Management Accounting Systems and Tools

VerifiedAdded on 2020/10/23

|16

|4120

|211

AI Summary

This assignment provides a detailed overview of management accounting systems and tools. It explores the role of marginal and absorption costing in determining profit, as well as the use of variance analysis to identify inefficiencies in business activities. Additionally, it discusses the importance of benchmarking and other planning tools in helping businesses develop strategies for financial performance enhancement.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

- ``

“Business”

“Business”

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

TASK 1............................................................................................................................................3

P 3 Preparation of income statement and calculation of cost of production using marginal and

absorption costing techniques.....................................................................................................3

TASK 2............................................................................................................................................8

P4 Advantages and used disadvantage of different type of planning tool for budgetary control

.....................................................................................................................................................8

P 5 Evaluation of management accounting system as to responding to various financial

problems....................................................................................................................................10

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

TASK 1............................................................................................................................................3

P 3 Preparation of income statement and calculation of cost of production using marginal and

absorption costing techniques.....................................................................................................3

TASK 2............................................................................................................................................8

P4 Advantages and used disadvantage of different type of planning tool for budgetary control

.....................................................................................................................................................8

P 5 Evaluation of management accounting system as to responding to various financial

problems....................................................................................................................................10

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

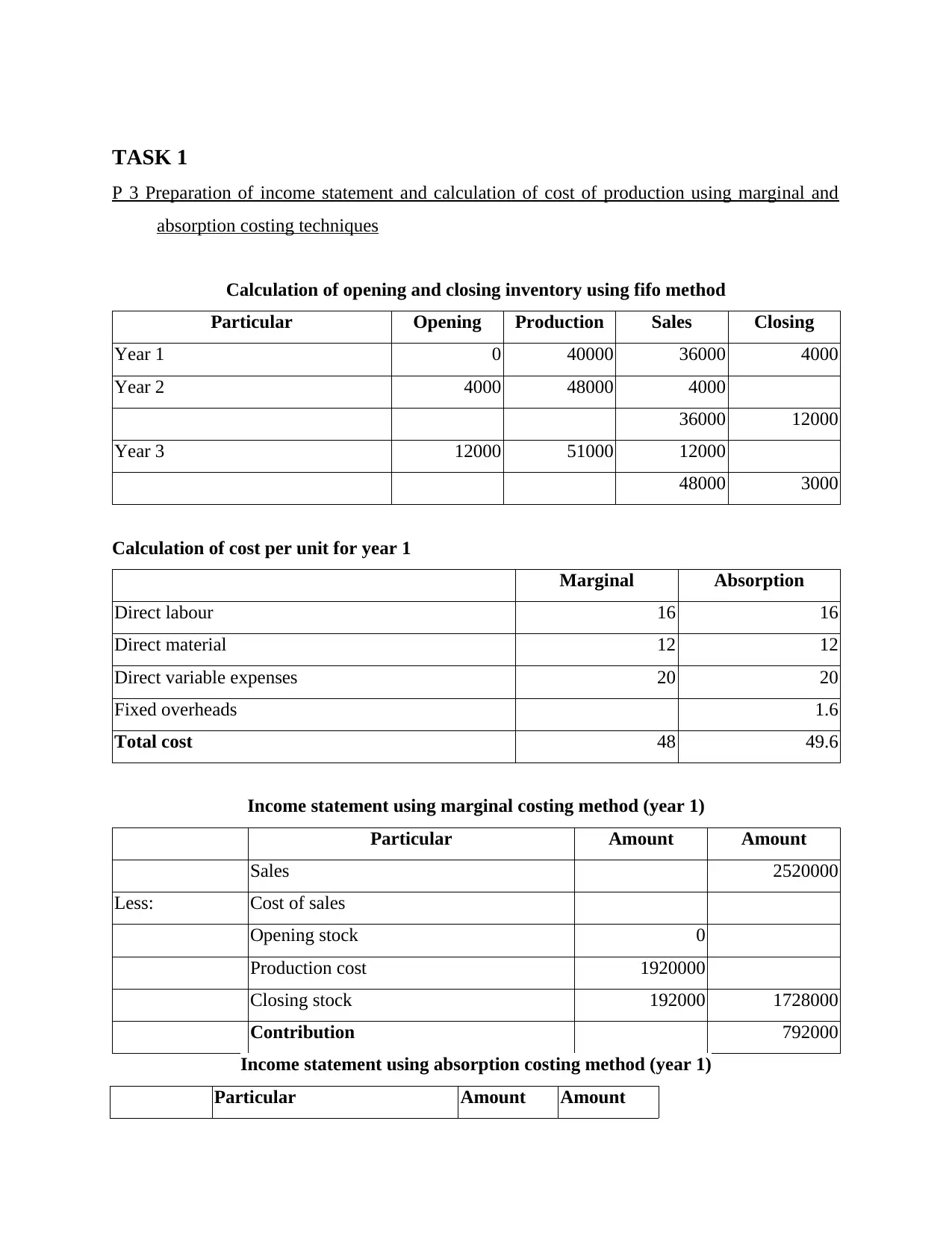

TASK 1

P 3 Preparation of income statement and calculation of cost of production using marginal and

absorption costing techniques

Calculation of opening and closing inventory using fifo method

Particular Opening Production Sales Closing

Year 1 0 40000 36000 4000

Year 2 4000 48000 4000

36000 12000

Year 3 12000 51000 12000

48000 3000

Calculation of cost per unit for year 1

Marginal Absorption

Direct labour 16 16

Direct material 12 12

Direct variable expenses 20 20

Fixed overheads 1.6

Total cost 48 49.6

Income statement using marginal costing method (year 1)

