Comprehensive Analysis of UK Housing Market Trends: 2009-2019, BABS

VerifiedAdded on 2023/01/10

|12

|3770

|84

Report

AI Summary

This report provides a comprehensive analysis of the UK housing market from 2009 to 2019. It examines the changes in average house prices, highlighting significant increases and regional variations across the UK. The report delves into the economic determinants influencing these changes, including interest rates, economic growth, customer confidence, mortgage availability, and supply dynamics. Furthermore, it assesses the effects of government actions and policies on the housing market, evaluating their impact on market trends. The report also explores the impact of the Coronavirus (COVID-19) pandemic on the UK housing industry, analyzing its effects on market operations and providing insights into strategies for organizations to gain a competitive edge. Through this analysis, the report offers a detailed understanding of the complex interplay of factors shaping the UK housing market over the past decade.

Evaluating Internal

and External

Business

Environment

and External

Business

Environment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

Changes in Average House Prices in UK from 2009 to 2019.....................................................3

Economic Determinants of the Changes in Average Housing Prices from 2009 to 2019...........5

Effects of Government’s Actions on the Housing Markets of UK from 2009 to 2019...............7

Impact of Coronavirus (COVID-19) on the Housing Markets of UK.........................................8

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

Changes in Average House Prices in UK from 2009 to 2019.....................................................3

Economic Determinants of the Changes in Average Housing Prices from 2009 to 2019...........5

Effects of Government’s Actions on the Housing Markets of UK from 2009 to 2019...............7

Impact of Coronavirus (COVID-19) on the Housing Markets of UK.........................................8

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

Business environment of an organisation or industry refers to all of the external and

internal factors that come to affect how the business operates within the operational industries

including all the operational processes of the business or industry such as management,

customers, supply chain, demand etc. There are present various external and internal factors in

the business environment of the housing industry of UK which have had a severe impact on all

of its operations in the past decade (Agnihotri and Bhattacharya, 2017). This report analyses the

changes in average house prices in the last decade and also evaluates the impact that the UK

government has had on the housing markets of UK. The report assesses the impact that

Coronavirus (COVID-19) has had on the housing industry of UK and evaluates strategies that

can help organisations gain a competitive edge in the current times.

