Investment Finance: Time Series Analysis, Returns and Risk Report

VerifiedAdded on 2023/04/04

|10

|1796

|202

Report

AI Summary

This report provides an analysis of investment finance, focusing on time series data for the S&P 500, Boeing Company (BA), and General Dynamics (GD) stock prices. It examines trends, outliers, and seasonality within these time series. The report calculates and compares the returns of GD and BA,...

Running Header: INVESTMENT FINANCE 1

Investment Finance

Student's name:

Institution:

Professor's name:

Course:

Investment Finance

Student's name:

Institution:

Professor's name:

Course:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Investment Finance 2

Time series charts

a) S&P 500 Price Index

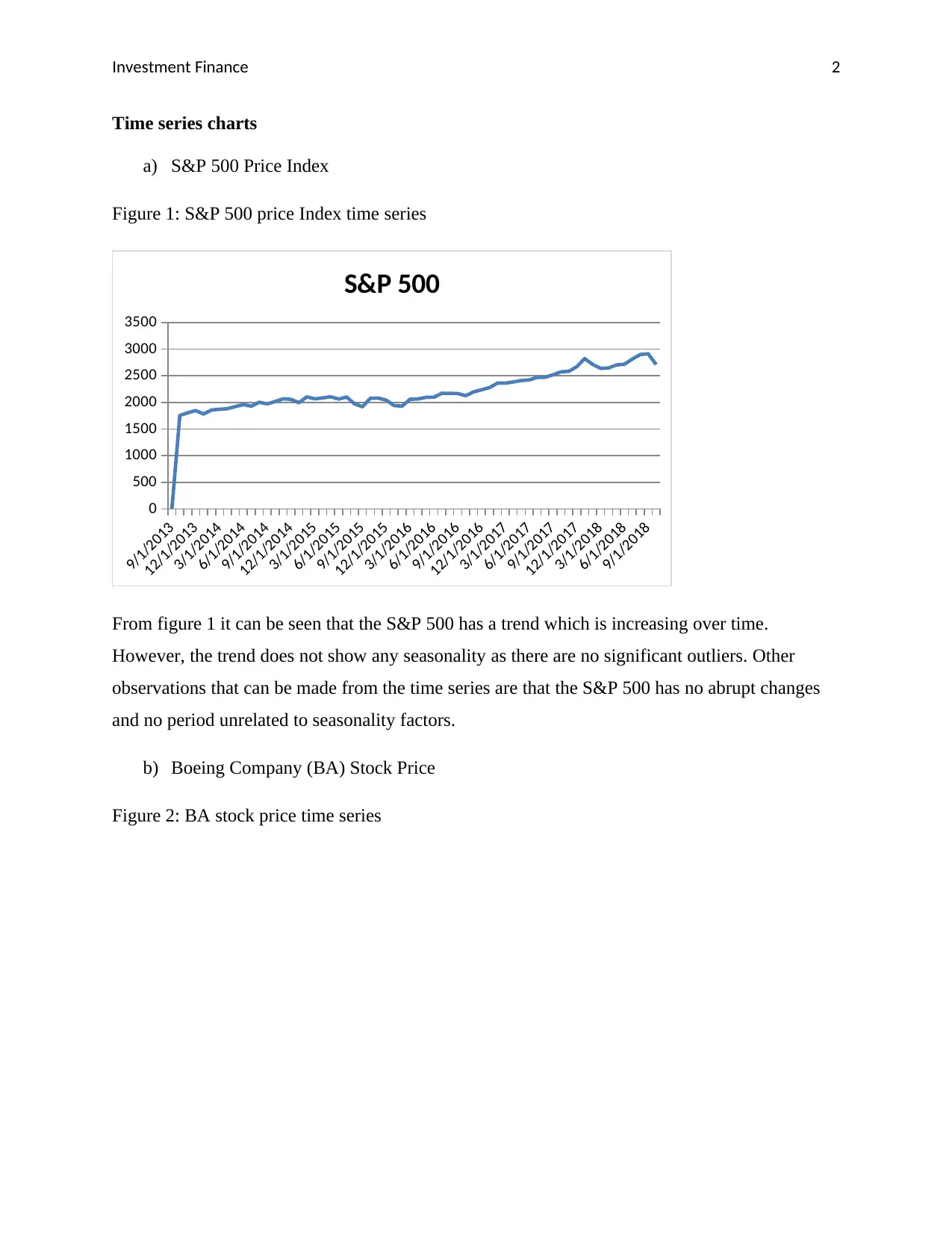

Figure 1: S&P 500 price Index time series

9/1/2013

12/1/2013

3/1/2014

6/1/2014

9/1/2014

12/1/2014

3/1/2015

6/1/2015

9/1/2015

12/1/2015

3/1/2016

6/1/2016

9/1/2016

12/1/2016

3/1/2017

6/1/2017

9/1/2017

12/1/2017

3/1/2018

6/1/2018

9/1/2018

0

500

1000

1500

2000

2500

3000

3500

S&P 500

From figure 1 it can be seen that the S&P 500 has a trend which is increasing over time.

