Evaluation of Financial Performance and Position of Clariton Antiques

VerifiedAdded on 2020/01/28

STUDENT ID:

ASSIGNMENT ID:

ASSIGNMENT TITLE: EVALUATION OF FINANCIAL

PERFORMACE AND POSITION

1

Paraphrase This Document

Introduction......................................................................................................................................3

Task 1...............................................................................................................................................3

1.1 Identifying the sources of finance available to the business......................................................3

1.2 Assessing the implications of sources of finance......................................................................3

1.3 Evaluating most appropriate sources of finance for Clariton Antiques.....................................4

2.1 Assess and compare the costs of above mentioned sources of finance with reference to.........5

2.2 Explaining the importance of financial planning.......................................................................5

2.3 Describing the information needs of different decision makers................................................6

2.4 Describing the impact on the financial statements with reference to........................................7

Task 3...............................................................................................................................................8

3.1 Analyzing cash budgets for Clariton Antiques and making appropriate decisions...................8

3.2 Explaining how unit costs are calculated to make pricing decisions (giving examples)...........9

3.3 Assessing the viability of a projects using investment appraisal techniques whether the

options satisfy Peter’s criteria for investment...............................................................................10

Task 4.............................................................................................................................................14

4.1 Explaining key components of main financial statements......................................................14

4.2 Compare appropriate formats of financial statements for different types of business............16

4.3 Analysing financial statements using appropriate ratios and comparing with previous years 16

Conclusion.....................................................................................................................................18

Reference List................................................................................................................................19

2

Clariton Antiques Ltd. is retail store dealing in sales of antiquities. It was started five years ago

by its four partners. It was started as an unincorporated business but slowly and steadily has

grown into reputable business organization. It has two branches in central London and plans to

expand itself by acquiring a building in Birmingham to launch a new store. It requires £0.5m for

launch and has few loans up its sleeve. The following report draws considerable sources of

finance that would help Clariton to finance its new store.

Task 1

1.1 Identifying the sources of finance available to the business

a) Unincorporated business

Unincorporated business owners are responsible for every actions of business and they have to

bear all expenses out of the business. These businesses are sole proprietor or partnership

companies. They raise finances for their business through both external and internal sources.

Internal sources include retained earnings and fixed assets. Retained earnings are profits

generated after deducting every dividends and expenses (Roberts, 2015, p.351). Fixed assets are

tangible assets in possession of the company for a long time that is usually in the forms of non

cash, such as machines and equipments, factories and offices, etc. External sources are

comprised of long term loans, hire buy and leasing and share capitals.

b) Incorporated business

Incorporated are companies that have separated entities from their owners and have its own

rights. It consists shareholders and owners are not sole proprietor of companies and business

decisions are taken by a group of people (Mason et al. 2015, p.55). Its sources of finance include

current assets, venture capitals, shareholders and director’s fund, trade creditors, etc.

1.2 Assessing the implications of sources of finance

a) External sources

External financial sources are sources that company seeks from outside when it do not have

adequate finances from internal sources. External sources can raise big capitals but have few

implications with it. When taking help of investors or shareholders, companies have to give up

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

them which create larger profits in smaller chunks (Carbó‐Valverde et al. 2016, p.140). Venture

capitalists take substantial parts in the ownership of the company. Banks loans or drafts could be

over expensive at times and companies are companies have to make timely repays to resist any

actions.

b) Internal sources

Internal sources make up the internal finances used for company needs. It enforces quick

decisions and avoid wait for financial approval. But using it has some disadvantages. Main

concern for using internal sources is when companies spend their profits or capitals; they are left

with less money to maintain their daily expenses (Gorodnichenko and Schnitzer, 2013, p.1120).

It competes with budgets which are already weak. Benefits of assets sold can no longer accrue to

the business. At time of crisis, companies have no money to sustain themselves or to surface

above the crisis. Internal sources require regular standard business performance for a long time.

1.3 Evaluating most appropriate sources of finance for Clariton Antiques

Clariton Antiques are need of potential financial sources that can fund its plan to acquire a

building to launch a new store. It has various options to procure financial assistance from for its

business expansion. Clariton since being an unincorporated institution can finances from bank

loans. It has accounted profit since its introduction and enjoys considerable reputation in antique

markets. So it can easily get loans from the banks. Bank loans for small capitals would also not

generate larger interests (Bellavitis et al. 2017, p.138). It has also the options of hire buy or

leasing which would enable Clariton to lease their assets for a certain period and raise capitals.

This would enable them to use their equipments and own them after contracts ends. Procuring

capitals from prospective venture capitalists would also be feasible option as it will allow them

to take suggestions from them, already having experiences in investing in other companies and

earning higher profits. This would prevent Clariton from using up their internal finances and gain

profitable partners with only parting with limited shares. Stock trading or getting shareholders

are also potential sources that would generate sums whatever they anticipate or require.

4

Paraphrase This Document

2.1 Assess and compare the costs of above mentioned sources of finance with

reference to

a) Dividends: Dividend is considered as the portion of net earnings to the company at a

particular period of time. Dividend o equity share capital and preference share capital are paid to

the shareholders as per their return percentage effectively. In this regard it should have to

consider that the company’s Profit after tax are to be distributed as dividend respectively

(Acharya and Shin, 2016, p.96). I the statement of changes in equities dividend is to be placed as

per the accounting rules and regulations.

b) Interests: Interest is the amount that is charged by the lender to the loan takers or loan taking

company. Interest is the cost that the lender charges as the compensation. In the Clariton

Antiques financial statement the interest on borrowing of funds in the liability side are to be

evaluated effectively and appropriately that can lead to represent the accurate financial position.

c) Tax: Assessment of tax in case of financial sources of an organisation is considered as an

important aspect which should have to be paid by the company for the particular financial period.

In the income statement income tax expenses are determined that can lead to measure the net

income of the company for 2014 and 2015. Therefore it can be concluded that the effect of tax

can decrease the financial performance and net income (Foreman-Peck and Zhou, 2016, p.134).

2.2 Explaining the importance of financial planning

Financial planning is required to modify and regulate business spending and meet financial

goals. Making financial plans in advance entails supervisions over financial decisions and allows

making suitable investments.

a) Budgeting: Clariton Antiques Ltd. is only five year old organization and a medium scale

limited company. Budget is integral to its financial plans. Financial planning shall enable

Clariton to measure its financial strength and formulate budgets for business plans within its

scope. Proper and efficient plans concerning finances would enable the company to make

suitable investments in appropriate business markets (Alviniussen and Jankensgard, 2015,

p.172). This helps to understand how to allocate funds in right projects. Financial planning helps

in deciding debt/equity ratio and plan out budget accordingly.

