Essay on Impairment Loss Computation and Disclosure in Finance

VerifiedAdded on 2020/05/16

|9

|1380

|97

Essay

AI Summary

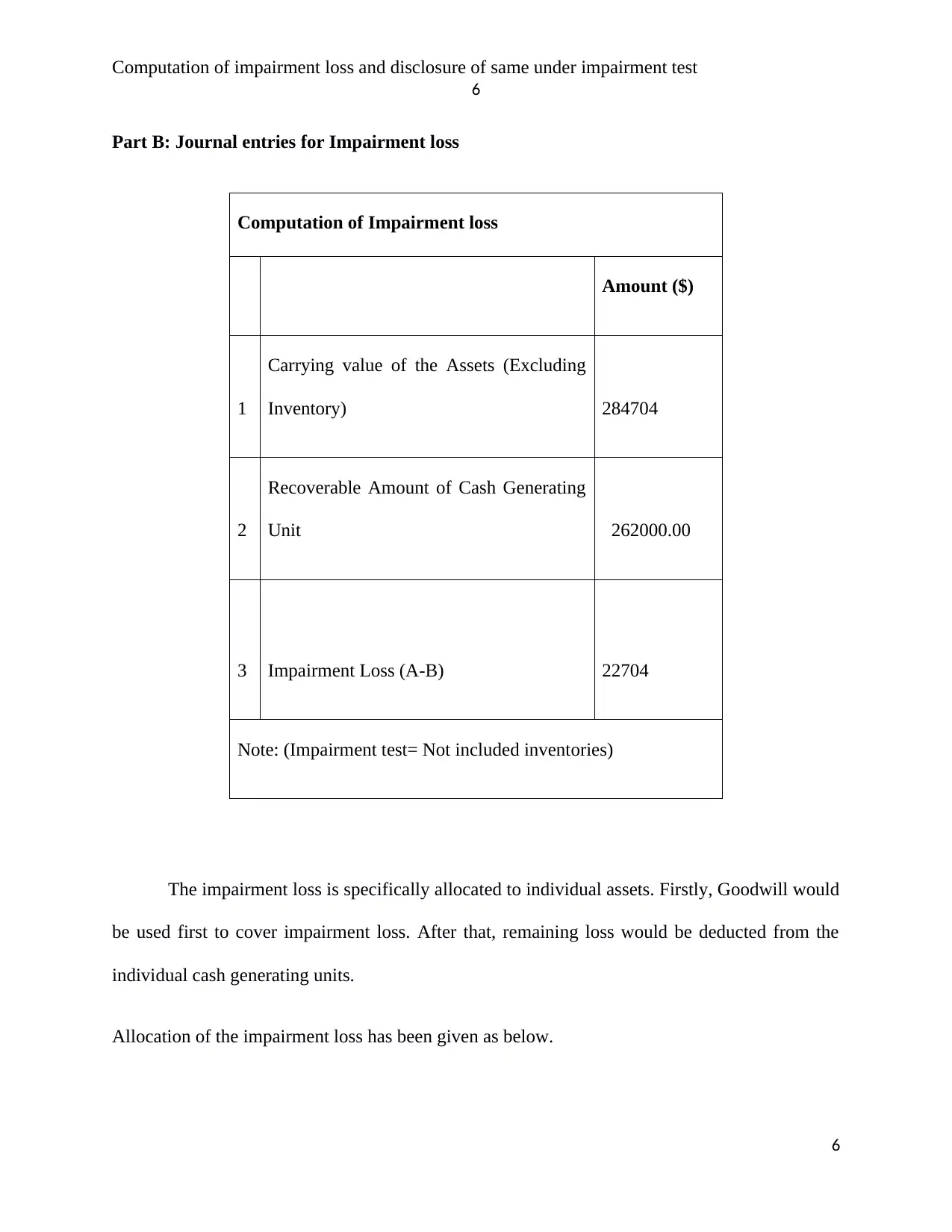

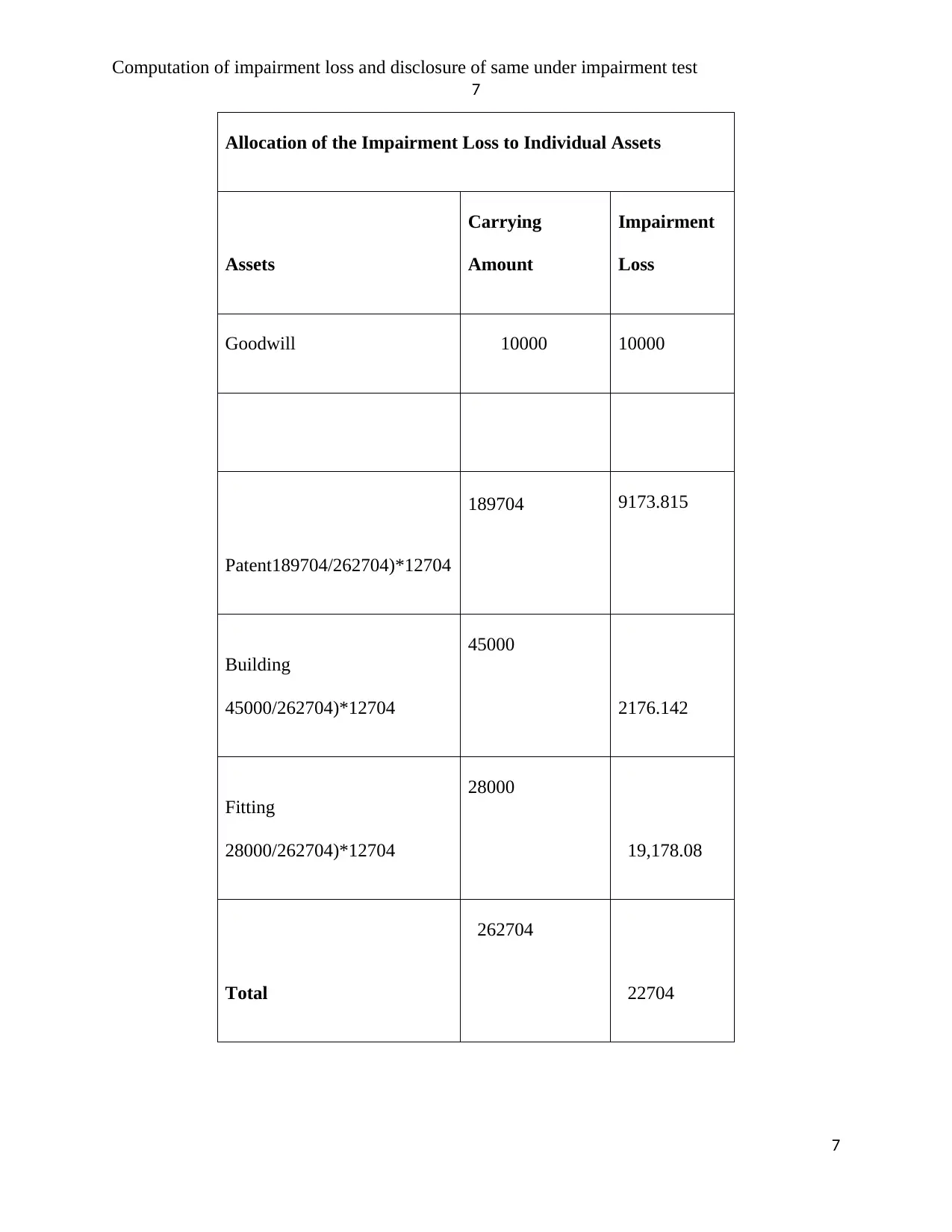

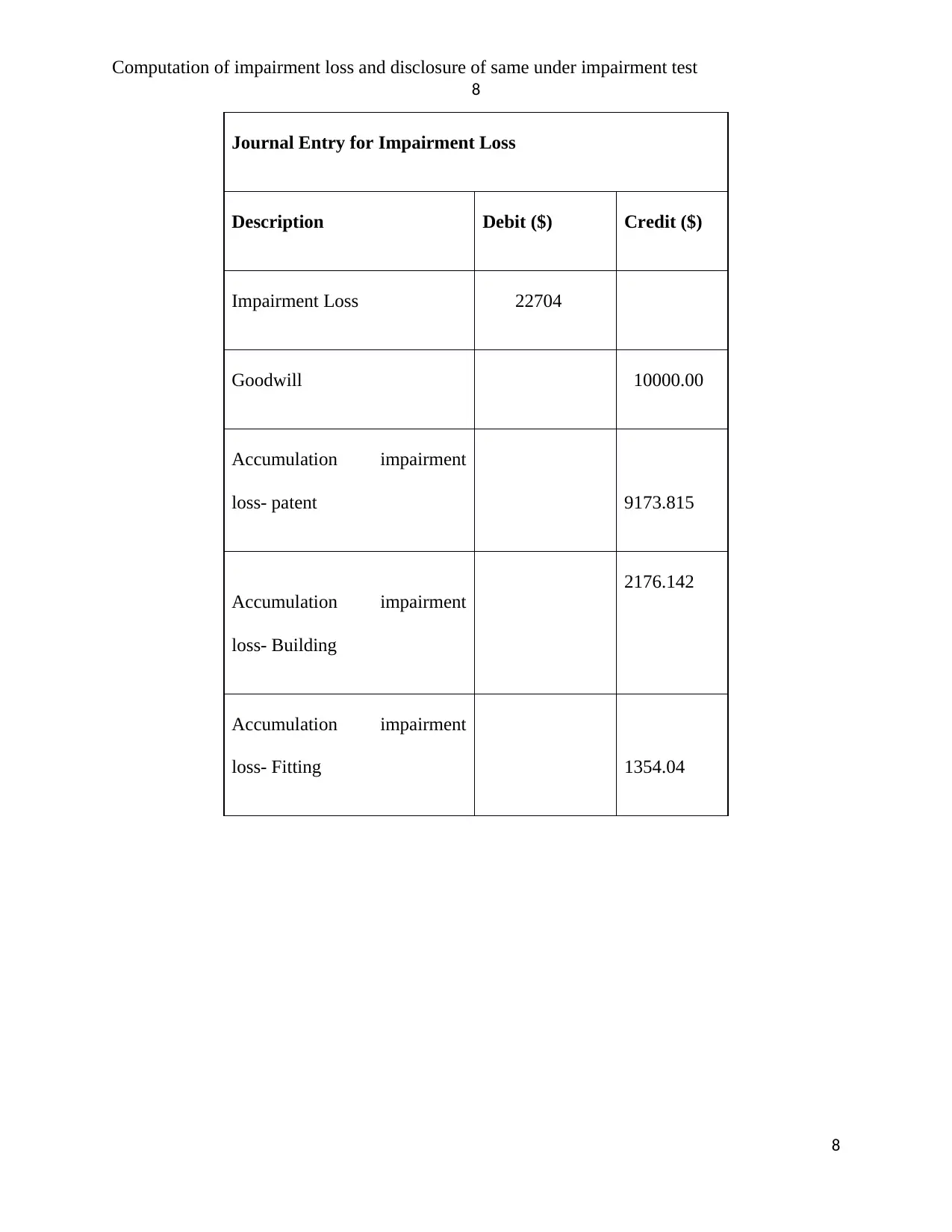

This essay delves into the concept of impairment loss, focusing on its computation and the necessary disclosure requirements under accounting standards, specifically AASB 136. The essay explains the nature of impairment loss, emphasizing how it reflects the true and fair value of assets in financial statements due to internal and external factors affecting asset values. It outlines the process of calculating impairment loss by comparing the carrying amount with the recoverable amount and discusses the circumstances under which impairment losses can be reversed. The essay also covers the disclosure requirements for impairment loss, including the need for detailed information about impairment tests, allocation of losses to cash-generating units, and proper recording in the books of account. Part B of the assignment provides a practical application with the computation of impairment loss, its allocation to different assets, and the corresponding journal entries.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.