University Finance Module: Estimation and Testing of the CAPM

VerifiedAdded on 2020/10/23

|12

|1900

|98

Homework Assignment

AI Summary

This assignment analyzes the Capital Asset Pricing Model (CAPM) through regression analysis and hypothesis testing. It begins with a regression analysis of Microsoft stock, interpreting the beta coefficient and testing the null hypothesis that alpha equals zero. Further, it involves performing hypothesis tests on beta, evaluating the aggressiveness of Microsoft stock, and interpreting the R-squared value. The assignment extends the analysis to GE, GM, IBM, Disney, and Mobil-Exxon, repeating the regression analysis for each. The document includes detailed regression outputs and interpretations, providing a comprehensive examination of the CAPM and its application to various stocks. The analysis covers topics such as market risk, predicted returns, and the assessment of stock volatility, providing insights into financial modeling and investment strategies.

Estimation and Testing of Capital Asset Pricing Model

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

1. Regression analysis..................................................................................................................3

2. Interpreting the estimate of βj from your regression result above...........................................3

3. Testing null hypothesis that αj = 0 for Microsoft stock in against to an appropriate

alternative hypotheses..................................................................................................................3

4. Performing a hypothesis test that βj = 0 against the alternative that βj ≠ 0 using the

Microsoft data..............................................................................................................................3

5. Evaluate whether Microsoft stock (a Tech stock) is an aggressive stock or not by applying

suitable test..................................................................................................................................4

6. Stating R2 for the regression and interpreting the same...........................................................5

7. Stating predicted return in relation to Microsoft for January 2009 if the risk free rate does

not change from December 2008 but the market return increases by 1%...................................5

8. Repeat Question 1 for GE, GM, IBM, Disney, and Mobil-Exxon..........................................5

APPENDIX......................................................................................................................................8

1...................................................................................................................................................8

2...................................................................................................................................................8

3...................................................................................................................................................8

1. Regression analysis..................................................................................................................3

2. Interpreting the estimate of βj from your regression result above...........................................3

3. Testing null hypothesis that αj = 0 for Microsoft stock in against to an appropriate

alternative hypotheses..................................................................................................................3

4. Performing a hypothesis test that βj = 0 against the alternative that βj ≠ 0 using the

Microsoft data..............................................................................................................................3

5. Evaluate whether Microsoft stock (a Tech stock) is an aggressive stock or not by applying

suitable test..................................................................................................................................4

6. Stating R2 for the regression and interpreting the same...........................................................5

7. Stating predicted return in relation to Microsoft for January 2009 if the risk free rate does

not change from December 2008 but the market return increases by 1%...................................5

8. Repeat Question 1 for GE, GM, IBM, Disney, and Mobil-Exxon..........................................5

APPENDIX......................................................................................................................................8

1...................................................................................................................................................8

2...................................................................................................................................................8

3...................................................................................................................................................8

