Equity Valuation And Analysis (Pdf)

VerifiedAdded on 2021/02/19

|9

|1631

|120

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

EQUITY VALUATION AND

ANALYSIS

ANALYSIS

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

Evaluate the strategy of the subject company, including its industry environment, competitive

position, corporate strategy and financial strategy..........................................................................1

Evaluate the company’s accounting policies and methods and identify red flags of inappropriate

accounting treatments......................................................................................................................2

Estimate the implications of accounting policies and perform accounting adjustments where

applicable.........................................................................................................................................2

CONCLUSION................................................................................................................................3

REFERENCES................................................................................................................................4

APPENDIX....................................................................................................................................................5

Table 1Free cash flow......................................................................................................................5

Table 2Percentage of sales...............................................................................................................5

Table 3Calculation of cost of equity................................................................................................5

Table 4WACC calculation...............................................................................................................6

Table 5Terminal value calculation..................................................................................................6

Table 6Equity value and intrinsic value of share.............................................................................7

INTRODUCTION...........................................................................................................................1

Evaluate the strategy of the subject company, including its industry environment, competitive

position, corporate strategy and financial strategy..........................................................................1

Evaluate the company’s accounting policies and methods and identify red flags of inappropriate

accounting treatments......................................................................................................................2

Estimate the implications of accounting policies and perform accounting adjustments where

applicable.........................................................................................................................................2

CONCLUSION................................................................................................................................3

REFERENCES................................................................................................................................4

APPENDIX....................................................................................................................................................5

Table 1Free cash flow......................................................................................................................5

Table 2Percentage of sales...............................................................................................................5

Table 3Calculation of cost of equity................................................................................................5

Table 4WACC calculation...............................................................................................................6

Table 5Terminal value calculation..................................................................................................6

Table 6Equity value and intrinsic value of share.............................................................................7

INTRODUCTION

Rio Tinto is known for large mining operations and use of innovative technology across

globe. Firm is currently listed in Australia stock exchange. In current report equity valuation of

Rio Tinto shares is done. In this regard DCF method is used. Apart from this, in the report

strategy followed by company, industry environment, competitive position of the firm, corporate

strategy and financial strategy is also discussed in detail. All these are taken in to account in

order to justify current equity value which is higher then value identified in DCF approach. At

end of the report, accounting approach which is wrongly used by the firm is identified and point

where improvement need to be made is identified. In this way, entire research work is carried

out.

Evaluate the strategy of the subject company, including its industry

environment, competitive position, corporate strategy and financial

strategy

Rio Tinto is one of Australia largest mining company. In year 2018 and 2019 strong fluctuations

are observed in country economic condition and also across the world. Such kind of conditions

create challenge for Rio Tinto to maintain consistency in earning of profit in the business.

Mentioned firm is following strategy under which it is focusing on 4 p’s which stand for

portfolio, performance, people and partners (Martin-Izard and et.al., 2015). Its strategy is to

make investment in assets which are reach and are mostly unexplored till the date. It focused on

safety of its employees and providing good working environment so that more and more can be

retained in the business which ultimately lead to good business performance. Firm focus is on

developing its technical and commercial capability and it is done by focusing on making

investment on HR. Ultimately, skill development of employees happened which benefit both

employees and firm. Rio Tinto is consistently focusing on making its current partnership strong

with suppliers and also adding new one in its supply chain (Martin-Izard. and et.al., 2015). Thus,

it can be said that firm is focusing on multiple fronts to ensure consistent business growth.

Industry condition is not so good as GDP of Australia is growing at low rate of 7% and

unemployement rate is 5%. Demand for house also reduced. Moreover, economic condition

1

Rio Tinto is known for large mining operations and use of innovative technology across

globe. Firm is currently listed in Australia stock exchange. In current report equity valuation of

Rio Tinto shares is done. In this regard DCF method is used. Apart from this, in the report

strategy followed by company, industry environment, competitive position of the firm, corporate

strategy and financial strategy is also discussed in detail. All these are taken in to account in

order to justify current equity value which is higher then value identified in DCF approach. At

end of the report, accounting approach which is wrongly used by the firm is identified and point

where improvement need to be made is identified. In this way, entire research work is carried

out.