However, the trend does not show any seasonality as there are no significant outliers. Other

observations that can be made from the time series are that the S&P 500 has no abrupt changes

and no period unrelated to seasonality factors.

b) Boeing Company (BA) Stock Price

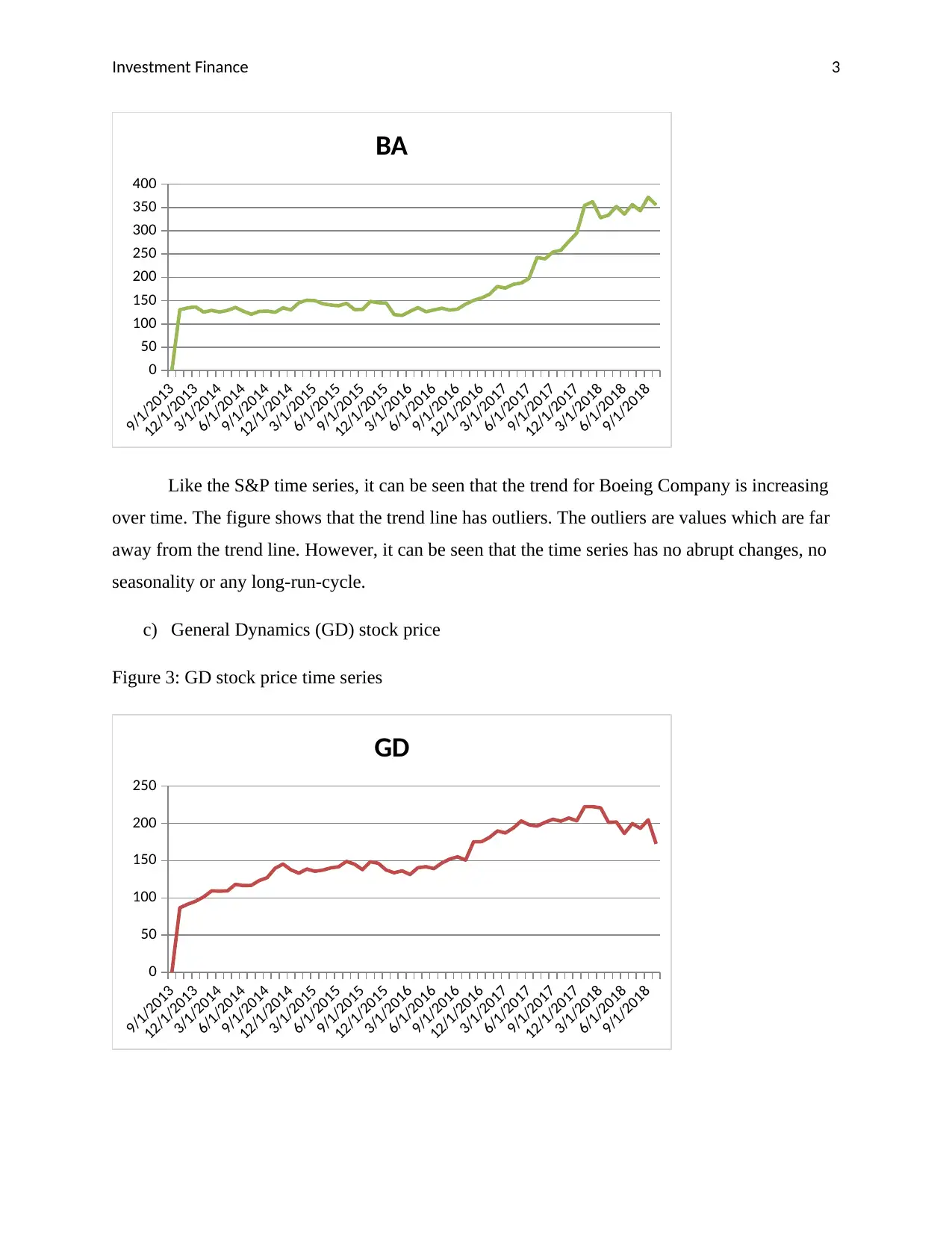

Figure 2: BA stock price time series

Time series charts

a) S&P 500 Price Index

Figure 1: S&P 500 price Index time series

9/1/2013

12/1/2013

3/1/2014

6/1/2014

9/1/2014

12/1/2014

3/1/2015

6/1/2015

9/1/2015

12/1/2015

3/1/2016

6/1/2016

9/1/2016

12/1/2016

3/1/2017

6/1/2017

9/1/2017

12/1/2017

3/1/2018

6/1/2018

9/1/2018

0

500

1000

1500

2000

2500

3000

3500

S&P 500

From figure 1 it can be seen that the S&P 500 has a trend which is increasing over time.

However, the trend does not show any seasonality as there are no significant outliers. Other

observations that can be made from the time series are that the S&P 500 has no abrupt changes

and no period unrelated to seasonality factors.

b) Boeing Company (BA) Stock Price

Figure 2: BA stock price time series

Investment Finance 3

9/1/2013

12/1/2013

3/1/2014

6/1/2014

9/1/2014

12/1/2014

3/1/2015

6/1/2015

9/1/2015

12/1/2015

3/1/2016

6/1/2016

9/1/2016

12/1/2016

3/1/2017

6/1/2017

9/1/2017

12/1/2017

3/1/2018

6/1/2018

9/1/2018

0

50

100

150

200

250

300

350

400

BA

Like the S&P time series, it can be seen that the trend for Boeing Company is increasing

over time. The figure shows that the trend line has outliers. The outliers are values which are far

away from the trend line. However, it can be seen that the time series has no abrupt changes, no

seasonality or any long-run-cycle.

