Financial Performance Evaluation: Woolworths (2018-2019) Analysis

VerifiedAdded on 2023/01/11

|13

|2591

|53

Essay

AI Summary

This essay presents a detailed financial analysis of Woolworths Group, Australia's largest supermarket chain, covering the years 2018 and 2019. The analysis employs various financial accounting tools, including ratio analysis, horizontal analysis, and vertical analysis, to assess the company's performance and financial position. The report examines profitability ratios (gross profit margin, net profit margin), liquidity ratios (current ratio, quick ratio), efficiency ratios (inventory turnover, asset turnover), and leverage ratios (debt-equity ratio, interest coverage ratio) to evaluate Woolworths' operational efficiency, ability to meet short-term obligations, and financial stability. Horizontal and vertical analyses are used to identify trends and assess the relative size of financial statement items over the two-year period. The conclusion summarizes the financial health of Woolworths and its capacity to meet its financial obligations. The report provides an in-depth understanding of Woolworths' financial performance and identifies areas of strength and potential improvement, based on the data available in the financial statements.

Essay

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive summary

The current report provides a detailed analysis of Woolworth’s financial statements by

making use of different financial accounting tools that includes ratio analysis, vertical &

horizontal analysis. This tool helps in determining and making comparative assessment of

company’s performance and position over the periods. From the study it has been reflected that it

is performing in a better and efficient manner by making best possible use of its assets, sales and

profits for meeting its liabilities and costs.

The current report provides a detailed analysis of Woolworth’s financial statements by

making use of different financial accounting tools that includes ratio analysis, vertical &

horizontal analysis. This tool helps in determining and making comparative assessment of

company’s performance and position over the periods. From the study it has been reflected that it

is performing in a better and efficient manner by making best possible use of its assets, sales and

profits for meeting its liabilities and costs.

TABLE OF CONTENT

Executive summary.......................................................................................................................2

INTRODUCTION.........................................................................................................................4

Discussion and analysis.................................................................................................................4

Ratio analysis...............................................................................................................................4

Horizontal analysis......................................................................................................................7

Vertical analysis...........................................................................................................................9

CONCLUSION............................................................................................................................11

REFERENCES............................................................................................................................13

Executive summary.......................................................................................................................2

INTRODUCTION.........................................................................................................................4

Discussion and analysis.................................................................................................................4

Ratio analysis...............................................................................................................................4

Horizontal analysis......................................................................................................................7

Vertical analysis...........................................................................................................................9

CONCLUSION............................................................................................................................11

REFERENCES............................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

