Commonwealth Bank of Australia: PR Theory and Practice Report

VerifiedAdded on 2023/06/10

|13

|4011

|251

Report

AI Summary

This report provides an in-depth analysis of the Commonwealth Bank of Australia (CBA), focusing on its public relations challenges and ethical scandals. The report begins with an introduction to CBA, its values, and its recent ethical issues, including bribery, fraud, and misleading clients. It then delves into a detailed analysis of the ethical scandals, outlining specific incidents and their impact. The report also examines CBA's stakeholders, including employees, customers, investors, and regulators, and their engagement mechanisms. Furthermore, it assesses the impact of these scandals on CBA's image and reputation, along with the existing barriers the bank faces, such as regulatory hurdles, misconduct, ineffective control, and technological changes. The report concludes by highlighting the role of public relations in crisis management and offering recommendations for enhancing Corporate Social Responsibility (CSR). This report is a valuable resource for students studying public relations, ethics, and crisis management, providing insights into real-world challenges faced by a major financial institution.

Running Head: Public Relations theory practice

0

Public relations theory practice

8/11/2018

0

Public relations theory practice

8/11/2018

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Public Relations theory practice 1

Introduction

Commonwealth Bank of Australia (CBA) is an Australian multi-national bank with

companies across Asia, New Zealand, the United Kingdom and the United States. It offers a

range of economic services comprising business, institutional, and retail backing, broking

services, reserves management, investment, assurance, and superannuation. It is the largest

bank in the Southern Hemisphere. This bank is one of the “enormous four” which is listed on

the Australian Stock Exchange in 1991. They have selected a new CEO who presently has a

huge accountability on his shoulders (Howell, 2015).

In 2018, discoveries from the Royal Commission into Misconduct in the Banking,

Superannuation and Financial Services Business have demonstrated a negative philosophy

within the bank, among claims of misrepresentation, deception, and tax evasion, among

various other crimes. Its vision is to exceed expectations and enhancing the well-being of

individual, business, and communities. To accomplish the organization argues that it has to

win the trust of the people it serves. The bank reinforces the trust of the client to ensure

success. CBA’s values incorporate collaboration, integrity, excellence, responsibility, and

service (Otchere and Chan, 2003). This value guarantees that clients have to be taken care

efficiently and competently so that outcomes in their satisfaction match with the

organization’s services. It advances the policies of environmental stewardship in computing

environmental footprint and enabling the use of renewable energy. It also develops a

disciplined monetary control system and committed governance for getting the current value

to clients.

In the following, an effort has been made to describe ethical standards through public

relations theory, identify the barriers to the organization, and recommendation to enhance its

CSR.

Analysis of the ethical scandals

Commonwealth Bank of Australia has faced many ethical standards that have influenced its

reputation and bank works continuously to legitimize its reputation. Some of the main

scandals faced by CBA are –

Bank official charged allegedly over the bribery scandal.

Bank staff concerned in alleged $76m fraud.

Introduction

Commonwealth Bank of Australia (CBA) is an Australian multi-national bank with

companies across Asia, New Zealand, the United Kingdom and the United States. It offers a

range of economic services comprising business, institutional, and retail backing, broking

services, reserves management, investment, assurance, and superannuation. It is the largest

bank in the Southern Hemisphere. This bank is one of the “enormous four” which is listed on

the Australian Stock Exchange in 1991. They have selected a new CEO who presently has a

huge accountability on his shoulders (Howell, 2015).

In 2018, discoveries from the Royal Commission into Misconduct in the Banking,

Superannuation and Financial Services Business have demonstrated a negative philosophy

within the bank, among claims of misrepresentation, deception, and tax evasion, among

various other crimes. Its vision is to exceed expectations and enhancing the well-being of

individual, business, and communities. To accomplish the organization argues that it has to

win the trust of the people it serves. The bank reinforces the trust of the client to ensure

success. CBA’s values incorporate collaboration, integrity, excellence, responsibility, and

service (Otchere and Chan, 2003). This value guarantees that clients have to be taken care

efficiently and competently so that outcomes in their satisfaction match with the

organization’s services. It advances the policies of environmental stewardship in computing

environmental footprint and enabling the use of renewable energy. It also develops a

disciplined monetary control system and committed governance for getting the current value

to clients.

In the following, an effort has been made to describe ethical standards through public

relations theory, identify the barriers to the organization, and recommendation to enhance its

CSR.

Analysis of the ethical scandals

Commonwealth Bank of Australia has faced many ethical standards that have influenced its

reputation and bank works continuously to legitimize its reputation. Some of the main

scandals faced by CBA are –

Bank official charged allegedly over the bribery scandal.

Bank staff concerned in alleged $76m fraud.

Public Relations theory practice 2

A vast majority of financial Planners betrayed client’s interest.

