Accounting Assignment: Financial Records, Statements, and Analysis

VerifiedAdded on 2022/10/04

ACCOUNTING

Paraphrase This Document

Table of Contents

Question 1: Origin of Accounting...............................................................................................................3

Question 2: Ethical Principles.....................................................................................................................5

List and explain each of the ethical principles in the code of ethics........................................................5

Principle of objectivity........................................................................................................................5

Principle of integrity............................................................................................................................5

Principle of confidentiality..................................................................................................................5

Principle of professional behavior.......................................................................................................5

Principles of due care and diligence....................................................................................................6

What should accountants do?..................................................................................................................6

References...................................................................................................................................................8

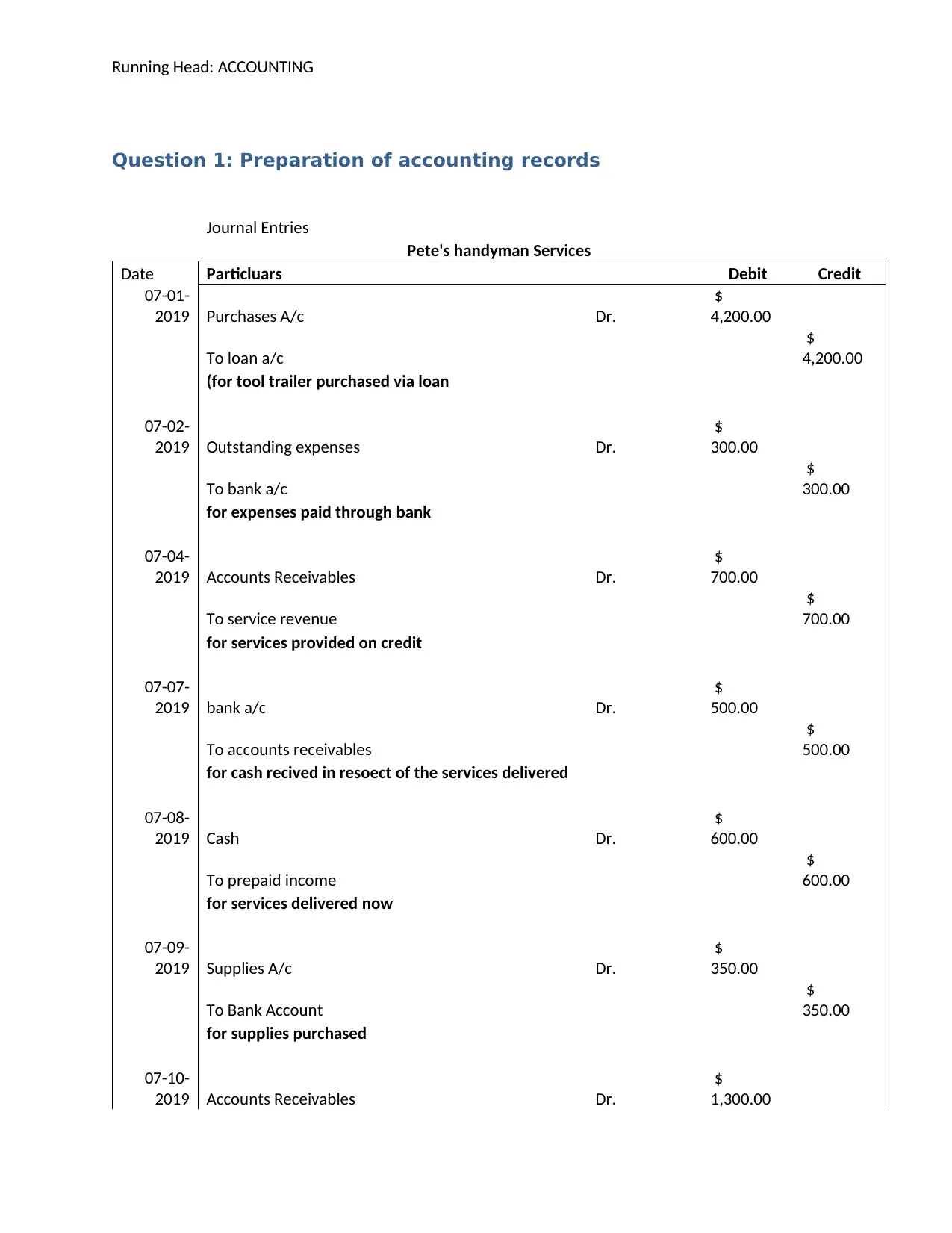

Question 1: Preparation of accounting records

Journal Entries

Pete's handyman Services

Date Particluars Debit Credit

07-01-

2019 Purchases A/c Dr.

$

4,200.00

To loan a/c

$

4,200.00

(for tool trailer purchased via loan

07-02-

2019 Outstanding expenses Dr.

$

300.00

To bank a/c

$

300.00

for expenses paid through bank

07-04-

2019 Accounts Receivables Dr.

$

700.00

To service revenue

$

700.00

for services provided on credit

07-07-

2019 bank a/c Dr.

$

500.00

To accounts receivables

$

500.00

for cash recived in resoect of the services delivered

07-08-

2019 Cash Dr.

$

600.00

To prepaid income

$

600.00

for services delivered now

07-09-

2019 Supplies A/c Dr.

$

350.00

To Bank Account

$

350.00

for supplies purchased

07-10-

2019 Accounts Receivables Dr.

$

1,300.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

To service revenue

$

1,300.00

for services provided on credit

07-12-

2019 Drawings A/c Dr.

$

2,500.00

To cash a/c

$

2,500.00

for cash withdrawn for personal use

14/7/19 Bank A/c Dr.

$

1,250.00

to service revenue

$

1,250.00

For services provided and payment receieved

15/7/19 Fuel expenses Dr.

$

80.00

To bank A/c

$

80.00

(for cash paid for the fuel)

16/7/19 Bank A/c Dr.

$

1,300.00

To Accounts Receivables

$

1,300.00

for cash received from Mrs. Budd

22/7/19 Accounts receivables Dr.

$

500.00

To service revenue

$

500.00

for sales made on credit

23/7/19 Service revenue Dr.