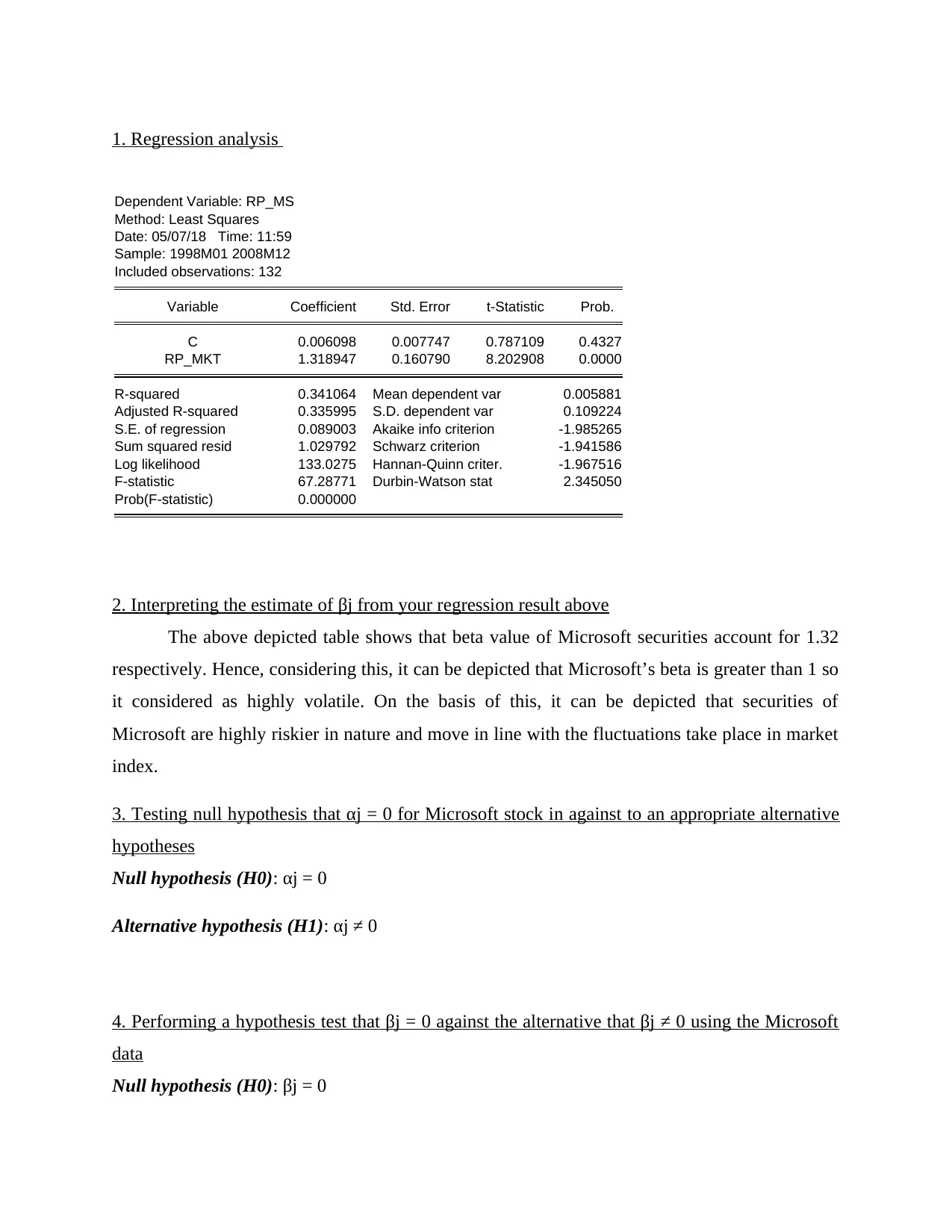

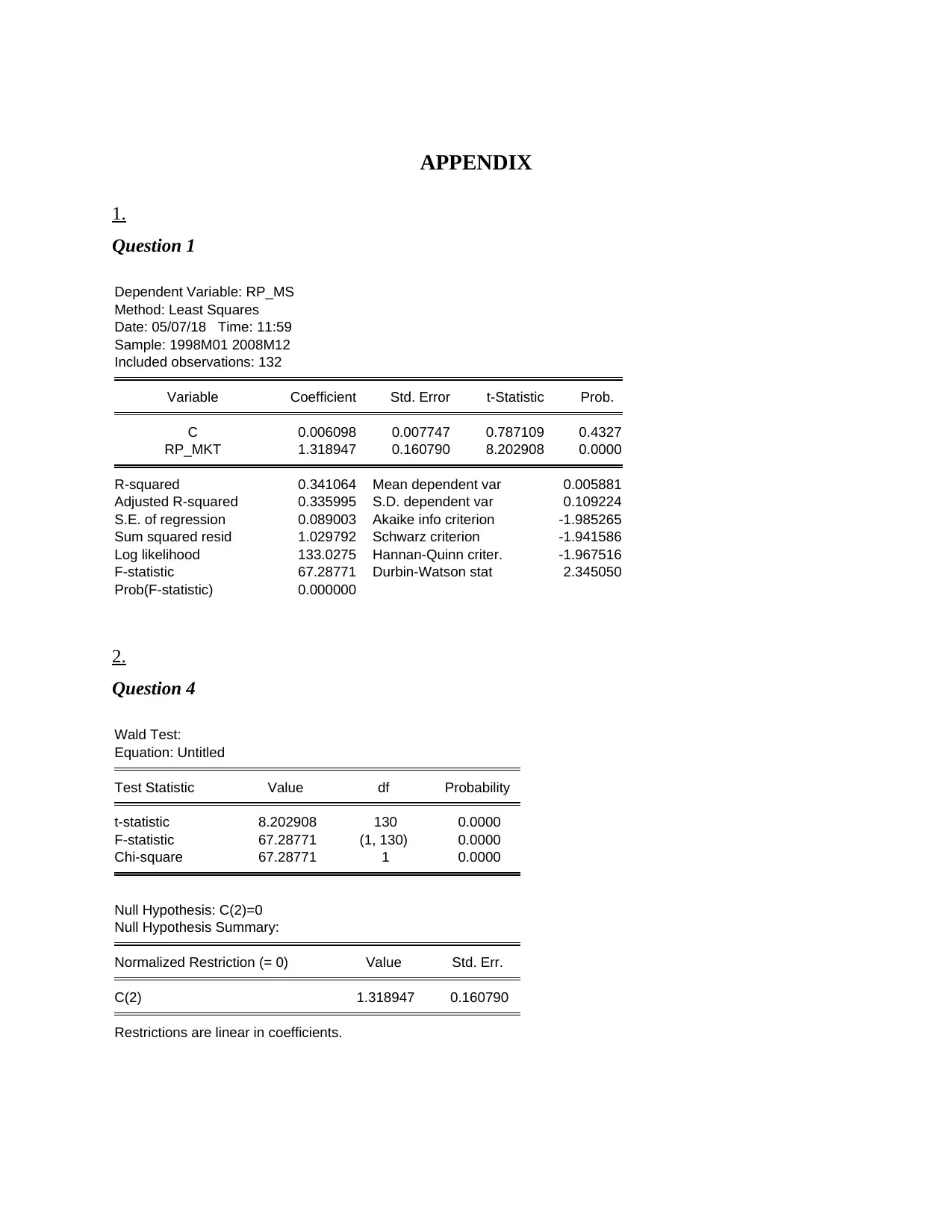

1. Regression analysis

Dependent Variable: RP_MS

Method: Least Squares

Date: 05/07/18 Time: 11:59

Sample: 1998M01 2008M12

Included observations: 132

Variable Coefficient Std. Error t-Statistic Prob.

C 0.006098 0.007747 0.787109 0.4327

RP_MKT 1.318947 0.160790 8.202908 0.0000

R-squared 0.341064 Mean dependent var 0.005881

Adjusted R-squared 0.335995 S.D. dependent var 0.109224

S.E. of regression 0.089003 Akaike info criterion -1.985265

Sum squared resid 1.029792 Schwarz criterion -1.941586

Log likelihood 133.0275 Hannan-Quinn criter. -1.967516

F-statistic 67.28771 Durbin-Watson stat 2.345050

Prob(F-statistic) 0.000000

2. Interpreting the estimate of βj from your regression result above

The above depicted table shows that beta value of Microsoft securities account for 1.32

respectively. Hence, considering this, it can be depicted that Microsoft’s beta is greater than 1 so

it considered as highly volatile. On the basis of this, it can be depicted that securities of

Microsoft are highly riskier in nature and move in line with the fluctuations take place in market

index.

3. Testing null hypothesis that αj = 0 for Microsoft stock in against to an appropriate alternative

hypotheses

Null hypothesis (H0): αj = 0

Alternative hypothesis (H1): αj ≠ 0

4. Performing a hypothesis test that βj = 0 against the alternative that βj ≠ 0 using the Microsoft

data

Null hypothesis (H0): βj = 0

Dependent Variable: RP_MS

Method: Least Squares

Date: 05/07/18 Time: 11:59

Sample: 1998M01 2008M12

Included observations: 132

Variable Coefficient Std. Error t-Statistic Prob.

C 0.006098 0.007747 0.787109 0.4327

RP_MKT 1.318947 0.160790 8.202908 0.0000

R-squared 0.341064 Mean dependent var 0.005881

Adjusted R-squared 0.335995 S.D. dependent var 0.109224

S.E. of regression 0.089003 Akaike info criterion -1.985265

Sum squared resid 1.029792 Schwarz criterion -1.941586

Log likelihood 133.0275 Hannan-Quinn criter. -1.967516

F-statistic 67.28771 Durbin-Watson stat 2.345050

Prob(F-statistic) 0.000000

2. Interpreting the estimate of βj from your regression result above

The above depicted table shows that beta value of Microsoft securities account for 1.32

respectively. Hence, considering this, it can be depicted that Microsoft’s beta is greater than 1 so

it considered as highly volatile. On the basis of this, it can be depicted that securities of

Microsoft are highly riskier in nature and move in line with the fluctuations take place in market

index.