Accusation over bribery scandal-

In bribery, scandal two Commonwealth Bank administrators, Keith Hunter (Previous director

of Technology Service Management) & Jon Waldron (GM of bank’s IT engineering

answered to Keith Hunter) were accused over a bribery scandal with a U.S based Technology

Company in 2013 with two counts of bribery. The co-conspirator Waldron was accused with

seven counts of receiving unethical payment associated to a lucrative agreement, which was

given by CBA to the Californian, centred IT firm Service Mesh. They helped them to secure

major IT tender to deliver products & services without putting it to general. Waldron &

Hunter expected a payment of almost $2.2 million in 2014 from an NGO, which was fixed by

Service Mesh. The bank identified in response to the scandal that they do not accept any

offense or illegal action by any of the banks' employee and will take genuine action. They

announced “Anti-bribery and corruption strategy and programme” in light of these scandals

(McIlroy, 2018).

Bank staff implicated over alleged fraud-

Bank staffs were apparently collusion in a $ 76 million Ponzi scheme and got undisclosed

commissions for their part in the suspected deception, which was overlooked by the bank's

administration for nearly five years-until forces were alarmed. Mr Zaia and Mr Jordanou are

alleged of using fake documents to acquire millions of dollars for some proper advances that

certainly not got off the ground. Assets were supposedly guided from client’s accounts

without their approval. Documents acquired by the Fairfax Media disclose the range of the

bank’s contribution and its disturbing integrity failings (Buckby, Gallery, and Ma, 2015).

Deceived client’s interest-

The head of financial advice for Anthony Regan, concedes he lost count and mislead the

corporate regulator, ASIC which compels to introduces public relations practices and

programmes. The company has suffered financial loss and failure to provide on-going

services (Sujan and Abeysekera, 2007).

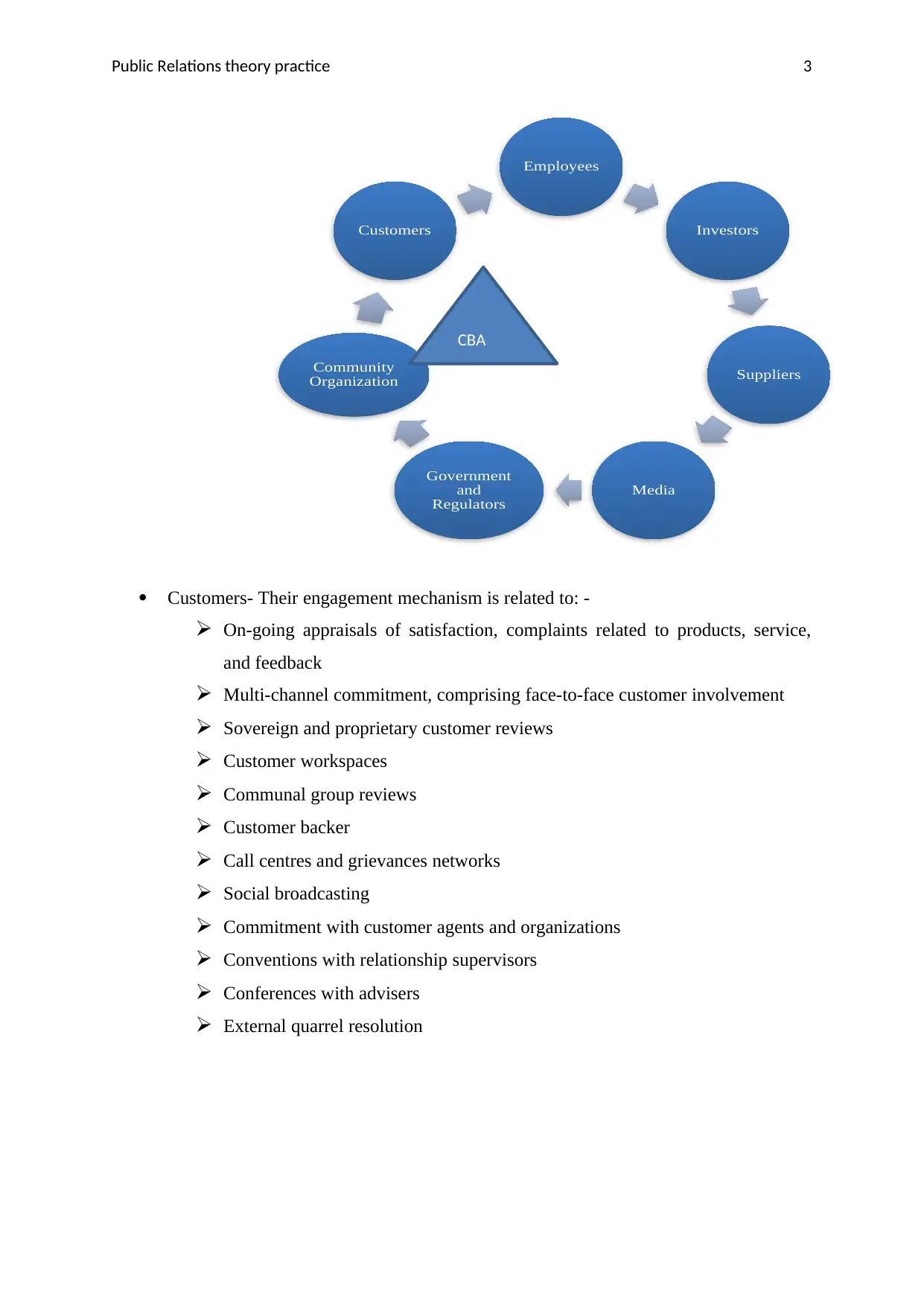

Stakeholders’ analysis

One of our commitment series of forums are devoted to progressing our stakeholder

engagement, which includes-

A vast majority of financial Planners betrayed client’s interest.