c) General Dynamics (GD) stock price

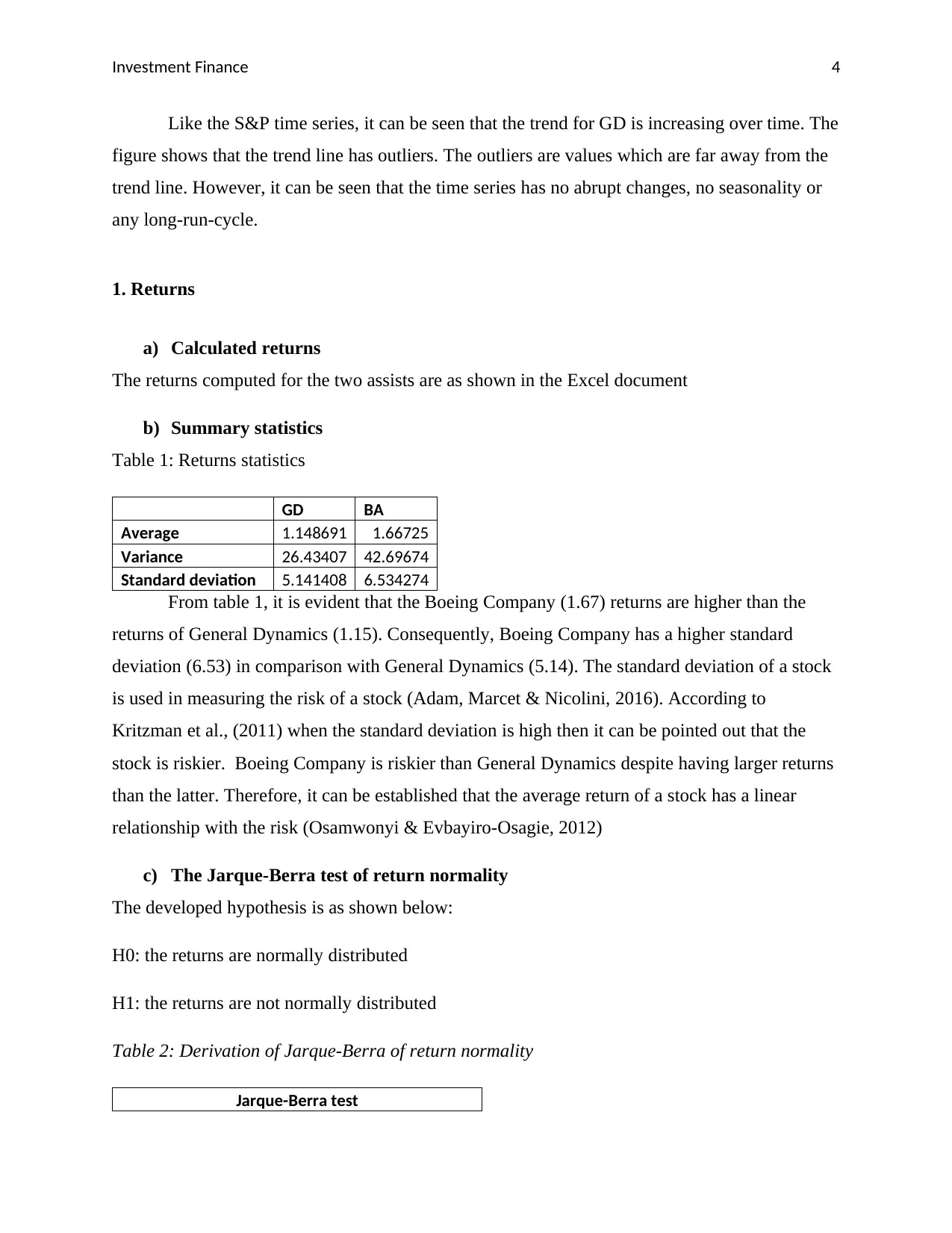

Figure 3: GD stock price time series

9/1/2013

12/1/2013

3/1/2014

6/1/2014

9/1/2014

12/1/2014

3/1/2015

6/1/2015

9/1/2015

12/1/2015

3/1/2016

6/1/2016

9/1/2016

12/1/2016

3/1/2017

6/1/2017

9/1/2017

12/1/2017

3/1/2018

6/1/2018

9/1/2018

0

50

100

150

200

250

GD

9/1/2013

12/1/2013

3/1/2014

6/1/2014

9/1/2014

12/1/2014

3/1/2015

6/1/2015

9/1/2015

12/1/2015

3/1/2016

6/1/2016

9/1/2016

12/1/2016

3/1/2017

6/1/2017

9/1/2017

12/1/2017

3/1/2018

6/1/2018

9/1/2018

0

50

100

150

200

250

300

350

400

BA

Like the S&P time series, it can be seen that the trend for Boeing Company is increasing

over time. The figure shows that the trend line has outliers. The outliers are values which are far

away from the trend line. However, it can be seen that the time series has no abrupt changes, no

seasonality or any long-run-cycle.

c) General Dynamics (GD) stock price

Figure 3: GD stock price time series

9/1/2013

12/1/2013

3/1/2014

6/1/2014

9/1/2014

12/1/2014

3/1/2015

6/1/2015

9/1/2015

12/1/2015

3/1/2016

6/1/2016

9/1/2016

12/1/2016

3/1/2017

6/1/2017

9/1/2017

12/1/2017

3/1/2018

6/1/2018

9/1/2018

0

50

100

150

200

250

GD

You're viewing a preview

Unlock full access by subscribing today!

Investment Finance 4

Like the S&P time series, it can be seen that the trend for GD is increasing over time. The

figure shows that the trend line has outliers. The outliers are values which are far away from the

trend line. However, it can be seen that the time series has no abrupt changes, no seasonality or

any long-run-cycle.