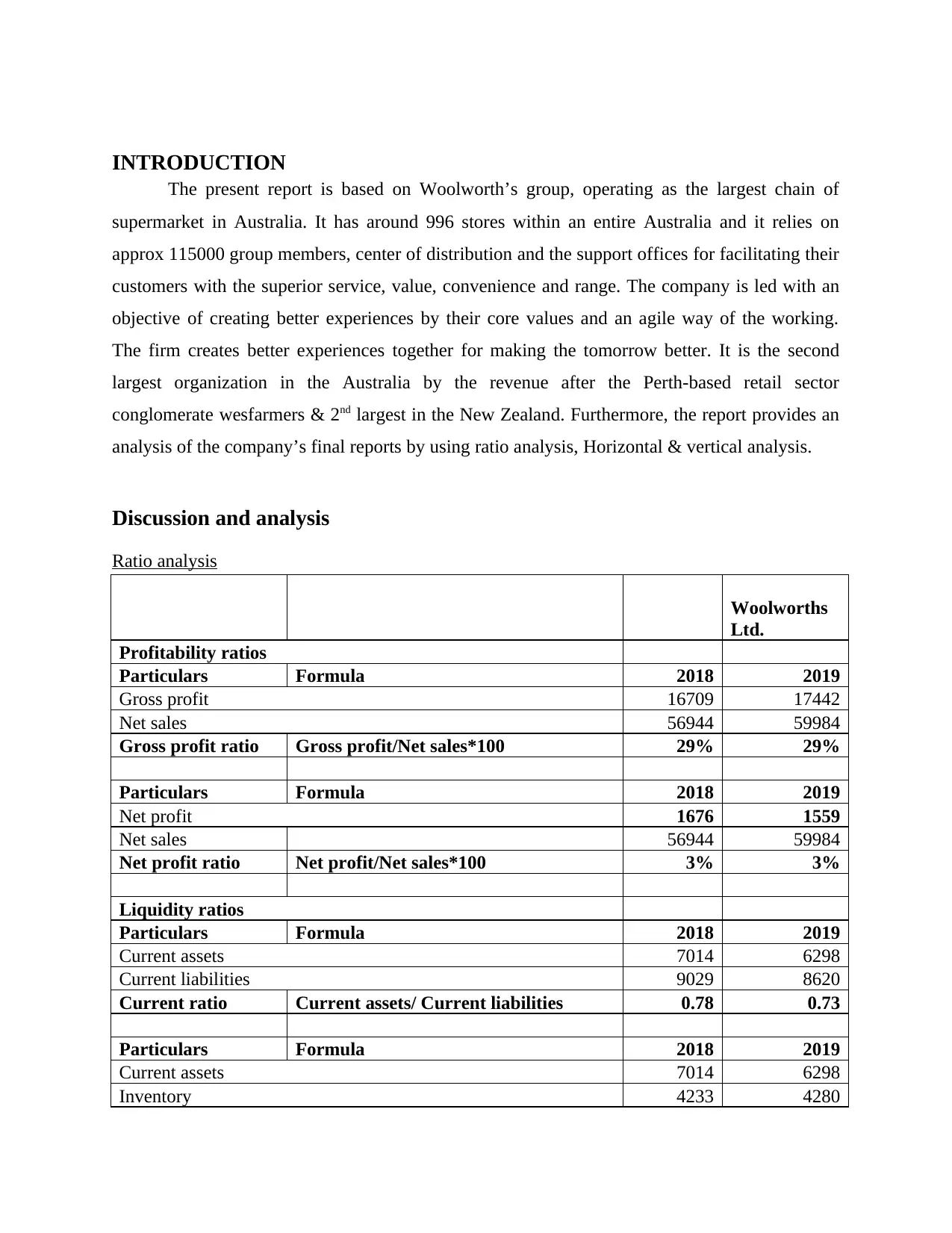

INTRODUCTION

The present report is based on Woolworth’s group, operating as the largest chain of

supermarket in Australia. It has around 996 stores within an entire Australia and it relies on

approx 115000 group members, center of distribution and the support offices for facilitating their

customers with the superior service, value, convenience and range. The company is led with an

objective of creating better experiences by their core values and an agile way of the working.

The firm creates better experiences together for making the tomorrow better. It is the second

largest organization in the Australia by the revenue after the Perth-based retail sector

conglomerate wesfarmers & 2nd largest in the New Zealand. Furthermore, the report provides an

analysis of the company’s final reports by using ratio analysis, Horizontal & vertical analysis.

Discussion and analysis

Ratio analysis

Woolworths

Ltd.

Profitability ratios

Particulars Formula 2018 2019

Gross profit 16709 17442

Net sales 56944 59984

Gross profit ratio Gross profit/Net sales*100 29% 29%

Particulars Formula 2018 2019

Net profit 1676 1559

Net sales 56944 59984

Net profit ratio Net profit/Net sales*100 3% 3%

Liquidity ratios

Particulars Formula 2018 2019

Current assets 7014 6298

Current liabilities 9029 8620

Current ratio Current assets/ Current liabilities 0.78 0.73

Particulars Formula 2018 2019

Current assets 7014 6298

Inventory 4233 4280

The present report is based on Woolworth’s group, operating as the largest chain of

supermarket in Australia. It has around 996 stores within an entire Australia and it relies on

approx 115000 group members, center of distribution and the support offices for facilitating their

customers with the superior service, value, convenience and range. The company is led with an

objective of creating better experiences by their core values and an agile way of the working.

The firm creates better experiences together for making the tomorrow better. It is the second

largest organization in the Australia by the revenue after the Perth-based retail sector

conglomerate wesfarmers & 2nd largest in the New Zealand. Furthermore, the report provides an

analysis of the company’s final reports by using ratio analysis, Horizontal & vertical analysis.

Discussion and analysis

Ratio analysis

Woolworths

Ltd.

Profitability ratios

Particulars Formula 2018 2019

Gross profit 16709 17442

Net sales 56944 59984

Gross profit ratio Gross profit/Net sales*100 29% 29%

Particulars Formula 2018 2019

Net profit 1676 1559

Net sales 56944 59984

Net profit ratio Net profit/Net sales*100 3% 3%

Liquidity ratios

Particulars Formula 2018 2019

Current assets 7014 6298

Current liabilities 9029 8620

Current ratio Current assets/ Current liabilities 0.78 0.73

Particulars Formula 2018 2019

Current assets 7014 6298

Inventory 4233 4280

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Quick assets Current assets-Inventory 2781 2018

