An Analysis of the European Sovereign Debt Crisis and Market Impacts

VerifiedAdded on 2020/04/01

|10

|2260

|199

Report

AI Summary

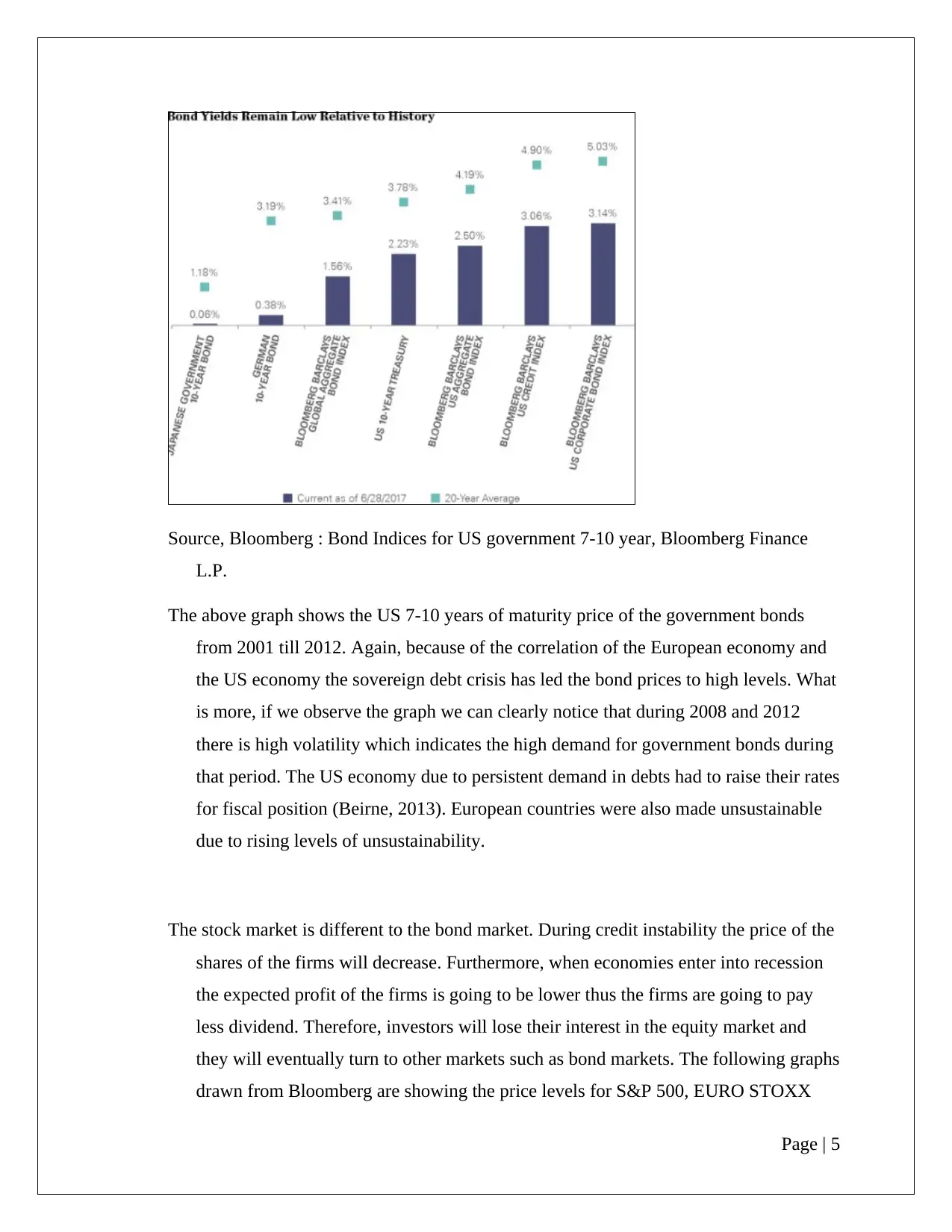

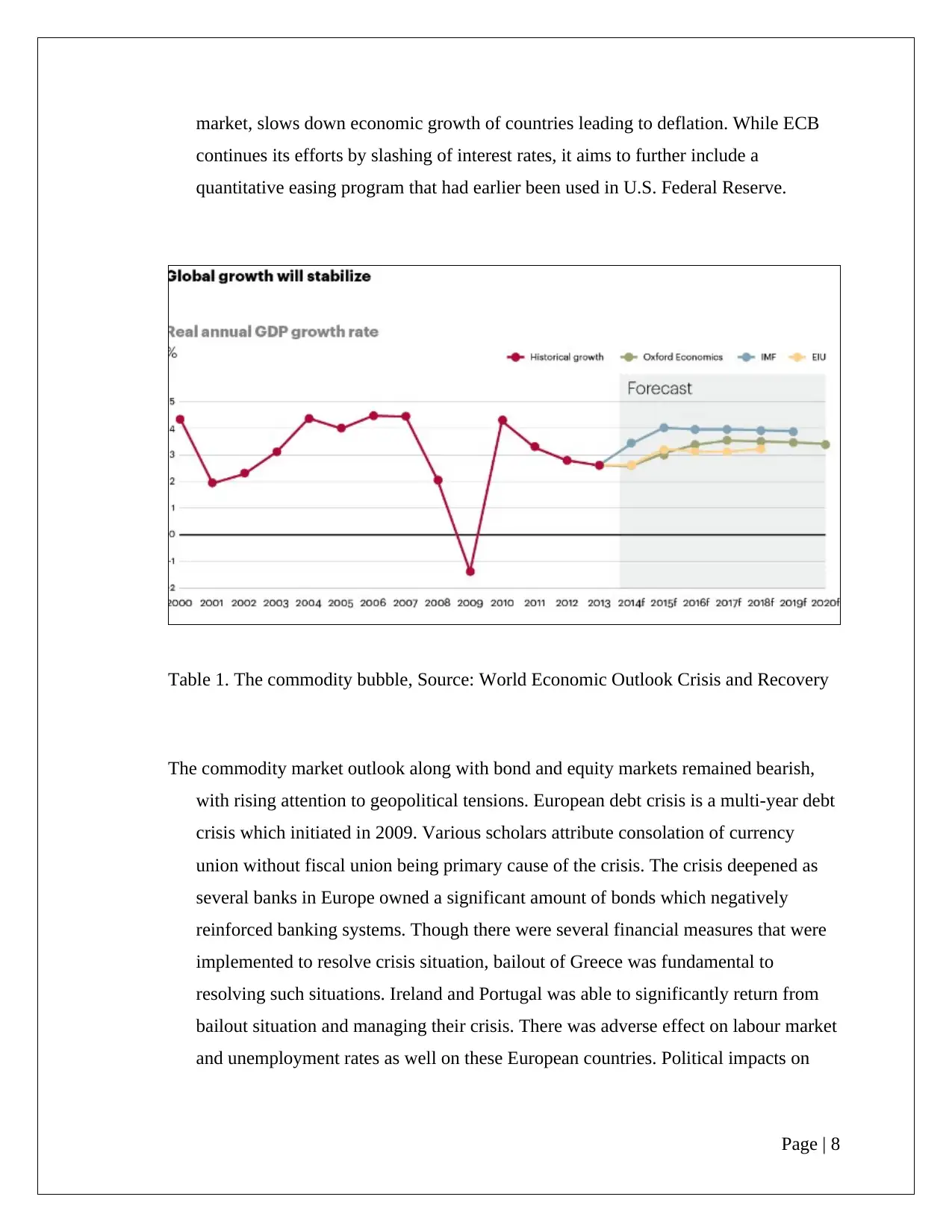

The report delves into the European Sovereign Debt Crisis, examining its profound impact on various financial markets. The crisis, originating from factors like fiscal strains in countries like Greece, led to increased bond yield spreads, market volatility, and a decline in investor confidence. The report highlights the cyclical nature of the crisis, with bailouts from the EU and IMF, and the subsequent shifts in investment from stock to bond markets. It analyzes the effects on different markets, including the bond, stock, and commodity markets. The report examines the impact on the US economy and the global financial markets and discusses implications on commodity prices, oil prices, and the political landscape of the European nations. The analysis includes the volatility in equity markets, panic selling, and the responses of central banks. The report concludes by underscoring the multi-year nature of the crisis and its lasting effects on the European economy and the world. The report also references the impacts on the labor market and unemployment rates in the affected European countries.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.