Accusation over bribery scandal-

In bribery, scandal two Commonwealth Bank administrators, Keith Hunter (Previous director

of Technology Service Management) & Jon Waldron (GM of bank’s IT engineering

answered to Keith Hunter) were accused over a bribery scandal with a U.S based Technology

Company in 2013 with two counts of bribery. The co-conspirator Waldron was accused with

seven counts of receiving unethical payment associated to a lucrative agreement, which was

given by CBA to the Californian, centred IT firm Service Mesh. They helped them to secure

major IT tender to deliver products & services without putting it to general. Waldron &

Hunter expected a payment of almost $2.2 million in 2014 from an NGO, which was fixed by

Service Mesh. The bank identified in response to the scandal that they do not accept any

offense or illegal action by any of the banks' employee and will take genuine action. They

announced “Anti-bribery and corruption strategy and programme” in light of these scandals

(McIlroy, 2018).

Bank staff implicated over alleged fraud-

Bank staffs were apparently collusion in a $ 76 million Ponzi scheme and got undisclosed

commissions for their part in the suspected deception, which was overlooked by the bank's

administration for nearly five years-until forces were alarmed. Mr Zaia and Mr Jordanou are

alleged of using fake documents to acquire millions of dollars for some proper advances that

certainly not got off the ground. Assets were supposedly guided from client’s accounts

without their approval. Documents acquired by the Fairfax Media disclose the range of the

bank’s contribution and its disturbing integrity failings (Buckby, Gallery, and Ma, 2015).

Deceived client’s interest-

The head of financial advice for Anthony Regan, concedes he lost count and mislead the

corporate regulator, ASIC which compels to introduces public relations practices and

programmes. The company has suffered financial loss and failure to provide on-going

services (Sujan and Abeysekera, 2007).

Stakeholders’ analysis

One of our commitment series of forums are devoted to progressing our stakeholder

engagement, which includes-

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Public Relations theory practice 3

Customers- Their engagement mechanism is related to: -

On-going appraisals of satisfaction, complaints related to products, service,

and feedback

Multi-channel commitment, comprising face-to-face customer involvement

Sovereign and proprietary customer reviews

Customer workspaces

Communal group reviews

Customer backer

Call centres and grievances networks

Social broadcasting

Commitment with customer agents and organizations

Conventions with relationship supervisors

Conferences with advisers

External quarrel resolution

Employees

Investors

Suppliers

Media

Government

and

Regulators

Community

Organization

Customers

CBA

Customers- Their engagement mechanism is related to: -

On-going appraisals of satisfaction, complaints related to products, service,

and feedback

Multi-channel commitment, comprising face-to-face customer involvement

Sovereign and proprietary customer reviews

Customer workspaces

Communal group reviews

Customer backer

Call centres and grievances networks

Social broadcasting

Commitment with customer agents and organizations

Conventions with relationship supervisors

Conferences with advisers

External quarrel resolution

Employees

Investors

Suppliers

Media

Government

and

Regulators

Community

Organization

Customers

CBA

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Public Relations theory practice 4

Employees- They are influenced by the negative publicity adjoining the scandal such

as: -

On-going appraisals of employee engagement and feedback beliefs, policy and

significances

CEO and Group Administrative in-boxes

Ad hoc reviews

Social and digital platform

Team conferences and training

Employee actions and Town Halls

Group widespread appraisal should be conducted (Martin, Evans, Rice, Lodhia

and Gibbons, 2016).

Investors- They are accountable for raising debt backing for the bank from the

national and international debt market

On-going negotiations regarding performance related matters

Monetary and non-monetary reporting

Seminars

Conferences

Assessments

AGM

Suppliers- They support in enhancing commitment to provide products and services

for our organization, people, community, and the economy to upgrade value and

manage supply chain

On-going debates associated to standards, commercials, and issues

Supplier conferences, seminars, and workshops

Risk valuations

Modernisation programs

Supplier protocol and Renewability Questionnaire

Supplier reviews

Media- They make an important announcement to brief community about subject

matters

Employees- They are influenced by the negative publicity adjoining the scandal such

as: -

On-going appraisals of employee engagement and feedback beliefs, policy and

significances

CEO and Group Administrative in-boxes

Ad hoc reviews

Social and digital platform

Team conferences and training

Employee actions and Town Halls

Group widespread appraisal should be conducted (Martin, Evans, Rice, Lodhia

and Gibbons, 2016).