Particular Amount Amount

Sales 2520000

Less: Cost of sales

Opening stock 0

Production cost 1920000

Closing stock 192000 1728000

Contribution 792000

Income statement using absorption costing method (year 1)

Particular Amount Amount

P 3 Preparation of income statement and calculation of cost of production using marginal and

absorption costing techniques

Calculation of opening and closing inventory using fifo method

Particular Opening Production Sales Closing

Year 1 0 40000 36000 4000

Year 2 4000 48000 4000

36000 12000

Year 3 12000 51000 12000

48000 3000

Calculation of cost per unit for year 1

Marginal Absorption

Direct labour 16 16

Direct material 12 12

Direct variable expenses 20 20

Fixed overheads 1.6

Total cost 48 49.6

Income statement using marginal costing method (year 1)

Particular Amount Amount

Sales 2520000

Less: Cost of sales

Opening stock 0

Production cost 1920000

Closing stock 192000 1728000

Contribution 792000

Income statement using absorption costing method (year 1)

Particular Amount Amount

Sales 2520000

Less: Cost of sales

Opening stock 0

Production 1984000

Closing stocck 198400 1785600

Gross profit 734400

Less:

Selling and distribution

overheads 10000

Administration overheads 15000 25000

Net profit 709400

Less: Interest expenses 1000

Net profit after interest and

taxes 708400

Calculation of cost per unit for year 2

Marginal Absorption

Direct labour 16 16

Direct material 12 12

Direct variable expenses 20 20

Fixed overheads 1.33

Total cost 48 49.33

Income statement using marginal costing method (year 2)

Particular Amount Amount

Sales 2800000

Cost of sales

Opening stock 192000

Production cost 2304000

Closing stock 576000 1920000

Contribution 880000

Less: Cost of sales

Opening stock 0

Production 1984000

Closing stocck 198400 1785600

Gross profit 734400

Less:

Selling and distribution

overheads 10000

Administration overheads 15000 25000

Net profit 709400

Less: Interest expenses 1000

Net profit after interest and

taxes 708400

Calculation of cost per unit for year 2

Marginal Absorption

Direct labour 16 16

Direct material 12 12

Direct variable expenses 20 20

Fixed overheads 1.33

Total cost 48 49.33

Income statement using marginal costing method (year 2)