$

2,600.00

To unearned revenue

$

2,600.00

for prepaid income received

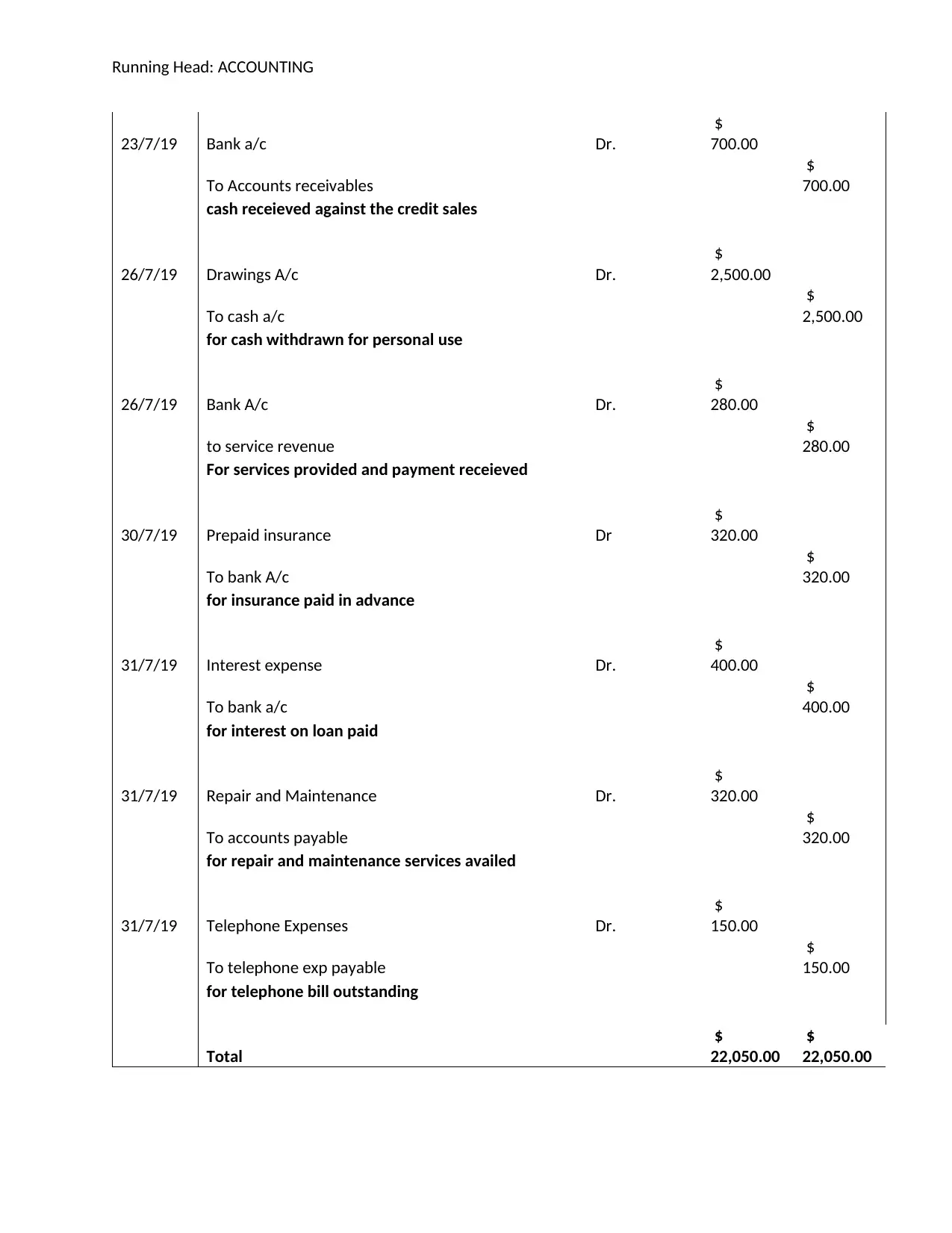

23/7/19 Advertising A/c Dr.

$

1,200.00

To Bank A/c

$

1,200.00

(for advertising charges paid thorugh bank account)

Paraphrase This Document

23/7/19 Bank a/c Dr.

$

700.00

To Accounts receivables

$

700.00

cash receieved against the credit sales

26/7/19 Drawings A/c Dr.

$

2,500.00

To cash a/c

$

2,500.00

for cash withdrawn for personal use

26/7/19 Bank A/c Dr.

$

280.00

to service revenue

$

280.00

For services provided and payment receieved

30/7/19 Prepaid insurance Dr

$

320.00

To bank A/c

$

320.00

for insurance paid in advance

31/7/19 Interest expense Dr.

$

400.00

To bank a/c

$

400.00

for interest on loan paid

31/7/19 Repair and Maintenance Dr.

$

320.00

To accounts payable

$

320.00

for repair and maintenance services availed

31/7/19 Telephone Expenses Dr.