5

structures suitably and in the protective hands of experts. It contains alternative steps and parallel

procedures to be followed if planning fails to meet the goals. Clariton proposes to acquire a

building in Birmingham to expand their business. So planning is important to them in terms of

financial execution so as to ascertain profits or loss that may come out of it (Finnerty, 2013,

p.236). This is primarily required to protect company from the implications if its financial

planning fails to finance the project adequately.

c) Overtrading: If launching a new branch succeeds and generate higher revenues for Clariton,

it can lead to overtrading. Clariton may face the difficulty to meet the increasing demands and

business expansion with limited financial resources which can lead to business failure. Financial

planning takes account of every possible outcome and estimates the possibility of prospective

financial gains or loss. Financial plans therefore may be useful in containing business overtrade

and make good use of profitable business expansion. Thus it is imperative that Clariton develops

financial plans where it identifies potential sources and ascertains how its expansion plan may

perform after implementation.

2.3 Describing the information needs of different decision makers

a) Partners: Partners of the company should have to get informed about the financial

information relating to the production, past financial performance, budget, and profitability.

Financial resources, share capital pattern, investment in share capital are the important financial

information that are needed by the partners for decision making appropriately.

b) Venture capitalists (we finance ltd): Venture capitalists at the time of making investments

in the company should have to understand the financial position and performance effectively

depending on which they can able to invest in the profitable securities. At the time of decision

making for the company the venture capitalists should have to evaluate the budgeted incomes

and expenditures accurately based on which investment can be made (Dutta and Folta, 2016,

p.54).

c) Finance broker: Finance broker in an organisation at the time of decision making for

development and improvement of business organisation and operational efficiency, provides

financial advice in order to invest in profitable securities for meeting the expected return

effectively at a particular period of time (Young, 2016, p.20).

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

a) Venture capitalists: Impact of venture capitalists on the company financial statements can be

evaluated as through venture capitalists advancing in the infrastructure and innovation level can

lead to increase production of the company effectively for which sales and profitability can get

maximised. Venture capitalists can make additional investments in company share capital that

can increase the stockholders equity that can be invested in the next financial year to increase

operational efficiency (Baklanova et al. 2016, p.231).

b) Finance broker: Finance brokers can act as the financial advisors of a company in order to

provide investment decisions to shareholders and investors for profitable investment as per their

expected return effectively and appropriately. Different types of finance options, debt

consolidation are provided by the finance broker respectively to the shareholders for whom a

company can increase the financial performance and financial position (Forshey and Levitas,

2016, p.12).

7

Paraphrase This Document

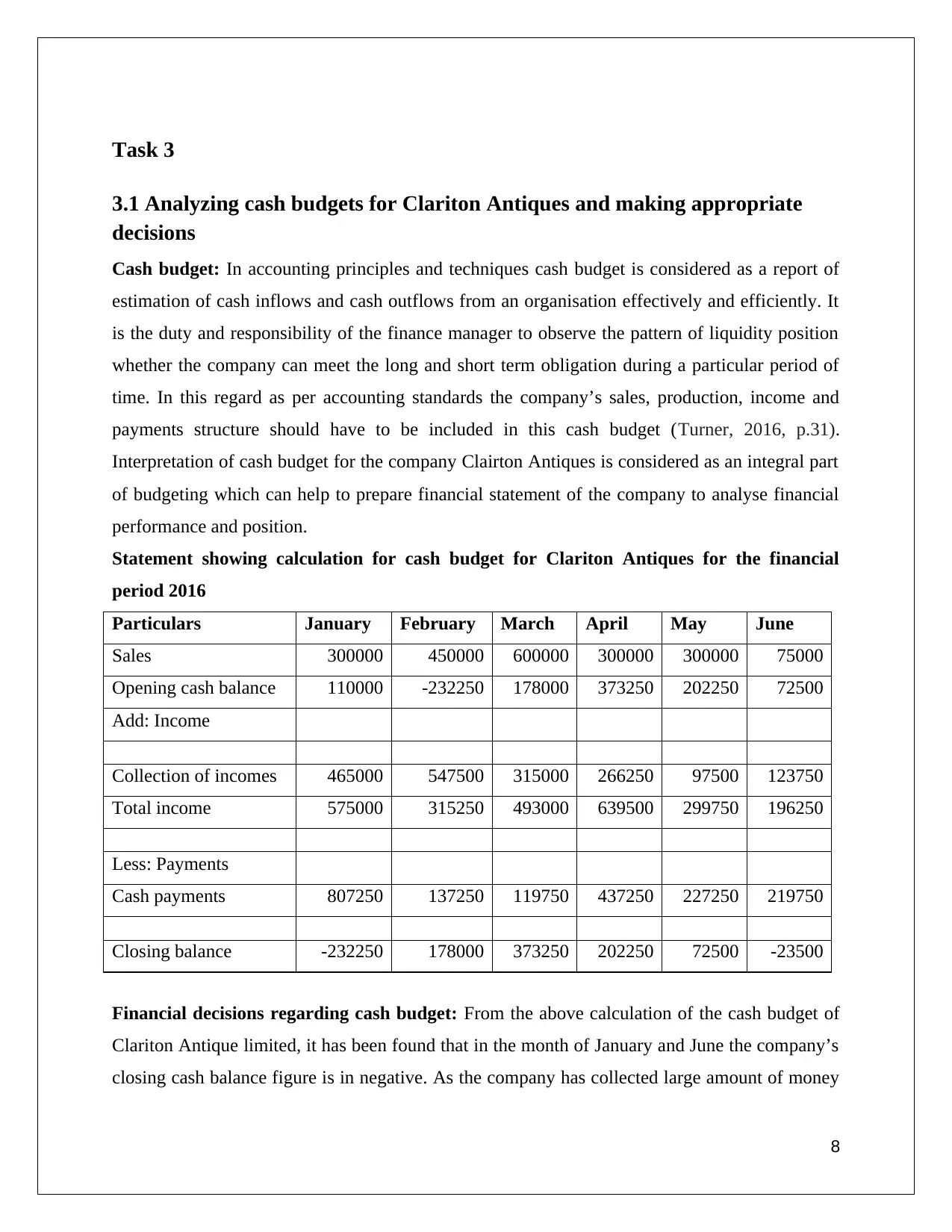

3.1 Analyzing cash budgets for Clariton Antiques and making appropriate

decisions

Cash budget: In accounting principles and techniques cash budget is considered as a report of

estimation of cash inflows and cash outflows from an organisation effectively and efficiently. It

is the duty and responsibility of the finance manager to observe the pattern of liquidity position

whether the company can meet the long and short term obligation during a particular period of

time. In this regard as per accounting standards the company’s sales, production, income and

payments structure should have to be included in this cash budget (Turner, 2016, p.31).

Interpretation of cash budget for the company Clairton Antiques is considered as an integral part

of budgeting which can help to prepare financial statement of the company to analyse financial

performance and position.