1. Returns

a) Calculated returns

The returns computed for the two assists are as shown in the Excel document

b) Summary statistics

Table 1: Returns statistics

GD BA

Average 1.148691 1.66725

Variance 26.43407 42.69674

Standard deviation 5.141408 6.534274

From table 1, it is evident that the Boeing Company (1.67) returns are higher than the

returns of General Dynamics (1.15). Consequently, Boeing Company has a higher standard

deviation (6.53) in comparison with General Dynamics (5.14). The standard deviation of a stock

is used in measuring the risk of a stock (Adam, Marcet & Nicolini, 2016). According to

Kritzman et al., (2011) when the standard deviation is high then it can be pointed out that the

stock is riskier. Boeing Company is riskier than General Dynamics despite having larger returns

than the latter. Therefore, it can be established that the average return of a stock has a linear

relationship with the risk (Osamwonyi & Evbayiro-Osagie, 2012)

c) The Jarque-Berra test of return normality

The developed hypothesis is as shown below:

H0: the returns are normally distributed

H1: the returns are not normally distributed

Table 2: Derivation of Jarque-Berra of return normality

Jarque-Berra test

Like the S&P time series, it can be seen that the trend for GD is increasing over time. The

figure shows that the trend line has outliers. The outliers are values which are far away from the

trend line. However, it can be seen that the time series has no abrupt changes, no seasonality or

any long-run-cycle.

1. Returns

a) Calculated returns

The returns computed for the two assists are as shown in the Excel document

b) Summary statistics

Table 1: Returns statistics

GD BA

Average 1.148691 1.66725

Variance 26.43407 42.69674

Standard deviation 5.141408 6.534274

From table 1, it is evident that the Boeing Company (1.67) returns are higher than the

returns of General Dynamics (1.15). Consequently, Boeing Company has a higher standard

deviation (6.53) in comparison with General Dynamics (5.14). The standard deviation of a stock

is used in measuring the risk of a stock (Adam, Marcet & Nicolini, 2016). According to

Kritzman et al., (2011) when the standard deviation is high then it can be pointed out that the

stock is riskier. Boeing Company is riskier than General Dynamics despite having larger returns

than the latter. Therefore, it can be established that the average return of a stock has a linear

relationship with the risk (Osamwonyi & Evbayiro-Osagie, 2012)

c) The Jarque-Berra test of return normality

The developed hypothesis is as shown below:

H0: the returns are normally distributed

H1: the returns are not normally distributed

Table 2: Derivation of Jarque-Berra of return normality

Jarque-Berra test

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Investment Finance 5

GD BA

skewness -0.503698679 0.005640474

Kurtosis 2.082174538 1.646777825

N 60 60

Jarque-Berra test 13.37575061 6.780011159

p-value 0.00 0.03

It is evident that the Jarque-Berra test p-values are less than 0.05 for the two stocks. The decision

is to reject the null hypothesis which claims that the returns follow a normal distribution.

Therefore, there is no sufficient evidence to prove that Boeing Company and General Dynamics

returns are normally distributed. According to Jarque (2011), normality tests are computed with

the aim of determining a suitable test which should be applied to the data.

2. Hypothesis test

To prove that the average return of Boeing Company is greater than 2.8%, a one-tailed z-test was

chosen for the test. Desmarais & Harden, (2013), a one-tailed z-test is aimed at checking for one

direction, which is greater than 2.8%.

According to the developed hypothesis:

H0: μ ≥ 0.028

H1: μ < 0.028

Conseqently,

Z = (x̅ - μ)/(σ/(√n))

= (1.667 - 0.028) / (6.534/ (√60))

= 1.94

The critical value for alpha at 0.05 for a one-tailed test is 1.94. The z-test is beyond the

acceptance region since 1.94 is greater than 1.645. Hence, there is no sufficient evidence to

prove that mean return of Boeing Company is at greater than 2.8%.

GD BA

skewness -0.503698679 0.005640474

Kurtosis 2.082174538 1.646777825

N 60 60

Jarque-Berra test 13.37575061 6.780011159

p-value 0.00 0.03

It is evident that the Jarque-Berra test p-values are less than 0.05 for the two stocks. The decision

is to reject the null hypothesis which claims that the returns follow a normal distribution.

Therefore, there is no sufficient evidence to prove that Boeing Company and General Dynamics

returns are normally distributed. According to Jarque (2011), normality tests are computed with

the aim of determining a suitable test which should be applied to the data.

2. Hypothesis test

To prove that the average return of Boeing Company is greater than 2.8%, a one-tailed z-test was

chosen for the test. Desmarais & Harden, (2013), a one-tailed z-test is aimed at checking for one

direction, which is greater than 2.8%.

According to the developed hypothesis:

H0: μ ≥ 0.028

H1: μ < 0.028

Conseqently,

Z = (x̅ - μ)/(σ/(√n))

= (1.667 - 0.028) / (6.534/ (√60))

= 1.94

The critical value for alpha at 0.05 for a one-tailed test is 1.94. The z-test is beyond the

acceptance region since 1.94 is greater than 1.645. Hence, there is no sufficient evidence to

prove that mean return of Boeing Company is at greater than 2.8%.