Evaluate the strategy of the subject company, including its industry

environment, competitive position, corporate strategy and financial

strategy

Rio Tinto is one of Australia largest mining company. In year 2018 and 2019 strong fluctuations

are observed in country economic condition and also across the world. Such kind of conditions

create challenge for Rio Tinto to maintain consistency in earning of profit in the business.

Mentioned firm is following strategy under which it is focusing on 4 p’s which stand for

portfolio, performance, people and partners (Martin-Izard and et.al., 2015). Its strategy is to

make investment in assets which are reach and are mostly unexplored till the date. It focused on

safety of its employees and providing good working environment so that more and more can be

retained in the business which ultimately lead to good business performance. Firm focus is on

developing its technical and commercial capability and it is done by focusing on making

investment on HR. Ultimately, skill development of employees happened which benefit both

employees and firm. Rio Tinto is consistently focusing on making its current partnership strong

with suppliers and also adding new one in its supply chain (Martin-Izard. and et.al., 2015). Thus,

it can be said that firm is focusing on multiple fronts to ensure consistent business growth.

Industry condition is not so good as GDP of Australia is growing at low rate of 7% and

unemployement rate is 5%. Demand for house also reduced. Moreover, economic condition

1

globally is also not good, China which is main market for Rio Tinto also observe decline in its

GDP growth rate from past few years. Thus, mining industry is facing lots of problems in current

time period.

Rio Tinto is highly competitive relative to rivals as it can be observed that it is focusing

on cost cutting through technology advancement. Firm is having long term contracts which

ensure that firm will have customers on regular basis. This make firm competitive to its rivals.

Under corporate strategy business firm is adding new products in its portfolio so that

business can be expand at rapid pace (Thibeault, Mézin and Martin, 2016). On other hand, cost

control is another area where firm is currently focusing under its corporate strategy. Under

financial strategy firm is doing capital allocation policy whereby first of all capital is kept aside

for investment in the business and few portions is used to pay dividend to shareholders. If any

amount remain aside same is used to make debt payment. By doing so firm time to time meet all

its obligations.

Company fair value is AUD 5 and current market price is AUD 49. This reflect that firm

shares are overvalued. Investors have lot of confidence on Rio Tinto due to its innovative

business operations and because of this more and more investors are making purchase of

mentioned firm shares. Hence, price of security is overvalued in the market.

Evaluate the company’s accounting policies and methods and identify red flags of

inappropriate accounting treatments

Under accounting policy firm is using impairment methods to revalue its assets so that true

financial position can be assessed. Under this policy Rio Tinto is using discounted value

approach under which present value of asset is computed (Rio Tinto annual report., 2018). There

are number of approaches that can be used by the firm to revalue its asset and one of them is

discounting method. Use of this approach prove wrong as number of cases are filed against Rio

Tinto in Mozambique and other African nations. Thus, on this point Rio Tinto need to pay due

attention to improve its business accounting operation.

Estimate the implications of accounting policies and perform accounting

adjustments where applicable

As discussed above there is loophole in firm accounting policy and it is not using

impairment approaches in proper manner. Rio Tinto must regularly use discounted method but it

must ensure that cash flows are predicted accurately. If cash flow will be computed wrongly then

2

GDP growth rate from past few years. Thus, mining industry is facing lots of problems in current

time period.

Rio Tinto is highly competitive relative to rivals as it can be observed that it is focusing

on cost cutting through technology advancement. Firm is having long term contracts which

ensure that firm will have customers on regular basis. This make firm competitive to its rivals.

Under corporate strategy business firm is adding new products in its portfolio so that

business can be expand at rapid pace (Thibeault, Mézin and Martin, 2016). On other hand, cost

control is another area where firm is currently focusing under its corporate strategy. Under

financial strategy firm is doing capital allocation policy whereby first of all capital is kept aside

for investment in the business and few portions is used to pay dividend to shareholders. If any

amount remain aside same is used to make debt payment. By doing so firm time to time meet all

its obligations.

Company fair value is AUD 5 and current market price is AUD 49. This reflect that firm

shares are overvalued. Investors have lot of confidence on Rio Tinto due to its innovative

business operations and because of this more and more investors are making purchase of

mentioned firm shares. Hence, price of security is overvalued in the market.