$

150.00

To telephone exp payable

$

150.00

for telephone bill outstanding

Total

$

22,050.00

$

22,050.00

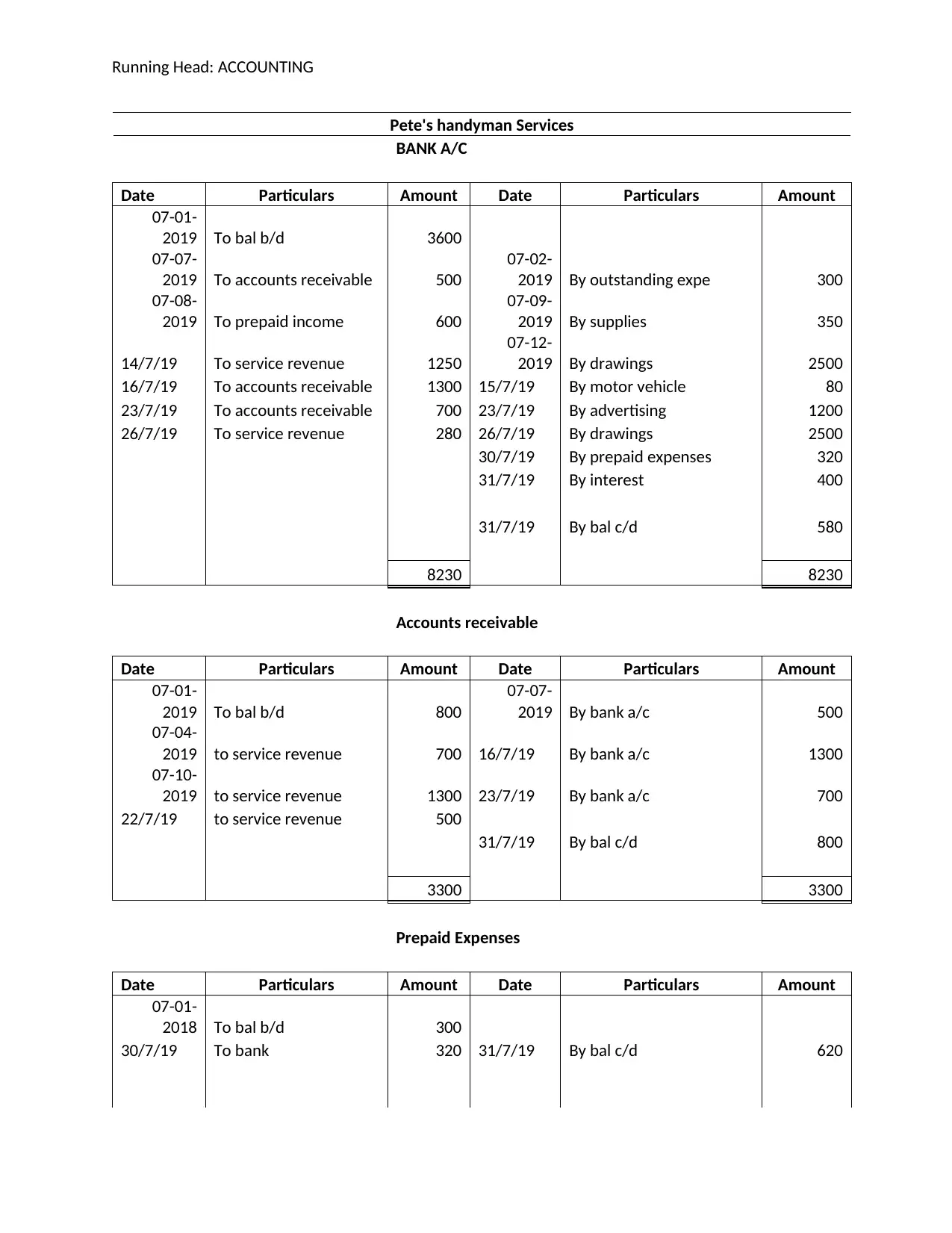

Ledger Accounts

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Pete's handyman Services

BANK A/C

Date Particulars Amount Date Particulars Amount

07-01-

2019 To bal b/d 3600

07-07-

2019 To accounts receivable 500

07-02-

2019 By outstanding expe 300

07-08-

2019 To prepaid income 600

07-09-

2019 By supplies 350

14/7/19 To service revenue 1250

07-12-

2019 By drawings 2500

16/7/19 To accounts receivable 1300 15/7/19 By motor vehicle 80

23/7/19 To accounts receivable 700 23/7/19 By advertising 1200

26/7/19 To service revenue 280 26/7/19 By drawings 2500

30/7/19 By prepaid expenses 320

31/7/19 By interest 400

31/7/19 By bal c/d 580

8230 8230

Accounts receivable

Date Particulars Amount Date Particulars Amount

07-01-

2019 To bal b/d 800

07-07-

2019 By bank a/c 500

07-04-

2019 to service revenue 700 16/7/19 By bank a/c 1300

07-10-

2019 to service revenue 1300 23/7/19 By bank a/c 700

22/7/19 to service revenue 500

31/7/19 By bal c/d 800

3300 3300

Prepaid Expenses

Date Particulars Amount Date Particulars Amount

07-01-

2018 To bal b/d 300

30/7/19 To bank 320 31/7/19 By bal c/d 620

Paraphrase This Document

620 620

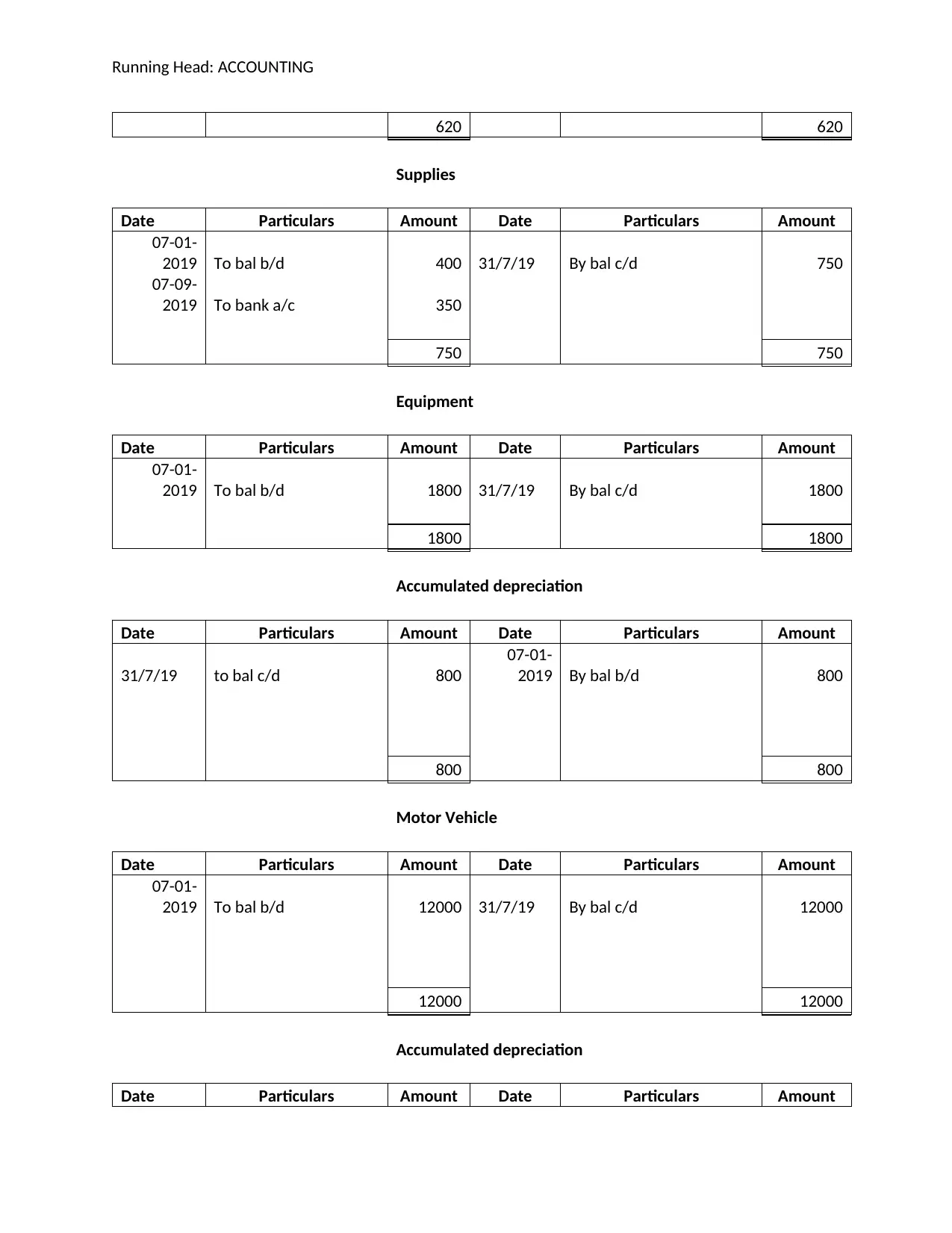

Supplies

Date Particulars Amount Date Particulars Amount

07-01-

2019 To bal b/d 400 31/7/19 By bal c/d 750

07-09-

2019 To bank a/c 350

750 750

Equipment

Date Particulars Amount Date Particulars Amount

07-01-

