Financial Statement Analysis and Evaluation Report, Semester 1

VerifiedAdded on 2019/09/13

|8

|1103

|320

Report

AI Summary

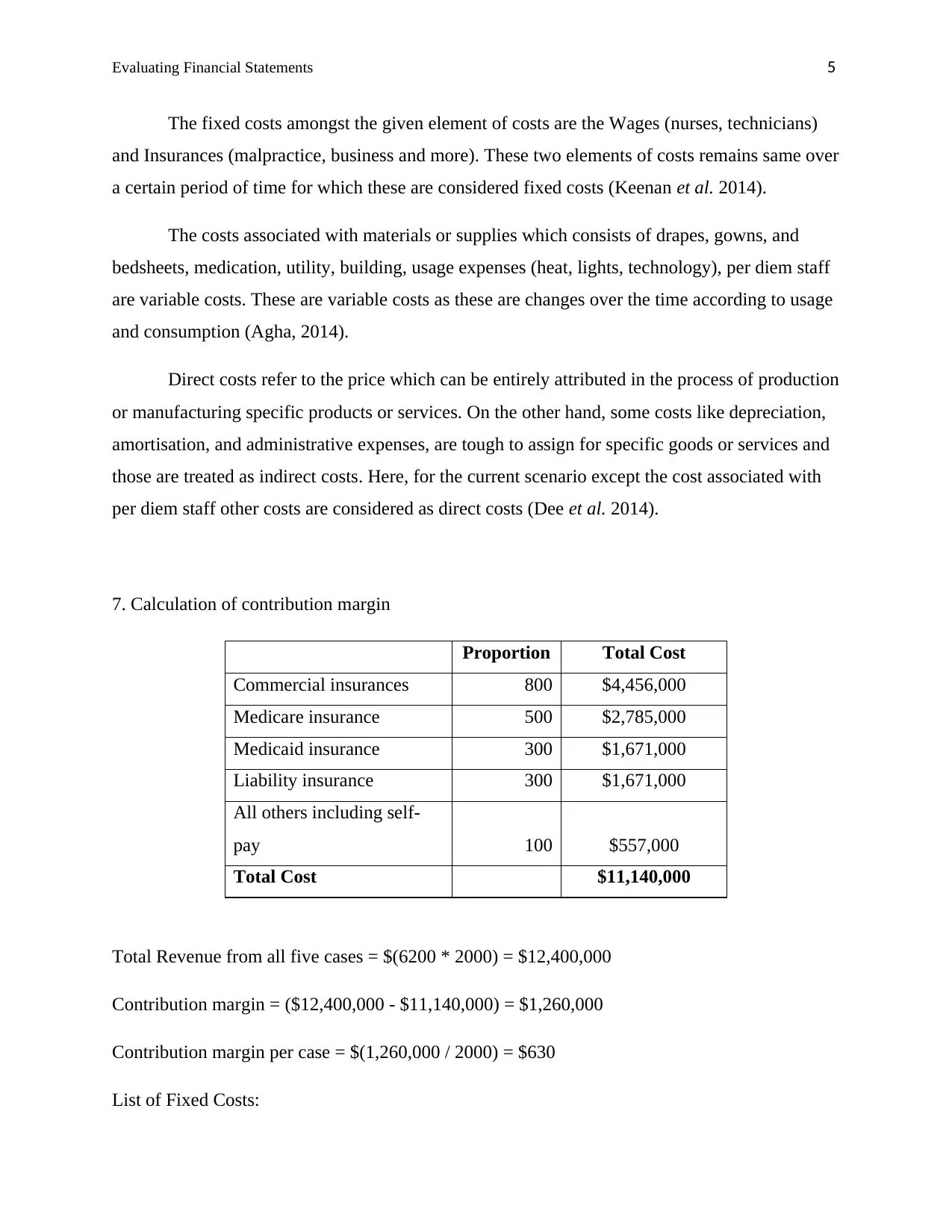

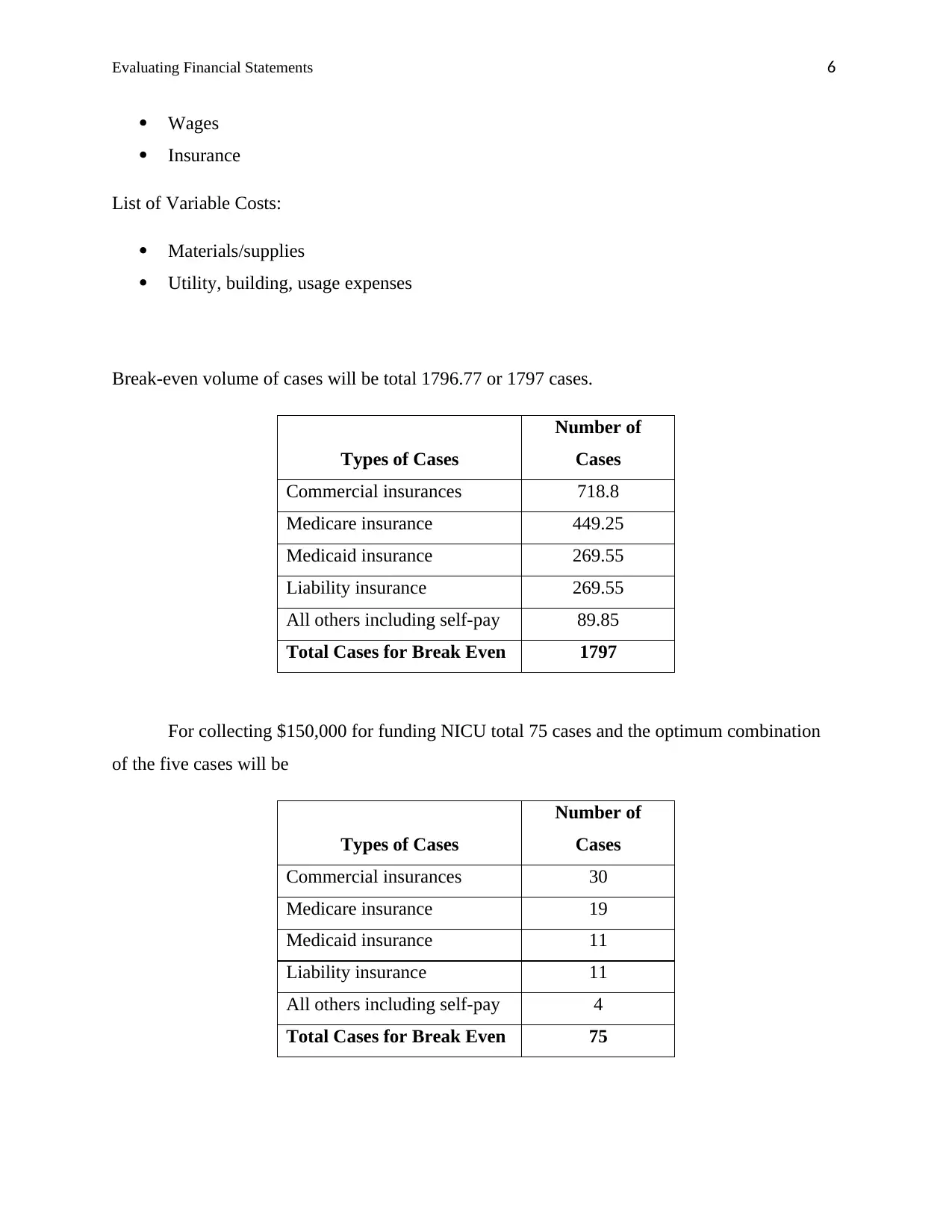

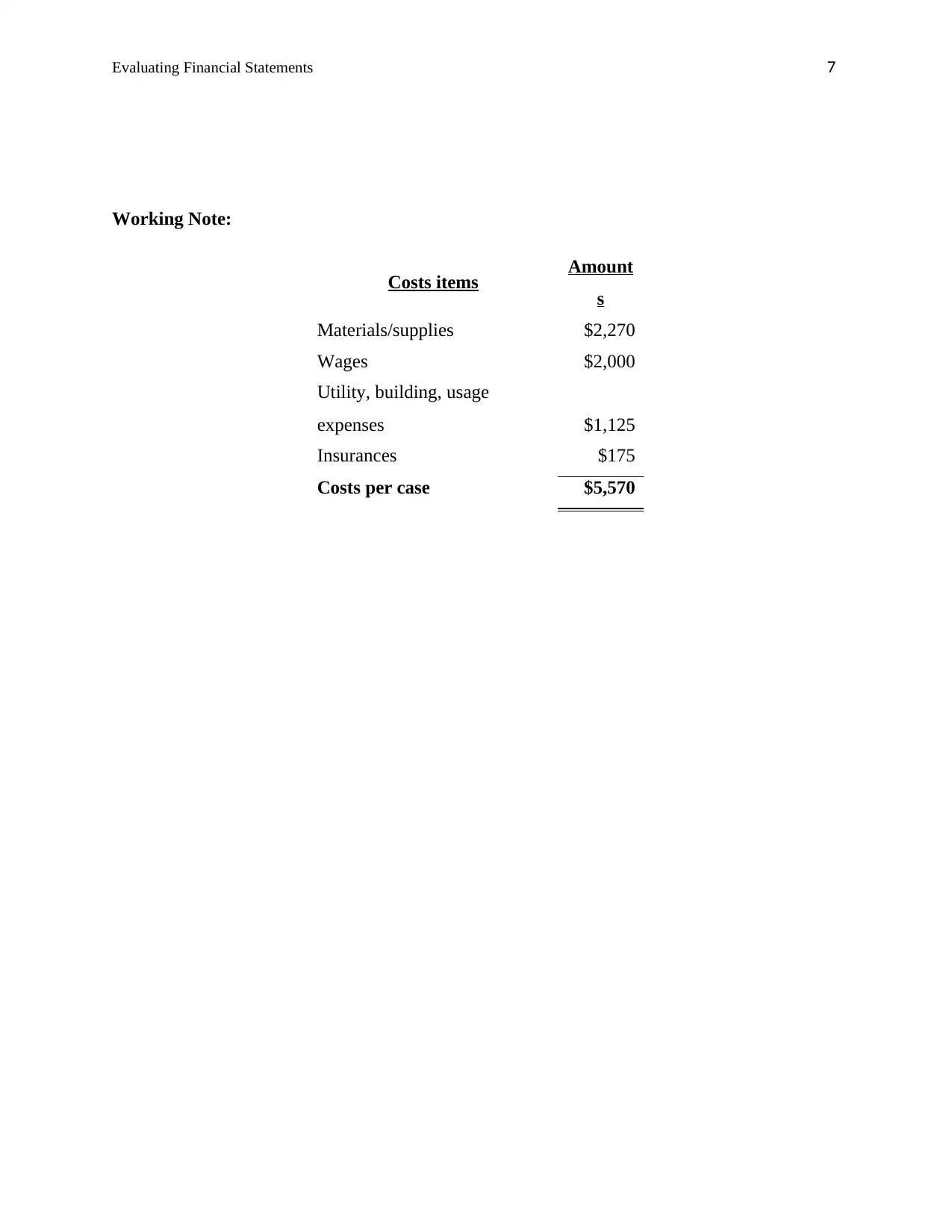

This report presents a comprehensive analysis of financial statements, focusing on the evaluation of different payers and their associated reimbursement rates. The analysis includes the computation of payer proportions, individual reimbursement rates, and the expected rates. The report calculates total charges based on a changed rate of services, highlighting the difference in A/R rates and their implications. It identifies fixed and variable costs, calculates the contribution margin, and determines the break-even volume of cases. Furthermore, the report includes the calculation for funding a NICU. The report offers insights into the financial aspects of healthcare, including payer mix, cost structures, and profitability analysis.

1 out of 8

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.