Evaluate the company’s accounting policies and methods and identify red flags of

inappropriate accounting treatments

Under accounting policy firm is using impairment methods to revalue its assets so that true

financial position can be assessed. Under this policy Rio Tinto is using discounted value

approach under which present value of asset is computed (Rio Tinto annual report., 2018). There

are number of approaches that can be used by the firm to revalue its asset and one of them is

discounting method. Use of this approach prove wrong as number of cases are filed against Rio

Tinto in Mozambique and other African nations. Thus, on this point Rio Tinto need to pay due

attention to improve its business accounting operation.

Estimate the implications of accounting policies and perform accounting

adjustments where applicable

As discussed above there is loophole in firm accounting policy and it is not using

impairment approaches in proper manner. Rio Tinto must regularly use discounted method but it

must ensure that cash flows are predicted accurately. If cash flow will be computed wrongly then

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

wrong value of asset can be computed which lead to computation of wrong value of asset. All

these things lead to preparation of inaccurate financial statements and making of wrong business

decisions (Mavris and et.al., 2018). Thus, cash flows must be based on some solid assumptions

so that relevant approach can be used accurately and proper decisions can be made in respect to

business.

CONCLUSION

At end of the report, it is concluded that there is significant importance of the discounted

cash flow approach because it assists firm in identifying actual value of its shares which further

reflect whether firm shares are overvalued or undervalued in the market. It is also concluded that

there are some calculations in accounting which require judgement. In case of judgement firm

must make decision based on assumptions which have solid foundations. In absence such kind of

strong logic wrong cash flows are estimated which lead to computation of wrong value of assets.

3

these things lead to preparation of inaccurate financial statements and making of wrong business

decisions (Mavris and et.al., 2018). Thus, cash flows must be based on some solid assumptions

so that relevant approach can be used accurately and proper decisions can be made in respect to

business.

CONCLUSION

At end of the report, it is concluded that there is significant importance of the discounted

cash flow approach because it assists firm in identifying actual value of its shares which further

reflect whether firm shares are overvalued or undervalued in the market. It is also concluded that

there are some calculations in accounting which require judgement. In case of judgement firm

must make decision based on assumptions which have solid foundations. In absence such kind of

strong logic wrong cash flows are estimated which lead to computation of wrong value of assets.

3

REFERENCES

Books and Journals

Kaplan, H.H. and et.al., 2016. Orbital evidence for clay and acidic sulfate assemblages on Mars

based on mineralogical analogs from Rio Tinto, Spain. Icarus. 275. pp.45-64.

Martin-Izard, A. and et.al., 2015. A new 3D geological model and interpretation of structural

evolution of the world-class Rio Tinto VMS deposit, Iberian Pyrite Belt (Spain). Ore

Geology Reviews. 71. pp.457-476.

Mavris, C. and et.al., 2018. Diverse mineral assemblages of acidic alteration in the Rio Tinto

area (southwest Spain): Implications for Mars. American Mineralogist. 103(12). pp.1877-

1890.

Thibeault, P., Mézin, H. and Martin, O., 2016. Rio Tinto AP44 cell technology development at

alma smelter. In Light Metals 2016 (pp. 295-300). Springer, Cham.

Online

Rio Tinto annual report., 2018. [Online]. Available through:<

http://www.riotinto.com/documents/RT_2018_annual_report.pdf>.

4

Books and Journals

Kaplan, H.H. and et.al., 2016. Orbital evidence for clay and acidic sulfate assemblages on Mars

based on mineralogical analogs from Rio Tinto, Spain. Icarus. 275. pp.45-64.

Martin-Izard, A. and et.al., 2015. A new 3D geological model and interpretation of structural

evolution of the world-class Rio Tinto VMS deposit, Iberian Pyrite Belt (Spain). Ore

Geology Reviews. 71. pp.457-476.

Mavris, C. and et.al., 2018. Diverse mineral assemblages of acidic alteration in the Rio Tinto

area (southwest Spain): Implications for Mars. American Mineralogist. 103(12). pp.1877-

1890.

Thibeault, P., Mézin, H. and Martin, O., 2016. Rio Tinto AP44 cell technology development at

alma smelter. In Light Metals 2016 (pp. 295-300). Springer, Cham.

Online

Rio Tinto annual report., 2018. [Online]. Available through:<

http://www.riotinto.com/documents/RT_2018_annual_report.pdf>.