3. Testing null hypothesis that αj = 0 for Microsoft stock in against to an appropriate alternative

hypotheses

Null hypothesis (H0): αj = 0

Alternative hypothesis (H1): αj ≠ 0

4. Performing a hypothesis test that βj = 0 against the alternative that βj ≠ 0 using the Microsoft

data

Null hypothesis (H0): βj = 0

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

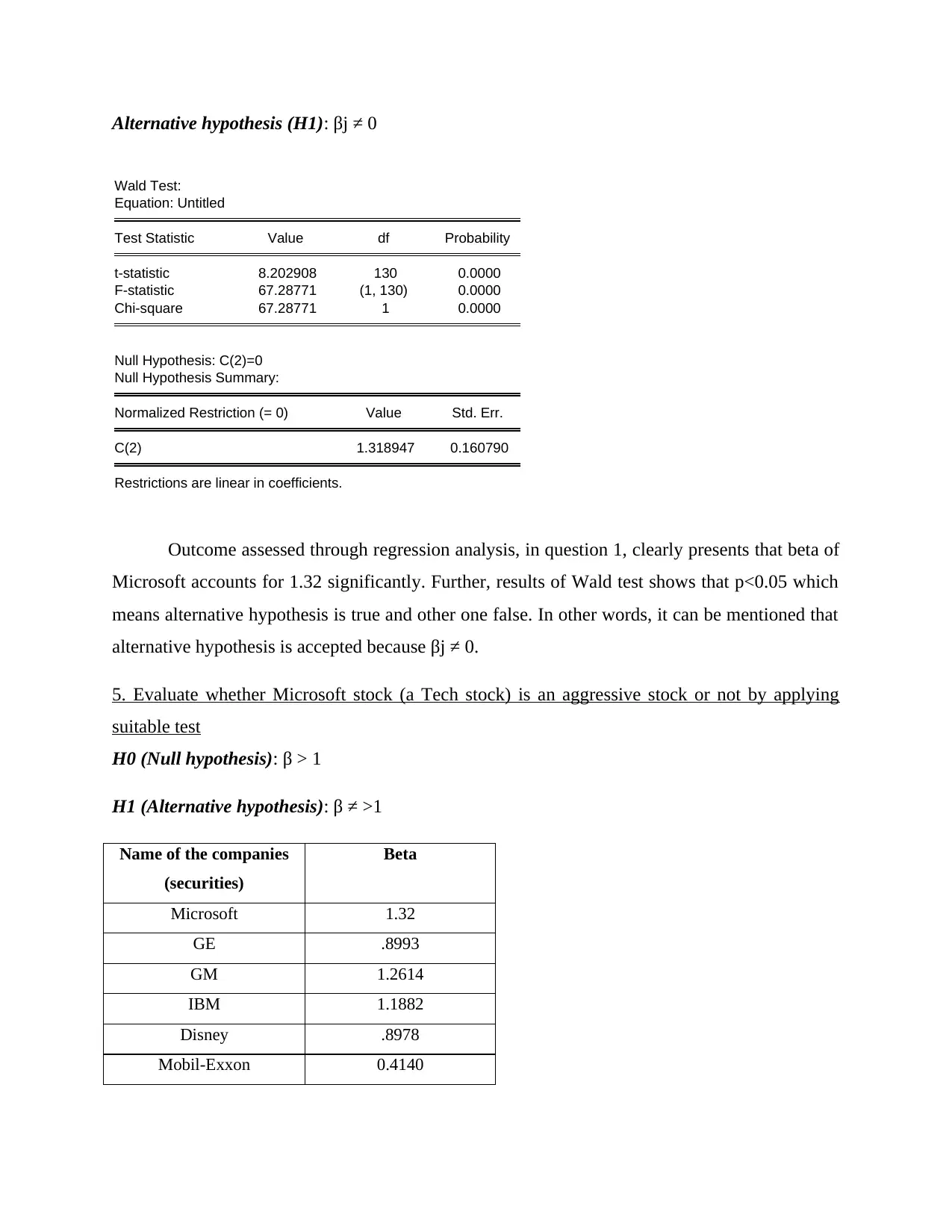

Alternative hypothesis (H1): βj ≠ 0

Wald Test:

Equation: Untitled

Test Statistic Value df Probability

t-statistic 8.202908 130 0.0000

F-statistic 67.28771 (1, 130) 0.0000

Chi-square 67.28771 1 0.0000

Null Hypothesis: C(2)=0

Null Hypothesis Summary:

Normalized Restriction (= 0) Value Std. Err.

C(2) 1.318947 0.160790

Restrictions are linear in coefficients.

Outcome assessed through regression analysis, in question 1, clearly presents that beta of

Microsoft accounts for 1.32 significantly. Further, results of Wald test shows that p<0.05 which

means alternative hypothesis is true and other one false. In other words, it can be mentioned that

alternative hypothesis is accepted because βj ≠ 0.

5. Evaluate whether Microsoft stock (a Tech stock) is an aggressive stock or not by applying

suitable test

H0 (Null hypothesis): β > 1

H1 (Alternative hypothesis): β ≠ >1

Name of the companies

(securities)

Beta

Microsoft 1.32

GE .8993

GM 1.2614

IBM 1.1882

Disney .8978

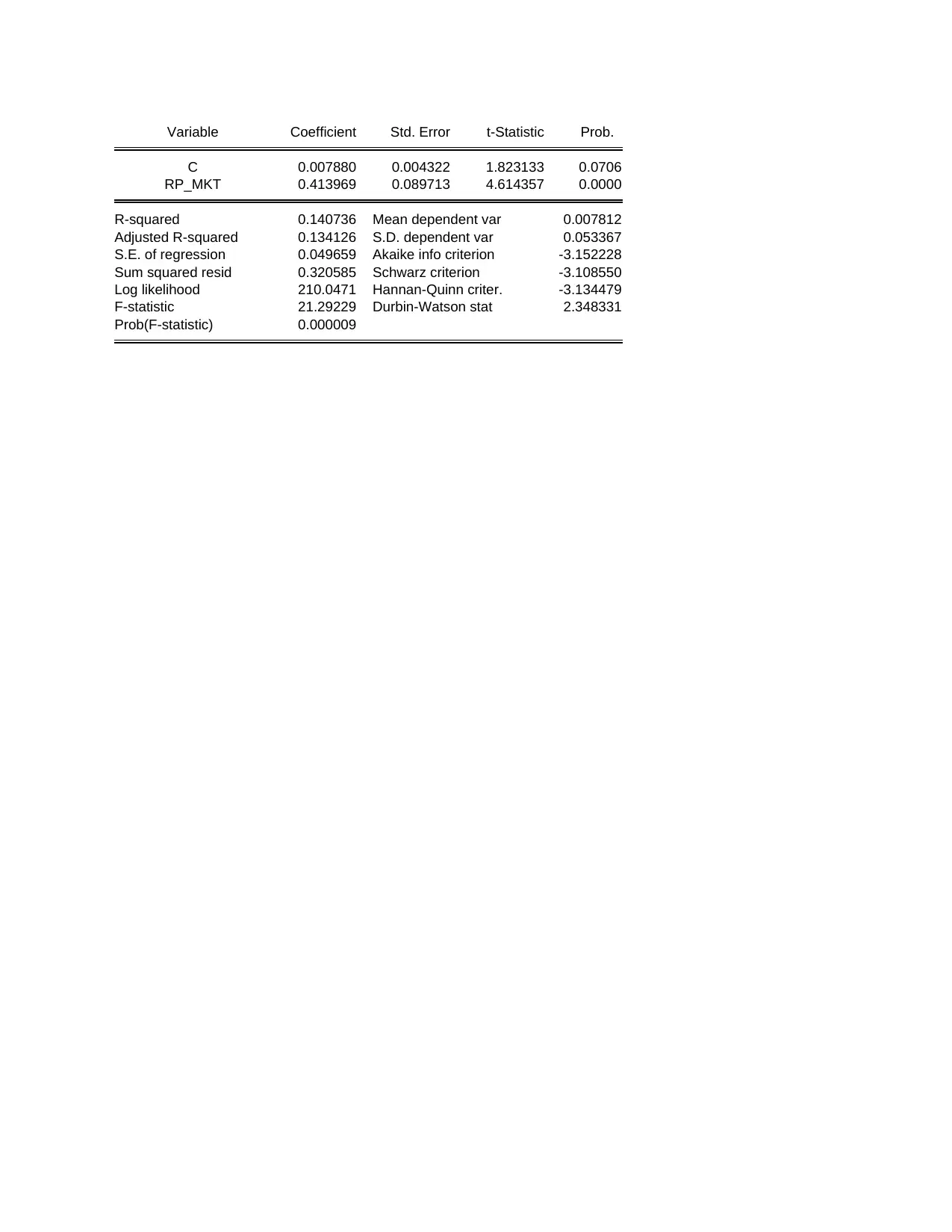

Mobil-Exxon 0.4140

Wald Test:

Equation: Untitled

Test Statistic Value df Probability

t-statistic 8.202908 130 0.0000

F-statistic 67.28771 (1, 130) 0.0000

Chi-square 67.28771 1 0.0000

Null Hypothesis: C(2)=0

Null Hypothesis Summary:

Normalized Restriction (= 0) Value Std. Err.