Particular Amount Amount

Sales 2800000

Cost of sales

Opening stock 192000

Production cost 2304000

Closing stock 576000 1920000

Contribution 880000

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

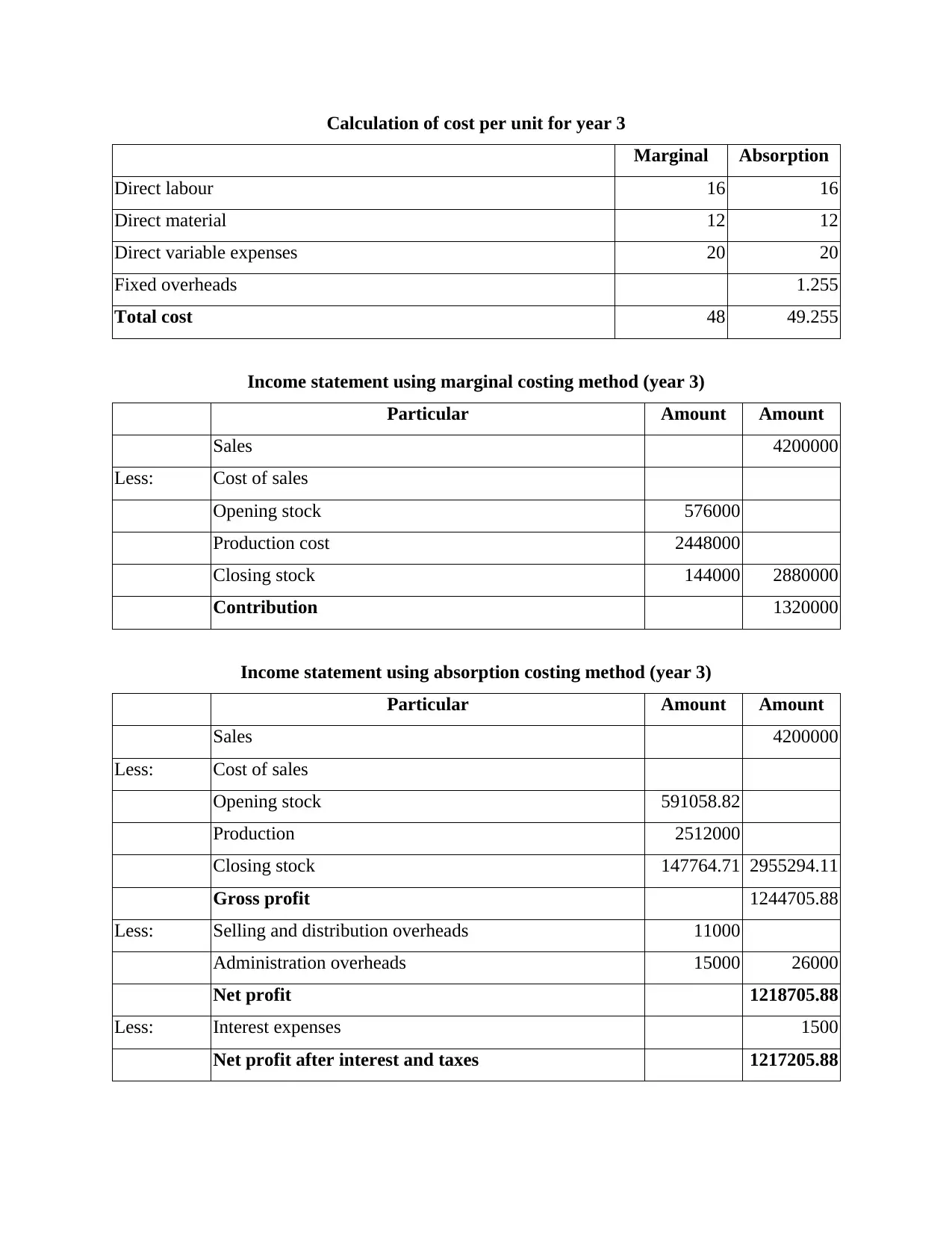

Calculation of cost per unit for year 3

Marginal Absorption

Direct labour 16 16

Direct material 12 12

Direct variable expenses 20 20

Fixed overheads 1.255

Total cost 48 49.255

Income statement using marginal costing method (year 3)

Particular Amount Amount

Sales 4200000

Less: Cost of sales

Opening stock 576000

Production cost 2448000

Closing stock 144000 2880000

Contribution 1320000

Income statement using absorption costing method (year 3)

Particular Amount Amount

Sales 4200000

Less: Cost of sales

Opening stock 591058.82

Production 2512000

Closing stock 147764.71 2955294.11

Gross profit 1244705.88

Less: Selling and distribution overheads 11000

Administration overheads 15000 26000

Net profit 1218705.88

Less: Interest expenses 1500

Net profit after interest and taxes 1217205.88

Marginal Absorption

Direct labour 16 16

Direct material 12 12

Direct variable expenses 20 20

Fixed overheads 1.255

Total cost 48 49.255

Income statement using marginal costing method (year 3)

Particular Amount Amount

Sales 4200000

Less: Cost of sales

Opening stock 576000

Production cost 2448000

Closing stock 144000 2880000

Contribution 1320000

Income statement using absorption costing method (year 3)

Particular Amount Amount

Sales 4200000

Less: Cost of sales

Opening stock 591058.82

Production 2512000

Closing stock 147764.71 2955294.11

Gross profit 1244705.88

Less: Selling and distribution overheads 11000

Administration overheads 15000 26000

Net profit 1218705.88

Less: Interest expenses 1500

Net profit after interest and taxes 1217205.88

From the analysis of above calculations, it can be evaluated that in marginal costing

method measures the profit in terms of contribution whereas, the absorption costing measures the

cost in terms of net profit. Further, while calculating cost per unit in absorption costing, fixed

production cost is also taken into account, which is not considered in the cost per unit under

marginal costing method.

Analysis of the above calculation is also interpreting that the marginal costing income

statement provides higher amount of profit than the absorption costing income statement. The

difference is arisen due to exclusion of all the fixed costs in the marginal costing method.

Marginal costing method:

Marginal costing method is a method used in the marginal accounting system in which all

the variable costs are charged to the product cost (Hieu and Dung, 2018). Further, the fixed costs

are treated as period cost.

Absorption costing method:

Absorption costing system is a technique in which each production cost including direct

and indirect production costs are considered as product cost and taken into account while

calculating the cost of production as well.

Difference between marginal costing and absorption costing method:

Key difference between these two methods are as under:

Basis Marginal costing Absorption costing

Meaning It is the management accounting

technique through which the

managers can take decisions

regarding ascertainment of cost and

determination of fixed and variable

cost as well.

Absorption costing is a technique

with the help of which managers can

allocate the cost among various cost

centres and determine the total cost

of production as well.

Profitability Marginal cost provides higher amount

of profitability to the business.

Profitability of the business is

recognised comparatively low in this

method.

Measurement Profit is measured as contribution in

this method.

In absorption costing method, the

profit is measured as net profit for

method measures the profit in terms of contribution whereas, the absorption costing measures the

cost in terms of net profit. Further, while calculating cost per unit in absorption costing, fixed

production cost is also taken into account, which is not considered in the cost per unit under

marginal costing method.

Analysis of the above calculation is also interpreting that the marginal costing income

statement provides higher amount of profit than the absorption costing income statement. The

difference is arisen due to exclusion of all the fixed costs in the marginal costing method.

Marginal costing method:

Marginal costing method is a method used in the marginal accounting system in which all

the variable costs are charged to the product cost (Hieu and Dung, 2018). Further, the fixed costs

are treated as period cost.

Absorption costing method:

Absorption costing system is a technique in which each production cost including direct

and indirect production costs are considered as product cost and taken into account while

calculating the cost of production as well.

Difference between marginal costing and absorption costing method:

Key difference between these two methods are as under:

Basis Marginal costing Absorption costing

Meaning It is the management accounting

technique through which the

managers can take decisions

regarding ascertainment of cost and

determination of fixed and variable

cost as well.

Absorption costing is a technique

with the help of which managers can

allocate the cost among various cost

centres and determine the total cost

of production as well.

Profitability Marginal cost provides higher amount

of profitability to the business.

Profitability of the business is

recognised comparatively low in this

method.

Measurement Profit is measured as contribution in

this method.

In absorption costing method, the

profit is measured as net profit for

the year.

Cost per unit Fixed production overheads are not

taken into account while calculating

cost of production(Difference between

Marginal and Absorption Costing,

2018).