2019 To bal b/d 1800 31/7/19 By bal c/d 1800

1800 1800

Accumulated depreciation

Date Particulars Amount Date Particulars Amount

31/7/19 to bal c/d 800

07-01-

2019 By bal b/d 800

800 800

Motor Vehicle

Date Particulars Amount Date Particulars Amount

07-01-

2019 To bal b/d 12000 31/7/19 By bal c/d 12000

12000 12000

Accumulated depreciation

Date Particulars Amount Date Particulars Amount

31/7/19 to bal c/d 3600

07-01-

2019 By bal b/d 3600

3600 3600

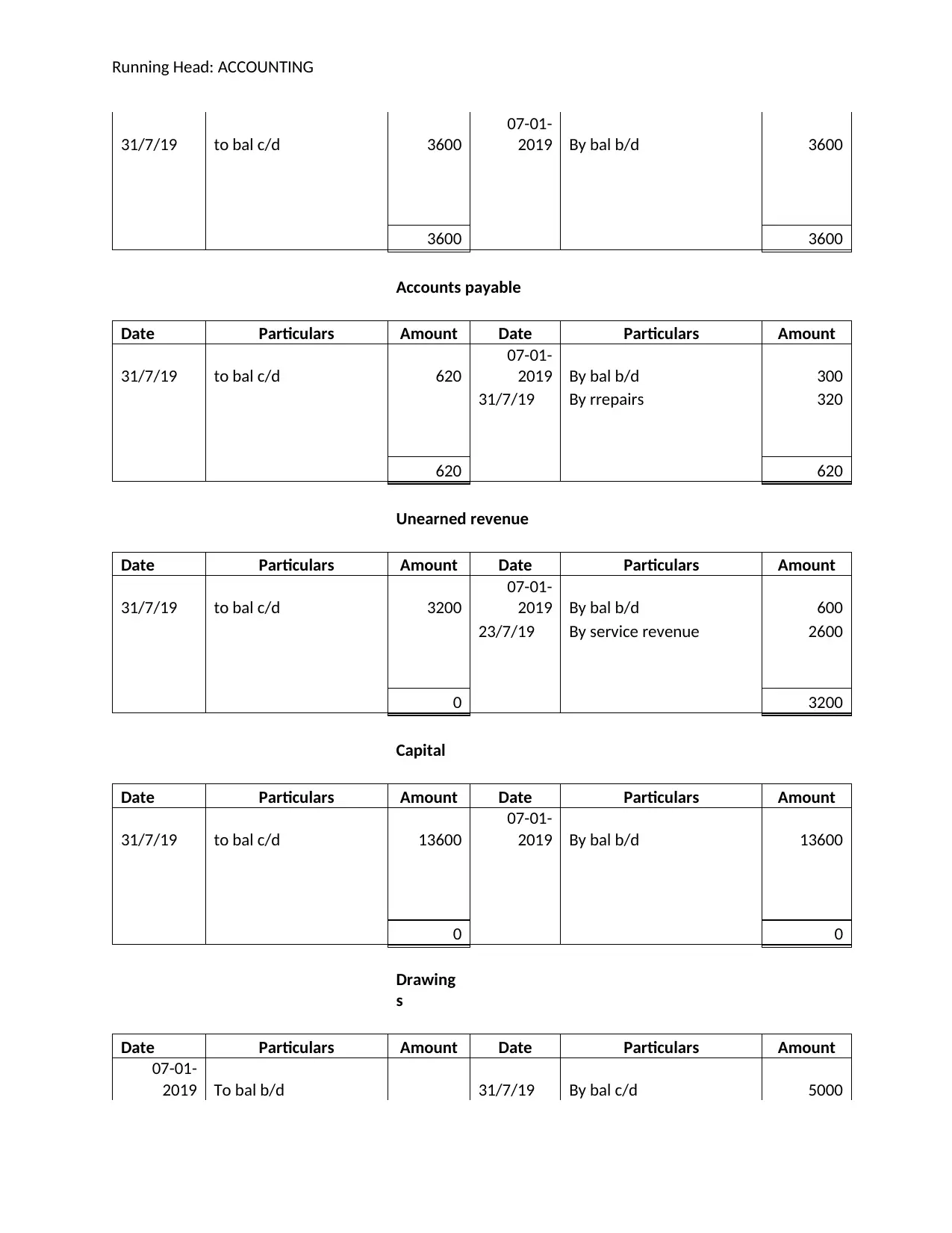

Accounts payable

Date Particulars Amount Date Particulars Amount

31/7/19 to bal c/d 620

07-01-

2019 By bal b/d 300

31/7/19 By rrepairs 320

620 620

Unearned revenue

Date Particulars Amount Date Particulars Amount

31/7/19 to bal c/d 3200

07-01-

2019 By bal b/d 600

23/7/19 By service revenue 2600

0 3200

Capital

Date Particulars Amount Date Particulars Amount

31/7/19 to bal c/d 13600

07-01-

2019 By bal b/d 13600

0 0

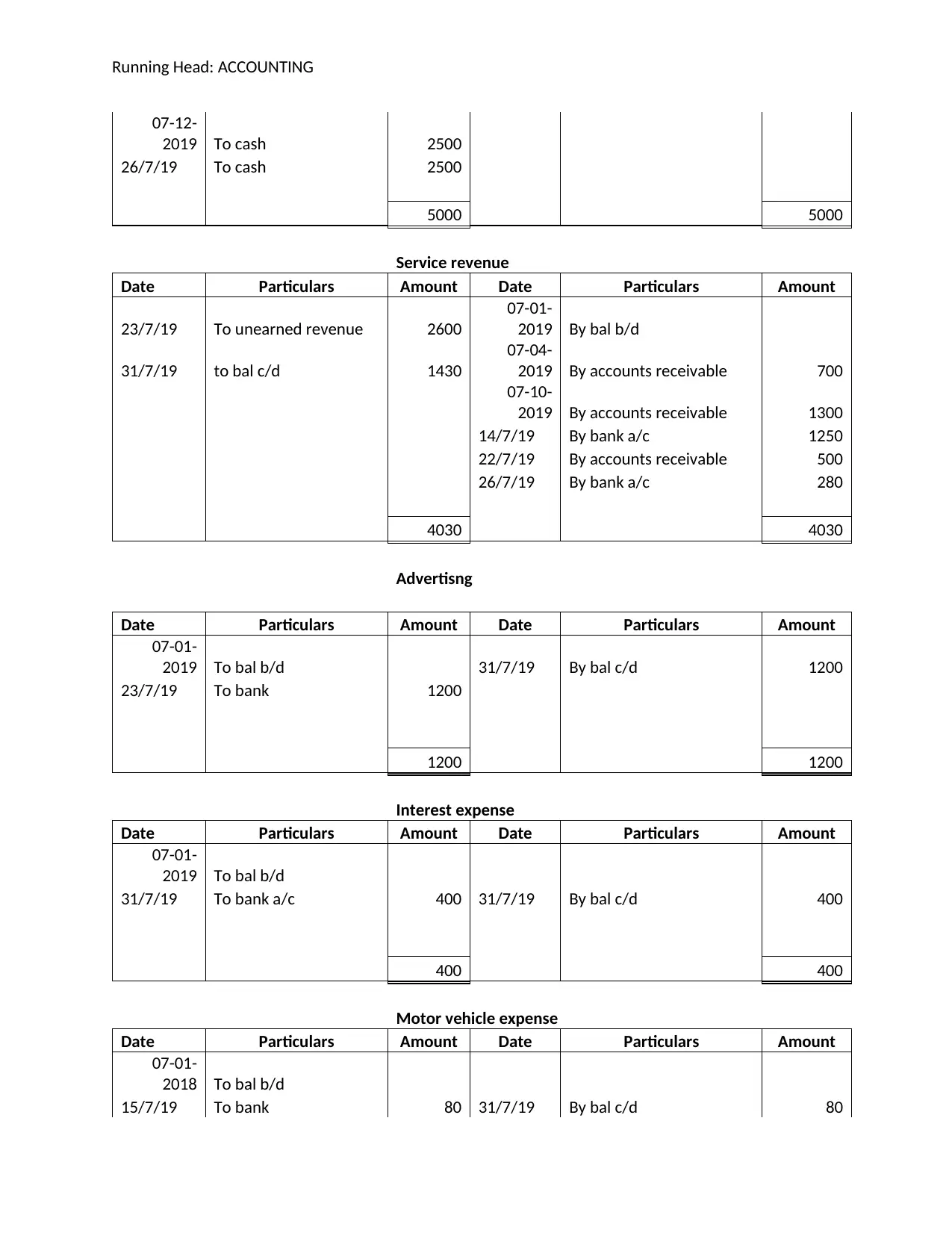

Drawing

s

Date Particulars Amount Date Particulars Amount

07-01-

2019 To bal b/d 31/7/19 By bal c/d 5000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

07-12-

2019 To cash 2500

26/7/19 To cash 2500

5000 5000

Service revenue

Date Particulars Amount Date Particulars Amount

23/7/19 To unearned revenue 2600

07-01-

2019 By bal b/d

31/7/19 to bal c/d 1430

07-04-

2019 By accounts receivable 700

07-10-

2019 By accounts receivable 1300

14/7/19 By bank a/c 1250

22/7/19 By accounts receivable 500

26/7/19 By bank a/c 280

4030 4030

Advertisng

Date Particulars Amount Date Particulars Amount

07-01-