Investment Finance 6

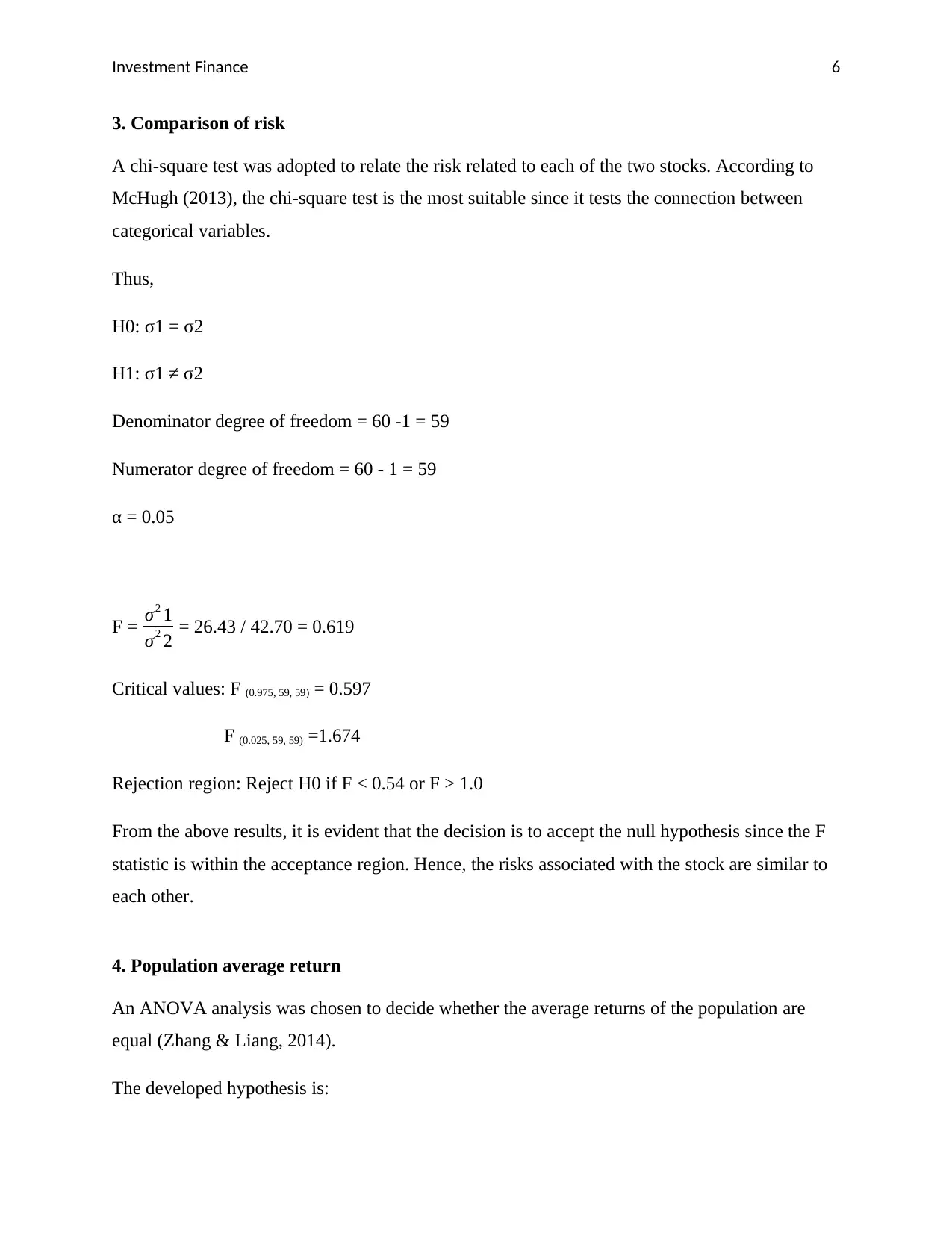

3. Comparison of risk

A chi-square test was adopted to relate the risk related to each of the two stocks. According to

McHugh (2013), the chi-square test is the most suitable since it tests the connection between

categorical variables.

Thus,

H0: σ1 = σ2

H1: σ1 ≠ σ2

Denominator degree of freedom = 60 -1 = 59

Numerator degree of freedom = 60 - 1 = 59

α = 0.05

F = σ2 1

σ2 2 = 26.43 / 42.70 = 0.619

Critical values: F (0.975, 59, 59) = 0.597

F (0.025, 59, 59) =1.674

Rejection region: Reject H0 if F < 0.54 or F > 1.0

From the above results, it is evident that the decision is to accept the null hypothesis since the F

statistic is within the acceptance region. Hence, the risks associated with the stock are similar to

each other.

4. Population average return

An ANOVA analysis was chosen to decide whether the average returns of the population are

equal (Zhang & Liang, 2014).

The developed hypothesis is:

3. Comparison of risk

A chi-square test was adopted to relate the risk related to each of the two stocks. According to

McHugh (2013), the chi-square test is the most suitable since it tests the connection between

categorical variables.

Thus,

H0: σ1 = σ2

H1: σ1 ≠ σ2

Denominator degree of freedom = 60 -1 = 59

Numerator degree of freedom = 60 - 1 = 59

α = 0.05

F = σ2 1

σ2 2 = 26.43 / 42.70 = 0.619

Critical values: F (0.975, 59, 59) = 0.597

F (0.025, 59, 59) =1.674

Rejection region: Reject H0 if F < 0.54 or F > 1.0

From the above results, it is evident that the decision is to accept the null hypothesis since the F

statistic is within the acceptance region. Hence, the risks associated with the stock are similar to

each other.

4. Population average return

An ANOVA analysis was chosen to decide whether the average returns of the population are

equal (Zhang & Liang, 2014).

The developed hypothesis is:

You're viewing a preview

Unlock full access by subscribing today!