Fixed production overheads are also

considered while calculating the cost

of production in absorption costing

method.

Classification of

overheads

Overheads are classified on the basis

of fixed and variable cost in this

method.

In the absorption costing method,

overheads are classified as

production overhead, selling and

distribution overheads,

administration overheads, etc.

Usage Income statement of marginal costing

system are used by the managers in

their decision making process.

Income statement made through

absorption costing method are used

for the purpose of external reporting

by the business.

Inventories Inventories are valued at the total

variable cost of production of the

company.

In this method, inventories are valued

at tota production cost incurred by

the business. Which results in higher

amount of inventory comes higher as

compare to the marginal costing

system.

Use of marginal costing in the business:

Marginal costing technique is adopted by the business organisations as it helps the

managers in their decision making process. Key usage of the marginal costing techniques are as

under:

Planning for profit: profit planning can be defined as planning for the purpose of

predicting all the future operations of the firm so that the company could generate the

maximum amount of profit from its business operations (Christian, 2018). In the marginal

costing method provides information about the contribution of the business through

Cost per unit Fixed production overheads are not

taken into account while calculating

cost of production(Difference between

Marginal and Absorption Costing,

2018).

Fixed production overheads are also

considered while calculating the cost

of production in absorption costing

method.

Classification of

overheads

Overheads are classified on the basis

of fixed and variable cost in this

method.

In the absorption costing method,

overheads are classified as

production overhead, selling and

distribution overheads,

administration overheads, etc.

Usage Income statement of marginal costing

system are used by the managers in

their decision making process.

Income statement made through

absorption costing method are used

for the purpose of external reporting

by the business.

Inventories Inventories are valued at the total

variable cost of production of the

company.

In this method, inventories are valued

at tota production cost incurred by

the business. Which results in higher

amount of inventory comes higher as

compare to the marginal costing

system.

Use of marginal costing in the business:

Marginal costing technique is adopted by the business organisations as it helps the

managers in their decision making process. Key usage of the marginal costing techniques are as

under:

Planning for profit: profit planning can be defined as planning for the purpose of

predicting all the future operations of the firm so that the company could generate the

maximum amount of profit from its business operations (Christian, 2018). In the marginal

costing method provides information about the contribution of the business through

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

which managers can easily determine the change in sales and marginal cost, selling price

over the year which are helpful in predicting the future cost and profit of the business as

well. In this regard, marginal costing technique helps the managers as a planning tool.

Decision making process: The contribution of the business is the key measure for ther

managers, as with the help of it, they can determine the production mix, sales mix,

variance in sales and marginal cost, etc. all these elements are the major elements

required by the managers in their decision making process.

Cost control: With the help of marginal cost statement, managers can easily determine

the cost related performance of the business, through which they can make more effective

strategies sand plans for controlling the overall cost of the business. In this regard, the

marginal costing system can be used in the cost controlling procedure by the managers

(Jermias, 2017).

In this regard, it can be analysed that the marginal costing technique is useful for the

managers in performing various managerial functions.

Reason behind difference arisen in the profit or loss under marginal and absorption costing

method

From the analysis of above calculation and study it can be evaluated that both marginal

costing and absorption costing provides different amount of profit. Key reasons behind this

difference are:

In both marginal costing and absorption costing, there is a difference in calculation of

closing stock. Which h arises the difference in cost of production and hence in the profit

as well.

Further, while preparing the income statement under marginal costing system, the fixed

cost are not taken into account (Fisher and Krumwiede, 2015). On the other hand, each

cost incurred by the business while manufacturing the products are taken into account in

the absorption costing method. Due to this method, total cost differs in both the methods.

It directly results in occurrence of difference in the profit of the company as well.

TASK 2

P4 Advantages and used disadvantage of different type of planning tool for budgetary control

Budgetary control is a process for the managers to set the financing performance goals

with the help of budgets and compare them with actual performance and make adjustments

over the year which are helpful in predicting the future cost and profit of the business as

well. In this regard, marginal costing technique helps the managers as a planning tool.

Decision making process: The contribution of the business is the key measure for ther

managers, as with the help of it, they can determine the production mix, sales mix,

variance in sales and marginal cost, etc. all these elements are the major elements

required by the managers in their decision making process.

Cost control: With the help of marginal cost statement, managers can easily determine

the cost related performance of the business, through which they can make more effective

strategies sand plans for controlling the overall cost of the business. In this regard, the

marginal costing system can be used in the cost controlling procedure by the managers

(Jermias, 2017).

In this regard, it can be analysed that the marginal costing technique is useful for the

managers in performing various managerial functions.

Reason behind difference arisen in the profit or loss under marginal and absorption costing

method

From the analysis of above calculation and study it can be evaluated that both marginal

costing and absorption costing provides different amount of profit. Key reasons behind this

difference are:

In both marginal costing and absorption costing, there is a difference in calculation of

closing stock. Which h arises the difference in cost of production and hence in the profit

as well.

Further, while preparing the income statement under marginal costing system, the fixed

cost are not taken into account (Fisher and Krumwiede, 2015). On the other hand, each

cost incurred by the business while manufacturing the products are taken into account in

the absorption costing method. Due to this method, total cost differs in both the methods.

It directly results in occurrence of difference in the profit of the company as well.

TASK 2

P4 Advantages and used disadvantage of different type of planning tool for budgetary control

Budgetary control is a process for the managers to set the financing performance goals

with the help of budgets and compare them with actual performance and make adjustments

where ever required. The planning tools are various types of budgets which assist the process of

budgetary control.

