Report: Analysis of APN Outdoor Group's Financial Structure

VerifiedAdded on 2020/03/23

|9

|1198

|472

Report

AI Summary

This report provides a comprehensive analysis of the APN Outdoor Group's capital structure and financial performance. It begins with an overview of capital budgeting techniques, including payback periods and average rates of return, and then delves into an examination of the APN Outdoor Group's weighted average cost of capital (WACC). The report analyzes the company's financial ratios, including current, cash, and quick ratios, as well as interest coverage and debt-to-asset ratios. It also compares the APN Group's performance to its competitor, Ooh Media, and discusses the impact of capital structure decisions on the cost of capital. The report concludes by highlighting the importance of financial decisions in generating satisfactory returns for shareholders and paying dividends.

Running head: ACCOUNTING AND FINANCE

Accounting and Finance

Name of Student:

Name of University:

Author’s Note:

Accounting and Finance

Name of Student:

Name of University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTING AND FINANCE

Answer to Part A:

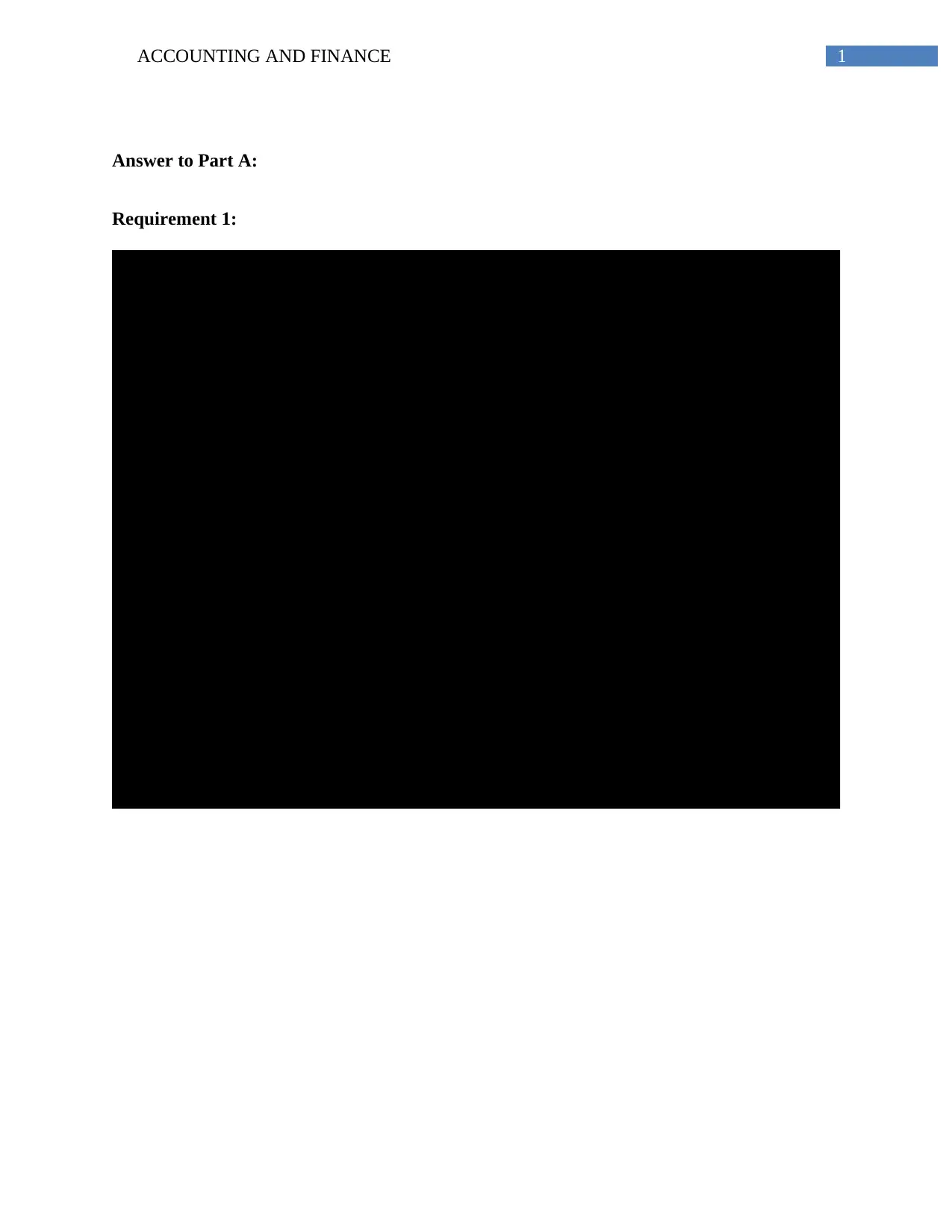

Requirement 1:

Particulars 0 1 2 3 4 5 6 7 8

Initial Investment ($1,650,000)

Annual Cash Flow:

Incremental Revene $1,445,000 $1,589,500 $1,748,450 $1,923,295 $2,115,625 $2,327,187 $2,559,906 $2,815,896

Staff Cost ($900,000) ($954,000) ($1,011,240) ($1,071,914) ($1,136,229) ($1,204,403) ($1,276,667) ($1,353,267)

Material Costs ($210,000) ($222,600) ($235,956) ($250,113) ($265,120) ($281,027) ($297,889) ($315,762)

Marketing Costs ($46,000) ($48,760) ($51,686) ($54,787) ($58,074) ($61,558) ($65,252) ($69,167)

Other Costs ($25,000) ($26,500) ($28,090) ($29,775) ($31,562) ($33,456) ($35,463) ($37,591)

Depreciation of Lab ($206,250) ($206,250) ($206,250) ($206,250) ($206,250) ($206,250) ($206,250) ($206,250)

Net Profit before Tax $57,750 $131,390 $215,228 $310,455 $418,389 $540,493 $678,385 $833,859

Less: Tax on Profit ($17,325) ($39,417) ($64,569) ($93,137) ($125,517) ($162,148) ($203,515) ($250,158)

Net Profit after Tax $40,425 $91,973 $150,660 $217,319 $292,872 $378,345 $474,869 $583,701

Add: Depreciation $206,250 $206,250 $206,250 $206,250 $206,250 $206,250 $206,250 $206,250

Annual After-Tax Cash Flow $246,675 $298,223 $356,910 $423,569 $499,122 $584,595 $681,119 $789,951

Salvage Value $100,000

Net Annual Cash Flow ($1,650,000) $246,675 $298,223 $356,910 $423,569 $499,122 $584,595 $681,119 $889,951

Cumulative Cash Flow ($1,650,000) ($1,403,325) ($1,105,102) ($748,192) ($324,624) $174,499 $759,094 $1,440,213 $2,330,164

Payback Period

Required Rate of Return 16% 16% 16% 16% 16% 16% 16% 16% 16%

Discounted Cash Flow ($1,650,000) $212,651 $221,628 $228,657 $233,933 $237,639 $239,942 $241,000 $271,458

Cumulative Discounted Cash Flow ($1,650,000) ($1,437,349) ($1,215,721) ($987,064) ($753,131) ($515,492) ($275,550) ($34,549) $236,908

Discounted Payback period

Net Present Value

Profitability Index

4.65

7.13

$236,908

114.36%

Period

Capital Budgeting for Base-Case:

Answer to Part A:

Requirement 1:

Particulars 0 1 2 3 4 5 6 7 8

Initial Investment ($1,650,000)

Annual Cash Flow:

Incremental Revene $1,445,000 $1,589,500 $1,748,450 $1,923,295 $2,115,625 $2,327,187 $2,559,906 $2,815,896

Staff Cost ($900,000) ($954,000) ($1,011,240) ($1,071,914) ($1,136,229) ($1,204,403) ($1,276,667) ($1,353,267)

Material Costs ($210,000) ($222,600) ($235,956) ($250,113) ($265,120) ($281,027) ($297,889) ($315,762)

Marketing Costs ($46,000) ($48,760) ($51,686) ($54,787) ($58,074) ($61,558) ($65,252) ($69,167)

Other Costs ($25,000) ($26,500) ($28,090) ($29,775) ($31,562) ($33,456) ($35,463) ($37,591)

Depreciation of Lab ($206,250) ($206,250) ($206,250) ($206,250) ($206,250) ($206,250) ($206,250) ($206,250)

Net Profit before Tax $57,750 $131,390 $215,228 $310,455 $418,389 $540,493 $678,385 $833,859

Less: Tax on Profit ($17,325) ($39,417) ($64,569) ($93,137) ($125,517) ($162,148) ($203,515) ($250,158)

Net Profit after Tax $40,425 $91,973 $150,660 $217,319 $292,872 $378,345 $474,869 $583,701