MAIN BODY

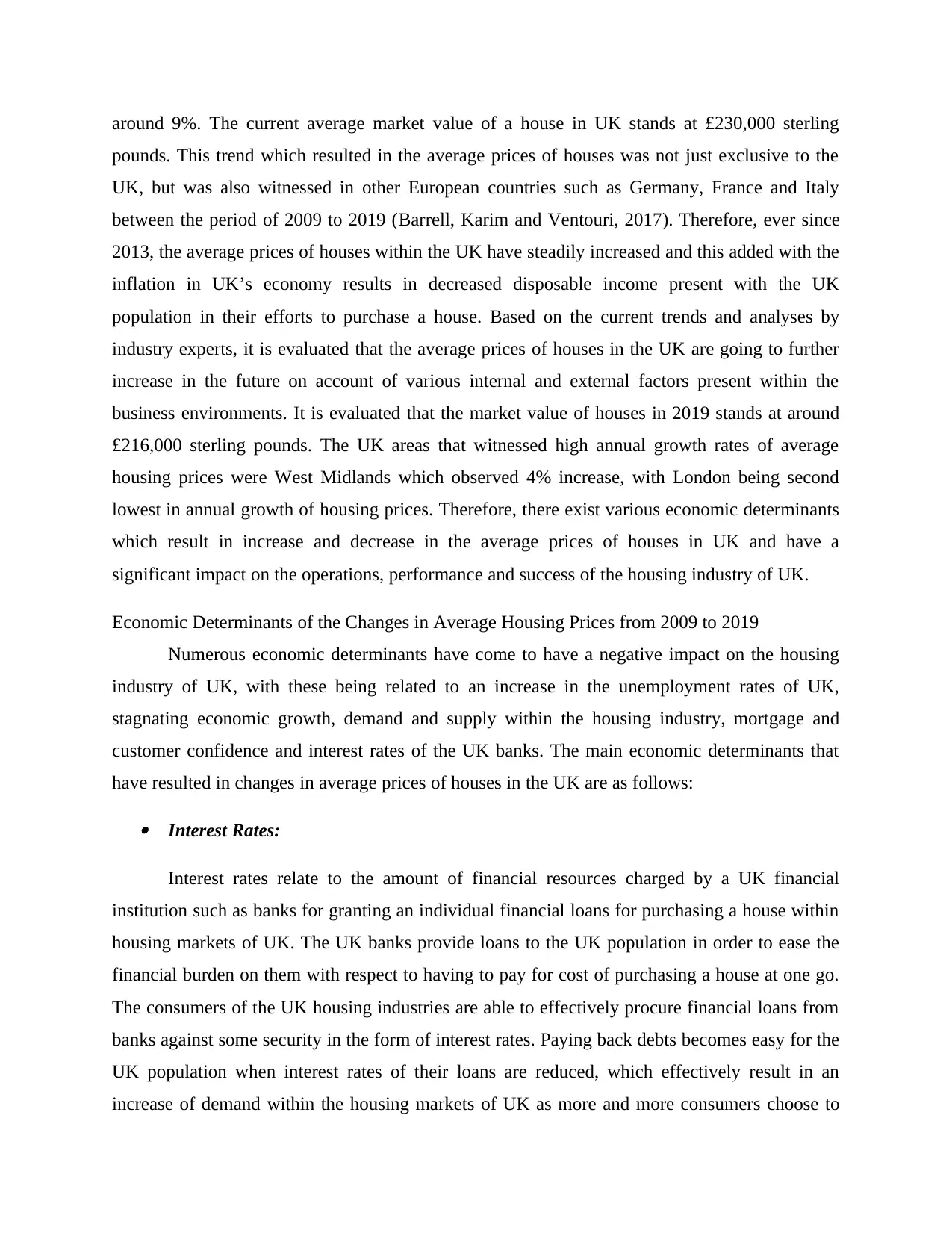

Changes in Average House Prices in UK from 2009 to 2019

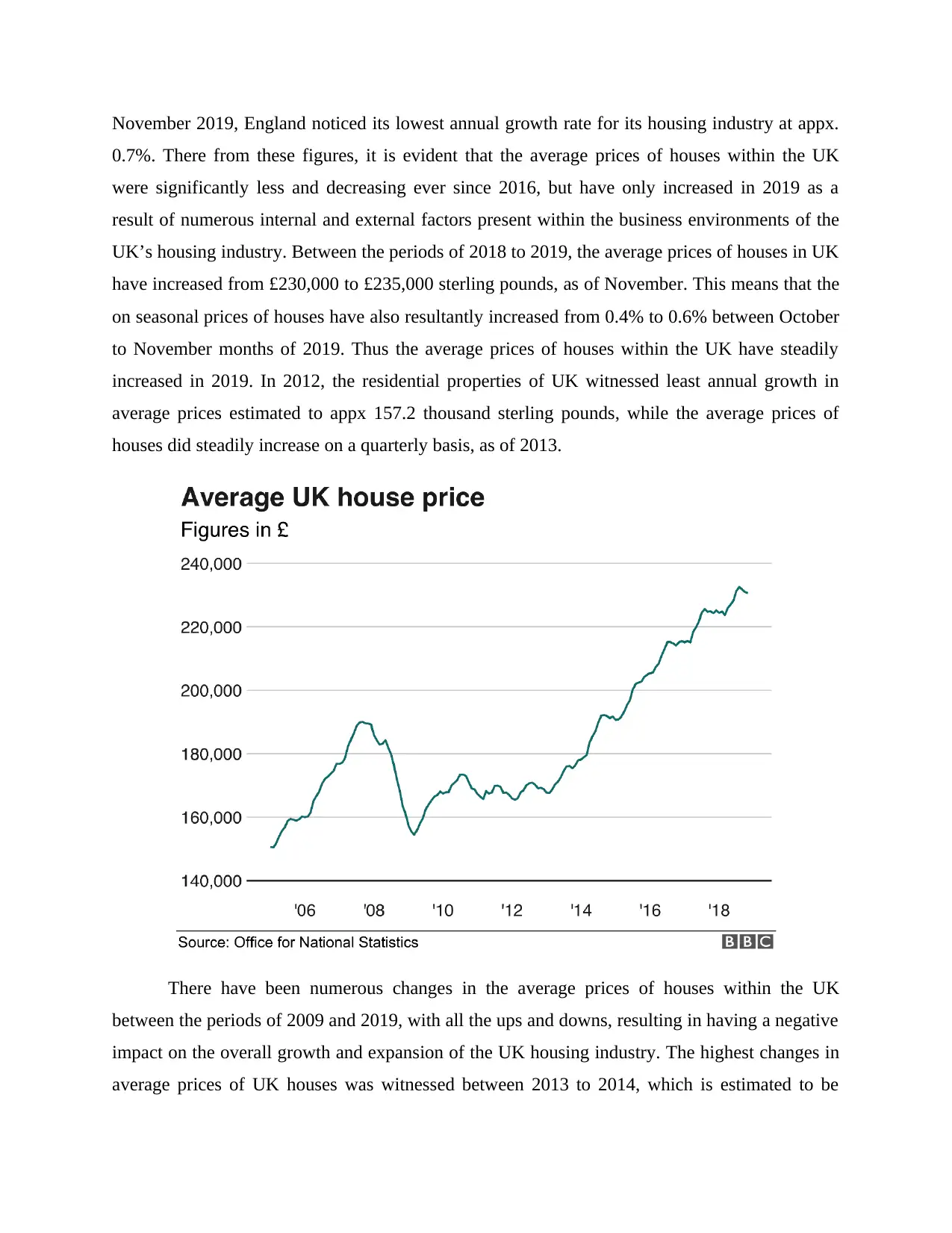

There has been a consistent increase in the average prices of houses in the UK over the

period of ten years from 2009 to 2019. On analysis it is found that the average pries of houses

within the UK have increased from 1.3% as of October to 22% as of November of 2019. The

areas in UK which have observed significant increase in the prices of houses in UK relate to the

West Midland and North West areas of England. Similarly, in Wales that is part of the UK, the

average prices of houses have increased by 7.8% as of 2019, with the average prices of houses

coming out to £173,000 sterling pounds. The average prices of houses in Northern Ireland part of

UK are close to £140,000 pounds. Contrastingly the prices of houses within England are much

higher than of Wales, with the average prices of houses in England coming out to £251,000

sterling pounds. This consistent increase in the average prices of UK houses has resulted in

various opportunities for business organisations and contractors in their objectives of making

increased profits within the housing industry of UK (Auzeby and et.al., 2017). Prior to 2019,

over many years there was observed an effective slow down of the growth of average prices of

houses within the UK, with this trend being more apparent in South and East part of England. In

Business environment of an organisation or industry refers to all of the external and

internal factors that come to affect how the business operates within the operational industries

including all the operational processes of the business or industry such as management,

customers, supply chain, demand etc. There are present various external and internal factors in

the business environment of the housing industry of UK which have had a severe impact on all

of its operations in the past decade (Agnihotri and Bhattacharya, 2017). This report analyses the

changes in average house prices in the last decade and also evaluates the impact that the UK

government has had on the housing markets of UK. The report assesses the impact that

Coronavirus (COVID-19) has had on the housing industry of UK and evaluates strategies that

can help organisations gain a competitive edge in the current times.