Investors- They are accountable for raising debt backing for the bank from the

national and international debt market

On-going negotiations regarding performance related matters

Monetary and non-monetary reporting

Seminars

Conferences

Assessments

AGM

Suppliers- They support in enhancing commitment to provide products and services

for our organization, people, community, and the economy to upgrade value and

manage supply chain

On-going debates associated to standards, commercials, and issues

Supplier conferences, seminars, and workshops

Risk valuations

Modernisation programs

Supplier protocol and Renewability Questionnaire

Supplier reviews

Media- They make an important announcement to brief community about subject

matters

Public Relations theory practice 5

On-going matters associated with topics of concentration

Meetings, conferences, and emails

Updates and media releases

Digital platform

Government and Regulators- They make innovation in Financial services and banking

reform should be regulated

On-going considerations associated with the monetary services production,

advocacy, and reform

Summits

Proposals

Inquiries and commissions

Financial establishment associations

Community Organization- Their engagement mechanism is associated with education

diversity, charity partnerships, customer assistance, disaster belief, and sustainability

(Chan, Watson and Woodliff, 2014).

Contribution on a variety of external recommended panels

Industry associations

On-going conferences with partners

Phone calls and emails

Sponsorship of events, forums, and summits

Impact on the image

The Commonwealth Bank has perceived its six months profits drop after it was enforced to

set aside $375m as arrangement against possible fines for charged money laundering and

subsidizing of violence. It has reported that its ultimate set of results under outbound CEO

Ian Narev, that its half-year money profit fell 1.9 % to $ 4.735bn. Statutory benefit for the six

months has dropped to a vast extent and market volatility remains at a risk given continuous

global uncertainty. The scandals in the bank have inflicted competitive image and reputation,

which has been spoiled by significant misconduct in its financial planning (Moradi-Motlagh

and Babacan, 2015). They have consented to $25 million to settle legitimate activity against it

by ASIC over bank charge swap rates. It has visible it to billions of dollars in potential

penalties and lost monetary statements of 20 million account holders. It has engaged in the

unconscionable behaviour, which could not monitor communication and trading of personnel.

On-going matters associated with topics of concentration

Meetings, conferences, and emails

Updates and media releases

Digital platform

Government and Regulators- They make innovation in Financial services and banking

reform should be regulated

On-going considerations associated with the monetary services production,

advocacy, and reform

Summits

Proposals

Inquiries and commissions

Financial establishment associations

Community Organization- Their engagement mechanism is associated with education

diversity, charity partnerships, customer assistance, disaster belief, and sustainability

(Chan, Watson and Woodliff, 2014).

Contribution on a variety of external recommended panels

Industry associations

On-going conferences with partners

Phone calls and emails

Sponsorship of events, forums, and summits

Impact on the image

The Commonwealth Bank has perceived its six months profits drop after it was enforced to

set aside $375m as arrangement against possible fines for charged money laundering and

subsidizing of violence. It has reported that its ultimate set of results under outbound CEO

Ian Narev, that its half-year money profit fell 1.9 % to $ 4.735bn. Statutory benefit for the six

months has dropped to a vast extent and market volatility remains at a risk given continuous

global uncertainty. The scandals in the bank have inflicted competitive image and reputation,

which has been spoiled by significant misconduct in its financial planning (Moradi-Motlagh

and Babacan, 2015). They have consented to $25 million to settle legitimate activity against it

by ASIC over bank charge swap rates. It has visible it to billions of dollars in potential

penalties and lost monetary statements of 20 million account holders. It has engaged in the

unconscionable behaviour, which could not monitor communication and trading of personnel.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Public Relations theory practice 6

They have to pay penalties to financial customer and ASIC. It comes in the wake of critical

revelations uncovered by the banking royal commission.

Meanwhile, an investor legal claim against CBA alleges that the bank did not consent to its

continuous exposure commitments to inform shareholders about the Austrac examination.

After the money laundering case, there is a possible lack of resourcing and compliance

functions at the bank. It has prompted to years in prison for launderers, an A$4bn fall in CBA

market estimation and the government's declaration of a public inquiry into unfortunate

behaviour. They have lost people trust and confidence they play in the brand as a social

image is associated with the customer perception. Customer sentimental attachment and

recognition is attached to the brand when it is breached satisfaction decreases. They are

accused of penetrating Counter-terrorism financing and Anti-Money Laundering Act over

mutual cash deposits. CBA admitted utilizing unscrupulous practices that conned individuals

out of life insurance payments, and Mr Narev apologized publicly after found to have given

clients poor money-related advice (Cummings and Durrani, 2016).

Analysis of existence barriers

The bank is an established business, and it becomes tough to adopt an innovation, as it will be

tedious to bring variations in the organization. It was currently understood that the greatest

hindrance to the bank is –

Regulator- The regulatory hindrances should be detached so that the financial sector

can be intended to provide greater retirement items to fulfil the requirements of the

women. The barriers should be detached which the stops the cost-adequacy in

planning the income stream product since it can cause risk (Hamman, 2016).

Misconduct- The bank is losing their clients because of the misconduct of the staffs

associated with the financial issues. In recent years, it was distinguished that the

personnel working in the bank were not executing their responsibilities according to

the compliance. They were engaged in a forgery of facts and documents, which

prompt to the huge financial damage. This unethical conduct of the personnel caused

an extreme harm to the reputation of the bank. Numerous clients discontinued their

accounts with the bank and opened in some other banks.

