Strategic Management Accounting: Financial Analysis of Westpac

VerifiedAdded on 2023/06/12

|8

|1224

|311

Report

AI Summary

This report provides a comprehensive financial performance evaluation of Westpac Banking Corporation using strategic management accounting principles. It assesses liquidity, activity, profitability, and leverage ratios derived from Westpac's 2017 annual report, including the current ratio, ROA, ROE, ...

Running head: STRATEGIC MANAGEMENT ACCOUNTING 1

STRATEGIC MANAGEMENT ACCOUNTING

Institution

Student

Course

Date

STRATEGIC MANAGEMENT ACCOUNTING

Institution

Student

Course

Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

STRATEGIC MANAGEMENT ACCOUNTING 2

3. Evaluate the performance of the company (you can use financial and management

accounting information). NB Performance can be assessed from the perspective of different

stakeholders.

Evaluating financial performance involves the process of quantifying the outcomes of a

company’s policies and operations in monetary terms. Other texts present financial performance

as a subjective measure of efficiently a firm utilizes its assets to create revenues. The term’s

broad approach encompasses the view that it is the measure of a firm’s overall financial health

over a given time frame. Financial statements analysis is the most objective method to evaluate

the financial performance of a given company. The analysis involves assessing a variety of

financial ratios which are principally used as tools for financial analysis. They include

profitability ratios, leverage or gearing ratios, activity ratios and liquidity ratios (Dev & Rao,

2006). They all seek to measure the financial performance of a company under different areas of

interest. Every company is comprised of a number of stakeholders; the management, customers,

creditors, employees, investors, the government and general public among others who all attach a

specific interest in following and tracking that particular company’s performance.

Information that is used in financial statements analysis is derived from the company’s annual

report. All public companies are required by law to publish and provide this document to its

stakeholders containing therein audited, signed, accurate and reliable financial statements to

inform their decision making. The major financial statements required in this analysis are the;

Statement of Comprehensive Income (Income Statement), Cash Flow Statements, and the

Statement of Financial Position or the Balance Sheet (Ittelson, 2011).

3. Evaluate the performance of the company (you can use financial and management

accounting information). NB Performance can be assessed from the perspective of different

stakeholders.

Evaluating financial performance involves the process of quantifying the outcomes of a

company’s policies and operations in monetary terms. Other texts present financial performance

as a subjective measure of efficiently a firm utilizes its assets to create revenues. The term’s

broad approach encompasses the view that it is the measure of a firm’s overall financial health

over a given time frame. Financial statements analysis is the most objective method to evaluate

the financial performance of a given company. The analysis involves assessing a variety of

financial ratios which are principally used as tools for financial analysis. They include

profitability ratios, leverage or gearing ratios, activity ratios and liquidity ratios (Dev & Rao,

2006). They all seek to measure the financial performance of a company under different areas of

interest. Every company is comprised of a number of stakeholders; the management, customers,

creditors, employees, investors, the government and general public among others who all attach a

specific interest in following and tracking that particular company’s performance.

Information that is used in financial statements analysis is derived from the company’s annual

report. All public companies are required by law to publish and provide this document to its

stakeholders containing therein audited, signed, accurate and reliable financial statements to

inform their decision making. The major financial statements required in this analysis are the;

Statement of Comprehensive Income (Income Statement), Cash Flow Statements, and the

Statement of Financial Position or the Balance Sheet (Ittelson, 2011).

STRATEGIC MANAGEMENT ACCOUNTING 3

The 2017 Westpac Annual Report, the consolidated Westpac Banking Corporation as at 30th

September 2017 attached herein in the appendix guides the following financial statements

analysis;