Current liabilities 9029 8620

Quick ratio Quick assets/Current liabilities 0.31 0.23

Efficiency ratios

Particulars Formula 2018 2019

Cost of goods sold 40235 42542

Inventory 4233 4280

Inventory

Turnover ratio Cost of goods sold/Inventory 9.5 9.9

Net sales 56944 59984

Average total assets 23,391 23491

Asset turnover

ratio Net sales/Average inventory 2.43 2.55

Leverage ratios

Particulars Formula 2018 2019

Debt (Long term funds) 942 986

Equity (owners fund) 10849 10669

Debt/Equity ratio Debt/Equity 11.52 10.82

Earnings before interest and taxes 2548 2353

Interest expense 154 126

Interest coverage

ratio

Earnings before interest and

taxes/Interest expense 16.55 18.67

Gross profit ratio- From the above analysis it has been interpreted that gross margin of

Woolworths over the years is accounted as stable. This ratio states the profits earned by the

company after meeting its cost relating to sales or variable cost. Higher the GP ratio better is the

operational performance of an enterprise (Parkinson, 2018). This analysis shows that the GP

ratio of Woolworths is equal in both the years which that the firm is gaining similar amount of

profits and revenue which in turn means that the business operations of an entity are functioning

smoothly.

Net profit margin- The table depicts that NP ratio of Woolworths accounted as 3% in

both the years which clearly reflects that the firm is generating stable income after paying off its

liabilities, costs or expenses and tax obligations. It is the ratio that measures an ability of the firm

in meeting all its expenses and costs by making use of its earnings. Higher the NP ratio better is

Current liabilities 9029 8620

Quick ratio Quick assets/Current liabilities 0.31 0.23

Efficiency ratios

Particulars Formula 2018 2019

Cost of goods sold 40235 42542

Inventory 4233 4280

Inventory

Turnover ratio Cost of goods sold/Inventory 9.5 9.9

Net sales 56944 59984

Average total assets 23,391 23491

Asset turnover

ratio Net sales/Average inventory 2.43 2.55

Leverage ratios

Particulars Formula 2018 2019

Debt (Long term funds) 942 986

Equity (owners fund) 10849 10669

Debt/Equity ratio Debt/Equity 11.52 10.82

Earnings before interest and taxes 2548 2353

Interest expense 154 126

Interest coverage

ratio

Earnings before interest and

taxes/Interest expense 16.55 18.67

Gross profit ratio- From the above analysis it has been interpreted that gross margin of

Woolworths over the years is accounted as stable. This ratio states the profits earned by the

company after meeting its cost relating to sales or variable cost. Higher the GP ratio better is the

operational performance of an enterprise (Parkinson, 2018). This analysis shows that the GP

ratio of Woolworths is equal in both the years which that the firm is gaining similar amount of

profits and revenue which in turn means that the business operations of an entity are functioning

smoothly.

Net profit margin- The table depicts that NP ratio of Woolworths accounted as 3% in

both the years which clearly reflects that the firm is generating stable income after paying off its

liabilities, costs or expenses and tax obligations. It is the ratio that measures an ability of the firm

in meeting all its expenses and costs by making use of its earnings. Higher the NP ratio better is

the performance of the firm. As ratio of Woolworths resulted as same in both the year, this

means that the profitability performance of an enterprise is better and shows that the firm is

stable in an overall industry or the market.

Current ratio- Current ratio is a liquidity ratio that helps in identifying an organization’s

ability to pay its short-term obligations or those due within an year. The ideal current ratio is 2:1

which means that the assets must double current liabilities in order to become a sound financial

ratio (Trotman and Carson, 2018). From the above data it can be interpreted that the Current

Ratio has declined from 0.78% to 073% which means that there is a 5% decline in the overall

ratio during a period of 1 year. Thus, it can be analyzed that the firm’s ability to repay its debt is

reducing and it can be difficult for Woolworths to meet its financial obligations in the near

future.

Quick ratio- The quick ratio is another liquidity ratio that helps in measuring a

company’s liquidity. It is also called as acid test ratio and it measures the total cash and

marketable securities then compare it to amount receivable from current liabilities. From the

above data, it can be interpreted that Woolworths company’s quick ratio dropped from 0.31% in

2018 to 0.23% in 2019 which means that the company will struggle to pay its debts and it is

more likely that it will have to sell its assets in order to make the repayment.

Inventory turnover ratio- The ITR helps in identifying how many times a company has

sold or replaced an inventory during a period of time (Flax, Bick and Abratt, 2016). It is

imperative for every company to keep a check on its ITR as it helps in making better decision

related to the purchasing and selling of inventory. From the above study, it is interpreted that the

ITR has increased from 9.5% to 9.9% which means that Woolworths Company is selling its

goods and services quickly and there still exists a good demand for its inventory in the market.