Ineffective control- Due to ineffective control framework within the organization, the

personnel were successful in making unreasonable financial advice to the customers

They have to pay penalties to financial customer and ASIC. It comes in the wake of critical

revelations uncovered by the banking royal commission.

Meanwhile, an investor legal claim against CBA alleges that the bank did not consent to its

continuous exposure commitments to inform shareholders about the Austrac examination.

After the money laundering case, there is a possible lack of resourcing and compliance

functions at the bank. It has prompted to years in prison for launderers, an A$4bn fall in CBA

market estimation and the government's declaration of a public inquiry into unfortunate

behaviour. They have lost people trust and confidence they play in the brand as a social

image is associated with the customer perception. Customer sentimental attachment and

recognition is attached to the brand when it is breached satisfaction decreases. They are

accused of penetrating Counter-terrorism financing and Anti-Money Laundering Act over

mutual cash deposits. CBA admitted utilizing unscrupulous practices that conned individuals

out of life insurance payments, and Mr Narev apologized publicly after found to have given

clients poor money-related advice (Cummings and Durrani, 2016).

Analysis of existence barriers

The bank is an established business, and it becomes tough to adopt an innovation, as it will be

tedious to bring variations in the organization. It was currently understood that the greatest

hindrance to the bank is –

Regulator- The regulatory hindrances should be detached so that the financial sector

can be intended to provide greater retirement items to fulfil the requirements of the

women. The barriers should be detached which the stops the cost-adequacy in

planning the income stream product since it can cause risk (Hamman, 2016).

Misconduct- The bank is losing their clients because of the misconduct of the staffs

associated with the financial issues. In recent years, it was distinguished that the

personnel working in the bank were not executing their responsibilities according to

the compliance. They were engaged in a forgery of facts and documents, which

prompt to the huge financial damage. This unethical conduct of the personnel caused

an extreme harm to the reputation of the bank. Numerous clients discontinued their

accounts with the bank and opened in some other banks.

Ineffective control- Due to ineffective control framework within the organization, the

personnel were successful in making unreasonable financial advice to the customers

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Public Relations theory practice 7

associated with the investment and bank accounts. Personnel were involved in making

forged signatures and manipulating the customers to make wrong choices. At the

point when the allegations were proved right, after a critical investigation, the

personnel were suspended and dismissed from work. An effective control framework

is must to keep in mind the activities performed by the workers. Proper records of all

the transactions should be sustained so that they can be confirmed as and when

required.

Hierarchical Structure-The bank follows a hierarchical arrangement in the

organization where only the top management is permitted to participate in decision-

making and policymaking. They have an inflexible working procedure and are not

willing to conform to the dynamic variation that takes place in the business

atmosphere. It is still centred in the following the inflexible structure in the work

procedure and because of this the opponents are performing and CBA is missing

behind (Wagland and Taylor, 2015).

Technological Changes- The bank is not able to adapt up to the technological

variations, clients are frequently complaining about the improper online

administrations. Customers are documenting complaints with respect to this matter on

social media, which is abolishing the association of goodwill in the market. Clients

are switching their businesses and accounts with different banks that are providing

better services.

Role of PR in Crisis management-

Public relations remain to be an integral part in managing the crisis and reconstructing the

reputations of the banks. Banks are currently connected on all sides to react to the public trust

entanglement while accusations of poor business practices proceed. It combines the public

distrust with flows of lawsuits from offended parties at all levels of the loan securities market.

PR experts know how to change public perception with the right words and marketing

campaign (Liu, 2015). They also know that supporting their customers with the right

strategies can mitigate many issues that accompany with a public crisis. Disaster management

is most likely best-known roles among other parts of PR (Sheehan and Quinn-Allan, 2015).

PR specialist will assess the situation and offer advice on what the banks should do to solve

the problem. To provide the right supervision, PR experts need to assess the background, the

type of the current disaster, and the immediate context, so that they can suggest a systematic

associated with the investment and bank accounts. Personnel were involved in making

forged signatures and manipulating the customers to make wrong choices. At the

point when the allegations were proved right, after a critical investigation, the

personnel were suspended and dismissed from work. An effective control framework

is must to keep in mind the activities performed by the workers. Proper records of all

the transactions should be sustained so that they can be confirmed as and when

required.

Hierarchical Structure-The bank follows a hierarchical arrangement in the

organization where only the top management is permitted to participate in decision-

making and policymaking. They have an inflexible working procedure and are not

willing to conform to the dynamic variation that takes place in the business

atmosphere. It is still centred in the following the inflexible structure in the work

procedure and because of this the opponents are performing and CBA is missing

behind (Wagland and Taylor, 2015).

Technological Changes- The bank is not able to adapt up to the technological

variations, clients are frequently complaining about the improper online

administrations. Customers are documenting complaints with respect to this matter on

social media, which is abolishing the association of goodwill in the market. Clients

are switching their businesses and accounts with different banks that are providing

better services.