Investment Finance 7

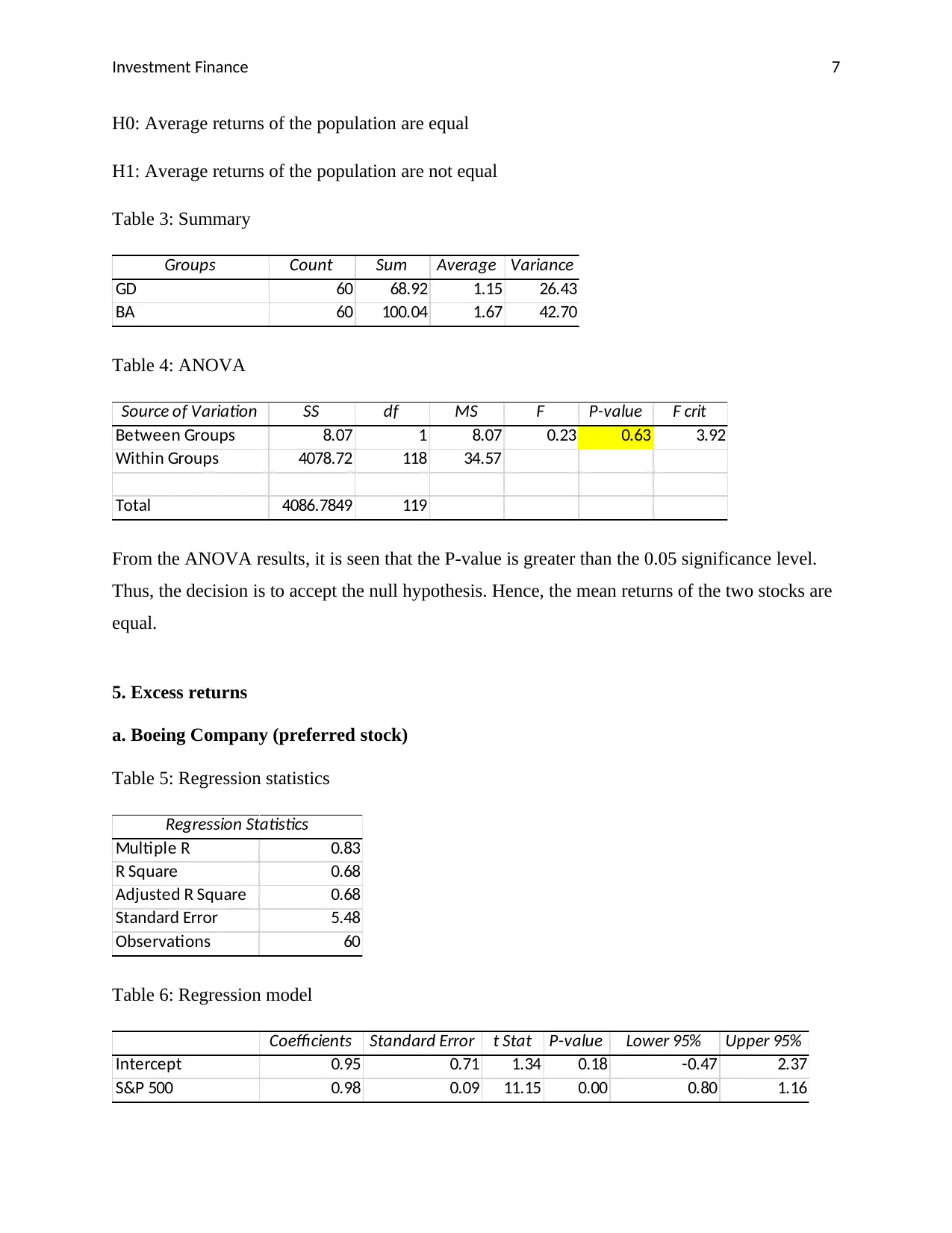

H0: Average returns of the population are equal

H1: Average returns of the population are not equal

Table 3: Summary

Groups Count Sum Average Variance

GD 60 68.92 1.15 26.43

BA 60 100.04 1.67 42.70

Table 4: ANOVA

Source of Variation SS df MS F P-value F crit

Between Groups 8.07 1 8.07 0.23 0.63 3.92

Within Groups 4078.72 118 34.57

Total 4086.7849 119

From the ANOVA results, it is seen that the P-value is greater than the 0.05 significance level.

Thus, the decision is to accept the null hypothesis. Hence, the mean returns of the two stocks are

equal.

5. Excess returns

a. Boeing Company (preferred stock)

Table 5: Regression statistics

Regression Statistics

Multiple R 0.83

R Square 0.68

Adjusted R Square 0.68

Standard Error 5.48

Observations 60

Table 6: Regression model

Coefficients Standard Error t Stat P-value Lower 95% Upper 95%

Intercept 0.95 0.71 1.34 0.18 -0.47 2.37

S&P 500 0.98 0.09 11.15 0.00 0.80 1.16

H0: Average returns of the population are equal

H1: Average returns of the population are not equal

Table 3: Summary

Groups Count Sum Average Variance

GD 60 68.92 1.15 26.43

BA 60 100.04 1.67 42.70

Table 4: ANOVA

Source of Variation SS df MS F P-value F crit

Between Groups 8.07 1 8.07 0.23 0.63 3.92

Within Groups 4078.72 118 34.57

Total 4086.7849 119

From the ANOVA results, it is seen that the P-value is greater than the 0.05 significance level.