Statement showing calculation for cash budget for Clariton Antiques for the financial

period 2016

Particulars January February March April May June

Sales 300000 450000 600000 300000 300000 75000

Opening cash balance 110000 -232250 178000 373250 202250 72500

Add: Income

Collection of incomes 465000 547500 315000 266250 97500 123750

Total income 575000 315250 493000 639500 299750 196250

Less: Payments

Cash payments 807250 137250 119750 437250 227250 219750

Closing balance -232250 178000 373250 202250 72500 -23500

Financial decisions regarding cash budget: From the above calculation of the cash budget of

Clariton Antique limited, it has been found that in the month of January and June the company’s

closing cash balance figure is in negative. As the company has collected large amount of money

8

long term and short term debt requirements in this regard. But in June the negative closing

balance of cash leads to face problem by the company at the time of paying debt obligations

respectively. In order to increase the financial performance preparation of an appropriate cash

budget is required which can lead to help in preparing financial statements. The company should

have to implement certain financial decisions to increase productivity level and sales pattern. In

this way the company can maximise closing cash balance and stronger liquidity position

effectively.

3.2 Explaining how unit costs are calculated to make pricing decisions (giving

examples)

Unit cost of production and cost of goods sold are to be calculated by every business

organisation in order to market their products and services to compete in the market place. If

organisations have produced large number of products and services then it is the duty and

responsibility of the finance manager to evaluate the cost per unit of the products in order to

track the company’s production expenses effectively (Crompton, 2016, p.100). In this regard the

firm should have to calculate the total manufacturing cost by adding the total fixed costs and

variable costs as per accounting standard and regulations.

In other method such as adding the direct material costs, direct labour cost and direct overhead

with variable overhead cost of the product's total manufacturing cost can be determined. After

that the total number of units produced for a particular time period should have to be divided

from total cost of production appropriately.

Formula for calculating cost per unit can be discussed as follows-

Total variable cost + Total fixed cost = Total cost per unit

Total variable cost = Direct material cost + Direct labour cost + Overhead cost

Therefore, Cost per unit = Total cost/ Number of units produced

As example, Clairton Antique has produced 12000 units of products with direct cost of 30000

pound, direct labour of 67000 pound and Overhead of 43000 pound respectively. The fixed cost

of these products is 150000 pound.

Therefore, Total variable cost = (30000+ 67000+ 43000) = 140000 pound

Total fixed cost = 150000 pound

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

= 290000/ 12000

= 24.17 pound per unit.

Therefore from the above calculation it can be concluded that the company’s cost per unit is

24.17 pound.

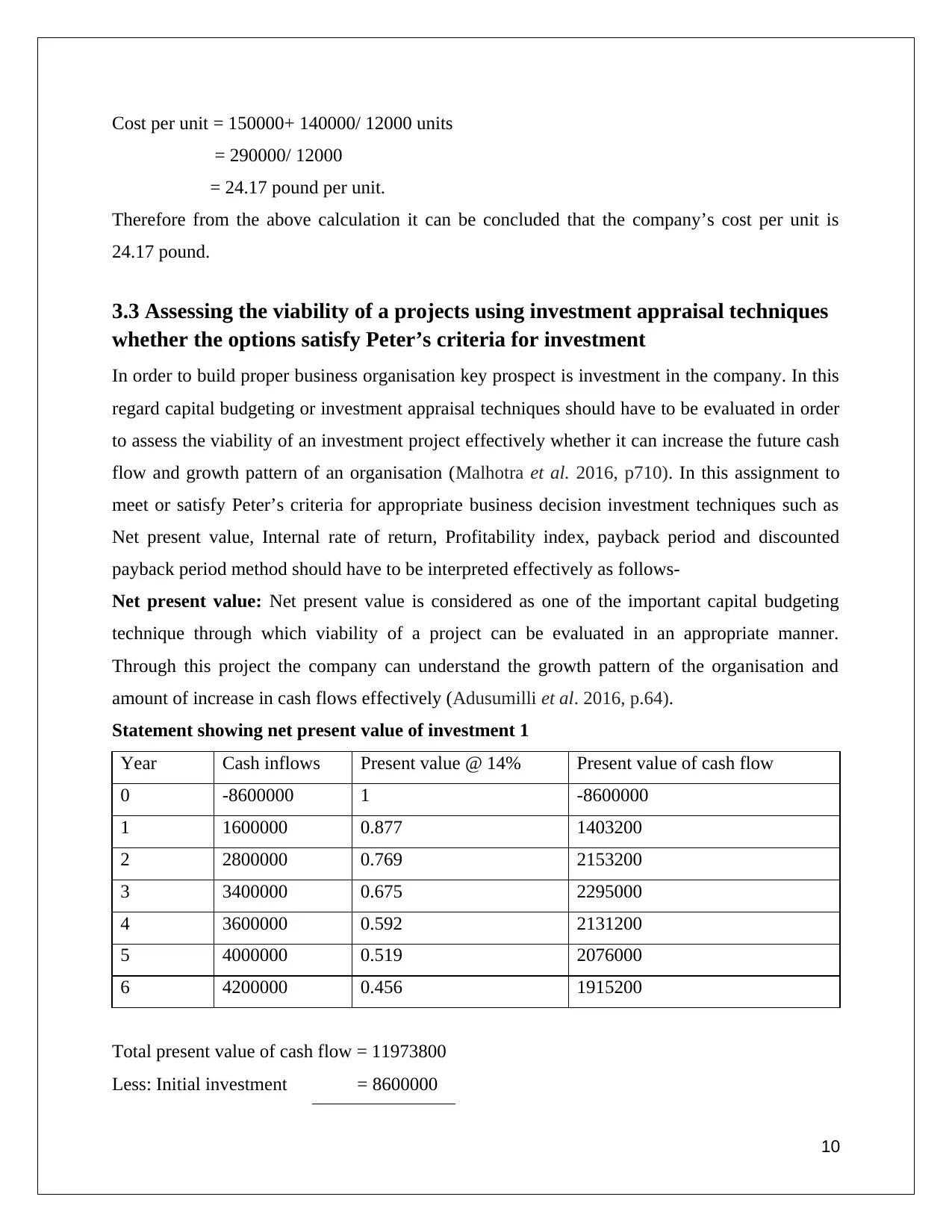

3.3 Assessing the viability of a projects using investment appraisal techniques

whether the options satisfy Peter’s criteria for investment

In order to build proper business organisation key prospect is investment in the company. In this

regard capital budgeting or investment appraisal techniques should have to be evaluated in order

to assess the viability of an investment project effectively whether it can increase the future cash

flow and growth pattern of an organisation (Malhotra et al. 2016, p710). In this assignment to

meet or satisfy Peter’s criteria for appropriate business decision investment techniques such as

Net present value, Internal rate of return, Profitability index, payback period and discounted

payback period method should have to be interpreted effectively as follows-

Net present value: Net present value is considered as one of the important capital budgeting

technique through which viability of a project can be evaluated in an appropriate manner.

Through this project the company can understand the growth pattern of the organisation and

amount of increase in cash flows effectively (Adusumilli et al. 2016, p.64).