Role of PR in Crisis management-

Public relations remain to be an integral part in managing the crisis and reconstructing the

reputations of the banks. Banks are currently connected on all sides to react to the public trust

entanglement while accusations of poor business practices proceed. It combines the public

distrust with flows of lawsuits from offended parties at all levels of the loan securities market.

PR experts know how to change public perception with the right words and marketing

campaign (Liu, 2015). They also know that supporting their customers with the right

strategies can mitigate many issues that accompany with a public crisis. Disaster management

is most likely best-known roles among other parts of PR (Sheehan and Quinn-Allan, 2015).

PR specialist will assess the situation and offer advice on what the banks should do to solve

the problem. To provide the right supervision, PR experts need to assess the background, the

type of the current disaster, and the immediate context, so that they can suggest a systematic

Public Relations theory practice 8

guide on dealing with the incident (Drennan, McConnell and Stark, 2014). They should know

which viewers they should address first when making an open declaration, which terms they

should avoid, and their response matters. They react to what happening in the media and offer

continually updated advice on the best way to deal with the circumstance. They should

support statements and materials on behalf of the client, while at the same time schedule

interviews and meetings with the media to guarantee that it comes off in the most ideal light.

They should offer insights on maintaining the brand loyalty of their shareholders, investors,

and customers (Liu, Cutcher, and Grant, 2017).

After the initial crises have conceded, PR has to begin strategies to reconcile the damage that

was finished during the calamity. For example, they may create a proposal that attracts more

attention to the positive part of the brand's identity. They should set up important interviews

and press releases to help take most of the public attention away from the event that happened

and help the bank in returning to as usual (Ciro, 2016).

Press release to the shareholders

Commonwealth bank delivers a press release after scandal in which they announce an annual

report on 9 August 2017 by CEO Ian Narev and CFO Rob Jesudason. Commonwealth bank

performance this year has again donated to the monetary prosperity of our investors, our

people, clients, and the Australian economy. This is the consequence of our reliable focus on

innovation, client loyalty, and economic strength (Brown and Karpavičius, 2017).

This announcement provides:

A summary of the improvements made to financial reporting; and

An updated financial full-year profit was announced.

Financial report improvements-

Minor improvements have been made to the distribution of the customer balances and related

revenue and expenses between business sections. The group has changed its accounting plan

in connection to long-term incentives delivered to specific employees in the Global Asset

Management business, to support the accounting treatment with characterized commitment

plans under employee benefits. Minor improvements have been also made to the revelation of

Fund under Administration (FUA) balances (Reinig and Tilt, 2008).

guide on dealing with the incident (Drennan, McConnell and Stark, 2014). They should know

which viewers they should address first when making an open declaration, which terms they

should avoid, and their response matters. They react to what happening in the media and offer

continually updated advice on the best way to deal with the circumstance. They should

support statements and materials on behalf of the client, while at the same time schedule

interviews and meetings with the media to guarantee that it comes off in the most ideal light.

They should offer insights on maintaining the brand loyalty of their shareholders, investors,

and customers (Liu, Cutcher, and Grant, 2017).

After the initial crises have conceded, PR has to begin strategies to reconcile the damage that

was finished during the calamity. For example, they may create a proposal that attracts more

attention to the positive part of the brand's identity. They should set up important interviews

and press releases to help take most of the public attention away from the event that happened

and help the bank in returning to as usual (Ciro, 2016).

Press release to the shareholders

Commonwealth bank delivers a press release after scandal in which they announce an annual

report on 9 August 2017 by CEO Ian Narev and CFO Rob Jesudason. Commonwealth bank

performance this year has again donated to the monetary prosperity of our investors, our

people, clients, and the Australian economy. This is the consequence of our reliable focus on

innovation, client loyalty, and economic strength (Brown and Karpavičius, 2017).

This announcement provides:

A summary of the improvements made to financial reporting; and

An updated financial full-year profit was announced.

Financial report improvements-

Minor improvements have been made to the distribution of the customer balances and related

revenue and expenses between business sections. The group has changed its accounting plan

in connection to long-term incentives delivered to specific employees in the Global Asset

Management business, to support the accounting treatment with characterized commitment

plans under employee benefits. Minor improvements have been also made to the revelation of

Fund under Administration (FUA) balances (Reinig and Tilt, 2008).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Public Relations theory practice 9

Financial full-year profit-

Following enhancement to approach in the recent period, there was a variation to the

arrangement of credit disclosures by credit grade for advances, which neither were due, nor

debilitated (Schlagwein, Thorogood and Willcocks, 2014).

They talked about the strong point of CBA’s monetary performance has reinforced the

Board’s aim of steady dividends for investors. CBA dividends are remunerated to in excess

of investors and through their super funds. They have focussed on enhancing and securing the

financial comfort of individuals, industries, and the communities, and the arrangement of

assurance items to our clients. They support clients through technology and convey great

customer experience through channels (Willcocks and Reynolds, 2015).

Recommendation

CBA should strengthen governance, management of non-budgetary risk, and

misunderstanding.