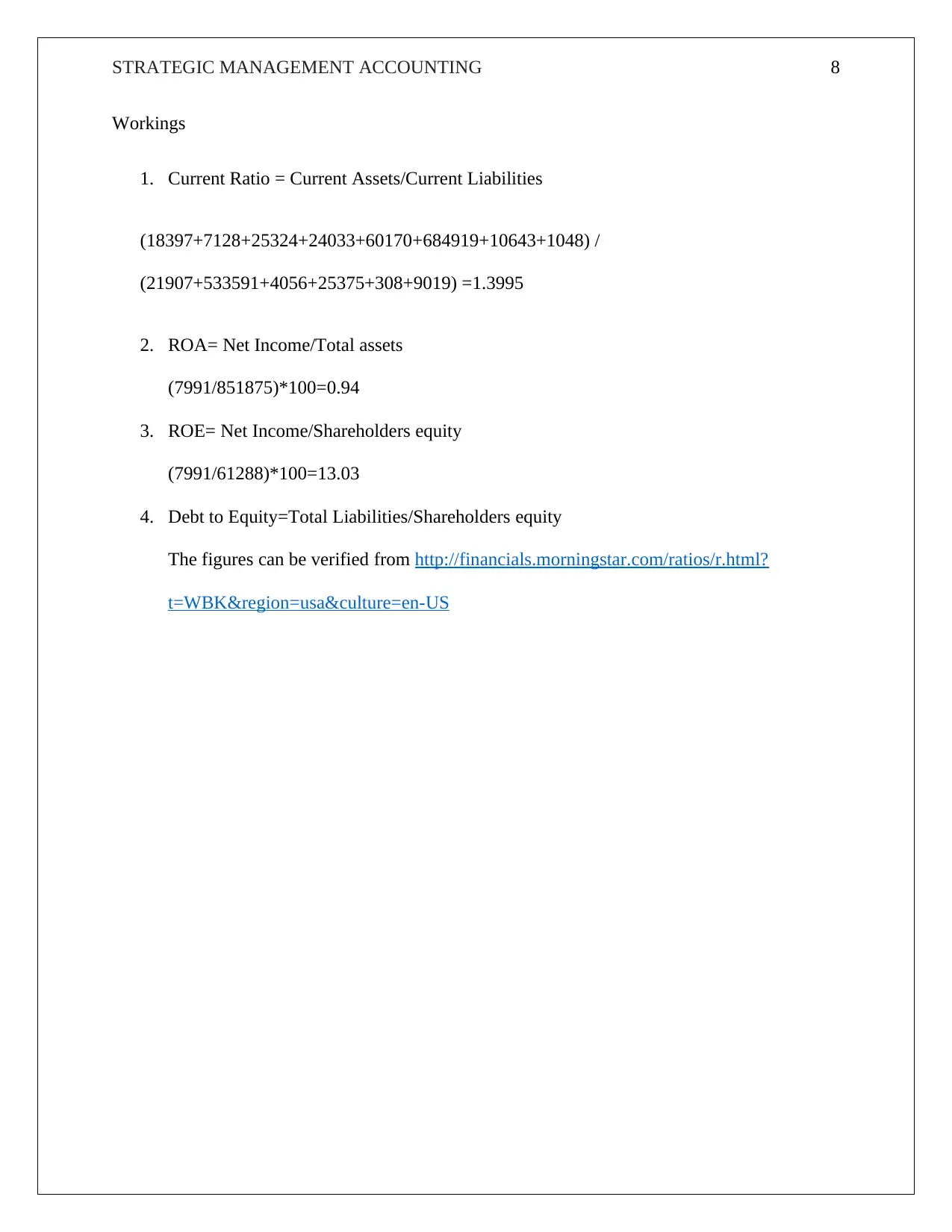

Liquidity Ratios

The major ratios assessed here are the Current and quick ratios. The current ratio also the

working capital ratio is simply current assets divided by current liabilities. Current ratio

measures a firm’s capability to meet both short term and long term maturing obligations.

Westpac has a current ratio of 1.3995 and this has the implication that the firm is in a position to

meet its short-term obligations since its current assets are greater than the current liabilities.

Quick ratio/ acid test ratio has current assets, marketable securities and accounts receivables on

the numerator. It reflects a firm's capability to settle its short-term debts. Creditors of the firm

find this ratio particularly useful in determining whether the company will be able to settle dues

for supplies made (Leach, 2010).