Asset turnover ratio- Asset turnover ratio is concerned with a company’s capacity to

generate sales from its assets by comparing net sales with average total assets. From the above

table, it was interpreted that the asset turnover ratio of Woolworths Company increased from

2.43% to 2.55% which means that the business is using its assets more effectively and efficiently

and is generating more sales with the help of these assets.

means that the profitability performance of an enterprise is better and shows that the firm is

stable in an overall industry or the market.

Current ratio- Current ratio is a liquidity ratio that helps in identifying an organization’s

ability to pay its short-term obligations or those due within an year. The ideal current ratio is 2:1

which means that the assets must double current liabilities in order to become a sound financial

ratio (Trotman and Carson, 2018). From the above data it can be interpreted that the Current

Ratio has declined from 0.78% to 073% which means that there is a 5% decline in the overall

ratio during a period of 1 year. Thus, it can be analyzed that the firm’s ability to repay its debt is

reducing and it can be difficult for Woolworths to meet its financial obligations in the near

future.

Quick ratio- The quick ratio is another liquidity ratio that helps in measuring a

company’s liquidity. It is also called as acid test ratio and it measures the total cash and

marketable securities then compare it to amount receivable from current liabilities. From the

above data, it can be interpreted that Woolworths company’s quick ratio dropped from 0.31% in

2018 to 0.23% in 2019 which means that the company will struggle to pay its debts and it is

more likely that it will have to sell its assets in order to make the repayment.

Inventory turnover ratio- The ITR helps in identifying how many times a company has

sold or replaced an inventory during a period of time (Flax, Bick and Abratt, 2016). It is

imperative for every company to keep a check on its ITR as it helps in making better decision

related to the purchasing and selling of inventory. From the above study, it is interpreted that the

ITR has increased from 9.5% to 9.9% which means that Woolworths Company is selling its

goods and services quickly and there still exists a good demand for its inventory in the market.

Asset turnover ratio- Asset turnover ratio is concerned with a company’s capacity to

generate sales from its assets by comparing net sales with average total assets. From the above

table, it was interpreted that the asset turnover ratio of Woolworths Company increased from

2.43% to 2.55% which means that the business is using its assets more effectively and efficiently

and is generating more sales with the help of these assets.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Debt-equity ratio- In order to compute debt to equity ratio, the company’s total liabilities

are divided by its shareholders equity that are available on the balance sheet of the company’s

financial statements (HOTEL, 2016). It was interpreted by the company that its D.E.R reduced

from 11.52% to 10.82% which means that the Woolworths Company is not able to capitalize on

the increased profits that are brought by the financial leverage. In order to improve the ratio, it is

important for the company to increase its sales and invest its funds into purchasing of assets.

Interest coverage ratio- This ratio helps in determining the ability of a company to pay

its interest expenses on outstanding debt. It can be computed by dividing the earning before

interest and taxes (EBIT) of a company by the interest expenses of similar period. The interest

coverage ratio increased from 16.55 to 18.67% thus a higher ratio indicates strong financial

health and stability of Woolworth’s organization and its capacity to meet its financial obligations

in a better manner.

Horizontal analysis

Horizontal analysis of income statement

Particulars 2018 2019

%

chang

e

Revenue

5694

4

5998

4 5%

Cost of goods

sold

-

4023

5

-

4254

2 6%

Gross profit

1670

9

1744

2 4%

Other revenue 222 288 30%

Branch expense

-

1085

4

-

1169

5 8%

Administrative

expense

-

3529

-

3682 4%

EBIT 2548 2353 -8%

Finance cost -154 -126 -18%

PBT 2394 2227 -7%

are divided by its shareholders equity that are available on the balance sheet of the company’s

financial statements (HOTEL, 2016). It was interpreted by the company that its D.E.R reduced

from 11.52% to 10.82% which means that the Woolworths Company is not able to capitalize on

the increased profits that are brought by the financial leverage. In order to improve the ratio, it is

important for the company to increase its sales and invest its funds into purchasing of assets.

Interest coverage ratio- This ratio helps in determining the ability of a company to pay

its interest expenses on outstanding debt. It can be computed by dividing the earning before

interest and taxes (EBIT) of a company by the interest expenses of similar period. The interest

coverage ratio increased from 16.55 to 18.67% thus a higher ratio indicates strong financial

health and stability of Woolworth’s organization and its capacity to meet its financial obligations

in a better manner.

