Charles Sturt University ACC515 Report: Project Evaluation and Finance

VerifiedAdded on 2020/01/07

|9

|1645

|195

Report

AI Summary

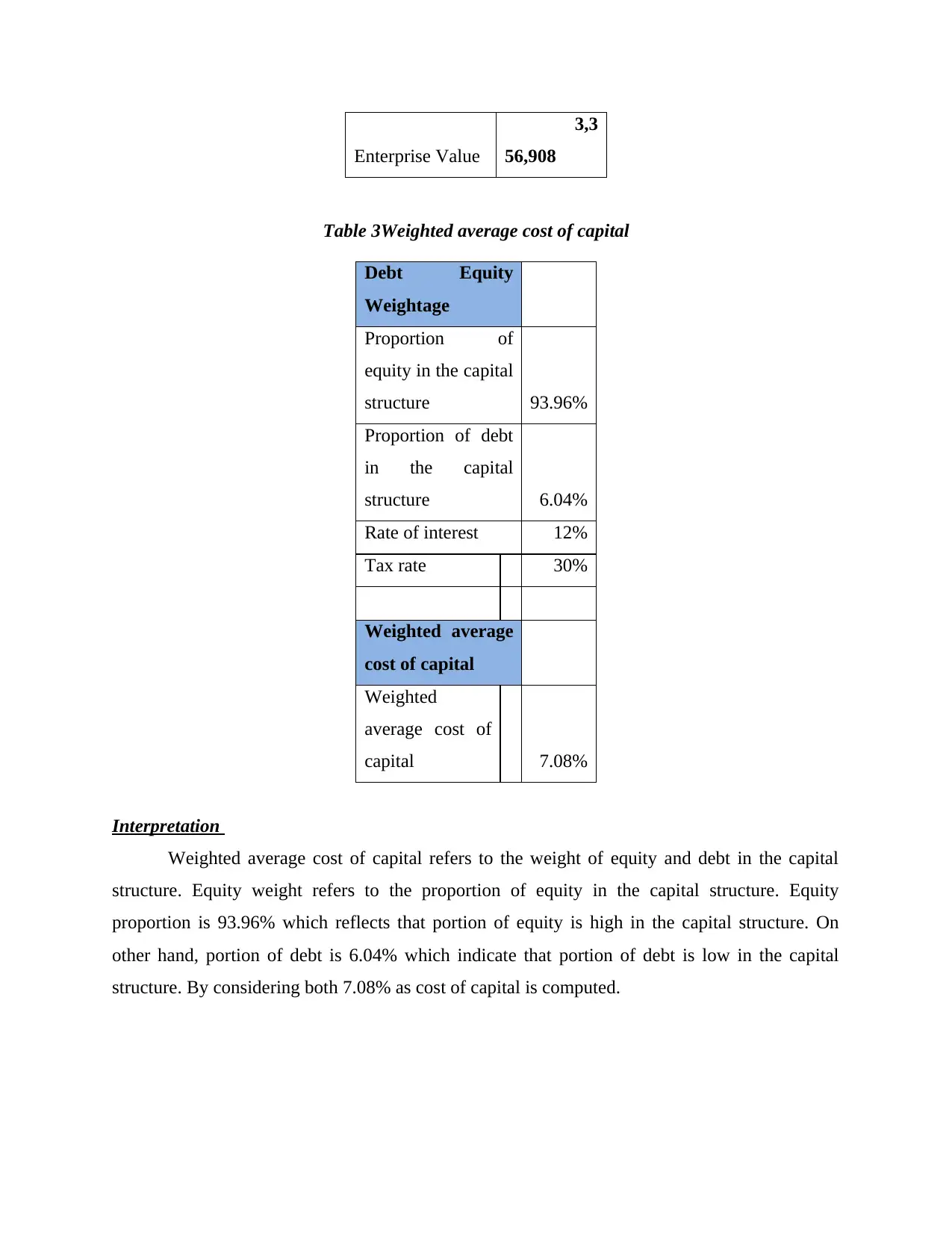

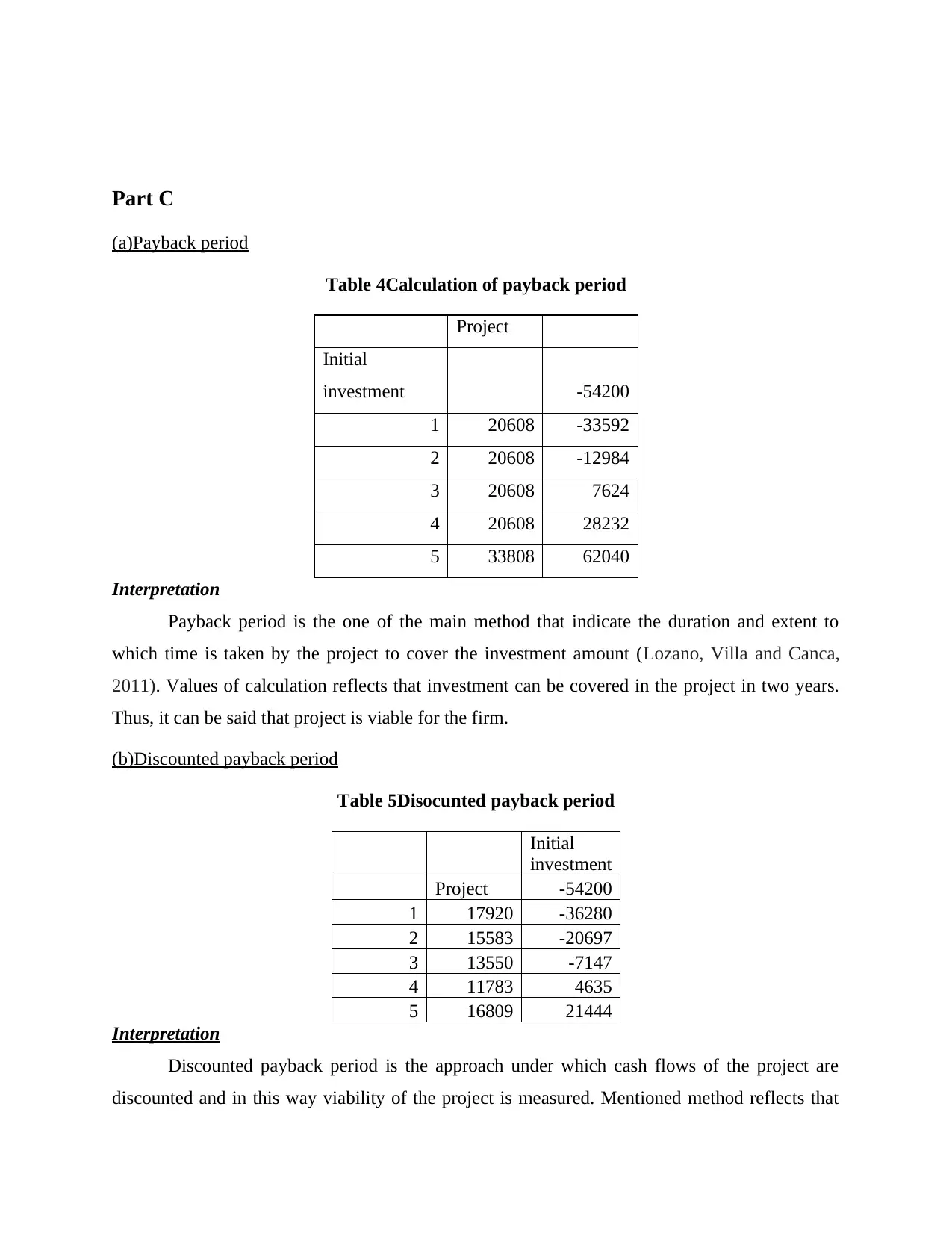

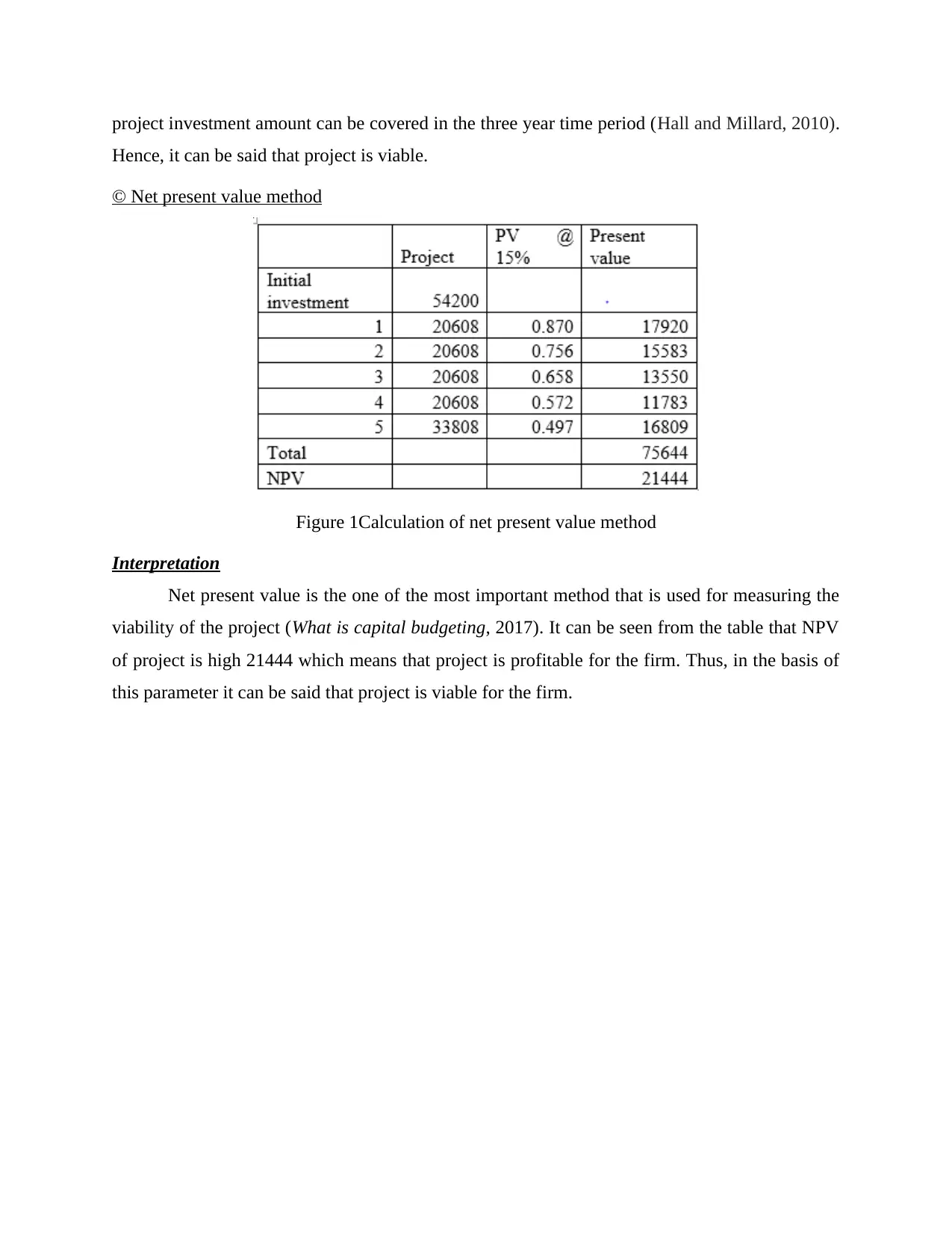

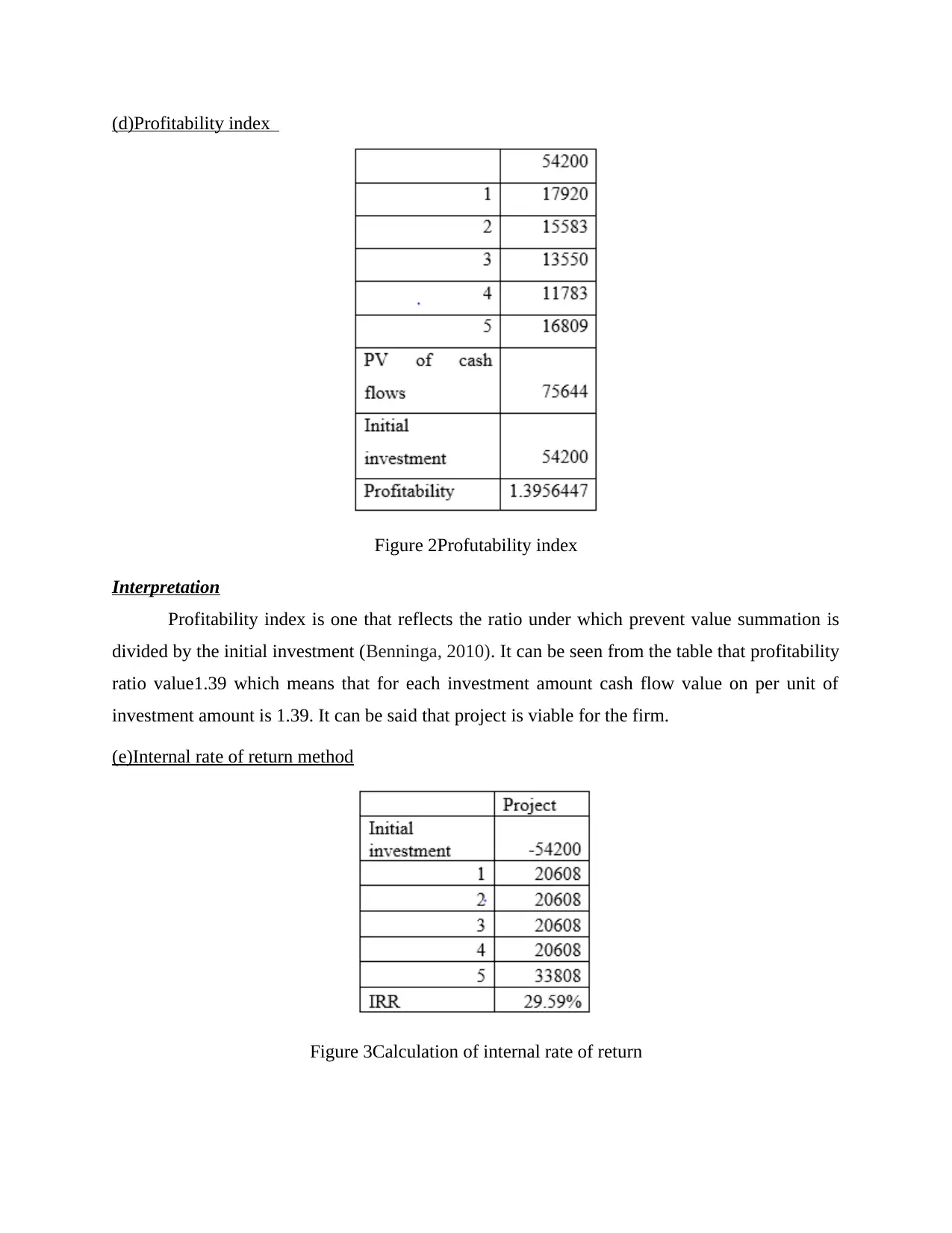

This report, prepared for an ACC515 Accounting and Finance course, delves into the critical aspects of capital budgeting, emphasizing the importance of ethical considerations in the process. It begins by highlighting the necessity of ethical practices when evaluating projects and making financial projections. The report then proceeds to calculate the weighted average cost of capital (WACC) using provided data and assumptions, which is crucial for determining the discount rate. Furthermore, the report applies various project evaluation methods, including the payback period, discounted payback period, net present value (NPV), profitability index, and internal rate of return (IRR), to assess the viability of a hypothetical project. Through these calculations and interpretations, the report provides a comprehensive analysis of the project's financial performance, offering insights into its potential profitability and risk. The report concludes by summarizing the significance of project budgeting methods and the importance of ethical considerations in financial decision-making.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.