MAIN BODY

Changes in Average House Prices in UK from 2009 to 2019

There has been a consistent increase in the average prices of houses in the UK over the

period of ten years from 2009 to 2019. On analysis it is found that the average pries of houses

within the UK have increased from 1.3% as of October to 22% as of November of 2019. The

areas in UK which have observed significant increase in the prices of houses in UK relate to the

West Midland and North West areas of England. Similarly, in Wales that is part of the UK, the

average prices of houses have increased by 7.8% as of 2019, with the average prices of houses

coming out to £173,000 sterling pounds. The average prices of houses in Northern Ireland part of

UK are close to £140,000 pounds. Contrastingly the prices of houses within England are much

higher than of Wales, with the average prices of houses in England coming out to £251,000

sterling pounds. This consistent increase in the average prices of UK houses has resulted in

various opportunities for business organisations and contractors in their objectives of making

increased profits within the housing industry of UK (Auzeby and et.al., 2017). Prior to 2019,

over many years there was observed an effective slow down of the growth of average prices of

houses within the UK, with this trend being more apparent in South and East part of England. In

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

November 2019, England noticed its lowest annual growth rate for its housing industry at appx.

0.7%. There from these figures, it is evident that the average prices of houses within the UK

were significantly less and decreasing ever since 2016, but have only increased in 2019 as a

result of numerous internal and external factors present within the business environments of the

UK’s housing industry. Between the periods of 2018 to 2019, the average prices of houses in UK

have increased from £230,000 to £235,000 sterling pounds, as of November. This means that the

on seasonal prices of houses have also resultantly increased from 0.4% to 0.6% between October

to November months of 2019. Thus the average prices of houses within the UK have steadily

increased in 2019. In 2012, the residential properties of UK witnessed least annual growth in

average prices estimated to appx 157.2 thousand sterling pounds, while the average prices of

houses did steadily increase on a quarterly basis, as of 2013.

There have been numerous changes in the average prices of houses within the UK

between the periods of 2009 and 2019, with all the ups and downs, resulting in having a negative

impact on the overall growth and expansion of the UK housing industry. The highest changes in

average prices of UK houses was witnessed between 2013 to 2014, which is estimated to be

0.7%. There from these figures, it is evident that the average prices of houses within the UK

were significantly less and decreasing ever since 2016, but have only increased in 2019 as a

result of numerous internal and external factors present within the business environments of the

UK’s housing industry. Between the periods of 2018 to 2019, the average prices of houses in UK

have increased from £230,000 to £235,000 sterling pounds, as of November. This means that the

on seasonal prices of houses have also resultantly increased from 0.4% to 0.6% between October

to November months of 2019. Thus the average prices of houses within the UK have steadily

increased in 2019. In 2012, the residential properties of UK witnessed least annual growth in

average prices estimated to appx 157.2 thousand sterling pounds, while the average prices of

houses did steadily increase on a quarterly basis, as of 2013.

There have been numerous changes in the average prices of houses within the UK

between the periods of 2009 and 2019, with all the ups and downs, resulting in having a negative

impact on the overall growth and expansion of the UK housing industry. The highest changes in

average prices of UK houses was witnessed between 2013 to 2014, which is estimated to be

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

around 9%. The current average market value of a house in UK stands at £230,000 sterling

pounds. This trend which resulted in the average prices of houses was not just exclusive to the

UK, but was also witnessed in other European countries such as Germany, France and Italy

between the period of 2009 to 2019 (Barrell, Karim and Ventouri, 2017). Therefore, ever since

2013, the average prices of houses within the UK have steadily increased and this added with the

inflation in UK’s economy results in decreased disposable income present with the UK

population in their efforts to purchase a house. Based on the current trends and analyses by

industry experts, it is evaluated that the average prices of houses in the UK are going to further

increase in the future on account of various internal and external factors present within the

business environments. It is evaluated that the market value of houses in 2019 stands at around

£216,000 sterling pounds. The UK areas that witnessed high annual growth rates of average

housing prices were West Midlands which observed 4% increase, with London being second

lowest in annual growth of housing prices. Therefore, there exist various economic determinants

which result in increase and decrease in the average prices of houses in UK and have a

significant impact on the operations, performance and success of the housing industry of UK.

Economic Determinants of the Changes in Average Housing Prices from 2009 to 2019

Numerous economic determinants have come to have a negative impact on the housing

industry of UK, with these being related to an increase in the unemployment rates of UK,

stagnating economic growth, demand and supply within the housing industry, mortgage and

customer confidence and interest rates of the UK banks. The main economic determinants that

have resulted in changes in average prices of houses in the UK are as follows:

Interest Rates:

Interest rates relate to the amount of financial resources charged by a UK financial

institution such as banks for granting an individual financial loans for purchasing a house within

housing markets of UK. The UK banks provide loans to the UK population in order to ease the

financial burden on them with respect to having to pay for cost of purchasing a house at one go.