Cash budgets:

Advantages:

This budget assist in avoiding the debt with setting out the emergency situation which can

arise in the future.

It helps in identification of the potential deficits as it determine the ability of the business

to meet its immediate cash obligation.

Disadvantages

The actual availability of cash limits the spending power of the business.

This budget also causes distortions as the cash flows never match with the profits.

Variance Analysis:

Advantages:

Assist in finding the remedial actions with compression of actual and budgeted

performance.

This helps in fixation of responsibilities for an individual, department of the business.

Disadvantages:

Takes long time to examine the effect of variance and hence the correction actions get

delayed.

The level and reason of inefficiency in the performance is not determined by this budget.

Pricing strategy

Advantages:

This assist the organisation to set the prices of product as per the will of the consumers

which they are ready to pay.

This makes the good appealing to consumers while covering its cost.

Disadvantages:

This can make the price non appealing to consumers leading to their dissatisfaction.

The prices can be set such which do not provide the organisation the income which it

requires.

budgetary control.

Cash budgets:

Advantages:

This budget assist in avoiding the debt with setting out the emergency situation which can

arise in the future.

It helps in identification of the potential deficits as it determine the ability of the business

to meet its immediate cash obligation.

Disadvantages

The actual availability of cash limits the spending power of the business.

This budget also causes distortions as the cash flows never match with the profits.

Variance Analysis:

Advantages:

Assist in finding the remedial actions with compression of actual and budgeted

performance.

This helps in fixation of responsibilities for an individual, department of the business.

Disadvantages:

Takes long time to examine the effect of variance and hence the correction actions get

delayed.

The level and reason of inefficiency in the performance is not determined by this budget.

Pricing strategy

Advantages:

This assist the organisation to set the prices of product as per the will of the consumers

which they are ready to pay.

This makes the good appealing to consumers while covering its cost.

Disadvantages:

This can make the price non appealing to consumers leading to their dissatisfaction.

The prices can be set such which do not provide the organisation the income which it

requires.

Fixed budget: fixed budget is also known as static budget and is an essential tool to

measure the success of the business. The fixed budgets records all the financial a responsibility

when making the small and large expenditure for the business.

Advantages:

Allows business to measure both long tern as well as short term budgets. The fixed budget allocates a set amount of money towards essentials such as overhead

cost.

Disadvantages:

It operates at one level of activity only.

Do not do consider the significance difference in the activity level.

Flexible budget: is the one which adjust and make changes in the volume to the activity.

This is more sophisticated and useful as compared to the static budgets, it takes into

consideration the changes in the activity level.

Advantages:

Considers the actual changes in the volumes and activity level. The outcomes are always reals and positives as the actual volume is considered than the

planned one.

Disadvantages:

Does not take into consideration the actual expenses as when the sales changes cost of

production also changes but the expenses do not change leading t to vary the selling cost.

Incremental budgets: is prepared by using the figures from actual previous data and it is

a traditional method of making the budgets (Incremental budgeting, 2018). This includes slight

changes in the earlier budget of the organization.

Advantages:

Based on previous financial record so it is very simple to prepare. This require funding form data of multiple years to achieve a specific outcome, therefor

ensure the flow in the budgets.

Disadvantages:

Only minor changes from the preceding period so actual figures are not considered.

Managers tend to build too little revenue growth and excessive expenses into incremental

budgets.

measure the success of the business. The fixed budgets records all the financial a responsibility

when making the small and large expenditure for the business.

Advantages:

Allows business to measure both long tern as well as short term budgets. The fixed budget allocates a set amount of money towards essentials such as overhead

cost.

Disadvantages:

It operates at one level of activity only.

Do not do consider the significance difference in the activity level.

Flexible budget: is the one which adjust and make changes in the volume to the activity.

This is more sophisticated and useful as compared to the static budgets, it takes into

consideration the changes in the activity level.

Advantages:

Considers the actual changes in the volumes and activity level. The outcomes are always reals and positives as the actual volume is considered than the

planned one.

Disadvantages:

Does not take into consideration the actual expenses as when the sales changes cost of

production also changes but the expenses do not change leading t to vary the selling cost.

Incremental budgets: is prepared by using the figures from actual previous data and it is

a traditional method of making the budgets (Incremental budgeting, 2018). This includes slight

changes in the earlier budget of the organization.

Advantages:

Based on previous financial record so it is very simple to prepare. This require funding form data of multiple years to achieve a specific outcome, therefor

ensure the flow in the budgets.

Disadvantages:

Only minor changes from the preceding period so actual figures are not considered.

Managers tend to build too little revenue growth and excessive expenses into incremental

budgets.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Zero based budget: Zero base budgeting is recognized as method of budgeting in which all the

expenditures are justified for each accounting year. Such type of budgeting procedure starts with

Zero as base. It can also be considered to be as management accounting which includes

preparation of budget from scratch. Such type of budget emphasizes on preparation of new

economic proposal, where the revaluation of all tasks are being done. Zero based budgeting

assist manager in identifying the cots effective way of improving activities.

Advantages

it is flexible and emphasizes on operations. Makes the budges from the scratch.

Disadvantage

There is high chances of resource intensiveness.

It is not effective for short term planning.

Variance analysis: is a technique which determines the gap between actual and budgeted

outcomes of the organization (VARIANCE ANALYSIS, 2018). This difference found out is

significant and material to the performance of the firm.

Advantages:

it is very simple and act as a standard to attain the budgeted performance. This responsibly assist them managers in the performance analysis.