2019 To bal b/d 31/7/19 By bal c/d 1200

23/7/19 To bank 1200

1200 1200

Interest expense

Date Particulars Amount Date Particulars Amount

07-01-

2019 To bal b/d

31/7/19 To bank a/c 400 31/7/19 By bal c/d 400

400 400

Motor vehicle expense

Date Particulars Amount Date Particulars Amount

07-01-

2018 To bal b/d

15/7/19 To bank 80 31/7/19 By bal c/d 80

Paraphrase This Document

80 80

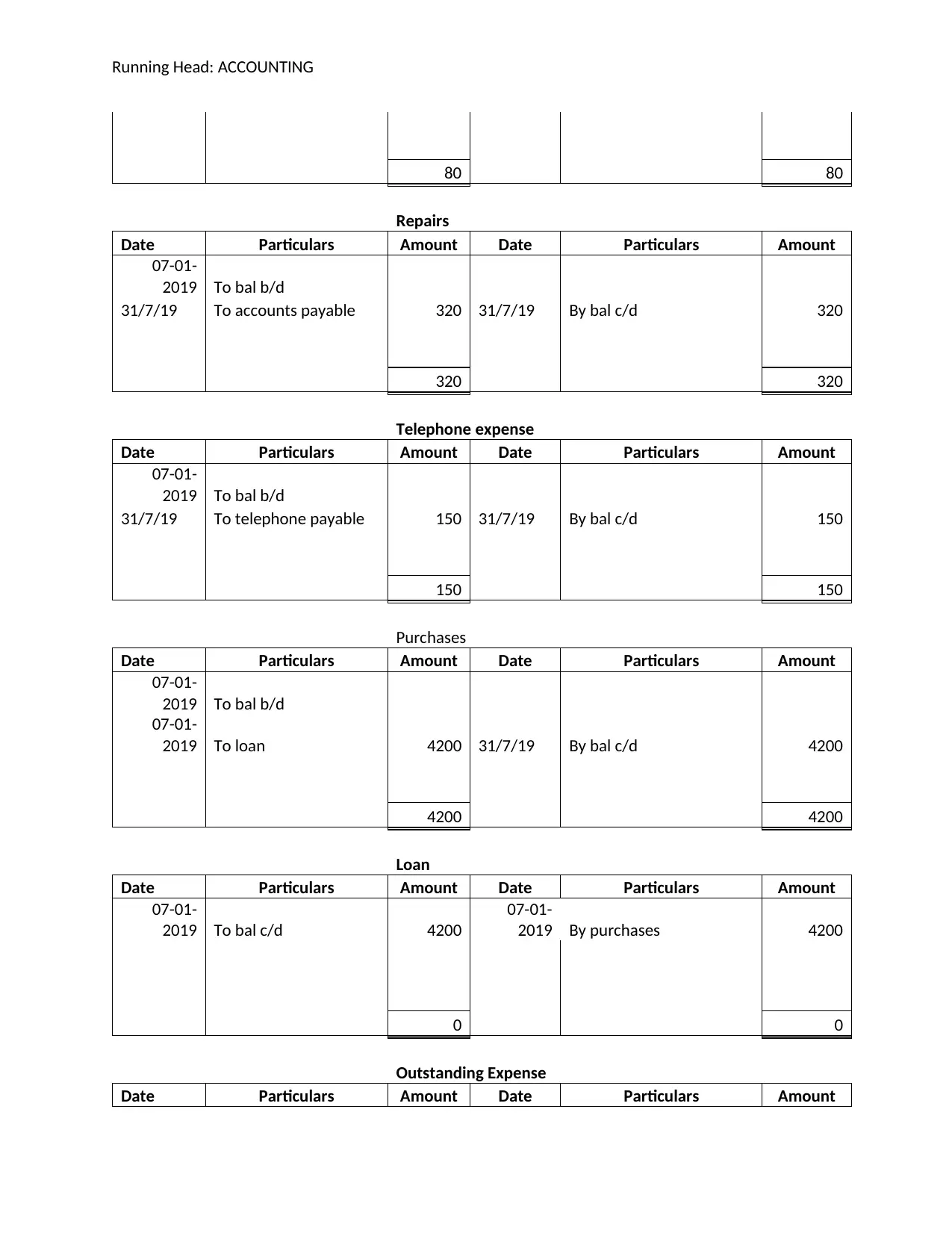

Repairs

Date Particulars Amount Date Particulars Amount

07-01-

2019 To bal b/d

31/7/19 To accounts payable 320 31/7/19 By bal c/d 320

320 320

Telephone expense

Date Particulars Amount Date Particulars Amount

07-01-

2019 To bal b/d

31/7/19 To telephone payable 150 31/7/19 By bal c/d 150

150 150

Purchases

Date Particulars Amount Date Particulars Amount

07-01-

2019 To bal b/d

07-01-

2019 To loan 4200 31/7/19 By bal c/d 4200

4200 4200

Loan

Date Particulars Amount Date Particulars Amount

07-01-

2019 To bal c/d 4200

07-01-

2019 By purchases 4200

0 0

Outstanding Expense

Date Particulars Amount Date Particulars Amount

07-02-

2019 To bank a/c 300 31/7/19 By bal c/d 300

300 300

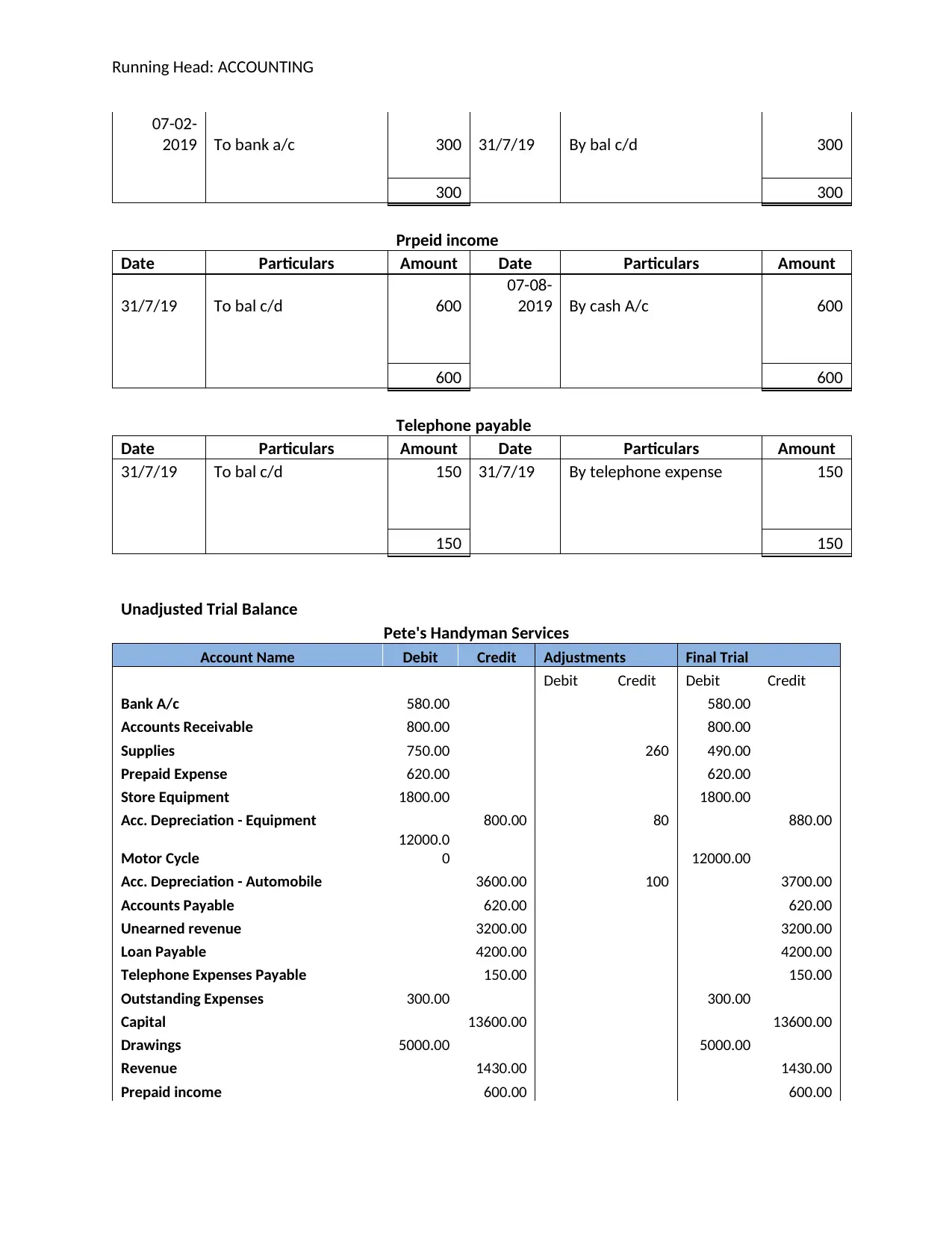

Prpeid income

Date Particulars Amount Date Particulars Amount

31/7/19 To bal c/d 600

07-08-

2019 By cash A/c 600

600 600

Telephone payable

Date Particulars Amount Date Particulars Amount

31/7/19 To bal c/d 150 31/7/19 By telephone expense 150

150 150

Unadjusted Trial Balance

Pete's Handyman Services

Account Name Debit Credit Adjustments Final Trial

Debit Credit Debit Credit

Bank A/c 580.00 580.00