The consumers of the UK housing industries are able to effectively procure financial loans from

banks against some security in the form of interest rates. Paying back debts becomes easy for the

UK population when interest rates of their loans are reduced, which effectively result in an

increase of demand within the housing markets of UK as more and more consumers choose to

pounds. This trend which resulted in the average prices of houses was not just exclusive to the

UK, but was also witnessed in other European countries such as Germany, France and Italy

between the period of 2009 to 2019 (Barrell, Karim and Ventouri, 2017). Therefore, ever since

2013, the average prices of houses within the UK have steadily increased and this added with the

inflation in UK’s economy results in decreased disposable income present with the UK

population in their efforts to purchase a house. Based on the current trends and analyses by

industry experts, it is evaluated that the average prices of houses in the UK are going to further

increase in the future on account of various internal and external factors present within the

business environments. It is evaluated that the market value of houses in 2019 stands at around

£216,000 sterling pounds. The UK areas that witnessed high annual growth rates of average

housing prices were West Midlands which observed 4% increase, with London being second

lowest in annual growth of housing prices. Therefore, there exist various economic determinants

which result in increase and decrease in the average prices of houses in UK and have a

significant impact on the operations, performance and success of the housing industry of UK.

Economic Determinants of the Changes in Average Housing Prices from 2009 to 2019

Numerous economic determinants have come to have a negative impact on the housing

industry of UK, with these being related to an increase in the unemployment rates of UK,

stagnating economic growth, demand and supply within the housing industry, mortgage and

customer confidence and interest rates of the UK banks. The main economic determinants that

have resulted in changes in average prices of houses in the UK are as follows:

Interest Rates:

Interest rates relate to the amount of financial resources charged by a UK financial

institution such as banks for granting an individual financial loans for purchasing a house within

housing markets of UK. The UK banks provide loans to the UK population in order to ease the

financial burden on them with respect to having to pay for cost of purchasing a house at one go.

The consumers of the UK housing industries are able to effectively procure financial loans from

banks against some security in the form of interest rates. Paying back debts becomes easy for the

UK population when interest rates of their loans are reduced, which effectively result in an

increase of demand within the housing markets of UK as more and more consumers choose to

opt for taking a loan on reduced interests rates and being assured that they would be able to pay

back the loan and interest without much trouble (Benetton, 2018). Contrastingly, when the

interest rates charged by UK banks are increased, it effectively results in a decrease in the

demand within the housing markets of UK as customers do not wish to undertake heavy debts in

their process of purchasing a house, which they might not be able to effectively pay the bank

back. A lack of demand within the UK housing markets results in excess supply being available,

a situation which has an immensely negative impact on the housing industry of UK. As the banks

do not listen to any kinds of excuses from the loaners and demand month timely instalments of

their pay back loans, the interest rates on loans procured by customers of the housing industry of

UK has a significant and immense impact on the operations, prices charged, demand, supply and

success of the housing industry of UK.

Economic Growth:

The UK is one of the fastest growing economies of the entire world, with the quality of

life of the UK population also being proportionally high. High economic growth of UK allows

for its population to possess increased purchasing power on account of having more disposable

personal income to spend on the housing industry of UK. This increased purchasing power of the

UK population increases the overall demand within the housing industry of UK and results in an

increase in the average prices of houses, as the sellers also wish to optimise their profitability

within the housing industry. When the economy of UK is growing fast, then the consumers also

possess increased disposable income, this results in increased demand, and resultantly increases

the average prices of houses within the UK (Claessens, 2017). The UK’s economy has been

witnessing recession from 2012 onwards with this being exacerbated by the proportionally

increasing unemployment rates of the UK population. This has resulted in reduced personal

disposable income being possessed by the UK population, resulting in decreased demand within

the housing industry of UK. Therefore, the economic growth and recession metrics also have a

significant impact on the housing industry of UK and are an economic determinant that result in

changes of average housing prices within the UK.

back the loan and interest without much trouble (Benetton, 2018). Contrastingly, when the

interest rates charged by UK banks are increased, it effectively results in a decrease in the

demand within the housing markets of UK as customers do not wish to undertake heavy debts in

their process of purchasing a house, which they might not be able to effectively pay the bank

back. A lack of demand within the UK housing markets results in excess supply being available,

a situation which has an immensely negative impact on the housing industry of UK. As the banks

do not listen to any kinds of excuses from the loaners and demand month timely instalments of

their pay back loans, the interest rates on loans procured by customers of the housing industry of

UK has a significant and immense impact on the operations, prices charged, demand, supply and

success of the housing industry of UK.

Economic Growth:

The UK is one of the fastest growing economies of the entire world, with the quality of

life of the UK population also being proportionally high. High economic growth of UK allows

for its population to possess increased purchasing power on account of having more disposable

personal income to spend on the housing industry of UK. This increased purchasing power of the

UK population increases the overall demand within the housing industry of UK and results in an

increase in the average prices of houses, as the sellers also wish to optimise their profitability

within the housing industry. When the economy of UK is growing fast, then the consumers also

possess increased disposable income, this results in increased demand, and resultantly increases

the average prices of houses within the UK (Claessens, 2017). The UK’s economy has been

witnessing recession from 2012 onwards with this being exacerbated by the proportionally

increasing unemployment rates of the UK population. This has resulted in reduced personal

disposable income being possessed by the UK population, resulting in decreased demand within

the housing industry of UK. Therefore, the economic growth and recession metrics also have a

significant impact on the housing industry of UK and are an economic determinant that result in

changes of average housing prices within the UK.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Customer Confidence:

Another economic determinant that has a significant impact on the changes in average

housing prices within the housing industry of UK relates to the confidence that its customers

have. Customer confidence relates to the risk taking potential that the customers of housing

industry possess towards purchasing houses in UK. As houses are expensive assets and require

significant risks for the purchasers, the confidence that the customer has towards the asset being

profitable in the long run has an immense impact on their involvement with the housing industry

of UK and influences the average prices of houses in UK. Customer of housing industry need to

be confident that the risk that they take when purchasing a house in UK, in terms of financial

resources invested in the process into the house, will pay off in the long term. The confidence of

customers depends on a variety of other external factors such as the unemployment rate,

economic growth, demand and supply, interest rates, resale value, depreciation costs etc. (Clair

and et.al., 2016). If the economy of UK is booming and interest rates are low, with the resale

value of houses being high at low depreciation costs, then the customers become confident in

their operations within the housing industry of UK and are more inclined to take on calculated

Another economic determinant that has a significant impact on the changes in average

housing prices within the housing industry of UK relates to the confidence that its customers

have. Customer confidence relates to the risk taking potential that the customers of housing

industry possess towards purchasing houses in UK. As houses are expensive assets and require

significant risks for the purchasers, the confidence that the customer has towards the asset being

profitable in the long run has an immense impact on their involvement with the housing industry

of UK and influences the average prices of houses in UK. Customer of housing industry need to

be confident that the risk that they take when purchasing a house in UK, in terms of financial

resources invested in the process into the house, will pay off in the long term. The confidence of

customers depends on a variety of other external factors such as the unemployment rate,

economic growth, demand and supply, interest rates, resale value, depreciation costs etc. (Clair

and et.al., 2016). If the economy of UK is booming and interest rates are low, with the resale

value of houses being high at low depreciation costs, then the customers become confident in

their operations within the housing industry of UK and are more inclined to take on calculated

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

risks. This is how customer confidence impacts the average housing prices of UK in a significant

manner.

Mortgage:

Mortgage is debt instrument through which customers of housing industry of UK can

take on loans from financial institutions of UK by using their real estate property as a collateral.

The availability of mortgages in UK also has a significant impact on customer operations within

the housing industry of UK. Due to economic recession in UK and the shortage of finance, the

mortgage has reduced significantly, which has resulted in the prices of houses in UK also

decreasing. With loans at high interest rates and no mortgages available to the customers, the

demand for the houses goes down in UK, resulting in reduction of their prices as well.

Supply:

Supply metrics also have an immense impact on the average prices of houses within the

UK. When there exists high supply of houses in UK, then the customers have increased choice in

terms of options available and their prices, resulting in the average prices of houses within the

housing industry effectively reducing (Cook and Watson, 2016). On the other hand, when supply

is restricted, a lot of customers have limited choice and have to compete against one another in

order to be able to purchase house in UK, which results in increase of average prices of houses in

UK. The rise of average prices of houses in UK in 2012 can be directly attributed to increased

population resulting in increased demand, while the supply was quite limited.

Effects of Government’s Actions on the Housing Markets of UK from 2009 to 2019

The UK government’s actions have also had a significant impact on the housing

industries between the period of 2009 to 2019. The UK’s economy fluctuate quite a bit in 2008,

facing numerous ups and downs. In 2009 as a direct result of the economic recession of 2008, the

UK housing markets witnessed a significant dip, which also effectively contributed to the

decreased growth of the UK economy and had an adverse impact on development operations

within the country. In 2009, the UK witnessed a financial crisis, which resulted in an increase in

the unemployment rates of the country. This had an adverse impact on the UK population’s per

capita income being reduced, with decreased number of customers from the UK population

choosing to invest into the housing industry of UK. This again had a negative impact on the

manner.

Mortgage:

Mortgage is debt instrument through which customers of housing industry of UK can

take on loans from financial institutions of UK by using their real estate property as a collateral.

The availability of mortgages in UK also has a significant impact on customer operations within

the housing industry of UK. Due to economic recession in UK and the shortage of finance, the

mortgage has reduced significantly, which has resulted in the prices of houses in UK also

decreasing. With loans at high interest rates and no mortgages available to the customers, the

demand for the houses goes down in UK, resulting in reduction of their prices as well.

Supply:

Supply metrics also have an immense impact on the average prices of houses within the

UK. When there exists high supply of houses in UK, then the customers have increased choice in

terms of options available and their prices, resulting in the average prices of houses within the

housing industry effectively reducing (Cook and Watson, 2016). On the other hand, when supply

is restricted, a lot of customers have limited choice and have to compete against one another in

order to be able to purchase house in UK, which results in increase of average prices of houses in

UK. The rise of average prices of houses in UK in 2012 can be directly attributed to increased

population resulting in increased demand, while the supply was quite limited.

Effects of Government’s Actions on the Housing Markets of UK from 2009 to 2019

The UK government’s actions have also had a significant impact on the housing

industries between the period of 2009 to 2019. The UK’s economy fluctuate quite a bit in 2008,

facing numerous ups and downs. In 2009 as a direct result of the economic recession of 2008, the

UK housing markets witnessed a significant dip, which also effectively contributed to the

decreased growth of the UK economy and had an adverse impact on development operations

within the country. In 2009, the UK witnessed a financial crisis, which resulted in an increase in

the unemployment rates of the country. This had an adverse impact on the UK population’s per

capita income being reduced, with decreased number of customers from the UK population

choosing to invest into the housing industry of UK. This again had a negative impact on the

housing industry as the demand for houses by customers effective reduced and prices of houses

resultantly fell severely in 2009. All of the external factors collectively impacted the housing

industry of UK, the market value of the houses also fell considerably, which again had a negative

impact on the UK’s ability to recover from the economic recession (Dorling, 2019). With the

housing markets of UK already witnessing decreased growth and demand from 2006, in 2009,

the number of sales within the housing industry also took a sharp decline based on all the

previously discussed factors and the UK government was forced into taking actions to remedy

the situation.