Disadvantages:

This does not consider the forces of market changes in the analysis.

The decisions of the departmental wise managers can lead to more consumption than the

actual and this raw information do not taken in account in the analysis.

P 5 Evaluation of management accounting system as to responding to various financial problems

Management accounting is the process of making management reports for the internal

members of the organization like mangers, stakeholders, employees who are directly related with

the organization (Otley, 2016). Management accounting is done to prepare the financial

statements which are used for strategic decision making to evaluate and analyse the information

and make strategic plans accordingly to achieve organizational goals and objectives.

Evolution of management accounting over decades:

expenditures are justified for each accounting year. Such type of budgeting procedure starts with

Zero as base. It can also be considered to be as management accounting which includes

preparation of budget from scratch. Such type of budget emphasizes on preparation of new

economic proposal, where the revaluation of all tasks are being done. Zero based budgeting

assist manager in identifying the cots effective way of improving activities.

Advantages

it is flexible and emphasizes on operations. Makes the budges from the scratch.

Disadvantage

There is high chances of resource intensiveness.

It is not effective for short term planning.

Variance analysis: is a technique which determines the gap between actual and budgeted

outcomes of the organization (VARIANCE ANALYSIS, 2018). This difference found out is

significant and material to the performance of the firm.

Advantages:

it is very simple and act as a standard to attain the budgeted performance. This responsibly assist them managers in the performance analysis.

Disadvantages:

This does not consider the forces of market changes in the analysis.

The decisions of the departmental wise managers can lead to more consumption than the

actual and this raw information do not taken in account in the analysis.

P 5 Evaluation of management accounting system as to responding to various financial problems

Management accounting is the process of making management reports for the internal

members of the organization like mangers, stakeholders, employees who are directly related with

the organization (Otley, 2016). Management accounting is done to prepare the financial

statements which are used for strategic decision making to evaluate and analyse the information

and make strategic plans accordingly to achieve organizational goals and objectives.

Evolution of management accounting over decades:

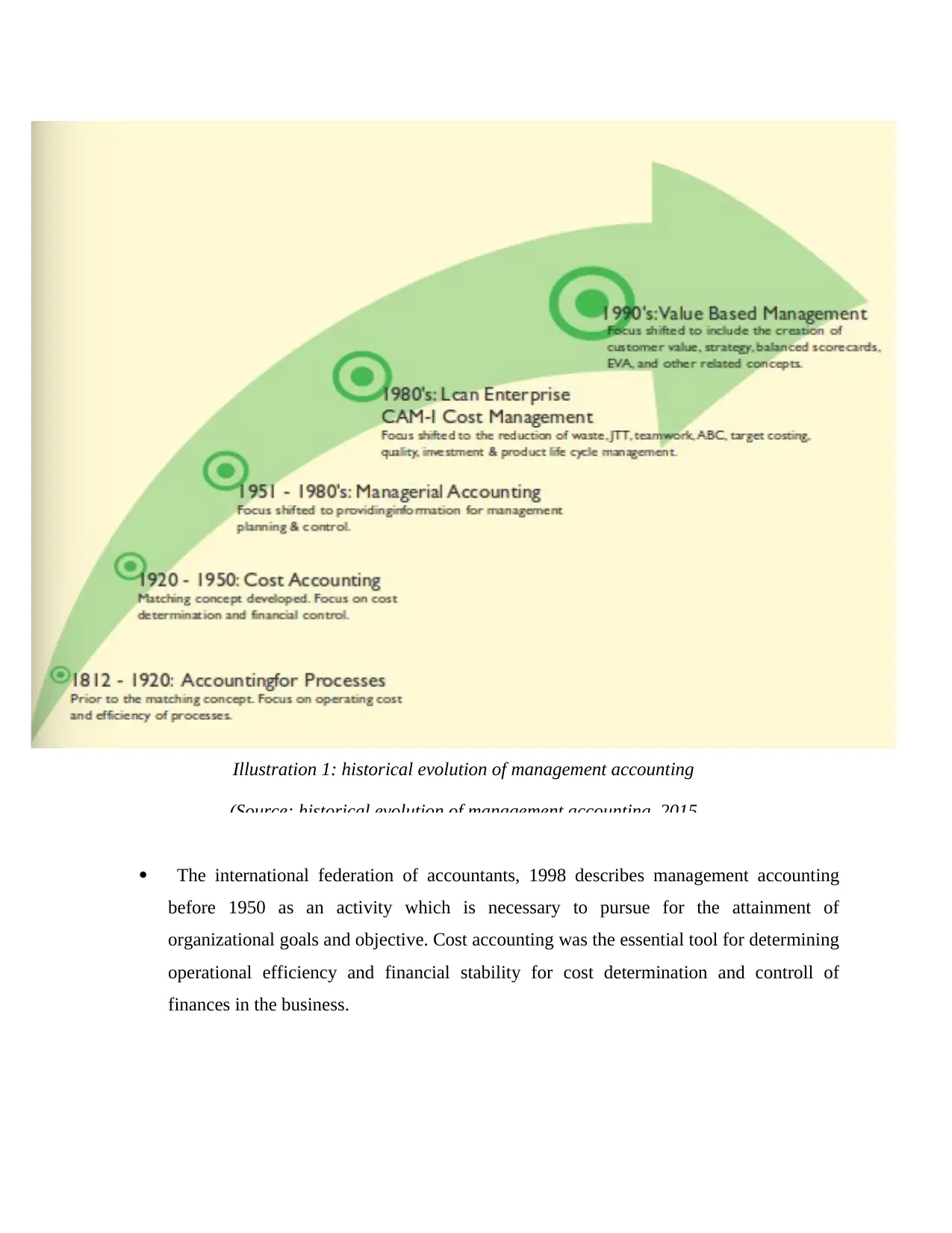

The international federation of accountants, 1998 describes management accounting

before 1950 as an activity which is necessary to pursue for the attainment of

organizational goals and objective. Cost accounting was the essential tool for determining

operational efficiency and financial stability for cost determination and controll of

finances in the business.

