ElectroServe PLC: Evaluation of Proposed Investment (BFK450)

VerifiedAdded on 2023/01/16

|6

|1777

|77

Report

AI Summary

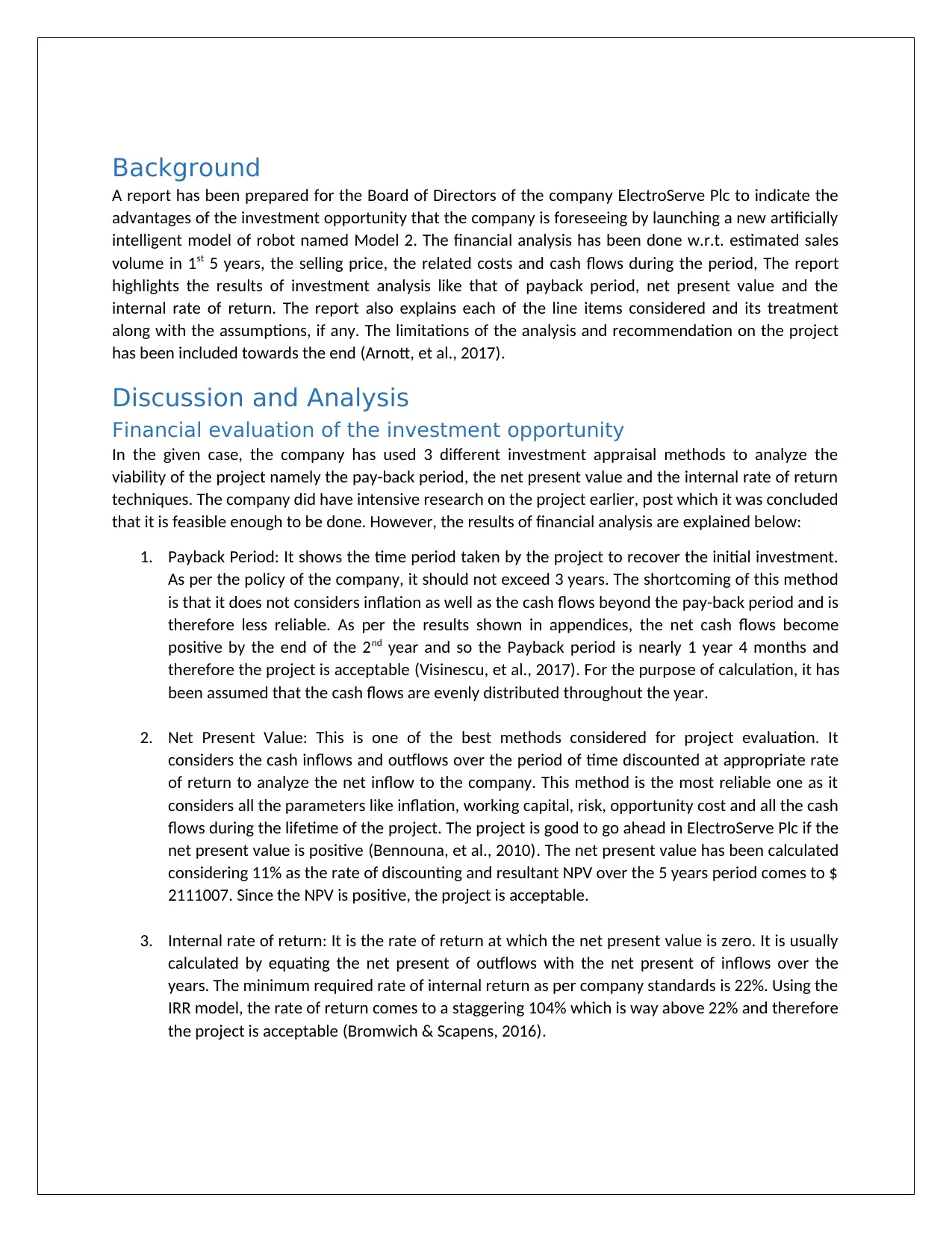

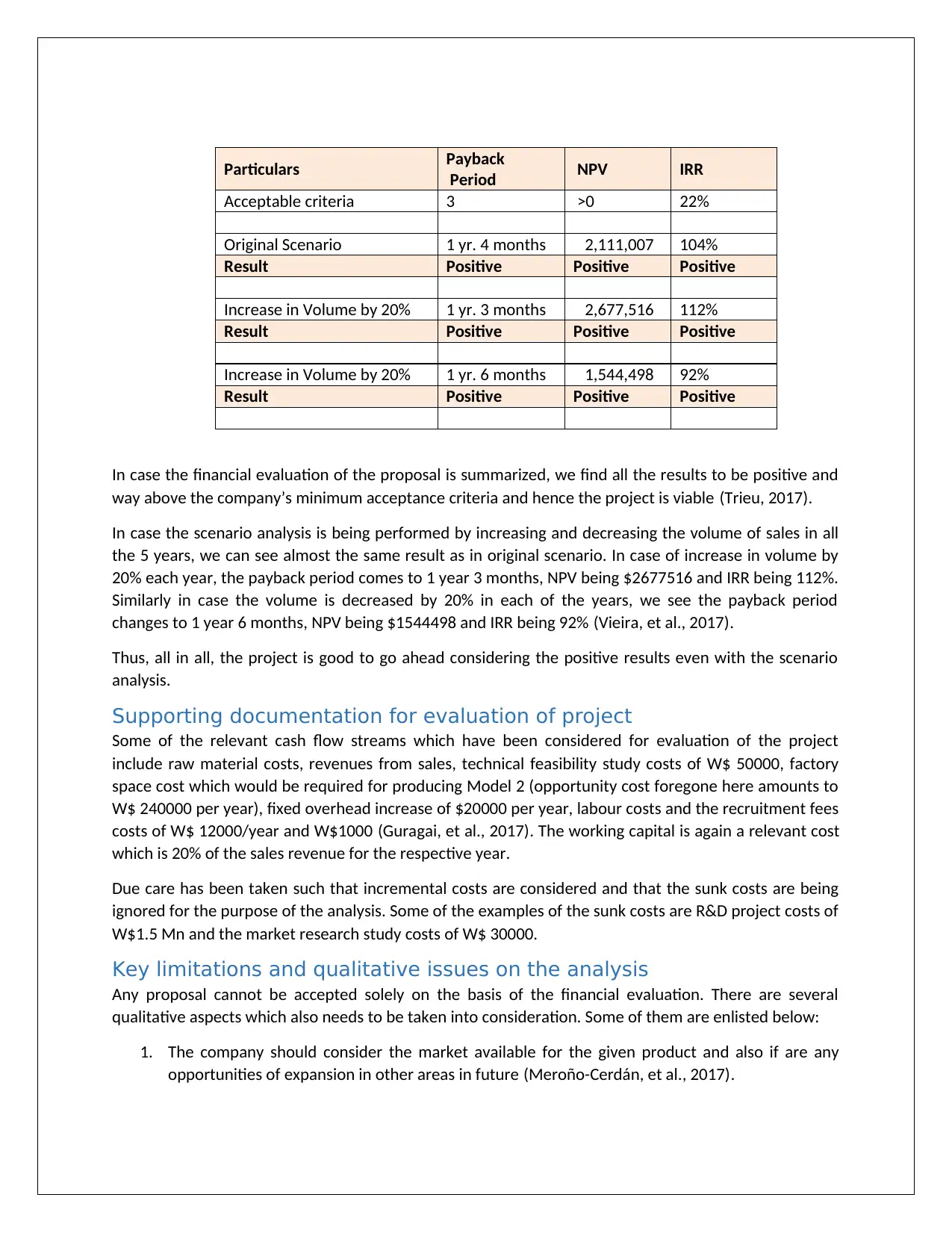

This report evaluates ElectroServe PLC's proposed investment in a new artificially intelligent robot model ('Model 2'). The analysis employs three investment appraisal methods: payback period, net present value (NPV), and internal rate of return (IRR). The report details the financial evaluation, including estimated sales, costs, and cash flows over five years. It calculates the payback period (approximately 1 year 4 months), NPV ($2,111,007), and IRR (104%), concluding the project is financially viable. Scenario analysis, considering 20% increases and decreases in sales volume, further supports this conclusion. The report also outlines supporting documentation such as costs of raw materials, revenue from sales, and factory space costs. Key limitations and qualitative aspects, such as market availability and alignment with company objectives, are discussed, and a recommendation to the Board of Directors is provided. The analysis is based on assumptions like cash transactions and a 11% discount rate.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.