Accounts Receivable 800.00 800.00

Supplies 750.00 260 490.00

Prepaid Expense 620.00 620.00

Store Equipment 1800.00 1800.00

Acc. Depreciation - Equipment 800.00 80 880.00

Motor Cycle

12000.0

0 12000.00

Acc. Depreciation - Automobile 3600.00 100 3700.00

Accounts Payable 620.00 620.00

Unearned revenue 3200.00 3200.00

Loan Payable 4200.00 4200.00

Telephone Expenses Payable 150.00 150.00

Outstanding Expenses 300.00 300.00

Capital 13600.00 13600.00

Drawings 5000.00 5000.00

Revenue 1430.00 1430.00

Prepaid income 600.00 600.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Advertising Expense 1200.00 1200.00

purchases 4200.00 4200.00

Depreciation Expense - Store

Equipment 80 80.00

Depreciation Expense - Motor Cycle 100 100.00

Repair and maintenance 320.00 320.00

Supplies Expense 260 260.00

Telephone Expenses 150.00 150.00

Fuel Expenses 80.00 80.00

Interest Expense 400.00 400.00

28200.0

0 28200.00 440.00 440.00 28380.00

28380.0

0

Pete's Handyman Services

Adjusting Jounal entires

Date Particluars Debit Credit

31/07/201

9 Depreciation

Dr

.

$

80.00

To accumulated Depreciation

$

80.00

for depreciation charged on equipment

31/07/201

9 Accumulated Depreciation

Dr

.

$

80.00

To equipment

$

80.00

for accumulated depreciation recorded

31/07/201

9 Depreciation

Dr

.

$

100.00

To accumulated Depreciation

$

100.00

for depreciation charged on vehicle

31/07/201

9 Accumulated Depreciation

Dr

.

$

100.00

To vehicle

$

100.00

for accumulated depreciation recorded

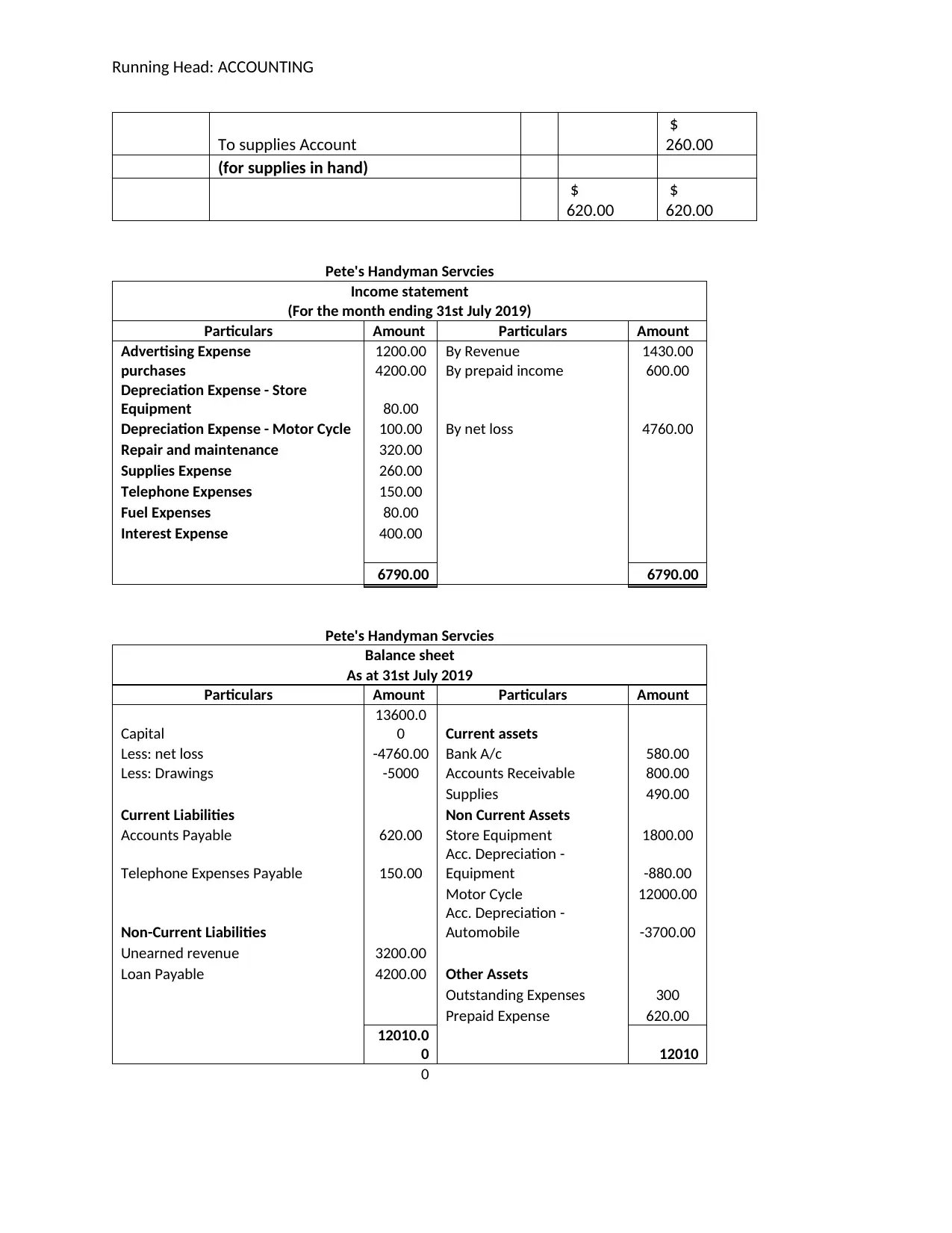

31/07/201

9 Supplies Expenses

Dr

.