Thus, the decision is to accept the null hypothesis. Hence, the mean returns of the two stocks are

equal.

5. Excess returns

a. Boeing Company (preferred stock)

Table 5: Regression statistics

Regression Statistics

Multiple R 0.83

R Square 0.68

Adjusted R Square 0.68

Standard Error 5.48

Observations 60

Table 6: Regression model

Coefficients Standard Error t Stat P-value Lower 95% Upper 95%

Intercept 0.95 0.71 1.34 0.18 -0.47 2.37

S&P 500 0.98 0.09 11.15 0.00 0.80 1.16

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Investment Finance 8

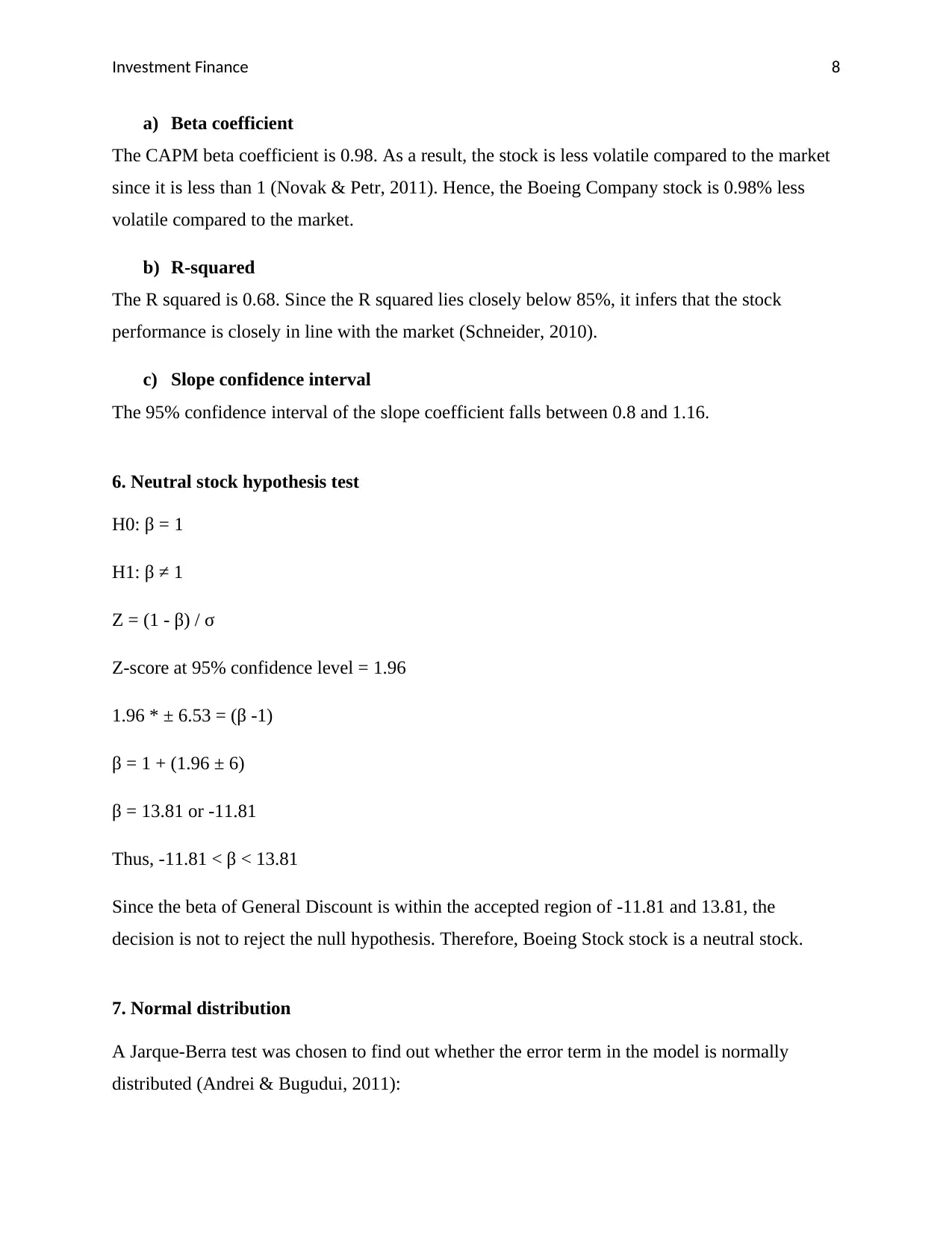

a) Beta coefficient

The CAPM beta coefficient is 0.98. As a result, the stock is less volatile compared to the market

since it is less than 1 (Novak & Petr, 2011). Hence, the Boeing Company stock is 0.98% less

volatile compared to the market.

b) R-squared

The R squared is 0.68. Since the R squared lies closely below 85%, it infers that the stock

performance is closely in line with the market (Schneider, 2010).

c) Slope confidence interval

The 95% confidence interval of the slope coefficient falls between 0.8 and 1.16.

6. Neutral stock hypothesis test

H0: β = 1

H1: β ≠ 1

Z = (1 - β) / σ

Z-score at 95% confidence level = 1.96

1.96 * ± 6.53 = (β -1)

β = 1 + (1.96 ± 6)

β = 13.81 or -11.81

Thus, -11.81 < β < 13.81

Since the beta of General Discount is within the accepted region of -11.81 and 13.81, the

decision is not to reject the null hypothesis. Therefore, Boeing Stock stock is a neutral stock.