Statement showing net present value of investment 1

Year Cash inflows Present value @ 14% Present value of cash flow

0 -8600000 1 -8600000

1 1600000 0.877 1403200

2 2800000 0.769 2153200

3 3400000 0.675 2295000

4 3600000 0.592 2131200

5 4000000 0.519 2076000

6 4200000 0.456 1915200

Total present value of cash flow = 11973800

Less: Initial investment = 8600000

10

Paraphrase This Document

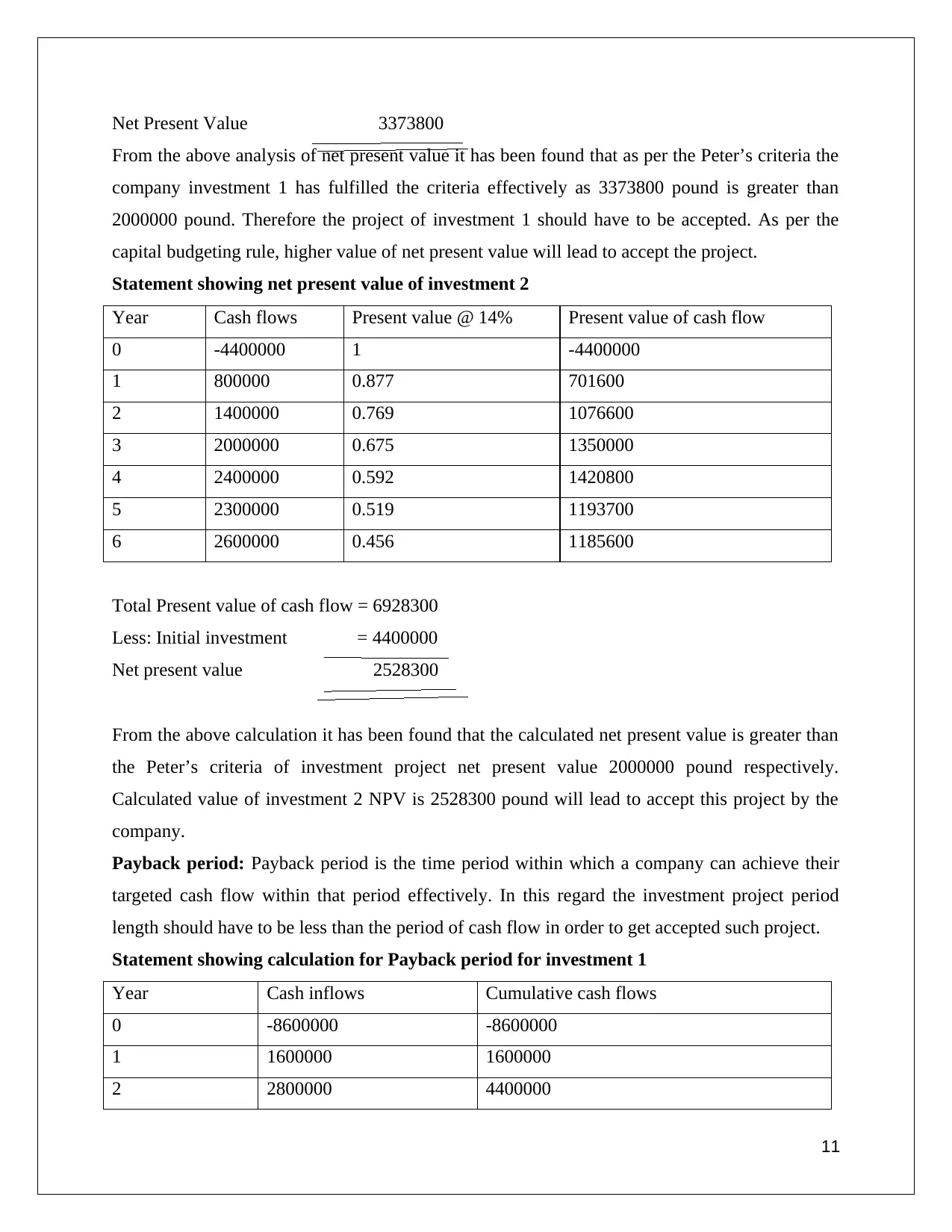

From the above analysis of net present value it has been found that as per the Peter’s criteria the

company investment 1 has fulfilled the criteria effectively as 3373800 pound is greater than

2000000 pound. Therefore the project of investment 1 should have to be accepted. As per the

capital budgeting rule, higher value of net present value will lead to accept the project.

Statement showing net present value of investment 2

Year Cash flows Present value @ 14% Present value of cash flow

0 -4400000 1 -4400000

1 800000 0.877 701600

2 1400000 0.769 1076600

3 2000000 0.675 1350000

4 2400000 0.592 1420800

5 2300000 0.519 1193700

6 2600000 0.456 1185600

Total Present value of cash flow = 6928300

Less: Initial investment = 4400000

Net present value 2528300

From the above calculation it has been found that the calculated net present value is greater than

the Peter’s criteria of investment project net present value 2000000 pound respectively.

Calculated value of investment 2 NPV is 2528300 pound will lead to accept this project by the

company.

Payback period: Payback period is the time period within which a company can achieve their

targeted cash flow within that period effectively. In this regard the investment project period

length should have to be less than the period of cash flow in order to get accepted such project.