Add: Depreciation $206,250 $206,250 $206,250 $206,250 $206,250 $206,250 $206,250 $206,250

Annual After-Tax Cash Flow $246,675 $298,223 $356,910 $423,569 $499,122 $584,595 $681,119 $789,951

Salvage Value $100,000

Net Annual Cash Flow ($1,650,000) $246,675 $298,223 $356,910 $423,569 $499,122 $584,595 $681,119 $889,951

Cumulative Cash Flow ($1,650,000) ($1,403,325) ($1,105,102) ($748,192) ($324,624) $174,499 $759,094 $1,440,213 $2,330,164

Payback Period

Required Rate of Return 16% 16% 16% 16% 16% 16% 16% 16% 16%

Discounted Cash Flow ($1,650,000) $212,651 $221,628 $228,657 $233,933 $237,639 $239,942 $241,000 $271,458

Cumulative Discounted Cash Flow ($1,650,000) ($1,437,349) ($1,215,721) ($987,064) ($753,131) ($515,492) ($275,550) ($34,549) $236,908

Discounted Payback period

Net Present Value

Profitability Index

4.65

7.13

$236,908

114.36%

Period

Capital Budgeting for Base-Case:

2ACCOUNTING AND FINANCE

Particulars 0 1 2 3 4 5 6 7 8

Initial Investment ($1,650,000)

Annual Cash Flow:

Incremental Revene $1,445,000 $1,531,700 $1,623,602 $1,721,018 $1,824,279 $1,933,736 $2,049,760 $2,172,746

Staff Cost ($900,000) ($990,000) ($1,089,000) ($1,197,900) ($1,317,690) ($1,449,459) ($1,594,405) ($1,753,845)

Material Costs ($210,000) ($231,000) ($254,100) ($279,510) ($307,461) ($338,207) ($372,028) ($409,231)

Marketing Costs ($46,000) ($50,600) ($55,660) ($61,226) ($67,349) ($74,083) ($81,492) ($89,641)

Other Costs ($25,000) ($27,500) ($30,250) ($33,275) ($36,603) ($40,263) ($44,289) ($48,718)

Depreciation of Lab ($206,250) ($206,250) ($206,250) ($206,250) ($206,250) ($206,250) ($206,250) ($206,250)

Net Profit before Tax $57,750 $26,350 ($11,658) ($57,143) ($111,073) ($174,526) ($248,703) ($334,939)

Less: Tax on Profit ($17,325) ($7,905) $3,497 $17,143 $33,322 $52,358 $74,611 $100,482

Net Profit after Tax $40,425 $18,445 ($8,161) ($40,000) ($77,751) ($122,168) ($174,092) ($234,457)

Add: Depreciation $206,250 $206,250 $206,250 $206,250 $206,250 $206,250 $206,250 $206,250

Annual After-Tax Cash Flow $246,675 $224,695 $198,089 $166,250 $128,499 $84,082 $32,158 ($28,207)

Salvage Value $100,000

Net Annual Cash Flow ($1,650,000) $246,675 $224,695 $198,089 $166,250 $128,499 $84,082 $32,158 $71,793

Cumulative Cash Flow ($1,650,000) ($1,403,325) ($1,178,630) ($980,541) ($814,291) ($685,792) ($601,710) ($569,552) ($497,760)

Payback Period

Required Rate of Return 16% 16% 16% 16% 16% 16% 16% 16% 16%

Discounted Cash Flow ($1,650,000) $212,651 $166,985 $126,907 $91,818 $61,180 $34,511 $11,378 $21,899

Cumulative Discounted Cash Flow ($1,650,000) ($1,437,349) ($1,270,364) ($1,143,457) ($1,051,638) ($990,458) ($955,948) ($944,569) ($922,671)

Discounted Payback period

Net Present Value

Profitability Index

Capital Budgeting for Worst-Case:

Period

10.34

50.13

($922,671)

44.08%

Particulars 0 1 2 3 4 5 6 7 8

Initial Investment ($1,650,000)

Annual Cash Flow:

Incremental Revene $1,445,000 $1,531,700 $1,623,602 $1,721,018 $1,824,279 $1,933,736 $2,049,760 $2,172,746

Staff Cost ($900,000) ($990,000) ($1,089,000) ($1,197,900) ($1,317,690) ($1,449,459) ($1,594,405) ($1,753,845)

Material Costs ($210,000) ($231,000) ($254,100) ($279,510) ($307,461) ($338,207) ($372,028) ($409,231)