Illustration 1: historical evolution of management accounting

(Source: historical evolution of management accounting, 2015

before 1950 as an activity which is necessary to pursue for the attainment of

organizational goals and objective. Cost accounting was the essential tool for determining

operational efficiency and financial stability for cost determination and controll of

finances in the business.

Illustration 1: historical evolution of management accounting

(Source: historical evolution of management accounting, 2015

Cost accounting further evolved as managerial accounting in the year 1951 till 1980 to

provide information to management for planning and controlling and take necessary

decision accordingly(Historical evolution of management accounting, 2019).

It further evolved as cost management in the year 1980's to reduce wastage by applying

various cost techniques and product life cycle management.

The current scenario of management accounting which evolved in the year 1990 focus on

value based management where it aims at satisfying the need of customers by applying

various strategy.

Ratio analysis

Ratio analysis is a quantitative and fundamental analysis of data for gaining information

regarding company's profitability, liquidity and operational efficiency, productivity and financial

stability of the company.

Detection of financial problem through ratio analysis

◦ Liquidity ratio : This ratio helps in detecting weakness of the company and it also

measures the ability to pay off its liabilities. Lower the liquidity ratio higher the risk

to the company.

◦ Current ratio helps in detecting financial problems of the company in case liabilities

are more than asset.

Key performance indicator ( KPI's )

This is a type of performance measurement which helps in understanding and

evaluation the performance of the organization and it also analyses the performance of

department which are crucial for the development of the organization (Geiszler, Baker and

Lippitt, 2017). Key performance indicators are of numerous types like, cost of service delivery,

cost of managing various processes, return on investment, revenues from each employee,

efficiency in production, etc. all these types of KPIs helps the managers in detecting efficiency in

performing various activities of the business. With the help of which the managers can determine

their efficiency and in case of lack of efficiency, they can easily detect the problem that can be

arise due to these inefficiencies and determine their solutions as well.

provide information to management for planning and controlling and take necessary

decision accordingly(Historical evolution of management accounting, 2019).

It further evolved as cost management in the year 1980's to reduce wastage by applying

various cost techniques and product life cycle management.

The current scenario of management accounting which evolved in the year 1990 focus on

value based management where it aims at satisfying the need of customers by applying

various strategy.

Ratio analysis

Ratio analysis is a quantitative and fundamental analysis of data for gaining information

regarding company's profitability, liquidity and operational efficiency, productivity and financial

stability of the company.

Detection of financial problem through ratio analysis

◦ Liquidity ratio : This ratio helps in detecting weakness of the company and it also

measures the ability to pay off its liabilities. Lower the liquidity ratio higher the risk

to the company.

◦ Current ratio helps in detecting financial problems of the company in case liabilities

are more than asset.

Key performance indicator ( KPI's )

This is a type of performance measurement which helps in understanding and

evaluation the performance of the organization and it also analyses the performance of

department which are crucial for the development of the organization (Geiszler, Baker and

Lippitt, 2017). Key performance indicators are of numerous types like, cost of service delivery,

cost of managing various processes, return on investment, revenues from each employee,

efficiency in production, etc. all these types of KPIs helps the managers in detecting efficiency in

performing various activities of the business. With the help of which the managers can determine

their efficiency and in case of lack of efficiency, they can easily detect the problem that can be

arise due to these inefficiencies and determine their solutions as well.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Detection of financial problem through KPI's

For example, with the help of return on investment KPI system, the managers can easily

detect the areas from which the company is getting lower amount of return. Further, with the

help of it, they can easily determine the areas of lower returns, they can effectively determine

the solution for the future problems and help the company in becoming more effective in

resolving the financial problems as well. Further, Each department of the organization can

analyse sale and cost associated with tehm which help them detect and analyse the operations of

the particular department and measures regarding them. It detects revenue and profit and take

effective necessary measures to reduce cost. It also detects the expenses and cost of goods sold to

to detect the problems in case of any operational inefficiency.

Benchmarking

Benchmarking is a process of measuring performance of the company product, services,

cost, revenue sales and profit with the set benchmark. In case of any deviation in the production

process, sales process it helps in finding problem to the solution(What is Benchmarking, 2018).

Detection of financial problem through Benchmarking

In case there is deviation in production process from the set benchmark it helps in

detecting the actual cause of the deviation and it helps analyse the actual cause of the problem by

taking necessary measures regarding it.

An analysis of how management accounting as to help in responding to various financial

problems

There are numerous types of management accounting systems that helps the managerial

functioning. Further, there are various tools like cost control, inventory management, price

optimization, etc. that provides help to the managers in solving a range of financial problems of

the business in more effective way. Many companies like Volkswagen group, Toyota group,

Mercedes-Benz, etc. Uses these management accounting system tools for the purpose of

responding to numerous financial problems effectively as under:

Cost control system: cost control system refers to a practice of managers through which

they can detect use of cash resources within an organisation . They can also detect the

For example, with the help of return on investment KPI system, the managers can easily

detect the areas from which the company is getting lower amount of return. Further, with the

help of it, they can easily determine the areas of lower returns, they can effectively determine

the solution for the future problems and help the company in becoming more effective in

resolving the financial problems as well. Further, Each department of the organization can

analyse sale and cost associated with tehm which help them detect and analyse the operations of

the particular department and measures regarding them. It detects revenue and profit and take

effective necessary measures to reduce cost. It also detects the expenses and cost of goods sold to

to detect the problems in case of any operational inefficiency.