Horizontal analysis

Horizontal analysis of income statement

Particulars 2018 2019

%

chang

e

Revenue

5694

4

5998

4 5%

Cost of goods

sold

-

4023

5

-

4254

2 6%

Gross profit

1670

9

1744

2 4%

Other revenue 222 288 30%

Branch expense

-

1085

4

-

1169

5 8%

Administrative

expense

-

3529

-

3682 4%

EBIT 2548 2353 -8%

Finance cost -154 -126 -18%

PBT 2394 2227 -7%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Income tax

expense -718 -668 -7%

PAT 1559 1676 8%

Interpretation- From the above assessment it has been depicted that over 2 years,

revenue of the company is increasing with 5% along with increase in the cost of sales and gross

profit with 6 and 4%. However, the earnings before interest and tax resulted as negative in value

which that expenses and finance cost of an entity is higher than its gross profits (Walters and

Helman, 2020). Moreover, the net profit after the tax account as declining and leads to profits for

the firm.

Horizontal analysis of Balance sheet

Particulars 2018 2019

%

chang

e

Current assets

cash 1273 1066 -16%

receivables 634 682 8%

inventories 4233 4280 1%

Other financial assets 53 45 -15%

Assets for sale 821 225 -73%

Total CA 7014 6298 -10%

Non-current assets

Receivables 93 145 56%

Other financial assets 522 692 33%

Plant, property & equipment 9026 9519 5%

Intangible assets 6465 6526 1%

Deferred tax asset 271 311 15%

Total non-current asset

1637

7

1719

3 5%

Total assets

2339

1

2349

1 0%

Current liabilities

Payables 6793 6676 -2%

Borrowings 604 274 -55%

Tax payable 110 84 -24%

Other types of financial liabilities 50 58 16%

Provisions 1451 1528 5%

expense -718 -668 -7%

PAT 1559 1676 8%

Interpretation- From the above assessment it has been depicted that over 2 years,

revenue of the company is increasing with 5% along with increase in the cost of sales and gross

profit with 6 and 4%. However, the earnings before interest and tax resulted as negative in value

which that expenses and finance cost of an entity is higher than its gross profits (Walters and

Helman, 2020). Moreover, the net profit after the tax account as declining and leads to profits for

the firm.

Horizontal analysis of Balance sheet

Particulars 2018 2019

%

chang

e

Current assets

cash 1273 1066 -16%

receivables 634 682 8%

inventories 4233 4280 1%

Other financial assets 53 45 -15%

Assets for sale 821 225 -73%

Total CA 7014 6298 -10%

Non-current assets

Receivables 93 145 56%

Other financial assets 522 692 33%

Plant, property & equipment 9026 9519 5%

Intangible assets 6465 6526 1%

Deferred tax asset 271 311 15%

Total non-current asset

1637

7

1719

3 5%

Total assets

2339

1

2349

1 0%

Current liabilities

Payables 6793 6676 -2%

Borrowings 604 274 -55%

Tax payable 110 84 -24%

Other types of financial liabilities 50 58 16%

Provisions 1451 1528 5%

Liabilities for the sale 21 0 -100%

Total CL 9029 8620 -5%

Non-current liabilities

Borrowings 2199 2855 30%

Other types of financial liablities 61 24 -61%

Provisions 942 986 5%

Other long term liabilities 311 337 8%

Total LT liabilities 3513 4202 20%

Total liabilities

1254

2

1282

2 2%

Net assets

1084

9

1066

9 -2%

Equity

Contributed equity 6055 5828 -4%

Reserves 353 490 39%

Retained earnings 4073 3968 -3%

Equity attributed to equity shareholders of

parent entity

1048

1

1028

6 -2%

Non-controlling interests 368 383 4%

Total equity

1084

9

1066

9 -2%

Interpretation- In this the current year’s assets and the liabilities are been compared with

that of the previous year’s assets & liabilities. The results reflects that the current assets of the

company is reducing from one accounting period to another, however, non-current assets of an

entity are increasing which shows that firm seeks for purchasing long term assets rather than

current assets (Beaton-Wells and Paul-Taylor, 2017). Moreover, Current liabilities of

Woolworths are also declining with an increase in non-current liabilities. Similarly reserves and

equities of firm are also declining from one period to other.