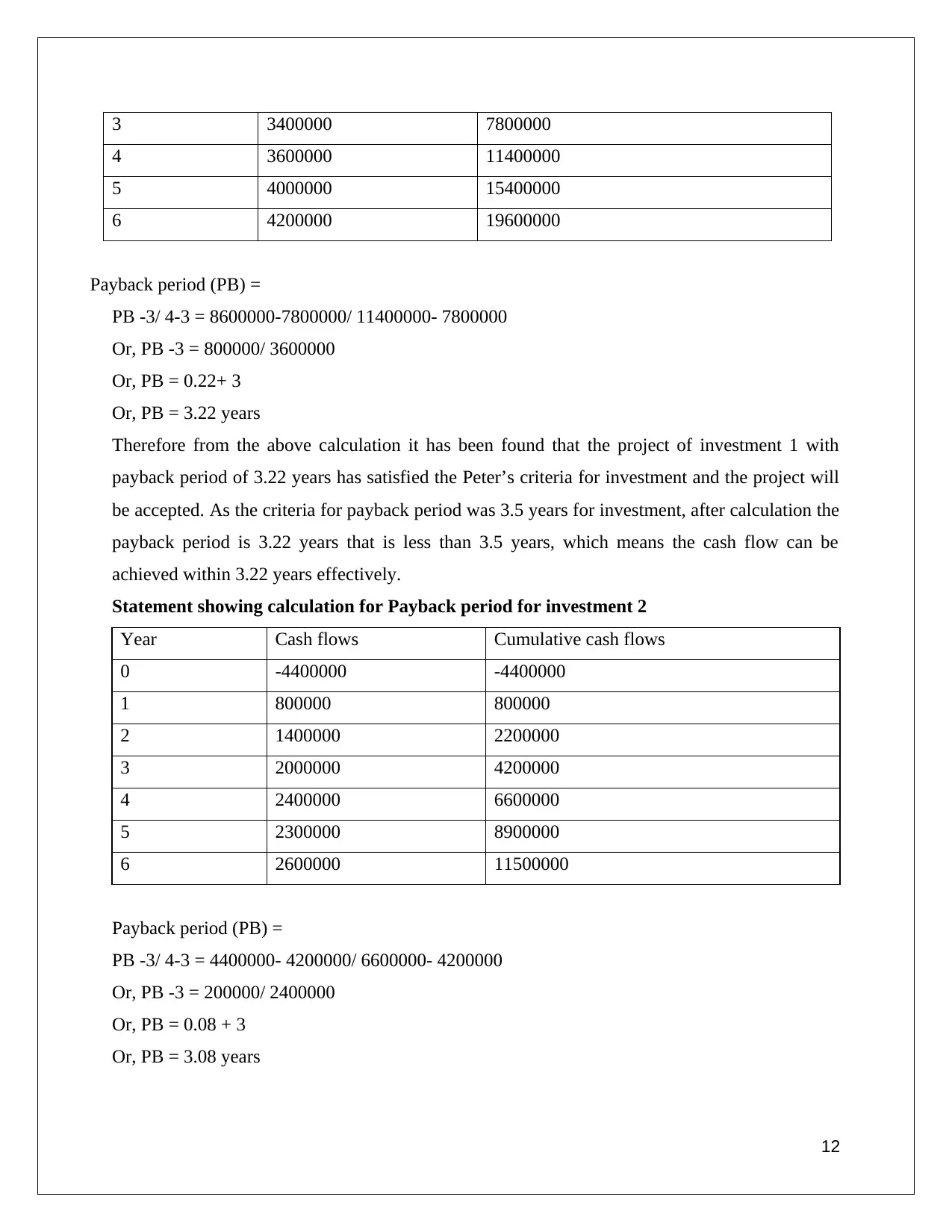

Statement showing calculation for Payback period for investment 1

Year Cash inflows Cumulative cash flows

0 -8600000 -8600000

1 1600000 1600000

2 2800000 4400000

11

4 3600000 11400000

5 4000000 15400000

6 4200000 19600000

Payback period (PB) =

PB -3/ 4-3 = 8600000-7800000/ 11400000- 7800000

Or, PB -3 = 800000/ 3600000

Or, PB = 0.22+ 3

Or, PB = 3.22 years

Therefore from the above calculation it has been found that the project of investment 1 with

payback period of 3.22 years has satisfied the Peter’s criteria for investment and the project will

be accepted. As the criteria for payback period was 3.5 years for investment, after calculation the

payback period is 3.22 years that is less than 3.5 years, which means the cash flow can be

achieved within 3.22 years effectively.

Statement showing calculation for Payback period for investment 2

Year Cash flows Cumulative cash flows

0 -4400000 -4400000

1 800000 800000

2 1400000 2200000

3 2000000 4200000

4 2400000 6600000

5 2300000 8900000

6 2600000 11500000

Payback period (PB) =

PB -3/ 4-3 = 4400000- 4200000/ 6600000- 4200000

Or, PB -3 = 200000/ 2400000

Or, PB = 0.08 + 3

Or, PB = 3.08 years

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

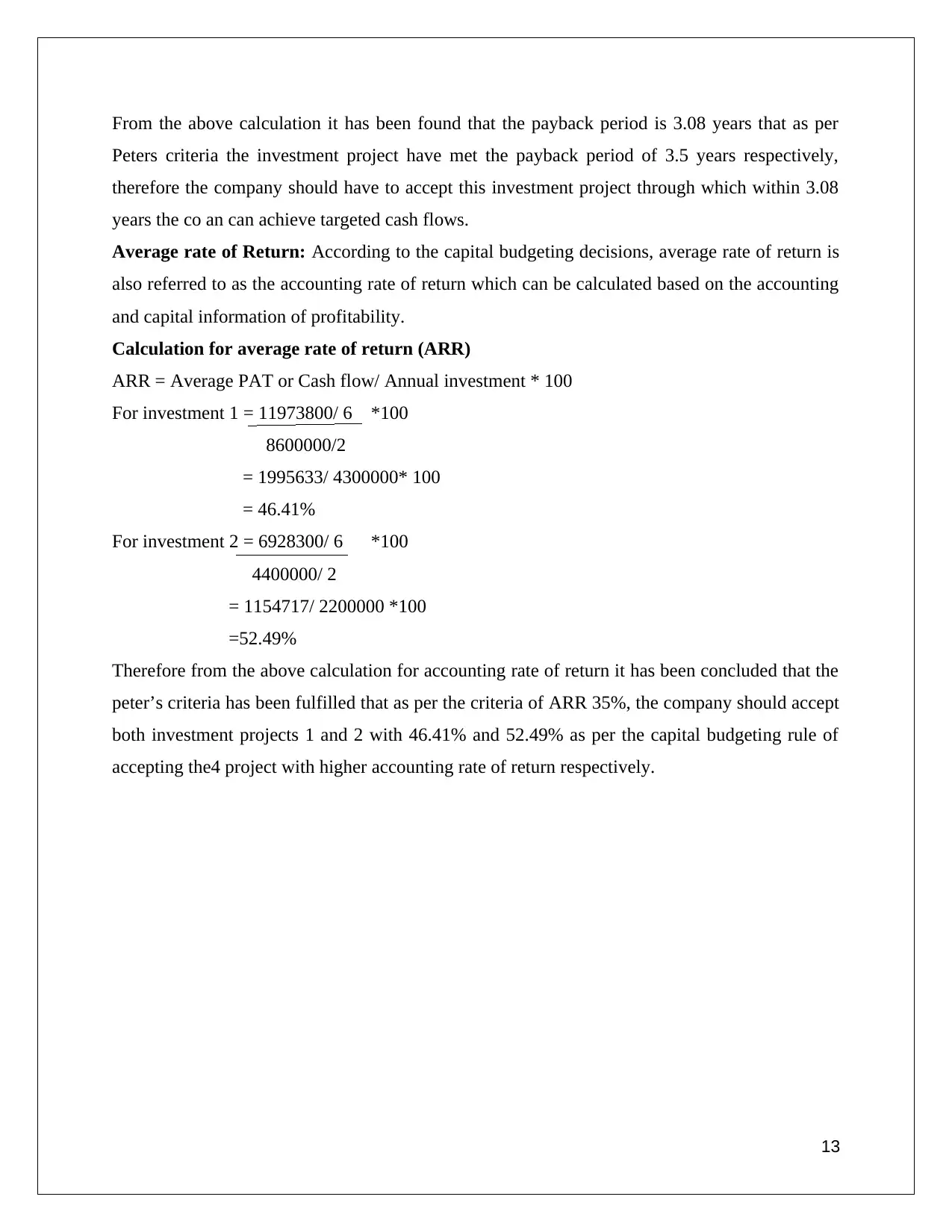

Peters criteria the investment project have met the payback period of 3.5 years respectively,

therefore the company should have to accept this investment project through which within 3.08

years the co an can achieve targeted cash flows.