$

260.00

Paraphrase This Document

To supplies Account

$

260.00

(for supplies in hand)

$

620.00

$

620.00

Pete's Handyman Servcies

Income statement

(For the month ending 31st July 2019)

Particulars Amount Particulars Amount

Advertising Expense 1200.00 By Revenue 1430.00

purchases 4200.00 By prepaid income 600.00

Depreciation Expense - Store

Equipment 80.00

Depreciation Expense - Motor Cycle 100.00 By net loss 4760.00

Repair and maintenance 320.00

Supplies Expense 260.00

Telephone Expenses 150.00

Fuel Expenses 80.00

Interest Expense 400.00

6790.00 6790.00

Pete's Handyman Servcies

Balance sheet

As at 31st July 2019

Particulars Amount Particulars Amount

Capital

13600.0

0 Current assets

Less: net loss -4760.00 Bank A/c 580.00

Less: Drawings -5000 Accounts Receivable 800.00

Supplies 490.00

Current Liabilities Non Current Assets

Accounts Payable 620.00 Store Equipment 1800.00

Telephone Expenses Payable 150.00

Acc. Depreciation -

Equipment -880.00

Motor Cycle 12000.00

Non-Current Liabilities

Acc. Depreciation -

Automobile -3700.00

Unearned revenue 3200.00

Loan Payable 4200.00 Other Assets

Outstanding Expenses 300

Prepaid Expense 620.00

12010.0

0 12010

0

Ratios

Current ratio Current Assets 1870.00 2.43

Current Liabilities 770.00

Debt Ratio Debt 4200.00 0.31

Capital

13600.0

0

Question 2: Origin of Accounting

Accounting has been circulating since the ancient times, the times of the Mesopotamia.

Early financial experts built up the training as an approach to track trades of the agriculture and

to further build up the fiscal system of the earlier stage in the efficient tool to create an altogether

a new history. Accounting has also been given credit in religious books, for example, the Islamic

book of confidence. The enhanced modern day activity of the accounting is surely unmistakably

more complex than its antiquated ancestors, however its establishment and intentions have

continued as before. The sole reason for bookkeeping is to precisely ascertain and track financial

trades. The term accounting has travelled from Egypt and Babylon to India as well. In India,

Chankaya also wrote a manuscript which resembles to the financial management book, in the

Mauryan Empire time period. The book written by him was named as Arthashastra in inclusive

of few aspects of how to follow the accounting and the book keeping for Sovereign State (Ma. et

al 2015).

The accounting records are 7000 years ago and the trading started from the trading of the

temples. The early development of the accounting is closely related with the terms like writing,

money and the counting. Accounting is well known for systemic recording of all the financial

transactions leading to organization. As per the accounting, it is used to analyst, report and

summaries certain transaction when overseeing agencies, tax collection entities and the

regulators. This profession is defined as a system of relatable recording and finally summarizing

the financial transactions to keep the track of commerce. For last thousands, accountants have

been examining data, interpreting the data, keeping certain record, and producing the records for

the operational activities by enabling stakeholders, business owners and other people in order to

make them sound (Chen, et al 2015).

Accounting has developed around time societies, which has started trading with each

other. Accounting was first time visible in early 2000 and 3300 B.C on the basis of Egypt and

clay tablet. Every culture has adopted mathematical calculations for accounting. Luca Pacioli

who was famous for the creation of system of the basic accounting as recorded in simple

textbook. There is a section and description of double entry system accounting as Pacioli is the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

“father of Accounting” but it does not system of ledgers, receivables, trail balance, and closing

balances and these methods are used. The writer has change the life environment to people with

greater things while planning their book of expertise and expense of its business especially, there

is a need for creative ideas rather partnership (Mereghetti, Pons & Melatos, 2015). With the

advancement of technology, it is seen that it is readily available as companies cannot wait long

time nearly to two weeks after the books have been closed while receiving the reports on the

basis of historical data (Chenhall & Moers, 2015). MNCs and large companies have started

leveraging the advanced technology and using the accounting system rather the actual collected

time with the purpose of qualitative and quantitative analysis. There was extremely complex

situation where scholars said that there is a need for writing and accounting evolved side by side.

The increase in the factors will lead to entities such as governments and the royal families. With

an span of time Lucas has settled a comprehensive cycle for accounting that describes clear

process as included in the accounting to follow. Among all these other things, Lucas has

introduced ledgers on the basis of account payable, account receivable, income accounts, capital,

liabilities, inventories and expenditure. At large level and while flourishing the double entry

system, number of factors has to be considered that private properties, large scaled commerce,

systematic writing, credit, arithmetic, and the capitalization (Nobes, 2015).

After using and maintaining the books of accounting, the technology entered the world of

accounting including automated and other flexible processes where organizations will have to

analyst, present, and manage related financial information as per the industry standards where it

is customized to the needs of the company. Rather than limiting the procedure, the system have

certainly added flexibility rather than requiring customer coding and new software. This helps

the business analysts to have a deeper insight to foresee the relative cost and profitability and

finally change the direction of corrections needed. Further, cloud-based system offers a low

costing and huge productivity. With typical integration, it is easier to create a best solution by

combining with the software solutions while creating the best possible solutions for the business.

With minimum efforts, the system automatically functions where accounts payable, accounts

receivable, financial closings, expense capture, management, and revenue recognition where

modern accounting systems are meant to be designed and formulated as per the requirement of

the business environment. Accounting profession certainly has long history with its starting that

remains a robust as humans have conducted transactions (Marra, 2018).

Certainly, accounting is one of the major functions for every business, which may be

handled by an accountant if it is small sized and it can be group of accountants if it is a larger

organization. The necessary reports generated are cot accounting and other is management

accounting that becomes valuable source of streams and data for decision-making. Qualified

professionals who actually own designation (CPA- Certified Public Accountant) to handle

accounting function. With industrialization, there are more advanced accounting standards and

accounting methods that highlights cost accounting system addressing external funding such as

shareowners and this is need to be calculated and finally predict profits on the basis of profit

Paraphrase This Document

prediction on their operation on real financial data. Several people correctly or incorrectly

involved in bookkeeping where they use their knowledge in the preparation of financial

statements, interpret them, and record all the day-to-day transaction. This includes assuring that

whether the financial statements have been complying with GAAP (Generally Accepted

accounting principles) that could provide full disclosure of necessary financial information so

that it could remain free from material errors and misconceptions (Dayanandan, Donker, Ivanof,

& Karahan, 2016).