4

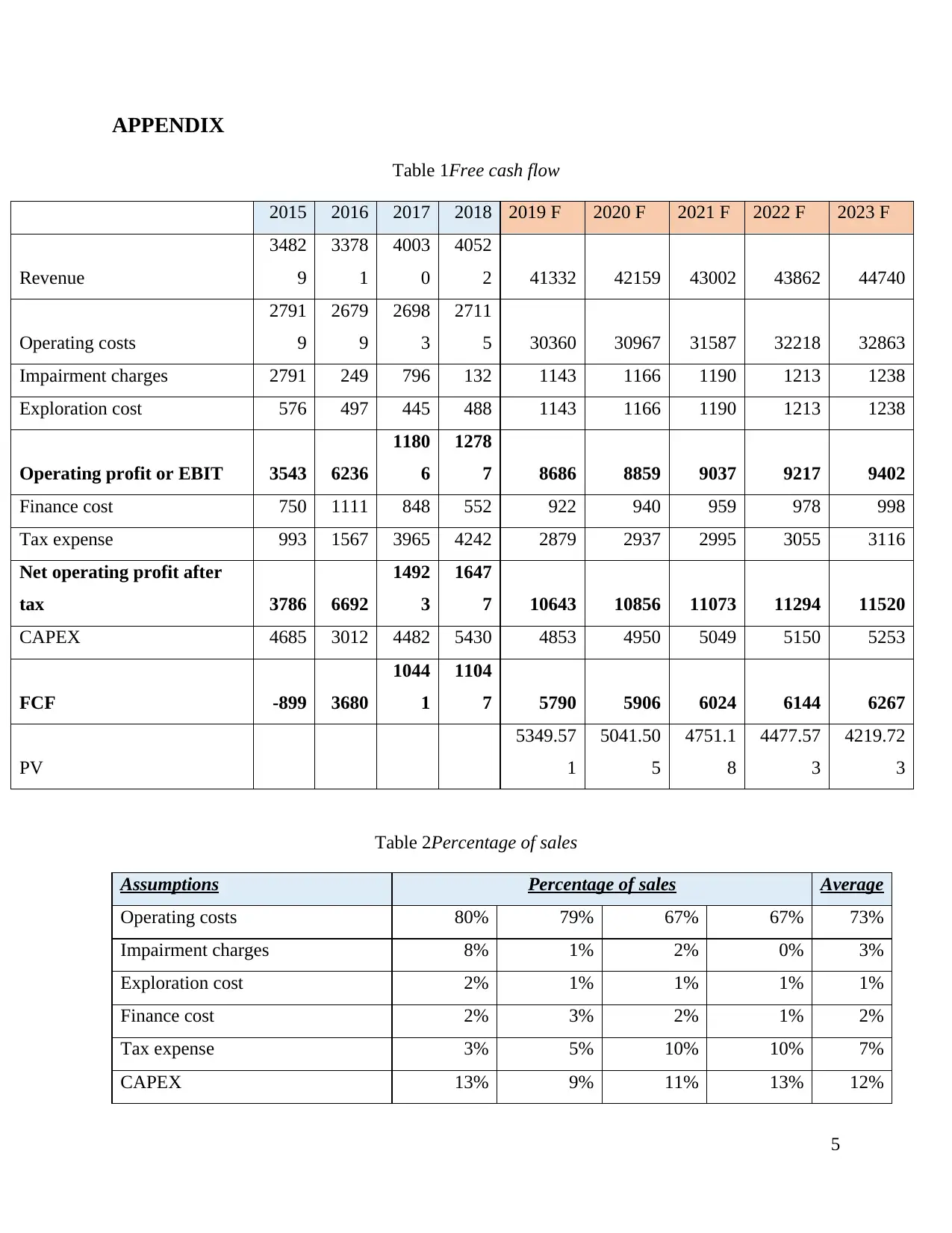

APPENDIX

Table 1Free cash flow

2015 2016 2017 2018 2019 F 2020 F 2021 F 2022 F 2023 F

Revenue

3482

9

3378

1

4003

0

4052

2 41332 42159 43002 43862 44740

Operating costs

2791

9

2679

9

2698

3

2711

5 30360 30967 31587 32218 32863

Impairment charges 2791 249 796 132 1143 1166 1190 1213 1238

Exploration cost 576 497 445 488 1143 1166 1190 1213 1238

Operating profit or EBIT 3543 6236

1180

6

1278

7 8686 8859 9037 9217 9402

Finance cost 750 1111 848 552 922 940 959 978 998

Tax expense 993 1567 3965 4242 2879 2937 2995 3055 3116

Net operating profit after

tax 3786 6692

1492

3

1647

7 10643 10856 11073 11294 11520

CAPEX 4685 3012 4482 5430 4853 4950 5049 5150 5253

FCF -899 3680

1044

1

1104

7 5790 5906 6024 6144 6267

PV

5349.57

1

5041.50

5

4751.1

8

4477.57

3

4219.72

3

Table 2Percentage of sales

Assumptions Percentage of sales Average

Operating costs 80% 79% 67% 67% 73%

Impairment charges 8% 1% 2% 0% 3%

Exploration cost 2% 1% 1% 1% 1%

Finance cost 2% 3% 2% 1% 2%