The UK government intervened and through the public banks, provided increased

customers of housing industry of UK with unsecured loans in order to encourage them towards

taking risk and conducting financial transactions within the housing markets of UK. This was

also done so that the stagnant housing industry of UK can contribute towards the economic

growth and development of the country to recover from the economic recession. The UK

government also reduced the interest rates that banks charged on their financial loans in order to

encourage the UK population to conduct their operations and generate economic profits and

employment opportunities for the UK populations. In addition, the UK government also

increased the local manufacturing and production operations within UK and made efforts to

increase the cash flow of financial resources within its operational markets, in order to

effectively recover from the financial and economic recession (Lea, 2020). With time, due to the

actions taken by the government of UK towards recovering from the adverse effects of the

economic recession, the housing markets of UK were able to operate successfully, witnessing

increased customer demand, sales and profitability. In 2012 the government also created

dedicated schemes to allow for UK population to easily purchase houses by providing them with

decreased interest rates and mortgage options, with zero rate mortgages also having a

significantly positive impact on the overall operations of housing markets of UK.

Impact of Coronavirus (COVID-19) on the Housing Markets of UK

The Coronavirus (COVID-19) has also had an immense impact on all operations of

housing industry within UK. The entire housing industry of UK was closed down by orders of

the UK government from mid march 2020, on account of the spreading virus. This halted all

operations of the housing industry as no UK citizen was allowed to move, switch or rent houses.

resultantly fell severely in 2009. All of the external factors collectively impacted the housing

industry of UK, the market value of the houses also fell considerably, which again had a negative

impact on the UK’s ability to recover from the economic recession (Dorling, 2019). With the

housing markets of UK already witnessing decreased growth and demand from 2006, in 2009,

the number of sales within the housing industry also took a sharp decline based on all the

previously discussed factors and the UK government was forced into taking actions to remedy

the situation.

The UK government intervened and through the public banks, provided increased

customers of housing industry of UK with unsecured loans in order to encourage them towards

taking risk and conducting financial transactions within the housing markets of UK. This was

also done so that the stagnant housing industry of UK can contribute towards the economic

growth and development of the country to recover from the economic recession. The UK

government also reduced the interest rates that banks charged on their financial loans in order to

encourage the UK population to conduct their operations and generate economic profits and

employment opportunities for the UK populations. In addition, the UK government also

increased the local manufacturing and production operations within UK and made efforts to

increase the cash flow of financial resources within its operational markets, in order to

effectively recover from the financial and economic recession (Lea, 2020). With time, due to the

actions taken by the government of UK towards recovering from the adverse effects of the

economic recession, the housing markets of UK were able to operate successfully, witnessing

increased customer demand, sales and profitability. In 2012 the government also created

dedicated schemes to allow for UK population to easily purchase houses by providing them with

decreased interest rates and mortgage options, with zero rate mortgages also having a

significantly positive impact on the overall operations of housing markets of UK.

Impact of Coronavirus (COVID-19) on the Housing Markets of UK

The Coronavirus (COVID-19) has also had an immense impact on all operations of

housing industry within UK. The entire housing industry of UK was closed down by orders of

the UK government from mid march 2020, on account of the spreading virus. This halted all

operations of the housing industry as no UK citizen was allowed to move, switch or rent houses.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