They should achieve better clients and risk outcomes

They should more responsible, customer-centred, and transparent culture.

Taking a proactive approach to deal with situations and improve execution.

Supporting the inducements of banks with communal benefits is greatly assisted by

increasing the responsibilities of directors to take into consideration societal and

ecological elements (Williams, 2016).

Describing disclosure necessities and protecting these in business governance

framework would help to coherences values, rise comparability and increase

clearness, while reducing facts irregularity and the incidence of ethical exposures.

If an activity has a supposed hazard of causing damage to humanity or the situation,

the liability of proof should fall on the potential investors of the activity.

The administration should more aggressively satisfy its responsibility as the protector

of public attention.

A renewed focus on listening to clients and enhanced framework and methods are

implemented for reporting and settling client grievances (Steen, McGrath and Wong,

2016).

Financial full-year profit-

Following enhancement to approach in the recent period, there was a variation to the

arrangement of credit disclosures by credit grade for advances, which neither were due, nor

debilitated (Schlagwein, Thorogood and Willcocks, 2014).

They talked about the strong point of CBA’s monetary performance has reinforced the

Board’s aim of steady dividends for investors. CBA dividends are remunerated to in excess

of investors and through their super funds. They have focussed on enhancing and securing the

financial comfort of individuals, industries, and the communities, and the arrangement of

assurance items to our clients. They support clients through technology and convey great

customer experience through channels (Willcocks and Reynolds, 2015).

Recommendation

CBA should strengthen governance, management of non-budgetary risk, and

misunderstanding.

They should achieve better clients and risk outcomes

They should more responsible, customer-centred, and transparent culture.

Taking a proactive approach to deal with situations and improve execution.

Supporting the inducements of banks with communal benefits is greatly assisted by

increasing the responsibilities of directors to take into consideration societal and

ecological elements (Williams, 2016).

Describing disclosure necessities and protecting these in business governance

framework would help to coherences values, rise comparability and increase

clearness, while reducing facts irregularity and the incidence of ethical exposures.

If an activity has a supposed hazard of causing damage to humanity or the situation,

the liability of proof should fall on the potential investors of the activity.

The administration should more aggressively satisfy its responsibility as the protector

of public attention.

A renewed focus on listening to clients and enhanced framework and methods are

implemented for reporting and settling client grievances (Steen, McGrath and Wong,

2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Public Relations theory practice 10

Conclusion

Commonwealth Bank of Australia offers financial and banking services. It offers them to

small business, retail, corporate, and institutional customers. A robust banking area is

condemning to a strong economy. Many have contended that bank was shielded from the

poorest effects of the Global Monetary Crises. Their reputation has accepted a major hit over

financial advice scandals and an enormous money laundering case. ASIC has started

legitimate action over apparent market control. These are claims that could eventually cost

the bank billions of dollars in penalties. The alleged ruptures of money laundering and

terrorism financing enactment were the most recent in a progression of scandals that had

extremely damaged brand CBA.

To be strong bank build upon the support of their investors, the trust of their clients, and an

active working relationship with regulators and government. The Big 4 Australian banks

were the largest companies on the Australian Securities Exchange. There has been an active

debate about whether the Australian banks should pledge a Royal Commission into banking

business practices. They are constructed in a foundation of trust and they have to win that

trust through being vulnerable and answerable at all times. Therefore, it is important to

advocate widespread adoption of CSR without considering the consequences.

References

Howell, N.J., (2015) Revisiting the Australian code of banking practice: is self-regulation still

relevant for improving consumer protection standards. UNSWLJ,38, p.544.

Otchere, I. and Chan, J., (2003) Intra-industry effects of bank privatization: A clinical

analysis of the privatization of the Commonwealth Bank of Australia. Journal of Banking &

Finance, 27(5), pp.949-975.

Conclusion

Commonwealth Bank of Australia offers financial and banking services. It offers them to

small business, retail, corporate, and institutional customers. A robust banking area is

condemning to a strong economy. Many have contended that bank was shielded from the

poorest effects of the Global Monetary Crises. Their reputation has accepted a major hit over

financial advice scandals and an enormous money laundering case. ASIC has started

legitimate action over apparent market control. These are claims that could eventually cost

the bank billions of dollars in penalties. The alleged ruptures of money laundering and

terrorism financing enactment were the most recent in a progression of scandals that had

extremely damaged brand CBA.

To be strong bank build upon the support of their investors, the trust of their clients, and an

active working relationship with regulators and government. The Big 4 Australian banks

were the largest companies on the Australian Securities Exchange. There has been an active

debate about whether the Australian banks should pledge a Royal Commission into banking

business practices. They are constructed in a foundation of trust and they have to win that

trust through being vulnerable and answerable at all times. Therefore, it is important to

advocate widespread adoption of CSR without considering the consequences.

References

Howell, N.J., (2015) Revisiting the Australian code of banking practice: is self-regulation still

relevant for improving consumer protection standards. UNSWLJ,38, p.544.

Otchere, I. and Chan, J., (2003) Intra-industry effects of bank privatization: A clinical

analysis of the privatization of the Commonwealth Bank of Australia. Journal of Banking &

Finance, 27(5), pp.949-975.