Tax expense 3% 5% 10% 10% 7%

CAPEX 13% 9% 11% 13% 12%

5

Table 1Free cash flow

2015 2016 2017 2018 2019 F 2020 F 2021 F 2022 F 2023 F

Revenue

3482

9

3378

1

4003

0

4052

2 41332 42159 43002 43862 44740

Operating costs

2791

9

2679

9

2698

3

2711

5 30360 30967 31587 32218 32863

Impairment charges 2791 249 796 132 1143 1166 1190 1213 1238

Exploration cost 576 497 445 488 1143 1166 1190 1213 1238

Operating profit or EBIT 3543 6236

1180

6

1278

7 8686 8859 9037 9217 9402

Finance cost 750 1111 848 552 922 940 959 978 998

Tax expense 993 1567 3965 4242 2879 2937 2995 3055 3116

Net operating profit after

tax 3786 6692

1492

3

1647

7 10643 10856 11073 11294 11520

CAPEX 4685 3012 4482 5430 4853 4950 5049 5150 5253

FCF -899 3680

1044

1

1104

7 5790 5906 6024 6144 6267

PV

5349.57

1

5041.50

5

4751.1

8

4477.57

3

4219.72

3

Table 2Percentage of sales

Assumptions Percentage of sales Average

Operating costs 80% 79% 67% 67% 73%

Impairment charges 8% 1% 2% 0% 3%

Exploration cost 2% 1% 1% 1% 1%

Finance cost 2% 3% 2% 1% 2%