Marketing Costs ($46,000) ($50,600) ($55,660) ($61,226) ($67,349) ($74,083) ($81,492) ($89,641)

Other Costs ($25,000) ($27,500) ($30,250) ($33,275) ($36,603) ($40,263) ($44,289) ($48,718)

Depreciation of Lab ($206,250) ($206,250) ($206,250) ($206,250) ($206,250) ($206,250) ($206,250) ($206,250)

Net Profit before Tax $57,750 $26,350 ($11,658) ($57,143) ($111,073) ($174,526) ($248,703) ($334,939)

Less: Tax on Profit ($17,325) ($7,905) $3,497 $17,143 $33,322 $52,358 $74,611 $100,482

Net Profit after Tax $40,425 $18,445 ($8,161) ($40,000) ($77,751) ($122,168) ($174,092) ($234,457)

Add: Depreciation $206,250 $206,250 $206,250 $206,250 $206,250 $206,250 $206,250 $206,250

Annual After-Tax Cash Flow $246,675 $224,695 $198,089 $166,250 $128,499 $84,082 $32,158 ($28,207)

Salvage Value $100,000

Net Annual Cash Flow ($1,650,000) $246,675 $224,695 $198,089 $166,250 $128,499 $84,082 $32,158 $71,793

Cumulative Cash Flow ($1,650,000) ($1,403,325) ($1,178,630) ($980,541) ($814,291) ($685,792) ($601,710) ($569,552) ($497,760)

Payback Period

Required Rate of Return 16% 16% 16% 16% 16% 16% 16% 16% 16%

Discounted Cash Flow ($1,650,000) $212,651 $166,985 $126,907 $91,818 $61,180 $34,511 $11,378 $21,899

Cumulative Discounted Cash Flow ($1,650,000) ($1,437,349) ($1,270,364) ($1,143,457) ($1,051,638) ($990,458) ($955,948) ($944,569) ($922,671)

Discounted Payback period

Net Present Value

Profitability Index

Capital Budgeting for Worst-Case:

Period

10.34

50.13

($922,671)

44.08%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTING AND FINANCE

Particulars 0 1 2 3 4 5 6 7 8

Initial Investment ($1,650,000)

Annual Cash Flow:

Incremental Revene $1,445,000 $1,661,750 $1,911,013 $2,197,664 $2,527,314 $2,906,411 $3,342,373 $3,843,729

Staff Cost ($900,000) ($927,000) ($954,810) ($983,454) ($1,012,958) ($1,043,347) ($1,074,647) ($1,106,886)

Material Costs ($210,000) ($216,300) ($222,789) ($229,473) ($236,357) ($243,448) ($250,751) ($258,274)

Marketing Costs ($46,000) ($47,380) ($48,801) ($50,265) ($51,773) ($53,327) ($54,926) ($56,574)

Other Costs ($25,000) ($25,750) ($26,523) ($27,318) ($28,138) ($28,982) ($29,851) ($30,747)

Depreciation of Lab ($206,250) ($206,250) ($206,250) ($206,250) ($206,250) ($206,250) ($206,250) ($206,250)

Net Profit before Tax $57,750 $239,070 $451,840 $700,904 $991,838 $1,331,058 $1,725,947 $2,184,998

Less: Tax on Profit ($17,325) ($71,721) ($135,552) ($210,271) ($297,551) ($399,318) ($517,784) ($655,499)

Net Profit after Tax $40,425 $167,349 $316,288 $490,633 $694,287 $931,741 $1,208,163 $1,529,498

Add: Depreciation $206,250 $206,250 $206,250 $206,250 $206,250 $206,250 $206,250 $206,250

Annual After-Tax Cash Flow $246,675 $373,599 $522,538 $696,883 $900,537 $1,137,991 $1,414,413 $1,735,748

Salvage Value $100,000

Net Annual Cash Flow ($1,650,000) $246,675 $373,599 $522,538 $696,883 $900,537 $1,137,991 $1,414,413 $1,835,748

Cumulative Cash Flow ($1,650,000) ($1,403,325) ($1,029,726) ($507,188) $189,694 $1,090,231 $2,228,222 $3,642,635 $5,478,383

Payback Period

Required Rate of Return 16% 16% 16% 16% 16% 16% 16% 16% 16%

Discounted Cash Flow ($1,650,000) $212,651 $277,645 $334,768 $384,882 $428,757 $467,080 $500,461 $559,950

Cumulative Discounted Cash Flow ($1,650,000) ($1,437,349) ($1,159,704) ($824,936) ($440,054) ($11,297) $455,782 $956,244 $1,516,194

Discounted Payback period

Net Present Value

Profitability Index

Capital Budgeting for Best-Case:

Period

3.79

5.29

$1,516,194

191.89%

Requirement 2:

It is clear from the table shown above the net value at present methods have been utilised

for determining the future cash flow of the project. The approaches of capital budgeting involve

several techniques for the case projection. Payback periods and average rates of return are the

methods used for the estimation of project risks.