C(2) 1.318947 0.160790

Restrictions are linear in coefficients.

Outcome assessed through regression analysis, in question 1, clearly presents that beta of

Microsoft accounts for 1.32 significantly. Further, results of Wald test shows that p<0.05 which

means alternative hypothesis is true and other one false. In other words, it can be mentioned that

alternative hypothesis is accepted because βj ≠ 0.

5. Evaluate whether Microsoft stock (a Tech stock) is an aggressive stock or not by applying

suitable test

H0 (Null hypothesis): β > 1

H1 (Alternative hypothesis): β ≠ >1

Name of the companies

(securities)

Beta

Microsoft 1.32

GE .8993

GM 1.2614

IBM 1.1882

Disney .8978

Mobil-Exxon 0.4140

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

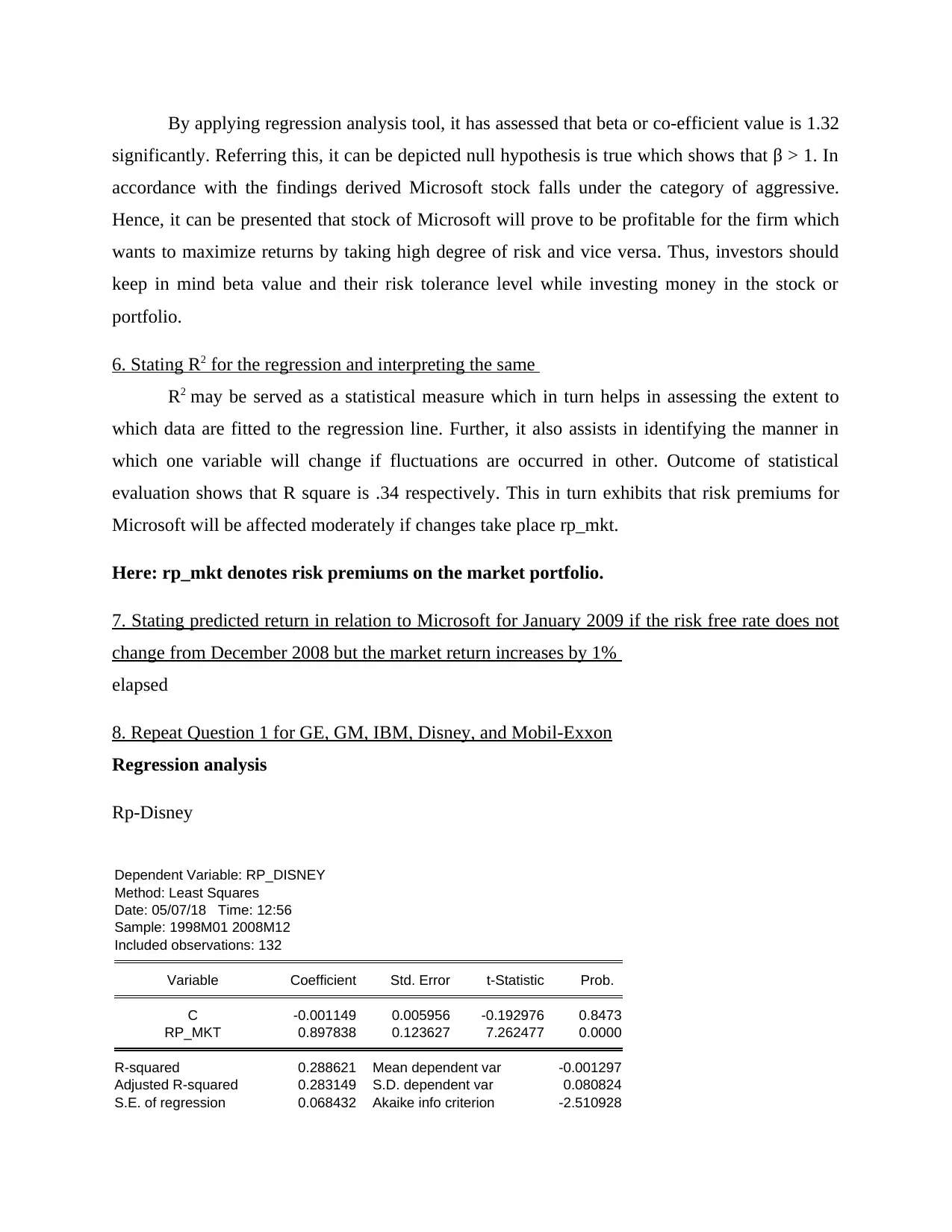

By applying regression analysis tool, it has assessed that beta or co-efficient value is 1.32

significantly. Referring this, it can be depicted null hypothesis is true which shows that β > 1. In

accordance with the findings derived Microsoft stock falls under the category of aggressive.

Hence, it can be presented that stock of Microsoft will prove to be profitable for the firm which

wants to maximize returns by taking high degree of risk and vice versa. Thus, investors should

keep in mind beta value and their risk tolerance level while investing money in the stock or

portfolio.

6. Stating R2 for the regression and interpreting the same

R2 may be served as a statistical measure which in turn helps in assessing the extent to

which data are fitted to the regression line. Further, it also assists in identifying the manner in

which one variable will change if fluctuations are occurred in other. Outcome of statistical

evaluation shows that R square is .34 respectively. This in turn exhibits that risk premiums for

Microsoft will be affected moderately if changes take place rp_mkt.

Here: rp_mkt denotes risk premiums on the market portfolio.