Activity/ Efficiency Ratios

The Fixed Asset turnover and Sales per revenue are used in this analysis. The fixed asset

turnover ratio reflects how well the firm is using its fixed assets to create sales. It utilizes

information from both the income statement and the balance sheet (Leach, 2010). Westpac

posted a fixed asset turnover of 13.34%. The interpretation of this metric only gains valuable

meaning when a comparison with other firms in the same industry is conducted. However, higher

ratios of fixed asset turnover signify greater efficiency in managing the fixed assets to generate

sales. Management gains insight from this metric by putting in place efficient use of fixed assets

to generate sales (Rappaport, 1986).

The 2017 Westpac Annual Report, the consolidated Westpac Banking Corporation as at 30th

September 2017 attached herein in the appendix guides the following financial statements

analysis;

Liquidity Ratios

The major ratios assessed here are the Current and quick ratios. The current ratio also the

working capital ratio is simply current assets divided by current liabilities. Current ratio

measures a firm’s capability to meet both short term and long term maturing obligations.

Westpac has a current ratio of 1.3995 and this has the implication that the firm is in a position to

meet its short-term obligations since its current assets are greater than the current liabilities.

Quick ratio/ acid test ratio has current assets, marketable securities and accounts receivables on

the numerator. It reflects a firm's capability to settle its short-term debts. Creditors of the firm

find this ratio particularly useful in determining whether the company will be able to settle dues

for supplies made (Leach, 2010).

Activity/ Efficiency Ratios

The Fixed Asset turnover and Sales per revenue are used in this analysis. The fixed asset

turnover ratio reflects how well the firm is using its fixed assets to create sales. It utilizes

information from both the income statement and the balance sheet (Leach, 2010). Westpac

posted a fixed asset turnover of 13.34%. The interpretation of this metric only gains valuable

meaning when a comparison with other firms in the same industry is conducted. However, higher

ratios of fixed asset turnover signify greater efficiency in managing the fixed assets to generate

sales. Management gains insight from this metric by putting in place efficient use of fixed assets

to generate sales (Rappaport, 1986).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

