Business Decision Making Essay: Financial and Non-Financial Factors

VerifiedAdded on 2023/01/11

|8

|1462

|59

Essay

AI Summary

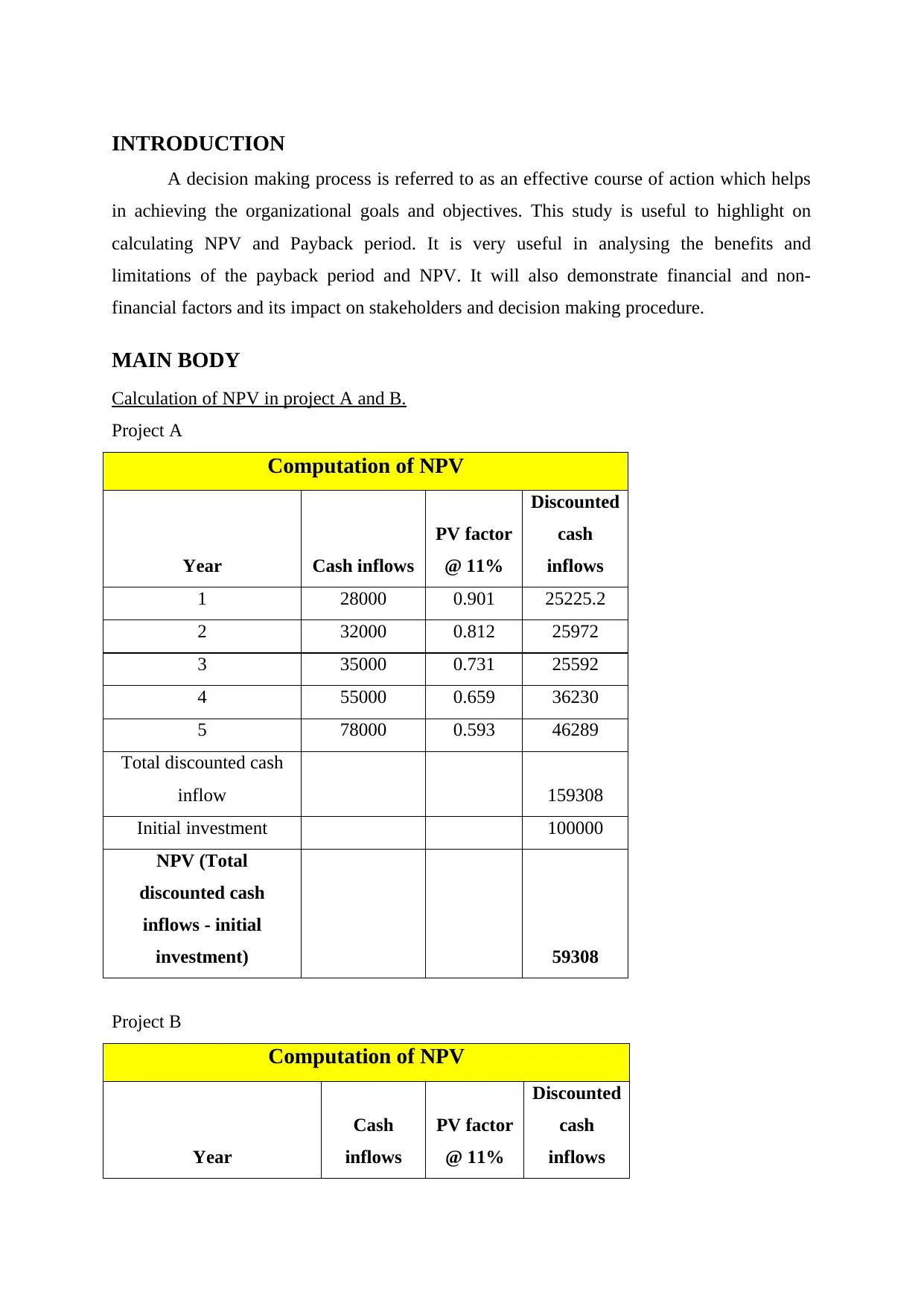

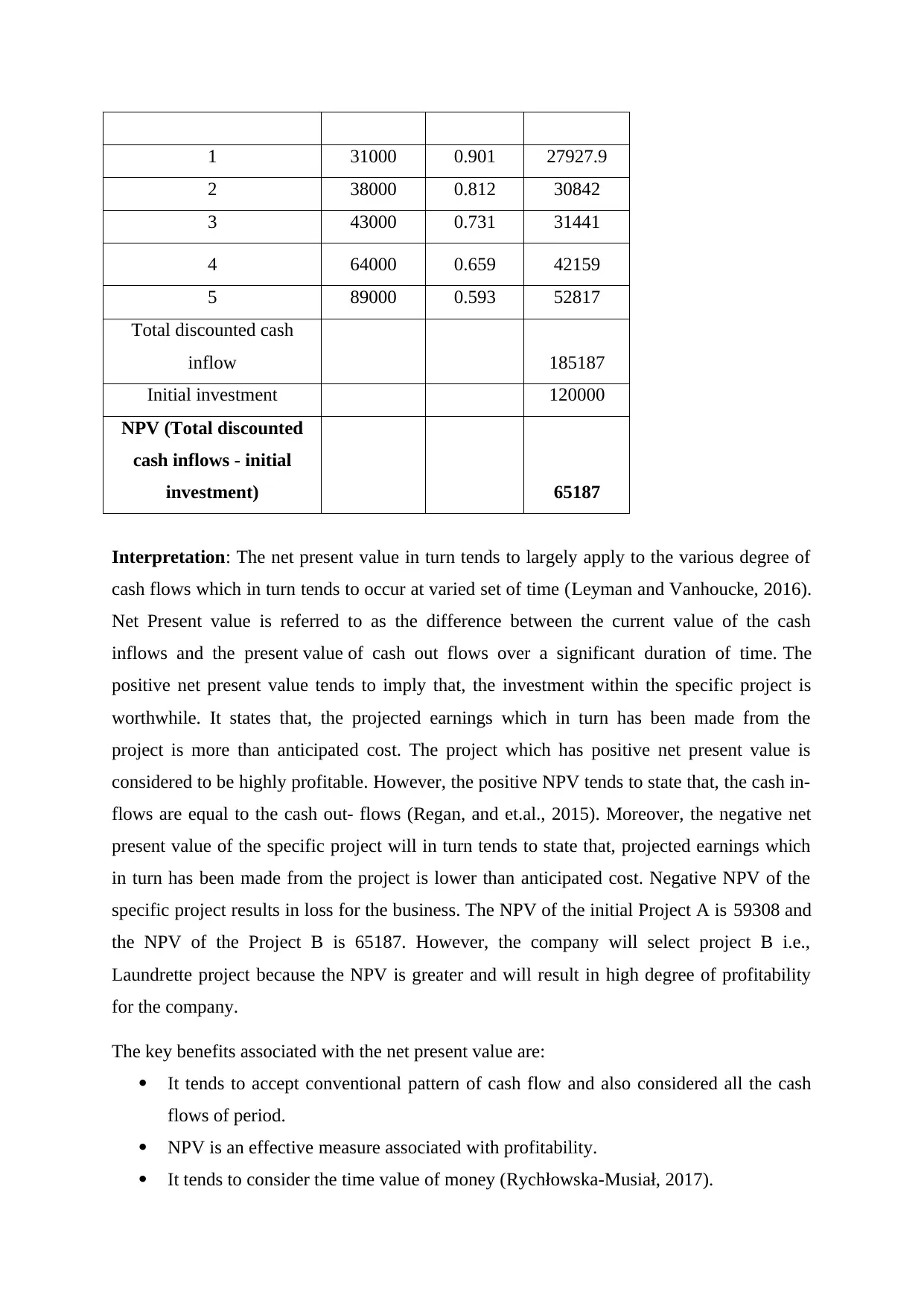

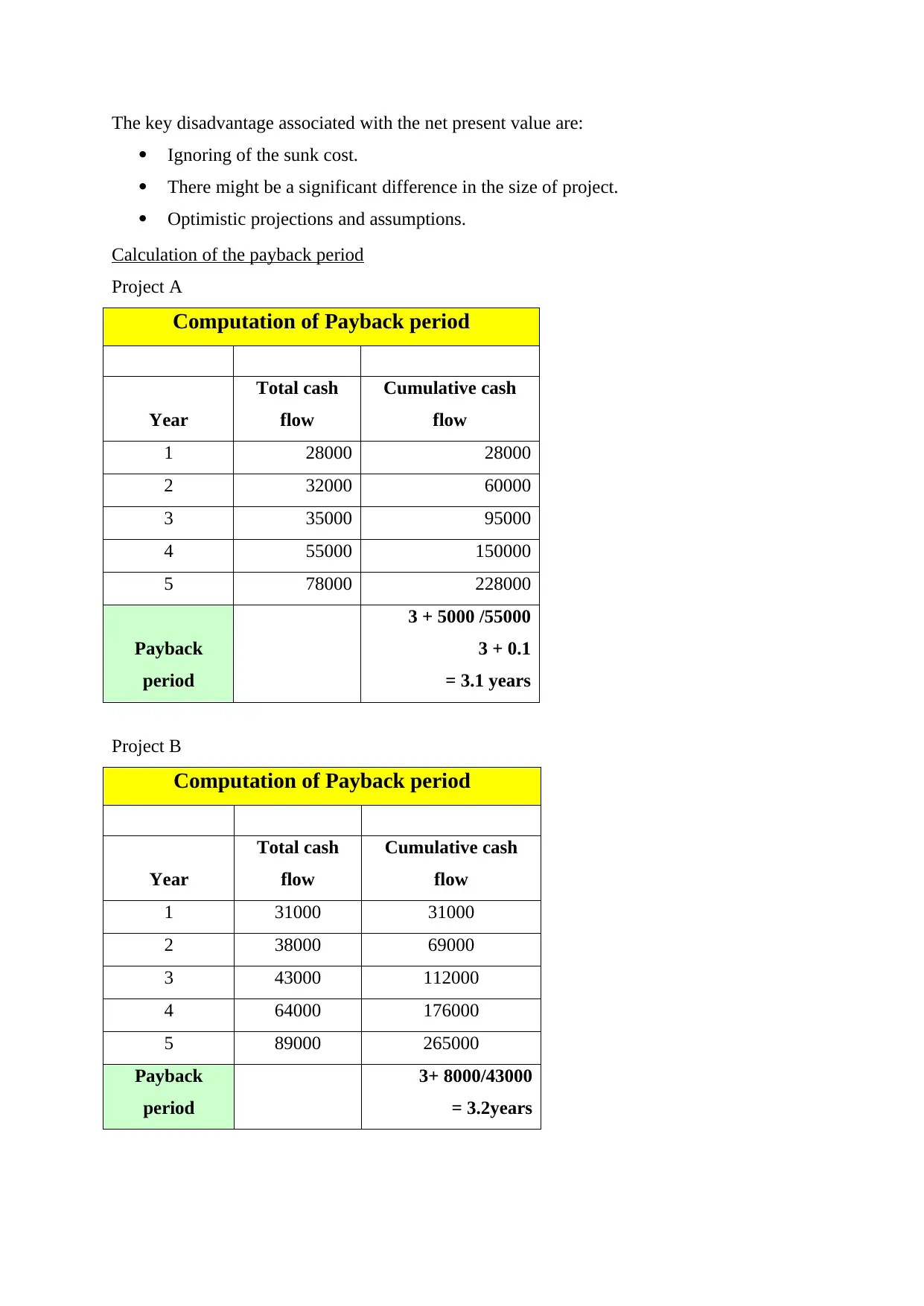

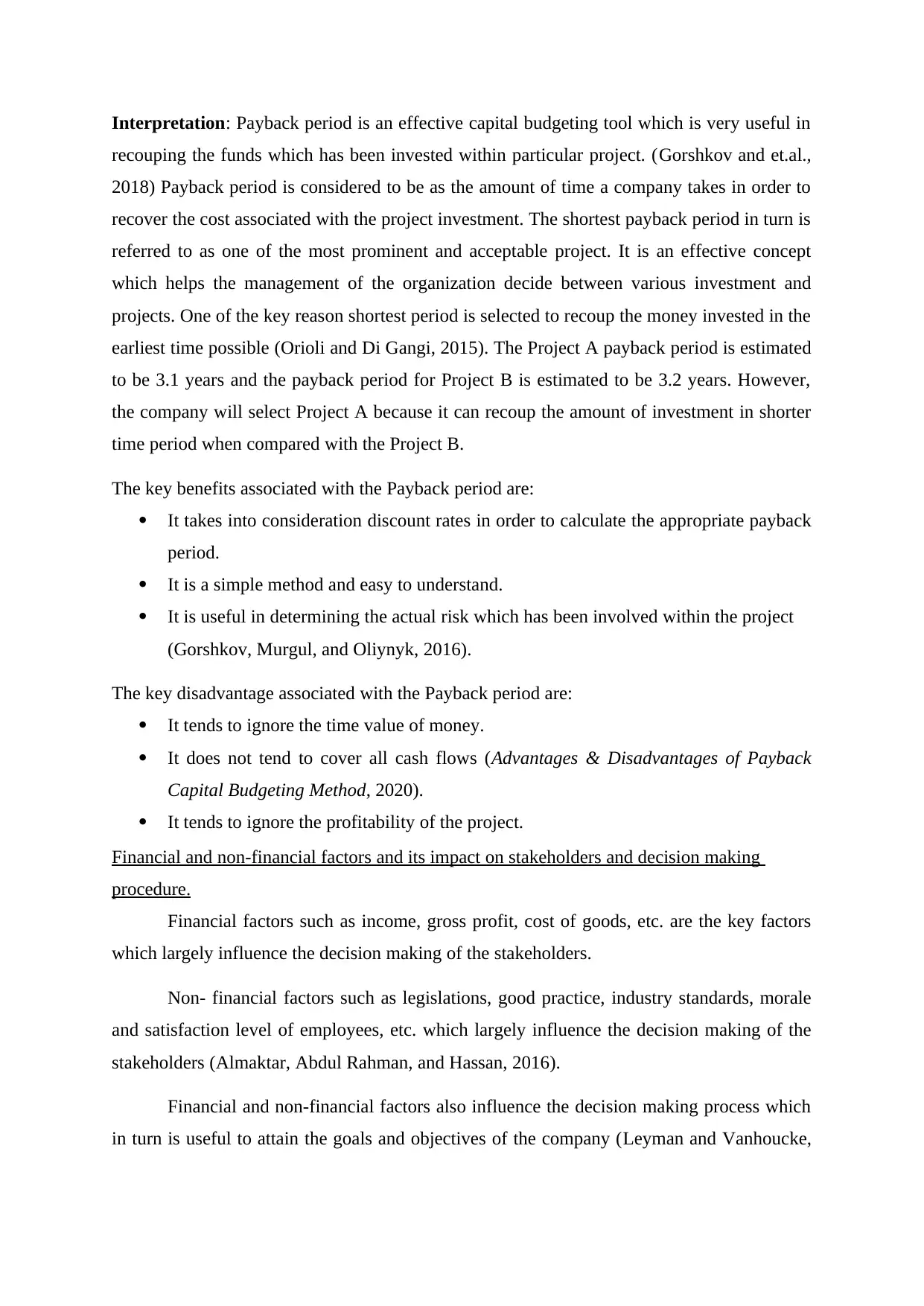

This essay delves into the core concepts of business decision-making, offering a comprehensive analysis of Net Present Value (NPV) and payback period calculations. The essay demonstrates the application of these financial tools in evaluating investment projects, comparing the profitability of two projects (A and B) using NPV and payback period. It highlights the significance of a positive NPV and a shorter payback period in investment decisions. Furthermore, the essay explores the influence of both financial factors (income, gross profit) and non-financial factors (legislation, employee morale) on stakeholders and the overall decision-making process. The conclusion summarizes the key findings, emphasizing the importance of considering both financial and non-financial aspects in achieving organizational goals. The essay references relevant academic sources to support its arguments.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.