7. Stating predicted return in relation to Microsoft for January 2009 if the risk free rate does not

change from December 2008 but the market return increases by 1%

elapsed

8. Repeat Question 1 for GE, GM, IBM, Disney, and Mobil-Exxon

Regression analysis

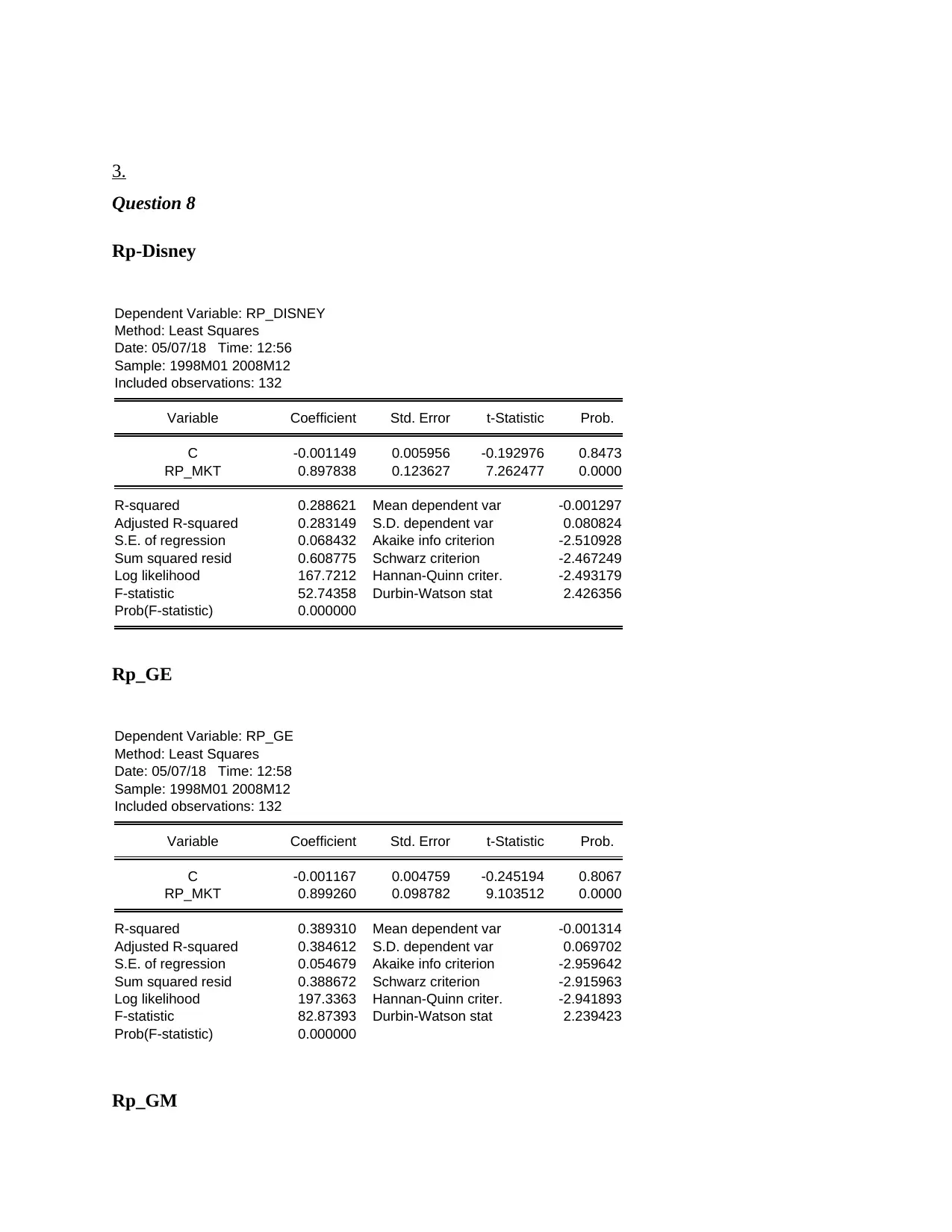

Rp-Disney

Dependent Variable: RP_DISNEY

Method: Least Squares

Date: 05/07/18 Time: 12:56

Sample: 1998M01 2008M12

Included observations: 132

Variable Coefficient Std. Error t-Statistic Prob.

C -0.001149 0.005956 -0.192976 0.8473

RP_MKT 0.897838 0.123627 7.262477 0.0000

R-squared 0.288621 Mean dependent var -0.001297

Adjusted R-squared 0.283149 S.D. dependent var 0.080824

S.E. of regression 0.068432 Akaike info criterion -2.510928

significantly. Referring this, it can be depicted null hypothesis is true which shows that β > 1. In

accordance with the findings derived Microsoft stock falls under the category of aggressive.

Hence, it can be presented that stock of Microsoft will prove to be profitable for the firm which

wants to maximize returns by taking high degree of risk and vice versa. Thus, investors should

keep in mind beta value and their risk tolerance level while investing money in the stock or

portfolio.

6. Stating R2 for the regression and interpreting the same

R2 may be served as a statistical measure which in turn helps in assessing the extent to

which data are fitted to the regression line. Further, it also assists in identifying the manner in

which one variable will change if fluctuations are occurred in other. Outcome of statistical

evaluation shows that R square is .34 respectively. This in turn exhibits that risk premiums for

Microsoft will be affected moderately if changes take place rp_mkt.

Here: rp_mkt denotes risk premiums on the market portfolio.

7. Stating predicted return in relation to Microsoft for January 2009 if the risk free rate does not

change from December 2008 but the market return increases by 1%

elapsed

8. Repeat Question 1 for GE, GM, IBM, Disney, and Mobil-Exxon

Regression analysis

Rp-Disney

Dependent Variable: RP_DISNEY

Method: Least Squares

Date: 05/07/18 Time: 12:56

Sample: 1998M01 2008M12

Included observations: 132

Variable Coefficient Std. Error t-Statistic Prob.

C -0.001149 0.005956 -0.192976 0.8473

RP_MKT 0.897838 0.123627 7.262477 0.0000

R-squared 0.288621 Mean dependent var -0.001297

Adjusted R-squared 0.283149 S.D. dependent var 0.080824

S.E. of regression 0.068432 Akaike info criterion -2.510928

Sum squared resid 0.608775 Schwarz criterion -2.467249

Log likelihood 167.7212 Hannan-Quinn criter. -2.493179

F-statistic 52.74358 Durbin-Watson stat 2.426356

Prob(F-statistic) 0.000000

Rp_GE

Dependent Variable: RP_GE

Method: Least Squares

Date: 05/07/18 Time: 12:58

Sample: 1998M01 2008M12

Included observations: 132

Variable Coefficient Std. Error t-Statistic Prob.

C -0.001167 0.004759 -0.245194 0.8067

RP_MKT 0.899260 0.098782 9.103512 0.0000

R-squared 0.389310 Mean dependent var -0.001314

Adjusted R-squared 0.384612 S.D. dependent var 0.069702

S.E. of regression 0.054679 Akaike info criterion -2.959642

Sum squared resid 0.388672 Schwarz criterion -2.915963

Log likelihood 197.3363 Hannan-Quinn criter. -2.941893

F-statistic 82.87393 Durbin-Watson stat 2.239423

Prob(F-statistic) 0.000000

Rp_GM

Dependent Variable: RP_GM

Method: Least Squares

Date: 05/07/18 Time: 12:58

Sample: 1998M01 2008M12

Included observations: 132

Variable Coefficient Std. Error t-Statistic Prob.

