MBA Financial Management: Evaluating Aunt Chiara's Business Venture

VerifiedAdded on 2023/04/22

|15

|2969

|371

Report

AI Summary

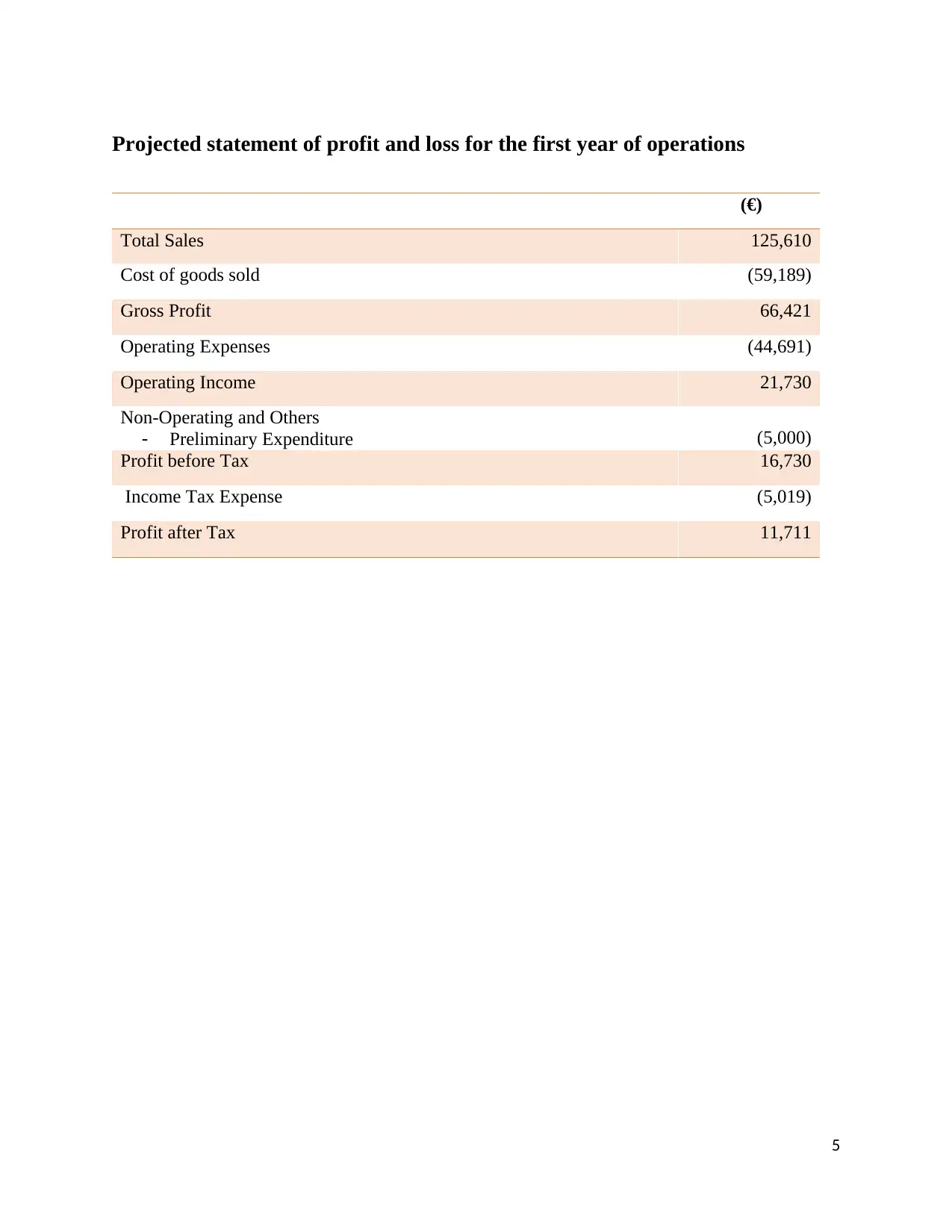

This assignment provides a detailed financial analysis of Aunt Chiara's prospective venture, focusing on the development of a profit and loss statement and a cash budget for the first year of operations. The analysis begins with projected financial statements, including monthly income statements and cost of goods sold calculations, based on various assumptions and estimates related to sales growth, material costs, and operating expenses. Key assumptions include a 16% monthly sales growth, consistent sales to Marco, and a four-year useful life for tangible assets. The report evaluates the venture's profitability, cash flow, and potential risks, such as foreign exchange exposure, and suggests hedging strategies to mitigate these risks. The analysis concludes with a critical appreciation of the venture, highlighting both its potential and areas for improvement. This student-contributed document is available on Desklib, offering valuable insights for students studying financial management.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.