STRATEGIC MANAGEMENT ACCOUNTING 4

Profitability Ratios

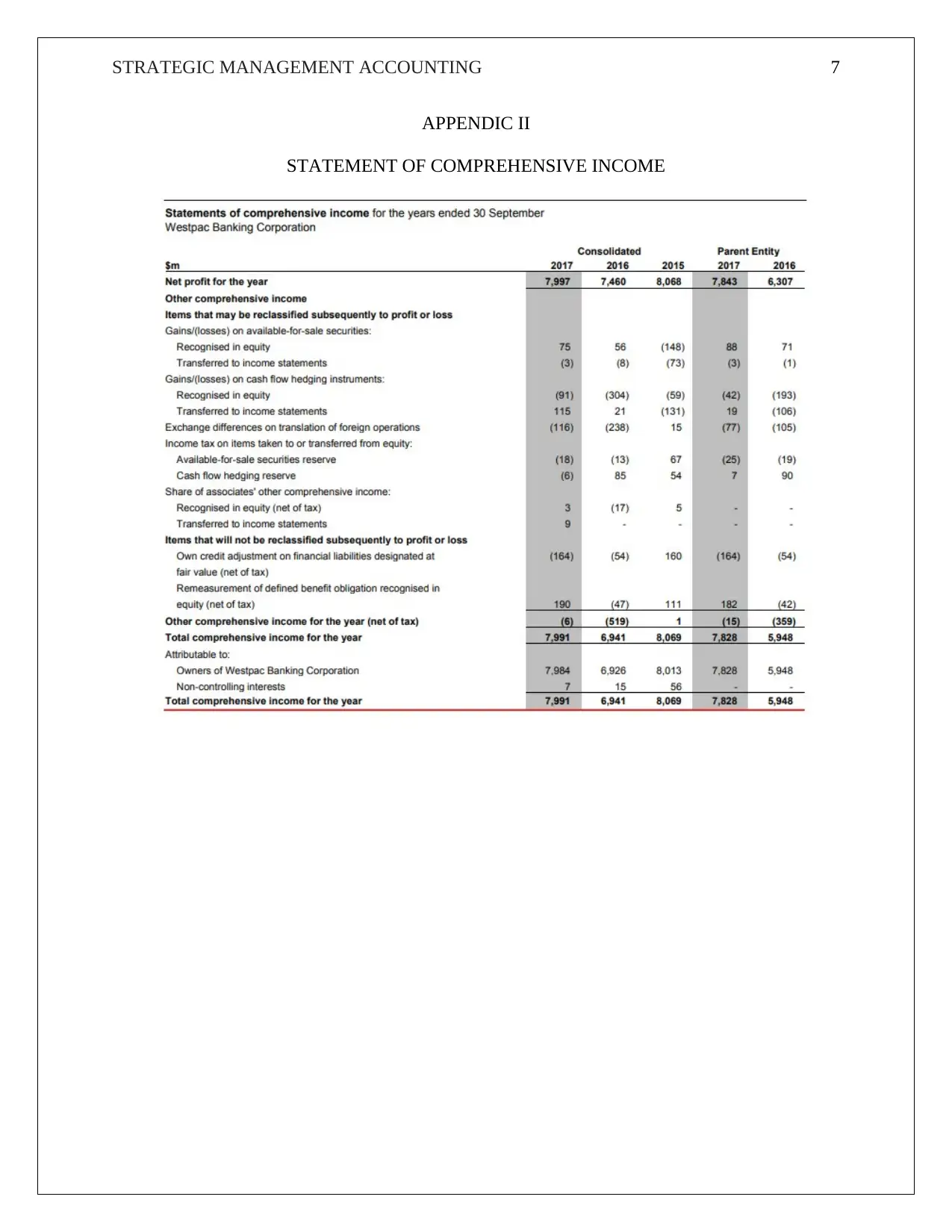

The Return on Assets (ROA) and Return on Equity (ROE) are primarily used in this analysis.

ROA measures how much a dollar invested in assets generates a dollar in terms of revenues.

Specifically, ROA is net income divided by the total assets (European Central Bank, 2010).

Westpac has a ROA of 0.94 which is a rise from previous year’s 0.90. ROA gives the

management, financial specialist, or analysts a thought with respect to how effective an

organization's administration is at utilizing its assets to generate earnings. This is remarkably a

good indicator that the assets of the bank are efficiently utilized. ROE, on the other hand, is the

amount of net income returned as a percentage of the shareholders' equity. Westpac posted a

ROE of 13.03%. It is a return on net worth and indicates that amounts invested by shareholders

yield 13.03% for every dollar invested (Westpac Group, 2017).

Leverage/ Gearing ratios

Debt to Equity and Debt to assets ratios are used in this analysis. Debt to Equity compares a

firm’s ability to pay off debt with a dollar in equity. It is given by total liabilities divided by

shareholders’ equity (Leach, 2010). Westpac posted a debt to equity ratio of 3.04. Although this

metric is industry specific, the ratio here implies that assets of the bank are funded 3-to-1 by

shareholders to creditors. In other words, shareholders account 75% while creditors 25% cents

for every dollar invested in assets (Westpac Group, 2017).

While the financial ratios are good indicators, they only derive valuable meaning when compared

to other players in the banking industry. Banking institutions have in the recent past developed

increasing complexity. However, the fundamental drivers of their performance largely are

incomes, efficiency in operations, risk-taking and leverage (Dev & Rao, 2006).

Profitability Ratios

The Return on Assets (ROA) and Return on Equity (ROE) are primarily used in this analysis.

ROA measures how much a dollar invested in assets generates a dollar in terms of revenues.

Specifically, ROA is net income divided by the total assets (European Central Bank, 2010).

Westpac has a ROA of 0.94 which is a rise from previous year’s 0.90. ROA gives the

management, financial specialist, or analysts a thought with respect to how effective an

organization's administration is at utilizing its assets to generate earnings. This is remarkably a

good indicator that the assets of the bank are efficiently utilized. ROE, on the other hand, is the

amount of net income returned as a percentage of the shareholders' equity. Westpac posted a

ROE of 13.03%. It is a return on net worth and indicates that amounts invested by shareholders

yield 13.03% for every dollar invested (Westpac Group, 2017).

