WaveRider Accounting Report: Financial Analysis and Evaluation

VerifiedAdded on 2023/04/22

|8

|1561

|259

Report

AI Summary

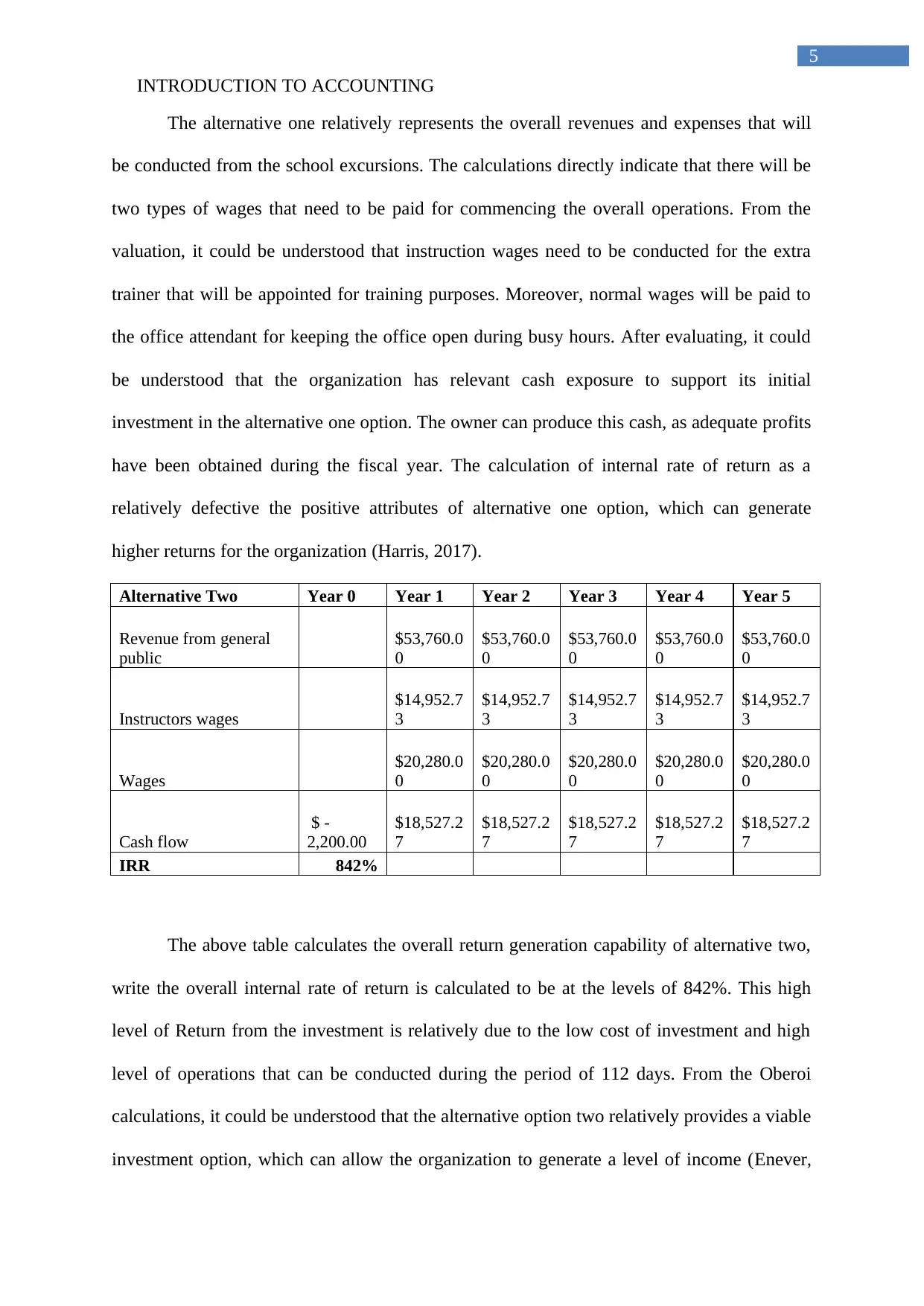

This report presents a financial analysis of WaveRider, a small service business, based on its 2018 financial data. It evaluates the company's profitability, liquidity, and financial stability using various ratios such as gross profit ratio, net profit ratio, current ratio, and debt-to-equity ratio. The report also compares WaveRider's annual turnover range with industry benchmarks, assessing its expense management and operational efficiency. Furthermore, it analyzes two alternative business scenarios, projecting revenues, expenses, and internal rates of return (IRR) to determine their viability and potential for generating income. The analysis suggests that WaveRider has adequate cash flow to support both alternatives, offering opportunities for long-term returns. This document is available on Desklib, a platform providing a wide range of study tools for students.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.