C -0.011550 0.009743 -1.185474 0.2380

RP_MKT 1.261411 0.202223 6.237709 0.0000

R-squared 0.230355 Mean dependent var -0.011757

Adjusted R-squared 0.224435 S.D. dependent var 0.127106

S.E. of regression 0.111937 Akaike info criterion -1.526719

Sum squared resid 1.628896 Schwarz criterion -1.483041

Log likelihood 102.7635 Hannan-Quinn criter. -1.508970

F-statistic 38.90901 Durbin-Watson stat 2.062907

Prob(F-statistic) 0.000000

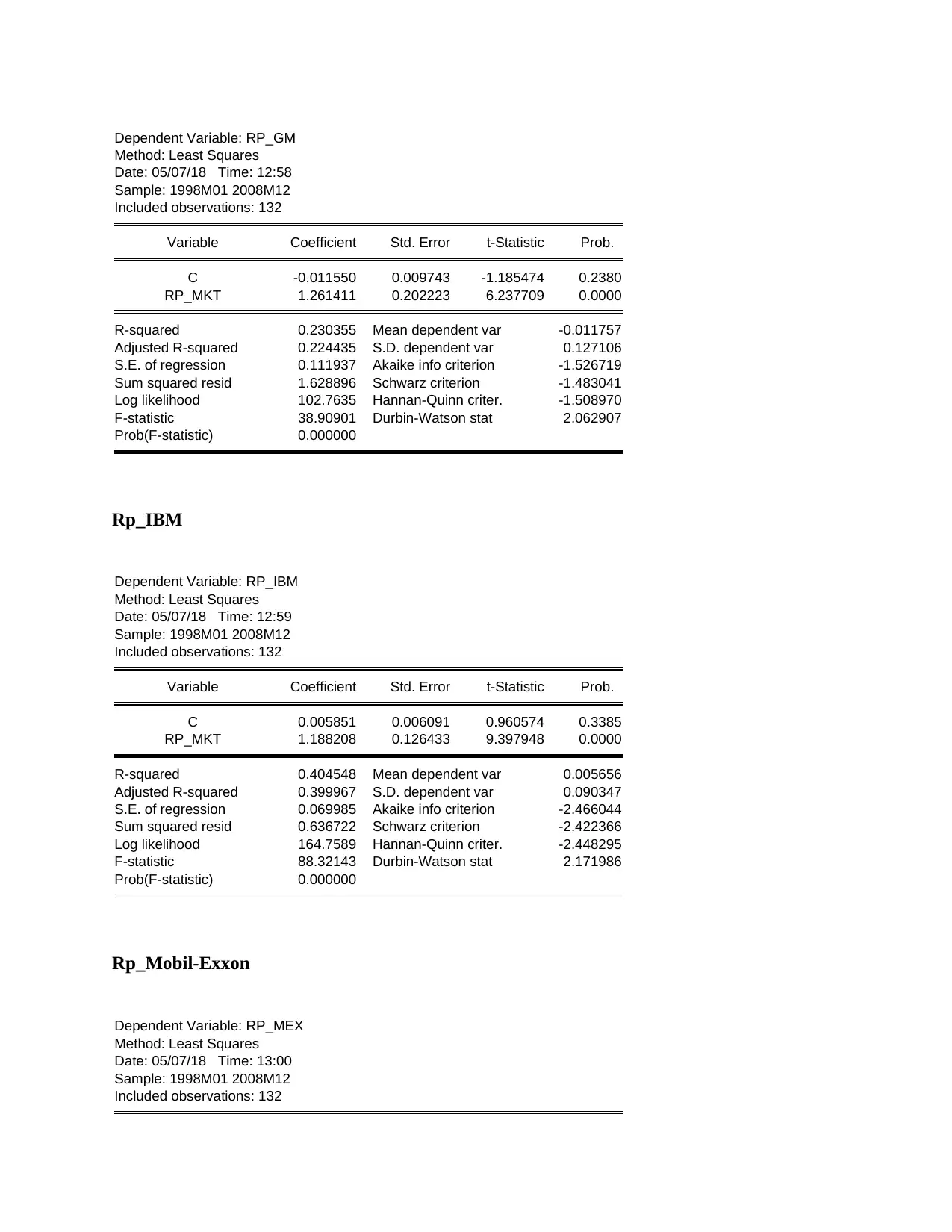

Rp_IBM

Log likelihood 167.7212 Hannan-Quinn criter. -2.493179

F-statistic 52.74358 Durbin-Watson stat 2.426356

Prob(F-statistic) 0.000000

Rp_GE

Dependent Variable: RP_GE

Method: Least Squares

Date: 05/07/18 Time: 12:58

Sample: 1998M01 2008M12

Included observations: 132

Variable Coefficient Std. Error t-Statistic Prob.

C -0.001167 0.004759 -0.245194 0.8067

RP_MKT 0.899260 0.098782 9.103512 0.0000

R-squared 0.389310 Mean dependent var -0.001314

Adjusted R-squared 0.384612 S.D. dependent var 0.069702

S.E. of regression 0.054679 Akaike info criterion -2.959642

Sum squared resid 0.388672 Schwarz criterion -2.915963

Log likelihood 197.3363 Hannan-Quinn criter. -2.941893

F-statistic 82.87393 Durbin-Watson stat 2.239423

Prob(F-statistic) 0.000000

Rp_GM

Dependent Variable: RP_GM

Method: Least Squares

Date: 05/07/18 Time: 12:58

Sample: 1998M01 2008M12

Included observations: 132

Variable Coefficient Std. Error t-Statistic Prob.