Requirement 3:

It is clear from the above table that the net value at present is positive and 191.89% is the

profitability index of the project. A positive value of the project is an indication that the project is

viable and investments can be undertaken. The profitability index helps in the measurement of

Particulars 0 1 2 3 4 5 6 7 8

Initial Investment ($1,650,000)

Annual Cash Flow:

Incremental Revene $1,445,000 $1,661,750 $1,911,013 $2,197,664 $2,527,314 $2,906,411 $3,342,373 $3,843,729

Staff Cost ($900,000) ($927,000) ($954,810) ($983,454) ($1,012,958) ($1,043,347) ($1,074,647) ($1,106,886)

Material Costs ($210,000) ($216,300) ($222,789) ($229,473) ($236,357) ($243,448) ($250,751) ($258,274)

Marketing Costs ($46,000) ($47,380) ($48,801) ($50,265) ($51,773) ($53,327) ($54,926) ($56,574)

Other Costs ($25,000) ($25,750) ($26,523) ($27,318) ($28,138) ($28,982) ($29,851) ($30,747)

Depreciation of Lab ($206,250) ($206,250) ($206,250) ($206,250) ($206,250) ($206,250) ($206,250) ($206,250)

Net Profit before Tax $57,750 $239,070 $451,840 $700,904 $991,838 $1,331,058 $1,725,947 $2,184,998

Less: Tax on Profit ($17,325) ($71,721) ($135,552) ($210,271) ($297,551) ($399,318) ($517,784) ($655,499)

Net Profit after Tax $40,425 $167,349 $316,288 $490,633 $694,287 $931,741 $1,208,163 $1,529,498

Add: Depreciation $206,250 $206,250 $206,250 $206,250 $206,250 $206,250 $206,250 $206,250

Annual After-Tax Cash Flow $246,675 $373,599 $522,538 $696,883 $900,537 $1,137,991 $1,414,413 $1,735,748

Salvage Value $100,000

Net Annual Cash Flow ($1,650,000) $246,675 $373,599 $522,538 $696,883 $900,537 $1,137,991 $1,414,413 $1,835,748

Cumulative Cash Flow ($1,650,000) ($1,403,325) ($1,029,726) ($507,188) $189,694 $1,090,231 $2,228,222 $3,642,635 $5,478,383

Payback Period

Required Rate of Return 16% 16% 16% 16% 16% 16% 16% 16% 16%

Discounted Cash Flow ($1,650,000) $212,651 $277,645 $334,768 $384,882 $428,757 $467,080 $500,461 $559,950

Cumulative Discounted Cash Flow ($1,650,000) ($1,437,349) ($1,159,704) ($824,936) ($440,054) ($11,297) $455,782 $956,244 $1,516,194

Discounted Payback period

Net Present Value

Profitability Index

Capital Budgeting for Best-Case:

Period

3.79

5.29

$1,516,194

191.89%

Requirement 2:

It is clear from the table shown above the net value at present methods have been utilised

for determining the future cash flow of the project. The approaches of capital budgeting involve

several techniques for the case projection. Payback periods and average rates of return are the

methods used for the estimation of project risks.

Requirement 3:

It is clear from the above table that the net value at present is positive and 191.89% is the

profitability index of the project. A positive value of the project is an indication that the project is

viable and investments can be undertaken. The profitability index helps in the measurement of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTING AND FINANCE

the cost benefit ratio. A value of 191.89% explains that the value of the cash flow at present is

more than the previous investment amount. Information related to the acceptance and refusal of

projects can be created by capital budgeting techniques (Hasan, 2013).

Answer to part B:

Introduction:

The report helps to understand the capital structure of the APN outdoor group which is

mentioned in the Australian Stock Exchange. The discussed report explains the weighted average

calculation as well as the major analysis of organisational fiscal ratios.