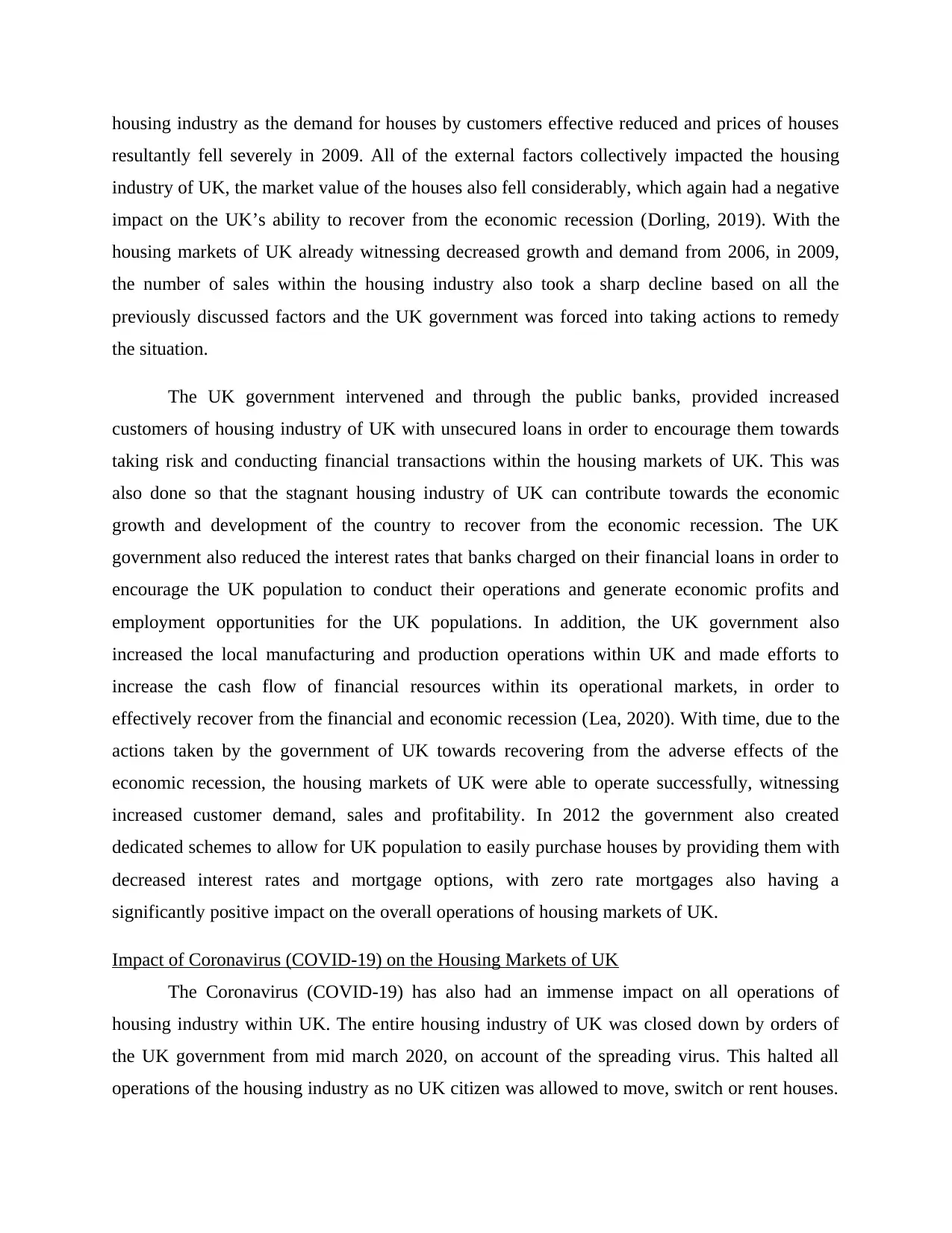

This had an immensely negative impact on the housing industry of UK, with it losing an estimate

of 450,000 distinct financial transactions in this period as a direct result of the spread of the

Coronavirus (COVID-19) pandemic in UK (Mussa, Nwaogu and Pozo, 2017). After the

lockdown, the UK government announced that the housing markets of UK shall reopen to the

customers from May onwards, imposing several safety and health requirements on the daily

operations of purchasers, sellers, vendors, realtors, contractors etc. all of whom operate within

the housing industries of UK.

Figure 1: Fall in number of sales due to COVID-19

Mandatory Guidelines: The UK government issued several guidelines that are mandated to be

followed by all individuals that operate and engage with the housing industry of UK such as

realtors, builders, customers, sellers, agents, surveyors, tenants, landlords etc. These guidelines

mandate that all parties and individuals operating within the housing markets of UK need to

maintain sufficient social distancing between each other. These guidelines also mandate all

individuals to be immensely cautious and careful while conducting any operations related to the

housing industry such as surveying houses, interacting with agents, sellers, customers etc., in

order to prevent the spread of the Coronavirus (COVID-19) due to operations of the housing

of 450,000 distinct financial transactions in this period as a direct result of the spread of the

Coronavirus (COVID-19) pandemic in UK (Mussa, Nwaogu and Pozo, 2017). After the

lockdown, the UK government announced that the housing markets of UK shall reopen to the

customers from May onwards, imposing several safety and health requirements on the daily

operations of purchasers, sellers, vendors, realtors, contractors etc. all of whom operate within

the housing industries of UK.

Figure 1: Fall in number of sales due to COVID-19

Mandatory Guidelines: The UK government issued several guidelines that are mandated to be

followed by all individuals that operate and engage with the housing industry of UK such as

realtors, builders, customers, sellers, agents, surveyors, tenants, landlords etc. These guidelines

mandate that all parties and individuals operating within the housing markets of UK need to

maintain sufficient social distancing between each other. These guidelines also mandate all

individuals to be immensely cautious and careful while conducting any operations related to the

housing industry such as surveying houses, interacting with agents, sellers, customers etc., in

order to prevent the spread of the Coronavirus (COVID-19) due to operations of the housing

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

industry of UK. Additionally, the guidelines mandated by UK government stopped any kind of

open house viewings which tend to attract increased number of people to a specific location,

which can spread the Coronavirus (COVID-19) to significant number of people going to the

open house viewing (Nicola and et.al., 2020). The government also mandated that all initial

viewing of a prospective house be conducted virtually by the customers wherever possible and if

not possible to be done virtually, the limit the number of viewers to a maximum of two

individuals instead of taking the entire family to oversee the prospective house.

Release of Building Demand: Due to the Coronavirus (COVID-19), with the UK being put

under lockdown, all operations of the housing markets of UK effectively were put on hold for

over 2 months, with this resulting in the demand being stalled and built up within the housing

industry of UK. Based on estimates, it is evaluated that Coronavirus (COVID-19) resulted in the

loss of appx 5.9 billion sterling pounds for the housing industry of UK (Saunders and Hotel,

2018). When the lockdown was eased and the operations of the housing industry of UK being

resumed it resulted in release of the built up demand from the past two months with the housing

industry witnessing increased sales and profitability after the lockdown.

CONCLUSION

Based on the findings of the report, it can effectively be concluded that there are several

external and internal factors present in the business environments that have had a significant

impact on the housing industry of UK in the past decade. This report analyses the changes in

prices of houses within the UK over the period of 10 years, from 2009 to 2019. Then the report

evaluates economic determinants of the changes because of which prices of houses have

effectively changed in the past decade. Further the report assesses the impact of UK

government’s actions over the past decade which have come to affect UK housing markets.