C -0.011550 0.009743 -1.185474 0.2380

RP_MKT 1.261411 0.202223 6.237709 0.0000

R-squared 0.230355 Mean dependent var -0.011757

Adjusted R-squared 0.224435 S.D. dependent var 0.127106

S.E. of regression 0.111937 Akaike info criterion -1.526719

Sum squared resid 1.628896 Schwarz criterion -1.483041

Log likelihood 102.7635 Hannan-Quinn criter. -1.508970

F-statistic 38.90901 Durbin-Watson stat 2.062907

Prob(F-statistic) 0.000000

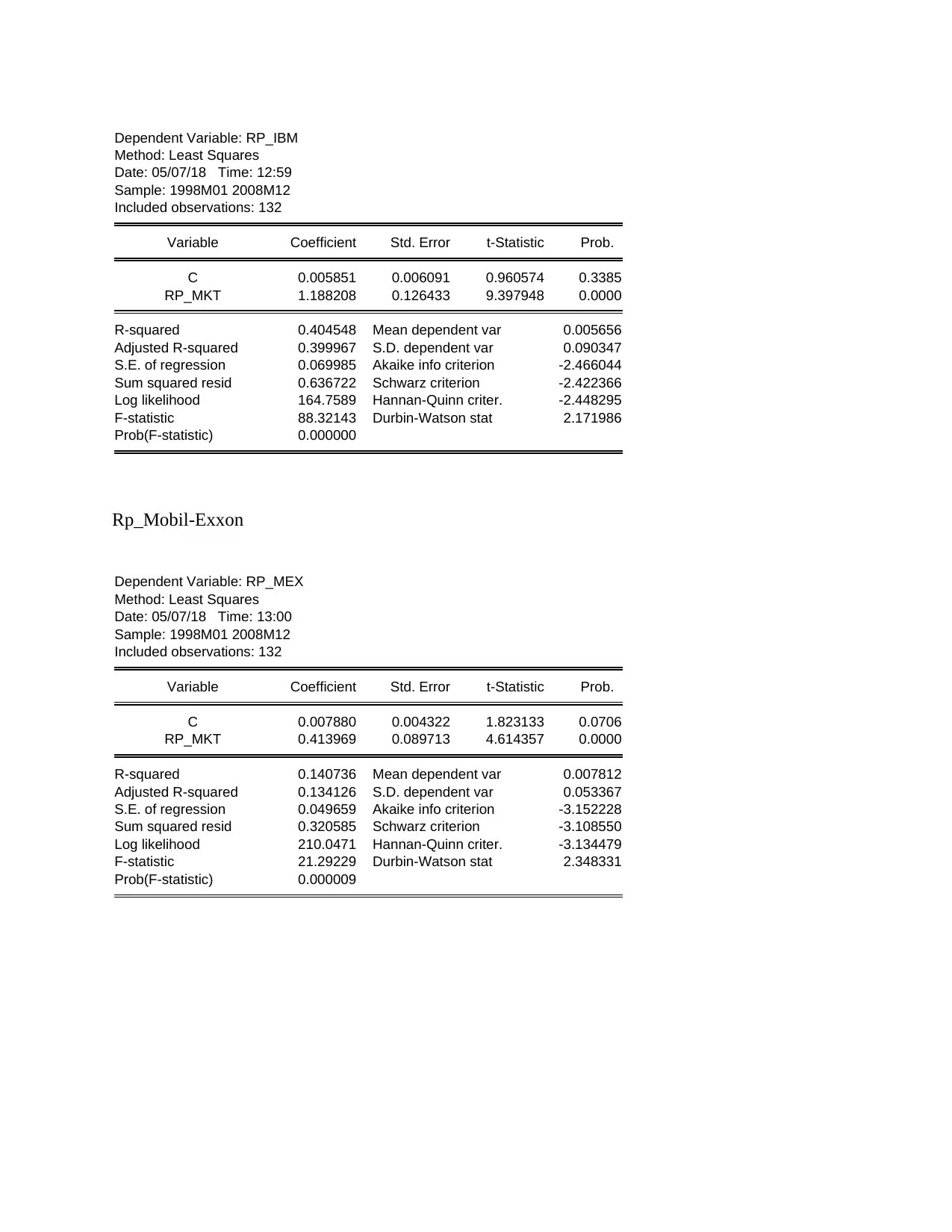

Rp_IBM

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Dependent Variable: RP_IBM

Method: Least Squares

Date: 05/07/18 Time: 12:59

Sample: 1998M01 2008M12

Included observations: 132

Variable Coefficient Std. Error t-Statistic Prob.

C 0.005851 0.006091 0.960574 0.3385

RP_MKT 1.188208 0.126433 9.397948 0.0000

R-squared 0.404548 Mean dependent var 0.005656

Adjusted R-squared 0.399967 S.D. dependent var 0.090347

S.E. of regression 0.069985 Akaike info criterion -2.466044

Sum squared resid 0.636722 Schwarz criterion -2.422366

Log likelihood 164.7589 Hannan-Quinn criter. -2.448295

F-statistic 88.32143 Durbin-Watson stat 2.171986

Prob(F-statistic) 0.000000

Rp_Mobil-Exxon

Dependent Variable: RP_MEX

Method: Least Squares

Date: 05/07/18 Time: 13:00

Sample: 1998M01 2008M12

Included observations: 132

Variable Coefficient Std. Error t-Statistic Prob.

C 0.007880 0.004322 1.823133 0.0706

RP_MKT 0.413969 0.089713 4.614357 0.0000

R-squared 0.140736 Mean dependent var 0.007812

Adjusted R-squared 0.134126 S.D. dependent var 0.053367

S.E. of regression 0.049659 Akaike info criterion -3.152228

Sum squared resid 0.320585 Schwarz criterion -3.108550

Log likelihood 210.0471 Hannan-Quinn criter. -3.134479

F-statistic 21.29229 Durbin-Watson stat 2.348331

Prob(F-statistic) 0.000009

Method: Least Squares

Date: 05/07/18 Time: 12:59

Sample: 1998M01 2008M12

Included observations: 132

Variable Coefficient Std. Error t-Statistic Prob.

C 0.005851 0.006091 0.960574 0.3385

RP_MKT 1.188208 0.126433 9.397948 0.0000

R-squared 0.404548 Mean dependent var 0.005656

Adjusted R-squared 0.399967 S.D. dependent var 0.090347

S.E. of regression 0.069985 Akaike info criterion -2.466044

Sum squared resid 0.636722 Schwarz criterion -2.422366

Log likelihood 164.7589 Hannan-Quinn criter. -2.448295

F-statistic 88.32143 Durbin-Watson stat 2.171986

Prob(F-statistic) 0.000000

Rp_Mobil-Exxon

Dependent Variable: RP_MEX

Method: Least Squares

Date: 05/07/18 Time: 13:00

Sample: 1998M01 2008M12

Included observations: 132

Variable Coefficient Std. Error t-Statistic Prob.

C 0.007880 0.004322 1.823133 0.0706

RP_MKT 0.413969 0.089713 4.614357 0.0000

R-squared 0.140736 Mean dependent var 0.007812

Adjusted R-squared 0.134126 S.D. dependent var 0.053367

S.E. of regression 0.049659 Akaike info criterion -3.152228

Sum squared resid 0.320585 Schwarz criterion -3.108550

Log likelihood 210.0471 Hannan-Quinn criter. -3.134479

F-statistic 21.29229 Durbin-Watson stat 2.348331

Prob(F-statistic) 0.000009

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

APPENDIX

1.

Question 1

Dependent Variable: RP_MS

Method: Least Squares

Date: 05/07/18 Time: 11:59

Sample: 1998M01 2008M12

Included observations: 132

Variable Coefficient Std. Error t-Statistic Prob.

C 0.006098 0.007747 0.787109 0.4327

RP_MKT 1.318947 0.160790 8.202908 0.0000

R-squared 0.341064 Mean dependent var 0.005881

Adjusted R-squared 0.335995 S.D. dependent var 0.109224

S.E. of regression 0.089003 Akaike info criterion -1.985265

Sum squared resid 1.029792 Schwarz criterion -1.941586

Log likelihood 133.0275 Hannan-Quinn criter. -1.967516

F-statistic 67.28771 Durbin-Watson stat 2.345050

Prob(F-statistic) 0.000000

2.

Question 4

Wald Test:

Equation: Untitled

Test Statistic Value df Probability

t-statistic 8.202908 130 0.0000

F-statistic 67.28771 (1, 130) 0.0000

Chi-square 67.28771 1 0.0000

Null Hypothesis: C(2)=0

Null Hypothesis Summary:

Normalized Restriction (= 0) Value Std. Err.

C(2) 1.318947 0.160790

Restrictions are linear in coefficients.

1.

Question 1

Dependent Variable: RP_MS

Method: Least Squares

Date: 05/07/18 Time: 11:59

Sample: 1998M01 2008M12

Included observations: 132

Variable Coefficient Std. Error t-Statistic Prob.

C 0.006098 0.007747 0.787109 0.4327

RP_MKT 1.318947 0.160790 8.202908 0.0000

R-squared 0.341064 Mean dependent var 0.005881

Adjusted R-squared 0.335995 S.D. dependent var 0.109224

S.E. of regression 0.089003 Akaike info criterion -1.985265

Sum squared resid 1.029792 Schwarz criterion -1.941586

Log likelihood 133.0275 Hannan-Quinn criter. -1.967516

F-statistic 67.28771 Durbin-Watson stat 2.345050

Prob(F-statistic) 0.000000

2.

Question 4

Wald Test:

Equation: Untitled

Test Statistic Value df Probability

t-statistic 8.202908 130 0.0000

F-statistic 67.28771 (1, 130) 0.0000

Chi-square 67.28771 1 0.0000

Null Hypothesis: C(2)=0

Null Hypothesis Summary:

Normalized Restriction (= 0) Value Std. Err.

C(2) 1.318947 0.160790

Restrictions are linear in coefficients.

3.

Question 8

Rp-Disney

Dependent Variable: RP_DISNEY

Method: Least Squares

Date: 05/07/18 Time: 12:56

Sample: 1998M01 2008M12

Included observations: 132

Variable Coefficient Std. Error t-Statistic Prob.

C -0.001149 0.005956 -0.192976 0.8473

RP_MKT 0.897838 0.123627 7.262477 0.0000

R-squared 0.288621 Mean dependent var -0.001297

Adjusted R-squared 0.283149 S.D. dependent var 0.080824

S.E. of regression 0.068432 Akaike info criterion -2.510928

Sum squared resid 0.608775 Schwarz criterion -2.467249

Log likelihood 167.7212 Hannan-Quinn criter. -2.493179

F-statistic 52.74358 Durbin-Watson stat 2.426356

Prob(F-statistic) 0.000000

Rp_GE

Dependent Variable: RP_GE

Method: Least Squares

Date: 05/07/18 Time: 12:58

Sample: 1998M01 2008M12

Included observations: 132

Variable Coefficient Std. Error t-Statistic Prob.