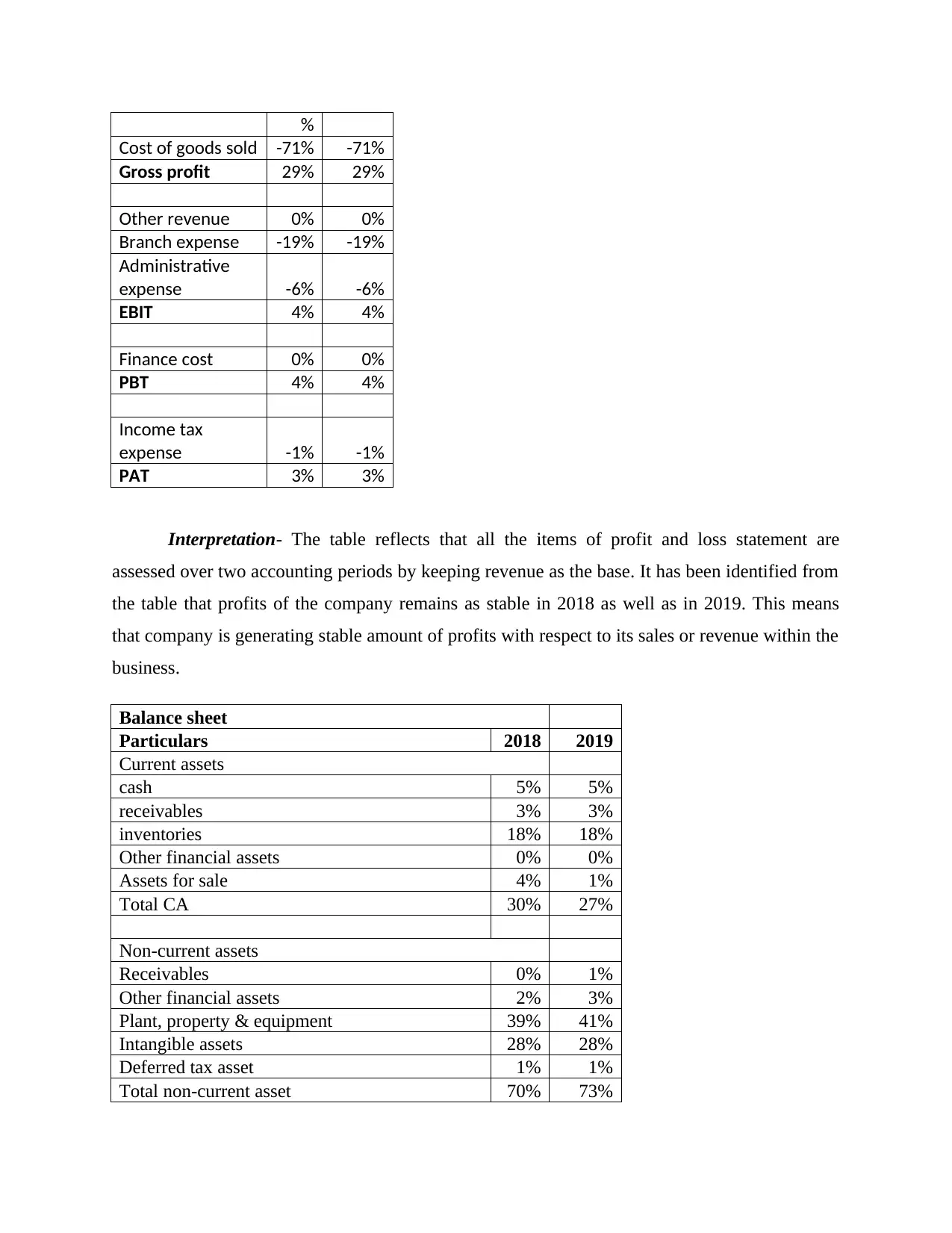

Vertical analysis

Income statement

Particulars 2018 2019

Revenue 100 100%

Total CL 9029 8620 -5%

Non-current liabilities

Borrowings 2199 2855 30%

Other types of financial liablities 61 24 -61%

Provisions 942 986 5%

Other long term liabilities 311 337 8%

Total LT liabilities 3513 4202 20%

Total liabilities

1254

2

1282

2 2%

Net assets

1084

9

1066

9 -2%

Equity

Contributed equity 6055 5828 -4%

Reserves 353 490 39%

Retained earnings 4073 3968 -3%

Equity attributed to equity shareholders of

parent entity

1048

1

1028

6 -2%

Non-controlling interests 368 383 4%

Total equity

1084

9

1066

9 -2%

Interpretation- In this the current year’s assets and the liabilities are been compared with

that of the previous year’s assets & liabilities. The results reflects that the current assets of the

company is reducing from one accounting period to another, however, non-current assets of an

entity are increasing which shows that firm seeks for purchasing long term assets rather than

current assets (Beaton-Wells and Paul-Taylor, 2017). Moreover, Current liabilities of

Woolworths are also declining with an increase in non-current liabilities. Similarly reserves and

equities of firm are also declining from one period to other.