Analysis of the capital structure of APN group:

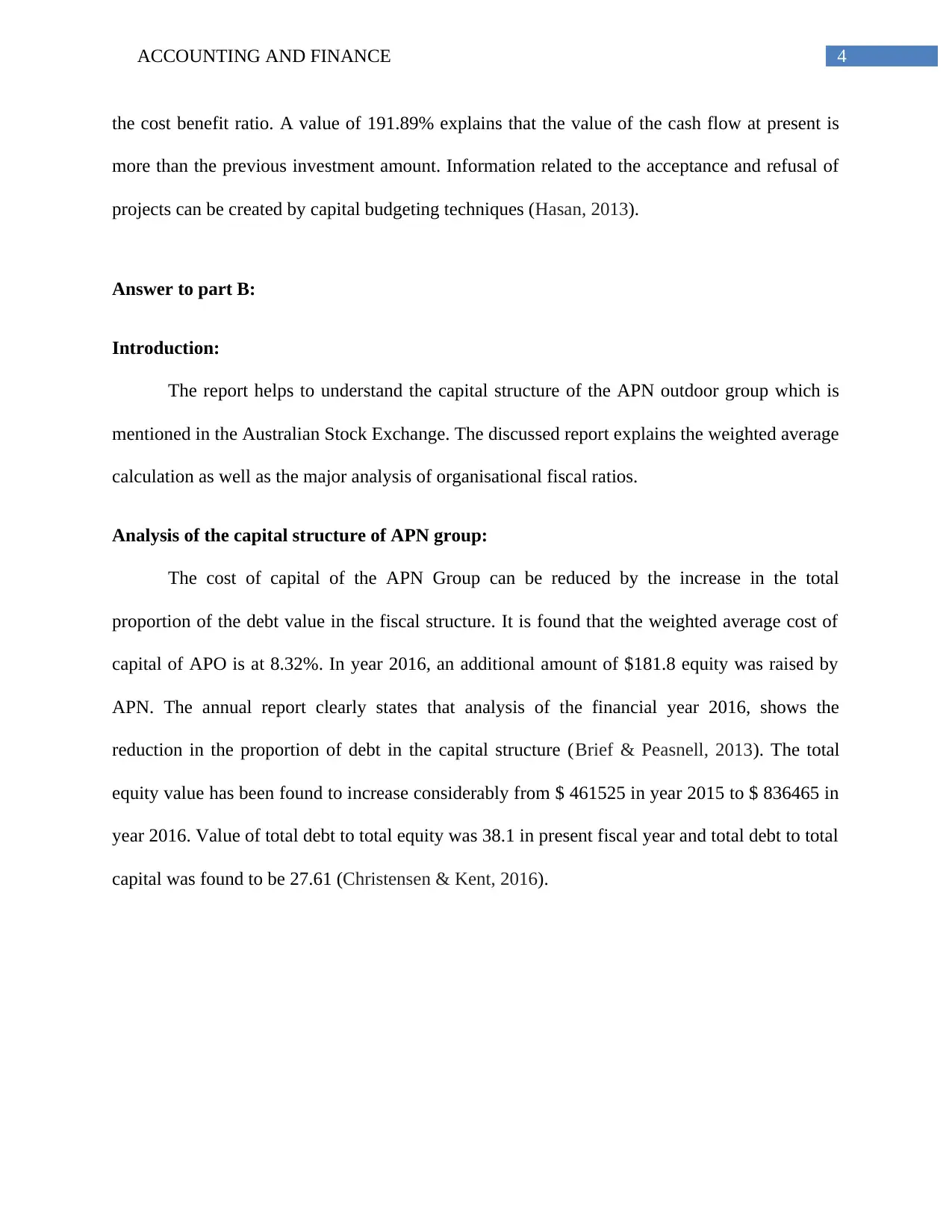

The cost of capital of the APN Group can be reduced by the increase in the total

proportion of the debt value in the fiscal structure. It is found that the weighted average cost of

capital of APO is at 8.32%. In year 2016, an additional amount of $181.8 equity was raised by

APN. The annual report clearly states that analysis of the financial year 2016, shows the

reduction in the proportion of debt in the capital structure (Brief & Peasnell, 2013). The total

equity value has been found to increase considerably from $ 461525 in year 2015 to $ 836465 in

year 2016. Value of total debt to total equity was 38.1 in present fiscal year and total debt to total

capital was found to be 27.61 (Christensen & Kent, 2016).

the cost benefit ratio. A value of 191.89% explains that the value of the cash flow at present is

more than the previous investment amount. Information related to the acceptance and refusal of

projects can be created by capital budgeting techniques (Hasan, 2013).