Tax expense 3% 5% 10% 10% 7%

CAPEX 13% 9% 11% 13% 12%

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

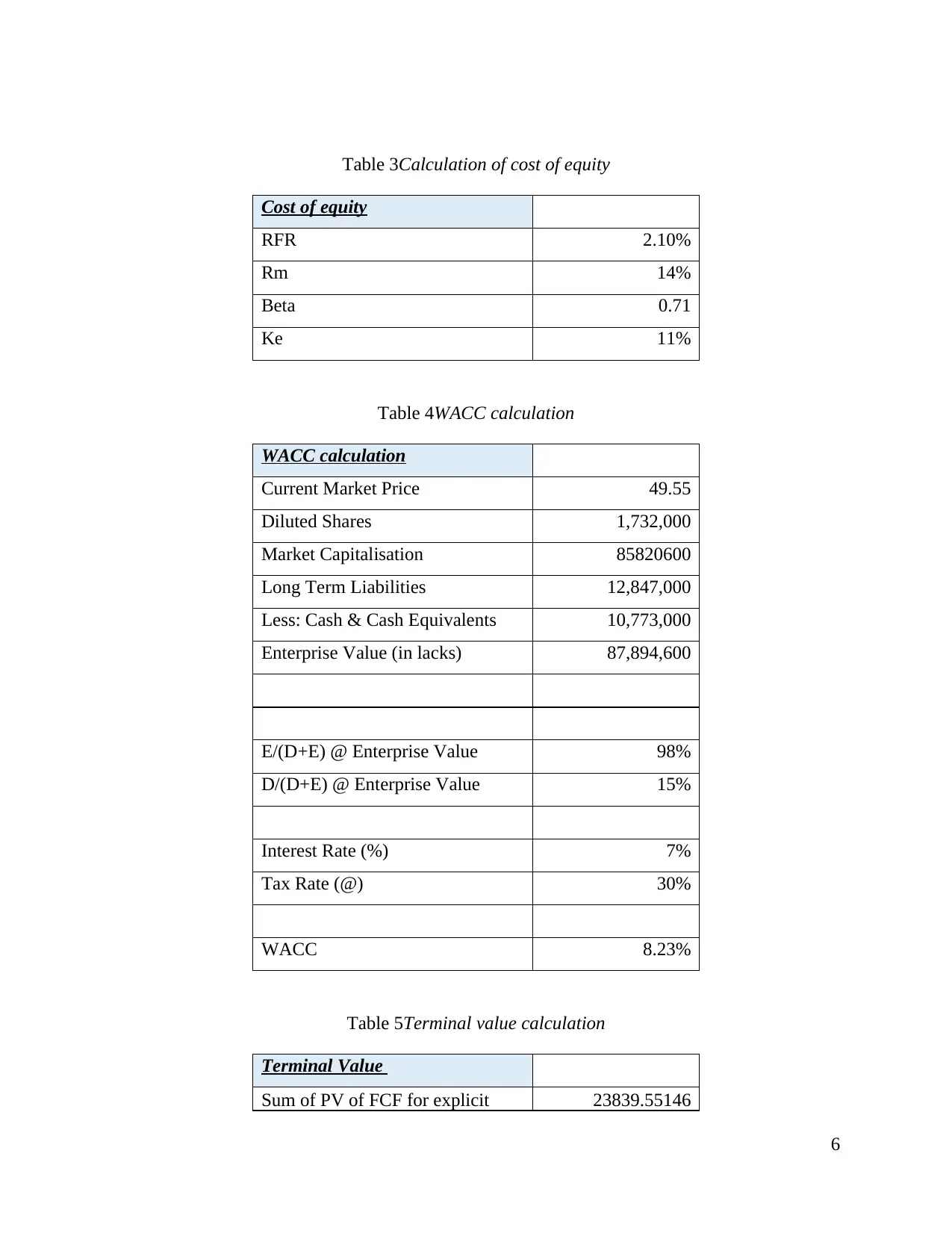

Table 3Calculation of cost of equity

Cost of equity

RFR 2.10%

Rm 14%

Beta 0.71

Ke 11%

Table 4WACC calculation

WACC calculation

Current Market Price 49.55

Diluted Shares 1,732,000

Market Capitalisation 85820600

Long Term Liabilities 12,847,000

Less: Cash & Cash Equivalents 10,773,000

Enterprise Value (in lacks) 87,894,600

E/(D+E) @ Enterprise Value 98%

D/(D+E) @ Enterprise Value 15%

Interest Rate (%) 7%

Tax Rate (@) 30%

WACC 8.23%

Table 5Terminal value calculation

Terminal Value

Sum of PV of FCF for explicit 23839.55146

6

Cost of equity

RFR 2.10%

Rm 14%

Beta 0.71

Ke 11%

Table 4WACC calculation

WACC calculation

Current Market Price 49.55

Diluted Shares 1,732,000

Market Capitalisation 85820600

Long Term Liabilities 12,847,000

Less: Cash & Cash Equivalents 10,773,000

Enterprise Value (in lacks) 87,894,600

E/(D+E) @ Enterprise Value 98%

D/(D+E) @ Enterprise Value 15%