Leverage/ Gearing ratios

Debt to Equity and Debt to assets ratios are used in this analysis. Debt to Equity compares a

firm’s ability to pay off debt with a dollar in equity. It is given by total liabilities divided by

shareholders’ equity (Leach, 2010). Westpac posted a debt to equity ratio of 3.04. Although this

metric is industry specific, the ratio here implies that assets of the bank are funded 3-to-1 by

shareholders to creditors. In other words, shareholders account 75% while creditors 25% cents

for every dollar invested in assets (Westpac Group, 2017).

While the financial ratios are good indicators, they only derive valuable meaning when compared

to other players in the banking industry. Banking institutions have in the recent past developed

increasing complexity. However, the fundamental drivers of their performance largely are

incomes, efficiency in operations, risk-taking and leverage (Dev & Rao, 2006).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

STRATEGIC MANAGEMENT ACCOUNTING 5

REFERENCES

Dev, A. & Rao, V., 2006. Performance Measurement in Financial Institutions in an ERM

framework; A Practitioner Guide. New Delhi: McGraw Hill.

European Central Bank, 2010. Beyond ROE- How to Measure Bank Performance, Frankfurt:

UCB.

Ittelson, T. R., 2011. Financial Statements: A step-by-step Guide to Understanding and Creating

Financial Reports. 2 ed. New Jersey: Career Press Inc.

Leach, R., 2010. Ratios Made Simple: A beginner's guide to the key financial Ratios paperback.

London: Harriman House.

Rappaport, A., 1986. Creating Shareholder Value. New York: The Free Press.

Westpac Group, 2017. Westpac bank Annual Report, Sydney: Westpac Group.

REFERENCES

Dev, A. & Rao, V., 2006. Performance Measurement in Financial Institutions in an ERM

framework; A Practitioner Guide. New Delhi: McGraw Hill.

European Central Bank, 2010. Beyond ROE- How to Measure Bank Performance, Frankfurt:

UCB.

Ittelson, T. R., 2011. Financial Statements: A step-by-step Guide to Understanding and Creating

Financial Reports. 2 ed. New Jersey: Career Press Inc.

Leach, R., 2010. Ratios Made Simple: A beginner's guide to the key financial Ratios paperback.

London: Harriman House.

Rappaport, A., 1986. Creating Shareholder Value. New York: The Free Press.

Westpac Group, 2017. Westpac bank Annual Report, Sydney: Westpac Group.

STRATEGIC MANAGEMENT ACCOUNTING 6

APPENDIX I

STATEMENT OF FINANCIAL POSTION

APPENDIX I

STATEMENT OF FINANCIAL POSTION

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

STRATEGIC MANAGEMENT ACCOUNTING 7

APPENDIC II

STATEMENT OF COMPREHENSIVE INCOME

APPENDIC II

STATEMENT OF COMPREHENSIVE INCOME

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

STRATEGIC MANAGEMENT ACCOUNTING 8

Workings

1. Current Ratio = Current Assets/Current Liabilities

(18397+7128+25324+24033+60170+684919+10643+1048) /

(21907+533591+4056+25375+308+9019) =1.3995

2. ROA= Net Income/Total assets

(7991/851875)*100=0.94

3. ROE= Net Income/Shareholders equity

(7991/61288)*100=13.03

4. Debt to Equity=Total Liabilities/Shareholders equity

The figures can be verified from http://financials.morningstar.com/ratios/r.html?

t=WBK®ion=usa&culture=en-US

Workings

1. Current Ratio = Current Assets/Current Liabilities

(18397+7128+25324+24033+60170+684919+10643+1048) /

(21907+533591+4056+25375+308+9019) =1.3995

2. ROA= Net Income/Total assets

(7991/851875)*100=0.94

3. ROE= Net Income/Shareholders equity

(7991/61288)*100=13.03

4. Debt to Equity=Total Liabilities/Shareholders equity

The figures can be verified from http://financials.morningstar.com/ratios/r.html?

t=WBK®ion=usa&culture=en-US

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.