7. Normal distribution

A Jarque-Berra test was chosen to find out whether the error term in the model is normally

distributed (Andrei & Bugudui, 2011):

a) Beta coefficient

The CAPM beta coefficient is 0.98. As a result, the stock is less volatile compared to the market

since it is less than 1 (Novak & Petr, 2011). Hence, the Boeing Company stock is 0.98% less

volatile compared to the market.

b) R-squared

The R squared is 0.68. Since the R squared lies closely below 85%, it infers that the stock

performance is closely in line with the market (Schneider, 2010).

c) Slope confidence interval

The 95% confidence interval of the slope coefficient falls between 0.8 and 1.16.

6. Neutral stock hypothesis test

H0: β = 1

H1: β ≠ 1

Z = (1 - β) / σ

Z-score at 95% confidence level = 1.96

1.96 * ± 6.53 = (β -1)

β = 1 + (1.96 ± 6)

β = 13.81 or -11.81

Thus, -11.81 < β < 13.81

Since the beta of General Discount is within the accepted region of -11.81 and 13.81, the

decision is not to reject the null hypothesis. Therefore, Boeing Stock stock is a neutral stock.

7. Normal distribution

A Jarque-Berra test was chosen to find out whether the error term in the model is normally

distributed (Andrei & Bugudui, 2011):

Investment Finance 9

Table 5: Jarque-Berra test for error term normality

Residuals

skewness 0.097954294

kurtosis 1.780890507

n 60

Jaque berra test 10.00

0.80

8.02

p-value 0.02

It is apparent that the p-values for the Jarque-Berra test are 0.02 for the residuals. Since the p-

value is less than 0.5, the decision is to reject the null hypothesis and conclude that there is no

sufficient evidence to prove that the standard error follows a normal distribution.

Reference

Adam, K., Marcet, A., & Nicolini, J. P. (2016). Stock market volatility and learning. The Journal of

Finance, 71(1), 33-82.

Andrei, E. A., & Bugudui, E. (2011). Econometric modeling of GDP time series. Theoretical and Applied

Economics, 10(10), 91.

Desmarais, B. A., & Harden, J. J. (2013). Testing for zero inflation in count models: Bias correction for the

Vuong test. The Stata Journal, 13(4), 810-835.

Table 5: Jarque-Berra test for error term normality

Residuals

skewness 0.097954294

kurtosis 1.780890507

n 60

Jaque berra test 10.00

0.80

8.02

p-value 0.02

It is apparent that the p-values for the Jarque-Berra test are 0.02 for the residuals. Since the p-

value is less than 0.5, the decision is to reject the null hypothesis and conclude that there is no

sufficient evidence to prove that the standard error follows a normal distribution.

Reference

Adam, K., Marcet, A., & Nicolini, J. P. (2016). Stock market volatility and learning. The Journal of

Finance, 71(1), 33-82.

Andrei, E. A., & Bugudui, E. (2011). Econometric modeling of GDP time series. Theoretical and Applied

Economics, 10(10), 91.

Desmarais, B. A., & Harden, J. J. (2013). Testing for zero inflation in count models: Bias correction for the

Vuong test. The Stata Journal, 13(4), 810-835.

You're viewing a preview

Unlock full access by subscribing today!

Investment Finance 10

Kritzman, M., Li, Y., Page, S., & Rigobon, R. (2011). Principal components as a measure of systemic

risk. The Journal of Portfolio Management, 37(4), 112-126.

Jarque, C. M. (2011). Jarque-bera test. International Encyclopedia of Statistical Science, 701-702.

McHugh, M. L. (2013). The chi-square test of independence. Biochemia medica: Biochemia

medica, 23(2), 143-149.

Novak, J., & Petr, D. (2011). CAPM Beta, Size, Book-to-Market, and Momentum in Realized Stock

Returns. Finance a Uver: Czech Journal of Economics & Finance, 61(1).

Osamwonyi, I. O., & Evbayiro-Osagie, E. I. (2012). The relationship between macroeconomic variables

and stock market index in Nigeria. Journal of Economics, 3(1), 55-63.

Schneider, S. (2010). Investments of Speculative Capital in Staple Foods: Effects and Implications

Exemplified by the Case of Corn. Diplomarbeiten Agentur.

Zhang, J. T., & Liang, X. (2014). One‐way ANOVA for functional data via globalizing the pointwise F‐

test. Scandinavian Journal of Statistics, 41(1), 51-71.

Kritzman, M., Li, Y., Page, S., & Rigobon, R. (2011). Principal components as a measure of systemic

risk. The Journal of Portfolio Management, 37(4), 112-126.

Jarque, C. M. (2011). Jarque-bera test. International Encyclopedia of Statistical Science, 701-702.

McHugh, M. L. (2013). The chi-square test of independence. Biochemia medica: Biochemia

medica, 23(2), 143-149.

Novak, J., & Petr, D. (2011). CAPM Beta, Size, Book-to-Market, and Momentum in Realized Stock

Returns. Finance a Uver: Czech Journal of Economics & Finance, 61(1).

Osamwonyi, I. O., & Evbayiro-Osagie, E. I. (2012). The relationship between macroeconomic variables

and stock market index in Nigeria. Journal of Economics, 3(1), 55-63.

Schneider, S. (2010). Investments of Speculative Capital in Staple Foods: Effects and Implications

Exemplified by the Case of Corn. Diplomarbeiten Agentur.

Zhang, J. T., & Liang, X. (2014). One‐way ANOVA for functional data via globalizing the pointwise F‐

test. Scandinavian Journal of Statistics, 41(1), 51-71.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.