Question 3: Ethical Principles

List and explain each of the ethical principles in the code of ethics

There are several ethical principle which are to be followed by the accountants are

deliberately required to keep a check on the ethical principles so that the code of the ethics is

maintained effectively and efficiently (Kamal, 2015).

Principle of objectivity

Example: The professional judgment of the accountant shall not be influenced by any third party

just on the basis of the personal relationships. Accountants shall not decide the recording of the

transactions while violating the concept of the accrual accounting to deliver the bonus to one of

the employees (APESB, 2018).

Principle of integrity

The principle of the integrity expects to be completely forthright, authentic and blunt with

a customer's money related data. Accounting ought to confine themselves from individual

increase or bit of leeway utilizing secret data.

Example: The accountants can be honest if they come across any information that can impact the

decisions of the management as well as stakeholders. The news about the insider trading could

be a good example (Cameron & O'Leary, 2015).

Principle of confidentiality

Accountant is committed to shield this data from unapproved divulgence or open

discharge. Since Accountant follows the secrecy standard, customers don't hesitate to talk

honestly and uncover pertinent actualities in regards to accounting as well as subsidiary issues,

empowering the Accountant to act in the customer's best advantage

Example: The accountants shall keep the data confidential despite the individual or the company

hires the subsequent experts or the accountant. The confidentiality shall be maintained even after

the end of the tenure (Amponsah, Boateng & Onuoha, 2016).

Principle of professional behavior

The principle of professional behavior conduct forces a commitment on every single

proficient accountant to consent to applicable laws and guidelines and stay away from any

activity that the expert accountant knows or should know may dishonor the calling.

Example: The relevant laws and regulations must be followed while dealing with any clients,

irrespective of any personal biasness to avoid any further repercussions (APESB, 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Principles of due care and diligence

Example: if the accountant comes across with any kind of the frauds and errors, the due care and

diligence shall be act upon immediately and the same information shall be communicated to the

management (APESB, 2018).

What should accountants do?

Chartered Accountants Australia and New Zealand and Certified Practicing Accountants

Australia, can generally face challenges in while incorporating the accounting principles. In

ethics an ethical dilemma is an issue in the process of taking the strategic decisions between two

potential choices, neither of which is totally adequate from a moral point of view. In spite of the

fact that the organizations face numerous moral and good issues throughout our life, the greater

part of them accompany with the relative solutions. In simpler terms it can be said that the ethical

dilemma is a conflict between the different alternative available, and the ethical principles are

bound to be compromised (CAAN, 2017).

In the field of the accounting the major trust relies on the following of the ethical

practices consistently by the firms and the organizations. In the field of the accounting ethical

responsibility means the firm or the company is recording and translating monetary information

genuinely and objectively without any biasness. The process of the accounting in controlled by

the government and to assist the accountants, different polies as well as procedures are derived to

safeguard the interest against irreconcilable circumstances and any kind of the unprofessional

misconduct, the American Institute of Certified Public Accountants (AICPA) proclaims a

Professional Code of Conduct, just as a synopsis that assists in evaluating various kinds of

threats and also provides the means to safeguard it by complying and adhering to the policies and

the procedures driven by the body (CAAN, (2017).

The typical example of the ethical dilemma is the recording of the transaction in an

incorrect manner. The instructions are provided by a subordinate representative to record an

exchange in a wrong way. For example, an organization with a calendar year of 31st March, signs

contracts with buyers to perform administrative services. The agreements are typically marked

and signed on March 1st and are a yearlong. As per the general principles of accounting, the

revenue shall be recorded only for the month of the March whereas the leftover revenue will be

accounted for in the next financial year. However the management instructs the subordinate to

record the entire amount in the month in which the contract has been established. The major

reason behind opting for this policy is to boost up the revenues for the current financial year. The

board gets a reward for the helped income and the subordinate gets acknowledgment in an

upcoming performance review (Institute of Public Accountants, 2018).

The major ethical dilemma lies here is the recording of the transactions in appropriate

manner just to showcase the business with the higher revenue irrespective of the ethical

accounting. In order to solve these kinds of the situations on the part of the accountants as well

Paraphrase This Document

as the management, an expert shall be hired to vouch the workings of the subordinates as well as

accountants. Such experts are more commonly known as auditors (CPA Australia, 2018).

The solutions could start with setting up of informant hotlines to urge representatives to

show trustworthiness and uprightness in the working environment and the corporate business

culture. The second step could be to explore whether the issue is controlled by law or approach.

The hotspot for data could be the top level management, any professional association, an

administrative body, for example, the U.S. Protections and Exchange Commission — or the

majority of the above mentioned. The American Institute for Certified Public Accountants

(AICPA) has a Code of Professional Conduct, and Financial Executives International has a Code

of Ethics which can be practiced and followed to avoid any issues relating to ethical dilemma.

Both are fantastic assets in case you're dubious about the morals of a circumstance and also

underpin the fundamental principles for the professional accountants (APESB, 2018).

References

Amponsah, E. B., Boateng, P. A., & Onuoha, L. N. (2016). Confidentiality of Accounting

Academics: Consequences of Nonconformity. Journal of education and practice, 7(3),

43-54.

APESB, (2018). Standards and Guidance. Retrieved from https://www.apesb.org.au/

CAAN, (2017). Governance. Retrieved from https://www.revolvy.com/page/Chartered-

Accountants-Australia-and-New-Zealand

Cameron, R. A., & O'Leary, C. (2015). Improving ethical attitudes or simply teaching ethical

codes? The reality of accounting ethics education. Accounting Education, 24(4), 275-290.

Chen, X., Gu, Y., Tao, G., Pei, Y., Wang, G., & Cui, N. (2015). Origin of hydrogen evolution

activity on MS 2 (M= Mo or Nb) monolayers. Journal of Materials Chemistry A, 3(37),

18898-18905.

Chenhall, R. H., & Moers, F. (2015). The role of innovation in the evolution of management

accounting and its integration into management control. Accounting, organizations and

society, 47, 1-13.

CPA Australia, (2018). ACCOUNTING PROFESSIONAL AND ETHICAL STANDARDS.

Retrieved from https://www.cpaaustralia.com.au/professional-resources/accounting-

professional-and-ethical-standards

Dayanandan, A., Donker, H., Ivanof, M., & Karahan, G. (2016). IFRS and accounting quality:

legal origin, regional, and disclosure impacts. International Journal of Accounting and

Information Management, 24(3), 296-316.

Institute of Public Accountants, (2018). Professional Practice Program APES 100 Code of

Ethics. Retrieved from https://www.publicaccountants.org.au/media/1543140/Module-2-

APES-100-Code-of-Ethics.pdf

Kamal, S. (2015). Historical evolution of management accounting. The cost and

management, 43(4), 12-19.

Ma, X., Hopkins, P. F., Faucher-Giguère, C. A., Zolman, N., Muratov, A. L., Kereš, D., &

Quataert, E. (2015). The origin and evolution of the galaxy mass–metallicity

relation. Monthly Notices of the Royal Astronomical Society, 456(2), 2140-2156.

Marra, A. (2018). CFO Country of Origin and Accounting Quality. A Cross-Country

Investigation. A Cross-Country Investigation (January 16, 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Mereghetti, S., Pons, J. A., & Melatos, A. (2015). Magnetars: properties, origin and

evolution. Space Science Reviews, 191(1-4), 315-338.

Nobes, C. (2015). Accounting for capital: the evolution of an idea. Accounting and Business

Research, 45(4), 413-441.

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.