Interest Rate (%) 7%

Tax Rate (@) 30%

WACC 8.23%

Table 5Terminal value calculation

Terminal Value

Sum of PV of FCF for explicit 23839.55146

6

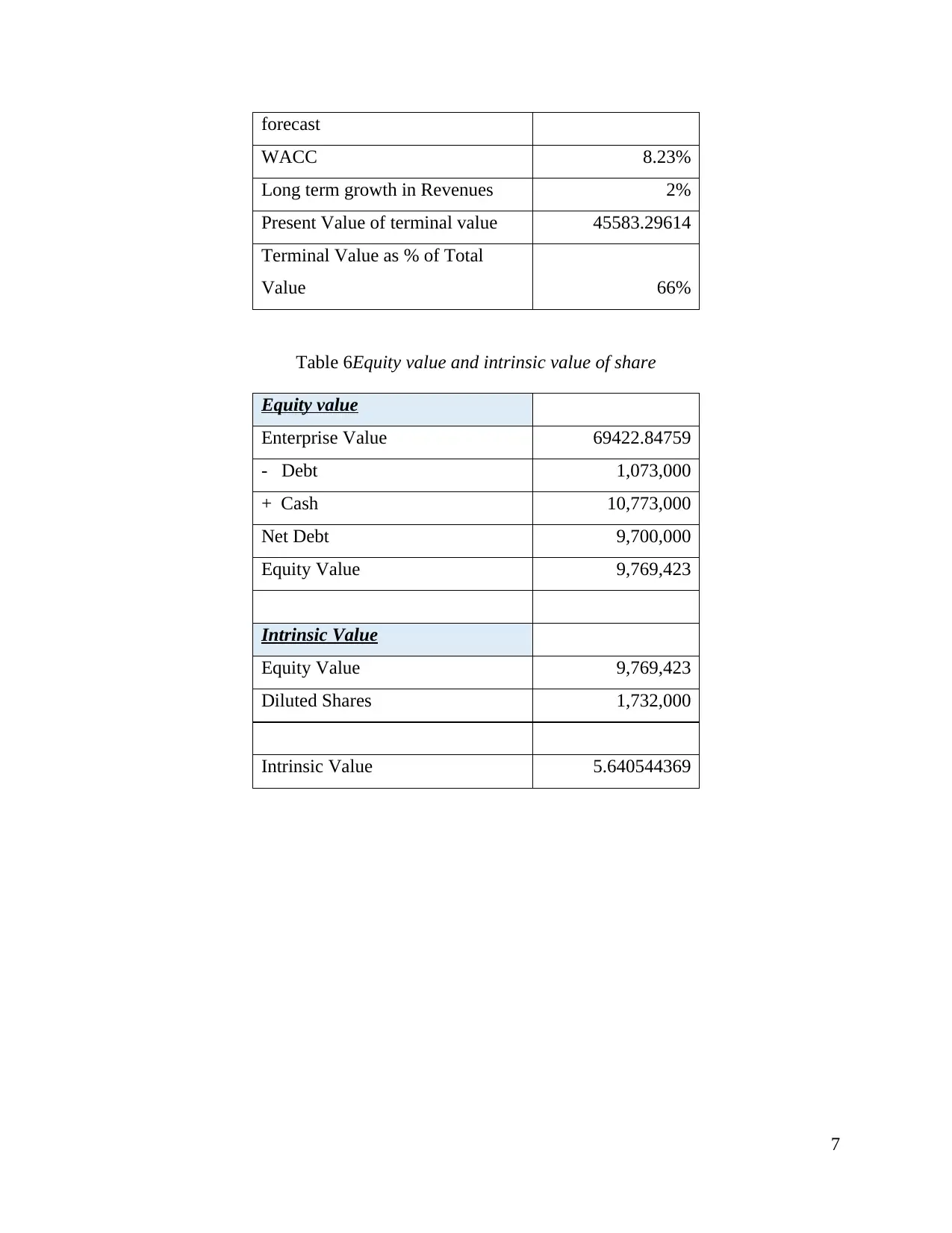

forecast

WACC 8.23%

Long term growth in Revenues 2%

Present Value of terminal value 45583.29614

Terminal Value as % of Total

Value 66%

Table 6Equity value and intrinsic value of share

Equity value

Enterprise Value 69422.84759

- Debt 1,073,000

+ Cash 10,773,000

Net Debt 9,700,000

Equity Value 9,769,423

Intrinsic Value

Equity Value 9,769,423

Diluted Shares 1,732,000

Intrinsic Value 5.640544369

7

WACC 8.23%

Long term growth in Revenues 2%

Present Value of terminal value 45583.29614

Terminal Value as % of Total

Value 66%

Table 6Equity value and intrinsic value of share

Equity value

Enterprise Value 69422.84759

- Debt 1,073,000

+ Cash 10,773,000

Net Debt 9,700,000

Equity Value 9,769,423

Intrinsic Value

Equity Value 9,769,423

Diluted Shares 1,732,000

Intrinsic Value 5.640544369

7

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.