Public Relations theory practice 11

Sujan, A. and Abeysekera, I., (2007) Intellectual capital reporting practices of the top

Australian firms. Australian Accounting Review, 17(42), pp.71-83.

McIlroy, J., (2018) Bank scandals fuel calls for completely new system: Why we should

nationalise the big four under democratic control. Green Left Weekly, (1178), p.8.

Martin, N., Evans, M., Rice, J., Lodhia, S. and Gibbons, P., (2016) Using offsets to mitigate

environmental impacts of major projects: A stakeholder analysis. Journal of environmental

management, 179, pp.58-65.

Chan, M.C., Watson, J. and Woodliff, D., (2014) Corporate governance quality and CSR

disclosures. Journal of Business Ethics, 125(1), pp.59-73.

Moradi-Motlagh, A. and Babacan, A., (2015) The impact of the global financial crisis on the

efficiency of Australian banks. Economic Modelling, 46, pp.397-406.

Cummings, J.R. and Durrani, K.J., (2016) Effect of the Basel Accord capital requirements on

the loan-loss provisioning practices of Australian banks. Journal of Banking & Finance, 67,

pp.23-36.

Hamman, E., (2016) The influence of environmental NGOs on project finance: a case study

of activism, development and Australia’s Great Barrier Reef. Journal of Sustainable Finance

& Investment, 6(1), pp.51-66.

Wagland, S. and Taylor, S.M., (2015) The conflict between financial decision-making and

indigenous Australian culture. Financial Planning Research Journal, 1(1), pp.33-54.

Sheehan, M. and Quinn-Allan, D. eds., (2015) Crisis communication in a digital world.

Australia: Cambridge University Press.

Drennan, L.T., McConnell, A. and Stark, A., (2014) Risk and crisis management in the public

sector. London: Routledge.

Liu, H., Cutcher, L. and Grant, D., (2017) Authentic leadership in context: An analysis of

banking CEO narratives during the global financial crisis. Human Relations, 70(6), pp.694-

724.

Ciro, T., (2016) The global financial crisis: Triggers, responses and aftermath. London:

Routledge.

Brown, A. and Karpavičius, S., (2017) The Reaction of the Australian Stock Market to

Monetary Policy Announcements from the Reserve Bank of Australia. Economic

Record, 93(300), pp.20-41.

Reinig, C.J. and Tilt, C.A., (2008) Corporate social responsibility issues in media releases: a

stakeholder analysis of Australian banks. Issues in Social and Environmental

Accounting, 2(2), pp.176-197.

Sujan, A. and Abeysekera, I., (2007) Intellectual capital reporting practices of the top

Australian firms. Australian Accounting Review, 17(42), pp.71-83.

McIlroy, J., (2018) Bank scandals fuel calls for completely new system: Why we should

nationalise the big four under democratic control. Green Left Weekly, (1178), p.8.

Martin, N., Evans, M., Rice, J., Lodhia, S. and Gibbons, P., (2016) Using offsets to mitigate

environmental impacts of major projects: A stakeholder analysis. Journal of environmental

management, 179, pp.58-65.

Chan, M.C., Watson, J. and Woodliff, D., (2014) Corporate governance quality and CSR

disclosures. Journal of Business Ethics, 125(1), pp.59-73.

Moradi-Motlagh, A. and Babacan, A., (2015) The impact of the global financial crisis on the

efficiency of Australian banks. Economic Modelling, 46, pp.397-406.

Cummings, J.R. and Durrani, K.J., (2016) Effect of the Basel Accord capital requirements on

the loan-loss provisioning practices of Australian banks. Journal of Banking & Finance, 67,

pp.23-36.

Hamman, E., (2016) The influence of environmental NGOs on project finance: a case study

of activism, development and Australia’s Great Barrier Reef. Journal of Sustainable Finance

& Investment, 6(1), pp.51-66.

Wagland, S. and Taylor, S.M., (2015) The conflict between financial decision-making and

indigenous Australian culture. Financial Planning Research Journal, 1(1), pp.33-54.

Sheehan, M. and Quinn-Allan, D. eds., (2015) Crisis communication in a digital world.

Australia: Cambridge University Press.

Drennan, L.T., McConnell, A. and Stark, A., (2014) Risk and crisis management in the public

sector. London: Routledge.

Liu, H., Cutcher, L. and Grant, D., (2017) Authentic leadership in context: An analysis of

banking CEO narratives during the global financial crisis. Human Relations, 70(6), pp.694-

724.

Ciro, T., (2016) The global financial crisis: Triggers, responses and aftermath. London:

Routledge.

Brown, A. and Karpavičius, S., (2017) The Reaction of the Australian Stock Market to

Monetary Policy Announcements from the Reserve Bank of Australia. Economic

Record, 93(300), pp.20-41.

Reinig, C.J. and Tilt, C.A., (2008) Corporate social responsibility issues in media releases: a

stakeholder analysis of Australian banks. Issues in Social and Environmental

Accounting, 2(2), pp.176-197.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.