Average rate of Return: According to the capital budgeting decisions, average rate of return is

also referred to as the accounting rate of return which can be calculated based on the accounting

and capital information of profitability.

Calculation for average rate of return (ARR)

ARR = Average PAT or Cash flow/ Annual investment * 100

For investment 1 = 11973800/ 6 *100

8600000/2

= 1995633/ 4300000* 100

= 46.41%

For investment 2 = 6928300/ 6 *100

4400000/ 2

= 1154717/ 2200000 *100

=52.49%

Therefore from the above calculation for accounting rate of return it has been concluded that the

peter’s criteria has been fulfilled that as per the criteria of ARR 35%, the company should accept

both investment projects 1 and 2 with 46.41% and 52.49% as per the capital budgeting rule of

accepting the4 project with higher accounting rate of return respectively.

13

Paraphrase This Document

4.1 Explaining key components of main financial statements

a) Income statement: Income statement is considered as the most important financial statement

of a company from which the financial performance of company can be evaluated effectively and

appropriately. Based on the earnings available to equity shareholders the earnings per share can

be calculated. Viewing the earnings per share shareholders and investors can evaluate the

company performance and from investment expected return of the shareholders appropriately

(Lee et al. 2016, p.18). Key components of income statements are gross profit, revenue,

operating profit, net income and earnings available to equity shareholders. Revenue is the

amount that indicates sales pattern of the company for a particular period. Subtracting cost of

goods sold from revenue gross profit can be determined from which operating expenses has to be

deducted to get operating profit. From EBIT or operating profit, interest and tax are to be

deducted to get Profit after tax from which preference dividend is to be deducted. In this way

EAES can be determined to which number of shares is to be divided to get Earnings per share

which is the key components of income statements (Anwar et al. 2016, p.238).

b) Statement of cash flows: Statement of cash is considered as the primary financial statement

of a company from which business analyst and accountant can understand the amount of cash

generated from the company for a particular period. Cash inflows and outflows can be evaluated

from these statements from which a firm’s liquidity position can be analysed. Key components

of statement of cash flows are Net cash flow from operating activities, cash flows from investing

activities and cash flows from financing activities respectively (Baik et al. 2016, p.331). At first

the net income from the income statement are to be placed in this statements in the top from

which increase or decrease in current assets and liabilities are to be added or deducted

respectively under operating activities from which net cash flow from operating activities can be

determined. Under cash flow from investing activities the sale of fixed assets are to be added

ands purchase of fixed assets are to be subtracted to get net cash flow from investing activities.

After that the cash flow from financing activities are to be determined by adding the issue of

share capital and deducting the payment of interest and dividend respectively (Ball et al. 2016,

p.29). In this way total cash flow can be calculated from which opening cash of that year is to be

added to get closing balance of cash and cash equivalent.

14

statement of changes in equities and gains which is also referred to as the statement of retained

earnings as per the GAAP. From this financial statement the changes in equities can be evaluated

with movement in the reserves and surplus of a company that will be entered in the liability side

of the company's balance sheet. Key components of this statement are increase or decrease in the

reserve and surplus, net profit attributable to shareholders, amount of payment of dividend to

shareholders , gains or losses in equity, effects of changes in accounting policy are to be included

in this statement respectively (Linsmeier, 2016, p.486).

d) Statement of financial position: Statement of balance sheet or financial position is the report

based on which the financial position or financial state of an organisation can be evaluated. It is a

statement in which liabilities and assets are the main two parts. Under liabilities shareholders

equity is another important component of financial statements of balance sheet. In this regard

under assets fixed assets, current assets and loans and advances are the three parts (Öztürk, M.

and Serçemeli, 2016, p.143). Tangible and intangible assets are the two aspects of fixed assets.

Cash and cash equivalent, inventories are the main aspects of current assets based on which

liquidity position of a company can be determined in order to pay the debt obligations. Under

liabilities Authorised capital, paid up capital including share capital. Reserve and surplus and

minorities interest of the company are to be considered as per accounting standards rules and

regulations. Share capital in this regard represents the amount of raising and issuing of capital

effectively (Agbemava et al. 2016, p.104). Retained earnings or reserve and surplus represent the

amount available in the reserve fund that the company can invest in the coming financial year in

order to accurate running of business operations.

e) Notes to the financial statement: Notes to financial statement is another financial statement

that can help a company to communicate their company financial information in order to

evaluate the financial position at the end of a financial year. Key components of this financial

statement are the sample of financial information based on which financial position statement ac

is prepared. Agency number, name, headquarter are the components of this financial statement.