Benchmarking

Benchmarking is a process of measuring performance of the company product, services,

cost, revenue sales and profit with the set benchmark. In case of any deviation in the production

process, sales process it helps in finding problem to the solution(What is Benchmarking, 2018).

Detection of financial problem through Benchmarking

In case there is deviation in production process from the set benchmark it helps in

detecting the actual cause of the deviation and it helps analyse the actual cause of the problem by

taking necessary measures regarding it.

An analysis of how management accounting as to help in responding to various financial

problems

There are numerous types of management accounting systems that helps the managerial

functioning. Further, there are various tools like cost control, inventory management, price

optimization, etc. that provides help to the managers in solving a range of financial problems of

the business in more effective way. Many companies like Volkswagen group, Toyota group,

Mercedes-Benz, etc. Uses these management accounting system tools for the purpose of

responding to numerous financial problems effectively as under:

Cost control system: cost control system refers to a practice of managers through which

they can detect use of cash resources within an organisation . They can also detect the

areas of wastage of cash, through which they can effectively manage the financial system

of the company.

Volkswagen group being an automobile manufacturing company, adopts various cost

controlling techniques like budgetary control system, variance analysis, etc. adoption of these

techniques helps in detecting the areas of inefficiencies and determining the numerous problems

that can be arisen due to these inefficiencies as well. In this regard, they can develop the

strategies and plans as to enable the company in facing those problems effectively. In this regard,

using cost control system helps the managers of Volkswagen in effectively solving numerous

financial problems.

Inventory management system: Inventory management system is a system that

provides help to the managers in tracking the movement of stock within or outside the

business organisation. The Mercedes-Benz company being a manufacturing business,

needs to maintain a range of stock in the business for the purpose of developing

smoothness in working.

With the help of adopting the best inventory management system, managers of the company can

detect the areas or departments at which the inventories are being wasted within the organisation.

In this regard, managers enables the company in facing various financial problems like shortfall

of inventories, insufficient production, etc. by developing appropriate solution for these problems

and for eliminating wastage of stocks as well.

Price optimization system: Price optimization system refers to a system of management

accounting system that helps in determining the best price for selling the product at which

the company could earn the maximum profit and customer could get maximum

satisfaction as well.

Toyota group helps Uses the adopts price optimisation technique while determining the price of

the products of the company. It helps the company in deciding the best price of the product that

helps the business in attracting maximum amount of customers towards it.

Therefore, it can be analysed that all the management accounting system tools enables

managers in determining all tfinancial problems due to inefficiencies in numeorus business

activities. It helps the managers in making the company unable to face all the probloms in an

effective way.

of the company.

Volkswagen group being an automobile manufacturing company, adopts various cost

controlling techniques like budgetary control system, variance analysis, etc. adoption of these

techniques helps in detecting the areas of inefficiencies and determining the numerous problems

that can be arisen due to these inefficiencies as well. In this regard, they can develop the

strategies and plans as to enable the company in facing those problems effectively. In this regard,

using cost control system helps the managers of Volkswagen in effectively solving numerous

financial problems.

Inventory management system: Inventory management system is a system that

provides help to the managers in tracking the movement of stock within or outside the

business organisation. The Mercedes-Benz company being a manufacturing business,

needs to maintain a range of stock in the business for the purpose of developing

smoothness in working.

With the help of adopting the best inventory management system, managers of the company can

detect the areas or departments at which the inventories are being wasted within the organisation.

In this regard, managers enables the company in facing various financial problems like shortfall

of inventories, insufficient production, etc. by developing appropriate solution for these problems

and for eliminating wastage of stocks as well.

Price optimization system: Price optimization system refers to a system of management

accounting system that helps in determining the best price for selling the product at which

the company could earn the maximum profit and customer could get maximum

satisfaction as well.

Toyota group helps Uses the adopts price optimisation technique while determining the price of

the products of the company. It helps the company in deciding the best price of the product that

helps the business in attracting maximum amount of customers towards it.

Therefore, it can be analysed that all the management accounting system tools enables

managers in determining all tfinancial problems due to inefficiencies in numeorus business

activities. It helps the managers in making the company unable to face all the probloms in an

effective way.

Further, with help of these systems, managers can develop the best strategies for the

business through which the company can enhance its financial performance and attain a rapid

growth and success in the competitive market as well.

CONCLUSION

From the above study it can be concluded that management accounting system helps the

business in developing proper strategies for the business for enhancing its financial performance.

Both marginal and absorption costing helps the business in determining profit of the business.

Further, there are various management accounting system and planning tools that helps the

business in predetermining various financial problems and solving them in more effectively as

well.

business through which the company can enhance its financial performance and attain a rapid

growth and success in the competitive market as well.

CONCLUSION

From the above study it can be concluded that management accounting system helps the

business in developing proper strategies for the business for enhancing its financial performance.

Both marginal and absorption costing helps the business in determining profit of the business.

Further, there are various management accounting system and planning tools that helps the

business in predetermining various financial problems and solving them in more effectively as

well.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.