Vertical analysis

Income statement

Particulars 2018 2019

Revenue 100 100%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

%

Cost of goods sold -71% -71%

Gross profit 29% 29%

Other revenue 0% 0%

Branch expense -19% -19%

Administrative

expense -6% -6%

EBIT 4% 4%

Finance cost 0% 0%

PBT 4% 4%

Income tax

expense -1% -1%

PAT 3% 3%

Interpretation- The table reflects that all the items of profit and loss statement are

assessed over two accounting periods by keeping revenue as the base. It has been identified from

the table that profits of the company remains as stable in 2018 as well as in 2019. This means

that company is generating stable amount of profits with respect to its sales or revenue within the

business.

Balance sheet

Particulars 2018 2019

Current assets

cash 5% 5%

receivables 3% 3%

inventories 18% 18%

Other financial assets 0% 0%

Assets for sale 4% 1%

Total CA 30% 27%

Non-current assets

Receivables 0% 1%

Other financial assets 2% 3%

Plant, property & equipment 39% 41%

Intangible assets 28% 28%

Deferred tax asset 1% 1%

Total non-current asset 70% 73%

Cost of goods sold -71% -71%

Gross profit 29% 29%

Other revenue 0% 0%

Branch expense -19% -19%

Administrative

expense -6% -6%

EBIT 4% 4%

Finance cost 0% 0%

PBT 4% 4%

Income tax

expense -1% -1%

PAT 3% 3%

Interpretation- The table reflects that all the items of profit and loss statement are

assessed over two accounting periods by keeping revenue as the base. It has been identified from

the table that profits of the company remains as stable in 2018 as well as in 2019. This means

that company is generating stable amount of profits with respect to its sales or revenue within the

business.

Balance sheet

Particulars 2018 2019

Current assets

cash 5% 5%

receivables 3% 3%

inventories 18% 18%

Other financial assets 0% 0%

Assets for sale 4% 1%

Total CA 30% 27%

Non-current assets

Receivables 0% 1%

Other financial assets 2% 3%

Plant, property & equipment 39% 41%

Intangible assets 28% 28%

Deferred tax asset 1% 1%

Total non-current asset 70% 73%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