15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

business

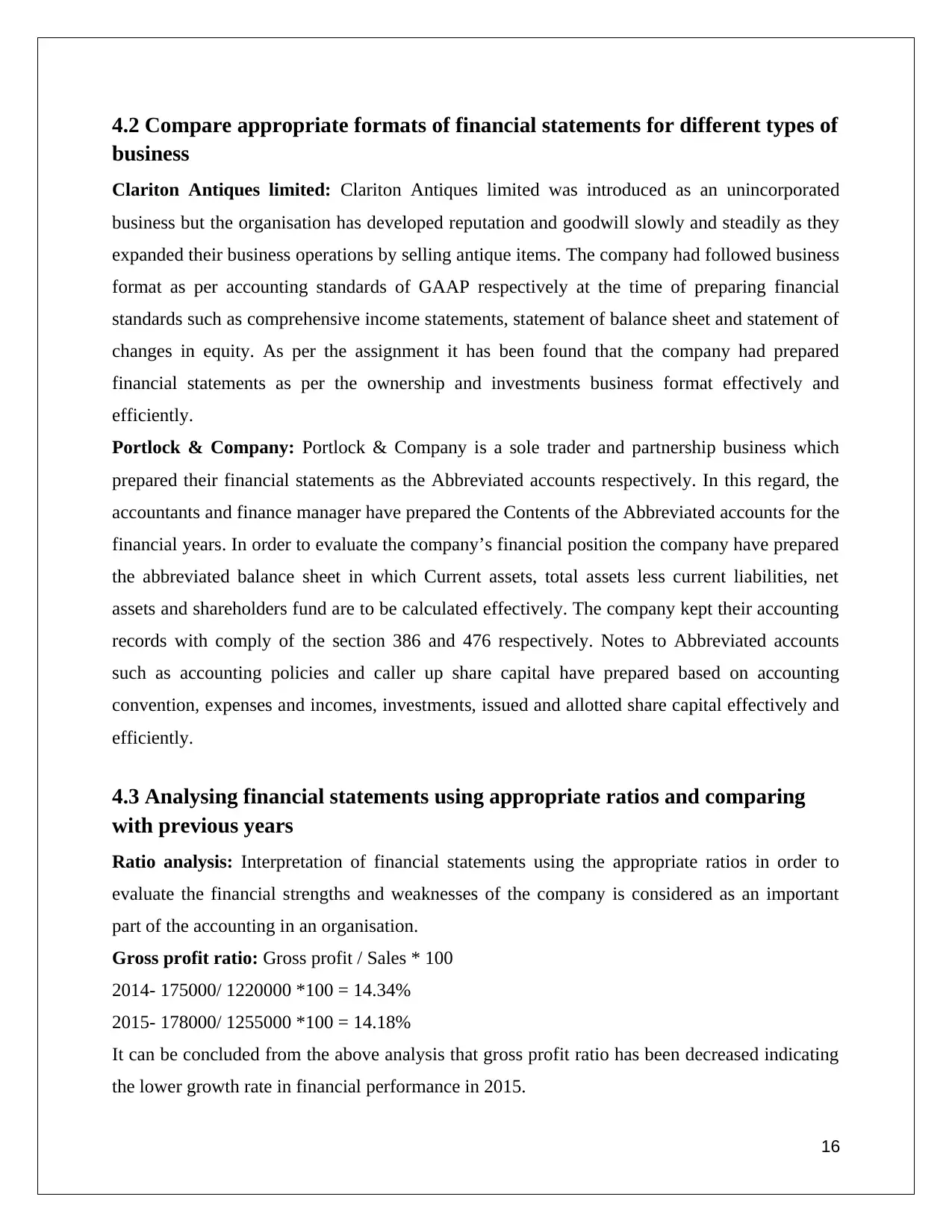

Clariton Antiques limited: Clariton Antiques limited was introduced as an unincorporated

business but the organisation has developed reputation and goodwill slowly and steadily as they

expanded their business operations by selling antique items. The company had followed business

format as per accounting standards of GAAP respectively at the time of preparing financial

standards such as comprehensive income statements, statement of balance sheet and statement of

changes in equity. As per the assignment it has been found that the company had prepared

financial statements as per the ownership and investments business format effectively and

efficiently.

Portlock & Company: Portlock & Company is a sole trader and partnership business which

prepared their financial statements as the Abbreviated accounts respectively. In this regard, the

accountants and finance manager have prepared the Contents of the Abbreviated accounts for the

financial years. In order to evaluate the company’s financial position the company have prepared

the abbreviated balance sheet in which Current assets, total assets less current liabilities, net

assets and shareholders fund are to be calculated effectively. The company kept their accounting

records with comply of the section 386 and 476 respectively. Notes to Abbreviated accounts

such as accounting policies and caller up share capital have prepared based on accounting

convention, expenses and incomes, investments, issued and allotted share capital effectively and

efficiently.

4.3 Analysing financial statements using appropriate ratios and comparing

with previous years

Ratio analysis: Interpretation of financial statements using the appropriate ratios in order to

evaluate the financial strengths and weaknesses of the company is considered as an important

part of the accounting in an organisation.

Gross profit ratio: Gross profit / Sales * 100

2014- 175000/ 1220000 *100 = 14.34%

2015- 178000/ 1255000 *100 = 14.18%

It can be concluded from the above analysis that gross profit ratio has been decreased indicating

the lower growth rate in financial performance in 2015.

16

Paraphrase This Document

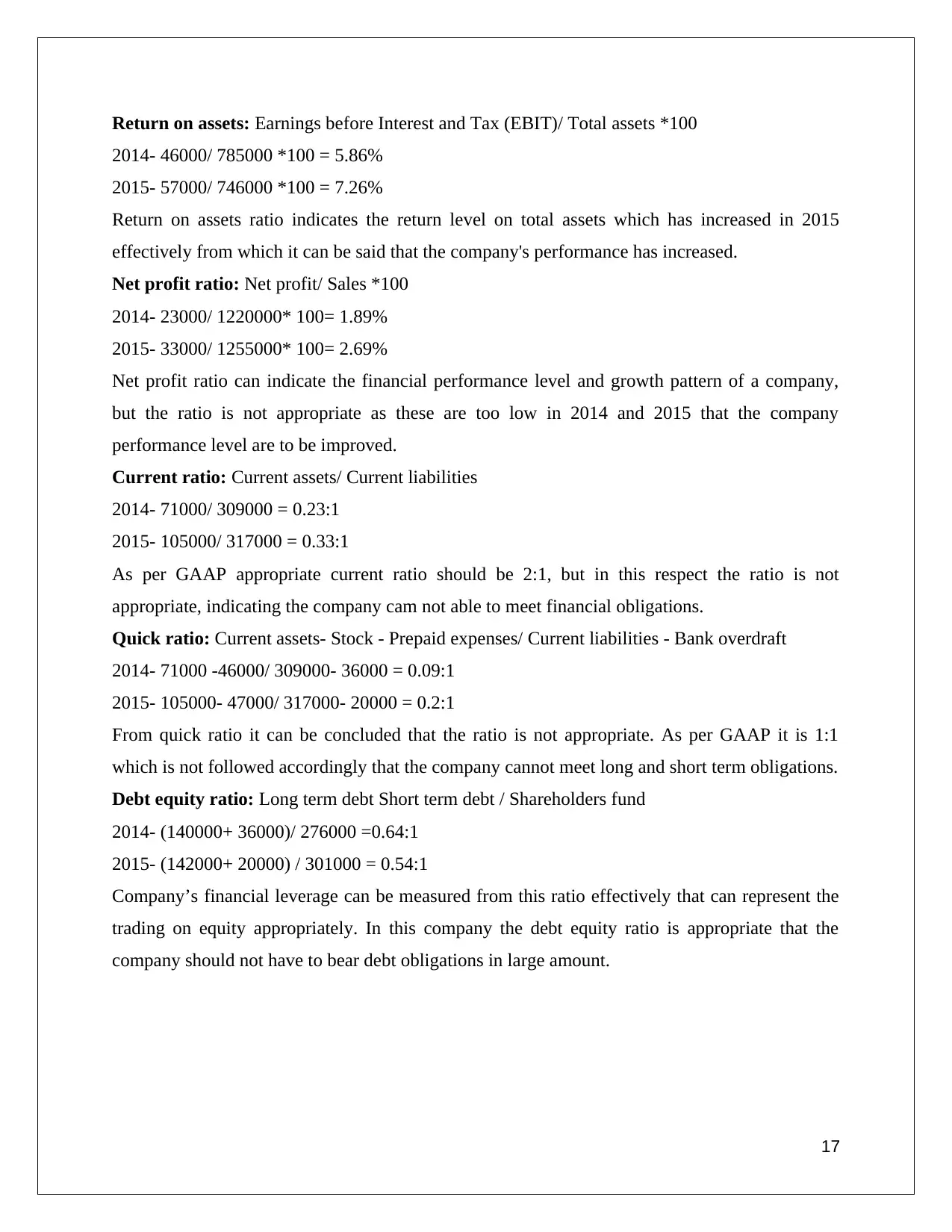

2014- 46000/ 785000 *100 = 5.86%

2015- 57000/ 746000 *100 = 7.26%

Return on assets ratio indicates the return level on total assets which has increased in 2015

effectively from which it can be said that the company's performance has increased.

