ACC511 Investment Analysis: Project Evaluation for RWE Enterprises

VerifiedAdded on 2023/06/11

|8

|1931

|263

Report

AI Summary

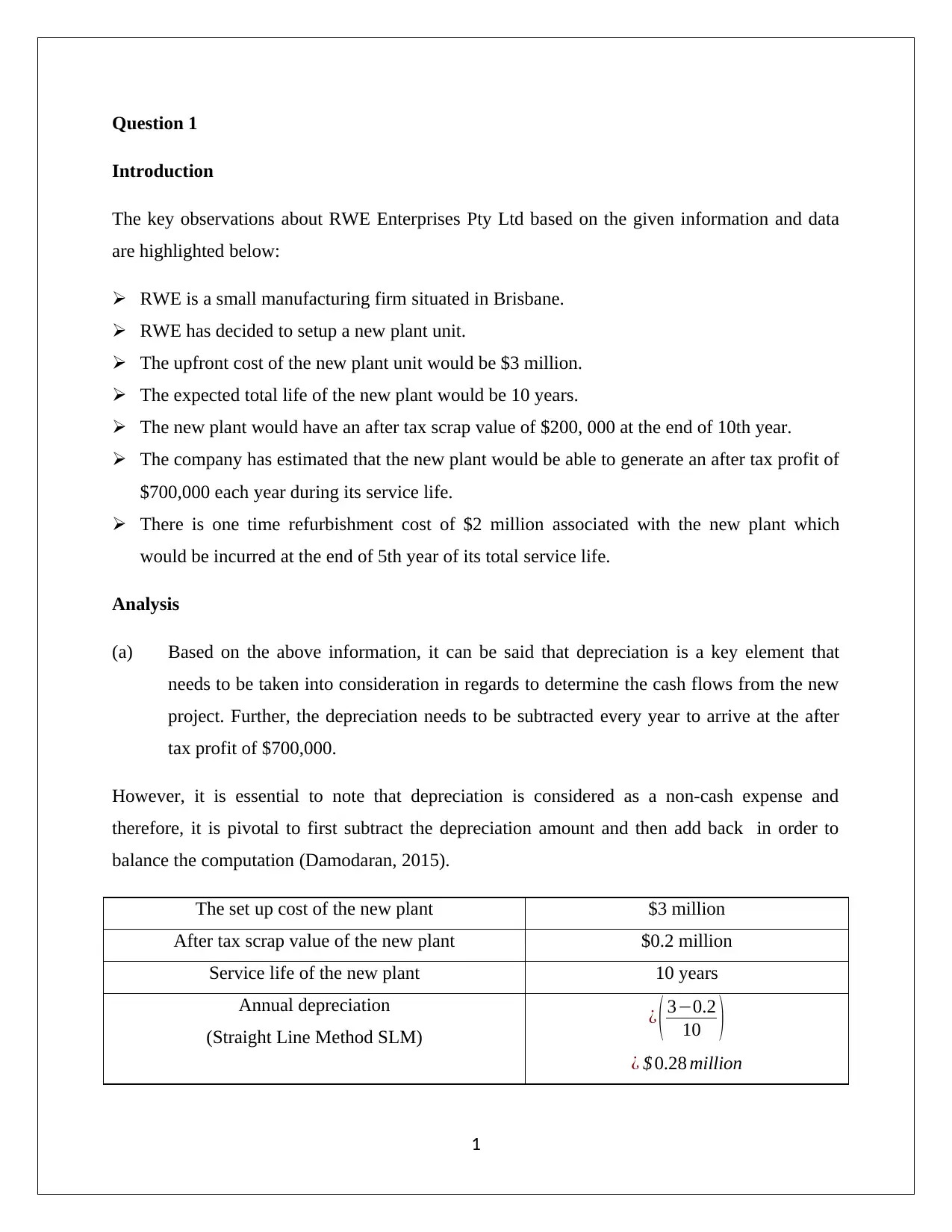

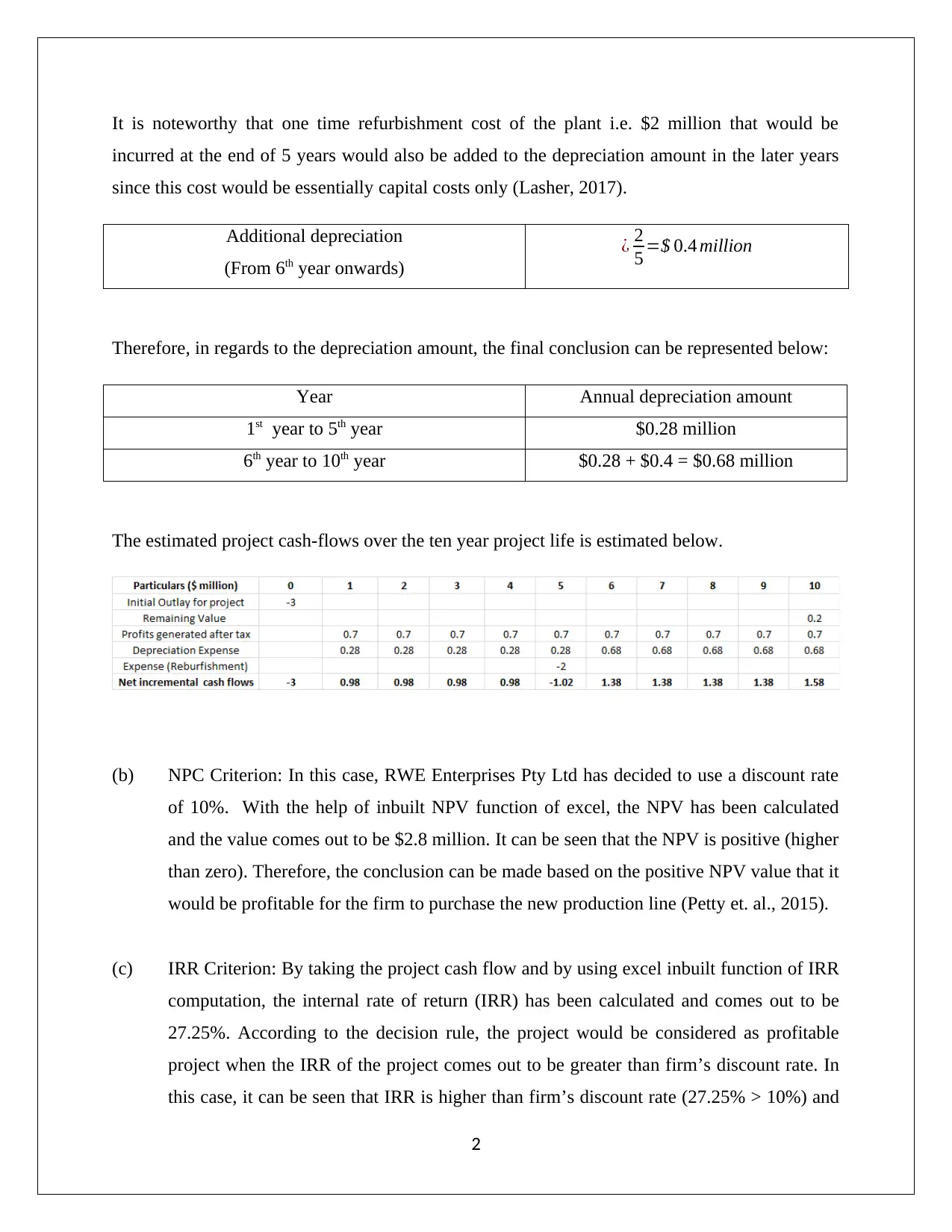

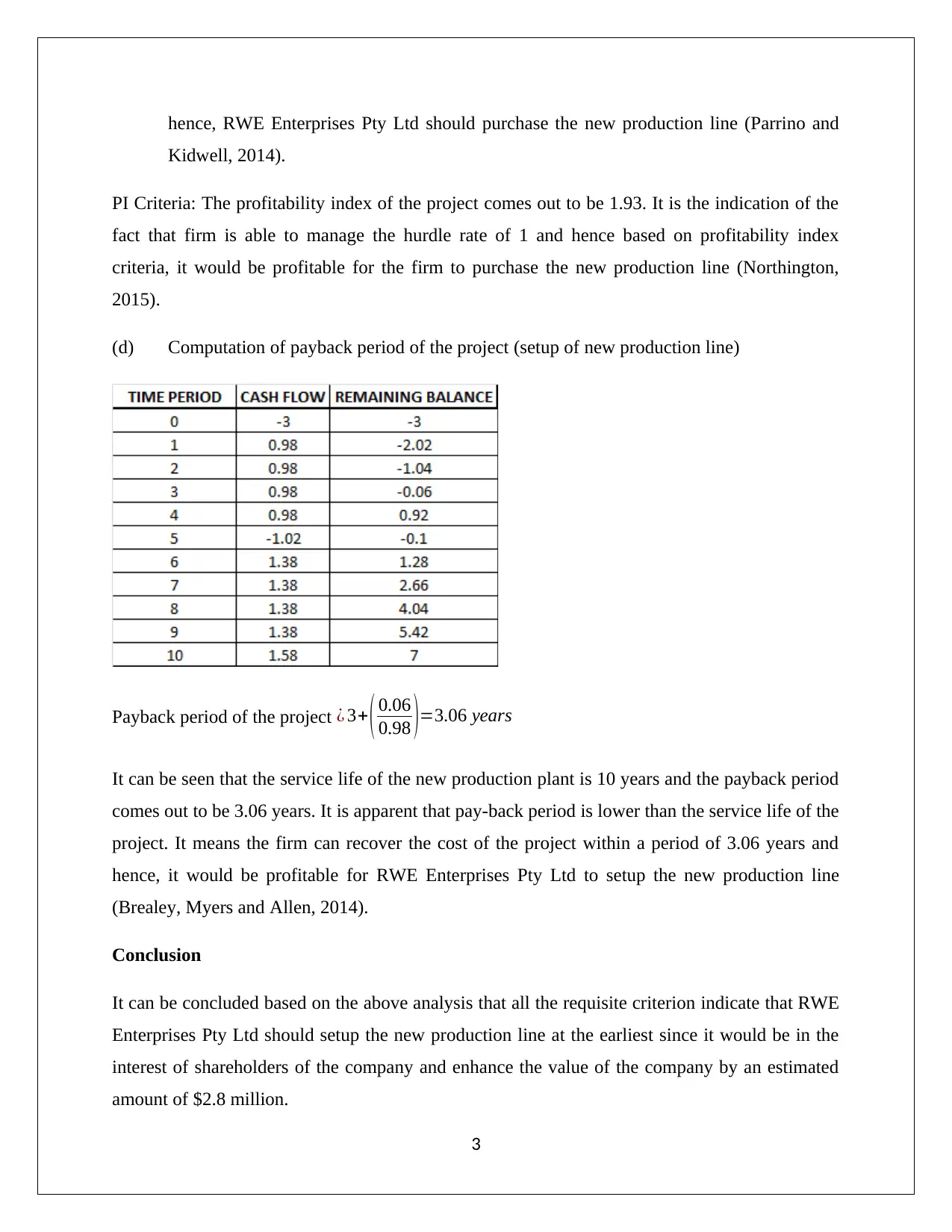

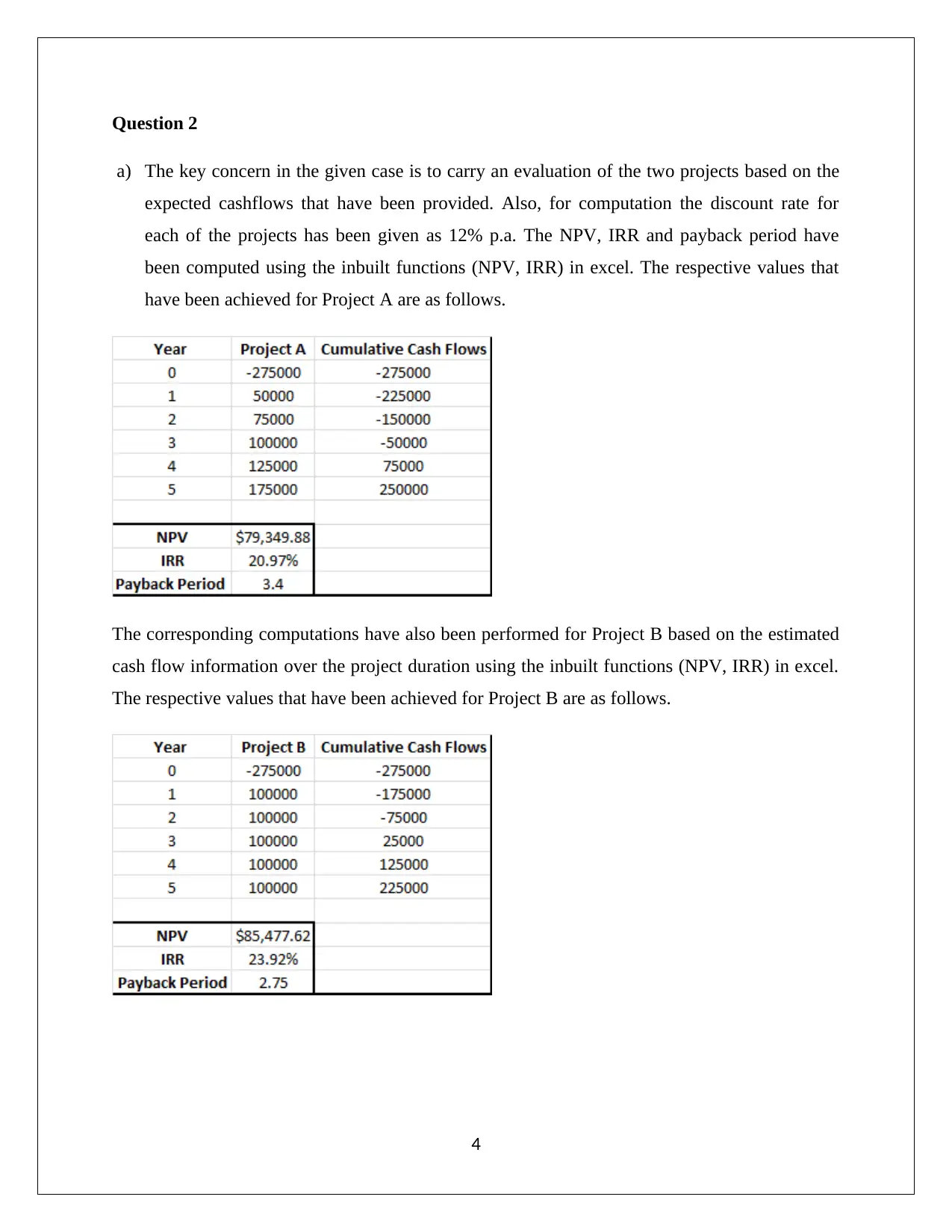

This report provides a detailed project evaluation for RWE Enterprises Pty Ltd, a small manufacturing firm in Brisbane considering setting up a new plant. The analysis includes calculating the Net Present Value (NPV), Internal Rate of Return (IRR), profitability index, and payback period for the proposed plant, considering factors like upfront costs, scrap value, after-tax profits, and refurbishment costs. The report evaluates two projects, A and B, based on their cash flows and acceptability criteria, including NPV, IRR, and payback period. It concludes that Project B is preferable due to its superior ranking across all evaluation metrics. This document is available on Desklib, where students can find a wealth of solved assignments and past papers to aid their studies.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.