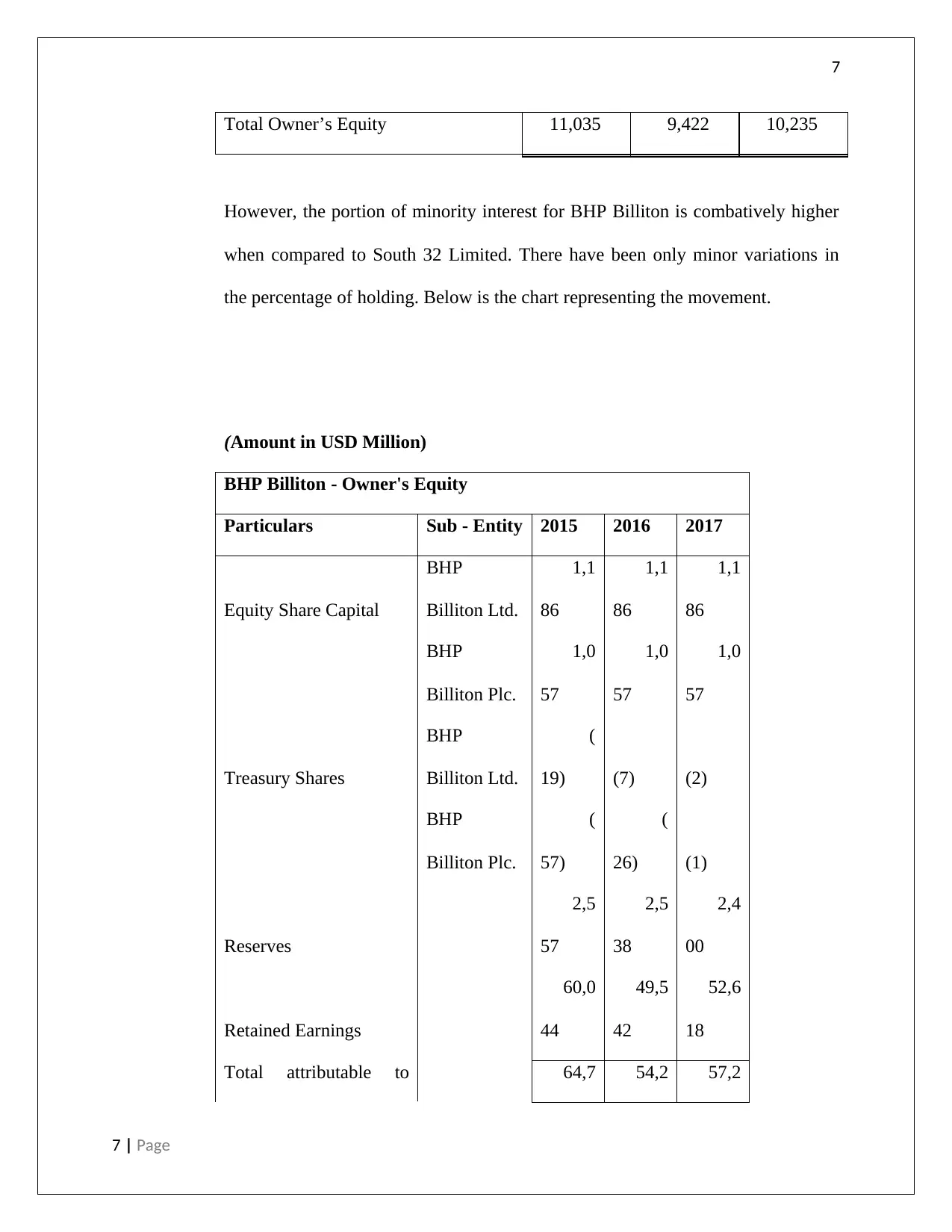

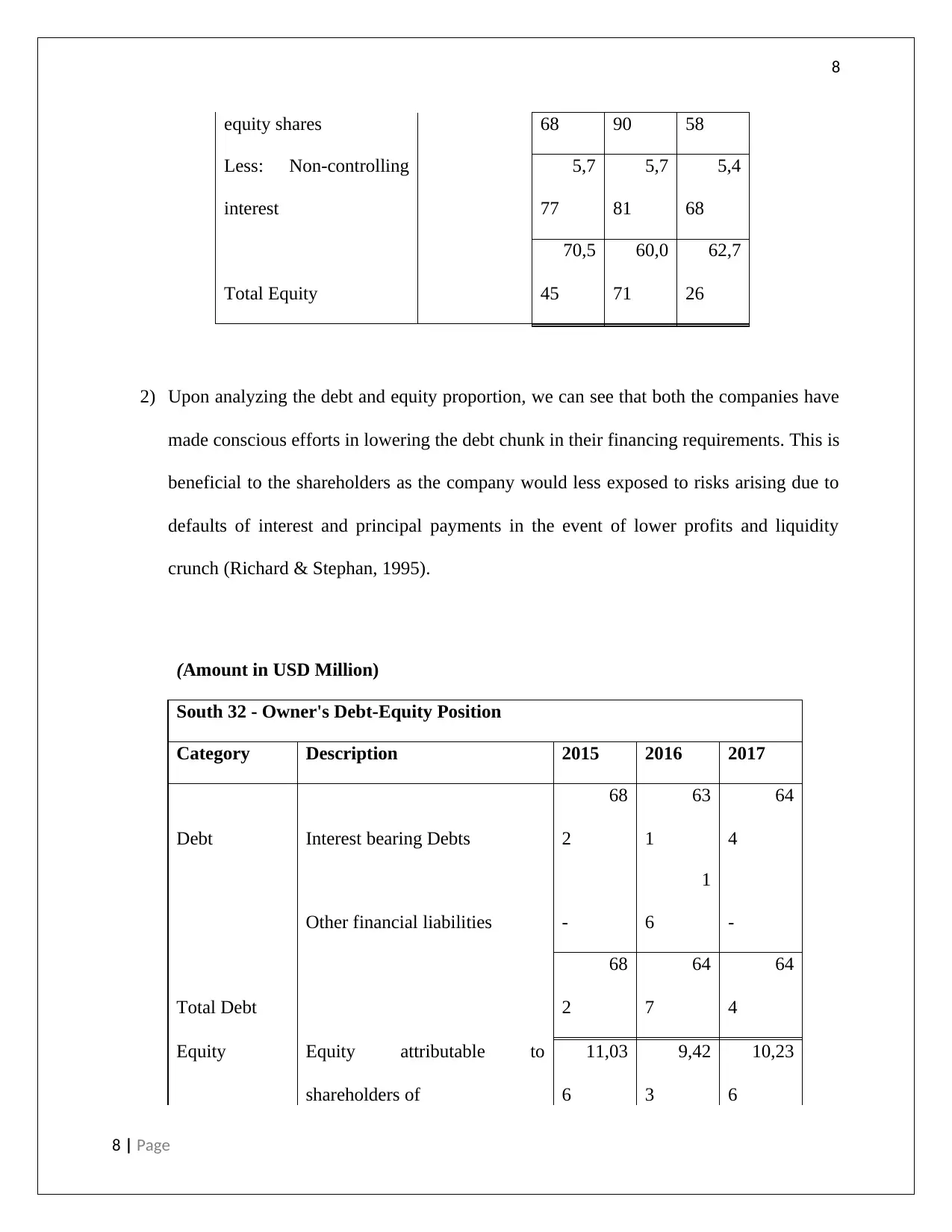

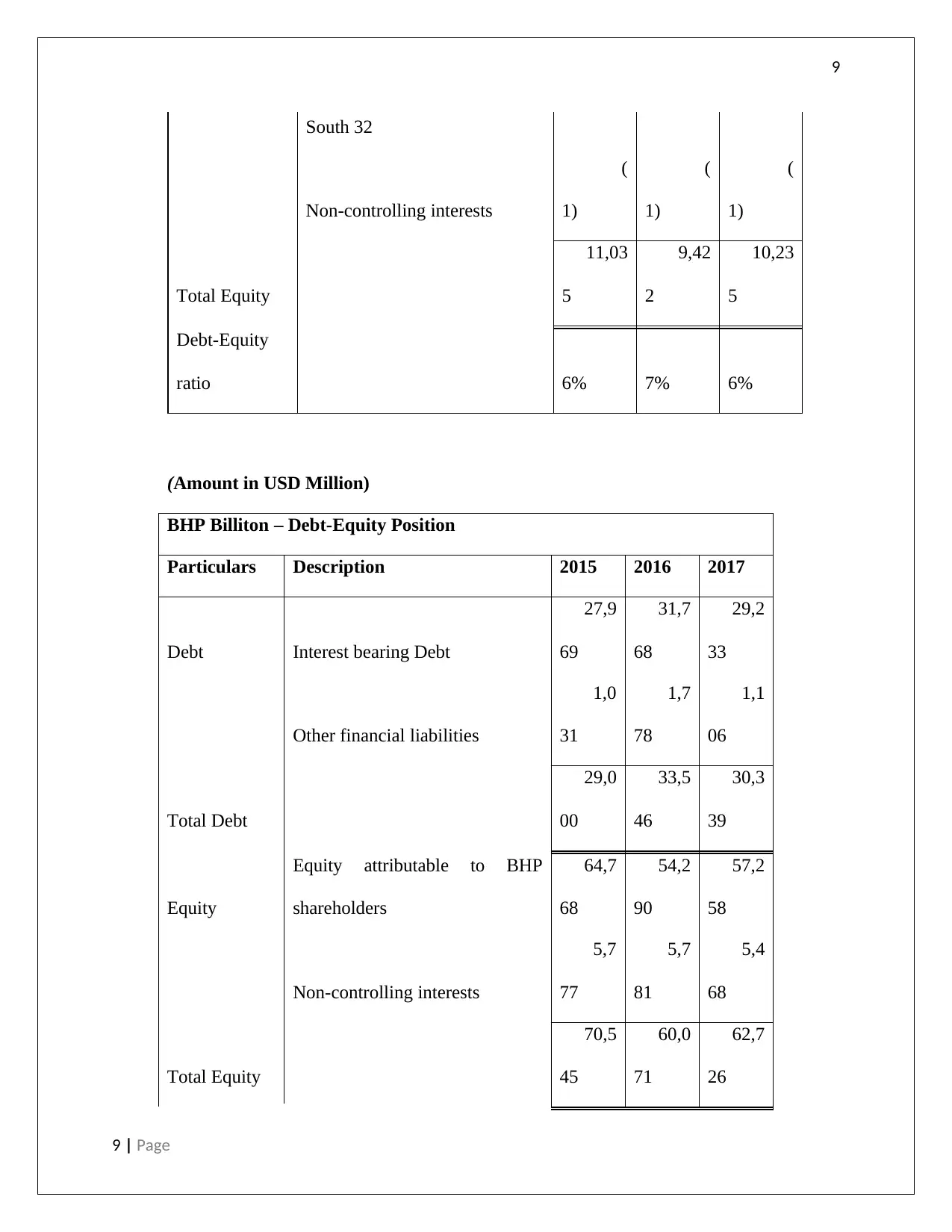

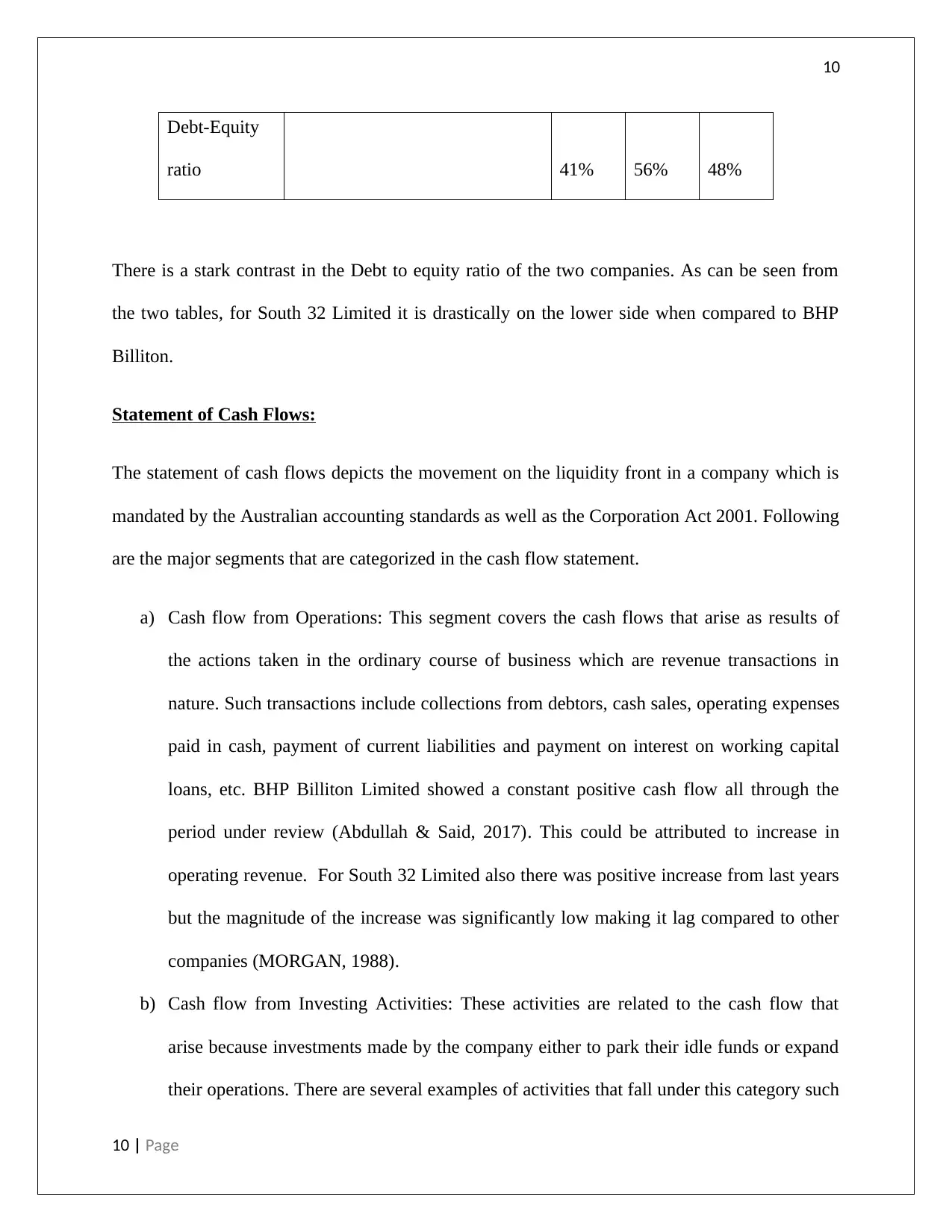

This report presents a comparative analysis of the financial performance of BHP Billiton Limited and South32 Limited, both listed on the Australian Securities Exchange (ASX). The report examines the companies' owner's equity, analyzing components like equity share capital, retained earnings, and other reserves over the period from 2015 to 2017. It also delves into the cash flow statements, categorizing cash flows from operations, investing activities, and financing activities. Furthermore, the analysis includes a comparison of the debt-equity ratios of the two companies, highlighting their financing strategies. The report provides a detailed overview of the financial positions of both companies, offering insights into their performance and financial health. The report follows the structure of the assignment brief, including an executive summary, introduction, body, conclusion and references.

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.