Answer to part B:

Introduction:

The report helps to understand the capital structure of the APN outdoor group which is

mentioned in the Australian Stock Exchange. The discussed report explains the weighted average

calculation as well as the major analysis of organisational fiscal ratios.

Analysis of the capital structure of APN group:

The cost of capital of the APN Group can be reduced by the increase in the total

proportion of the debt value in the fiscal structure. It is found that the weighted average cost of

capital of APO is at 8.32%. In year 2016, an additional amount of $181.8 equity was raised by

APN. The annual report clearly states that analysis of the financial year 2016, shows the

reduction in the proportion of debt in the capital structure (Brief & Peasnell, 2013). The total

equity value has been found to increase considerably from $ 461525 in year 2015 to $ 836465 in

year 2016. Value of total debt to total equity was 38.1 in present fiscal year and total debt to total

capital was found to be 27.61 (Christensen & Kent, 2016).

5ACCOUNTING AND FINANCE

Computation of After-Tax WACC:

Particulars Amount Weightage Return Rate

Weighted

Return

Total Equity Capital $836,465 83.83% 8.38% 7.03%

Total Debt Capital $161,309 16.17% 11.42% 1.85%

Tax Rate 30%

After-Tax Weighted Average Cost

of Capital 8.32%

Computation of After-Tax Weighted Avergae Cost of Capital:

Fiscal ratio analysis of APN:

The analysis of the liquidity position of the organisations is performed by viewing the

figures of the present ratios, cash ratios as well as quick ratios. Cash ratio of APN was found to

be 0.38, current ratio as 1.90 and quick ratio as 1.89. Organisational ratio of interest coverage is

obtained as 25.96 and 0.23 is found to be the long-term debt to total assets (Andor, Mohanty &

Toth, 2015).

It can be clearly stated that the net operational flow of cash in the companies has reduced

significantly in the last three fiscal years. The earnings per share of the group was 19% below

target. This is believed to be because of strategic activities and in the present year, the value

stood at 0.29. A significant decline in earnings per share was noticed from 44.4 in year 2015 to

31.4 in year 2016. Price earnings ratio for year 2017 stood at 16.92.

Competitor performance of APN group:

The APN group has Ooh Media as one of its competitors. The equity capital value

increased including the organisational borrowings. This the group has both debt as well as equity

Computation of After-Tax WACC:

Particulars Amount Weightage Return Rate

Weighted

Return

Total Equity Capital $836,465 83.83% 8.38% 7.03%

Total Debt Capital $161,309 16.17% 11.42% 1.85%

Tax Rate 30%

After-Tax Weighted Average Cost

of Capital 8.32%

Computation of After-Tax Weighted Avergae Cost of Capital:

Fiscal ratio analysis of APN:

The analysis of the liquidity position of the organisations is performed by viewing the

figures of the present ratios, cash ratios as well as quick ratios. Cash ratio of APN was found to

be 0.38, current ratio as 1.90 and quick ratio as 1.89. Organisational ratio of interest coverage is

obtained as 25.96 and 0.23 is found to be the long-term debt to total assets (Andor, Mohanty &

Toth, 2015).

It can be clearly stated that the net operational flow of cash in the companies has reduced

significantly in the last three fiscal years. The earnings per share of the group was 19% below

target. This is believed to be because of strategic activities and in the present year, the value

stood at 0.29. A significant decline in earnings per share was noticed from 44.4 in year 2015 to

31.4 in year 2016. Price earnings ratio for year 2017 stood at 16.92.

Competitor performance of APN group:

The APN group has Ooh Media as one of its competitors. The equity capital value

increased including the organisational borrowings. This the group has both debt as well as equity

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTING AND FINANCE

in the capital structure. Despite this the dependency on the equity is comparatively more

(Gerrans, Faff & Hartnett, 2015).

The APN group has felt a strong flow of cash helping in the funding of the investment

activities. However the capitalistic nature of both the organisations is similar (Hise & Strawser,

2013).

The APN Outdoor Group Structure of Capital:

Basically the cost of the capital is the rate of the return that is expected by the

organisation on the capital. This is for the purpose of earning a substitute investment value with

an equivalent amount of the risk. The organisational structure of capital includes the

amalgamation of the debts with the equity for the reason of the financing of the assets. T he

weighted average cost of the capital is influenced significantly by the fiscal decisions of the

company and the changes in the capital structure influences the weighted average cost. It must

also be considered that the rise or fall of the weighted cost of the capital is directly proportional.