Net profit ratio: Net profit/ Sales *100

2014- 23000/ 1220000* 100= 1.89%

2015- 33000/ 1255000* 100= 2.69%

Net profit ratio can indicate the financial performance level and growth pattern of a company,

but the ratio is not appropriate as these are too low in 2014 and 2015 that the company

performance level are to be improved.

Current ratio: Current assets/ Current liabilities

2014- 71000/ 309000 = 0.23:1

2015- 105000/ 317000 = 0.33:1

As per GAAP appropriate current ratio should be 2:1, but in this respect the ratio is not

appropriate, indicating the company cam not able to meet financial obligations.

Quick ratio: Current assets- Stock - Prepaid expenses/ Current liabilities - Bank overdraft

2014- 71000 -46000/ 309000- 36000 = 0.09:1

2015- 105000- 47000/ 317000- 20000 = 0.2:1

From quick ratio it can be concluded that the ratio is not appropriate. As per GAAP it is 1:1

which is not followed accordingly that the company cannot meet long and short term obligations.

Debt equity ratio: Long term debt Short term debt / Shareholders fund

2014- (140000+ 36000)/ 276000 =0.64:1

2015- (142000+ 20000) / 301000 = 0.54:1

Company’s financial leverage can be measured from this ratio effectively that can represent the

trading on equity appropriately. In this company the debt equity ratio is appropriate that the

company should not have to bear debt obligations in large amount.

17

Financial position and performance of a company can be measured by evaluating the financial

statements such as income statement, balance sheet, and changes in equity and cash flow

statements effectively and efficiently. In this regard in order to analyse the company’s financial

strengths and weaknesses, ratio analysis is considered as the important financial technique and

tool. In this regard budget should have to be prepared appropriately to compare actual income

and expenditures that can lead to analyse financial performance of the company.

18

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Acharya, V.V., Le, H. and Shin, H.S., 2016. Bank capital and dividend externalities. Review of

Financial Studies, p.96.

Adusumilli, N., Davis, S. and Fromme, D., 2016. Economic evaluation of using surge valves in

furrow irrigation of row crops in Louisiana: A net present value approach. Agricultural Water

Management, 174, pp.61-65.

Agbemava, E., Ahiase, G., Sedzro, E., Adade, T.C., Bediako, A.K., Nyarko, I.K. and Kudo,

M.B., 2016. Assessing the Effects of Sound Financial Statement Preparation on the Growth of

Small and Medium-Scale Enterprises. The International Journal of Business & Management,

4(3), p.104.

Alviniussen, A. and Jankensgard, H., 2015. Enterprise risk budgeting: bringing risk management

into the financial planning process.

Anwar, S.M., Rahmawati, R., Rismawati, R. and Rukmini, R., 2016. FINANCIAL RATIO

ANALYSIS USING ADDED VALUE, INCOME STATEMENT. Qualitative and Quantitative

Research Review, 1(3).

Baik, B., Cho, H., Choi, W. and Lee, K., 2016. Who classifies interest payments as financing

activities? An analysis of classification shifting in the statement of cash flows at the adoption of

IFRS. Journal of Accounting and Public Policy, 35(4), pp.331-351.

Baklanova, V., Caglio, C., Cipriani, M. and Copeland, A.M., 2016. A new survey of the US

bilateral repo market: a snapshot of broker-dealer activity.

Ball, R., Gerakos, J., Linnainmaa, J.T. and Nikolaev, V., 2016. Accruals, cash flows, and

operating profitability in the cross section of stock returns. Journal of Financial Economics,

121(1), pp.28-45.

Bellavitis, C., Filatotchev, I., Kamuriwo, D.S. and Vanacker, T., 2017. Entrepreneurial finance:

new frontiers of research and practice: Editorial for the special issue Embracing entrepreneurial

funding innovations.

Carbó‐Valverde, S., Rodríguez‐Fernández, F. and Udell, G.F., 2016. Trade credit, the financial

crisis, and SME access to finance. Journal of Money, Credit and Banking, 48(1), pp.113-143.

Crompton, J.L., 2016. A policy framework for analyzing multi-use pass pricing decisions.

Managing Sport and Leisure, 21(2), pp.91-101.

19

Paraphrase This Document

innovation and value creation. Journal of business venturing, 31(1), pp.39-54.

Finnerty, J.D., 2013. Project financing: Asset-based financial engineering. John Wiley & Sons.

Foreman-Peck, J. and Zhou, P., 2016. Migration and Tax Yields in a Devolved Economy (No.

E2016/7). Cardiff University, Cardiff Business School, Economics Section.

Forshey, P. and Levitas, E., 2016. The Impact of Venture Capital on Funding Amounts Promised

in Alliance Contracts. Academy of Strategic Management Journal, 15(1), p.12.

Gorodnichenko, Y. and Schnitzer, M., 2013. Financial constraints and innovation: Why poor

countries don't catch up. Journal of the European Economic Association, 11(5), pp.1115-1152.

Lee, B.B., Shin, H., Vetter, W. and Kim, D.W., 2016. Management of Income Statement

Variables to Report Small Positive Earnings Numbers. Asian Review of Accounting, 25(1).

Linsmeier, T.J., 2016. Revised model for presentation in statement (s) of financial performance:

Potential implications for measurement in the conceptual framework. Accounting Horizons,

30(4), pp.485-498.

Malhotra, A., Battke, B., Beuse, M., Stephan, A. and Schmidt, T., 2016. Use cases for stationary

battery technologies: A review of the literature and existing projects. Renewable and Sustainable

Energy Reviews, 56, pp.705-721.

Mason, C.M. and Harrison, R.T., 2015. Business angel investment activity in the financial crisis:

UK evidence and policy implications. Environment and Planning C: Government and Policy,

33(1), pp.43-60.

Öztürk, M. and Serçemeli, M., 2016. Impact of New Standard" IFRS 16 Leases" on Statement of

Financial Position and Key Ratios: A Case Study on an Airline Company in Turkey. Business

and Economics Research Journal, 7(4), p.143.

Roberts, R., 2015. Finance for Small and Entrepreneurial Business. Routledge.

Turner, J.A., 2016. Net Operating Working Capital, Capital Budgeting, And Cash Budgets: A

Teaching Example. American Journal of Business Education (Online), 9(1), p.31.

Young, K., 2016. A partnership between a selling agent and a buyer's agent could mean better

business success-for both agents. REIQ Journal, (Feb 2016), p.20.

20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.