Finally, the report evaluates the impact of the Coronavirus (COVID-19) on the housing markets

of UK.

open house viewings which tend to attract increased number of people to a specific location,

which can spread the Coronavirus (COVID-19) to significant number of people going to the

open house viewing (Nicola and et.al., 2020). The government also mandated that all initial

viewing of a prospective house be conducted virtually by the customers wherever possible and if

not possible to be done virtually, the limit the number of viewers to a maximum of two

individuals instead of taking the entire family to oversee the prospective house.

Release of Building Demand: Due to the Coronavirus (COVID-19), with the UK being put

under lockdown, all operations of the housing markets of UK effectively were put on hold for

over 2 months, with this resulting in the demand being stalled and built up within the housing

industry of UK. Based on estimates, it is evaluated that Coronavirus (COVID-19) resulted in the

loss of appx 5.9 billion sterling pounds for the housing industry of UK (Saunders and Hotel,

2018). When the lockdown was eased and the operations of the housing industry of UK being

resumed it resulted in release of the built up demand from the past two months with the housing

industry witnessing increased sales and profitability after the lockdown.

CONCLUSION

Based on the findings of the report, it can effectively be concluded that there are several

external and internal factors present in the business environments that have had a significant

impact on the housing industry of UK in the past decade. This report analyses the changes in

prices of houses within the UK over the period of 10 years, from 2009 to 2019. Then the report

evaluates economic determinants of the changes because of which prices of houses have

effectively changed in the past decade. Further the report assesses the impact of UK

government’s actions over the past decade which have come to affect UK housing markets.

Finally, the report evaluates the impact of the Coronavirus (COVID-19) on the housing markets

of UK.

REFERENCES

Books and Journals

Agnihotri, A. and Bhattacharya, S., 2017. Corporate name change and the market valuation of

firms: Evidence from an emerging market. International Journal of the Economics of

Business, 24(1). pp.73-90.

Auzeby, M and et.al., 2017. Using phase change materials to reduce overheating issues in UK

residential buildings. Energy Procedia, 105. pp.4072-4077.

Barrell, R., Karim, D. and Ventouri, A., 2017. Interest rate liberalization and capital adequacy in

models of financial crises. Journal of Financial Stability, 33. pp.261-272.

Benetton, M., 2018. Leverage regulation and market structure: An empirical model of the uk

mortgage market. Available at SSRN 3247956.

Claessens, S., 2017. Regulation and structural change in financial systems. Centre for Economic

Policy Research.

Clair, A and et.al., 2016. The impact of housing payment problems on health status during

economic recession: A comparative analysis of longitudinal EU SILC data of 27

European states, 2008–2010. SSM-population health. 2. pp.306-316.

Cook, S. and Watson, D., 2016. A new perspective on the ripple effect in the UK housing

market: Comovement, cyclical subsamples and alternative indices. Urban Studies. 53(14).

pp.3048-3062.

Dorling, D., 2019. INFLUENCES AND CONSEQUENCES.

Lea, R., 2020. The coronavirus crisis: the debate shifts towards the exit strategy.

Mussa, A., Nwaogu, U. G. and Pozo, S., 2017. Immigration and housing: A spatial econometric

analysis. Journal of Housing Economics, 35. pp.13-25.

Nicola, M. and et.al., 2020. The Socio-Economic Implications of the Coronavirus and COVID-

19 Pandemic: A Review. International Journal of Surgery.

Saunders, M. and Hotel, M. B. S., 2018. Some effects of demographic change on the UK

Economy.

Books and Journals

Agnihotri, A. and Bhattacharya, S., 2017. Corporate name change and the market valuation of

firms: Evidence from an emerging market. International Journal of the Economics of

Business, 24(1). pp.73-90.

Auzeby, M and et.al., 2017. Using phase change materials to reduce overheating issues in UK

residential buildings. Energy Procedia, 105. pp.4072-4077.

Barrell, R., Karim, D. and Ventouri, A., 2017. Interest rate liberalization and capital adequacy in

models of financial crises. Journal of Financial Stability, 33. pp.261-272.

Benetton, M., 2018. Leverage regulation and market structure: An empirical model of the uk

mortgage market. Available at SSRN 3247956.

Claessens, S., 2017. Regulation and structural change in financial systems. Centre for Economic

Policy Research.

Clair, A and et.al., 2016. The impact of housing payment problems on health status during

economic recession: A comparative analysis of longitudinal EU SILC data of 27

European states, 2008–2010. SSM-population health. 2. pp.306-316.

Cook, S. and Watson, D., 2016. A new perspective on the ripple effect in the UK housing

market: Comovement, cyclical subsamples and alternative indices. Urban Studies. 53(14).

pp.3048-3062.

Dorling, D., 2019. INFLUENCES AND CONSEQUENCES.

Lea, R., 2020. The coronavirus crisis: the debate shifts towards the exit strategy.

Mussa, A., Nwaogu, U. G. and Pozo, S., 2017. Immigration and housing: A spatial econometric

analysis. Journal of Housing Economics, 35. pp.13-25.

Nicola, M. and et.al., 2020. The Socio-Economic Implications of the Coronavirus and COVID-

19 Pandemic: A Review. International Journal of Surgery.

Saunders, M. and Hotel, M. B. S., 2018. Some effects of demographic change on the UK

Economy.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.