It is crucial for an organisation to reduce the capital cost in order to increase the market

value. An important method for the reduction is the restricting of the capital as well as the cost of

the capital as well. The funding will get cheaper as the lost of the capital gets lower. The

financial cost can also be reduced by opening the line of credit. Bank loans, bonds and credit

card debts include some of the common natures of bank loans.

Conclusion:

It can be understood from the analysis and explanation discussed above that the fiscal

structure of the APN group includes both debentures as well as equity. The revenues as well as

in the capital structure. Despite this the dependency on the equity is comparatively more

(Gerrans, Faff & Hartnett, 2015).

The APN group has felt a strong flow of cash helping in the funding of the investment

activities. However the capitalistic nature of both the organisations is similar (Hise & Strawser,

2013).

The APN Outdoor Group Structure of Capital:

Basically the cost of the capital is the rate of the return that is expected by the

organisation on the capital. This is for the purpose of earning a substitute investment value with

an equivalent amount of the risk. The organisational structure of capital includes the

amalgamation of the debts with the equity for the reason of the financing of the assets. T he

weighted average cost of the capital is influenced significantly by the fiscal decisions of the

company and the changes in the capital structure influences the weighted average cost. It must

also be considered that the rise or fall of the weighted cost of the capital is directly proportional.

It is crucial for an organisation to reduce the capital cost in order to increase the market

value. An important method for the reduction is the restricting of the capital as well as the cost of

the capital as well. The funding will get cheaper as the lost of the capital gets lower. The

financial cost can also be reduced by opening the line of credit. Bank loans, bonds and credit

card debts include some of the common natures of bank loans.

Conclusion:

It can be understood from the analysis and explanation discussed above that the fiscal

structure of the APN group includes both debentures as well as equity. The revenues as well as

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING AND FINANCE

the earnings before the interest have experienced a trend of an upward nature. This has also been

experienced by organisational taxes that assist in the generation of the satisfactory returns to the

shareholders. Satisfactory returns have been provided to the shareholders and also in the payment

of dividends to them.

the earnings before the interest have experienced a trend of an upward nature. This has also been

experienced by organisational taxes that assist in the generation of the satisfactory returns to the

shareholders. Satisfactory returns have been provided to the shareholders and also in the payment

of dividends to them.

8ACCOUNTING AND FINANCE

References:

Andor, G., Mohanty, S. K., & Toth, T. (2015). Capital budgeting practices: A survey of Central

and Eastern European firms. Emerging Markets Review, 23, 148-172.

Brief, R. P., & Peasnell, K. V. (Eds.). (2013). Clean surplus: A link between accounting and

finance. Routledge.

Christensen, J., & Kent, P. (2016). The decision to outsource risk management

services. Accounting & Finance, 56(4), 985-1015.

Gerrans, P., Faff, R., & Hartnett, N. (2015). Individual financial risk tolerance and the global

financial crisis. Accounting & Finance, 55(1), 165-185.

Hasan, M. (2013). Capital budgeting techniques used by small manufacturing

companies. Journal of Service Science and Management, 6(01), 38.

Hise, R. T., & Strawser, R. H. (2013). Application of Capital Budgeting Techniques to

Marketing Operations. Readings in Managerial Economics: Pergamon International

Library of Science, Technology, Engineering and Social Studies, 419.

References:

Andor, G., Mohanty, S. K., & Toth, T. (2015). Capital budgeting practices: A survey of Central

and Eastern European firms. Emerging Markets Review, 23, 148-172.

Brief, R. P., & Peasnell, K. V. (Eds.). (2013). Clean surplus: A link between accounting and

finance. Routledge.

Christensen, J., & Kent, P. (2016). The decision to outsource risk management

services. Accounting & Finance, 56(4), 985-1015.

Gerrans, P., Faff, R., & Hartnett, N. (2015). Individual financial risk tolerance and the global

financial crisis. Accounting & Finance, 55(1), 165-185.

Hasan, M. (2013). Capital budgeting techniques used by small manufacturing

companies. Journal of Service Science and Management, 6(01), 38.

Hise, R. T., & Strawser, R. H. (2013). Application of Capital Budgeting Techniques to

Marketing Operations. Readings in Managerial Economics: Pergamon International

Library of Science, Technology, Engineering and Social Studies, 419.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.