C -0.001167 0.004759 -0.245194 0.8067

RP_MKT 0.899260 0.098782 9.103512 0.0000

R-squared 0.389310 Mean dependent var -0.001314

Adjusted R-squared 0.384612 S.D. dependent var 0.069702

S.E. of regression 0.054679 Akaike info criterion -2.959642

Sum squared resid 0.388672 Schwarz criterion -2.915963

Log likelihood 197.3363 Hannan-Quinn criter. -2.941893

F-statistic 82.87393 Durbin-Watson stat 2.239423

Prob(F-statistic) 0.000000

Rp_GM

Question 8

Rp-Disney

Dependent Variable: RP_DISNEY

Method: Least Squares

Date: 05/07/18 Time: 12:56

Sample: 1998M01 2008M12

Included observations: 132

Variable Coefficient Std. Error t-Statistic Prob.

C -0.001149 0.005956 -0.192976 0.8473

RP_MKT 0.897838 0.123627 7.262477 0.0000

R-squared 0.288621 Mean dependent var -0.001297

Adjusted R-squared 0.283149 S.D. dependent var 0.080824

S.E. of regression 0.068432 Akaike info criterion -2.510928

Sum squared resid 0.608775 Schwarz criterion -2.467249

Log likelihood 167.7212 Hannan-Quinn criter. -2.493179

F-statistic 52.74358 Durbin-Watson stat 2.426356

Prob(F-statistic) 0.000000

Rp_GE

Dependent Variable: RP_GE

Method: Least Squares

Date: 05/07/18 Time: 12:58

Sample: 1998M01 2008M12

Included observations: 132

Variable Coefficient Std. Error t-Statistic Prob.

C -0.001167 0.004759 -0.245194 0.8067

RP_MKT 0.899260 0.098782 9.103512 0.0000

R-squared 0.389310 Mean dependent var -0.001314

Adjusted R-squared 0.384612 S.D. dependent var 0.069702

S.E. of regression 0.054679 Akaike info criterion -2.959642

Sum squared resid 0.388672 Schwarz criterion -2.915963

Log likelihood 197.3363 Hannan-Quinn criter. -2.941893

F-statistic 82.87393 Durbin-Watson stat 2.239423

Prob(F-statistic) 0.000000

Rp_GM

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Dependent Variable: RP_GM

Method: Least Squares

Date: 05/07/18 Time: 12:58

Sample: 1998M01 2008M12

Included observations: 132

Variable Coefficient Std. Error t-Statistic Prob.

C -0.011550 0.009743 -1.185474 0.2380

RP_MKT 1.261411 0.202223 6.237709 0.0000

R-squared 0.230355 Mean dependent var -0.011757

Adjusted R-squared 0.224435 S.D. dependent var 0.127106

S.E. of regression 0.111937 Akaike info criterion -1.526719

Sum squared resid 1.628896 Schwarz criterion -1.483041

Log likelihood 102.7635 Hannan-Quinn criter. -1.508970

F-statistic 38.90901 Durbin-Watson stat 2.062907

Prob(F-statistic) 0.000000

Rp_IBM

Dependent Variable: RP_IBM

Method: Least Squares

Date: 05/07/18 Time: 12:59

Sample: 1998M01 2008M12

Included observations: 132

Variable Coefficient Std. Error t-Statistic Prob.

C 0.005851 0.006091 0.960574 0.3385

RP_MKT 1.188208 0.126433 9.397948 0.0000

R-squared 0.404548 Mean dependent var 0.005656

Adjusted R-squared 0.399967 S.D. dependent var 0.090347

S.E. of regression 0.069985 Akaike info criterion -2.466044

Sum squared resid 0.636722 Schwarz criterion -2.422366

Log likelihood 164.7589 Hannan-Quinn criter. -2.448295

F-statistic 88.32143 Durbin-Watson stat 2.171986

Prob(F-statistic) 0.000000

Rp_Mobil-Exxon

Dependent Variable: RP_MEX

Method: Least Squares

Date: 05/07/18 Time: 13:00

Sample: 1998M01 2008M12

Included observations: 132

Method: Least Squares

Date: 05/07/18 Time: 12:58

Sample: 1998M01 2008M12

Included observations: 132

Variable Coefficient Std. Error t-Statistic Prob.

C -0.011550 0.009743 -1.185474 0.2380

RP_MKT 1.261411 0.202223 6.237709 0.0000

R-squared 0.230355 Mean dependent var -0.011757

Adjusted R-squared 0.224435 S.D. dependent var 0.127106

S.E. of regression 0.111937 Akaike info criterion -1.526719

Sum squared resid 1.628896 Schwarz criterion -1.483041

Log likelihood 102.7635 Hannan-Quinn criter. -1.508970

F-statistic 38.90901 Durbin-Watson stat 2.062907

Prob(F-statistic) 0.000000

Rp_IBM

Dependent Variable: RP_IBM

Method: Least Squares

Date: 05/07/18 Time: 12:59

Sample: 1998M01 2008M12

Included observations: 132

Variable Coefficient Std. Error t-Statistic Prob.

C 0.005851 0.006091 0.960574 0.3385

RP_MKT 1.188208 0.126433 9.397948 0.0000

R-squared 0.404548 Mean dependent var 0.005656

Adjusted R-squared 0.399967 S.D. dependent var 0.090347

S.E. of regression 0.069985 Akaike info criterion -2.466044

Sum squared resid 0.636722 Schwarz criterion -2.422366

Log likelihood 164.7589 Hannan-Quinn criter. -2.448295

F-statistic 88.32143 Durbin-Watson stat 2.171986

Prob(F-statistic) 0.000000

Rp_Mobil-Exxon

Dependent Variable: RP_MEX

Method: Least Squares

Date: 05/07/18 Time: 13:00

Sample: 1998M01 2008M12

Included observations: 132

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Variable Coefficient Std. Error t-Statistic Prob.

C 0.007880 0.004322 1.823133 0.0706

RP_MKT 0.413969 0.089713 4.614357 0.0000

R-squared 0.140736 Mean dependent var 0.007812

Adjusted R-squared 0.134126 S.D. dependent var 0.053367

S.E. of regression 0.049659 Akaike info criterion -3.152228

Sum squared resid 0.320585 Schwarz criterion -3.108550

Log likelihood 210.0471 Hannan-Quinn criter. -3.134479

F-statistic 21.29229 Durbin-Watson stat 2.348331

Prob(F-statistic) 0.000009

C 0.007880 0.004322 1.823133 0.0706

RP_MKT 0.413969 0.089713 4.614357 0.0000

R-squared 0.140736 Mean dependent var 0.007812

Adjusted R-squared 0.134126 S.D. dependent var 0.053367

S.E. of regression 0.049659 Akaike info criterion -3.152228

Sum squared resid 0.320585 Schwarz criterion -3.108550

Log likelihood 210.0471 Hannan-Quinn criter. -3.134479

F-statistic 21.29229 Durbin-Watson stat 2.348331

Prob(F-statistic) 0.000009

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12