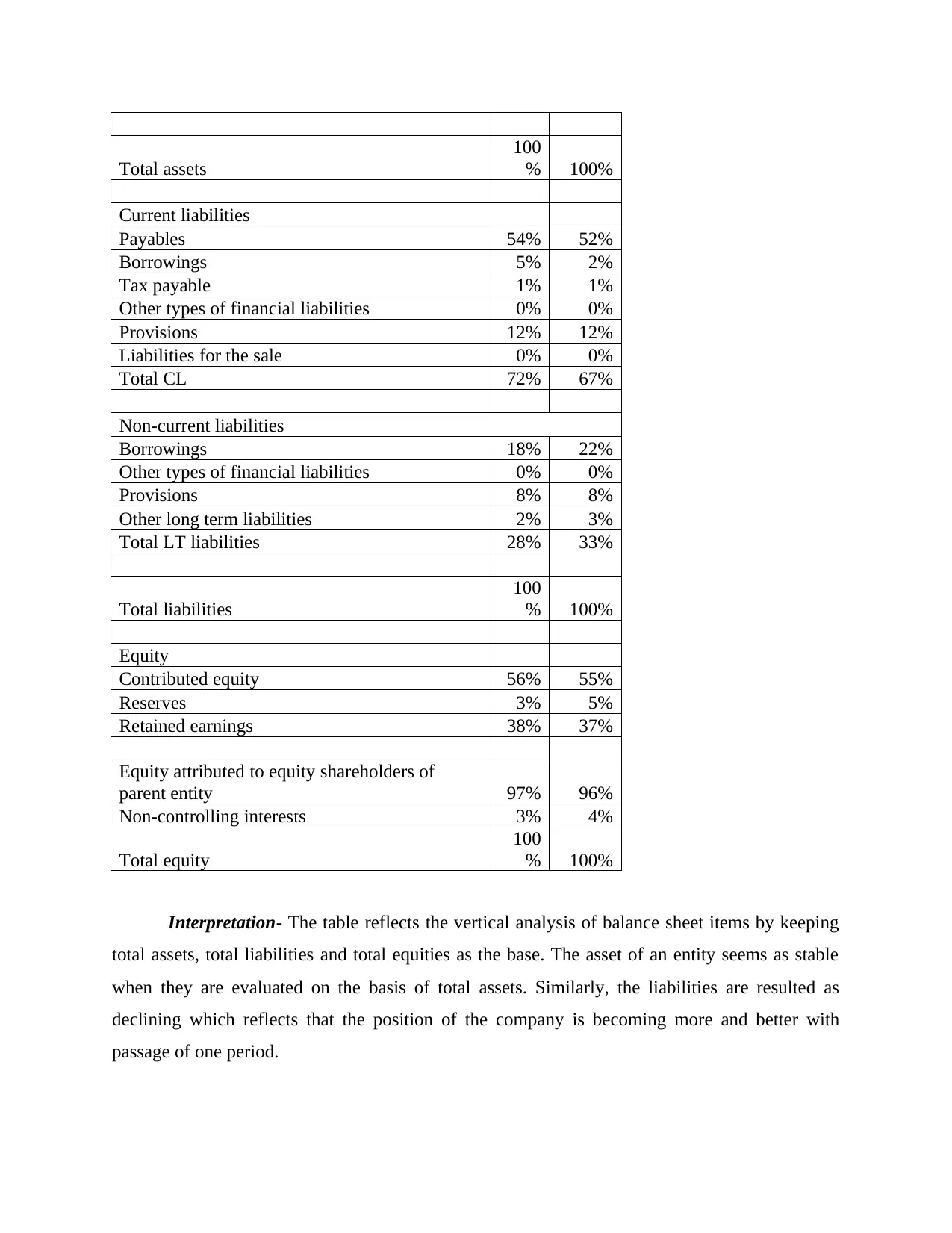

Total assets

100

% 100%

Current liabilities

Payables 54% 52%

Borrowings 5% 2%

Tax payable 1% 1%

Other types of financial liabilities 0% 0%

Provisions 12% 12%

Liabilities for the sale 0% 0%

Total CL 72% 67%

Non-current liabilities

Borrowings 18% 22%

Other types of financial liabilities 0% 0%

Provisions 8% 8%

Other long term liabilities 2% 3%

Total LT liabilities 28% 33%

Total liabilities

100

% 100%

Equity

Contributed equity 56% 55%

Reserves 3% 5%

Retained earnings 38% 37%

Equity attributed to equity shareholders of

parent entity 97% 96%

Non-controlling interests 3% 4%

Total equity

100

% 100%

Interpretation- The table reflects the vertical analysis of balance sheet items by keeping

total assets, total liabilities and total equities as the base. The asset of an entity seems as stable

when they are evaluated on the basis of total assets. Similarly, the liabilities are resulted as

declining which reflects that the position of the company is becoming more and better with

passage of one period.

100

% 100%

Current liabilities

Payables 54% 52%

Borrowings 5% 2%

Tax payable 1% 1%

Other types of financial liabilities 0% 0%

Provisions 12% 12%

Liabilities for the sale 0% 0%

Total CL 72% 67%

Non-current liabilities

Borrowings 18% 22%

Other types of financial liabilities 0% 0%

Provisions 8% 8%

Other long term liabilities 2% 3%

Total LT liabilities 28% 33%

Total liabilities

100

% 100%

Equity

Contributed equity 56% 55%

Reserves 3% 5%

Retained earnings 38% 37%

Equity attributed to equity shareholders of

parent entity 97% 96%

Non-controlling interests 3% 4%

Total equity

100

% 100%

Interpretation- The table reflects the vertical analysis of balance sheet items by keeping

total assets, total liabilities and total equities as the base. The asset of an entity seems as stable

when they are evaluated on the basis of total assets. Similarly, the liabilities are resulted as

declining which reflects that the position of the company is becoming more and better with

passage of one period.

CONCLUSION

The above analysis summarized that the financial position and performance of

Wesfarmers is sound and better. Ratio analysis has been found as the best tool in making

comparison of the current year’s results with that of the past years results in an effective and

efficient manner. Moreover, Horizon analysis helps in analyzing and depicting the changes

occurred in all the items of income and balance sheet report between current and the past year so

that performance of the company could be measured effectively. Vertical analysis also acts as the

best tool as it enables in comparing of the absolute amounts of the different sizes that do not

provide for a useful conclusions regarding their financial position & performance. It helps in

finding the changes or the variations in the financial items of an individual account of asset or

the group of assets.

The above analysis summarized that the financial position and performance of

Wesfarmers is sound and better. Ratio analysis has been found as the best tool in making

comparison of the current year’s results with that of the past years results in an effective and

efficient manner. Moreover, Horizon analysis helps in analyzing and depicting the changes

occurred in all the items of income and balance sheet report between current and the past year so

that performance of the company could be measured effectively. Vertical analysis also acts as the

best tool as it enables in comparing of the absolute amounts of the different sizes that do not

provide for a useful conclusions regarding their financial position & performance. It helps in

finding the changes or the variations in the financial items of an individual account of asset or

the group of assets.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.